News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

That was debunked a thousand times.

the Gse’s took $40 billion in toxic MBS on their books at the direction of hank Paulson.

your posts are way too long. Please try to be more concise

I've posted (G) LOSSES. Can't you read?

neither entity met any of the twelve conditions for conservatorship

You are publishing lies!

The placement in Conservatorship is the only lawful action.

With (G) LOSSES, like to incur (fabricated) losses that deplete their capital. Already commented which ones.

And about the arrangements, all forms part of a SEPARATE ACCOUNT like the FHLBanks in their 1989 bailout by Congress, with assessments sent to a separate account,

.jpeg)

Without realizing that, the FHLBanks had to pay $300 million in interests annually (a 10% rate on a $30B obligation, applying a 0.299% spread over Treasuries. GAO report. It was precisely, Sandra Thompson, who tapped the maximum amount authorized in the law, $30B, just when she arrived at the FDIC in 1990. Not a prudent course. And DeMarco in charge of accounting at GAO, requiring in the report to expel the independent accountant PwC, in order to save recourses. We later knew why: they were just reducing the 40-year interest payments from Funding Corp, where the FHLBanks were Equity holders, that only paid interests, without realizing that their SEPARATE ACCOUNT was for the REDUCTION OF THE PRINCIPAL of the obligation, not just those interests. Then, ST and DeMarco (GAO, UST, FHFA) needed funds to repay the principal. Thank goodness Silicon Valley Bank came across and ST happens to be the FHFA director, authorizing massive leverage in SVB with the advances -loans- from a FHLBank, disregarding the liquidity risk and with an AOCI opt-out election -unrealized losses in Equity- through FDIC regulation. They chose Held-To-Maturity portfolio instead, to evade recording their unrealized losses. Famous Trump's deregulation rhetoric, by removing the safeguards), the rest (on paper) reduces the principal of the RefCorp obligation (initially, a 40-year obligation), but with FnF, the dividend payments are restricted in a provision covered up by all the crooked litigants and the peddlers of the government theft story (the coverup of a material fact is a felony of Making False Statements.)

Therefore, with FnF, the entire assessment was used to repay the principal of the SPS obligation (obligation in respect of Capital Stock), knowing that later on, it will be assessed the true cumulative dividend on SPS the UST is entitled to: like the FHLBanks, it was established a spread over Treasuries, as set forth in the original UST backup of FnF in the Charter Act:

Taking into consideration the Treasury yield as of the end of the month preceding the purchase.

Any FHLBank with a net loss for a quarter, is not required to pay the RefCorp assessment for that quarter.

A layman making a comparison: Net Worth 2008-2023.

Notwithstanding that today's Balance Sheet (once the S.E.C. fixes their Financial Statement fraud with the $125B worth of SPS LP increased for free as of December 2017, and its offset with reduction of Retained Earnings account, absent from their Balance Sheets), is comprised of:

- $316B SPS LP outstanding.

- $-216B Accumulated Deficit Retained Earnings accounts, and account that absorbs the future (unexpected) losses, which is what the Capital ratios are for (Retained Earnings is Core Capital). So much for "rehabilitation".

Capital Stocks DO NOT absorb losses (reduction). They just offset a negative Retained Earnings account, so the Net Worth remains with positive balance.

Regarding their Net Worth, today's $125B NW has been built with the $125B SPS LP increased for free since December 2017, absent from the Balance Sheet. Thefore, out of $125B Net Worth, $0 corresponds to the Common Stocks and $0 corresponds to the JPS.

Your comparison of Net Worth 2008-2023 is another plan of deception, in order to conceal the reality of Fanniegate, with your boss Tim Pagliara involved for sure:

I have been involved in every aspect of this issue at the highest levels for 9 years. Source

With respect to capitalization, I am not a regulatory lawyer. I am a litigator....That's being watched by a number of sophisticated lawyers...

The ongoing Common Equity Sweep not only is seen in the Income Statement posted yesterday.

Net Income

Less the amount of SPS LP increased for free (10% and NWS dividends on SPS before)

= Net Income Attributable to common shareholders

Thus, close to $0 EPS every quarter.

It's also seen in the other Financial Statement, the Balance Sheet, if it wasn't because it's missing both the $125B SPS LP increased for free, and its offset with $125B reduction of Retained Earnings account (Financial Statement fraud).

Fannie Mae: There is always $121B SPS LP, when the real SPS LP oustanding as of December 31, 2023, including the one scheduled to be increased on March 31 that must show up as well, is $199B.

Freddie Mac: The SPS LP stuck at $73B every quarter, when the real SPS LP outanding, including the one scheduled to be increased on March 31, is $120B.

As we can see in the Adjusted Net Worth activity table:

Another capital distribution, restricted, we consider that this Common Equity is held in escrow, in compliance with the exception "for Recap" in the Restriction on Capital Distributions (CFR 1237.12) and also with the FHFA-C's Rehab power: Put FnF in a sound and solvent condition, related to Capital levels.

Because this payment existed and we are just legalizing. Carry out thanks to the FHFA-C's Incidental Power (Any action authorized by this section, in the best interests of FnF or the Agency): 3rd phase: "Just joking. Zing!"

This is what the FHFA is interested in.

Sandra Thompson continues to peddle the lie about capital requirements met with "$125B Capital Reserve" (amount of Net Worth above the Capital Stock) that she sees on the Balance Sheet, in her written testimony in Congress last week. Enough reason to fire her for cause, because the FHEFSSA and her own ERCF state otherwise (they are met either with Core Capital, Total Capital, CET1 or Tier 1 Capital)

By the way, once adjusted for the Financial Statement fraud mentioned, the Capital Reserve =$0 (All the Net Worth is SPS)

The FHFA Director doesn't have authority to break the Charter Act with the CRT operations.

Let alone to set up a parallel Housing Finance System with them, called "GSE Reform".

CRT is only authorized the UST with its portion (Capital Magnet Fund) of the 4.2 bps allocated to two Affordable Housing Funds managed by HUD and the UST. Source.

The CRT is a normal bond used as an excuse to make FnF pay interests, that began with a steep 5% - 6% rate, which looked like the fraud in early conservatorship with their 30-year zero coupon callable MTNs, where FnF paid an outstanding rate when they were redeemed soon after being issued.

Now, they include arrangements in these back-end CRT "Bonds" (after FnF had carried out foreclosure prevention actions to bail out these CRT investors), and thus, it serves at the will of a random FHFA director whether he requires the payment of claims or not (Utility Model).

On the other hand, the PMI required to borrowers with LTV >80%, and today's Commingled Securities (Catastrophic-Loss Reinsurance or resecuritizations) 100% insured by other guarantors against default, are authorized CRT operations (number 1 and number 3 in the clause Credit Enhancement of the Charte Act, respectively)

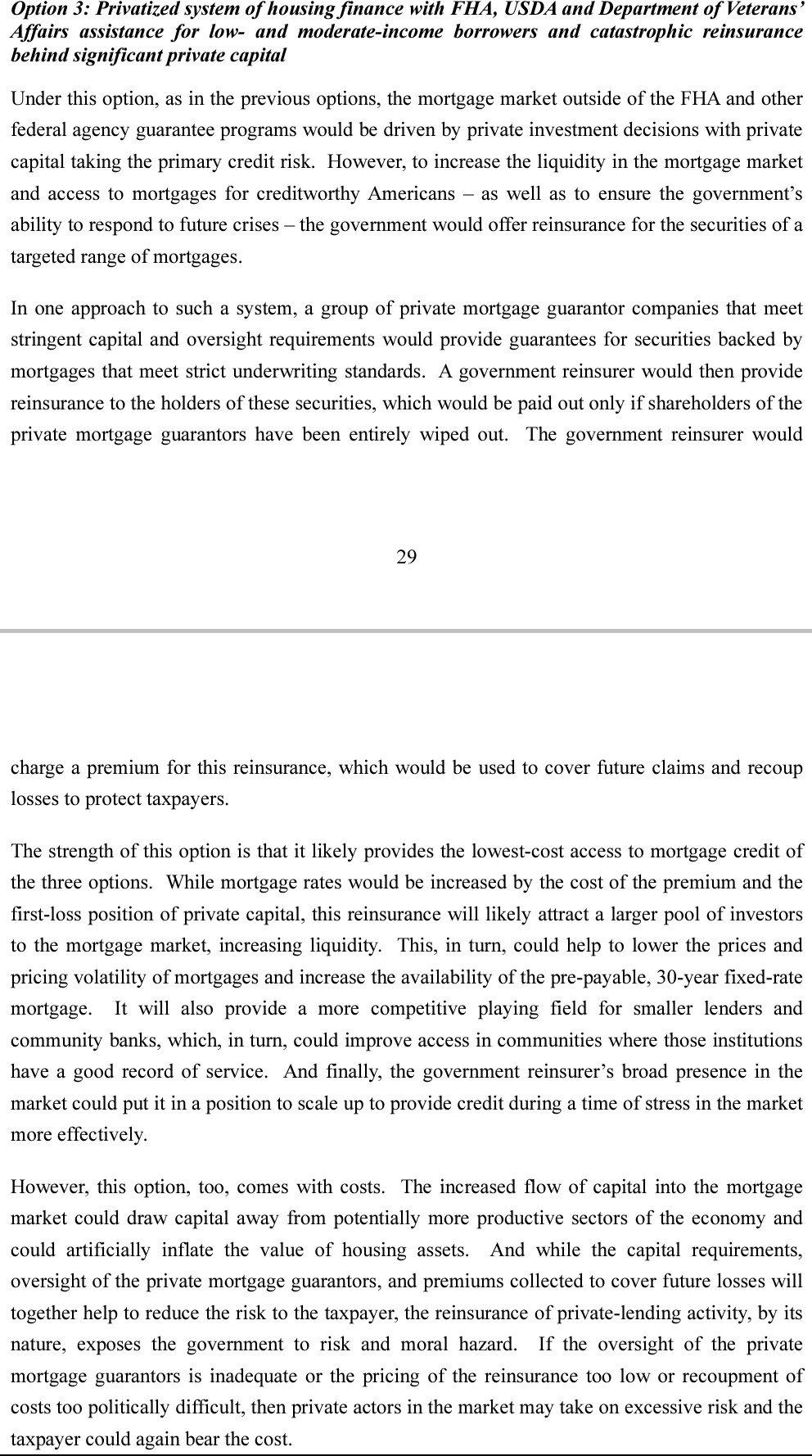

It's precisely, the Commingled Securites or Catastrophic-Loss Reinsurance, a new product for the 3-option Privatized Housing Finance System revamp, chosen by the UST in 2011 for the release from conservatorship, at the request of the Dodd-Frank law, because the option 3 is a Government Catastrophic-Loss Reinsurance and this product enables it:

This product can be used for a private Catastrophic-Loss Reinsurance as well, and then, we would be in the option 1 or 2.

It wasn't created to make FnF reinsure each other's UMBSs. Currently a pilot program, but, at some point, it has to be announced one of the 3 options.

This product was unveiled by Freddie Mac in June 2022 (Source. Notice how it's written that it began with a price of 50 bps. One week later, the FHFA changed it for 9.375 bps to better reflect the 2011 UST plan we are bound for, and not the ill-conceived Mnuchin's 2019 Plan with a Government Explicit Guarantee on MBSs)

It isn't the same a MBS with Govt Catastrophic-Loss Reinsurance and a MBS with Govt Explicit Gtee. In the first one, the credit risk is covered by private guarantors. It's activated once it files for bankruptcy.

Today, the MBS is guaranteed by FnF and there is only a cheap UST backup of FnF upon negative Net Worth. That's it. The "MBS with a Govt Implicit Gtee" is an attempt to conceal the reality of a UST backup of FnF.

The FHFA has a tendency to deviate from the normal course and it corrects itself, or, sometimes, it needs help.

The PLMBS was a product not authorized in this clause (Unlawful. Lack of credit enhancement operation) and it was one of the reasons for the conservatorships.

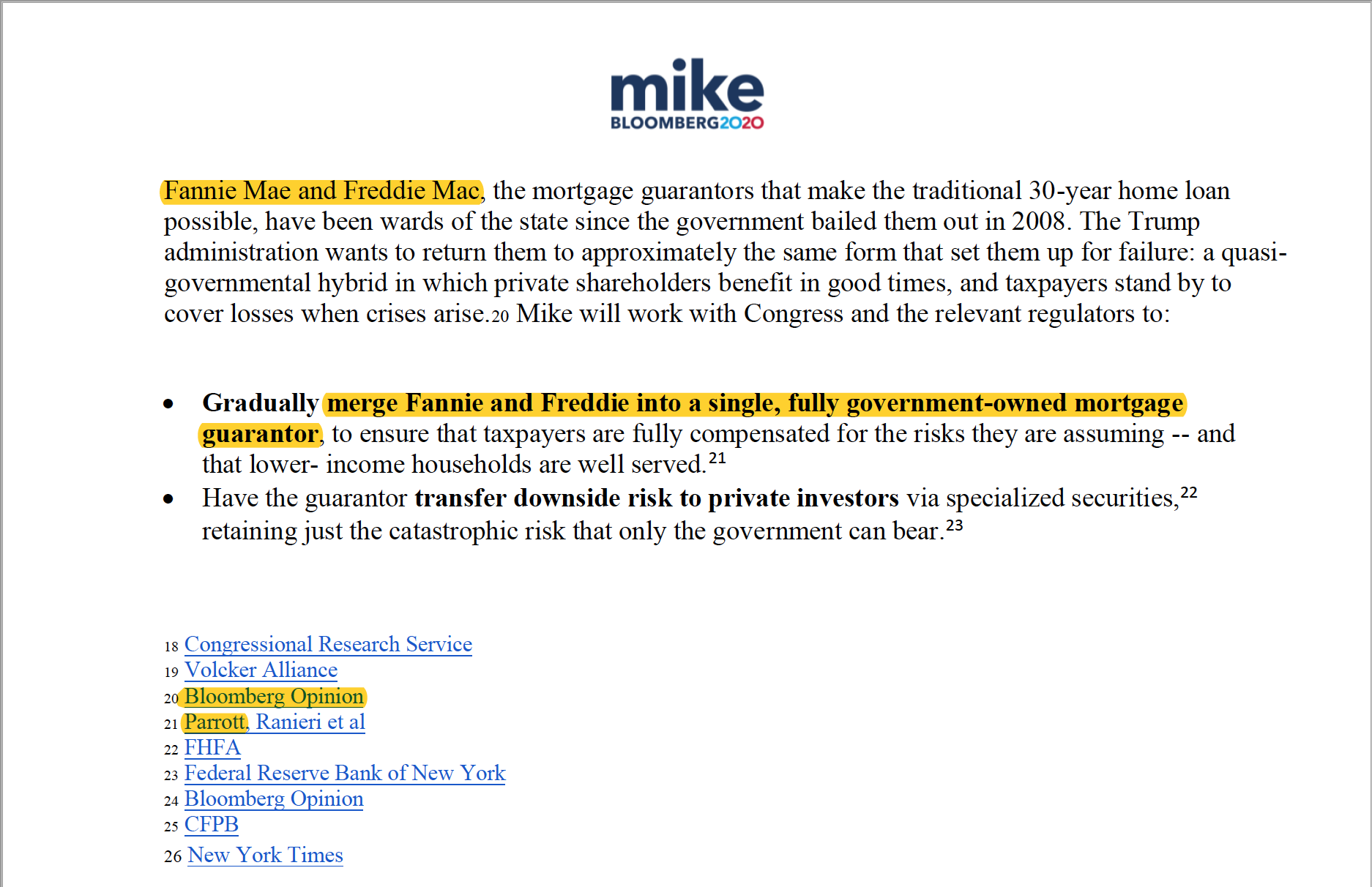

This time, the rogue FHFA can't be authorized to break the law again at its will, regardless that JPM, the Mnuchin Treasury Department and Mike Bloomberg (included in his electoral manifesto posted yesterday) love the CRTs. Barred in FnF.

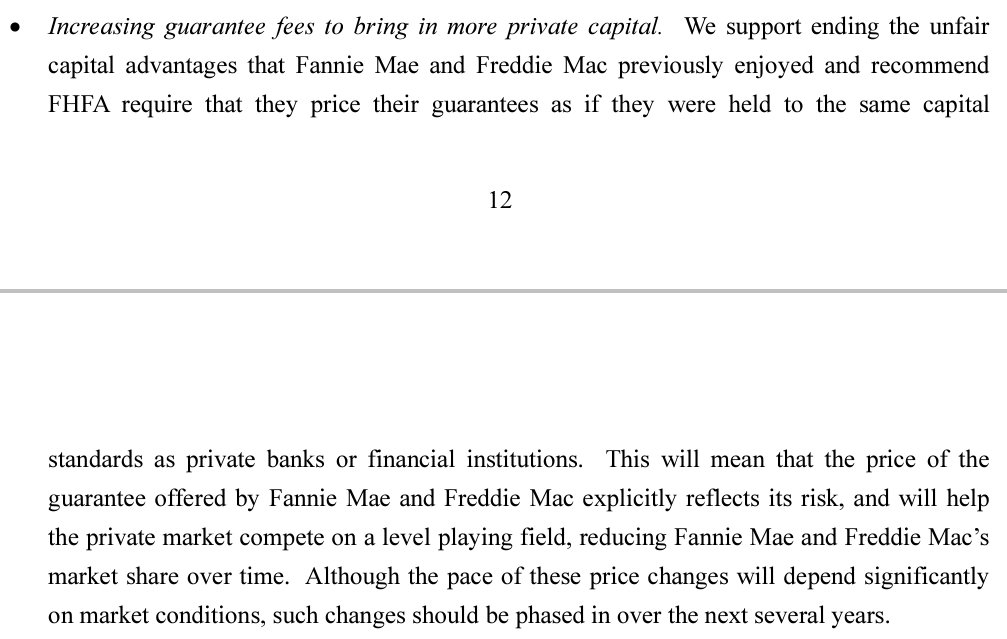

The grounds for a Housing Finance System revamp ("GSE Reform") was initiated by FHFA's DeMarco, in light of the 2011 UST plan for the release, that included g-fee hikes, Basel framework for capital requirements: "capital standards that cover the risk as if it was held by the banks" (Mel Watt attempted to deviate from this course in his proposed Capital Rule, and he was corrected by Calabria),...., that would end up with the removal of the most privilege of all: the Charter's UST backup of FnF (Charter revoked).

ST TRIES TO OVERSHADOW DEMARCO AS MASTERMIND OF REFORM

— Conservatives against Trump (@CarlosVignote) April 25, 2024

In her written testimony.

DeMarco(written testimony, May 2011)unveiled the preps of a Privatized Housing Finance Sys revamp, chosen for the release by the UST in a Report to Congress 3 mths earlier: g-fee hikes,...#Fanniegate https://t.co/mgjrPMllgX pic.twitter.com/TDKYNXTug4

Only Bloomberg, involved in Fanniegate.

Mike Bloomberg's campaign: Nationalization, CRTs,... Coincidence?

Analysts Expect FNMA To Report At least 0.60 EPS Next Week…

First, Barron is another alias of the rogue plaintiff Mr.Pro Se, among his 30+ different aliases he uses regularly on this board. Just so you know.

We don't need hedge fund managers turned into Shareholders' Rights advocates, and even the attorney Hamish Hume hiring a famous Human Rights activist, Rebecca Musarra (Source. At the same time President Biden was being portrayed on the media as a tyrant. Coincidence?), defending our property rights because they remain intact during a conservatorship.

Among the property rights, the legal ownership is embedded into a stock, and we have always had the right to dispose of our shares, that are kept in our broker accounts under custody.

Other rights that emanate from this ownership, like the Voting Right, right to scour the books, etc., were transferred to the conservator momentarily, so that it helps it fulfill its mandate, otherwise two-third shareholder vote would still be necessary and we would have opposed to every action, for the sake of saying no.

Therefore, our rights weren't "eliminated" as the hedge funds claim in court. They were transferred to the conservator. They are still there and, at some point, they will be returned.

And a point in time is related to the soundness and solvency of FnF "Put FnF in a sound and solvent condition", that is, their capital levels, which is how it's measured. This is why the prior FHEFSSA established MANDATORY release upon declared Undercapitalized: Core Capital > minimum (Leverage) capital requirement. Struck by Calabria's HERA but it's still a useful threshold to ponder.

What has happened is that, before, the minimum Leverage capital requirement was calculated with 0.45% of the off-balance sheet obligations (MBS Trusts. Financial statements consolidated on the balance sheets), and now, it's 2.5%. Notice the difference?

A Basel framework for capital requirement pursuant to the UST's recommendations on ending the conservatorships. A 3-option Privatized Housing Finance System revamp, with the goal to remove their privileges in capital standards as a result of a subsidized guarantee-fee, and the UST backup of FnF attached: Finance their operations as a last resort (upon negative Net Worth), after FnF had tapped the private capital markets before ((2) in the Public Mission: "respond appropriately to the private capital markets". What FnF did during 2006-2008 with issuances of Cs and JPS), otherwise their Public Mission can't be carried out (high credit risk and not properly compensated).

The crooked litigants with their frivolous lawsuits, have had the mission to deprive FnF of the possibility to rebuild their capital. First, agreeing with a 10% dividend during conservatorship and pretending that FnF are mutual funds, so they simply ask for SPS "repaid" and with the SPS overpayment, a $29B cash refund. $0 Core Capital recovered as a result.

They haven't challenged the SPS LP increased for free, so that now, they stage a necessary haircut in the amount of this gifted SPS, and attach it to a haircut on the JPS too, as required by Mnuchin for the JPS of his buddy Berkowitz (holding several series of JPS that nowadays no one knows where they are, and no one cares. All lies.) and Co, according to Calabria in his book.

The last option, they ask for debt forgiveness (Argentina/IMF- style), which is pathetic and it's struck down right away, after agreeing with the government that everything is authorized, forgetting the second leg regarding that it forms part of a Separate Account plan that rehabilitates FnF (the "authorized by this section" in the FHFA-C's Incidental Power), as required by Justice Alito and judge Willett (financial rehabiltation is related to capital levels: SOUNDNESS. Not with a $125B Net Worth built with the $125B SPS LP absent from the balance sheets, but with the $426B common equity generated by FnF and held in escrow in accordance with the law).

Finally, the courts have no say on the conservatorship of FnF, so going to court is pointless. Besides, it can be considered unlawful for the fact that to become Director of the FHFA and thus, conservator nowadays, it's required by law to have a deep understanding of mortgage finance and financial matters, which isn't the case in a judge, let alone the jurors.

(f)Limitation on court action

Except as provided in this section or at the request of the Director, no court may take any action to restrain or affect the exercise of powers or functions of the Agency as a conservator.

"Bad faith and unfair dealing when the Regulator......"

It's a Conservator to begin with. Wake up, bro.

You still don't understand that the CONSERVATOR's Incidental Power allows it to pay down the SPS and recapitalize FnF in a Separate Account and lie about it (your "bad faith and unfair dealing"). This is why the Separate Account plan is both authorized and lawful, and we can't claim the payment of Punitive Damages for it (although it has needed 7 Securites Law violations that aren't authorized, obviously, that need to be settled. One of them is stock price manipulation, precisely, for this Separate Acct plan), because it's:

any action authorized by this section, in the best interests of FnF or the Agency

It represents the amount of future Net Income that will need to be realized before remittances to the Treasury resume.

Any attempt to ask for debt forgiveness (SPS, canceled) will be defused.

FnF are NOT a third world country.

Yeah! FnF are doing great! Like 🇦🇷 w/ the IMF, right?

— Conservatives against Trump (@CarlosVignote) April 24, 2024

Then,debt forgiveness(FnF/🇦🇷)

Adj $402B C.C. shortfall over Min Leverage C.requirement.

$426B Common Equity held in escrow in accordance w/ the law/rules/Finance.

"Judge for yourself what that means."

No, you first.#Fanniegate https://t.co/S39QTqSKi9

"GSE Act" is how FnF call the FHEFSSA of 1992 in their Earnings reports, deviating from the original name cut short for "FHE Act" that appears in formal documents, like in the SPSPA:

It isn't just an attempt to undermine the existence of the FHEFSSA, with all the definitions capital-related, and to conceal the fact that FnF have a congressional Charter (The Charter Act), blending both names into GSE Act, already pointed out.

It's worth highlighting that they also target the fact that FnF are private corporations, and instead, they follow the mantra initiated by Mnuchin, of emphasizing that FnF are Government Sponsored Enterprises (GSEs) when talking about FnF, pretending that this concept prevents the notion that FnF are private shareholder-owned enterprises and public companies (publicly traded stocks that represent an aliquot portion of the ownership of FnF), along with the other mantra: "Cash Equity", all of a sudden, they turn the FHFA into HUD, and FnF turned into the FHA's MMIF.

In sum, they conceal that FnF are congressionally-chartered private corporations.

There is nothing wrong with the name GSEs, if it isn't an attempt to conceal that it's a name deviated from the original government-sponsored private corporation, that we can see in the 1968 Act with the privatization of Fannie Mae, where Ginnie Mae was spun off, taking the special assistance functions with it.

Finally, if someone watched the Senate hearing of last week, he hardly would have noticed that FnF are still in Conservatorship (Conservatorship occurs only in your imagination) and then, shocked after realizing that there isn't the required autonomy of the FHFA from FnF, 15 years on.

A lot going on with a simple: "GSE Act".

They want to deprive everything of its value or meaning: unbacked tokens, etc.

The case against the crooked litigants and other peddlers of the government theft story using formal documents, publicly available, is clear.

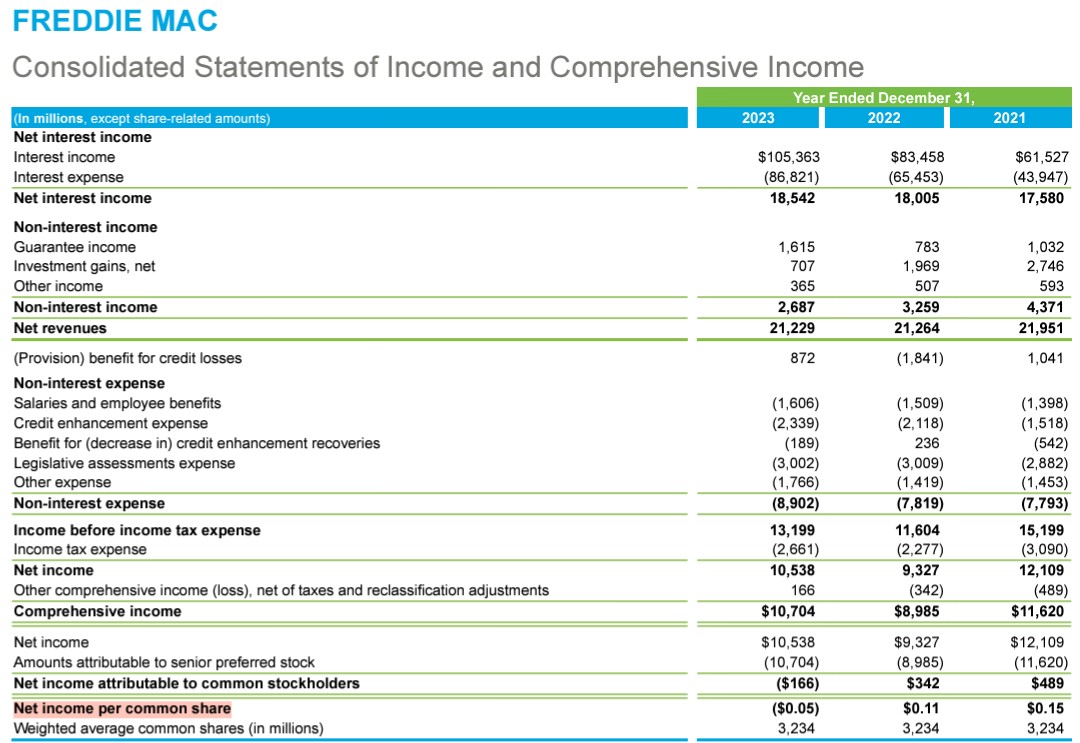

It began with "SPS, repaid" and with the overpayment, a "cash refund", thinking that FnF are Mutual Funds, like the FHA's MMIF, disregarding that, if FnF reduced the SPS and more, under the guise of dividend payments, it prevented them from recording the Retained Earnings as Core Capital in the first place (double entry accounting Cash-RE), and then, the SPS are reduced with simple cash. Watch the chart of Freddie Mac in my signature image, to see how it played out (This is fixed with the way the adjusted Common Equity as of end of 2023 was assessed, for the BVPS).

It has ended up asking for debt forgiveness (SPS canceled), like Argentina and the IMF nowadays, both begging for an authorization by the UST to cancel the debt.

IMF: "Argentina is doing great!". Yeah...great, with the IMF interest payments of April in arrears.

All of the above can't be part of the complaint and remedies sought by a serious lawyer. This is the reason why the attorney for Berkwitz and other 4 cases he seized control of, expelling the original lawyers to control the narrative and school the judges against us, David Thompson, said that he is an unsophisticated lawyer in financial and Capital Adequacy matters (watch the tweet cited below that includes an audio recording, during a Conference Call hosted by Pagliara), in an attempt to be exempt from crippling liabilities: stock price manipulation, abuse of court process and Making False Statements.

He also has formally asked in the U.S. courts for a swap SPS for Common Stocks, at the same time that Mnuchin required the same terms for the JPS, despite that the JPS would be wiped out with the current $125B Net Worth and $310B SPS LP outstanding, according to Calabria in his book, so we don't have documentary evidence of this government proposal to bail out the JPS holders and the assault on the ownership by the holders of preferred stocks (After a haircut, a swap at a rigged price automatically makes them whole on day one when the price rises).

This is called "playing the fool", because the Separate Account plan is what legalizes every action, in other words, it's set forth in the law, rules and basic finance, that all of them are being shamelessly covered up or deprived of their meaning, on daily basis. Therefore, we don't need Treasury documents corroborating it. A Separate Account was already carried out for the FHLBanks in 1989 through legislation (Section: Separate Account for the repayment of principal of the Refcorp obligation). We also see the intention to carry it out with the FHFA Final Rule of July 20, 2011, expressly writing that it's a follow-on plan ("the supplemental") in the CFR 1237.12, that authorizes "a capital distribution (deplete capital) for their recapitalization (build capital)", in a separate account, obviously (outside their Balance Sheets), suitable for the moment the SPS LP had been fully paid down with the exception to the Restriction on Capital Distributions by statute:

(c) It supplements and shall not replace or affect any other restriction on capital distributions by statute.

If Ds claim they confiscated💵and judges agree,Ps can't claim the same.

— Conservatives against Trump (@CarlosVignote) April 23, 2024

Flawed complaint &remedies:

-SPS repaid

-$29B cash refund

-Swap SPS/JPS(Mnuchin)for Cs.

0️⃣C.C.recovered(Adj $402B shortfall over Min L.requiremnt)

-SPS canceled? For a 3rd🌎country.0️⃣chance in FnF.#Fanniegate https://t.co/MZtgDZ1hTg pic.twitter.com/rpSv9P2aij

That's related to a LIBOR settlement approved in 2020. Hello?

The LIBOR case comprises several litigation alleging the existence of an international conspiracy, better known as "The Allies".

Your are talking about the brief filed yesterday by one plaintiff of those awarded a settlement, the Exchange-based Plaintiffs that transacted in LIBOR-based Eurodollar futures or options on exchanges, and regarding a dispute with his lawyer.

https://www.usdliboreurodollarsettlements.com/

As far as I know, FnF are in a different group of plaintiffs: The OTC Plaintiffs, basically those that used swaps for hedging interest rates.

There is also a Class Action for those with investments Libor-based.

You want to pass it off as a settlement with FnF using multiple aliases, "Hi Ron!", because you've been ordered to post court news no matter what.

You even post the estimation of calendar for the release of the first quarter of 2024 Earnings report wrong, because all the financial websites I checked out, provide an estimation of April 30th. At least, tell us your source.

Although we have to wait for the official announcement of the scheduled release by the managements a few days earlier.

Looks like Libor settlement will be announced in conjunction with earnings May 5-6, 2024.

By the way, Hamish, as part of a Takings case, not as part of the Separate Account plan (SPS LP increased for free is the Phase 3) in accordance with the law.

Another one crying out loud: "We've been robbed!"

Fanniegate will be an "inverse settlement" case with all the frivolous litigation.

The litigants and company will have to pay Punitive Damages to the Equity holders, accused of stock price manipulation, abuse of court process and Making False Statements for the cover-up of many statutory provisions and rules, like the Restriction on Capital Distributions, besides financial concepts.

There is a 6-box checklist for scrutiny of the plotters and to levy a penalty for punitive damages.

Although the checklist is extended to 9 boxes to see the extent of their involvement in the Fanniegate scandal.

It was posted here.

It's you who defends the SPS LP increased for free along with the rest of plaintiffs and other plotters (Ackman, Berkowitz, etc.), because you haven't brought it up to court in your lawsuit.

Only the attorney Hamish Hume just a few months ago in the Wazee case and with a 3rd amended complaint. But he is covering it up in the Lamberth court where he is a party too, because it would blast his case and the claim of damages of one-day share price drop on the 3rd amendment-day, as it is the same Common Equity Sweep as before with the NWS dividend, and also, it blasts the Class Action altogether, as it wouldn't put an end to the controversy as a prerequisite to authorize Class Actions.

We even have the case of the attorney for Berkowitz, the almighty and omnipresent David Thompson, who even claims in court in the Rop case that with the SPS LP increased for free, it has achieved a Wonderland scenario based on the Financial Statement fraud in FnF (these gifted SPS LP and its offset, reduction of Retained Earnings account, are absent from the Balance Sheets), where the UST gets rich with gifted SPS and, at the same time, FnF are recapitalized, and thus, he requested constitutional damages, arguing that the "for cause" removal restriction prevented this scenario from happening sooner, sacking Mel Watt before.

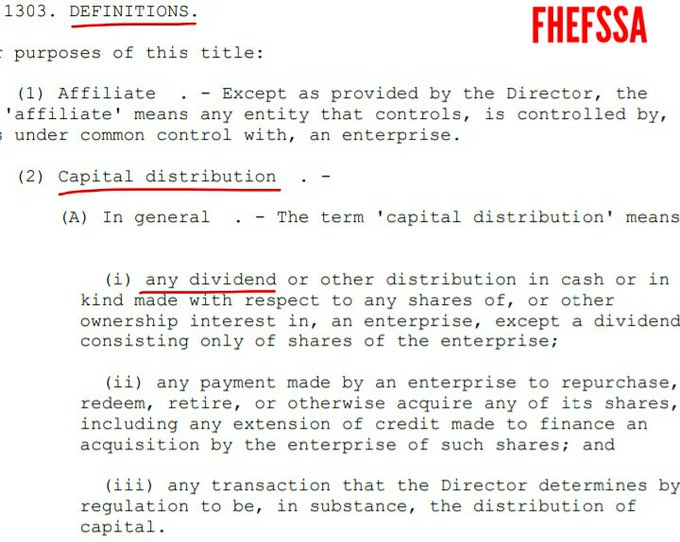

On the other hand, the Separate Account plan, that states that the SPS LP increased for free as compensation to the UST in the absence of dividend payments, is a capital distribution (Definition number 1: 12 U.S.Code §4502(5)(A)) restricted (U.S.Code §4614(e)), and therefore, it's applied towards the exception to the restriction in order to legalize it.

In this case, the exception added to the one the statute posted before, enacted in a July 20, 2011 Final Rule "for the transparency of the conservatorships", and also with the objective to uphold the FHFA-C's "PUT FnF IN A SOUND CONDITION" power: recapitalization in a separate account (12 CFR 1237.12, in either of the 4 exceptions, because it supplements and shall not replace or affect the restriction by statute posted before, that also means recapitalization at the same time the SPS LP is reduced, with assessments sent to UST under the guise of dividend payments, as they are restricted too -Number 1 in the definition of capital distribution-, besides unavailable Earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts.)

Therefore, the way to comply with the law is simply: the Common Equity is held in escrow, pending unwinding the operations. Other theme is that it's unnecessary to do it in the Balance Sheet if the operations haven't been recorded in the first place.

We can see how it's held in escrow in this image:

Actions have consequences and now, no one can pretend that it didn't happen: It needs a settlement of this Securities Law violation (7 in total during conservatorship: SPS LP increased instead of issued, to skip the December 2009 deadline on purchases by UST of high yield SPS, etc.), that the S.E.C. is aware of:

S.E.C. complaint 15976-876-848 submitted on August 2020.

Important clarification: the charge on the Income Statement that makes FnF post $0 EPS every quarter, is correct.

Finally, it gets better. The Lamberth rebate is another capital distribution and thus, restricted, included in the definition of capital distribution in an amendment inserted by the FHFA Final Rule of July 20, 2011, thanks to an express grant of authority to do it in the FHEFSSA posted above (Definition number 3: CFR 1229.13)

The Liquidation Preference continues to increase. And this is okay?

There are always capital requirements. The thresholds are statutory.

Not binding, but FnF have to build capital retaining earnings (Core Capital) once they've been generated.

There is no switch on/off button either.

And no. What the FHFA/UST are doing isn't legal. The Separate Account plan is what is legal, pending unwinding it.

You are showing the ERCF based on the illegal Government theft story that you and other plotters defend in court.

Instead, with the Separate Acct plan, CET1 >2.5 % of ATA.

English much?

Playing the fool again,Mr.Pro Se? ST filed a motion Rule 50(b) for JMOL, with the objective to alter or amend the judgment based on the jury's verdict.

It was a shadow appeal because, first, the judge didn't reply whether she can file 55 pages, breaking the page limitation.

Secondly, it wasn't related to a jury issue but whether claims travel with the shares that the judge already ruled positively on.

A motion 50(b) (28-day deadline after the judgment) must be a replica of the motion 50(a) for JMOL already submitted previously before the trial, with evidence that had to be submitted to the jury for deliberation. This is why 50(b) is called RENEWED motion for JMOL.

FHFA submitted an oral 50(a) motion, which would hinder the assertion that the same evidence was submitted later in the 50(b) motion with 55 pages.

This is why this 50(b) motion is more like a shadow appeal, although the formal appeal hasn't been submitted yet, with a deadline of 60 days after the judgment.

But, because the judge extended the deadline for filing the brief with the attorney's fees and costs, to 45 days (May 6th) instead of what is stated in the Rule (14 days), he also added that he reserves his discretion to change the deadline for the appeal, making this deadline May 6th, a brief that would be considered a date that resets the 60-day deadline for the appeal.

Quit playing the fool to fabricate court news 24/7 on this board.

You ask a question or post flawed information, expecting that someone will reply or you reply to yourself with your 30+ aliases on this board.

The court news are for the hedge funds, investment banks and Private Equity firms.

The retail investor is waiting for a swift administrative resolution with the announcement of the Separate Account plan.

No, I did not see where Sandra filed a motion to throw away Jury verdict and throw away Lamberth verdict in Lamberth court.

Link to the defendant's motion to appeal? Will you kindly share it. Thanks

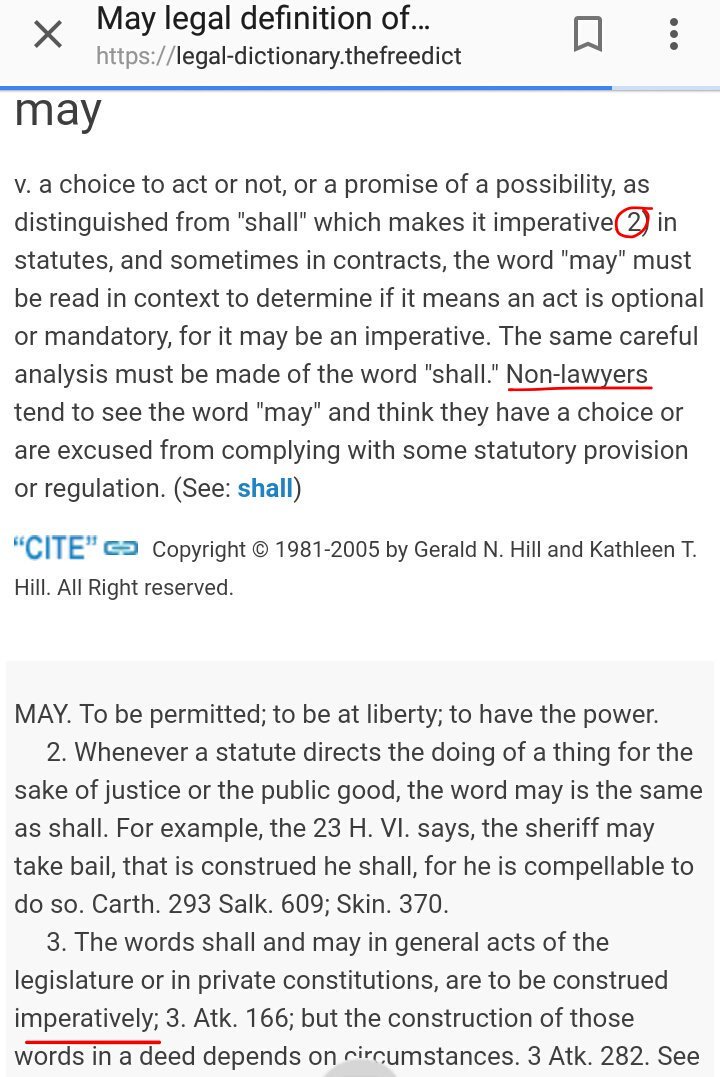

One thing is that the FHFA suspended the Capital Classifications in 2008 and the capital requirements aren't binding, which is typical of conservatorship, pursuant to the "may" in the FHFA-C's Power: "may put FnF in a sound and solvent condition" and also the FHFA-C's Incidental Power: "Any action authorized by this section, in the best interests of FnF or the FHFA". That is, it's necessary so that the conservator has some leeway to administer the conservatorship, at the time when the companies and the economy are bleeding and still do and in need to fix their operations, organization,...15 years later, that's why the FHFA director still needs the powers and rights from FnF and ours.

In other words, this way, the conservator isn't tied up.

And a different thing is that:

1- The capital requirements must be published because they are statutory (FHEFSSA). This is why FnF have posted the Minimum (Leverage) Capital requirement on their Earnings reports every quarter since day one. The Risk-Based Capital requirement was missing because HERA struck the entire section in the FHEFSSA with the formulaic, with the mandate to the director to come out with a new one.

Not "binding" but they are good to know.

Freddie Mac:

2- You seem to suggest that, because there are no capital requirements, FnF aren't required to build capital. Then, you can take all their capital generated away. Even without thresholds (requirements), they have to build capital.

This is the typical "playing with the words" by the Fanniegate attorneys we are used to. We need to know the thresholds to track the capital shortfall, evaluate their soundness and solvency and to uphold the FHFA-C's power (which means to restore the capital levels: recapitalization), and I've already mentioned that "may" is imperative once the capital has been generated and not a choice, in the legal dictionary.

That is, the statutory capital levels are financial indicators of the financial condition in a financial company.

3- The suspension of Capital Classifications doesn't mean that the statutory section "Capital Classifications" was suspended or repealed, which is another take by the Fanniegate attorneys, where all the definitions regarding capital are set forth, so we learn that the Minimum (Leverage) capital requirement is met with Core Capital and added in the Capital Rule, the CET1 Capital and Tier1 capital; that the Risk-Based Capital requiement is met with Total Capital; that there is a Critical Capital level called "irrelevant" by the FHFA because it triggers a conservatorship during a conservatorship, but it forgot that it needs to be published regardless, currently illegally absent from the ERCF.

They aren't met with the capital metric "Capital Reserve".

The plotters don't like the rules, this is why the Mnuchin Treasury Department recommended Congress to repeal these FHEFSSA definitions in its 2019 UST Plan at the request of a Presidential Memorandum, which attempted to substitute the real 2011 UST 3-option Privatized Housing Finance System for the release, at the request of the Dodd-Frank law and a Report to Congress.

4- The key for the suspension of Capital Classifications that didn't bother to anyone in the first place: somehow the plotters think that, pretending that it was the FHEFSSA section Capital Classifications what was suspended too, commented before, the Restriction on Capital Distributions (U.S.Code §4614(e)) was repealed too, because, HERA, surprisingly, inserted it at the end of the section, whereas the same provision is a stand alone section: Prompt Corrective Action in the banks' FDI Act.

HERA:

5- Likewise, the fact that it took 12 years for the FHFA director to come up with the changes in the capital requirements of the FHEFSSA (18-Month Implementation section, missing), that it was authorized/mandated to carry out in an amendment inserted by HERA (Capital Rule effective February 16, 2021), doesn't mean that FnF don't have to build capital for their financial rehabilitation in the meantime. That is, the typical Transition Period to build capital given by any Federal Agency when there are changes, and the Equity holders have suffered Regulatory Risk (Basel framework for capital requirements, in light of the 2011 UST Plan). It has just made it a "Back-end Capital Rule".

Besides Conservator Risk, not only for the Separate Account plan (Legal, except the 7 Securities Law violations in the process), but also for the extended period beyond what would have been reasonable thresholds for the release (Undercapitalized: C.C. or Tier 1 Captial > 2.5% of ATA. Mandatory release in the prior FHEFSSA; or the resumption of dividend payments afterwards), but "in the best interests of the FHFA" (membership cleansing) it has been extended to CET1 > 2.5% of ATA, so FnF can redeem the JPS (AT1 Capital) and still meet the ERCF with Tier 1 Captial > 2.5% of ATA.

Wait! Because it was extended one quarter more to 4Q2023, so that the laggard Fannie Mae meets the threshold for the resumption of dividend payments (25% of the Prescribed Capital Buffer. Table 8: Payout ratio) after the redemption of JPS, and under the Separate Account plan.

BOOM. This image from JPM illustrates my point: the PLMBSs skyrocketed just after FnF were placed in Conservatorship.

Trough date is the date the PLMBSs hit the bottom. We see that in most of the different groups, it was 3 months after the day of Conservatorship. Other, one year later.

Later they skyrocketed (From trough date to the end of 2009, up to 30% higher)

The link between unrealized losses and the conservatorship is clear.

FnF were placed in conservatorship pursuant to the FHEFSSA section 1367(a) APPOINTMENT OF THE AGENCY AS CONSERVATOR (which, by the way, was an amendment inserted by HERA in the FHEFSSA), according to the SPSPA:

Although it isn't specified, there are 12 reasons for the conservatorship at the discretion of the FHFA.

Likely, it was chosen (G) LOSSES: Likely to incur losses that would deplete all of its capital.

Related to future (fabricated) losses, not past losses as Washington Federal (bailed out by the Treasury Department in 2008) claimed in court in a clear case of misrepresentation of the law.

Spot on! Those future losses came true if they were all fabricated:

-The 10% dividend to Treasury.

-The DTA valuation allowance.

-Outsized provisions for loan losses caused by the prior Incur Loss accounting standard and the Obama's programs, as FnF were compelled to set aside a reserve equal to the concession granted to borrowers, not the actual expected loss (it was changed in January 2020 for the CECL accounting standard). An amended in 2011 ballooned the borrowers elegible, as now, it was up to the management to decide if one borrower current on its mortgage payments was at risk of default.

-The initial $1B SPS LP issued for free, it reduce the Additional Paid-In Capital account (Core Capital) in the same amount (currently in place with the SPS LP increased for free every quarter, but the managements commit financial statement fraud by not posting both operations on the balance sheets)

-The mispricing of the PLMBSs.

Their ambition to prompt losses, so more SPS LP is increased, fired back, because the dividend was restricted and unavailable, and instead, it was a separate account for the reduction of the principal of the obligation, similar to the one with the FHLBanks in 1989.

Finally, have you noticed in the screenshot that the FHEFSSA is cut short with "FHE Act"? Typical in documents. But then, it has deviated to today's "GSE Act" in the Earnings reports from FnF.

This way, they seek to delete any trace of the FHEFSSA that contains the only authorized capital metrics and their definition; the capital classifications and definitions, to see that the Minimum Leverage Capital level is met with Core Capital or with CET1 and T1 Capital added recently, and the Risk-Based Capital requirement, met with Total Capital. They aren't met with "Capital Reserve", an invalid capital metric in the FHEFSSA and badly assessed (adjusted Capital Reserve = $0), only used by the Federal Reserve System in its battered Balance Sheet (Called "Capital Surplus" but it's the same concept).

"GSE Act", looks more like the Charter Act, which is also being concealed.

This is like other plotters all day with "HERA, HERA, HERA" (Rosner and the plaintiff Joshua Angel and khtomp19 on this board), when it's the FHEFSSA (and the Charter Act) as amended by HERA. Never HERA alone.

They don't want you to see what HERA didn't amend: Critical Capital level, definitions, etc. And also, what did HERA amend? Because HERA struck the prior MANDATORY release Undercapitalized: when the Core Capital (Tier 1 Capital) > Minimum (Leverage) Capital requirement (2.5% of ATA in their ERCF).

Calabria/Mnuchin chose a steep CET1 > 3% of ATA, which was snubbed.

Under the Separate Account plan, FnF have CET1 > 2.5% of ATA. Which bodes well for the redemption of the JPS (AT1 Capital) at their fair value of par value, and then, FnF would comply with the ERCF of Tier 1 Capital > 2.5% of ATA. Also complying with the FHFA's desire of "membership cleansing" before the Privatized Housing Finance System revamp chosen for the release in 2011 by the UST, at the request of the Dodd-Frank law, as seen in its 2016 Final Rule with the FHLBanks, that ordered the expulsion of the unwanted members.

We can even spot that Calabria forgot with HERA to include in the FHEFSSA the typical "18-month implementation" (like in the very FHEFSSA in question when the first capital ratios in 1992), when it directed the FHFA director to change the capital requirements and add new capital metrics (CET1 and Tier 1) besides a Capital Buffer, that would have prevented the current "back-end Capital Rule" (effective February 16, 2021), that is, enacted after the Transition Period to build capital, given always by any Federal Agency when there are changes.

The mandatory release implies that FnF have to build regulatory capital in the first place.

Playing with the words is their modus operandi: "dividend obligation", in order to pass it off as interest payments on obligations (1989 FHLBanks' bailout) and skip the Restriction on Capital Distributions (Dividends; SPS LP increased for free; the Lamberth rebate), besides unavailable Earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts all along.

The information about bond insurers and bond insurance coverage was a topic in their earnings reports in early conservatorship, but nowadays FnF don't talk about it, primarily because they no longer hold PLMBSs.

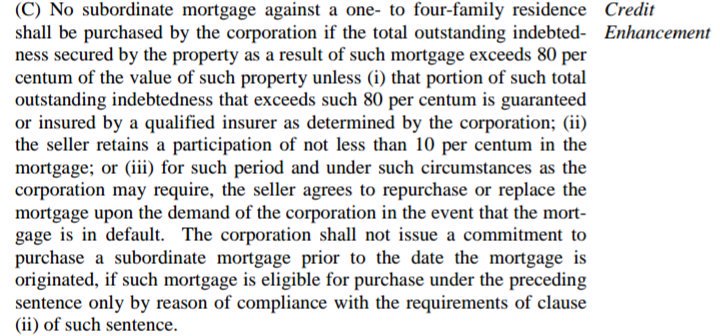

The important thing is that the purchase of PLMBS was illegal in the Credit Enhancement clause of the Charter Act (Lack of credit enhancement operation. For instance, today's commingled securites/resecuritizations/Catastrophic-Loss Reinsurance do comply with this clause, as the underlying securities are 100% insured by other guarantors. Credit Enhancement operation number (iii)).

Had the FHFA complied with the law, the conservatorships wouldn't have existed.

Nowadays, more illegal operations with the Credit Risk Transfers (CRTs), because it's not one of the enumerated Credit Enhancement operations authorized.

The fact that there are senators like the former senator Toomey or currently, senator Rounds this week, encouraging the FHFA director to do CRTs, doesn't make it a law, or an amendment of the Charter Act.

Both repeat the same slogan as Sandra Thompson: "To protect the taxpayer". The taxpayer doesn't bear credit risk in FnF. It just buys obligations SPS upon negative Net Worth ("capital deficiency"), which matches the "finance their operations as a last resort" written in the section Purposes of the Charter Act, in exchange for their Public Mission written below it (outdated nowadays if they no longer subsidize the g-fee; Duty to Serve protected by the Fair Housing Act, etc). That is, a UST backup and not govt implied guarantee on the MBS.

$19B in CRT expenses and recoveries, net, is due (turned into Retained Earnings account. This account is the sound and solvent condition to protect the SPS and the taxpayer: soundness and solvency)

Watching the UPB of those PLMBSs covered in 2010, and then, the unrealized losses, it doesn't look like the insurance claim against the bond insurers was large.

The main economic harm in FnF was caused by the mispricing of the PLMBSs by Wall Street, with the objective to prompt the conservatorships in FnF.

Later, the PLMBS skyrocketed in price.

The S.E.C. years later found no evidence of PLMBS price manipulation those years.

This is the line item AOCI (accumulated unrealized losses in AFS securities) in Equity that prompted the conservatorship. FnF didn't know the banks' trick of "Held-to-maturity portfolio".

Freddie Mac:

At March 31, 2010, we had coverage, including secondary policies on securities, totaling $11.5 billion of unpaid principal balance of our investments in securities. At March 31, 2010, the top five of our bond insurers, Ambac Assurance Corporation, or Ambac, Financial Guaranty Insurance Company, or FGIC, MBIA Insurance Corp., Assured Guaranty Municipal Corp., or AGMC, and National Public Finance Guarantee Corp., or NPFCG, each accounted for more than 10% of our overall bond insurance coverage and collectively represented approximately 99% of our total coverage.

We recognized other-than-temporary impairment losses during 2009 and the first quarter of 2010 related to investments in mortgage-related securities covered by bond insurance as a result of our uncertainty over whether or not certain insurers will meet our future claims in the event of a loss on the securities.

BOTTOM LINE. 2nd-lien mortgages turn into 1st-lien motgages, in the case of purchases of those cash-out refinancings.

After being bundled into UMBSs, it isn't a new product.

Is the purchase/sale of 2nd-lien mortgages in cash-out refinancings, a new product?

It would need approval, plus publication on the Federal Register for a comment period.

I don't think that it's a new product. Subject to the overall 80% LTV limit (Charter Act: the same Credit Enhancement clause that bars the CRTs) that takes into consideration the first mortgage it emanated from, when it was refinanced, and at the same interest rate.

So, not only mortgage-related but also it copycats the first mortgage.

It would be sold as a Uniform Mortgage-Backed Security (UMBS) like all others.

You may say that it's a new product because it's a new activity. It's the same activity when it was created: refinancing of the mortgage. Same collateral.

What we call "product" is the UMBS.

The same with the sale of RPL bundled into UMBS again. Nowadays RPL sold to GS.

It wouldn't be a good idea to consider it a new product, pricing-wise.

Not a personal loan at a 9.5% rate like the new proposal from Freddie Mac. This case, a new product.

Authorized in the Charter Act: "to lend on the security of a mortgage."

More if we are bound for a Charter-revoked scenario (2011 UST plan).

The thing is that that's a personal loan, not a second-lien mortgage.

A personal loan at a 9.5% rate, using the collateral (property) already owned by Freddie Mac.

Unrelated to a mortgage.

This is why it's been announced just after the CEO of Freddie Mac with 30+ years of experience in mortgage finance, resigned "in the 1Q2024". He finally left the company on March 15th.

I guess that Freddie Mac would have to apply for a banking licence.

High interest rates as a consequence of the price of the collateral ballooned (overheated), means that your are doubling down on credit risk, and at the time when FnF aren't allowed to take possession of that collateral that covers the credit risk, because they are compelled to sell their NPL and RPL to Goldman Sachs & Co and the hedge funds, even at a discount. Judicial states delay it, etc.

The same loan amount can be achieved with cash-out refinancings, when the entire UPB of the mortgage and more, is refinanced at low rates.

FnF purchase the first-lien mortgage and the banks keep the second-lien mortgage on their balance sheets.

You can read more about it in the FHFA website, in light of the request for comment on this new product.

I'm in favor of FnF purchasing the second-lien mortgages, but in cash-out refinancings (less risky: low rates and low home prices), not in personal loans that is what has been proposed.

There are second-lien mortgages worth $ billions in the banks' balance sheets, where FnF own the collateral, but the banks are allowed to do business with it (collateral-sharing)

This why the reason of the famous robosigning case with foreclosures in early conservatorship. The banks (servicers of the mortgages) wanted to foreclosure on the properties fast, in order to protect their second-lien mortgages. You would wonder why a 2nd-lien gets paid first.

The repurchase of all the second-lien mortgages in cash-out refinancings already outstanding, would boost the economy and the banks' battered balance sheets.

Mark Calabria was congratulated yesterday over on the Twitter #Fanniegate hashtag, for his proposal regarding Affordable Housing.

When he is right, he is right.

GREAT PROPOSAL BY CALABRIA

— Conservatives against Trump (@CarlosVignote) April 18, 2024

All federally-owned lands (@DeptofDefense's, massive in CA) transferred to the Municipalities, that would be in charge of Affordable Housing.

FnF invest in LIHTC like the hedge funds (Pagliara & Co). LIHTC is costly for Congress.#Fanniegate @WhiteHouse https://t.co/t2sbjUbrSj

The plotters react to the Legal definition "MAY" posted yesterday in the comment I'm replying to, and they tumbled the stock prices.

This word is very important because the FHFA's Wall Street law firm, bases all the defense on this word, stating that it's "permissive, rather than mandatory".

It's clear that it means to have permission to do something. An authority. A power.

But it doesn't mean that it can be excused from complying. That is, it's imperative once the capital has been generated, in order to (may) put FnF in a sound and solvent condition (FHFA-C's Power). That is, to restore regulatory capital levels, and since day one.

$426B of core capital is held in escrow, including the $125B corresponding to the offset attached to the $125B SPS LP increased for free (another capital distribution restricted)

"May" in the FHFA-C's Power is also interrelated to the FHFA-C's Incidental Power, about activities in the best interests of the FHFA, and it can be used this comment by Freddie Mac as explanatory note. It can be included the expenses to build the CSP, etc.

All the legal proceedings have been built around this, and it has ended up with the fiction of implied contract (the dividend was impeccably suspended, as per the Restriction on Capital Distributions) and false damages (one-day share price drop) in the Lamberth court, which, by the way, the motion for JMOL was fraudulently filed as a backdoor appeal, to show strength, and the real appeal will be filed when due, because it wasn't related to the evidence argued during the trial and a jury issue, required in a motion for JMOL, but this private sector law firm brought up again the issue of whether a claim travels with the shares. Judge Lamberth already said that it's correct, but now, it comes the appeal many years later, so it's reduced to those that can demonstrate that they held stocks on the day of the 3rd amendment. Basically, only Berkowitz and other plaintiffs get damages with money taken from FnF (back dividends), another capital distribution restricted by the way.

Judge Lamberth knew that the FHFA couldn't file 55 pages in a motion for JMOL Rule 50 (b), if the one Rule 50 (a) was an oral motion. This is why he didn't respond to the question whether it can file 55 pages and let the FHFA file a shadow appeal.

Evidence that everything has been rigged by the parties and the judge, since day one. Create expectations is always their modus operandi to act freely and draw more people into their cause, but seeking a different outcome.

The FHFA Directors and their Wall Street law firm will receive always the same response:

NO!

$1TRILLION SUIT LOOMS@FHFA says "may" is permissive rather than obligatory https://t.co/1RroDt7vgr

— Conservatives against Trump (@CarlosVignote) June 4, 2017

NO! https://t.co/G8pNhEgzIs#Fanniegate

Read the #Fanniegate hashtag for daily in-depth analysis.

The FHFA Director lies in her written testimony for today's hearing.

1st. She refers to the FHFA-R's duty "ensure that FnF operate in a safe and sound manner", but she omits once again (like all other FHFA directors) what comes up next: "...including maintenance of adequate capital".

And "capital", in this world, means regulatory capital if everything is set forth in the FHEFSSA that establishes the capital ratios, definitions, etc. She can't make up "Capital Reserve" and badly assessed (Adjusted Capital Reserve = $0) with the Net Worth.

Also, she omits her role as director of the FHFA acting as conservator, with a Power of recapitalization, commonly known as "Rehab power": "May put FnF in a sound and solvent condition", when soundness is related to capital levels. And "may" is related to some leeway in activities that carry more risk or incur losses, taking into account that supposedly the American economy is still bleeding (Huh?). In no event "may" means that it's excused from complying once the capital has been generated, authorizing to syphon it off to the Treasury.

Legal dictionary:

2nd. She has omitted this time, the prior slogan: "FnF remain undercapitalized". She must have read my comments pointing out that that was a quote taken from the Restriction on Capital Distributions in the law, as a reason for the restriction. Now she says that their capital available is "well below the minimum capital requirement".

3rd. The same lie: "FnF retain earnings", like Bill Ackman and his clerk, Bradford, and recently the FNMA CEO, based on the Financial Statement fraud of FnF, when they are reluctant to post on the balance sheet the SPS LP increased for free since December 2017, because they carry an offset (reduction of Retained Earnings account) that wipes out the Retained Earnings just built.

It would show that their current $125B Net Worth has been built solely with $125B SPS LP increased for free, currently missing.

She has omitted this time the: "FnF continue to build capital" before "through retained earnings", a slogan repeated by the others mentioned, and now she just says: "FnF built $125B Net Worth", when that's not a metric for the soundness in a financial company.

It's time to appoint someone with the knowledge in capital adequacy matters, who doesn't play with the words all the time: "Dividend obligation", in order to pass it off as the security "obligation" in the RefCorp obligation (FHLBanks' 1989 bailout).

This way, she wants to turn the dividend payments on SPS into the interest payments on RefCorp obligations, and skip the Restriction on Capital Distributions (Dividends, today's SPS LP increased for free and the Lamberth rebate).

A Goldman Sachs alumni will always do Goldman Sachs things.

Judge Lamberth, accomplice. FHFA files a motion for JMOL.

Under Rule 50 (b) and filed under seal, without the reply to the FHFA's Wall Street law firm of a question submitted last Friday, asking whether it can skip the page limitation to 55 pages.

Without the judge's required reply, the judge skips having to forfeit the motion at the same time, for the reasons outlined yesterday.

It was imprudent to file an oral motion for JMOL Rule 50(a) previously, during the trial, because the Rule requires that both have to have the same sufficiency-of-the-evidence arguments.

It isn't satisfied with an oral motion by any stretch of the imagination.

Therefore, judge Lamberth is accomplice of this delay tactic.

The judge has waived what his job requires, pointed out in my follow-up:

(*) Pending to know what the judge has to say in a reply.

You continue to skip the FHEFSSA's Critical Capital level.

You only talk about HERA, despite that HERA only inserted amendments in the FHEFSSA (and the Charter Act).

Thus, without amendments, the Critical Capital level remains as is. And therefore:

An enterprise shall be classified as critically undercapitalized if—

(ii)does not maintain an amount of core capital that is equal to or exceeds the critical capital level for the enterprise;

The FHFA will have its motion for JMOL to override the verdict, forfeited.

It was submitted on Friday.

(*) Pending to know what the judge has to say in a reply.

#FANNIEGATE ATTYS DRAMA TV SERIES

— Conservatives against Trump (@CarlosVignote) April 17, 2024

7th amnt:"No fact tried by a jury shall be otherwise re-examined in any Court",blasts an attempt to appeal a jury issue already decided.

Only a JMOL Rule 50(b),which needs 50(a):same sufficiency-of-the-evidence arguments w/ oral motion?

Forfeited https://t.co/AcdRN7ctRQ

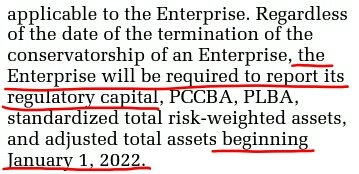

The Capital Rule is effective February 16, 2021.

Although the same Capital Rule stated that FnF must keep it secret until January 1st, 2022 (They only gave a broad figure with the 1Q2021 Earnings reports).

Therefore, the ERCF tables were posted for the first time with the 1Q2022 Earnings reports.

A measure tailored for representative French Hill in the annual testimony of the FHFA Director of July 2022, so he asked about the 2021 FHFA Report to Congress without the ERCF tables and huge regulatory capital shortfalls over capital requirements.

The same with representative McHenry in 2023. The 2022 FHFA Report to Congress in question was released in June 15, 2023, but he had already convened the annual testimony of the FHFA Director weeks earlier.

Anyway, the core capital available and Minimum Capital level have been posted every quarter since day one on their Earnings reports, because it's statutory (with the old weights).

The Risk-Based Capital requirement absent, because HERA struck the entire section with the formulaic in the FHEFSSA.

The capital shortfall is evidence in itself of a Separate Account plan (Adjusted $402B core capital shortfall over Minimum Leverage Capital requirement as of December 31, 2023, combined).

The Joint Statement of Undisputed Facts is dated 07/26/23.

The deposition by the former FNMA CEO was given in 2020, but submitted to court in 08/10/23, for the second trial too.

Judge Lamberth refuses to reply to Sandra Thompson and her Wall Street law firm, when they submitted an unopposed motion for Judgment as a Matter of Law on Friday.

Story developing.

NO REPLY TO ST'S CALL FOR JUDGMENT AS A MATTER OF LAW

— Conservatives against Trump (@CarlosVignote) April 16, 2024

Judge tired of:

-Making False Statements

-Abuse of court process

Like:

-Joint Stmnt of Undisputed Facts👇

-Howard @ SCOTUS:"SPS,non-repayable securities"

Targeting the exception to the Restr on C.Distribution:↓SPS#Fanniegate https://t.co/iFIcgHnZ4C pic.twitter.com/R0fCXxBrMW

The CBO has not been in the making.

You picked the wrong document.

It's the UST 2011 3-option Privatized Housing Finance System revamp, a Report to Congress at the request of the Wall Street Reform and Consumer Protection Act of 2010 (The Dodd-Frank law), as "recommendations on ending the Conservatorships".

Option 3: a government Catastrophic-Loss Reinsurance. The commingled securities enable it, unveiled by Freddie Mac in June 2022.

You can't stop scheming, can you (Emphasis added):

attached pdf that was produced by the government. plan accordingly.

More about the Wall Street law firm representing the FHFA in court.

It's been denounced multiple times that it claimed in the Lamberth court that the dividends are "mandatory", according to Katie Buehler that attended the trial (watch her tweet below).

But we didn't have documentary evidence, until yesterday. Two different court briefs double down on the same flawed idea, with: "dividend obligation".

- The FHFA and the plaintiffs in the Lamberth court: Joint Statement of Undisputed Facts. Not only their "fact" is flawed, but also the cover-up of many other facts is why they are accused of Making False Statements.

-Fannie Mae, as stated in the deposition given by the former CEO and submitted to the Lamberth court as well.

Mandatory dividend doesn't exist. In the end, they want to turn the dividend payments into interest payments (An expense. Without restrictions).

They attempted to replicate the 1989 FHLBanks' bailout with assessments funneled into a Separate Account written by law ($300 million annually in interest payments on RefCorp obligations, assessed with a 0.299% spread over Treasuries -GAO report-, and the rest, invested in zero coupon Treasuries, that is, sent to UST like FnF have done).

Because FnF pay dividends on SPS (obligations in respect of Capital Stock. Source: SPSPA) and there were no earnings available for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts, and also, dividends are restricted when FnF are undercapitalized in the Restriction on Capital Distributions, the entire assessments were applied towards the exceptions to the aforementioned restriction in order to legalize them:

-To reduce the SPS, U.S. Code §4614(e).

-For their recapitalization, CFR 1237.12.

When they were aware of this outcome, they began the plan of deception: "Mandatory dividends"; "dividend obligation"; Howard: "SPS, non-repayable securities", etc.

(*)The cumulative dividend rate on SPS was assessed at 1.8%, with a 0.5% spread over Treasuries.

DIVS AREN'T INTEREST PAYMENTS

— Conservatives against Trump (@CarlosVignote) April 14, 2024

-Wall St law firm representing @FHFA:"Mandatory divs"

🆕-Joint Stmt of Facts & FNMA:"Div obligation"

1-Div, a distribution of earnings. Unavailable(Acc Deficit Retained Earnings acct)

2-Restriction on Capital Distribution.#Fanniegate @TheJusticeDept https://t.co/APWhh2JNo2 pic.twitter.com/cK8G2RyAnx

Our enemy Howard should add a disclaimer: "Writing as member of Berkowitz's legal team".

He talks about misinformation, when he is accused of going to the Supreme Court as amicus to lie, writing a dozen times that the SPS are non-repayable securities.

Not only it isn't written anywhere, but also it's precisely the repayment of SPS the only capital distribution authorized when FnF are undercapitalized, as exception to the Restriction on Capital Distributions by law, U.S. Code §4614(e).

What FnF have done through the assessments sent to UST under the guise of dividend payments (10% and NWS dividends. Phases 1 and 2). No actual dividend was ever paid, as there were no earnings available for distribution as dividend with Accumulated Deficit Retained Earnings accounts, and a capital distribution restricted.

This is authorized in the FHFA-C's Incidental Power: "Any action authorized by this section,...."

Then, the FHFA added the recapitalization in a separate account (CFR 1237.12) in the July 20, 2011 Final Rule, as another exception to the same statutory restriction ("It supplements and shall not replace or affect it", that is, a follow-on plan), when it foresaw that, with the coming NWS dividend (fastest speed to that end), the SPS would be fully repaid fast. End of 2013 in Freddie Mac (signature image below) and end of 2014 in Fannie Mae.

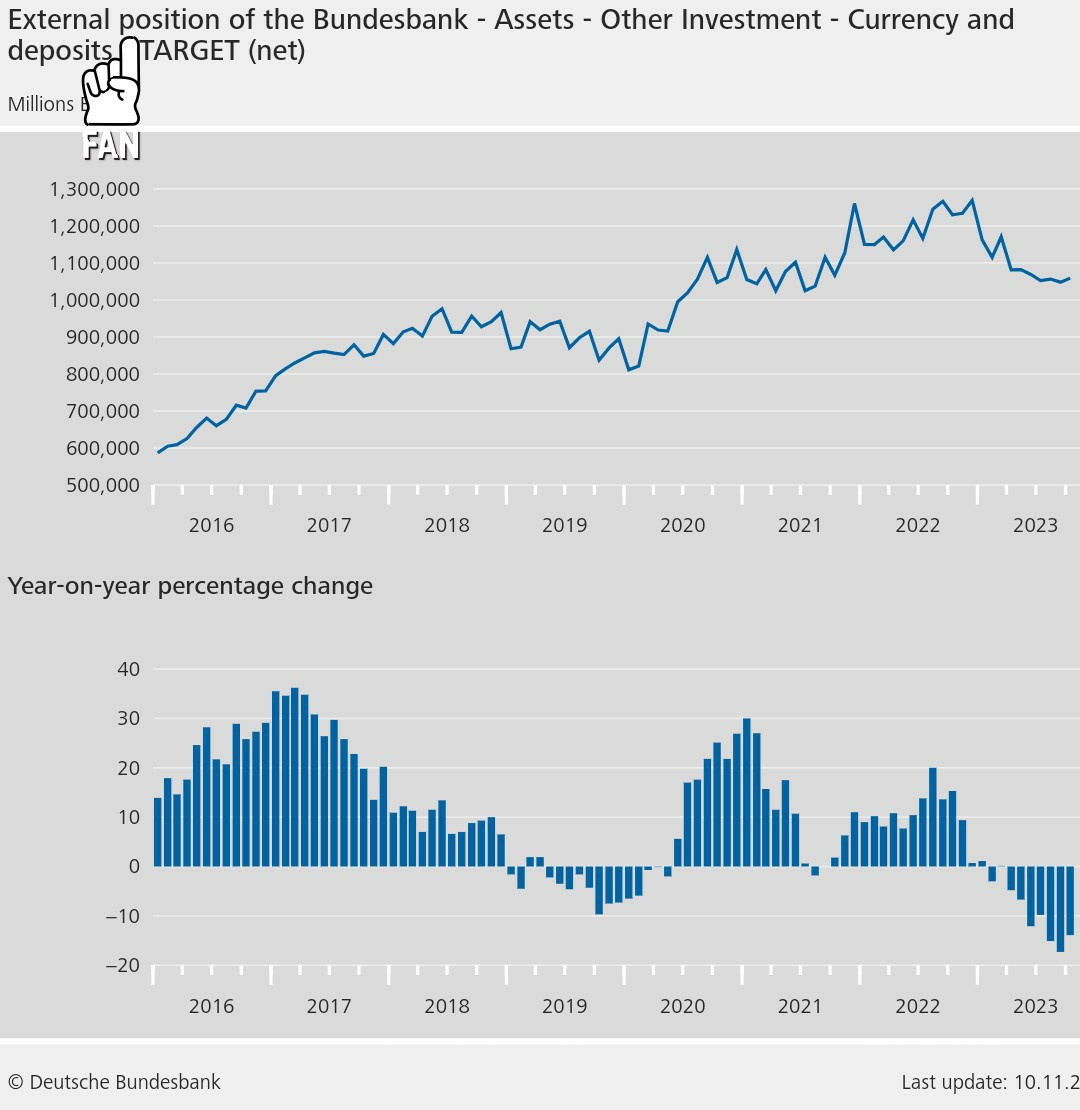

These assessments in the form of capital distributions, are currently in the 3rd phase with the SPS LP increased for free (another capital distribution, like the dividends) and its corresponding offset with reduction of Retained Earnings account (core capital). Thus, in reality, this reduction of core capital is common equity held in escrow, which would uphold the FHFA-C's Rehabilitation power (recapitalization) as well, pending unwinding this operation, because, in this world, the rehabilitation is on the Balance Sheet. Ain't no External Position, Bundesbank-style. That's fraud.

Net Worth/Regulatory capital/Stress Test are different things.

What we are waiting for on Monday, is Bloomberg announcing that it has received a Wells Notice from the S.E.C., for participating in the Fanniegate conspiracy, commented yesterday.

A Wells Notice doesn't mean that the S.E.C. will end up pressing charges against the corporation.

🚨The image of the Credit Enhancement clause in the Charter Act, was missing at the bottom of my prior comment.

That's more proper of a Charter revoked scenario.

First of all, "GSE Act" doesn't exist. Both Fannie Mae and Freddie Mac say "GSE Act" when talking about the FHEFSSA currently in force. By concealing the FHEFSSA, they peddle the idea of HERA, when the law in force is the FHEFSSA and Charter Act, as amended by HERA, as a way to conceal the rest of these two only laws in force.

They attempt to blend the FHEFSSA with the Charter Act, and say "GSE Act".

It's also a way to deny the existence of the Charter Act, like all the attorneys and judges have done in the U.S. courts.

FHFA must place us into receivership if they determine that our assets are less than our obligations (that is, we have a net worth deficit)