Friday, December 01, 2023 3:27:22 AM

I do not support Calabria's policy of keeping the GSEs small with excessive capital requirements.

It began with Mel Watt with a proposed Capital Rule in the third quarter of 2017, that was technically flawed when he included a "going-concern buffer" inside the Total capital requirement, when now the capital buffers aren't capital requirements (outside the Total capital requirement)

It isn't Calabria's because it's a Basel framework for capital requirements. An international standard for all the financial institutions and for the same risk exposure.

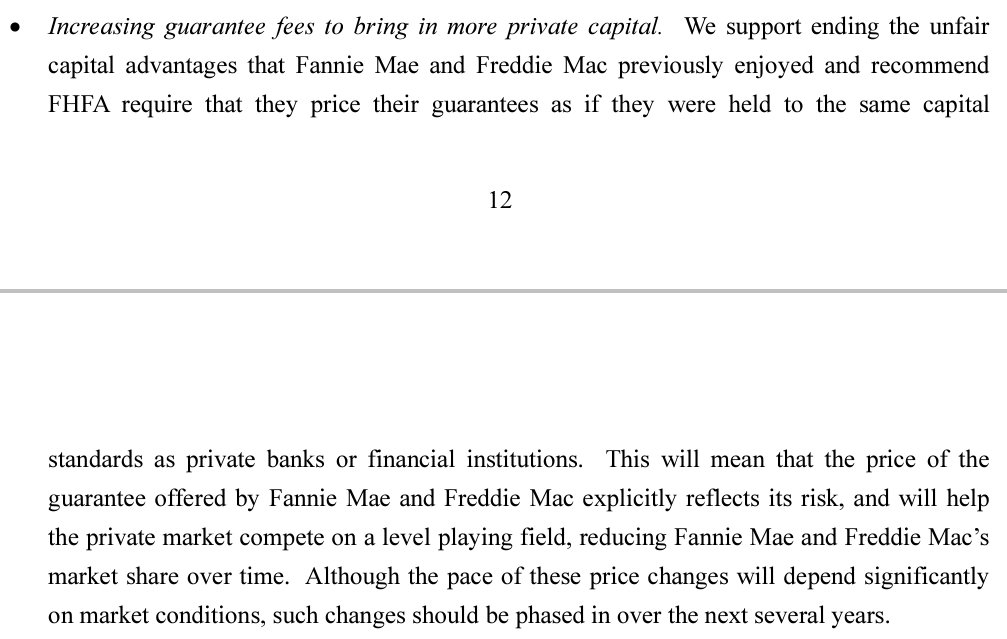

From the beginning, it's was all about removing all the privileges that FnF and, therefore, their shareholders (unless you live in Venezuela or China) enjoy in the Charter Act, criticized also by the CBO that called "subsidy cost" to the subsidized guarantee fee delivered by FnF as per the Charter Purposes, and this cost was recorded in the Federal Budget.

As seen in this screenshot of the 2011 UST's Report to Congress that will be commented next, along with the greatest privilege of all: the UST backup of FnF as a last resort, which is removed only with the Charter revoked.

But the thing is that the rogue Mel Watt, co-sponsor of the 2012 TCCA (Fees prohibited in the Charter's Fee Limitation) together with Pelosi (HERA sole sponsor. 4.2 bps on new acquisitions sent to UST/HUD, also prohibited. Many other flaws.) and Maxine Waters (her chamber investor, Tim Pagliara, made Guido recently, repeat her slogan "Federal government conservatorship"), didn't get the memo, because everything has its origin in the Dodd-Frank law of 2010, that required the Treasury to come out with "recommendations on ending the conservatorships, no later than January 31, 2011", and the UST/HUD came up with the February 2011 3-option Housing Finance System revamp, a report to Congress.

The 3 options that had one thing in common: Privatized System for Housing Finance. Hence, FnF are subject to the same capital standards as everyone else.

Watt also known for attempting to create a shadow Housing Finance System in the meantime, with the States' and Municipalities' Housing Finance Agencies (HFAs) turned into guarantors and using Freddie Mac to securitize their products. So, Watt had a different agenda.

BOTTOM LINE

Called "back-end Capital Rule" because we see that it's been announced close to the end of the typical Transition Period to build capital, bound for the endpoint of Charter revoked scenario, where the UST backup of FnF is pointless under the Basel framework and culminates with the objective of FnF competing on a level playing field.

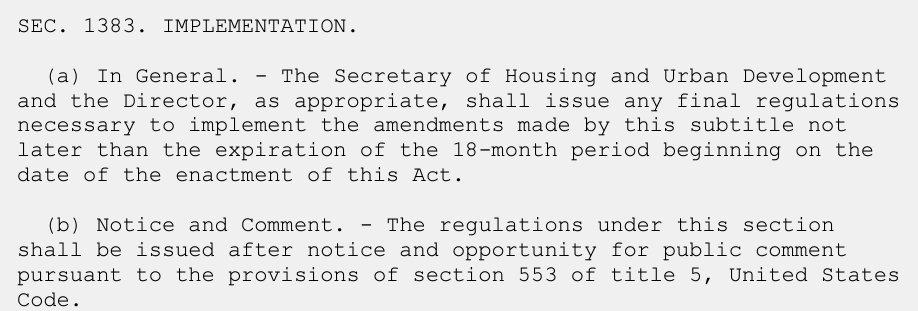

The fact that Calabria, who helped to draft HERA, didn't specify the typical 18-month time frame given to an Agency when a law demands a new capital rule or changes. For instance, in the very 1992 FHEFSSA in question, that established capital ratios for the first time in FnF. So, Calabria "forgot" to include this subsection "IMPLEMENTATION":

The more obscurantism, the more evidence of a Separate Account planned from the onset. Or the opposite, with DeMarco writing extensively about the case of payment of Securities Litigation judgments in the July 2011 Final Rule, when it's supposed that it was a normal conservatorship and when there was no litigation at the time. But he felt the need to write about it as an exit strategy, evidence that he had in mind the 2nd phase with the NWS dividend, for which he needed another exception to apply the phony dividends towards (CFR 1237.12, exceptions 1, 2, 3, 4: capital distributions that deplete capital, for their recapitalization outside their balance sheets). Exit strategy also known as a poison pill for rogue litigants that fell into DeMarco's trap. DeMarco, now known as "the trapper", when he amended the definition of capital distribution to include this case and prohibiting the payment of the claim outlined in the jury's verdict 12 years later, and thus, exposing the other cases of capital distributions restricted, with the dividend payments and SPS increased for free.

HERA struck the provision in the FHEFSSA with the formulaic of Risk-Based Capital requirement, a required a new one from scratch without the aforementioned time frame.

It also authorized the director to revise the percentages of the Minimum (Leverage) capital requirement, that remain in force in the meantime, as seen quarterly posted since day one in their earnings reports.

It also authorized it to add new capital metrics: CET1, Tier 1 capital and AT1 capital.

The Critical Capital level remains as is but, surprisingly, the FHFA has concealed it in the ERCF without authority in the law.

The concept of "back-end capital rule" is important because the existing shareholder is entitled to the full Privatized System scenario envisioned in 2011, in an acquisition by bigger players or release as is, and where the stock valuation captures the full earnings power (adjusted EPS calculated without legislative fees)

Only in a Takings, with the adjusted Common Equity, we wouldn't capture it.

Duane Forrester Joins INDEXR as SVP of Search • MONI • Jul 31, 2024 11:46 AM

Lingerie Fighting Championships Help Fulfill Death-Bed Promise With First Major Motion Picture • BOTY • Jul 31, 2024 9:00 AM

Kona Gold Beverage Significantly Reduces Debt from Multiple Holders • KGKG • Jul 31, 2024 9:00 AM

Avant Technologies Opens Equity Line with GHS Investments as Company Explores Expansion into Additional Technologies • AVAI • Jul 30, 2024 8:00 AM

ELEMENT79 GOLD CORP PROVIDES UPDATE ON CHACHAS COMMUNITY CHARTER AND REVENUE GENERATION, M&A ACTIVITIES • ELMGF • Jul 30, 2024 8:00 AM

INDEXR AI Merges With Moon Equity Holdings Corp. (MONI), Creating a Leading-edge Technology Company • MONI • Jul 29, 2024 9:59 AM