News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

XenaLives

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

You have been posting B.S. since 2018...

STFU

rayovacAAA

Re: None

Wednesday, October 24, 2018 3:59:47 PM

Post#

3021 of 8888

NVDA getting destroyed. Where is the fireman?

rayovacAAA

Re: None

Wednesday, October 24, 2018 3:59:47 PM

Post#

3021 of 8888

NVDA getting destroyed. Where is the fireman?

oops...

(see replied to post, note date)

And restricting the flow of oxygen to your lungs torpedos your immune system.

Are you an AI experiment spreading lies and disinformation?

Your post is totally non sequitur to my post. My post had nothing to do with drones.

Here's an AI database query for you to consider:

Including results for israeli settlers semitic genetic

Search only for israeli settlers semitic genotype

AI overviews are experimental. Learn more

According to Wikipedia, the term "Semitic people" is an outdated term for a cultural, ethnic, or racial group associated with people from the Middle East. This includes Jews, Arabs, Akkadians, and Phoenicians. The term is now mostly used in linguistics to group "Semitic languages".

According to Wikipedia, Ashkenazi, North African, and Sephardi Jews share a significant amount of genetic ancestry. This ancestry comes from Middle Eastern and European populations.

According to Wikipedia, about 85% of the world's Jews are Ashkenazim, and the other 15% are Sephardim. About 10% of the world's Ashkenazim live in Israel, compared with about 80% of all Sephardim. The Sephardim make up about 55% of Israel's Jewish population, and the Ashkenazim about 45%.

According to Wikipedia, Kurdish and Sephardi Jews have indistinguishable paternal genetic heritage. About 32% of Ashkenazi Jews belong to the mitochondrial Haplogroup K. A 2006 study suggests that about 40% of the current Ashkenazi population is descended matrilineally from just four women.

Genetic markers cannot determine Jewish descent

Raphael Falk 1

Affiliations expand

PMID: 25653666 PMCID: PMC4301023 DOI: 10.3389/fgene.2014.00462

Abstract

Humans differentiate, classify, and discriminate: social interaction is a basic property of human Darwinian evolution. Presumably inherent differential physical as well as behavioral properties have always been criteria for identifying friend or foe. Yet, biological determinism is a relatively modern term, and scientific racism is, oddly enough, largely a consequence or a product of the Age of Enlightenment and the establishment of the notion of human equality. In recent decades ever-increasing efforts and ingenuity were invested in identifying Biblical Israelite genotypic common denominators by analysing an assortment of phenotypes, like facial patterns, blood types, diseases, DNA-sequences, and more. It becomes overwhelmingly clear that although Jews maintained detectable vertical genetic continuity along generations of socio-religious-cultural relationship, also intensive horizontal genetic relations were maintained both between Jewish communities and with the gentile surrounding. Thus, in spite of considerable consanguinity, there is no Jewish genotype to identify.

Keywords: Khazar origins of Ashkenazim; Y-chromosome inheritance of Cohanim; biology of the Jews; evolution at DNA-sequence level; genetics of race; horizontal vs. vertical inheritance.

PubMed Disclaimer

A society that waits more than five years to act on information like this is in failure mode...

The interests of individual persons and families is secondary to economic exploitation.

Have we got Alzheimer's disease all wrong?

7.30 /

By national medical reporter Sophie Scott and the Specialist Reporting Team's Rebecca Armitage

Posted Mon 24 Sep 2018 at 12:51pmMonday 24 Sep 2018 at 12:51pm, updated Mon 24 Sep 2018 at 11:29pm

......

If not plaque, then what?

Scientists who believe plaque could be a symptom rather than the cause of Alzheimer's disease are now putting all their efforts into preventing it developing in the brain in the first place.

For more information on the Anavex 2-73 trial, visit their website. To volunteer for the Australian Alzheimer's Research Foundation's testosterone trial, visit their website.

"We are now at a stage where we can diagnose Alzheimer's well before the symptoms appear — at least 20 years earlier," Professor Ralph Martins, an Alzheimer's researcher from Macquarie University, said.

"And this is the time when we think we can have the greatest impact because the brain is relatively preserved."

Professor Martins is conducting a trial to discover whether receiving shots of testosterone and taking fish oil could stave off the plaque.

"What hormones do is basically suppress the production of this amyloid," he said.

"In men, it's testosterone, and in women it's estrogen. Once we get older, our testosterone falls, that's when the amyloid starts rising."

Max McGown stands outside in a garden.

Max McGown became convinced he was likely to develop Alzheimer's disease.(ABC News: Rebecca Armitage)

When Max McGown heard about the study, he volunteered immediately.

The 67-year-old Sydney retiree watched Alzheimer's disease slowly rob his mother Gladys of her memories and her independence, and he became convinced he was next.

"I sometimes stumble for a word that I think I should know and scratch my head and wonder why I can't remember it until 3:00am the next morning," Mr McGown said.

"So, I guess it's just this feeling that I hope this is not one of the symptoms."

But after undergoing a PET scan, and waiting three agonising days for the results, Mr McGown was surprised to receive good news.

A society that waits more than five years to act on information like this is in failure mode...

The interests of individual persons and families is secondary to economic exploitation.

Have we got Alzheimer's disease all wrong?

7.30 /

By national medical reporter Sophie Scott and the Specialist Reporting Team's Rebecca Armitage

Posted Mon 24 Sep 2018 at 12:51pmMonday 24 Sep 2018 at 12:51pm, updated Mon 24 Sep 2018 at 11:29pm

......

If not plaque, then what?

Scientists who believe plaque could be a symptom rather than the cause of Alzheimer's disease are now putting all their efforts into preventing it developing in the brain in the first place.

For more information on the Anavex 2-73 trial, visit their website. To volunteer for the Australian Alzheimer's Research Foundation's testosterone trial, visit their website.

"We are now at a stage where we can diagnose Alzheimer's well before the symptoms appear — at least 20 years earlier," Professor Ralph Martins, an Alzheimer's researcher from Macquarie University, said.

"And this is the time when we think we can have the greatest impact because the brain is relatively preserved."

Professor Martins is conducting a trial to discover whether receiving shots of testosterone and taking fish oil could stave off the plaque.

"What hormones do is basically suppress the production of this amyloid," he said.

"In men, it's testosterone, and in women it's estrogen. Once we get older, our testosterone falls, that's when the amyloid starts rising."

Max McGown stands outside in a garden.

Max McGown became convinced he was likely to develop Alzheimer's disease.(ABC News: Rebecca Armitage)

When Max McGown heard about the study, he volunteered immediately.

The 67-year-old Sydney retiree watched Alzheimer's disease slowly rob his mother Gladys of her memories and her independence, and he became convinced he was next.

"I sometimes stumble for a word that I think I should know and scratch my head and wonder why I can't remember it until 3:00am the next morning," Mr McGown said.

"So, I guess it's just this feeling that I hope this is not one of the symptoms."

But after undergoing a PET scan, and waiting three agonising days for the results, Mr McGown was surprised to receive good news.

Genefic - a bogus franchise con...

About.

Experienced team of medical experts delivering advanced diagnostic and vaccination services designed to keep communities healthy and safe.

Genefic proudly provides gold-standard professional diagnostic services for easy on-site and mobile testing and vaccination. All services are performed on-site by our specially-trained medical staff including registered nurses and lab technicians. We offer easy testing and reporting, plus the ability to administer various vaccinations – with typically no out-of-pocket costs for patients. More testing and analysis capabilities are expected to be ready soon as we expand our staff and services. All testing measures and vaccines are approved or recommended by local health authorities as well as the Centers for Disease Control and Prevention (CDC).

I liked this part, and it also explains why uptake has been slow but sure....

If it works, you don't want to break it.

By leveraging the mature semiconductor ecosystem, silicon photonics has historically afforded unparalleled cost reduction and a deep level of integration, though due to fundamental physics limitations, silicon photonics are reaching the performance limit to reach the bandwidth and power requirements necessary in the modern era. This announcement demonstrates that a hybrid approach, leveraging the cost and integration benefits of silicon photonics along with the unparalleled bandwidth and low power advantages of Lightwave Logic’s proprietary EO polymers, lays a clear path for competitive performance and integration for current and future optical pluggable transceivers.

Lousy trading - Friday.

Last trade was over an hour before close.

04/12/24 14:46:47 0.224 0.22 0.23 2,500

04/12/24 14:46:37 0.224 0.00 0.00 625

04/12/24 14:46:22 0.224 0.00 0.00 625

04/12/24 14:46:07 0.224 0.00 0.00 625

04/12/24 14:34:06 0.22 0.22 0.23 50

04/12/24 14:34:06 0.22 0.22 0.23 10,900

04/12/24 12:32:11 0.224 0.22 0.23 50

04/12/24 12:32:11 0.224 0.22 0.23 1,000

04/12/24 11:41:13 0.23 0.22 0.23 2,500

04/12/24 11:32:34 0.22 0.22 0.23 7,000

04/12/24 11:32:13 0.223 0.22 0.23 3,000

04/12/24 10:40:00 0.234 0.22 0.234 20,500

04/12/24 10:39:53 0.227 0.22 0.234 500

04/12/24 10:39:52 0.227 0.00 0.00 125

04/12/24 10:39:37 0.227 0.00 0.00 125

04/12/24 10:39:22 0.227 0.00 0.00 125

04/12/24 10:39:07 0.227 0.00 0.00 125

04/12/24 10:34:20 0.225 0.22 0.225 15,500

04/12/24 10:34:12 0.225 0.22 0.225 16

04/12/24 10:34:12 0.225 0.22 0.225 30,100

04/12/24 10:34:07 0.225 0.22 0.225 72

04/12/24 10:34:07 0.225 0.22 0.225 1,400

04/12/24 10:34:06 0.2225 0.22 0.225 500

04/12/24 10:28:13 0.225 0.22 0.225 28

04/12/24 10:28:13 0.225 0.22 0.225 2,500

04/12/24 10:28:13 0.225 0.22 0.225 1,000

04/12/24 10:24:15 0.22 0.22 0.225 78

04/12/24 10:24:15 0.22 0.22 0.225 3,500

04/12/24 10:24:14 0.22 0.22 0.225 2,000

04/12/24 10:23:57 0.2225 0.22 0.225 500

04/12/24 10:04:48 0.225 0.22 0.225 20

04/12/24 10:04:48 0.225 0.22 0.225 200

04/12/24 09:57:34 0.2225 0.22 0.225 800

04/12/24 09:51:51 0.2197 0.211 0.2197 2,500

04/12/24 09:33:12 0.2171 0.211 0.2197 75

04/12/24 09:33:12 0.2171 0.211 0.2197 100

04/12/24 09:30:03 0.195 0.195 0.2197 100

Ownership of restricted shares allows BONAR and other insiders to retain control when the shell goes bust.

The chart only goes back to '95 but he was playing this game in the '80's.

So this is how the junk penny DFCO closed out the week.

Every lousy trade, no filtering.

04/12/24 14:46:47 0.224 0.22 0.23 2,500

04/12/24 14:46:37 0.224 0.00 0.00 625

04/12/24 14:46:22 0.224 0.00 0.00 625

04/12/24 14:46:07 0.224 0.00 0.00 625

04/12/24 14:34:06 0.22 0.22 0.23 50

04/12/24 14:34:06 0.22 0.22 0.23 10,900

04/12/24 12:32:11 0.224 0.22 0.23 50

04/12/24 12:32:11 0.224 0.22 0.23 1,000

04/12/24 11:41:13 0.23 0.22 0.23 2,500

04/12/24 11:32:34 0.22 0.22 0.23 7,000

04/12/24 11:32:13 0.223 0.22 0.23 3,000

04/12/24 10:40:00 0.234 0.22 0.234 20,500

04/12/24 10:39:53 0.227 0.22 0.234 500

04/12/24 10:39:52 0.227 0.00 0.00 125

04/12/24 10:39:37 0.227 0.00 0.00 125

04/12/24 10:39:22 0.227 0.00 0.00 125

04/12/24 10:39:07 0.227 0.00 0.00 125

04/12/24 10:34:20 0.225 0.22 0.225 15,500

04/12/24 10:34:12 0.225 0.22 0.225 16

04/12/24 10:34:12 0.225 0.22 0.225 30,100

04/12/24 10:34:07 0.225 0.22 0.225 72

04/12/24 10:34:07 0.225 0.22 0.225 1,400

04/12/24 10:34:06 0.2225 0.22 0.225 500

04/12/24 10:28:13 0.225 0.22 0.225 28

04/12/24 10:28:13 0.225 0.22 0.225 2,500

04/12/24 10:28:13 0.225 0.22 0.225 1,000

04/12/24 10:24:15 0.22 0.22 0.225 78

04/12/24 10:24:15 0.22 0.22 0.225 3,500

04/12/24 10:24:14 0.22 0.22 0.225 2,000

04/12/24 10:23:57 0.2225 0.22 0.225 500

04/12/24 10:04:48 0.225 0.22 0.225 20

04/12/24 10:04:48 0.225 0.22 0.225 200

04/12/24 09:57:34 0.2225 0.22 0.225 800

04/12/24 09:51:51 0.2197 0.211 0.2197 2,500

04/12/24 09:33:12 0.2171 0.211 0.2197 75

04/12/24 09:33:12 0.2171 0.211 0.2197 100

04/12/24 09:30:03 0.195 0.195 0.2197 100

04/11/24 15:40:59 0.2095 0.195 0.2095 1,000

04/11/24 15:40:52 0.2095 0.195 0.2095 1,000

04/11/24 15:38:10 0.195 0.195 0.2049 9,000

04/11/24 15:38:04 0.20 0.195 0.2049 2,200

04/11/24 15:05:16 0.20 0.195 0.2049 2,000

04/11/24 15:05:15 0.2025 0.20 0.2049 500

04/11/24 14:58:37 0.20 0.20 0.2049 92

04/11/24 14:58:37 0.20 0.196 0.2049 2,100

04/11/24 14:40:39 0.20 0.196 0.2049 1

04/11/24 13:51:33 0.20 0.1902 0.20 300

04/11/24 13:10:41 0.1976 0.1902 0.205 400

04/11/24 12:25:47 0.195 0.1902 0.198 400

04/11/24 11:57:14 0.1941 0.1902 0.198 400

04/11/24 11:48:12 0.198 0.1902 0.198 48

04/11/24 11:48:12 0.198 0.1902 0.2094 1,000

04/11/24 11:48:12 0.198 0.1902 0.2094 500

04/11/24 11:48:06 0.1902 0.1902 0.2094 13

04/11/24 11:48:06 0.1902 0.1902 0.2094 48,000

04/11/24 11:48:00 0.204 0.1902 0.2094 87

04/11/24 11:48:00 0.204 0.1902 0.2094 1,400

04/11/24 11:47:59 0.1998 0.1902 0.2094 500

04/11/24 11:40:05 0.1902 0.1902 0.2094 6,300

04/11/24 11:39:17 0.204 0.1902 0.2094 59

04/11/24 11:39:17 0.204 0.1902 0.2094 500

04/11/24 11:39:16 0.2067 0.204 0.2094 500

04/11/24 10:21:24 0.2036 0.1902 0.2094 73

04/11/24 10:21:24 0.2036 0.1902 0.2094 100

04/11/24 09:56:31 0.198 0.1902 0.21 37,000

04/11/24 09:56:22 0.20 0.20 0.21 2,500

04/11/24 09:56:22 0.20 0.20 0.21 5,000

04/11/24 09:56:22 0.2001 0.2001 0.21 2,500

04/11/24 09:56:15 0.2002 0.2001 0.21 2,500

04/11/24 09:56:13 0.201 0.201 0.21 2,500

04/11/24 09:55:51 0.2055 0.201 0.21 500

04/11/24 09:51:17 0.2046 0.201 0.21 2,500

04/11/24 09:46:47 0.21 0.201 0.21 2,000

04/11/24 09:46:46 0.201 0.201 0.21 2,000

04/11/24 09:45:28 0.21 0.201 0.21 100

04/11/24 09:45:23 0.2055 0.201 0.21 500

04/11/24 09:44:17 0.21 0.205 0.21 90

04/11/24 09:44:17 0.21 0.205 0.23 2,400

04/11/24 09:44:11 0.21 0.211 0.23 15,000

04/11/24 09:44:09 0.211 0.211 0.23 2,500

04/11/24 09:43:59 0.201 0.205 0.23 179,000

04/11/24 09:43:56 0.215 0.201 0.23 74

04/11/24 09:43:56 0.215 0.215 0.23 17,000

04/11/24 09:43:47 0.2151 0.2151 0.23 2,500

04/11/24 09:43:35 0.218 0.218 0.23 22,500

04/11/24 09:43:34 0.218 0.218 0.23 2,500

04/11/24 09:31:07 0.235 0.22 0.235 5,000

04/11/24 09:30:03 0.24 0.22 0.235 12,500

04/10/24 15:58:42 0.225 0.225 0.235 500

04/10/24 15:58:41 0.23 0.225 0.235 500

04/10/24 15:58:33 0.229 0.225 0.235 2,500

04/10/24 15:56:25 0.23 0.225 0.235 300

04/10/24 15:52:12 0.231 0.225 0.235 3,500

04/10/24 15:48:32 0.225 0.201 0.235 3,300

04/10/24 15:48:01 0.225 0.225 0.234 2,400

04/10/24 15:48:01 0.2295 0.225 0.234 500

04/10/24 15:44:17 0.2313 0.225 0.234 100

04/10/24 15:43:44 0.225 0.225 0.234 19,500

04/10/24 15:43:44 0.2295 0.225 0.234 500

04/10/24 15:43:37 0.225 0.00 0.00 5,000

04/10/24 15:43:22 0.2295 0.00 0.00 5,000

04/10/24 15:43:07 0.2295 0.00 0.00 5,000

04/10/24 15:07:16 0.23 0.225 0.23 3,000

04/10/24 14:22:24 0.2285 0.225 0.23 200

04/10/24 14:13:38 0.225 0.225 0.23 500

04/10/24 14:13:38 0.2275 0.225 0.23 500

04/10/24 14:08:57 0.2275 0.225 0.23 46

04/10/24 14:08:57 0.2275 0.225 0.23 200

04/10/24 13:48:05 0.23 0.225 0.23 1,000

04/10/24 13:41:25 0.234 0.225 0.23 5,000

04/10/24 13:41:23 0.23 0.225 0.23 10,000

04/10/24 13:26:23 0.225 0.225 0.23 500

04/10/24 13:25:21 0.225 0.215 0.23 2,000

04/10/24 13:25:20 0.225 0.215 0.23 84

04/10/24 13:25:20 0.225 0.215 0.225 4,000

04/10/24 13:25:20 0.2249 0.215 0.225 2,000

04/10/24 13:25:02 0.22 0.215 0.225 42

04/10/24 13:25:02 0.22 0.215 0.225 200

04/10/24 13:25:01 0.22 0.215 0.225 500

04/10/24 13:07:00 0.2214 0.216 0.225 2,000

04/10/24 12:56:20 0.2205 0.216 0.225 20

04/10/24 12:56:20 0.2205 0.216 0.225 20

04/10/24 12:45:32 0.2205 0.216 0.225 88

04/10/24 12:45:32 0.2205 0.216 0.225 8,900

04/10/24 12:44:53 0.2225 0.216 0.225 28

04/10/24 12:23:05 0.2225 0.215 0.23 3,900

04/10/24 12:22:46 0.2225 0.215 0.23 500

04/10/24 11:37:45 0.225 0.215 0.23 2,500

04/10/24 11:37:44 0.23 0.215 0.225 2,500

04/10/24 10:40:52 0.225 0.215 0.225 16

04/10/24 10:40:52 0.225 0.215 0.225 58

04/10/24 10:40:52 0.225 0.215 0.225 75

04/10/24 10:40:52 0.225 0.215 0.225 500

04/10/24 10:25:40 0.221 0.215 0.23 20

04/10/24 10:25:40 0.221 0.215 0.23 100

04/10/24 10:22:36 0.2263 0.215 0.23 8,000

04/10/24 10:12:00 0.2248 0.215 0.23 3,000

04/10/24 09:56:17 0.219 0.215 0.23 2,500

04/10/24 09:56:12 0.22 0.215 0.219 17,300

04/10/24 09:55:55 0.219 0.21 0.219 2,500

04/10/24 09:55:55 0.219 0.21 0.219 900

04/10/24 09:45:56 0.21 0.21 0.219 23,000

04/10/24 09:38:39 0.219 0.21 0.219 400

04/10/24 09:37:57 0.21 0.21 0.219 900

04/10/24 09:30:04 0.219 0.20 0.219 12,000

04/10/24 09:30:04 0.219 0.20 0.219 100

04/10/24 09:30:04 0.20 0.20 0.219 3,100

04/10/24 09:30:01 0.20 0.20 0.219 4,000

04/10/24 09:30:01 0.20 0.20 0.219 5,000

04/09/24 15:28:48 0.2114 0.20 0.219 1,500

04/09/24 15:28:37 0.2114 0.00 0.00 375

04/09/24 15:28:22 0.2114 0.00 0.00 375

04/09/24 15:28:07 0.2114 0.00 0.00 375

04/09/24 15:04:28 0.20 0.20 0.219 2,000

04/09/24 15:04:03 0.2114 0.20 0.219 3,000

04/09/24 14:58:41 0.219 0.20 0.219 1,000

04/09/24 13:53:55 0.219 0.20 0.219 2,500

04/09/24 13:48:26 0.21 0.21 0.219 4,000

04/09/24 13:47:48 0.21 0.21 0.219 3,900

04/09/24 13:21:39 0.21 0.21 0.219 100

04/09/24 13:16:45 0.219 0.21 0.219 2,500

04/09/24 13:15:08 0.2154 0.21 0.219 4,000

04/09/24 13:14:32 0.2188 0.21 0.219 2,500

04/09/24 13:14:20 0.2144 0.21 0.2188 2,000

04/09/24 13:14:14 0.2135 0.21 0.2188 3,000

04/09/24 13:13:52 0.2144 0.21 0.2188 2,000

04/09/24 13:13:32 0.2153 0.21 0.2188 3,000

04/09/24 13:10:25 0.21 0.1901 0.2188 12,000

04/09/24 13:08:45 0.21 0.21 0.2188 5,000

04/09/24 13:07:07 0.2122 0.2055 0.2188 300

04/09/24 12:51:41 0.2122 0.2055 0.2188 300

04/09/24 12:27:57 0.2095 0.2055 0.2188 2,500

04/09/24 12:27:38 0.2095 0.2055 0.2188 2,500

04/09/24 12:26:53 0.21 0.20 0.21 1,500

04/09/24 12:26:47 0.205 0.20 0.21 500

04/09/24 12:25:24 0.20 0.20 0.21 2,500

04/09/24 12:24:31 0.203 0.20 0.21 2,500

04/09/24 12:23:38 0.203 0.20 0.21 2,500

04/09/24 11:41:00 0.20 0.19 0.21 100

04/09/24 11:36:45 0.21 0.19 0.21 100

04/09/24 11:28:35 0.20 0.19 0.21 3,500

04/09/24 11:28:21 0.1903 0.19 0.21 1,000

04/09/24 11:28:20 0.1903 0.19 0.21 500

04/09/24 11:28:20 0.20 0.19 0.21 500

04/09/24 11:21:47 0.21 0.185 0.21 1,000

04/09/24 10:54:57 0.185 0.185 0.20 1,300

04/09/24 10:54:57 0.20 0.185 0.20 1,300

04/09/24 10:54:46 0.185 0.185 0.20 1,200

04/09/24 10:54:46 0.20 0.185 0.20 1,200

04/09/24 10:54:43 0.20 0.185 0.20 5,600

04/09/24 10:54:43 0.185 0.185 0.20 5,600

04/09/24 09:48:56 0.1903 0.185 0.20 1,500

04/09/24 09:46:15 0.20 0.185 0.20 2,000

04/09/24 09:44:05 0.20 0.185 0.20 300

04/09/24 09:35:19 0.1925 0.185 0.20 200

04/09/24 09:30:03 0.20 0.185 0.20 1,000

04/09/24 09:30:03 0.20 0.185 0.20 600

04/09/24 09:30:03 0.20 0.185 0.20 500

04/09/24 09:30:03 0.20 0.185 0.20 2,175

04/09/24 09:30:00 0.20 0.185 0.20 2,500

04/09/24 09:30:00 0.20 0.185 0.20 4,000

04/08/24 15:54:17 0.20 0.185 0.20 7,500

04/08/24 15:54:16 0.20 0.185 0.20 100

04/08/24 15:54:12 0.20 0.185 0.20 2,400

04/08/24 15:54:09 0.20 0.185 0.20 5,000

04/08/24 15:51:25 0.199 0.185 0.20 100

04/08/24 15:51:25 0.1955 0.185 0.20 200

04/08/24 15:41:41 0.1925 0.185 0.20 100

04/08/24 15:41:38 0.1925 0.185 0.20 500

04/08/24 15:29:30 0.1948 0.185 0.20 33

04/08/24 15:29:30 0.1948 0.185 0.20 65

04/08/24 15:29:28 0.1948 0.185 0.20 50

04/08/24 15:29:28 0.1948 0.185 0.20 200

04/08/24 15:23:39 0.199 0.185 0.20 100

04/08/24 15:23:39 0.1925 0.185 0.20 500

04/08/24 15:13:30 0.20 0.185 0.20 100

04/08/24 15:13:26 0.1925 0.185 0.20 500

04/08/24 15:12:52 0.20 0.20 0.21 10,000

04/08/24 15:12:44 0.20 0.20 0.215 54

04/08/24 15:12:44 0.20 0.20 0.215 4,200

04/08/24 15:12:38 0.2075 0.20 0.2149 500

04/08/24 14:53:06 0.2001 0.1812 0.219 500

04/08/24 14:51:56 0.20 0.20 0.22 2,500

04/08/24 14:51:50 0.205 0.20 0.22 5,900

04/08/24 14:51:50 0.20 0.20 0.22 5,900

04/08/24 14:51:44 0.206 0.20 0.22 3,000

04/08/24 14:49:01 0.215 0.20 0.215 2,500

04/08/24 14:48:56 0.211 0.20 0.211 2,500

04/08/24 14:48:37 0.22 0.20 0.22 12

04/08/24 14:48:37 0.22 0.20 0.22 1,000

04/08/24 14:48:37 0.22 0.20 0.22 700

04/08/24 14:48:34 0.22 0.20 0.22 2,500

04/08/24 14:48:28 0.22 0.20 0.22 5,000

04/08/24 14:48:27 0.2194 0.20 0.22 2,000

04/08/24 14:48:13 0.219 0.211 0.219 9,100

04/08/24 14:48:04 0.215 0.211 0.219 500

04/08/24 14:48:03 0.219 0.211 0.219 25,000

04/08/24 14:47:35 0.219 0.211 0.219 20,000

04/08/24 14:47:00 0.21 0.21 0.219 6,500

04/08/24 14:46:56 0.21 0.205 0.219 1,000

04/08/24 14:46:51 0.21 0.205 0.219 2,500

04/08/24 14:46:45 0.21 0.206 0.21 2,500

04/08/24 14:46:09 0.20 0.198 0.20 4,100

04/08/24 14:46:00 0.199 0.198 0.20 500

04/08/24 14:45:57 0.199 0.198 0.20 5,000

04/08/24 14:45:54 0.20 0.198 0.199 10,000

04/08/24 14:45:54 0.198 0.185 0.198 2,500

04/08/24 14:45:41 0.198 0.1802 0.198 10,000

04/08/24 14:45:25 0.198 0.1801 0.198 5,000

04/08/24 14:42:24 0.19 0.19 0.198 15,700

04/08/24 14:40:50 0.19 0.19 0.198 2,000

04/08/24 14:40:43 0.194 0.19 0.198 500

04/08/24 14:35:05 0.19 0.19 0.199 2,500

04/08/24 14:35:02 0.1945 0.1769 0.19 2,500

04/08/24 14:35:02 0.19 0.1769 0.19 5,000

04/08/24 14:35:00 0.184 0.1769 0.189 1,000

04/08/24 14:35:00 0.189 0.1769 0.189 5,000

04/08/24 14:34:47 0.189 0.1769 0.189 300

04/08/24 14:30:11 0.1835 0.178 0.189 300

04/08/24 14:30:08 0.1835 0.178 0.189 500

04/08/24 14:24:40 0.1825 0.176 0.1825 6,600

04/08/24 14:24:31 0.1793 0.176 0.1825 500

04/08/24 14:20:41 0.1825 0.176 0.1825 1,500

04/08/24 14:20:19 0.1793 0.176 0.1825 500

04/08/24 14:08:18 0.1806 0.176 0.1825 2,600

04/08/24 13:51:48 0.1825 0.1764 0.189 600

04/08/24 13:43:02 0.1827 0.1763 0.189 1,000

04/08/24 13:36:43 0.1829 0.1767 0.189 900

04/08/24 13:36:39 0.187 0.1767 0.189 100

04/08/24 13:29:40 0.189 0.1762 0.189 11,000

04/08/24 13:29:39 0.1887 0.1762 0.189 5,000

04/08/24 13:29:09 0.1885 0.1761 0.1887 2,800

04/08/24 13:29:09 0.1885 0.1761 0.1887 500

04/08/24 13:29:09 0.1844 0.1761 0.1887 500

04/08/24 13:27:17 0.1887 0.18 0.1887 3,300

04/08/24 13:27:11 0.1844 0.18 0.1887 500

04/08/24 13:25:34 0.1887 0.18 0.1887 2,100

04/08/24 13:25:21 0.1844 0.18 0.1887 500

04/08/24 13:14:39 0.1844 0.18 0.1887 200

04/08/24 13:14:19 0.18 0.176 0.1887 100

04/08/24 13:14:19 0.18 0.176 0.1887 5,100

04/08/24 13:14:04 0.178 0.176 0.18 500

04/08/24 13:12:45 0.178 0.176 0.18 200

04/08/24 13:12:29 0.1772 0.176 0.18 5,000

04/08/24 13:05:35 0.18 0.175 0.18 1,000

04/08/24 13:04:53 0.175 0.174 0.18 2,500

04/08/24 13:01:18 0.1758 0.174 0.18 10,000

04/08/24 12:57:21 0.174 0.1725 0.174 10,000

04/08/24 12:57:00 0.1735 0.1725 0.174 10,000

04/08/24 12:56:36 0.174 0.1725 0.174 10,000

04/08/24 12:48:56 0.1725 0.1651 0.174 9,000

04/08/24 12:48:56 0.1725 0.1651 0.174 1,000

04/08/24 12:47:22 0.1688 0.1651 0.1725 500

04/08/24 12:46:27 0.1688 0.1651 0.1725 400

04/08/24 12:46:14 0.1688 0.1651 0.1725 600

04/08/24 12:36:25 0.1699 0.1651 0.1725 1,500

04/08/24 12:29:10 0.17 0.1651 0.17 2,000

04/08/24 12:29:03 0.1676 0.1651 0.17 500

04/08/24 12:28:35 0.1685 0.1651 0.17 200

04/08/24 12:28:20 0.168 0.1651 0.17 4,000

04/08/24 12:14:25 0.1714 0.1651 0.1725 200

04/08/24 12:11:02 0.1691 0.1651 0.173 1,000

04/08/24 12:10:57 0.1691 0.1651 0.173 500

04/08/24 11:24:42 0.1706 0.1651 0.173 100

04/08/24 11:24:00 0.17 0.165 0.17 5,200

04/08/24 11:23:54 0.17 0.165 0.17 9,800

04/08/24 11:08:37 0.1704 0.165 0.174 4,000

04/08/24 11:05:02 0.175 0.165 0.175 2,600

04/08/24 11:05:02 0.172 0.165 0.175 3,000

04/08/24 11:02:51 0.175 0.164 0.175 200

04/08/24 11:02:51 0.1734 0.164 0.175 200

04/08/24 11:01:51 0.165 0.165 0.175 22,500

04/08/24 11:01:37 0.175 0.165 0.175 500

04/08/24 11:00:33 0.175 0.1651 0.179 200

04/08/24 11:00:33 0.1721 0.1651 0.179 200

04/08/24 11:00:23 0.1721 0.1651 0.179 200

04/08/24 11:00:17 0.1721 0.1651 0.179 300

04/08/24 10:53:04 0.175 0.1651 0.179 200

04/08/24 10:53:04 0.1721 0.1651 0.179 200

04/08/24 10:53:00 0.167 0.167 0.179 1,900

04/08/24 10:52:56 0.175 0.167 0.179 200

04/08/24 10:52:56 0.173 0.167 0.179 200

04/08/24 10:52:52 0.173 0.167 0.179 200

04/08/24 10:52:39 0.173 0.167 0.179 500

04/08/24 10:46:34 0.1781 0.167 0.18 1,000

04/08/24 10:46:17 0.1682 0.1682 0.18 17,500

04/08/24 10:46:14 0.1712 0.1682 0.18 7,500

04/08/24 10:44:06 0.1742 0.1683 0.18 2,700

04/08/24 10:44:00 0.1742 0.1683 0.18 500

04/08/24 10:37:37 0.18 0.1671 0.18 5,000

04/08/24 10:37:31 0.18 0.1671 0.18 100

04/08/24 10:37:31 0.18 0.1671 0.18 4,900

04/08/24 10:21:17 0.18 0.164 0.18 5,000

04/08/24 10:21:16 0.18 0.164 0.18 100

04/08/24 10:20:56 0.172 0.164 0.18 500

04/08/24 10:08:45 0.1776 0.164 0.18 200

04/08/24 10:03:15 0.1645 0.164 0.165 9,500

04/08/24 10:03:10 0.1645 0.164 0.165 500

04/08/24 10:02:22 0.164 0.164 0.165 5,500

04/08/24 10:02:17 0.165 0.164 0.165 1,000

04/08/24 10:02:07 0.165 0.00 0.00 1,625

04/08/24 09:59:56 0.164 0.164 0.165 1,900

04/08/24 09:59:34 0.1646 0.164 0.165 500

04/08/24 09:58:41 0.164 0.158 0.164 12,000

04/08/24 09:48:11 0.164 0.158 0.165 10,000

04/08/24 09:38:22 0.1622 0.158 0.165 200

04/08/24 09:30:09 0.16 0.158 0.165 1,000

04/05/24 15:47:36 0.1565 0.153 0.16 50

04/05/24 15:47:36 0.1565 0.153 0.16 100

04/05/24 15:47:20 0.153 0.153 0.16 29

04/05/24 15:47:20 0.153 0.153 0.16 100

04/05/24 14:56:54 0.16 0.153 0.16 82

04/05/24 14:56:54 0.16 0.153 0.16 1,100

04/05/24 14:29:20 0.1565 0.153 0.16 2,500

04/05/24 14:26:54 0.1579 0.153 0.16 2,500

04/05/24 13:34:33 0.1579 0.153 0.16 500

04/05/24 13:34:22 0.1565 0.153 0.16 500

04/05/24 13:34:11 0.1565 0.153 0.16 73

04/05/24 13:34:11 0.1565 0.153 0.16 2,100

04/05/24 13:22:33 0.1579 0.153 0.16 500

04/05/24 13:01:28 0.155 0.155 0.16 400

04/05/24 13:01:19 0.155 0.155 0.16 1,000

04/05/24 12:25:23 0.1575 0.155 0.16 2,000

04/05/24 12:25:17 0.1575 0.155 0.16 500

04/05/24 12:11:46 0.16 0.155 0.16 500

04/05/24 10:48:32 0.155 0.155 0.16 5,000

04/05/24 09:33:46 0.165 0.152 0.165 5,800

04/05/24 09:32:00 0.165 0.152 0.165 20

04/05/24 09:30:28 0.165 0.152 0.165 100

04/05/24 09:30:02 0.152 0.152 0.165 81,300

04/05/24 09:30:02 0.165 0.152 0.165 81,311

04/05/24 09:30:00 0.165 0.152 0.165 100

04/04/24 15:42:15 0.1665 0.1651 0.1697 10,000

04/04/24 14:39:18 0.1651 0.1651 0.1697 5,000

04/04/24 14:06:59 0.1685 0.1651 0.1685 2,500

04/04/24 14:06:59 0.1668 0.1651 0.1685 500

04/04/24 13:58:51 0.1651 0.1651 0.1685 6,700

04/04/24 13:58:48 0.1651 0.1651 0.1685 1,000

04/04/24 13:44:25 0.1681 0.1651 0.1697 10,000

04/04/24 13:39:37 0.1697 0.1651 0.1697 2,400

04/04/24 13:39:32 0.1674 0.1651 0.1697 500

04/04/24 13:01:46 0.1697 0.1651 0.1697 1,000

04/04/24 12:58:49 0.1651 0.1651 0.1697 1,500

04/04/24 12:58:29 0.1674 0.1651 0.1697 500

04/04/24 12:23:23 0.1651 0.1651 0.1697 3,500

04/04/24 11:55:52 0.1651 0.1651 0.1697 2,800

04/04/24 11:55:49 0.1651 0.1651 0.1697 1,000

04/04/24 11:52:51 0.1681 0.1651 0.1697 7,000

04/04/24 11:50:22 0.1674 0.165 0.1697 28,900

04/04/24 11:50:14 0.1674 0.165 0.1697 500

04/04/24 11:44:22 0.165 0.165 0.1697 2,000

04/04/24 11:44:21 0.1674 0.165 0.1697 500

04/04/24 11:41:06 0.165 0.165 0.1697 3,000

04/04/24 11:37:13 0.1651 0.165 0.1697 7,000

04/04/24 11:36:41 0.1697 0.165 0.1697 1,000

04/04/24 11:24:08 0.168 0.1585 0.1697 100

04/04/24 11:22:25 0.1585 0.1585 0.1697 10,000

04/04/24 10:48:53 0.1663 0.1585 0.1697 1,000

04/04/24 10:46:32 0.1697 0.1585 0.1697 2,000

04/04/24 10:46:24 0.1641 0.1585 0.1697 500

04/04/24 10:23:43 0.165 0.156 0.1697 12,900

04/04/24 10:23:41 0.165 0.156 0.165 8,700

04/04/24 10:23:37 0.164 0.156 0.164 8,400

04/04/24 10:22:51 0.164 0.156 0.164 6,600

04/04/24 10:22:44 0.164 0.156 0.164 8,400

04/04/24 10:05:51 0.1595 0.155 0.164 500

04/04/24 10:02:31 0.1598 0.1598 0.164 5,600

04/04/24 09:59:47 0.1598 0.155 0.1598 5,000

04/04/24 09:59:46 0.1598 0.155 0.1598 5,000

04/04/24 09:31:41 0.1549 0.152 0.1549 5,000

04/04/24 09:31:37 0.155 0.152 0.1549 24,000

04/04/24 09:31:25 0.1538 0.1538 0.1549 8,000

04/04/24 09:30:00 0.159 0.152 0.159 600

04/04/24 09:30:00 0.155 0.152 0.159 645

04/04/24 09:30:00 0.155 0.152 0.159 7,000

04/03/24 15:59:43 0.1549 0.1511 0.1549 50

04/03/24 15:59:43 0.1549 0.1511 0.1549 100

04/03/24 15:47:12 0.1511 0.1511 0.1549 71

04/03/24 15:47:12 0.1511 0.1511 0.1549 100

04/03/24 15:44:56 0.1517 0.1511 0.1549 1,000

04/03/24 14:51:45 0.1549 0.151 0.1549 50

04/03/24 14:51:45 0.1549 0.151 0.1549 100

04/03/24 14:49:41 0.1508 0.1503 0.1549 50,000

04/03/24 14:47:16 0.1549 0.1503 0.1549 1,000

04/03/24 14:46:44 0.1549 0.1503 0.1549 1,000

04/03/24 14:17:20 0.1503 0.1503 0.1549 15,600

04/03/24 14:17:13 0.1504 0.1503 0.1549 500

04/03/24 14:16:17 0.1505 0.1503 0.1505 7,800

04/03/24 14:15:53 0.1505 0.1503 0.1505 2,500

04/03/24 14:15:44 0.1505 0.1504 0.1505 2,000

04/03/24 14:15:39 0.1505 0.1504 0.1505 5,000

04/03/24 14:15:33 0.1505 0.1505 0.155 500

04/03/24 14:15:30 0.1505 0.1505 0.155 5,000

04/03/24 14:15:29 0.1507 0.1505 0.155 5,000

04/03/24 14:15:21 0.1505 0.1505 0.155 5,000

04/03/24 14:15:20 0.1507 0.1505 0.155 5,000

04/03/24 14:14:52 0.1507 0.1505 0.155 5,000

04/03/24 12:41:37 0.15 0.15 0.1597 33,000

04/03/24 12:41:31 0.151 0.151 0.1597 5,000

04/03/24 12:41:00 0.151 0.151 0.1597 5,000

04/03/24 12:40:22 0.151 0.151 0.157 8,000

04/03/24 12:39:20 0.157 0.151 0.157 99

04/03/24 12:39:20 0.157 0.151 0.157 69,600

04/03/24 12:37:28 0.151 0.151 0.157 86

04/03/24 12:37:28 0.151 0.151 0.157 13,300

04/03/24 12:22:22 0.157 0.151 0.157 3,000

04/03/24 12:22:16 0.154 0.151 0.157 500

04/03/24 12:22:14 0.154 0.151 0.157 7,000

04/03/24 12:22:08 0.156 0.151 0.157 500

04/03/24 10:38:43 0.151 0.151 0.157 40

04/03/24 10:38:38 0.151 0.151 0.1598 13,000

04/03/24 10:38:26 0.151 0.151 0.1598 5,000

04/03/24 10:30:19 0.155 0.155 0.1599 1,500

04/03/24 10:29:58 0.1575 0.155 0.1599 500

04/03/24 09:52:29 0.156 0.156 0.1599 5,000

04/03/24 09:52:21 0.155 0.156 0.1599 5,000

04/03/24 09:33:57 0.1599 0.156 0.1599 2,000

From the AI response..

AI overviews are experimental. Learn more

Altered filamin A (FLNA) is a scaffolding protein that is linked to Alzheimer's disease (AD) and amyloid and tau pathologies. A 2017 study found that altered FLNA is prevalent in AD brains and is induced by amyloid beta (Aß). The study also found that altered FLNA is required for two prominent pathogenic signaling pathways of Aß.

PubMed

Altered filamin A enables amyloid beta-induced tau hyperphosphorylation and neuroinflammation in Alzheimer's disease

A DNA change that alters the blueprint for making the FLNA protein can result in an abnormally short version of the protein. Researchers suspect that this altered protein may not be able to interact with other molecules normally. This inability to bind to other proteins can disrupt important processes involved in skeletal development and cell growth, leading to bone and skin abnormalities.

FLNA is highly expressed in the brain, and its protein interactions are regulated by mechanical forces, phosphorylation, cleavage, and other factors. An altered conformation of FLNA would likely alter certain protein interactions or induce aberrant ones.

Historic Short Interest:

You can go to this link to check short interest in a stock:

http://nasdaqtrader.com/Trader.aspx?id=ShortInterest

Publication schedule is here:

http://nasdaqtrader.com/Trader.aspx?id=ShortIntPubSch

NOTE: Short interest was bumped up from 12/15/22 to 12/30/22 to take the stock below $5.

In the summer of 2022 short interest was at 20 million for three reporting periods, then they were able to cover about two million. Short interest went back to the 19-20 million range for the EOY dump and has only been reduced slightly because the company raised additional funds.

SHORTS ARE BETWEEN A ROCK AND A HARD PLACE.

Imminent "DEALS" will be revealed when the parties involved are ready to announce their new products,

NOTHING HAPPENED, the DEALS have begun.

Comments can be discussed here:

https://investorshub.advfn.com/Xenas-Study-Hall-29911

Settlement Date/Short Interest/Percent Change/

Average Daily Share Volume/Days to Cover

03/28/2024 19,892,741 (0.10) 624,180 31.87

03/15/2024 19,912,038 (4.38) 657,767 30.27

02/29/2024 20,824,373 (0.76) 516,557 40.31

02/15/2024 20,982,959 (3.21) 568,780 36.89

01/31/2024 21,679,862 (0.54) 663,205 32.69

01/12/2024 21,798,205 (2.54) 683,858 31.88

12/29/2023 22,366,585 2.30 735,997 30.39

12/15/2023 21,863,663 (0.31) 1,035,021 21.12

11/30/2023 21,931,805 (0.71) 461,494 47.52

11/15/2023 22,088,725 (0.53) 504,513 43.78

10/31/2023 22,205,898 (2.42) 512,860 43.30

10/13/2023 22,757,363 2.16 618,592 36.7

10/13/2023 22,757,363 2.16 618,592 36.79

09/29/2023 22,276,786 1.31 635,227 35.07

09/15/2023 21,989,156 2.77 560,869 39.21

08/31/2023 21,397,092 1.87 498,218 42.9

08/31/2023 21,397,092 1.87 498,218 42.95

08/15/2023 21,004,221 (0.58) 496,542 42.30

07/31/2023 21,126,205 (4.72) 739,769 28.56

07/14/2023 22,173,921 0.03 651,044 34.06

06/30/2023 22,167,474 0.03 814,363 27.22

06/15/2023 22,160,433 1.19 1,045,219 21.20

05/31/2023 21,899,366 7.56 1,683,984 13.00

05/15/2023 20,361,079 (0.09) 569,849 35.73

04/28/2023 20,379,295 (0.13) 466,808 43.66

04/14/2023 20,405,568 0.40 480,636 42.46

03/31/2023 20,325,220 1.87 671,254 30.28

03/15/2023 19,951,615 (0.69) 594,548 33.56

02/28/2023 20,090,333 2.05 482,648 41.63

02/15/2023 19,686,886 1.20 566,324 34.76

01/31/2023 19,453,568 (2.05) 535,632 36.32

01/13/2023 19,861,250 3.71 792,682 25.06

12/30/2022 19,150,187 3.67 1,285,439 14.90

12/15/2022 18,472,956 2.54 599,737 30.80

11/30/2022 18,014,908 2.62 519,921 34.65

11/15/2022 17,555,582 (1.41) 602,853 29.12

10/31/2022 17,806,460 0.09 701,576 25.38

10/14/2022 17,789,950 (0.63) 651,652 27.30

09/30/2022 17,903,415 (0.75) 648,513 27.61

09/15/2022 18,038,444 3.00 677,288 26.63

08/31/2022 17,513,561 (2.28) 766,506 22.85

08/15/2022 17,922,814 (3.15) 650,757 27.54

07/29/2022 18,506,638 (5.50) 750,589 24.66

07/15/2022 19,584,292 (5.88) 1,043,751 18.76

06/30/2022 20,807,845 6.79 2,426,677 8.57

06/15/2022 19,485,684 10.05 1,865,235 10.45

05/31/2022 17,706,834 9.34 1,427,860 12.40

05/13/2022 16,194,010 8.82 1,715,225 9.40

04/29/2022 14,881,642 12.40 1,063,592 13.99

04/14/2022 13,239,579 3.50 678,095 19.52

03/31/2022 12,791,395 10.45 875,640 14.61

03/15/2022 11,580,686 5.05 890,355 13.01

02/28/2022 11,023,861 4.63 872,453 12.64

02/15/2022 10,536,146 28.11 977,195 10.78

01/31/2022 8,224,272 67.06 1,996,611 4.12

01/14/2022 4,922,847 9.97 1,113,918 4.42

12/31/2021 4,476,575 102.34 1,842,236 2.43

12/15/2021 2,212,448 28.67 1,649,231 1.34

11/30/2021 1,719,480 (5.48) 944,571 1.82

11/15/2021 1,819,143 (5.38) 715,036 2.54

10/29/2021 1,922,613 (9.60) 403,339 4.77

10/15/2021 2,126,831 38.81 477,119 4.40

09/30/2021 1,532,236 (16.60) 846,969 1.81

09/15/2021 1,837,252 367,816 5.00

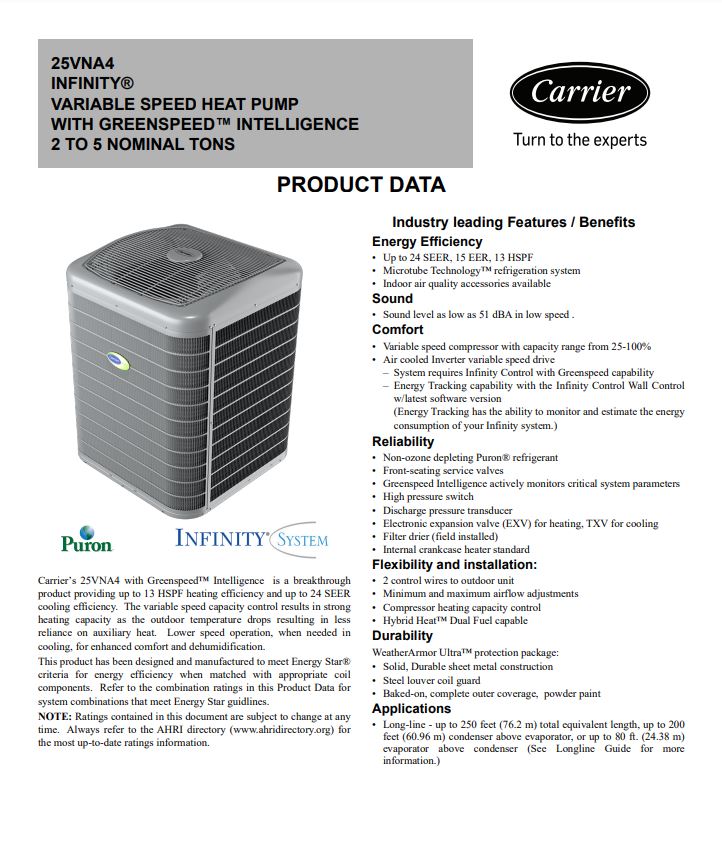

The heat pump has no unique IP - not even a spec sheet.

This is not a residential heat pump...

This is the only model DFCO has presented to the public, and the image appears to be photoshopped on this page, so stuckholders don't even have proof that it exists.

This is what a residential heat pump looks like:

This is what a spec sheet looks like:

Mr, Bonar knows exactly how I feel about his attempts to intimidate me.

We don't agree about anything, I clearly said it had nothing to do with personal issues.

What I just stated:

It's a moral vendetta - nothing personal about it, except for the fact that he chose to go after me personally for telling the truth.

Up 7% on 3.821 shares traded....

Just the BONAR BUDDIES playing footsie here.

No patents, no unique IP and a recycled business plan.

This is a junk stock being wash traded up by BONAR & his BUDDIES...

IT IS STILL A JUNK PENNY WITH NO PATENTS AND NO UNIQUE TECH

That is the only reason it's green while the rest of the market is red. It has nothing to do with the fake IP for "utilty tokens" which can't be verified. He has no heat pump IP, he has not even pretended to file.

04/12/24 10:23:57 0.2225 0.22 0.225 500

04/12/24 10:04:48 0.225 0.22 0.225 20

04/12/24 10:04:48 0.225 0.22 0.225 200

04/12/24 09:57:34 0.2225 0.22 0.225 800

04/12/24 09:51:51 0.2197 0.211 0.2197 2,500

04/12/24 09:33:12 0.2171 0.211 0.2197 75

04/12/24 09:33:12 0.2171 0.211 0.2197 100

04/12/24 09:30:03 0.195 0.195 0.2197 100

04/11/24 15:40:59 0.2095 0.195 0.2095 1,000

04/11/24 15:40:52 0.2095 0.195 0.2095 1,000

04/11/24 15:38:10 0.195 0.195 0.2049 9,000

04/11/24 15:38:04 0.20 0.195 0.2049 2,200

04/11/24 15:05:16 0.20 0.195 0.2049 2,000

04/11/24 15:05:15 0.2025 0.20 0.2049 500

04/11/24 14:58:37 0.20 0.20 0.2049 92

04/11/24 14:58:37 0.20 0.196 0.2049 2,100

04/11/24 14:40:39 0.20 0.196 0.2049 1

04/11/24 13:51:33 0.20 0.1902 0.20 300

04/11/24 13:10:41 0.1976 0.1902 0.205 400

04/11/24 12:25:47 0.195 0.1902 0.198 400

04/11/24 11:57:14 0.1941 0.1902 0.198 400

04/11/24 11:48:12 0.198 0.1902 0.198 48

04/11/24 11:48:12 0.198 0.1902 0.2094 1,000

04/11/24 11:48:12 0.198 0.1902 0.2094 500

04/11/24 11:48:06 0.1902 0.1902 0.2094 13

04/11/24 11:48:06 0.1902 0.1902 0.2094 48,000

04/11/24 11:48:00 0.204 0.1902 0.2094 87

04/11/24 11:48:00 0.204 0.1902 0.2094 1,400

04/11/24 11:47:59 0.1998 0.1902 0.2094 500

04/11/24 11:40:05 0.1902 0.1902 0.2094 6,300

04/11/24 11:39:17 0.204 0.1902 0.2094 59

04/11/24 11:39:17 0.204 0.1902 0.2094 500

04/11/24 11:39:16 0.2067 0.204 0.2094 500

04/11/24 10:21:24 0.2036 0.1902 0.2094 73

04/11/24 10:21:24 0.2036 0.1902 0.2094 100

04/11/24 09:56:31 0.198 0.1902 0.21 37,000

04/11/24 09:56:22 0.20 0.20 0.21 2,500

04/11/24 09:56:22 0.20 0.20 0.21 5,000

04/11/24 09:56:22 0.2001 0.2001 0.21 2,500

04/11/24 09:56:15 0.2002 0.2001 0.21 2,500

04/11/24 09:56:13 0.201 0.201 0.21 2,500

04/11/24 09:55:51 0.2055 0.201 0.21 500

04/11/24 09:51:17 0.2046 0.201 0.21 2,500

04/11/24 09:46:47 0.21 0.201 0.21 2,000

04/11/24 09:46:46 0.201 0.201 0.21 2,000

04/11/24 09:45:28 0.21 0.201 0.21 100

04/11/24 09:45:23 0.2055 0.201 0.21 500

04/11/24 09:44:17 0.21 0.205 0.21 90

04/11/24 09:44:17 0.21 0.205 0.23 2,400

04/11/24 09:44:11 0.21 0.211 0.23 15,000

04/11/24 09:44:09 0.211 0.211 0.23 2,500

04/11/24 09:43:59 0.201 0.205 0.23 179,000

04/11/24 09:43:56 0.215 0.201 0.23 74

04/11/24 09:43:56 0.215 0.215 0.23 17,000

04/11/24 09:43:47 0.2151 0.2151 0.23 2,500

04/11/24 09:43:35 0.218 0.218 0.23 22,500

04/11/24 09:43:34 0.218 0.218 0.23 2,500

04/11/24 09:31:07 0.235 0.22 0.235 5,000

04/11/24 09:30:03 0.24 0.22 0.235 12,500

04/10/24 15:58:42 0.225 0.225 0.235 500

04/10/24 15:58:41 0.23 0.225 0.235 500

04/10/24 15:58:33 0.229 0.225 0.235 2,500

04/10/24 15:56:25 0.23 0.225 0.235 300

04/10/24 15:52:12 0.231 0.225 0.235 3,500

04/10/24 15:48:32 0.225 0.201 0.235 3,300

04/10/24 15:48:01 0.225 0.225 0.234 2,400

04/10/24 15:48:01 0.2295 0.225 0.234 500

04/10/24 15:44:17 0.2313 0.225 0.234 100

04/10/24 15:43:44 0.225 0.225 0.234 19,500

04/10/24 15:43:44 0.2295 0.225 0.234 500

04/10/24 15:43:37 0.225 0.00 0.00 5,000

04/10/24 15:43:22 0.2295 0.00 0.00 5,000

04/10/24 15:43:07 0.2295 0.00 0.00 5,000

04/10/24 15:07:16 0.23 0.225 0.23 3,000

04/10/24 14:22:24 0.2285 0.225 0.23 200

04/10/24 14:13:38 0.225 0.225 0.23 500

04/10/24 14:13:38 0.2275 0.225 0.23 500

04/10/24 14:08:57 0.2275 0.225 0.23 46

04/10/24 14:08:57 0.2275 0.225 0.23 200

04/10/24 13:48:05 0.23 0.225 0.23 1,000

04/10/24 13:41:25 0.234 0.225 0.23 5,000

04/10/24 13:41:23 0.23 0.225 0.23 10,000

04/10/24 13:26:23 0.225 0.225 0.23 500

04/10/24 13:25:21 0.225 0.215 0.23 2,000

04/10/24 13:25:20 0.225 0.215 0.23 84

04/10/24 13:25:20 0.225 0.215 0.225 4,000

04/10/24 13:25:20 0.2249 0.215 0.225 2,000

04/10/24 13:25:02 0.22 0.215 0.225 42

04/10/24 13:25:02 0.22 0.215 0.225 200

04/10/24 13:25:01 0.22 0.215 0.225 500

04/10/24 13:07:00 0.2214 0.216 0.225 2,000

04/10/24 12:56:20 0.2205 0.216 0.225 20

04/10/24 12:56:20 0.2205 0.216 0.225 20

04/10/24 12:45:32 0.2205 0.216 0.225 88

04/10/24 12:45:32 0.2205 0.216 0.225 8,900

04/10/24 12:44:53 0.2225 0.216 0.225 28

04/10/24 12:23:05 0.2225 0.215 0.23 3,900

04/10/24 12:22:46 0.2225 0.215 0.23 500

04/10/24 11:37:45 0.225 0.215 0.23 2,500

04/10/24 11:37:44 0.23 0.215 0.225 2,500

04/10/24 10:40:52 0.225 0.215 0.225 16

04/10/24 10:40:52 0.225 0.215 0.225 58

04/10/24 10:40:52 0.225 0.215 0.225 75

04/10/24 10:40:52 0.225 0.215 0.225 500

04/10/24 10:25:40 0.221 0.215 0.23 20

04/10/24 10:25:40 0.221 0.215 0.23 100

04/10/24 10:22:36 0.2263 0.215 0.23 8,000

04/10/24 10:12:00 0.2248 0.215 0.23 3,000

04/10/24 09:56:17 0.219 0.215 0.23 2,500

04/10/24 09:56:12 0.22 0.215 0.219 17,300

04/10/24 09:55:55 0.219 0.21 0.219 2,500

04/10/24 09:55:55 0.219 0.21 0.219 900

04/10/24 09:45:56 0.21 0.21 0.219 23,000

04/10/24 09:38:39 0.219 0.21 0.219 400

04/10/24 09:37:57 0.21 0.21 0.219 900

04/10/24 09:30:04 0.219 0.20 0.219 12,000

04/10/24 09:30:04 0.219 0.20 0.219 100

04/10/24 09:30:04 0.20 0.20 0.219 3,100

04/10/24 09:30:01 0.20 0.20 0.219 4,000

04/10/24 09:30:01 0.20 0.20 0.219 5,000

04/09/24 15:28:48 0.2114 0.20 0.219 1,500

04/09/24 15:28:37 0.2114 0.00 0.00 375

04/09/24 15:28:22 0.2114 0.00 0.00 375

04/09/24 15:28:07 0.2114 0.00 0.00 375

04/09/24 15:04:28 0.20 0.20 0.219 2,000

04/09/24 15:04:03 0.2114 0.20 0.219 3,000

04/09/24 14:58:41 0.219 0.20 0.219 1,000

04/09/24 13:53:55 0.219 0.20 0.219 2,500

04/09/24 13:48:26 0.21 0.21 0.219 4,000

04/09/24 13:47:48 0.21 0.21 0.219 3,900

04/09/24 13:21:39 0.21 0.21 0.219 100

04/09/24 13:16:45 0.219 0.21 0.219 2,500

04/09/24 13:15:08 0.2154 0.21 0.219 4,000

04/09/24 13:14:32 0.2188 0.21 0.219 2,500

04/09/24 13:14:20 0.2144 0.21 0.2188 2,000

04/09/24 13:14:14 0.2135 0.21 0.2188 3,000

04/09/24 13:13:52 0.2144 0.21 0.2188 2,000

04/09/24 13:13:32 0.2153 0.21 0.2188 3,000

04/09/24 13:10:25 0.21 0.1901 0.2188 12,000

04/09/24 13:08:45 0.21 0.21 0.2188 5,000

04/09/24 13:07:07 0.2122 0.2055 0.2188 300

04/09/24 12:51:41 0.2122 0.2055 0.2188 300

04/09/24 12:27:57 0.2095 0.2055 0.2188 2,500

04/09/24 12:27:38 0.2095 0.2055 0.2188 2,500

04/09/24 12:26:53 0.21 0.20 0.21 1,500

04/09/24 12:26:47 0.205 0.20 0.21 500

04/09/24 12:25:24 0.20 0.20 0.21 2,500

04/09/24 12:24:31 0.203 0.20 0.21 2,500

04/09/24 12:23:38 0.203 0.20 0.21 2,500

04/09/24 11:41:00 0.20 0.19 0.21 100

04/09/24 11:36:45 0.21 0.19 0.21 100

04/09/24 11:28:35 0.20 0.19 0.21 3,500

04/09/24 11:28:21 0.1903 0.19 0.21 1,000

04/09/24 11:28:20 0.1903 0.19 0.21 500

04/09/24 11:28:20 0.20 0.19 0.21 500

04/09/24 11:21:47 0.21 0.185 0.21 1,000

04/09/24 10:54:57 0.185 0.185 0.20 1,300

04/09/24 10:54:57 0.20 0.185 0.20 1,300

04/09/24 10:54:46 0.185 0.185 0.20 1,200

04/09/24 10:54:46 0.20 0.185 0.20 1,200

04/09/24 10:54:43 0.20 0.185 0.20 5,600

04/09/24 10:54:43 0.185 0.185 0.20 5,600

04/09/24 09:48:56 0.1903 0.185 0.20 1,500

04/09/24 09:46:15 0.20 0.185 0.20 2,000

04/09/24 09:44:05 0.20 0.185 0.20 300

04/09/24 09:35:19 0.1925 0.185 0.20 200

04/09/24 09:30:03 0.20 0.185 0.20 1,000

04/09/24 09:30:03 0.20 0.185 0.20 600

04/09/24 09:30:03 0.20 0.185 0.20 500

04/09/24 09:30:03 0.20 0.185 0.20 2,175

04/09/24 09:30:00 0.20 0.185 0.20 2,500

04/09/24 09:30:00 0.20 0.185 0.20 4,000

04/08/24 15:54:17 0.20 0.185 0.20 7,500

04/08/24 15:54:16 0.20 0.185 0.20 100

04/08/24 15:54:12 0.20 0.185 0.20 2,400

04/08/24 15:54:09 0.20 0.185 0.20 5,000

04/08/24 15:51:25 0.199 0.185 0.20 100

04/08/24 15:51:25 0.1955 0.185 0.20 200

04/08/24 15:41:41 0.1925 0.185 0.20 100

04/08/24 15:41:38 0.1925 0.185 0.20 500

04/08/24 15:29:30 0.1948 0.185 0.20 33

04/08/24 15:29:30 0.1948 0.185 0.20 65

04/08/24 15:29:28 0.1948 0.185 0.20 50

04/08/24 15:29:28 0.1948 0.185 0.20 200

04/08/24 15:23:39 0.199 0.185 0.20 100

04/08/24 15:23:39 0.1925 0.185 0.20 500

04/08/24 15:13:30 0.20 0.185 0.20 100

04/08/24 15:13:26 0.1925 0.185 0.20 500

04/08/24 15:12:52 0.20 0.20 0.21 10,000

04/08/24 15:12:44 0.20 0.20 0.215 54

04/08/24 15:12:44 0.20 0.20 0.215 4,200

04/08/24 15:12:38 0.2075 0.20 0.2149 500

04/08/24 14:53:06 0.2001 0.1812 0.219 500

04/08/24 14:51:56 0.20 0.20 0.22 2,500

04/08/24 14:51:50 0.205 0.20 0.22 5,900

04/08/24 14:51:50 0.20 0.20 0.22 5,900

04/08/24 14:51:44 0.206 0.20 0.22 3,000

04/08/24 14:49:01 0.215 0.20 0.215 2,500

04/08/24 14:48:56 0.211 0.20 0.211 2,500

04/08/24 14:48:37 0.22 0.20 0.22 12

04/08/24 14:48:37 0.22 0.20 0.22 1,000

04/08/24 14:48:37 0.22 0.20 0.22 700

04/08/24 14:48:34 0.22 0.20 0.22 2,500

04/08/24 14:48:28 0.22 0.20 0.22 5,000

04/08/24 14:48:27 0.2194 0.20 0.22 2,000

04/08/24 14:48:13 0.219 0.211 0.219 9,100

04/08/24 14:48:04 0.215 0.211 0.219 500

04/08/24 14:48:03 0.219 0.211 0.219 25,000

04/08/24 14:47:35 0.219 0.211 0.219 20,000

04/08/24 14:47:00 0.21 0.21 0.219 6,500

04/08/24 14:46:56 0.21 0.205 0.219 1,000

04/08/24 14:46:51 0.21 0.205 0.219 2,500

04/08/24 14:46:45 0.21 0.206 0.21 2,500

04/08/24 14:46:09 0.20 0.198 0.20 4,100

04/08/24 14:46:00 0.199 0.198 0.20 500

04/08/24 14:45:57 0.199 0.198 0.20 5,000

04/08/24 14:45:54 0.20 0.198 0.199 10,000

04/08/24 14:45:54 0.198 0.185 0.198 2,500

04/08/24 14:45:41 0.198 0.1802 0.198 10,000

04/08/24 14:45:25 0.198 0.1801 0.198 5,000

04/08/24 14:42:24 0.19 0.19 0.198 15,700

04/08/24 14:40:50 0.19 0.19 0.198 2,000

04/08/24 14:40:43 0.194 0.19 0.198 500

04/08/24 14:35:05 0.19 0.19 0.199 2,500

04/08/24 14:35:02 0.1945 0.1769 0.19 2,500

04/08/24 14:35:02 0.19 0.1769 0.19 5,000

04/08/24 14:35:00 0.184 0.1769 0.189 1,000

04/08/24 14:35:00 0.189 0.1769 0.189 5,000

04/08/24 14:34:47 0.189 0.1769 0.189 300

04/08/24 14:30:11 0.1835 0.178 0.189 300

04/08/24 14:30:08 0.1835 0.178 0.189 500

04/08/24 14:24:40 0.1825 0.176 0.1825 6,600

04/08/24 14:24:31 0.1793 0.176 0.1825 500

04/08/24 14:20:41 0.1825 0.176 0.1825 1,500

04/08/24 14:20:19 0.1793 0.176 0.1825 500

04/08/24 14:08:18 0.1806 0.176 0.1825 2,600

04/08/24 13:51:48 0.1825 0.1764 0.189 600

04/08/24 13:43:02 0.1827 0.1763 0.189 1,000

04/08/24 13:36:43 0.1829 0.1767 0.189 900

04/08/24 13:36:39 0.187 0.1767 0.189 100

04/08/24 13:29:40 0.189 0.1762 0.189 11,000

04/08/24 13:29:39 0.1887 0.1762 0.189 5,000

04/08/24 13:29:09 0.1885 0.1761 0.1887 2,800

04/08/24 13:29:09 0.1885 0.1761 0.1887 500

04/08/24 13:29:09 0.1844 0.1761 0.1887 500

04/08/24 13:27:17 0.1887 0.18 0.1887 3,300

04/08/24 13:27:11 0.1844 0.18 0.1887 500

04/08/24 13:25:34 0.1887 0.18 0.1887 2,100

04/08/24 13:25:21 0.1844 0.18 0.1887 500

04/08/24 13:14:39 0.1844 0.18 0.1887 200

04/08/24 13:14:19 0.18 0.176 0.1887 100

04/08/24 13:14:19 0.18 0.176 0.1887 5,100

04/08/24 13:14:04 0.178 0.176 0.18 500

04/08/24 13:12:45 0.178 0.176 0.18 200

04/08/24 13:12:29 0.1772 0.176 0.18 5,000

04/08/24 13:05:35 0.18 0.175 0.18 1,000

04/08/24 13:04:53 0.175 0.174 0.18 2,500

04/08/24 13:01:18 0.1758 0.174 0.18 10,000

04/08/24 12:57:21 0.174 0.1725 0.174 10,000

04/08/24 12:57:00 0.1735 0.1725 0.174 10,000

04/08/24 12:56:36 0.174 0.1725 0.174 10,000

04/08/24 12:48:56 0.1725 0.1651 0.174 9,000

04/08/24 12:48:56 0.1725 0.1651 0.174 1,000

04/08/24 12:47:22 0.1688 0.1651 0.1725 500

04/08/24 12:46:27 0.1688 0.1651 0.1725 400

04/08/24 12:46:14 0.1688 0.1651 0.1725 600

04/08/24 12:36:25 0.1699 0.1651 0.1725 1,500

04/08/24 12:29:10 0.17 0.1651 0.17 2,000

04/08/24 12:29:03 0.1676 0.1651 0.17 500

04/08/24 12:28:35 0.1685 0.1651 0.17 200

04/08/24 12:28:20 0.168 0.1651 0.17 4,000

04/08/24 12:14:25 0.1714 0.1651 0.1725 200

04/08/24 12:11:02 0.1691 0.1651 0.173 1,000

04/08/24 12:10:57 0.1691 0.1651 0.173 500

04/08/24 11:24:42 0.1706 0.1651 0.173 100

04/08/24 11:24:00 0.17 0.165 0.17 5,200

04/08/24 11:23:54 0.17 0.165 0.17 9,800

04/08/24 11:08:37 0.1704 0.165 0.174 4,000

04/08/24 11:05:02 0.175 0.165 0.175 2,600

04/08/24 11:05:02 0.172 0.165 0.175 3,000

04/08/24 11:02:51 0.175 0.164 0.175 200

04/08/24 11:02:51 0.1734 0.164 0.175 200

04/08/24 11:01:51 0.165 0.165 0.175 22,500

04/08/24 11:01:37 0.175 0.165 0.175 500

04/08/24 11:00:33 0.175 0.1651 0.179 200

04/08/24 11:00:33 0.1721 0.1651 0.179 200

04/08/24 11:00:23 0.1721 0.1651 0.179 200

04/08/24 11:00:17 0.1721 0.1651 0.179 300

04/08/24 10:53:04 0.175 0.1651 0.179 200

04/08/24 10:53:04 0.1721 0.1651 0.179 200

04/08/24 10:53:00 0.167 0.167 0.179 1,900

04/08/24 10:52:56 0.175 0.167 0.179 200

04/08/24 10:52:56 0.173 0.167 0.179 200

04/08/24 10:52:52 0.173 0.167 0.179 200

04/08/24 10:52:39 0.173 0.167 0.179 500

04/08/24 10:46:34 0.1781 0.167 0.18 1,000

04/08/24 10:46:17 0.1682 0.1682 0.18 17,500

04/08/24 10:46:14 0.1712 0.1682 0.18 7,500

04/08/24 10:44:06 0.1742 0.1683 0.18 2,700

04/08/24 10:44:00 0.1742 0.1683 0.18 500

04/08/24 10:37:37 0.18 0.1671 0.18 5,000

04/08/24 10:37:31 0.18 0.1671 0.18 100

04/08/24 10:37:31 0.18 0.1671 0.18 4,900

04/08/24 10:21:17 0.18 0.164 0.18 5,000

04/08/24 10:21:16 0.18 0.164 0.18 100

04/08/24 10:20:56 0.172 0.164 0.18 500

04/08/24 10:08:45 0.1776 0.164 0.18 200

04/08/24 10:03:15 0.1645 0.164 0.165 9,500

04/08/24 10:03:10 0.1645 0.164 0.165 500

04/08/24 10:02:22 0.164 0.164 0.165 5,500

04/08/24 10:02:17 0.165 0.164 0.165 1,000

04/08/24 10:02:07 0.165 0.00 0.00 1,625

04/08/24 09:59:56 0.164 0.164 0.165 1,900

04/08/24 09:59:34 0.1646 0.164 0.165 500

04/08/24 09:58:41 0.164 0.158 0.164 12,000

04/08/24 09:48:11 0.164 0.158 0.165 10,000

04/08/24 09:38:22 0.1622 0.158 0.165 200

04/08/24 09:30:09 0.16 0.158 0.165 1,000

04/05/24 15:47:36 0.1565 0.153 0.16 50

04/05/24 15:47:36 0.1565 0.153 0.16 100

04/05/24 15:47:20 0.153 0.153 0.16 29

04/05/24 15:47:20 0.153 0.153 0.16 100

04/05/24 14:56:54 0.16 0.153 0.16 82

04/05/24 14:56:54 0.16 0.153 0.16 1,100

04/05/24 14:29:20 0.1565 0.153 0.16 2,500

04/05/24 14:26:54 0.1579 0.153 0.16 2,500

04/05/24 13:34:33 0.1579 0.153 0.16 500

04/05/24 13:34:22 0.1565 0.153 0.16 500

04/05/24 13:34:11 0.1565 0.153 0.16 73

04/05/24 13:34:11 0.1565 0.153 0.16 2,100

04/05/24 13:22:33 0.1579 0.153 0.16 500

04/05/24 13:01:28 0.155 0.155 0.16 400

04/05/24 13:01:19 0.155 0.155 0.16 1,000

04/05/24 12:25:23 0.1575 0.155 0.16 2,000

04/05/24 12:25:17 0.1575 0.155 0.16 500

04/05/24 12:11:46 0.16 0.155 0.16 500

04/05/24 10:48:32 0.155 0.155 0.16 5,000

04/05/24 09:33:46 0.165 0.152 0.165 5,800

04/05/24 09:32:00 0.165 0.152 0.165 20

04/05/24 09:30:28 0.165 0.152 0.165 100

04/05/24 09:30:02 0.152 0.152 0.165 81,300

04/05/24 09:30:02 0.165 0.152 0.165 81,311

04/05/24 09:30:00 0.165 0.152 0.165 100

04/04/24 15:42:15 0.1665 0.1651 0.1697 10,000

04/04/24 14:39:18 0.1651 0.1651 0.1697 5,000

04/04/24 14:06:59 0.1685 0.1651 0.1685 2,500

04/04/24 14:06:59 0.1668 0.1651 0.1685 500

04/04/24 13:58:51 0.1651 0.1651 0.1685 6,700

04/04/24 13:58:48 0.1651 0.1651 0.1685 1,000

04/04/24 13:44:25 0.1681 0.1651 0.1697 10,000

04/04/24 13:39:37 0.1697 0.1651 0.1697 2,400

04/04/24 13:39:32 0.1674 0.1651 0.1697 500

04/04/24 13:01:46 0.1697 0.1651 0.1697 1,000

04/04/24 12:58:49 0.1651 0.1651 0.1697 1,500

04/04/24 12:58:29 0.1674 0.1651 0.1697 500

04/04/24 12:23:23 0.1651 0.1651 0.1697 3,500

04/04/24 11:55:52 0.1651 0.1651 0.1697 2,800

04/04/24 11:55:49 0.1651 0.1651 0.1697 1,000

04/04/24 11:52:51 0.1681 0.1651 0.1697 7,000

04/04/24 11:50:22 0.1674 0.165 0.1697 28,900

04/04/24 11:50:14 0.1674 0.165 0.1697 500

04/04/24 11:44:22 0.165 0.165 0.1697 2,000

04/04/24 11:44:21 0.1674 0.165 0.1697 500

04/04/24 11:41:06 0.165 0.165 0.1697 3,000

04/04/24 11:37:13 0.1651 0.165 0.1697 7,000

04/04/24 11:36:41 0.1697 0.165 0.1697 1,000

04/04/24 11:24:08 0.168 0.1585 0.1697 100

04/04/24 11:22:25 0.1585 0.1585 0.1697 10,000

04/04/24 10:48:53 0.1663 0.1585 0.1697 1,000

04/04/24 10:46:32 0.1697 0.1585 0.1697 2,000

04/04/24 10:46:24 0.1641 0.1585 0.1697 500

04/04/24 10:23:43 0.165 0.156 0.1697 12,900

04/04/24 10:23:41 0.165 0.156 0.165 8,700

04/04/24 10:23:37 0.164 0.156 0.164 8,400

04/04/24 10:22:51 0.164 0.156 0.164 6,600

04/04/24 10:22:44 0.164 0.156 0.164 8,400

04/04/24 10:05:51 0.1595 0.155 0.164 500

04/04/24 10:02:31 0.1598 0.1598 0.164 5,600

04/04/24 09:59:47 0.1598 0.155 0.1598 5,000

04/04/24 09:59:46 0.1598 0.155 0.1598 5,000

04/04/24 09:31:41 0.1549 0.152 0.1549 5,000

04/04/24 09:31:37 0.155 0.152 0.1549 24,000

04/04/24 09:31:25 0.1538 0.1538 0.1549 8,000

04/04/24 09:30:00 0.159 0.152 0.159 600

04/04/24 09:30:00 0.155 0.152 0.159 645

04/04/24 09:30:00 0.155 0.152 0.159 7,000

04/03/24 15:59:43 0.1549 0.1511 0.1549 50

04/03/24 15:59:43 0.1549 0.1511 0.1549 100

04/03/24 15:47:12 0.1511 0.1511 0.1549 71

04/03/24 15:47:12 0.1511 0.1511 0.1549 100

04/03/24 15:44:56 0.1517 0.1511 0.1549 1,000

04/03/24 14:51:45 0.1549 0.151 0.1549 50

04/03/24 14:51:45 0.1549 0.151 0.1549 100

04/03/24 14:49:41 0.1508 0.1503 0.1549 50,000

04/03/24 14:47:16 0.1549 0.1503 0.1549 1,000

04/03/24 14:46:44 0.1549 0.1503 0.1549 1,000

04/03/24 14:17:20 0.1503 0.1503 0.1549 15,600

04/03/24 14:17:13 0.1504 0.1503 0.1549 500

04/03/24 14:16:17 0.1505 0.1503 0.1505 7,800

04/03/24 14:15:53 0.1505 0.1503 0.1505 2,500

04/03/24 14:15:44 0.1505 0.1504 0.1505 2,000

04/03/24 14:15:39 0.1505 0.1504 0.1505 5,000

04/03/24 14:15:33 0.1505 0.1505 0.155 500

04/03/24 14:15:30 0.1505 0.1505 0.155 5,000

04/03/24 14:15:29 0.1507 0.1505 0.155 5,000

04/03/24 14:15:21 0.1505 0.1505 0.155 5,000

04/03/24 14:15:20 0.1507 0.1505 0.155 5,000

04/03/24 14:14:52 0.1507 0.1505 0.155 5,000

04/03/24 12:41:37 0.15 0.15 0.1597 33,000

04/03/24 12:41:31 0.151 0.151 0.1597 5,000

04/03/24 12:41:00 0.151 0.151 0.1597 5,000

04/03/24 12:40:22 0.151 0.151 0.157 8,000

04/03/24 12:39:20 0.157 0.151 0.157 99

04/03/24 12:39:20 0.157 0.151 0.157 69,600

04/03/24 12:37:28 0.151 0.151 0.157 86

04/03/24 12:37:28 0.151 0.151 0.157 13,300

04/03/24 12:22:22 0.157 0.151 0.157 3,000

04/03/24 12:22:16 0.154 0.151 0.157 500

04/03/24 12:22:14 0.154 0.151 0.157 7,000

04/03/24 12:22:08 0.156 0.151 0.157 500

04/03/24 10:38:43 0.151 0.151 0.157 40

04/03/24 10:38:38 0.151 0.151 0.1598 13,000

04/03/24 10:38:26 0.151 0.151 0.1598 5,000

04/03/24 10:30:19 0.155 0.155 0.1599 1,500

04/03/24 10:29:58 0.1575 0.155 0.1599 500

04/03/24 09:52:29 0.156 0.156 0.1599 5,000

04/03/24 09:52:21 0.155 0.156 0.1599 5,000

04/03/24 09:33:57 0.1599 0.156 0.1599 2,000

How on earth can you say that exposing decades of stock market pump and dumps from the CEO, BONAR, has no "facts"?

He has not run a single successful public company, every one failed while he got rich.

That is public knowledge.

Did you hear the one about BONAR and the Nigerian money launderers?

You can start reading here:

XenaLives

Member Level

Re: Lazarus post# 10439

Monday, August 26, 2019 1:08:16 PM

Post# 10446 of 10800

So did BONAR get suckered by the Nigerians?

If he didn't know about WSML he got suckered.

If he did know about WSML he was complicit in a Nigerian scam.

Not good either way.

BONAR trained stock market crooks that caused a good man to lose his business.

It's a moral vendetta - nothing personal about it, except for the fact that he chose to go after me personally for telling the truth.

B.B. tried that B.S. to intimidate me before..

He even lied to IHUB to get my personal info.

He has no cause of action.

Perhaps we have another BONAR alias here....

You're no freekin' lawyer.

Neither is BONAR

My posts are well documented. I've been following this fraud's history for decades.

MM's don't give a damn about BONAR and his pump and dumps.

I guess you missed the LOL !!!!! part of that post.

You also overlooked decades of documented BONAR pump and dump history.

Hmmmm......

Gee... when you're doing something that has never been done before and you have to collaborate with other parties to get it done..

Things don't always go as planned...

This discussion is absurd.

You can see block sales and comment here:

https://investorshub.advfn.com/Xenas-Study-Hall-29911

This is really important information...

The complete text from X followed by the post and video:

This might be one of the most important documentaries that anyone can watch right now given current events and escalations between Hamas, Israel, Iran, and the US.

All wars are bankers wars.

If you are still caught up in the left vs right, Israel vs Palestine, Ukraine vs Russia narratives, treating geopolitics and war as if it's a football game where you are rooting for one side to win as the real moral authority, then you need to take 45 minutes out of your day to watch this in full.

I've shared this documentary already weeks ago and a lot of people saw it and appreciated it, but I think it's now more important than ever for as many people to see it as possible and to really understand the profound and eye opening truth behind those words, and how EVERY SINGLE conflict has had powers above it funding both sides with nefarious intent behind it and a broader agenda that is not in the true interests of the people.

I don't think any of what's happening right now is organic. I don't think Hamas getting into Israel to murder and capture civilians was a mistake, nor do I think the $6bil the Biden admin unfroze for Iran in exchange for hostages before the attack was a mistake either. They're constructing narratives right in front of us and we cannot just blindly believe them on surface level evaluation, especially when these narratives are being given by the establishment and MSM.

I've said this before and I'll say it again. You need to think like they do with strategy, perception, and propagandistic motivations in mind. You need to try and understand why they are presenting whatever information to the public and for what purpose. You need to question every action, every directive, every media spin.

Why is the narrative now shifting towards Biden admin causing this attack by releasing funds to Iran? Why is Lindsey Graham pre-emptively suggesting war with Iran in conjunction with this? What if this is designed to ensure Biden attacks Iran to cover his ass in giving them $6bil back?

Also...Why was there such a huge focus of attention on anti-semitism on X in the weeks leading up to this attack? Was that organic? or was that planned in advance knowing there would be an attack on Israel and perceptions needed to be pre-emptively put in place for justifying censorship?

Question everything. Assume conspiracy.

This might be one of the most important documentaries that anyone can watch right now given current events and escalations between Hamas, Israel, Iran, and the US.

— Inversionism (@Inversionism) October 8, 2023

All wars are bankers wars.

If you are still caught up in the left vs right, Israel vs Palestine, Ukraine vs… pic.twitter.com/1X7oWbwsY5

Every stock offering that Brian Bonar has done for close to 50 years has been a scam...

Why did IBM kick him out?

Probably because they knew he was a crook.

Did I post enough facts today?

There's lots more that I can bring up if you want me to.

OK - if 3-71 must be dosed 3x per day there will be noncompliance.

So maybe 3-71 will be given in a supervised care setting to get a patient on track and later moved to 2-73 with a longer half life.

That would make a lot of sense.

It would also explain why 2-73 was trialed first.

Trades >=1K

All of April so far, linking back to March data..

04/11/24 16:02:22 4.18 4.02 4.28 2,100

04/11/24 16:01:58 4.18 4.02 4.28 13,200

04/11/24 16:00:03 4.19 4.17 4.19 1,113

04/11/24 16:00:01 4.19 4.17 4.19 9,464

04/11/24 16:00:00 4.19 4.18 4.19 82,073

04/11/24 15:46:30 4.185 4.18 4.19 1,000

04/11/24 15:18:31 4.1693 4.16 4.17 1,000

04/11/24 13:29:15 4.2701 4.27 4.28 1,000

04/11/24 13:29:15 4.2701 4.27 4.28 6,000

04/11/24 13:25:01 4.2427 4.24 4.25 1,000

04/11/24 13:21:57 4.24 4.23 4.24 9,900

04/11/24 13:17:19 4.21 4.21 4.22 1,800

04/11/24 13:17:19 4.21 4.21 4.22 2,200

04/11/24 13:17:00 4.21 4.22 4.23 2,300

04/11/24 13:16:54 4.22 4.22 4.23 1,600

04/11/24 13:16:54 4.22 4.22 4.23 1,400

04/11/24 13:08:54 4.19 4.19 4.20 1,600

04/11/24 13:07:51 4.2009 4.20 4.21 3,000

04/11/24 13:02:56 4.18 4.15 4.16 3,400

04/11/24 13:02:56 4.16 4.15 4.16 1,700

04/11/24 13:01:24 4.1501 4.15 4.16 1,000

04/11/24 13:01:13 4.1494 4.14 4.15 1,000

04/11/24 12:43:43 4.15 4.15 4.16 3,800

04/11/24 12:43:31 4.14 4.15 4.16 2,200

04/11/24 12:43:31 4.15 4.15 4.16 1,100

04/11/24 12:43:31 4.15 4.15 4.16 1,000

04/11/24 12:25:48 4.145 4.14 4.15 1,200

04/11/24 12:25:40 4.1501 4.15 4.16 3,300

04/11/24 12:25:40 4.1511 4.15 4.16 3,300

04/11/24 12:15:50 4.1394 4.13 4.14 1,900

04/11/24 12:15:50 4.1394 4.13 4.14 1,000

04/11/24 12:10:17 4.1299 4.12 4.13 2,000

04/11/24 12:05:04 4.135 4.13 4.14 1,000

04/11/24 11:58:52 4.1109 4.11 4.12 2,900

04/11/24 11:57:19 4.12 4.11 4.12 1,100

04/11/24 11:57:09 4.11 4.10 4.11 1,100

04/11/24 11:55:36 4.10 4.10 4.11 3,300

04/11/24 11:55:32 4.10 4.10 4.11 1,132

04/11/24 11:53:33 4.0599 4.05 4.06 7,600

04/11/24 11:35:43 4.0209 4.02 4.03 1,700

04/11/24 11:35:43 4.0209 4.02 4.03 1,200

04/11/24 11:08:58 4.0299 4.02 4.03 2,500

04/11/24 10:58:15 4.04 4.04 4.05 1,300

04/11/24 10:26:21 4.035 4.03 4.04 1,000

04/11/24 10:24:05 4.0399 4.03 4.04 1,000

04/11/24 10:16:26 4.0301 4.03 4.04 1,900

04/11/24 10:16:26 4.0301 4.03 4.04 1,000

04/11/24 10:12:59 4.0398 4.03 4.04 1,000

04/11/24 10:10:59 4.05 4.05 4.06 1,800

04/11/24 10:10:59 4.05 4.05 4.06 1,700

04/11/24 10:07:12 4.06 4.06 4.07 1,700

04/11/24 10:07:12 4.06 4.06 4.07 2,200

04/11/24 10:03:45 4.0699 4.06 4.07 1,700

04/11/24 10:03:45 4.0699 4.06 4.07 1,200

04/11/24 10:02:52 4.05 4.07 4.08 5,800

04/11/24 10:02:52 4.07 4.07 4.08 2,800

04/11/24 10:02:24 4.07 4.08 4.09 7,800

04/11/24 10:01:05 4.085 4.08 4.09 2,400

04/11/24 09:59:05 4.1001 4.10 4.11 2,900

04/11/24 09:59:05 4.1001 4.10 4.11 1,200

04/11/24 09:50:28 4.1099 4.10 4.11 4,900

04/11/24 09:49:30 4.1024 4.10 4.11 3,000

04/11/24 09:46:07 4.1098 4.10 4.11 3,000

04/11/24 09:44:42 4.10 4.10 4.11 1,100

04/11/24 09:39:07 4.12 4.12 4.13 1,700

04/11/24 09:33:11 4.155 4.14 4.17 1,000

04/11/24 09:31:17 4.16 4.13 4.16 1,400

04/11/24 09:31:17 4.16 4.13 4.16 2,500

04/11/24 09:31:17 4.15 4.13 4.16 1,300

04/11/24 09:30:00 4.12 4.08 4.24 11,000

04/11/24 09:23:30 4.11 4.07 4.11 2,700

04/11/24 09:21:59 4.12 4.07 4.18 3,200

04/11/24 09:19:08 4.22 4.22 4.26 2,800

04/11/24 06:07:10 4.11 4.11 4.44 1,000

04/10/24 16:02:27 4.12 4.05 4.28 1,700

04/10/24 16:02:25 4.12 4.05 4.28 2,700

04/10/24 16:01:35 4.12 4.05 4.28 1,700

04/10/24 16:00:06 4.12 4.09 4.13 4,115

04/10/24 16:00:02 4.12 4.09 4.13 1,799

04/10/24 16:00:01 4.12 4.09 4.13 104,452

04/10/24 15:59:51 4.12 4.11 4.12 1,975

04/10/24 15:59:04 4.115 4.11 4.12 1,218

04/10/24 15:57:34 4.13 4.12 4.13 1,200

04/10/24 15:57:01 4.12 4.12 4.13 1,600

04/10/24 15:57:01 4.12 4.12 4.13 1,800

04/10/24 15:57:01 4.12 4.12 4.13 3,400

04/10/24 15:56:44 4.1299 4.12 4.13 3,000

04/10/24 15:56:19 4.1201 4.12 4.13 2,500

04/10/24 15:56:08 4.1208 4.12 4.13 1,700

04/10/24 15:56:08 4.1208 4.12 4.13 1,200

04/10/24 15:54:45 4.1285 4.12 4.13 1,000

04/10/24 15:45:37 4.11 4.10 4.11 1,400

04/10/24 15:43:08 4.10 4.10 4.11 1,800

04/10/24 15:26:16 4.1261 4.12 4.13 1,000

04/10/24 15:02:56 4.0985 4.09 4.10 1,000

04/10/24 13:36:38 4.10 4.09 4.10 2,300

04/10/24 13:36:38 4.095 4.09 4.10 2,400

04/10/24 13:01:44 4.10 4.08 4.09 10,000

04/10/24 13:01:44 4.10 4.08 4.09 7,600

04/10/24 13:01:44 4.10 4.08 4.09 1,400

04/10/24 13:01:43 4.10 4.08 4.10 21,200

04/10/24 12:54:37 4.1009 4.10 4.11 1,800

04/10/24 12:54:37 4.1009 4.10 4.11 1,100

04/10/24 12:47:08 4.10 4.10 4.11 1,000

04/10/24 11:35:41 4.1001 4.10 4.11 1,100

04/10/24 11:33:34 4.10 4.10 4.11 1,000

04/10/24 11:24:36 4.10 4.10 4.11 3,300

04/10/24 11:10:16 4.09 4.09 4.10 1,300

04/10/24 11:10:16 4.09 4.09 4.10 1,000

04/10/24 11:09:41 4.10 4.10 4.11 1,400

04/10/24 10:57:02 4.11 4.10 4.11 1,100

04/10/24 10:55:03 4.0999 4.10 4.11 1,429

04/10/24 10:48:10 4.12 4.10 4.11 1,900

04/10/24 10:48:10 4.12 4.10 4.11 1,000

04/10/24 10:25:36 4.1454 4.14 4.15 1,400

04/10/24 10:24:59 4.1406 4.14 4.15 2,000

04/10/24 10:23:33 4.13 4.14 4.15 1,100

04/10/24 10:23:33 4.13 4.14 4.15 1,200

04/10/24 10:21:36 4.1493 4.14 4.15 2,300

04/10/24 10:08:35 4.125 4.12 4.13 1,000

04/10/24 10:06:11 4.1193 4.11 4.12 1,000

04/10/24 10:02:33 4.095 4.09 4.10 1,000

04/10/24 10:00:37 4.1099 4.11 4.12 1,200

04/10/24 09:59:54 4.11 4.10 4.11 1,200

04/10/24 09:59:54 4.11 4.10 4.11 1,200

04/10/24 09:48:22 4.09 4.08 4.09 2,200

04/10/24 09:36:18 4.11 4.11 4.13 2,600

04/10/24 09:35:38 4.14 4.10 4.11 7,300

04/10/24 09:32:07 4.0902 4.07 4.10 1,300

04/10/24 09:31:38 4.08 4.08 4.11 1,200

04/10/24 09:30:09 4.11 4.10 4.13 1,600

04/10/24 09:30:09 4.10 4.10 4.13 1,900

04/10/24 09:30:09 4.10 4.10 4.13 1,800

04/10/24 09:30:01 4.15 4.12 4.15 15,600

04/10/24 09:26:26 4.07 4.05 4.07 2,600

04/09/24 16:01:30 4.26 4.15 4.44 3,200

04/09/24 16:00:00 4.26 4.24 4.28 34,259

04/09/24 15:55:05 4.26 4.25 4.26 1,400

04/09/24 15:54:40 4.26 4.25 4.26 25,000

04/09/24 15:54:40 4.26 4.25 4.26 7,600

04/09/24 15:54:40 4.26 4.25 4.26 44,536

04/09/24 15:51:25 4.27 4.27 4.28 1,000

04/09/24 15:49:24 4.271 4.27 4.28 1,000

04/09/24 15:40:00 4.255 4.25 4.26 1,029

04/09/24 15:22:17 4.24 4.24 4.25 1,100

04/09/24 15:21:31 4.25 4.25 4.26 1,000

04/09/24 16:01:30 4.26 4.15 4.44 3,200

04/09/24 16:00:00 4.26 4.24 4.28 34,259

04/09/24 15:55:05 4.26 4.25 4.26 1,400

04/09/24 15:54:40 4.26 4.25 4.26 25,000

04/09/24 15:54:40 4.26 4.25 4.26 7,600

04/09/24 15:54:40 4.26 4.25 4.26 44,536

04/09/24 15:51:25 4.27 4.27 4.28 1,000

04/09/24 15:49:24 4.271 4.27 4.28 1,000

04/09/24 15:40:00 4.255 4.25 4.26 1,029

04/09/24 15:22:17 4.24 4.24 4.25 1,100

04/09/24 15:21:31 4.25 4.25 4.26 1,000

04/09/24 15:20:52 4.25 4.24 4.25 1,300

04/09/24 15:18:20 4.24 4.23 4.24 8,000

04/09/24 15:14:50 4.23 4.23 4.24 1,100

04/09/24 15:14:50 4.23 4.23 4.24 1,200

04/09/24 15:12:27 4.24 4.24 4.25 1,000

04/09/24 15:10:18 4.245 4.24 4.25 1,200

04/09/24 15:10:18 4.245 4.24 4.25 1,200

04/09/24 15:10:13 4.245 4.24 4.25 1,000

04/09/24 15:09:18 4.2499 4.24 4.25 2,500

04/09/24 15:06:59 4.2407 4.24 4.25 1,000

04/09/24 15:05:33 4.249 4.24 4.25 1,000

04/09/24 15:01:15 4.24 4.24 4.25 1,000

04/09/24 14:58:35 4.2503 4.25 4.26 1,000

04/09/24 14:58:31 4.2506 4.25 4.26 1,000

04/09/24 14:58:27 4.2501 4.25 4.26 1,000

04/09/24 14:56:08 4.255 4.25 4.26 1,000

04/09/24 14:46:21 4.25 4.27 4.28 3,500

04/09/24 14:34:46 4.285 4.28 4.29 1,000

04/09/24 14:18:04 4.31 4.31 4.32 1,900

04/09/24 14:18:04 4.31 4.31 4.32 1,000

04/09/24 14:16:33 4.3101 4.31 4.32 2,500

04/09/24 14:16:10 4.315 4.31 4.32 1,000

04/09/24 14:08:28 4.3001 4.30 4.31 1,000

04/09/24 14:03:10 4.3001 4.30 4.31 1,600

04/09/24 14:02:57 4.3097 4.30 4.31 1,000

04/09/24 14:02:13 4.305 4.30 4.31 1,000

04/09/24 13:49:14 4.31 4.31 4.32 1,000

04/09/24 13:37:11 4.3201 4.32 4.33 1,000

04/09/24 13:33:02 4.3237 4.32 4.33 1,000

04/09/24 13:27:55 4.325 4.32 4.33 1,000

04/09/24 13:12:41 4.321 4.32 4.33 1,000

04/09/24 13:06:53 4.335 4.33 4.34 1,000

04/09/24 13:02:16 4.335 4.33 4.34 1,000

04/09/24 12:24:20 4.345 4.34 4.35 1,000

04/09/24 12:22:38 4.345 4.34 4.35 1,000

04/09/24 12:00:05 4.32 4.31 4.32 4,400

04/09/24 11:46:34 4.3096 4.30 4.31 5,000

04/09/24 11:44:16 4.31 4.31 4.32 5,000

04/09/24 11:39:31 4.315 4.31 4.32 1,000

04/09/24 11:01:49 4.33 4.31 4.32 1,100

04/09/24 11:01:49 4.33 4.31 4.32 1,400

04/09/24 11:00:53 4.3152 4.31 4.32 1,400

04/09/24 10:54:22 4.31 4.31 4.32 3,900

04/09/24 10:52:46 4.32 4.32 4.33 1,300

04/09/24 10:52:46 4.32 4.32 4.33 1,200

04/09/24 10:49:39 4.36 4.35 4.36 3,900

04/09/24 10:15:34 4.42 4.42 4.43 2,800

04/09/24 10:15:34 4.42 4.42 4.43 1,100

04/09/24 10:09:25 4.4183 4.41 4.42 2,500

04/09/24 10:08:04 4.415 4.41 4.42 1,000

04/09/24 10:05:23 4.425 4.42 4.43 1,000

04/09/24 09:59:39 4.4401 4.44 4.45 5,000

04/09/24 09:58:10 4.44 4.43 4.44 1,500

04/09/24 09:53:58 4.45 4.44 4.45 1,500

04/09/24 09:50:17 4.435 4.43 4.44 1,000

04/09/24 09:45:59 4.4168 4.41 4.42 1,000

04/09/24 09:43:08 4.415 4.41 4.42 1,100

04/09/24 09:41:25 4.425 4.42 4.43 1,000

04/09/24 09:30:00 4.38 4.18 4.65 1,100

04/09/24 09:30:00 4.43 4.18 4.65 18,400

04/08/24 16:13:00 4.36 4.25 4.65 1,700

04/08/24 16:00:07 4.365 4.34 4.38 4,376

04/08/24 16:00:00 4.365 4.36 4.37 50,897

04/08/24 15:59:45 4.365 4.36 4.37 1,271

04/08/24 15:59:35 4.365 4.36 4.37 1,300

04/08/24 15:41:30 4.375 4.37 4.38 1,300

04/08/24 15:19:45 4.365 4.36 4.37 1,100

04/08/24 14:39:20 4.38 4.38 4.39 1,700

04/08/24 14:39:20 4.38 4.38 4.39 1,200

04/08/24 13:55:10 4.39 4.39 4.40 1,055

04/08/24 13:36:38 4.38 4.38 4.39 1,600

04/08/24 13:35:22 4.38 4.38 4.39 1,000

04/08/24 13:32:15 4.39 4.38 4.39 2,200

04/08/24 13:04:43 4.3891 4.38 4.39 1,100

04/08/24 12:56:20 4.3801 4.38 4.39 1,000

04/08/24 12:55:28 4.385 4.38 4.39 1,000

04/08/24 12:49:05 4.385 4.38 4.39 2,500

04/08/24 12:40:56 4.3801 4.38 4.39 1,000

04/08/24 12:35:50 4.4015 4.40 4.41 1,000

04/08/24 12:34:51 4.4015 4.40 4.41 1,000

04/08/24 12:32:32 4.40 4.39 4.40 1,000

04/08/24 12:07:49 4.385 4.38 4.39 1,000

04/08/24 11:55:42 4.38 4.38 4.39 1,400

04/08/24 11:36:23 4.38 4.38 4.39 1,854

04/08/24 11:12:42 4.3901 4.39 4.40 1,000

04/08/24 10:57:57 4.3801 4.38 4.39 1,000

04/08/24 10:52:32 4.355 4.35 4.36 1,200

04/08/24 10:49:43 4.355 4.35 4.36 1,000

04/08/24 10:46:49 4.355 4.35 4.36 1,000

04/08/24 10:32:41 4.355 4.35 4.36 1,000

04/08/24 10:22:30 4.3302 4.33 4.34 1,100

04/08/24 09:52:13 4.3999 4.39 4.40 1,000

04/08/24 09:50:38 4.4101 4.41 4.42 2,200

04/08/24 09:50:38 4.4101 4.41 4.42 1,200

04/08/24 09:42:25 4.395 4.39 4.40 1,000

04/08/24 09:40:50 4.385 4.38 4.39 2,500

04/08/24 09:38:45 4.395 4.39 4.40 1,000

04/08/24 09:36:51 4.415 4.41 4.42 1,100

04/08/24 09:34:38 4.39 4.39 4.41 1,500

04/08/24 09:30:01 4.41 4.40 4.49 1,900

04/05/24 16:02:04 4.36 4.18 4.55 2,200

04/05/24 16:01:57 4.36 4.18 4.55 1,900

04/05/24 16:01:32 4.36 4.18 4.55 3,300

04/05/24 16:00:00 4.37 4.34 4.38 56,402

04/05/24 15:58:24 4.365 4.36 4.37 2,000

04/05/24 15:58:00 4.3575 4.36 4.37 1,299

04/05/24 15:56:35 4.3528 4.35 4.36 1,100

04/05/24 15:48:29 4.35 4.35 4.36 1,447

04/05/24 15:48:28 4.35 4.35 4.36 2,400

04/05/24 15:36:18 4.37 4.37 4.38 3,500

04/05/24 14:57:20 4.34 4.33 4.34 1,600

04/05/24 14:57:20 4.34 4.33 4.34 1,000

04/05/24 14:57:20 4.34 4.33 4.34 6,860

04/05/24 14:00:40 4.34 4.34 4.35 2,200

04/05/24 14:00:40 4.34 4.34 4.35 1,700

04/05/24 13:56:50 4.3401 4.34 4.35 2,400

04/05/24 13:41:05 4.34 4.33 4.34 1,000

04/05/24 13:41:05 4.34 4.33 4.34 1,700

04/05/24 13:40:30 4.335 4.33 4.34 1,200

04/05/24 13:39:34 4.335 4.33 4.34 2,000

04/05/24 12:57:59 4.335 4.33 4.34 1,000

04/05/24 12:56:38 4.3301 4.33 4.34 1,000

04/05/24 12:46:38 4.325 4.32 4.33 1,000

04/05/24 12:40:03 4.33 4.32 4.33 1,409

04/05/24 11:45:40 4.365 4.36 4.37 4,800

04/05/24 11:45:08 4.3358 4.33 4.34 4,700

04/05/24 11:31:04 4.3201 4.32 4.33 1,000

04/05/24 11:22:17 4.3185 4.31 4.32 1,000

04/05/24 10:54:50 4.355 4.35 4.36 1,000

04/05/24 10:18:20 4.355 4.35 4.36 1,110

04/05/24 10:18:20 4.37 4.35 4.36 1,100

04/05/24 10:13:11 4.40 4.36 4.37 3,200

04/05/24 09:55:10 4.395 4.39 4.40 1,000

04/05/24 09:30:00 4.38 4.18 4.65 3,900

04/04/24 16:02:33 4.41 4.18 4.65 30,200