News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Treasury doesn't participate in listen-only mode roundtables, like Sandra Thompson attending a council meeting in the Town Hall of Pagliara's home town. Allegedly, because I haven't seen any image of the event.

What is Pagliara up to next?

Does Deputy Secretary Adeyemo know? Because he already had a roundtable about the subject at the NYSE, less than three months ago.

The reason this is important $fnma #fanniegate is because it picks up at Treasury where FHFA left off at Franklin TN. Sandra Thompson lit the torch there and now it is going nationwide. https://t.co/78DsGGWdFL

— Fanniegate Hero (@DoNotLose) December 12, 2023

Baby Bradford throws the stone and hides the hand.

If you claim that I lied, you have to prove it.

Just say that you don't understand the financial concepts.

What are you, eight?

It's YOU the one "pushing the cram-down trying to wipe out the common shareholders" when you are repeating it, plaintiff Joshua Angel, a JPS holder, along with our other enemy, Glen Bradford-LuLeVan.

The rest of us stick to the Separate Account plan, according to the Law.

Robert is a shill tasked with bothering the shareholders and mess around, so someone ends up saying: "It's complicated". A telltale sign when someone is being conned.

He even makes up what the SCOTUS said with quotation marks. Another sign, now of desperation:

the FHFA being able to do "whatever is in the bests interests of the FHFA and/or the public it serves."

It's time to put the "Finance for attorneys" to rest.

Remember, they stopped siphoning actual money almost 4.5 years ago. The ballooning liquidation preference doesn't hurt the companies at all.

"Capital Reserve End Date" in the January(not Sept)2021 amendment.

Fairholme Legal Team's Timothy Howard's integrity was compromised.

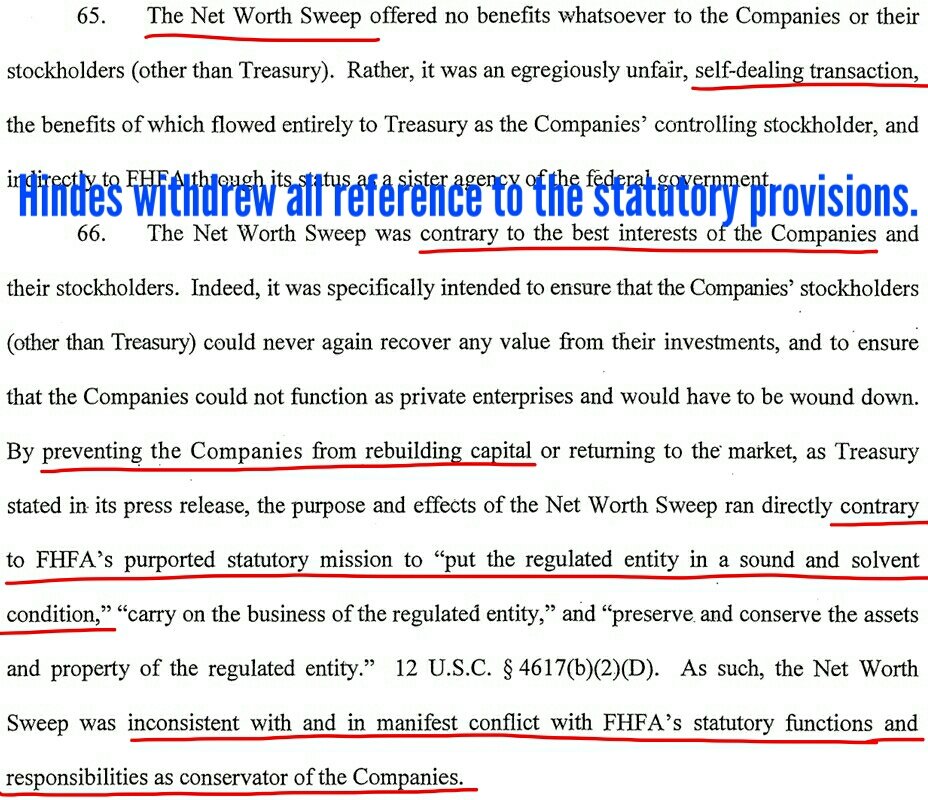

A Conservatorship preserves their status as private shareholder-owned enterprises, and it's a process for the financial rehabilitation of the enterprises, as Justice Alito stressed with "Rehabilitate FnF..." (adding the Marxist-way for the extortion of resources in the process), also according to the FHFA-C's Power (stance removed by Gary Hindes in an amended complaint, pointed out yesterday) and the fact that the FHEFSSA established a mandatory release Undercapitalized, though conveniently struck by Calabria's HERA (Source). Undercapitalized, a Capital Classification: Core Capital greater than the Minimum Leverage Capital requirements. Source) just in case that someone thinks that during Conservatorship, a company doesn't have to build capital.

Definition of Core Capital.

A conservatorship established for Critically Undercapitalized enterprises (Source) and banks (FDI Act), these people intend to make us believe that it's a status where they can start to decapitalize them on a great scale, with fat dividends to the government, SPS increased for free and the payment of Securities Litigation judgments (the 3 of them, capital distributions: 12 U.S.Code §4502(5)(A), amended by the FHFA to add the number 3 pointed out: CFR 1229.13, currently a breach in the Lamberth court, as FnF have already charged this payment in their Q3 reports. It's restricted for a reason (Recapitalization) and thus, you can't even set aside a reserve that has already deprived FnF of the capital they must retain. The FHEFSSA's Restriction on Capital Distributions, U.S.Code §4614(e) was inserted by HERA subtitle "Prompt Corrective Action" at the end of the section Capital Classifications in an attempt to make it go unnoticed, isn't just a fancy name), leaving FnF with an adjusted $-216 billion Accumulated Deficit Retained Earnings account combined. A CET1 account meant to absorb future losses (Today's Core Capital = $-194 billion combined). And later beg the UST to pardon the debentures. This isn't how it works. So much for rehabilitation, which is not the return to profitability as a judge claimed in the Federal Circuit, but those earnings must be retained to be considered the capital that measures the soundness in a financial company, as Calabria pointed out (Source). But "retained" for real, not retained and later eliminated with the offset (reduction of Retained Earnings) when the SPS are increased for free every quarter in the same amount (operation concealed with fraud: gifted SPS and offset, absent from the Balance Sheets, but we can see this effect in table).

returning the companies to their former states of shareholder-owned companies,

There is no implied contract by any stretch of the imagination, according to a British law firm.

Making clear that there's been Securities Law violations is important because the compensation for Punitive damages serves as an all-in settlement and thus, it leaves no other option than to pay damages.

-SPS increased, instead of issued.

-Gifted SPS absent from the balance sheets.

-Etc.

8 in total.

The fact that FnF are represented in the Lamberth court, when they don't have powers, which means that they don't exist under the Rule of Law until they are returned, can only be explained if they expect that, with the release from Conservatorship, these parties could fetch a confidential settlement with FnF.

In 2016, the auditor of Freddie Mac, PwC, agreed on a confidential settlement with several plaintiffs, where the terms were kept from the judge. This phony case was a trial balloon to stage that everything would be OK with all the felonies accumulated.

PwC has been on the news lately. At Mr. Crow's luxury resort and appointed to the BOD of Fannie Mae. Can you imagine that it was the same PwC executive?

PLAN OF ALLOCATION

The shareholders waive their claim to damages in the case of takeover or "as is" scenarios, with regard to the Securities Law violations/Punitive damages, and the round prompted by the Deferred Income accounting.

The plotters (plaintiffs, sponsors, etc) have no escape: $4.8 billion due.

So, one out of three rounds.

In the case of Takings plus Resale scenario, the shareholders request 3 rounds of $4.8 billion for the 3 damages.

On the other hand, the JPS holders' claim remains the same in the 3 rounds. So, they could get an annual 0.75% IRR on a JPS par value in interests, for these 15 years of lies "in the best interests of the Agency" (FHFA-C's Incidental Power).

The frivolous litigation has caused the damage of stocks trading at rock bottom prices.

Either for concealing the key statutory provisions and financial concepts, or for not challenging the Warrant.

Their stance in court doesn't recover even $1 of core capital, out of $420 billion worth of capital generated by FnF in 15 years ($301 billion cash dividend to UST and $118 billion through the offset when the SPS were increased for free with the new compensation to UST now in place), that would more than offset today's adjusted $402 billion capital deficit over Minimum Leverage capital requirement, FnF together and as of end of September 2023.

In order to have a sense of this misbehavior in court, we have the example of the hedge fund manager Gary Hindes, who filed an amended complaint on March 16, 2017, with the objective to remove every prior reference to the breach of statutory provision laid out in his first complaint filed on August 17, 2015.

The gang read in my tweets that the plaintiffs' take was insane, challenging the NWS dividend but not the 10% dividend, when both are the same breach of the FHFA-C's Rehab power that they were complaining about (a dividend depletes capital).

It's when the plaintiffs reagrouped and the Supreme Court was activated to target the FHFA-C's Incidental Power instead. Justice Alito only could play with words and attempt to mislead changing "best interests of the Agency" for "beneficial to the Agency" and adding "...and the public it serves" that isn't written in the law, in order to hold up the plotters' Government theft story a few more years, as counterparties of the DOJ in court, and try the fiction of Implied Contract breach, instead of the reality of the Separate Account plan, already carried out by the same officials in the 1989 bailout of the FHLBanks (Sandra Thompson at the FDIC and DeMarco at GAO first, the auditor, later at the UST)

The corrupt litigants and company face a $4.8 billion penalty for stock price manipulation in both Cs and JPS, in their conspiracy to defraud the shareholders in favor of the JPS holders, betting on a "restructuring" to share the booty with the UST.

Court delays directly impact FNMA/FMCC PPS.

In this world, we aren't ruled by implied rules.

You are just covering up the Charter Act, like many others: the Supreme Court, etc.

There is no Government Implicit Guarantee on the MBSs of FnF. There is a UST backup of FnF as a last resort ("Operations financed by private capital -Equity or Debt- to the maximum extent feasible". Section: Purposes) in exchange for their Public Mission (Section: Purposes), expressly written in the Charter Act.

You mix up a guarantee on MBSs, with a backup of the enterprises.

THEREFORE THERE IS AN IMPLICIT GUARANTEE NOT AN EXPLICIT FEDERAL GOVERNMENT GUARANTEE.

Why do you think Uncle Suggy wants so much Capital in a 1st Loss Position😉!

The feature of cash dividend added into LP of a preferred stock, in the case that the cash dividend is waived, which, as mentioned in the post that I'm replying to, it isn't our case with today's gifted SPS, as the dividend was eliminated as a response to judge Willett's ruling 3 weeks before, doesn't mean that an issuer can increase the LP when it taps the capital markets for funds, like FnF did, tapping the UST for funds every quarter in early conservatorship.

Because the underlying security in a Preferred Stock is a fixed-income security. An obligation to be precise and, as any obligation, they are unique and the issuer must issue the securites so they are dated and attached to a certificate of designations.

The UST hasn't purchased even one security. Everything "increased" or issued for free, like the Warrant to skip the prerequisite on purchases of "to protect the taxpayer" (collateral)

The increase in the SPS Liquidation Preference is, therefore, a Securities Law violation that others will call "deregulation", for which we are requesting a compensation for Punitive Damages, jointly with other 7 violations.

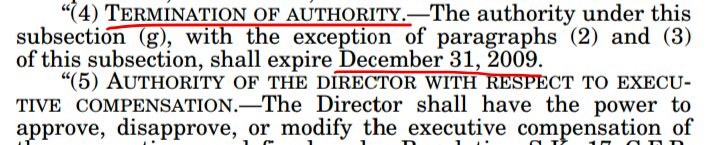

The objective was to skip the December 31, 2009 deadline in the "TEMPORARY authority of Treasury to purchase (high yield) SPS" inserted by HERA in the Charter Act for the Separate Account plan (the original one at a rate similar to Treasuries prevails. An estimated weighted-average 1.8% dividend rate, with a 0.5% spread over Treasuries in each "no-purchase" -LP increase-).

Another reason why GS's Paulson needed the initial $1 billion SPS issued for free, besides to reduce the Core Capital with its offset (source), he wanted to enable the following scheme of SPS LP increase, thinking of the deadline.

This deadline had an exception (3) FUNDING, that the UST and FHFA wanted to pass off as the UST Funding Commitment, when the PA was amended for a second time on December 24, 2009, just a few days before the aforementioned deadline, replacing Treasury’s $200 billion Funding Commitment with new formulaic commitments.

But this is false. The exception (3) FUNDING is related to how the UST funds the purchases it was authorized, using Public Debt, and unrelated to a funding commitment in FnF.

This subsection TERMINATION OF AUTHORITY would have compelled the UST to make a one-time investment in SPS, but Hank Paulson needed more time for the assault on the ownership of FnF through the Warrant: "shares assigned to any Person" (covenant 2.1) that never came to light, and Obama needed more time for the "Obama's programs" paid for by the FnF shareholders. Huge money still due, in the MHA programs (HAMP and HARP), estimated in $15 billion, even money that FnF advanced to the banks (mortgage servicers) under TARP, but later FnF weren't reimbursed for this cost. TARP deemed a success. Of course, after concealing that $15 billion is still due.

This $15 billion could be considered that falls squarely within the "beneficial to the Agency and the public it serves" laid out by justice Alito, commented in my prior post. So, more extortion of their resources.

Another windfall for the UST during conservatorship, like the estimated $46 billion in "legislative fees", barred in the Charter's Fee Limitation of the United States.

Good, but these windfalls must be considered in a final resolution, in the case of "as is" or takeover scenarios, where the UST will earn $0 in the bailout (cumulative dividend netted out with the interests on $153 billion due)

"GSE Agency Loan". Did the🇨🇳government pay you a visit?

The SCOTUS didn't understand that, in congressionally-chartered private corporations, the FHFA director has very limited powers, as the SCOTUS-appointed amicus representing the FHFA, professor Nielson, stated in his brief, and thus, the "for cause" removal restriction is authorized.

The second part of the SCOTUS, was correct, stressing that FnF must be rehabilitated, which, as Calabria pointed out, it has only one meaning

and judge Willett spotted as well when interpreting the conservator's Incidental Power, with: any action "within the enumerated powers"

to later focus on the "in the best interests of the Agency" part, that judge Willett missed,

attempting to mislead passing it off as "beneficial to the Agency", because it's not about monetary benefit but a benefit related to Housing Finance System revamp as we have witnessed building up through today, with the FHFA finalizing on November 22nd a Final Rule for the Catastrophic-Loss Reinsurance "supers" or commingled securities (option 3 in the 2011 UST's recommendations on ending the conservatorships in the case of Government reinsurance, otherwise option 1 or 2), with a Risk Weight of 5% and a Credit Conversion Factor of 50%.

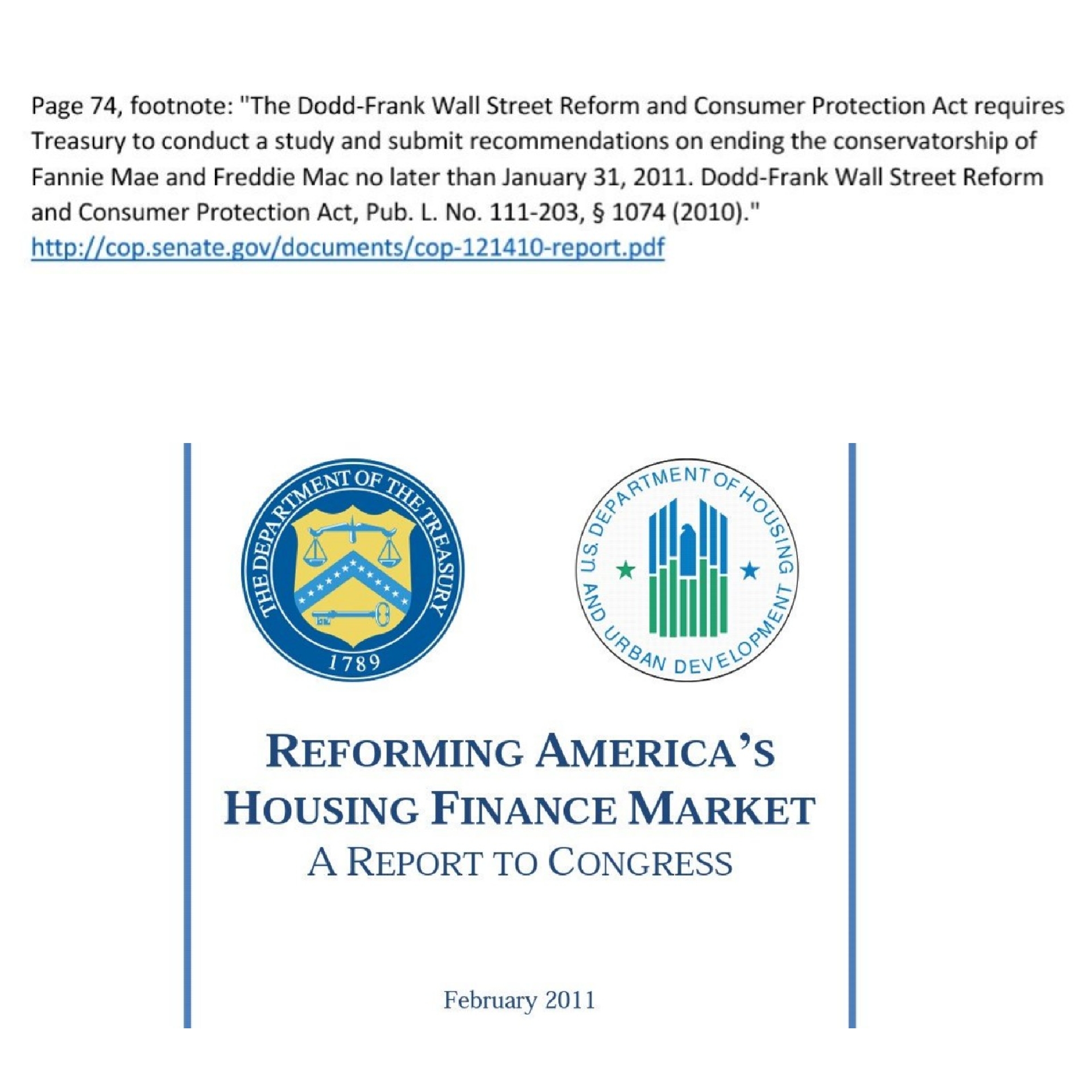

Plus other "interests", not benefits, like currently extending the Conservatorship beyond what is reasonable (upon Undercapitalized: Core Capital > Minimum Leverage Capital requirement, like in the prior mandatory release in the FHEFSSA -source- or with the resumption of dividend payments with the 3Q2022 results in Fannie Mae on year ago, as the exact moment when the FNMAS' fair value fetched its par value) with the objective to redeem the JPS when the CET1 > 2.5% of Adjusted Total Assets under the Separate Account plan -Fannie Mae as of the 3Q2023 results-, complying with Tier 1 capital > 2.5% once they are redeemed -ERCF-, in time for the announcement of release from Conservatorship and Housing Finance revamp, as per the UST's recommendations for the release from conservatorship outlined in its 2011 Report to Congress, at the request of the Dodd-Frank law of 2010.

Justice Alito, with his after-thought: "and the public it serves", simply wanted to add up more "interests of the Agency", with an authorization to sell NPL, RPL at a deep discount to capture the "debt forgiveness" string attached, and REO inventory, to special interest groups.

So, zero government policy but the sacking of FnF and the utilization of the enterprises to leverage the political negotiation between the GOP and Democrats.

This is very different from your "FHFA can do whatever the hell it wants" (source), echoing what your mentor Bill Ackman implied with: FHFA has absolute discretion (Source), in an attempt to pave the way to a negotiation outside the Rule of Law that your buddy David Stevens referred to as "old and tired". No wonder why yesterday he came up with a Govt Explicit Guarantee on MBSs and Utility Model.

David Stevens has always had problems with the law.

Conservatorship preserves their status as private shareholder-owned enterprises.

The former President and CEO at Mortgage Bankers Association (MBA): "The Rule of Law is old and tired".

The economic theory "The Age of Plunder" gains steam.

Episode: "The Trappers"

Choo Choo

#FANNIEGATE TRAPPERS

— Conservatives against Trump (@CarlosVignote) December 5, 2023

▪️DeMarco

-He barred the Securities Litigation payment ruled 12yrs later.

-Capital distr. for recap,CFR1237.12

▪️UST-litigants fell into their own trap, agreeing to decap FnF for a swap Ps→Cs. Only $118B SPS (NW),the rest wiped out, which boosts the C price. pic.twitter.com/NzIpVIMvqJ

Thank the corrupt litigants for the shareholder exodus from the ownership of FnF, plus others peddling the government theft story in formal documents and also their shills on social media.

This is why it's been requested 3 rounds of compensation for Punitive damages and one of them is against these people, because it coincides with one of the eight Securities Law violations that need to be settled with the DOJ in one of the rounds: the stock price manipulation, as the damage is, precisely, that with their government theft story, they are the necessary counterparty in court for the DOJ's "Yes, we are stealing it all", that prevented the stocks from trading at their fair value all along.

The idea that there is no proof of a Separate Account plan is ridiculous, because the proof is that it's what is set forth in the law, rules and financial concepts.

So, the fact that it's been carried out secretly thanks to the FHFA-C's Incidental Power, does not prevent any individual from learning about it, as it's publicly available information.

This way, a penalty will clear things up for those that still don't get it and it also serves as the necessary deterrence.

3X PUNITIVE DAMAGES

— Conservatives against Trump (@CarlosVignote) October 8, 2023

-8 Securities Law breaches

-Deferred Income accounting

-Law firms &Co

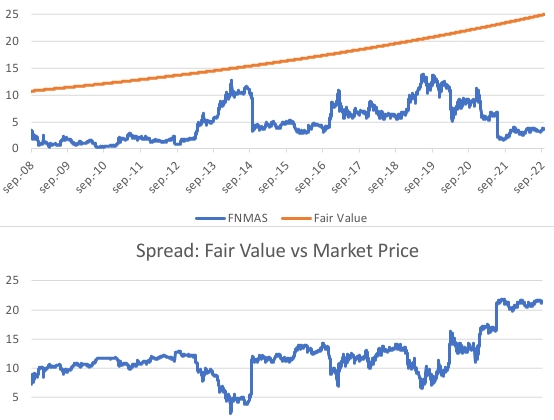

0.5% IRR on the harm for real(Avg gap FV🆚Mkt Price =half JPS) 15 years =$0.97 in a $25pv JPS (Cs=$50pv JPS)

Breakdown$FMCC $1.3B

JPS=$0.5B$FNMA $2.2B

JPS=$0.8B#Fanniegate @TheJusticeDept https://t.co/sz2YTYk8rC pic.twitter.com/cxU3v27ynd

15 years of FNMA/FMCC shareholders demise, total number of individual shareholders in 2012 - 12000, as of 2022 - 8000. A lot of shareholders already passed away. It's not about politics,it's about human's life and shareholders abuse. What a shame.

A dividend is a capital distribution, 12 U.S.Code §4502(5)(A).

And thus, restricted in the 12 U.S. Code §4614(e).

Besides, a dividend is a distribution of earnings and it can't be paid, out of an Accumulated Deficit Retained Earnings account in the Balance Sheet ($-216 billion combined), that is a picture of a company at a determined date.

So, it was NOT an actual dividend by any stretch of the imagination, but a capital distribution under the guise of dividend payment, applied towards the exceptions to this restriction: to reduce the SPS and, later on, for recap (CFR1237.12)

The FHFA-C's Incidental Power allows it to mislead and mess around in the best interests of the Agency, while upholding its Rehab Power.

Read my posts and the law before replying.

The dividend to Treasury was eliminated to all effects.

You are posting a covenant in the SPSPA stating that when there is no cash dividend, the SPS LP is increased. But this isn't the case.

First of all you should haven known that this scheme was enacted in the September 21, 2019 5th amendment of the PA ("Letter Agreement"), exactly three weeks after judge Willett ruled in the 5th Circuit court, regarding the Collins case, that the conservator exceeded its powers with the NWS dividend and thus, it compelled the FHFA and the UST to make a move.

Calabria and Mnuchin came up with what already was put in place in a prior amendment with Mel Watt, when $3 billion worth of SPS LP was handed out for free on December 31, 2017, which is missing in the Balance Sheets.

This is why they approved a brand new compensation to Treasury, set forth in a brand new covenant in the SPSPA (image posted below) that appears below the covenant that you mention and thus, it doesn't apply because it isn't a dividend.

This new compensation consists in increasing the SPS LP in the same amount as the Net Worth increase in the quarter. They later will peddle the lie of "FnF build capital" to pass it off as the "game changer" required by judge Willett implicitly when the conservator was called out.

But this slogan is a big lie when the outcome of this operation is that FnF are NOT building the regulatory capital that has to meet the capital requirements (ERCF), but capital stock SPS. In order to conceal this outcome, they simply chose to don't post these gifted SPS in the Balance Sheet, in order to not see the effect when a company issues/increases capital stock for free (without receiving the corresponding cash), which carries an offset with reduction of core capital, either Addition Paid-In Capital like occurred with the initial $1 billion SPS issued for free, or with these gifted SPS as of September 2019. This offset wipes out the regulatory capital just built.

This operation needs a regiment of shills on social media stating that FnF are retaining earnings and they "continue to build capital" (Bill Ackman in the Pershing's letters and his subordinate Bradford), along with happy emojis all the time.

Screenshot: initial SPS issued for free and their offset that reduced the Core Capital, necessary for the option (G) (manufactured) LOSSES, that justified the conservatorship, among other losses (dividend, provisions for modified loans, DTA valuation allowance).

So, you are concealing this brand new covenant in the SPSPA and instead, you post the one above that doesn't apply. I guess that you are another member of the Tipp-Ex gang, specialized in covering up laws, rules and financial concepts.

It's corroborated in the Treasury press release at the time, making clear that there is no dividend to Treasury anymore.

Why is this important? Because there is a stark difference between them. The gifted SPS in the absence of dividend, are considered a capital distribution in the FHEFSSA's definition, 12 U.S. Code §4502(5)(A):

A payment in kind with respect to "other ownership interest" (SPS) in an enterprise

Third part in the sequel to "navycmdr never learns".

Entitled: "French Hill road".

Navycmdr was told to post a bill introduced in congress in 2016 by representative French Hill, that would amend the Wall Street Reform and Consumer Protection Act of 2010 (Dodd Frank Law) in order to

force Treasury to study this issue and present its recommendations to Congress at least once a year, creating engagement on the best path forward on housing finance reform to end taxpayer exposure and ensure access to mortgage credit for Americans.”

Require Treasury to conduct a study and submit recommendations on ending the Conservatorships, no later than January 31, 2011.

Fanniegate: a story of trappers.

#FANNIEGATE TRAPPERS

— Conservatives against Trump (@CarlosVignote) December 5, 2023

▪️DeMarco

-He barred the Securities Litigation payment ruled 12yrs later.

-Capital distr. for recap,CFR1237.12

▪️UST-litigants fell into their own trap, agreeing to decap FnF for a swap Ps→Cs. Only $118B SPS (NW),the rest wiped out, which boosts the C price. pic.twitter.com/NzIpVIMvqJ

The rogue Bradford always deceiving to reap profits.

There is zero value added to the common equity and the JPS holders if the capital that has been built in the $118B Net Worth is the capital stock SPS, primarily because it isn't regulatory capital to meet the capital requirements and, secondly, it's owned by the UST, it's not our Net Worth.

Currently concealed with Financial Statement fraud: the $118B worth gifted SPS thanks to Calabria/Mnuchin and Berkowitz's attorney who signed off on it as commented below, do not appear on the balance sheet in order to not post its offset with reduction of the Retained Earnings account in the same amount (CET1). A NWS 2.0. The Common Equity (CET1) is still being syphoned off to the UST as before with the NWS dividend.

Or I should say, Common Equity held in escrow as before, in order to comply with the exceptions to the Restriction on Capital Distributions (Now: for Recap -CFR 1237.12-; Before: to reduce the SPS -U.S. Code §4614 (e)-), and in order to comply with the FHFA-C's Rehab power: Put FnF in a sound and solvent condition. And finally, it complies with the fact that no actual dividend was ever possible, with an Accumulated Deficit Retained Earnings account, as a dividend is a distribution of earnings and, first of all, this account has to be replenished.

Anyway, the total SPS outstanding stand at $312.5 billion, for just $118 billion Net Worth, just in case you still don't get who owns that Net Worth.

Talking about the controversial attorney for Berkowitz, David Thompson, who seized control of many cases to control the narrative (Bhatti, Robinson, Collins and Rop, besides Fairholme's Berkowitz case), went to 5th Cir. after the appeal in the SCOTUS with the Collins case, to claim constitutional damages, because the "for cause" removal restriction prevented the wonderland that you claim, where the UST gets rich and, at the same time, FnF are recapitalized retaining earnings, from happening sooner, with the sacking of Mel Watt before. More of the "Trump will save us" that now you and the chameleonic plaintiff Joshua Angel with more than 30 different aliases, peddle on this board 24/7.

This wonderland is a big lie and his assertion that he isn't a Securities lawyer won't exonerate him. A lie based on the Financial Statement fraud in FnF, as always happens in an elaborate conspiracy, where one statement is based on the felonies committed by other members. Later they will claim that the management and BOD of FnF aren't liable because they don't have powers during conservatorship and thus, the blame falls on the conservator FHFA and its Director, who doesn't care because it's the DOJ the one vicariously liable. That is, the taxpayer pays the bill or, as the world Socialists claim, "it's nobody's money".

Go away, rebel hippie Glen Bradford, alias LuLeVan. You don't add any value on this message board and you never learn.

The fact that FnF have since built up capital (today $120B net worth) - which also benefits commons (could reduce dilution) - is thanks to the JPS lawsuits.

I'm Bradford.

Now, I'm not Bradford.

I'm Bradford.

I'm not Bradford.

I'm Bradford.

I'm not Bradford.

If you can't even distinguish between people posting here based on style

That

"par paper at some point that’s taken years to accumulate"

Guys who own these pieces don’t care abt a few dimes

Bradford-LuLeVan, you write the same errors 2 hours after I corrected you in this post.

There is no minimum CET1 2.5% in the Leverage ratio and it's not HERA, but a capital rule pursuant to the FHEFSSA, as amended by HERA.

Also, I used 2.5% (which is the HERA minimum) instead of the 3% in the 4th Letter Agreement.

And 2.5% requirement of Adjusted Total Assets refers to Tier 1 Capital in the Capital Rule, pursuant to the FHEFSSA (not HERA)

There is no "required minimum" of CET1 for the Leverage ratio of the Capital rule as you claim.

What is important is that CET1 meets the required minimum. This minimum (FnF combined) is currently about $195 billion (= 2.5% HERA minimum of total assets).

The Net Worth is important for the stock valuation of the capital stocks. You mistake it for a Debt restructuring as I told you before, Glen Bradford, aka LuLeVan.

You don't even know that the SPS outstanding are $312 billion, not the $191 billion that you claim will be swapped for commons. You miss the $118 billion gifted SPS absent from the balance sheet that carry an offset with reduction of Retained Earnings (CET1) that you haven't adjusted in the ERCF tables, despite being told so a thousand times. Like your buddy in this conspiracy, the JPS holder navycmdr, you never learn. Also, you miss the $2 billion gifted SPS that do appear.

So, if that were the case, only $118 billion (current Net Worth) could be swapped for common stocks and, due to the "restructuring" nature of this operation, the rest of SPS would be wiped out and also all the JPS outstanding (not enough Net Worth for them). Therefore, we see that the SPS need the common stocks for their monetization and they always have some residual value as they represent a legal claim on future earnings. But the thing is that this restructuring, along with the cancellation of the Warrant that the UST got for free, would end up boosting the common stock price. So, it's like the "Treasury restructuring shop", a wannabe Moelis shop, fell into its own trap of decapitalizing FnF in collusion with the JPS holders, for the assault on the ownership of FnF (common stocks)

You don't know that the capital won't rise 1:1 with the conversion for commons, because FnF would have to pay taxes.

It's pathetic to see how sophisticated investors use you to transmit their proposal of the pillaging of FnF.

Above all, you don't understand the financial concepts of dividend (a distribution of earnings. There weren't funds available for distribution with an Accumulated Deficit Retained Earnings account), capital distribution (dividends, today's gifted SPS and today's payment of Securities Litigation judgment that has already been recorded), the mandate to put FnF in a sound and solvent condition (conservator's power), the UST backup of FnF in the Charter Act, at special rates (Hello?), etc., so you don't understand what has happened in the last 15 years, along with the fact that the law doesn't authorize stealing capital from the enterprises. Justice Alito and judge Willett simply authorized the Separate Account plan that is rehabilitating FnF on the sidelines.

The financial rehabilitation has not been satisfied with the current adjusted Balance Sheet (adjusted for the Financial Statement fraud with the gifted SPS absent from the balance sheet that you claim they are off-balance sheet operations, ignoring that it's false and, secondly, if that were the case, FnF present the results of these "off-balance sheet arrangements" on a consolidated basis in their Balance Sheets, like currently their multi-trillion-dollar MBS trusts, where mortgages and MBSs are deposited. They do appear on the balance sheet)

This isn't about how you rehabilitate FnF today, but it's been 15 years in the making, in what has been a Conservatorship.

Let alone that you don't get that the capital requirements are mandated in the FHEFSSA, not in HERA that simply inserted amendments in the FHEFSSA, as I explained on this board, but you never learn because you are here on a mission.

2.5% HERA minimum of total assets

Mnuchin-Berkowitz were seated at the court bench when the offer of conversion of JPS to Common Stocks was made, in the retailer Sears case, when they were accused of syphoning undervalued assests off to themselves, which is also the accusation that I'm posting here, about the extortion of resources out of FnF, with the sale of NPL, RPL and REO inventory to a Goldman Sachs subsidiary and others.

All the🇺🇲Officials are compelled to continue what's been already started.

Whether they want it or not. They have to build on it, which is what we are waiting for, with regard to an ultimate Housing Finance System revamp and whether there will be a Takings, takeover or as is scenario.

I don't think that you were there, but I was in the run up to the January 31, 2011 deadline by law, for the UST to come out with the Conservatorship endpoint.

I was there during the delay of 11 days.

Then, the news broke.

Geithner was criticized a lot, primarily for coming out with a plan with 3 options. Then, for envisioning a government Catastrophic-Loss Reinsurance in the option 3, at a time when FnF charged very little (28 bps guarantee fee) and they don't need to buy reinsurance in the first place. Later we saw the next years how the g-fee ticked up to today's 62 bps, though the 10 bps TCCA fee is included in the interim.

It has ended up in the Basel framework for capital standards, that took effect in February 16, 2021.

Now FnF charge fully private sector g-fees.

The frivolous lawsuits, Watt, Craig Phillips, Mnuchin, and all those peddling the Govt theft story in formal documents, are hurdles in this 12-year race.

What you are doing is stock price manipulation with Bradford86 and LuLeVan and you are clueless about financial matters, because you are mistaking the Net Worth built with SPS for regulatory capital, which is the metric that has to meet the capital requirements.

Currently $-75 billion Core Capital (stuck to $-194 billion every quarter, due to the gifted SPS, concealed with Financial Statement fraud in FnF: these gifted SPS are missing in the Balance Sheets) and it has to meet a Minimum Leverage Capital requirement of $208 billion.

Hence, an adjusted $402 billion capital shortfall in the scenario that you defend with:

You should be thankful for what he did accomplish even though it is not priced in.

It isn't Calabria's Capital Rule, but FHFA's.

I do not support Calabria's policy of keeping the GSEs small with excessive capital requirements.

Navycmdr writes a sequel: "Navycmdr never learns: $Town $Hall $Call"

The first movie was commented here.

The 2023 bill "requiring the UST to submit proposals to end the conservatorship", is an attempt to supplant the real mandate in force, pursuant to the Dodd-Frank law of 2010, "requiring the UST to submit recommendations on ending the conservatorship, no later than January 31, 2011", and subsequent UST/HUD 3-option Housing Finance System revamp, a Report to Congress 11 days after the deadline as usual, with one thing in common: Privatized System, which means Basel framework for capital requirements. Does it ring a bell? 12 years in the a making.

You are doing great!

Our negotiator slams the WSJ's Ackerman.

When talking about false rhetorics peddled by the plotters that want to keep the control over the enterprises, commented on Tuesday:

"Government implicit guarantee on MBSs"

"Wind down FnF by raising their guarantee fees"

"A NWS dividend is a typical renegotiation of obligations. Thus, within the FHFA-C's power."

"Conservatorship is being very profitable for the taxpayer"

"A rule requiring FnF to hold more capital than the $35 billion currently allowed to hold"

"The firms were taken over by the government in 2008".

"privatization".

"The ongoing support from US Treasury is necessary for their business model".

"backed by the government"

1st,Govt Implicit Gtee on MBS→Loan govt gteed→Now, loan govt backed.

— Conservatives against Trump (@CarlosVignote) November 29, 2023

Better "sponsored" if you wish, as the only "backing" is the UST backup of FnF as a last resort,purchasing SPS upon neg Net Worth(Capital Deficiency in the PA)

Pointless today under Basel framework.#Fanniegate https://t.co/RaYR6s5N0S

The CFPB is OFF-TOPIC.

It's been explained a thousand times that the FHFA oversees congressionally-chartered private corporations and thus, it has very limited powers.

For instance, this is the reason why we are requesting a refund of the CRT expenses, net (turned into Retained Earnings), without second-guessing. The CRT operations are barred in the Credit Enhancement clause of the Charter Act and its powers as conservator don't allow it to break the law at its will, creating a parallel Charter Act, with the objective to tailor good deals to crony investors and chamber investors, like JPM, BLK, BX, MS, etc. Remember their CRT symposiums attended by former MS and BLK Craig Phillips, BLK, among others? A telltale sign of a scam, later followed by the Bitcoin symposiums.

Let alone that it's barred in the Fee Limitation clause as well, in the case that it's money syphoned off to UST under the Mnuchin's slogan of "the taxpayer be appropriately compensated" or the "to protect the taxpayer" of the other Goldman Sachs alumni, Sandra Thompson, because this is also a lie: the taxpayer doesn't bear credit risk in FnF, the purchase of SPS isn't a loss to the taxpayer (UBS's Hensarling, former House representative). Not even as holder of obligations (compromise of repayment) SPS. The way that FnF are protected is, precisely, with the opposite: building capital that absorbs future (unexpected) losses, basically with their Retained Earnings accounts (CET1). Not with capital stock, by the way, which is tasked only with offsetting a negative Retained Earnings account like nowadays in the phony Balance Sheets, or in the adjusted Balance Sheet shown in my signature image below, in early conservatorship.

That's why the capital ratios, Basel framework, g-fee hikes, soundness, Table 8: Payout ratio, Restriction on Capital Distributions, etc. Does it ring a bell?

Nice going, plaintiff Joshua Angel.

Did you tell this to judge Lamberth and judge Sweeney as well?

Thanks for going through my ass to reach my brain to see what i am thinking.. It does hurt though

Wait a few days for the plaintiff Joshua Angel to post the same lies with one of his 30 different aliases (HappyAlways, EternalPatience, Fannie heyyyy, nagoya, Rodney, Barron, stvupdate, 5 bagger, etc), refuted over and over again (interest rate; HERA; 4 exceptions in the CFR 1237.12 to conceal the ones by statute U.S.Code §4614(e); refinancing option; PA, a contract; etc.)

This is the bread and butter during conservatorship with all the commissioned social media celebrities and attorneys that post here regularly.

It's time for the FBI to clamp down on this gang comprised of FHFA officials, plaintiffs and Co peddling the government theft story in formal documents ("involved in every aspect of this issue at the highest levels for 9 years", Pagliara told me in June 2017) and the DOJ and S.E.C. attorneys.

But we can't call it conspiracy nowadays. So, let's call it "Glampiracy©" that combines the words "glamour" and "conspiracy".

What has always been known as rogue people and pillaging: Piracy with glamour, so no one else notices it.

FHFA/@TheJusticeDept-PLAINTIFFS' LOSING WAR:CASE OF MISTAKEN IDENTITY

— Conservatives against Trump (@CarlosVignote) November 28, 2023

Plot to decapitalize FnF betting on a SPS/JPS' agreement:haircut/swap for Cs(Calabria's book quoting Mnuchin)

Ain't no debt restructuring.

Equity:$118B NW w/ $312B SPS→only $118B SPS. JPS,wiped out.#Fanniegate pic.twitter.com/jVYAbu97pP

Don't forget that no dividend can possible be distributed out of earnings, with Accumulated Deficit Retained Earnings accounts, in addition to the statutory restriction on capital distributions.

A dividend isn't interest payment, as you claim with your other alias, Rodney.

As always, the chameleonic plaintiff Joshua Angel with one of his more than 30 different aliases on this board and Yahoo's, writes something correctly but the objective is to post a lie at the same time, to see if it sticks:

as Wise Man has for years noted, FHFA has made a few exceptions to the prohibition on capital distributions. None of the exceptions allow dividends.

SCOTUS blessed the NWS dividend because it's authorized an infinite dividend rate on SPS and in an infinite amount, in the second UST backup of FnF inserted by HERA in the Charter Act, shamelessly just below the original one with a "rate that takes into consideration the Treasury yields as of the last day of the month preceding the purchase" (It's been considered a 0.5% spread. Weighted average 1.8% dividend rate in the 5- and 6-year investments in SPS of Freddie Mac and Fannie Mae, respectively. See my signature image for Freddie Mac), and with the same name: "Authority of Treasury to purchase obligations. Terms and conditions".

The Congress should have updated the outdated $2.25 billion limit in the original UST backup, established 60 years ago when the debt outstanding of Fannie Mae was only $15 billion, instead of enacting a second one. The advisors were more interested in replicating the provision entitled Separate Account of the FHLBanks in 1989, that saddled the taxpayer with losses (estimated $48.8 billion), where Sandra Thompson (FDIC, manager of RTC) and DeMarco (auditor at GAO) were to blame, and lie about it.

But Justice Alito started off his statement with "rehabilitate FnF", which has only one meaning that judge Willett corroborated in a prior ruling over the same case, interpreting the same Incidental Power: "Any action authorized by this section" means "within the enumerated powers", like its power of Rehabilitation of FnF: put FnF in a sound and solvent condition (Recapitalization and reduce the SPS, respectively)

Justice Alito simply authorized the use of the Incidental Power to lie about it "in the best interests of the Agency" and keep the money in escrow as part of a Separate Account, that he called "beneficial to the Agency" intentionally as he was told, to transmit an idea that isn't what is written, about monetary benefit, and aiming to back up the stock price manipulation with the hedge funds' government theft story, besides the use of FnF for the extortion of their resources "beneficial to the public", using the investment banks as conduit for public policies, like the sale of RPL at a deep discount to capture the debt forgiveness string that Trump attached. Sale of NPL and REO inventory to minority-owned businesses, women-owned businesses, LGTB associations, neighborhood associations, etc.

It has become known as "The pillaging doctrine".

Pretty much judge Willett, justice Alito and our negotiator on #Fanniegate were synchronized.

Mnuchin is a bond guy, head of the Fixed-Income Department at Goldman Sachs during many years.

Therefore, he is not an Equity guy, with knowledge in enterprise value and stock valuation. And I'm referring to pure Equity, not the JPS that are fixed-income securities, although recorded in Equity.

I doubt that he has ever seen a Balance Sheet of a company. He is more interested in the market rates, the Fed and macroeconomics in general.

Never try to explain something providing the statement from someone.

And the net worth of the Equity holders at a determined date, is the Net Worth as seen in the Balance Sheets. No more and no less. $118 billion Net Worth that belongs to the UST as holder of $312.5 billion SPS.

You are mistaking it for a Debt restructuring, where the debtholders begin to negotiate based on the face value of their securities recorded as Liability.

Who is going to explain to judge Lamberth the Separate Account plan and the fact that the corrupt litigants ate a poison pill?

FHFA's DeMarco prohibited the payment of Securities Litigation judgment 12 years before the jury's verdict (July 20, 2011 Final Rule), applying the FHEFSSA's Restriction on Capital Distributions 12 USC §4614(e),...

... at the same time that he amended the FHEFSSA's definition of capital distribution 12 USC §4502(5)(A), to include this case in the number 3...

... and adding the CFR 1237.12 that "supplements" the restriction by statute mentioned before.

What part of "JPS wiped out upon restructuring" you don't understand?

JPS cannot be diluted because they are contractually protected.

DeMarco "fooled both sides of the aisle" that wanted to be fooled.

They bought the rhetorics:

"Government implicit guarantee on MBSs"

"Wind-down FnF by raising their guarantee fees"

"A NWS dividend is a typical renegotiation of obligations. Thus, within the FHFA-C's power."

"Conservatorship is being very profitable for the taxpayer"

Etc.

In the meantime, DeMarco was enacting regulation that enables the continuation of the Separate Account plan and the poison pill of including the payment of Securities Litigation judgment in the FHEFSSA's definition of Capital Distribution (#3). This way, as an exit strategy, he made sure that at some point in the future, everybody will turn their heads toward the Restriction on Capital Distributions and their exceptions, as a Separate Account plan, and where he inserted more exceptions in the July 20, 2011 Final Rule, for the phases 2 and 3 (CFR 1237.12: capital distributions for their recapitalization outside their balance sheets), in a rule that clearly states in (c) that "it's intended to supplement" the restriction by statute, a word that transmits the idea of being a follow-on plan.

As of end of September 2023, FnF have accumulated so much capital that they are financially compelled to redeem the costly JPSs, because, afterwards, they would still meet the threshold of TIER 1 Capital > 2.5% of Adjusted Total Assets.