News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Fiduciary duties emerge ALWAYS that someone acts on behalf of other, which is what happened in the Succession Provision.

The conservator is using our rights and powers. It's not that they were eliminated, as all the hedge fund managers turned into Shareholder Rights advocates claim to deceive us, but transferred (Telephone Game). So, they still exist but held by the conservator momentarily.

In a Conservatorship, the rights and powers transferred to the conservator MUST be returned at some point when it fulfills its statutory goals: rehabilitation of FnF. Put in a sound condition = Soundness = build capital = what the Restriction on Capital Distributions is for (Dividend suspended, no SPS LP increased for free,...)

Therefore, it's linked to the capital levels (The MANDATORY RELEASE Undercapitalized in the FHEFSSA struck by HERA. When the Core Capital is greater than the Minumum Leverage Capital requirement). Nowadays, FnF have built a CET1 >2.5% of Adjusted Total Assets, lower than Mnuchin's overblown 3% required in the SPSPA that was snubbed (The JPS can be redeemed and still the ERCF with TIER 1 Capital >2.5% of ATA will be met)

Hence the g-fee hikes and Basel framework chosen as endpoint of the Conservatorship by the UST in its 3-option Privatized Housing Finance System revamp in 2011, at the request of the Dodd-Frank Law.

IT'S NOT THE FIDUCIARY DUTY TO ACT IN OUR BEST INTERESTS, like a Trustee (maximize profits, dividend payments, etc.), as everybody knows but navycmdr writing with Stockprofitter, to also shamelessly praise himself: "Thanks navy".

It doesn't mean that it can act against us (Telephone Game). It means that our interests aren't considered in the decision-making. Very different.

It turns out that there are more than one Fiduciary Duty, this is why it's in plural form (duties), something that judge Sweeney ignored: duty of care, loyalty, confidentiality, etc.

This makes sure that the conservator upholds the law, there is no secret plan and it publishes the accounts under GAAP, not with External Positions "off-balance sheet SPS", etc.

The duty of care might well be the "authorized by this section" after "take any action" in the conservator's Incidental Power, that compels it to uphold the law.

It was sent a certified mail to judge Sweeney with this issue.

It means that the breach of fiduciary duty isn't a tort claim but a breach of statutory provision and thus, it falls squarely within the CFC jurisdiction.

Remember that she tossed the Arrowhood case in the bin, with a breach of fiduciary duties, because she determined that it's a tort claim. Then, wrong court, she ruled.

The idea that you transfer your rights and powers to a conservator, and then it doesn't owe you anything, so free lunch to commit all sort of frauds, like today's Financial Statement fraud (gifted SPS and their offset, absent from the balance sheets), carry out a Separate Account with the Common Equity generated held in escrow (External Position), etc., is insane.

Exactly. FHFA has limited powers. Chevron deference, moot in Fanniegate.

A case of unethical behavior with an External Position in FnF with all the Common Equity generated (European Central Banks' Payment Systems-style) and corrupt litigants and Co peddling the Govt theft story, based on the coverup of the law, regulations and basic Finance.

How exactly has FHFA been abusing this deference? What 3rd party specific matters have been referred to FHFA that have been abusive?

Quit praising Trump. The Presidential Memorandum was an attempt to supplant the law in force (Dodd-Frank Law of 2010) that already directed the Treasury at the time to come out with "recommendations on ending the Conservatorships, no later than January 31, 2011", and subsequently, the February 2011 UST's 3-option Privatized Housing Finance System revamp, a Report to Congress.

Trump did try. He issued a White House memorandum to order that the GSEs be released.

H.R. 5549 (IH) - End of GSE Conservatorship Preparation Act of 2023.

To require the Secretary of the Treasury to submit to the Congress completed proposals for the termination of the conservatorships of Fannie Mae and Freddie Mac, and for other purposes.

President Emeritus of Harvard University Lawrence Summers met with People’s Bank of China Governor Pan Gongsheng on January 10, 2024.

The plotters Ackman, Pagliara, Bradford, plaintiff Joshua Angel on this board, etc., don't know how to sneak the word "Trump", who will finish off their government theft story with the assault on 99.9% of FnF (dilution through the Warrant, conversion Ps to Cs and stock offerings to build capital)

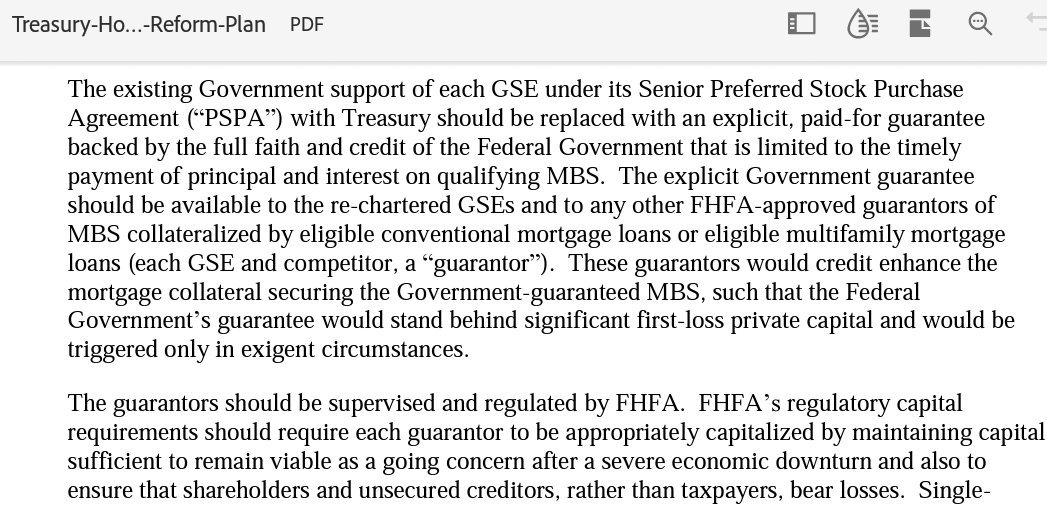

I'm not surprised to learn that there is a Bloomberg article endorsing "recapitalization and release". The recapitalization has already happened. 15 years in the making.

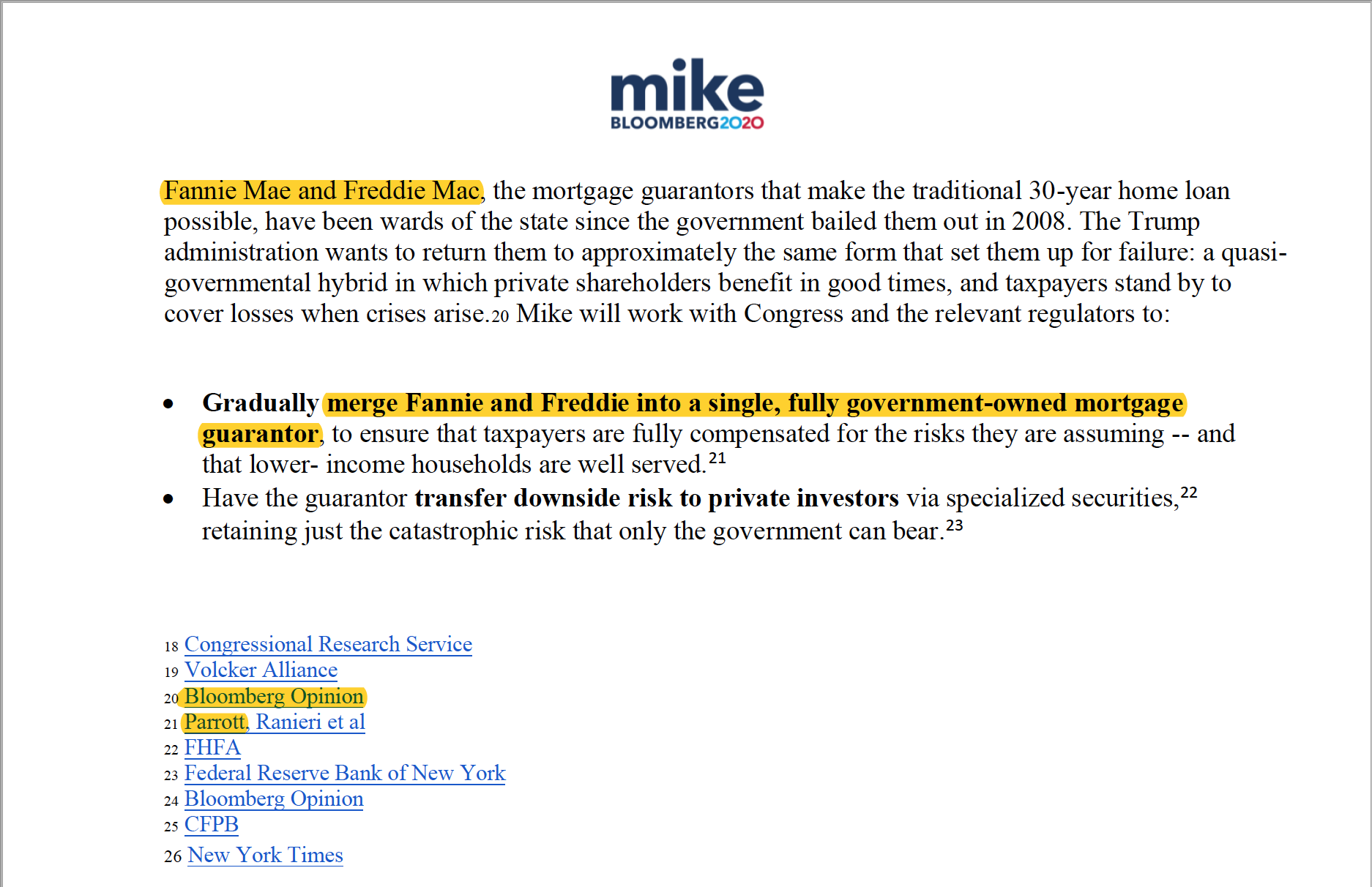

We know that Michael Bloomberg proposed a merger FnF and the nationalization of FnF thinking of China (as if this was even an option), with a Government Explicit Guarantee on MBSs. The United States isn't the Communist China.

Bloomberg is skewed toward the Wall Street firms that pay him the Bloomberg Terminal subscription rates that have made him billionaire. So, he owes them big time.

It's not a coincidence that the Bloomberg's take about a merger FnF, is the same as the Wall Street executives, according to their spokesperson, Gasparino, in 2010:

The report citing Wall Street sources said that the two mortgage firms will be combined into one agency.

Gasparino said that regulators purposely did not include Fannie and Freddie in the recent Dodd-Frank financial regulatory reform package due to a number of issues.

Don’t listen to banks…Their interests are not aligned perfectly with the broad interests of the American economy. Their job is to evade, or avoid, or weaken, any constraint on their ability to operate our job to make sure we’re protecting the american economy from the risks they inevitably take.

The president did not want the new rules to end up being written by those who brought us to the edge of catastrophic financial failure.

A Chevron case in Fanniegate is moot, because the FHFA has upheld the law, regulations and basic Finance with every action, under the Separate Account plan, a plan already carried out with the FHLBanks in 1989 by the same people (Sandra Thompson and DeMarco) and a plan that is rehabilitating FnF, according to Justice Alito's and Judge Willett's interpretation of the Incidental Power as conservator, spun to pursue a conspiracy jointly with the hedge funds and community banks, that happen to be JPS holders as well.

So, it's a case of ethics, since always it'll be very difficult to limit all the functions of a Federal Agency with legislative wording.

You write "take any action authorized by this section, in the best interests of the Agency", and some people think that it's an authorization to steal from private corporations.

Like the Telephone game, judge Sweeney omitted "authorized by this section" (So, she just wrote "take any action"), the 5th Circuit said that "any action authorized by this section" are those actions within its enumerated Powers, without pointing out that one of the Powers is the Rehabilitation of FnF, and the SCOTUS highlighted the "Rehabilitation of FnF" (Power or statutory goal), but omitted that he was interpreting the "authorized by this section". So, a mixture of Sweeney and Willett.

When talking about ethics, it isn't the same those that had the intent to uphold the law, like DeMarco, and others like Sandra Thompson obsessed with breaking the law and basic Finance, and get away with it with the help of the Judiciary.

We stand up for DeMarco.

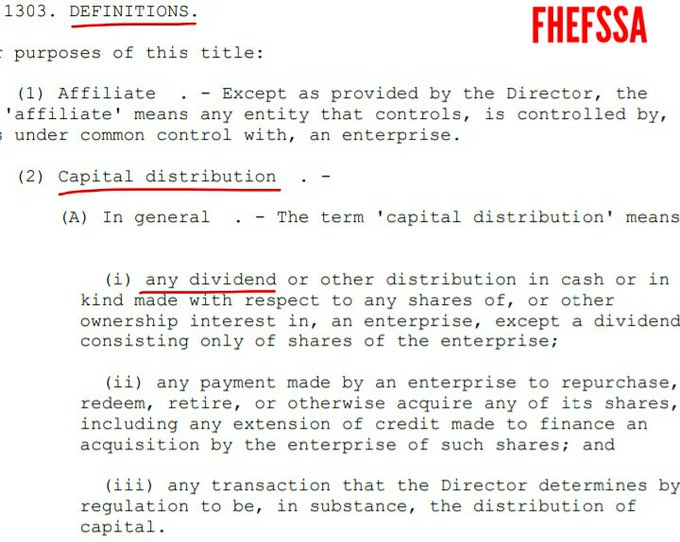

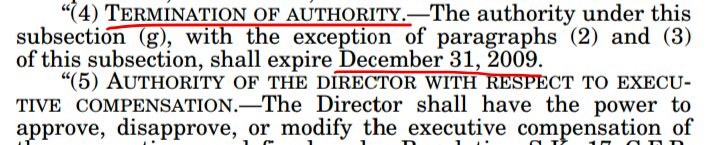

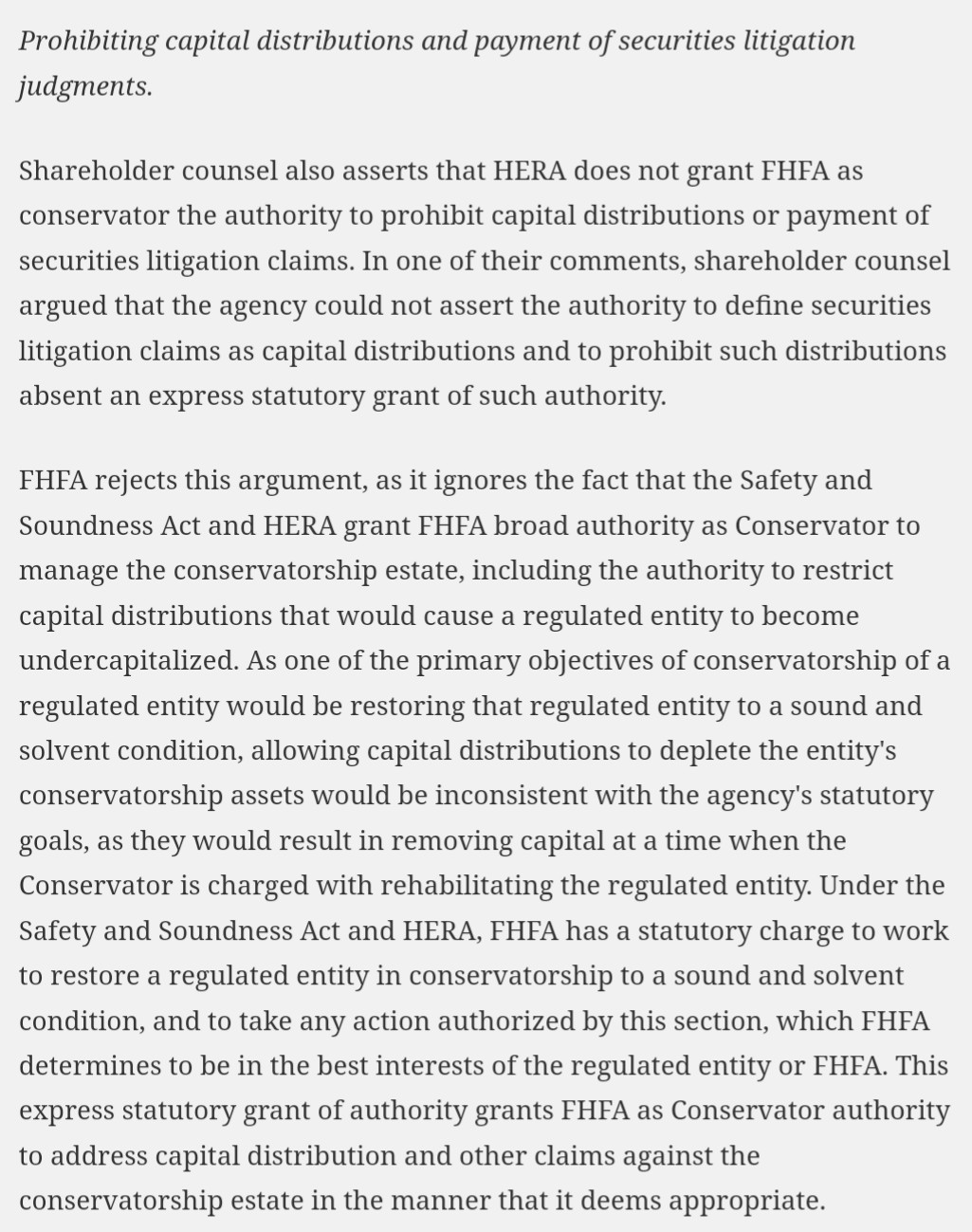

Expenses can be capital distributions, if they don't surge as a result of operations and, secondly, it's been expressly determined so through regulation, as required in the statutory definition of capital distributions, which is what the FHFA did in the famous July 20, 2011 Final Rule, amending the number 3 to include this case of payment of Securities Litigation judgments.

It's not about the money. The key is that the Lamberth rebate has uncovered the other 2 capital distributions during conservatorship that have gone through, despite being restricted. And this is why we apply them towards the exceptions to the restriction to legalize them, thanks to the FHFA-C's Incidental Power that allows this rogue Agency to mislead and mess around, if the endgame is "authorized by this section" (Rehabilitation).

A Separate Account.

An expense ends up reducing the Net Income in the Income Statement, which is later posted on the Balance Sheet (actual picture of a company) in the Accumulated Retained Earnings account, in turn, recorded as regulatory capital (Core Capital and CET1) and thus, it affects the Capital levels.

This is why it's restricted when FnF are undercapitalized (IN GENERAL). A restriction means that FnF keep it. So, don't just stop with "restriction".

The corrupt litigants rather see their dividend suspended in the Treasury's coffers (not only by covering up this Restriction on Capital Distributions, but also defending the payment of a 10% dividend to UST. The cover up the original low cost UST backup of FnF at rates similar to Treasuries and, secondly, they conceal that there were no Earnings available for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts. Evidence that what FnF sent to Treasury were assessments in the form of capital distributions, not actual dividends), than kept by FnF for their recapitalization, in order to increase their capital needs expecting stock offerings at rigged prices down the road and the assault on the ownership.

This is why all the investment banks, hedge funds and private equity firms are stuck to Fanniegate like parasites: Hindes, Bill Ackman, Fairholme, Perry Capital, Pagliara, JPM and Morgan Stanley ("underwriter advisors" selected by Freddie Mac and Fannie Mae, respectively)and the known sponsors of the Moelis Plan, BX and John Paulson.

Also, all the Wall Street law firms (Jones Days with the controversial former DOJ attorney Mooppan, etc.) or attorneys hired by them, like Bryndon Fisher, Joshua Angel, Hamish Hume, etc, that look more like mercenaries. Just read this comment by the controversial Bryndon Fisher proposing a settlement of the Collins case before the Oral Arguments at the SCOTUS, in exchange for a large sum of money just for their attorneys.

He is scheduled to file illegally a third appeal in the CFC case tomorrow, when his case has already been dismissed.

It was explained by the FHFA in the preface of the Final Rule where the Lamberth rebate was expressly included in the definiton of capital distribution (July 20, 2011) and also I remind you that it's when it was enacted another exception to the Restriction on Capital Distributions -12 CFR 1237.12- : A capital distribution (deplete capital) for .......wait for it.........for their recapitalization (build capital). A Separate Account wording suitable for the moment that the prior exception by statute, had reduced all the SPS outstanding (12 U.S. Code 4614 (e)). The FHFA needed another exception to keep on rolling the Separate Account plan. In either of the new 4 exceptions, it means "for Recap.", because it supplemented the restriction by statute (restricted for Recap as well). A follow-on plan.

PROHIBITED at a time of compliance with the Agency's statutory goal: the rehabilitation of FnF.

Wow! Did the DOJ pay you a visit, plaintiff Joshua Angel?

It's the first time that you post a correct comment among all your other 20+ aliases (HappyAlways, Barron4664, etc.)

Why didn't you tell the same thing to judge Sweeney and judge Lamberth, about capital distributions? Dividends, today's SPS LP increased for free and the Lamberth rebate.

Then, the Restriction on Capital Distributions.

Filing frivolous lawsuits has consequences.

$4.8B in punitive damages for the Equiity holders and payable jointly with all other members of your gang peddling the government theft story (Bryndon Fisher, Hindes, etc.) will do it.

Common Securitization Solutions(CSS) attracts buyers for a LBO (Leveraged Buyout) of FnF, as the purpose of this type of acquisition, is to use the Assets of the company acquired to fund it.

Besides their Contingency Portfolios and most liquid assets in the mortgage-related Investments Portfolios that I informed of every quarter, the acquirer will want to unlock the value and potential of CSS, a joint venture FnF in charge of managing the Common Securitization Platform, with a spin-off, distributing CSS shares among the common shareholders of FnF at the time.

However, the conservator could order FnF to redeem the JPS using its Incidental Power, so it's relieved of amending their dividend payments, redemption dates and regrouping all the series of JPSs into a single series, because the acquirer might want to keep them (more leverage), so more cash in FnF is used for the LBO.

It seems that the former FHFA Director Lockhart, heard something of this, and he rather spin it to lay out a case of setting up new subsidiaries replica of FnF. So, two "Mini-Me". This is beyond trash talk.

The JPS holders are behind this trash talk, desperate to grab a piece of CSS, now through these subsidiaries, because a swap JPS for Cs is impossible.

CSS is company that is already operating independently, with their own management, if it wasn't because the BOD is comprised of people from FnF.

I bet that the hedge fund manager behind this enchilada, is the one differentiating between SPS face value and Liquidation Preference when, first of all, the SPS have no face value/par value. Or calling the Common Stocks "options", to conceal that they trade at rock bottom prices because of the Government theft story that he and his shills peddle all the time, on social media and in the U. S. courts, not because there is some option.

There is never an option as far as upholding the law and basic Finance are concerned.

This renowned hedge fund manager later portrays himself as an options trader expert.

The spin-off of CSS from FnF can be done overnight.

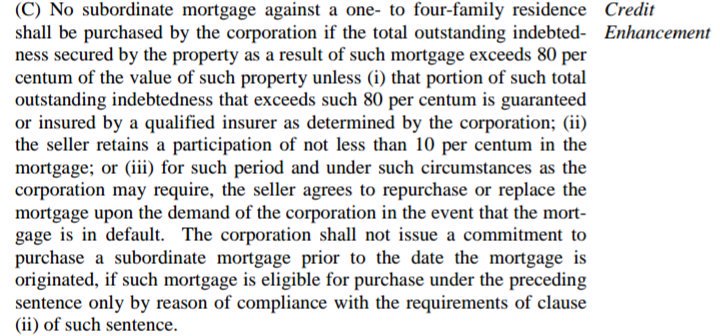

CRTs are illegal in the Charter's Credit Enhancement clause, because it's not one of the 3 credit enhancement operations that FnF are allowed to consider.

The compromised (the 2012 acquittal by a DC judge explains his misbehavior: Berko's legal team, SCOTUS amicus brief, etc.) Timothy Howard drives us to a debate about the economic sense of these operations instead.

There is no debate. They are unlawful. Otherwise the conservator might argue that it's authorized to do it in its Incidental Power, which is correct, despite being a scam to spin revenues out of FnF at a time of capital building.

And, likely, a backdoor fee sent to UST due to Mnuchin's slogan "taxpayer be appropriately compensated", which is barred in the Fee Limitation clause of the Charter Act as well. Source.

This is why Sandra Thompson repeats that the CRTs are necessary "to protect the taxpayer", when the taxpayer doesn't bear credit risk in FnF to begin with.

Likewise, the PLMBSs were illegal too, due to the lack of one of the three Credit Enhancement operations enumerated in the Charter Act.

A Charter Act that is being concealed by everybody: the SCOTUS in the first place, that turned FHFA into the FHA by removing the constitutional "for cause" removal restriction of its Director, which now has turned the FHFA Director into a copycat who is mimicking the FHA commissioner, etc...

They are depriving "congressionally-charter private corporations" and "overseer" of their meaning.

For instance, the new product commingled securities (Resecuritizations or Catastrophic-Loss Reinsurance) is authorized in this clause number 3, as the collateral therein is 100% guaranteed against default by other guarantors.

It's been requested a refund of $18B in CRT expenses, net (turned into Retained Earnings), either because the UST has been the recipient of the funds or the DOJ as vicariously responsible of this breach of the Charter Act by the Federal Agency FHFA. Then, the DOJ will have to recover the funds from the CRT investors, if they really exist.

Payment of Securities Litigation judgments IS a capital distribution.

It's the 3rd time that I have to reply to debunk your same lie.

A legal judgment is not considered to be a capital distribution.

Jesus!

Our negotiator takes the place of Hamish Hume and files an appeal in the Wazee case.

Wazee is the only case that challenges the SPS increased for free (NWS 2.0) in an amended complaint.

This attorney is also in the Lamberth court, filing frivolous lawsuits over the same issue: he covers up the Restriction on Capital Distributions and its exceptions, both in the 12 U.S. Code § 4614 (e) (Reduce the SPS) and the July 20, 2011 12 CFR 1237.12 that "supplements and shall not replace or affect any other restriction on Capital distribution by statute" and that statute is the 12 U.S. Code § 4614 (e) mentioned before (A follow-on plan. For their Recapitalization: exception 1, 2, 3 and 4)

This makes sure that FnF cannot distribute capital in the best interests of the taxpayers because it'd break the Restriction on Capital Distributions by statute. The "best interests of taxpayer" in the CFR 1237.12 can only be the Recapitalization of FnF.

🚨The key: both the reduction of the SPS and the Recapitalization in a Separate Account are recapitalizing FnF. Because the SPS are repaid with cash, not under the guise of cash dividends. You are depriving FnF of recording the Core Capital in the first place (double-entry accounting cash-Retained Earnings)

We can't allow the Fanniegate scandal to come down to a Sesame Street case, where we have to repeat over and over again the numbers 1, 2 and 3, with regard to the statutory definition of Capital distribution, amended also in the July 20, 2011 Final Rule, to include the payment of securities litigation judgment now in the Lamberth court covered up by the attorney Hamish Hume again.

Number 1. Any dividend and today's SPS LP increased for free in the absence of dividends.

Number 2. Stock buybacks and reduction of the Preferred Stocks.

Number 3. The payment of securities litigation claims (Lamberth court)

12 U.S. Code § 4502 (5)(A)

Amendment to include the Lamberth rebate in the number 3:

This tweet serves as appeal and it was sent to the DOJ.

WAZEE FILES NOTICE OF APPEAL

— Conservatives against Trump (@CarlosVignote) January 15, 2024

CFC case(Atty @ Lamberth court too)

In amended complaint,only one challenging today's NWS 2.0 (gifted SPS +offset,missing)

Another capital distribution restricted. It's applied twds Recap(CFR1237.12):Common Equity escrowed.#Fanniegate @TheJusticeDept pic.twitter.com/iBYeXpxeop

.jpeg)

Hard to watch Warrent Buffett's coulda/shoulda/woulda moment, referring to the purchase of Fannie Mae

20 years ago or close to it, when Fannie Mae was having some troubles.

I could have bought the whole company for practically nothing.

....

And I blew it.

the Fannie comments begin 4:30 mark

The SPS have no par value or face value.

When a stock doesn't have par value, it has stated value. The same concept.

For the SPS stated value, which is how the company values its securities on the Balance Sheet, they have used the Liquidation Preference value, as the Preferred Stocks have a Liquidation Right that is what makes this obligation be recorded on Equity, otherwise it'd be recorded on Debt. This is why it's considered an hybrid financial instrument.

On the other hand, the JPS do have par value of $25 or $50 per stock, and it's the stated value chosen to be recorded on their balance sheets. The par value coincides with the Liquidation Preference value.

Other companies use the Liquidation Preference value as stated value as well.

It represents the debenture that the companies have with their holders, as the underlying security in a Preferred Stock is an obligation. This is why their par value/face value/stated value isn't a symbolic amount ($0.1ps for instance) like in a common stock.

The amount ponied up by the common shareholders is reflected in other account: Additional Paid-In Capital account.

You keep on suggesting that the SPS and the LP are different things.

The liquidation preference keeps going up. The face value does not.

The cbo report monetizes the face value of the spspa.

Nothing is hiding. It is all there,

Ou! The plaintiff💩Joshua🤪Angel🤡strikes again:

"The SPS are products. This product required publication in the federal register, public notice and rule making, either prior to signing the SPSPA or after a temporary approval for emergency purposes."

"Ano" was humiliated on the Fanniegate hashtag.

We stand up for DeMarco.

Our hero.

He counted DeMarco's 210-day FVRA limit,but hid that July20,2011 is also a Final Rule:

— Conservatives against Trump (@CarlosVignote) January 14, 2024

-CFR1237.12

-Lamberth rebate=capital distribution.

He rather go rogue w/ staged email pro-Nationalization.

Others:"Release=Privatization"

Anyone could become conservator before HERA.#Fanniegate https://t.co/sbveoU2wYg pic.twitter.com/cVGeTIlKpi

S.Thompson:

"We're waiting for Congress to decide the future of the GSES."

Remove their privileges" was written in the very 2011 UST Report to Congress, in light of the "recommendations on ending the Conservatorships", at the request of the Dodd-Frank law of 2010, and with regard to a second privilege removed "Ending the capital advantages"...

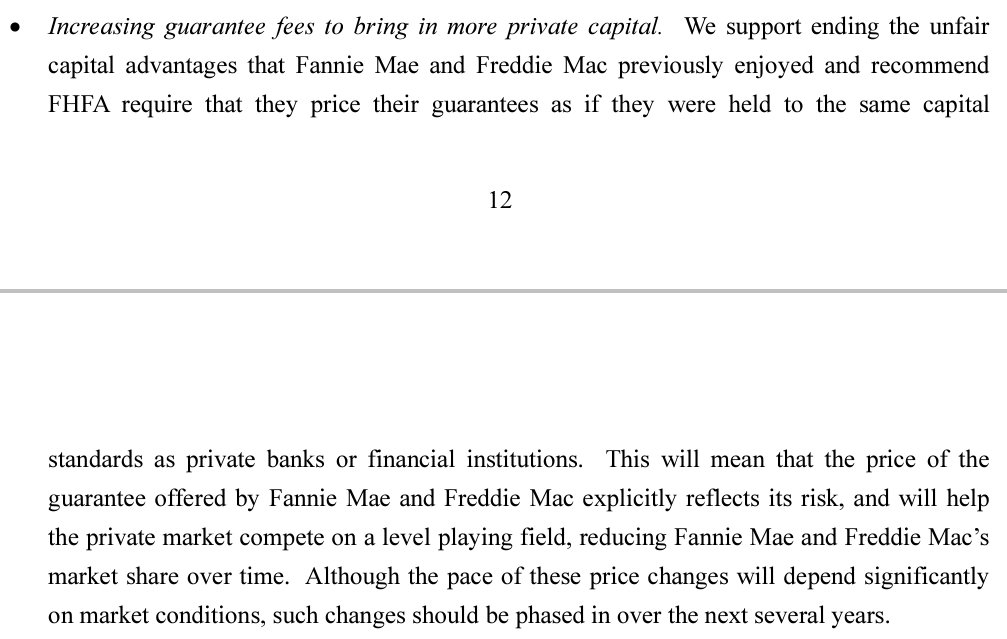

For the new the Basel framework (a back-end Capital Rule: effective after the Transition Period to build capital, not before as usual), FnF needed to charge a level of guarantee fees that reflect their risk.

Representative Ogles was reprimanded with body-language.

This image captures the moment, when she raised her hand several times at the end.

Another example of the Telephone game by Mr.Ogles was seen in the same exchange with secretary Fudge.

5 hour, 11 minute mark.

Are you seeing HUD prioritizing illegals over Americans?

We do not. The law specifically says that we cannot do it.

On your own record saying that the law states illegals cannot get set vouchers.

I'm not saying that in that exact way.

Rep.Ogles was reprimanded for attempting to pass the Conservatorship off as Nationalization.

Magnificent response by HUD secretary Fudge last Thursday to the representative from Tennessee, Mr. Ogles.

She had to repeat three times that FnF have plenty of capital to lend, because the representative, as a way to endorse stock offerings to the hedge funds, was calling the release from Conservatorship "privatization" and using as excuse, that the private capital raised is what is necessary for lending and to have impact on rents and mortgages.

For instance, stock offerings addressed to the controversial hedge fund manager from Tennessee Tim Pagliara, who set up a phony Association of Shareholders "Investors Unite" to rip them off (Warrant, 10% dividend, swap Ps for Cs, gifted SPS hidden and Shareholder Rights advocate when there is no need, as our rights and powers are very well preserved momentarily by the conservator, which translates into multiple stock offerings)

Mr. Ogles:

With more increase in privatization of the GSEs, we would see more available capital on the market.

If the GSEs were privatized and they had access to private capital that they can, in turn, lend.

Because part of the solution is more homes, the GSEs providing capital into the market, would that not be part of the solution, not a silver bullet, to fixing the housing crisis and the economy?

I do not believe so.

"The GSEs right now have about 6 trillion dollars. They have plenty to put resources into the market...."

I'm just saying that there are resources and they are now, for them to do the lending that we needed to have done.

If we find again impediments with the GSEs as it relates to HUD and there is a correlation there, we will certainly reach out.

That would be great.

Jesus! Who is this guy?

(*)100% CCF for their UMBSs. Commingled Securities? 50%.

First of all, "off-balance sheet" doesn't exist if later FnF present the financial statements on a consolidated basis and subject to a 100% Credit Conversion Factor (CCF): how external exposures are reflected on the balance sheet.

So, any Special Purpose Vehicule (SPV) like today with their MBS Trusts, is never really "off-balance sheet" if their accounts show up on their Balance Sheet.

By the way, the SPS LP increased for free that is absent from the Balance Sheet ($118B) is simply fraud, as they must appear, like the initial $1B gifted SPS that does appear, along their offset (reduction of Additional Paid-In Capital account back then. Now, reduction of Retained Earnings account).

Yet, there is always a shill calling the missing SPS "off-balance sheet", like kthompt19 and Glen Bradford with LuLeVan, to provide the alibi for the Financial Statement fraud with its absence. Even if that were the case, these SPS and their offset must be shown on the Balance Sheet once the accounts are presented on a consolidated basis.

Just say that you don't understand what "on a consolidated basis" means, another basic financial concept that you should know, more if you are a plaintiff.

It'd prove that the Common Equity is held in escrow with the aforementioned offset, in order to comply with the CFR 1237.12 (Recap.), and that FnF are not building regulatory capital nowadays (Ackman and his subordinate Bradford: "FnF continue to build capital")

Biden/FHFA/Treasury 'ordering'/setting up for F&F to purchase mortgages/mortgage securities off-balance sheet like they did in the '90s and 2000s up until Conservatorship.

The ones hiding information are the corrupt litigants.

But, no worries, the information covered up is publicly available, as they are the laws, rules and basic financial concepts, like "Dividends, a distribution of earnings, not interest payments".

You are the guy saying "NWS" instead of "NWS dividend", and "interests" instead of "dividends", pro se plaintiff.

Most transparent ? 11,000 GSE documents are still locked under presidential privilege for 12 years now. They are just some discussions on locking up the GSEs. Release them all now, people should know the truth.

Warning notice⚠️.The document with a Plan of Allocation will trigger a felony that cannot be unwound.

Scheduled for January 17th, a court brief where is laid out how the capital of FnF will be formally distributed among some Equity holders and a bunch of Wall Street law firms, at a time when there is a statutory Restriction on Capital Distributions in force (U.S. Code § 4614(e))

Neither the use of the judge's order as alibi, nor later the FHFA's response in opposition on January 31st, would relieve the litigants and the FHFA of the fact that a formal felony would have been committed.

The abuse of Court process will end up badly.

This isn't like all the prior felonies, where the litigants might play the fool and claim that they knew nothing about a Separate Account plan and the FHFA would reply: "Zing! I used the conservator's Incidental Power. Funny, right?". Therefore, only charges of stock price manipulation would be brought, with a monetary penalty (Punitive damages). It's one of the 8 Securities Law violations during conservatorship.

This time is an outright felony of breaking the law, written in formal document, and, where the FHFA can no longer claim that there is a Separate Account for this capital distribution, like occurred with the dividends and SPS LP increased for free, that is holding the Common Equity in escrow (CET1), in order to comply with its Rehab power as conservator: Put FnF in a sound and solvent condition.

This capital distribution with the Lamberth rebate, won't be recovered unwinding some scheme down the road. Charges of conspiracy and others would begin to pour in.

This document "Plan of Allocation" will be here to stay, for the world to see. Regardless that the final disbursement might be stopped on the last minute. The felonies won't disappear.

We would be playing in a different dimension, with crippling liabilities that I won't enumerate.

It's pretty obvious to think that they seek "an obligation to be honored", like the dividend declared but not paid the day of Conservatorship.

This time won't work. The law is quite clear and they can't use the JPS contract (prospectus) like before.

https://investorshub.advfn.com/uimage/uploads/2023/4/24/pixlkIMG_20220419_070019.jpg

This WARNING NOTICE was issued yesterday on the Fanniegate hashtag.

THE JAN 17 PLAN OF ALLOCATION DOC WILL TRIGGER A FELONY THAT CANNOT BE UNWOUND

— Conservatives against Trump (@CarlosVignote) January 11, 2024

So far, capital distributions(Divs/gifted SPS)hold Common Equity in escrow to uphold the exceptions to the Restr on Capital Distr +Rehab Power +Inc Power.

FHFA's Jan 31 response, irrelevant.#Fanniegate

There is no such thing as "perpetual Conservatorship".

The U.S. Treasury was directed in the Dodd-Frank law of 2010 to put an end point to the Conservatorship, and it attached to a 3-option Privatized Housing Finance System revamp (2011 Report to Congress), with a recommendation to increase the guarantee fees that correspond to this Basel framework for capital requirements.

A law and a Report to Congress are the essential formalities under the Rule of Law. The plotters want to substitute it for chit-chatting.

This doesn't mean that FnF wouldn't be released until they are fully capitalized, meeting the corresponding thresholds.

So, the Treasury wrote the endgame, not the exact end point.

Yet, here we are with the Common Equity that keeps on piling up, in accordance with the law.

Currently, with a CET1 > 2.5% of Adjusted Total Assets in both FnF, it seems that the goal is to get rid of the unwanted JPS holders before the announcement of a Housing Finance System revamp (compliance with Tier 1 Capital > 2.5% of ATA afterwards -ERCF-)

No one cares about the reasoning behind. Blame the FHFA in its capacity as conservator that continues to act "in the best interests of FHFA" (remember: "authorized by this section"), both with the Separate Account plan and now with an extended Conservatorship.

The important thing is to don't lose track of the numbers that later are reflected in the adjusted Fair Value of each stock class. And, the key, we will never allow the JPS holders to get rebates out of pity. At least, not with FnF's money.

All the Equity holders deserve a compensation for Punitive Damages. A claim against the DOJ as vicariously responsible of the FHFA's actions, and against the corrupt litigants and their accomplices with the Government theft story.

Quit peddling your "Nationalization" and "wind down" deranged diatribes, aiming to manipulate the stock prices and change what is clearly set forth in the law, rules and basic concepts in finance (Dividend, a distribution of Earnings. You need a positive balance for its distribution, in the Retained Earnings account. Today: Adjusted $-216 billion)

FnF are compelled to buy 3-month delinquent mortgages from their MBS Trusts and place them in their Retained Portfolio, so the foreclosure prevention actions start.

It seems that Bloomberg heard something like this and it decided to run the hoax of FnF buying toxic mortgages from the banks in the article that the footman of Pagliara, Guido, posts here regularly.

More 💩fan strategy to taint the atmosphere, like the pro se plaintiff who writes here like mad with 20+ aliases.

You don't need to quote the controversial Howard to debunk it. Had FnF purchased toxic mortgages from the banks, it would have showed up in their Delinquency rates. But, as the former CEO of Freddie Mac, Haldeman, said:

Freddie Mac holds a disproportionately small percentage of seriously delinquent mortgages...Freddie holds almost one quarter of all the mortgages outstanding, but only 10% of all serious delinquencies as of March 31, 2010.

I rephrase it: a Liability with Treasury is negative ($-134.5B), because first the Fed has to reduce this Deferred Asset (it should have been SPS), in order to start the true Liability (positive balance) with remittances due to Treasury, which are the figures that we were accustomed to see before.

The Federal Reserve's Deferred Asset is evidence of the Separate Account in FnF.

Deferred Asset and SPS are a similar concept: a debenture with the Treasury. This is why its Deferred Assets are: "Liabilities: Earnings remittances due to Treasury". Currently at $-134.5B as of January 3rd, 2024.

.png)

Like the SPS, whose underlying security is an obligation in respect of Capital Stock (source: SPSPA), like all the Preferred Stocks. That is, a debenture with the taxpayer that must be repaid asap (obligation = compromise of repayment). This is why all the Preferred Stocks are redeemable at the option of the issuer by definition.

And same mechanism for its repayment, as we can read in the definition of this Deferred Asset that appears on the Fed's web site:

It represents the amount of future Net Income that will need to be realized before remittances to the Treasury resume.

A #FED IN CONSERVATORSHIP

— Conservatives against Trump (@CarlosVignote) January 10, 2024

Upon operating loss,instead of:

-Need of SPS purchases upon neg Net Worth(FnF),when the NW<$42.8B.

-SPS,a fraudulent DA.

-SPS being repaid as the Common Equity (Net Income) increases (FnF),what is reduced is the DA.

Hence the definition of DA.#Fanniegate https://t.co/encMou9pfw pic.twitter.com/s8NSvx7mWk

Quit saying "NWS" instead of "NWS dividend", will ya.

And that it was authorized by the SCOTUS, without elaborating more.

because the NWS was legislatively authorized (per SCOTUS)

Don't mistake the 4th amendment of the SPS Certificate, dated April 13, 2021, for the 4th amendment of the SPSPA.

Because it's the fourth time it got amended. Knucklehead.

https://www.fhfa.gov/Conservatorship/Documents/Senior-Preferred-Stock-Agree/FNM/SPSPA-amends/FNM-Fourth-Amended-Restated-Certificate-04-13-21.pdf

After oral argument was held in this case, the FHFA and Treasury agreed to amend the stock purchasing agreements for a fourth time.

FnF have 1.25%-1.50% Capital

Remember also that, presumably, FnF appear as defendants (now illegally) aiming to settle the 8 Securities Law violations confidentially directly with FnF, once the Conservatorship is over and FnF recover their powers to carry out this deed.

At a time when there is a settlement proposal of these wrongdoings on social media with all the Equity holders, worth $4.8B., that also serves as compensation for Punitive Damages, and against the DOJ as vicariously responsible of the FHFA's actions.

Replica of the settlement reached by PwC, as auditor of Freddie Mac, in 2016 with some investors, we were told. Which sounds like a big lie and it was simply a trial balloon to teach us that, with a confidential settlement, not even the judge can see the terms of the settlement.

What a coincidence that a former PwC executive (the same individual at Mr. Crow's luxury retreat?) just landed as member of the BOD of Fannie Mae.

This is why the controversial Sheila Bair (she formed part of the conclave that made the decision of Conservatorship, according to a WSJ article on d-day: "top banking official", to later show up as chairman of the Board of Directors of Fannie Mae, pretending that FnF are managed by the FDIC, just like the failed 1989 RTC (Public-Private Partnerships with Wall Street), where the FHLBanks' Funding Corp invested in, that saddled the taxpayer with losses ($30B through the purchase of the Refcorp bond issued by Funding Corp, where the rogue FHLBs have only paid interests when their SEPARATE ACCOUNT provision was for "the repayment of principal"; and $18.8B invested directly in RTC)), one year ago surprised us with her dramatic appeal to release FnF from Conservatorship, despite their shocking $402 billion capital shortfall over minimum Leverage capital requirements.

They seek the release just to settle their 8 Securities Law violations (gifted SPS absent from the balance sheets, SPS increased instead of issued, etc.) confidentially with FnF.

By the way, you are also omitting that the U.S. Treasury is a party in the Lamberth court too, represented by the DOJ, according to Pacer. This compels the DOJ to find out everything happening in the Lamberth court.

Another honest mistake, Glen Bradford - LuLeVan -JOoa0ky?

Importantly, the government and Treasury are not defendants in Lamberth,

The claim arises from the retention of securities, not from the purchase. Thus, the date of issuance or purchase that you mention, is pointless.

these purchases occurred prior to the conservatorship, when FHFA did not even exist.

FHFA must assume the legal defense in conservatorship on behalf of the real defendants, Fannie and Freddie, precisely because FHFA is acting as conservator.

Not a coincidence the omission of FHFA "defendant" in its capacity as conservator, in the post of LuLeVan that I was replying to before:

The defendants in the Lamberth jury trial are neither the government nor Treasury, but the two companies, Fannie and Freddie.

The two companies (FnF)

have 1.25%-1.50% Capital

Navy Hedge Fund at it again.

it's ONLY "$Retained $Earnings" - $Court Order $Damages and ....

... THE $TRUMP TRADE ...

The Credit Risk Transfer (CRT) operations are another fiasco.

Following Mnuchin's slogan:"The taxpayer be appropriately compensated"

— Conservatives against Trump (@CarlosVignote) January 8, 2024

That's a different Charter.

Attempt to replicate the 1989 RTC (PP Partnerships) where the FHLBs' Funding Corp invested in, that saddled the taxpayer w/ losses:

$30B RefCorp bond

$18.8B invested directly in RTC pic.twitter.com/p72VSm9Gr8

Did you just say "stock buybacks"? Capital distribution, restricted.

I think that FNMA is rebuying it's [sic] own stock shares.

"...except to the extent the Director determines is in the interest of the conservatorship"

Do you happen to know the European farmer G.Bradford-LuLeVan?

If dividends are restricted and unavailable Earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts, you have to be smart enough to think that maybe there is other side in this deal.

More if the exception to the statutory Restriction on Capital Distributions (Dividends; today's gifted SPS; payment of Lamberth damages) is the repayment of the SPS (12 U.S. Code § 4614 (e)) and, later on, DeMarco enacted on July 20, 2011, another exception: for their Recapitalization (in a Separate Account, obviously), CFR1237.12, contemplating the case when the SPS were fully repaid.

Both actions help the conservator fulfill its statutory goals: Put FnF in a sound and solvent condition.

Above all, taking into consideration that the conservator's Incidental Power (which, by definition, are powers without an express grant of authority but useful to help it fulfill its main power) allows it to mislead and carry out a Separate Account plan: "Take any action authorized by this section (Rehab Power), in the best interests of FnF or the FHFA".

We can't accept people playing the fool and profit from it:

Paid Dividends under conservatorship ??

The Supreme Court simply authorized the Separate Account plan, that I remind you that Justice Alito highlighted that it's rehabilitating FnF.

The Separate Account isn't in the interests of FnF, pointed out in the same sentence, as seen in their horrible ERCF tables (Adjusted $402B Capital shortfall over Min Leverage Capital requirement) and Balance Sheets (adjusted $-216 billion Accumulated Deficit Retained Earnings accounts combined) and it's devastating for the shareholders' interests, also pointed out, as it makes the stocks to plummet, but, at some point, it'll have to be unwound to comply with his prerequisite of financial rehabilitation of FnF.

In this world, that occurs on-balance sheet.

The add-on "and the public it serves" out of the blue, would allow the Congress to keep the $15 billion owed to FnF for the Making Home Affordable plan, called "Obama's program' but fully paid for by the FnF Equity holders. Also, it authorizes all other schemes that use FnF for public policies, when it was Ginnie Mae the one that kept the special assistance functions in the 1968 Privatization Act and its spin-off from Fannie Mae.

Good! But at some point, it'll have to stop.

If you don't know what "rehabilitation" means, just read this excerpt taken from the preface of the famous Final Rule "for the transparency of the Conservatorship", on July 20, 2011, where FHFA calls it "statutory goal" referring to the conservator's Power, and an explanation brought up to justify why the capital distributions are restricted when FnF are undercapitalized, in a question about the payment of Securities Litigation judgments, now in the Lamberth court.

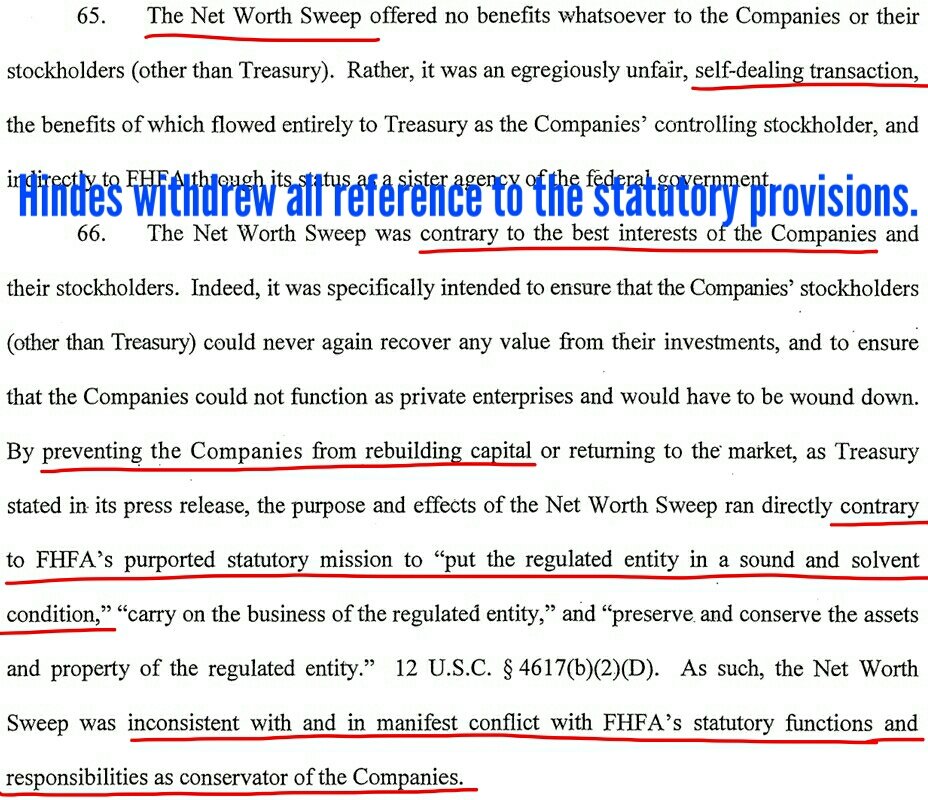

This statutory goal was called "statutory mission" by Gary Hindes but, surprisingly, he removed this remark in an amended complaint.

He was told that challenging the NWS dividend but not the 10% dividend, is insane, as both represent the same reduction of Core Capital and thus, a breach of the statutory mission that he was complaining about only with the NWS dividend.

He was told to change it and that the SCOTUS was going to be activated soon, aiming to mess around with the Incidental Power better, after the Sixth Circuit U.S. Court of Appeals was tasked with twisting this Power: "Put FnF in a sound and solvent condition", commented on Wednesday, with: "The return to Profitability and the Funding Commitment will do it".

A SCOTUS talking of "beneficial to the Agency" instead of what is written: "best interests of the Agency", to transmit the idea of monetary benefit, when it's about activities, etc. and play the hedge funds' game of stock price manipulation.

This isn't about throwing ideas at the wall.

The resolution of Fanniegate is upholding the law, rules and basic financial concepts.

1st. The Separate Account plan.

2nd. A refund of the CRT expenses, net (barred in the Charter Act, both in the Credit Enhandement clause and the Fee Limitation clause in the case of operations with the Treasury)

3rd. A refund of the PLMBS lawsuit settlemenent on behalf of FnF, net of attorney fees.

The only negotiation possible is about the compensation for Punitive Damages:

It's been requested a 0.25% IRR on a JPS par value, during 15 years.

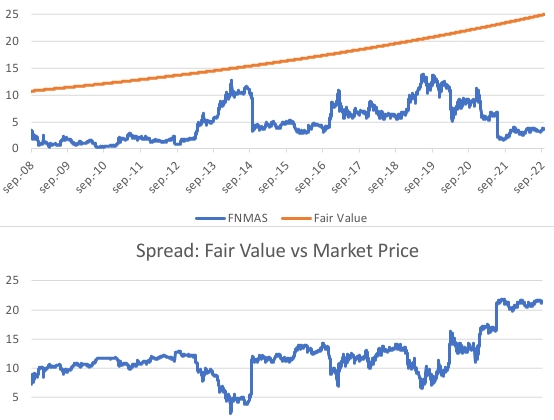

Calculated with a rate of 0.5%, because it's the spread over Treasuries under the Charter's original UST backup of FnF, for the estimated total 1.8% cumulative dividend on SPS that the UST has earned, until the SPS were fully repaid (end of 2013/2014). And an interest rate on half a JPS par value, which coincides with the average spread Fair Value vs Market Price, the real damage caused: the Separate Account plan prevented the stocks from trading at their fair value all along.

The amount of interests is $0.97 per $25 par value JPS. A common stock matches a $50 par value JPS because their fair values are closer.

Then, there are three rounds:

1- Agaist the DOJ for the 8 Securities Law violations during conservatorship: SPS increased instead of issued, to evade the December 2009 deadline on purchases; Stock price manipulation; Gifted SPS and their offset, absent from the balance sheet; Etc.

2- Against the DOJ again: the Deferred Income accounting. There was an accounting change in early Conservatorship with the consolidation of the MBS trusts that eliminated the prior accounting of Guaranty Obligation, but the FHFA later chose the same scheme with the Deferred Income. It should have been called Delivery Fee (before the product is launched) instead of upfront g-fee, and problem solved. It's valuable core capital already collected, that remains recorded on Debt. In a financial company, this is unacceptable, as it's subject to regulatory compliance with regard to capital levels.

The common shareholders waive these two claims in the case of resolution "as is" or "takeover" scenarios, not in "Taking", for having chosen the option more favorable.

3- Against the corrupt litigants that filed frivolous lawsuits covering up many statutory provisions and financial concepts. Also against their accomplices writing about a phony Govt theft story in formal documents, aiming to tumble the stock prices. This way, "everyone would be standing shoulder to shoulder", as Pagliara said when he shamelessly asked for a swap JPS for Cs, as a result of both stock classes trading at rock bottom prices, when each stock class has its own stock valuation, an the common stocks are affected by the Warrant and the Separate Account, not about the suspension of dividend payments, because they are kept by FnF and that's Common Equity.

You can't change the financial concepts and trample the Rule of Law, just because you are annoyed with the outcome. If someone has a problem with stock valuation, please attend a Finance Course, like everyone else has done before.

Can you imagine that the corrupt litigants are now in charge of "negotiating" a resolution with the FHFA? After both have deprived the Rule of Law of its meaning, with the frivolous lawsuits and crooked judges playing along, so now they stage a negotiation "cattle market-style" without any binding rule. The shareholders can throw in a cow and two goats.

Or is it a chess game? "Gimme this and I give you that. If you do this, I do that. ....You do that... I do that. ...Do that...do that. Dothatdothat..."

Or is it a tennis match: "Match point now in the Lamberth tennis court", where is scheduled for January 10th the sought-after "negotiation table" with the attorney for Berkowitz, David Thompson, achieving his plan: "The government has to come to me", a remark made in a conference call hosted by Pagliara many years ago (tape removed from the internet)

Hundreds of pages of legislative wording, rulemaking and financial concepts thrown in the bin.

Now we play in the Mob's playground: lawlessness. Everything has been covered up or twisted, that has ended up with the accessories claiming on social media that the conservator "can do whatever the hell it wants".

Finally,🚨this comment from the plaintiff Bryndon Fisher might have sounded the alarm at the DOJ and the SEC.🚨

It could be the reason why the litigants have filed so many frivolous lawsuits in the U.S. Courts. They are mercenaries that just seek a big check in a negotiation with the Government, knowing that the Government has unlimited resources.

Brydon Fisher proposed to settle the Collins case before the Oral Arguments at the Supreme Court.

The attorneys are negotiating their check, nothing about the rehabilitation of FnF. This is why a penalty for Punitive Damages is of supreme importance (deterrence)

By the way, is it me or Ace Trader sounds a lot like the plaintiff Bryndon Fisher? He always claims that Collins brought the wrong claim because he is smarter and he can file a better lawsuit than the Fairholme Plaintiffs. Also he seeks a Cattle Market-style negotiation with the Government and, the last clue, he seems always annoyed with other posters, even when they agree with him. For instance, in this reply to a poster, to point out the same that the poster had said, but he makes it look like both were in disagreement.

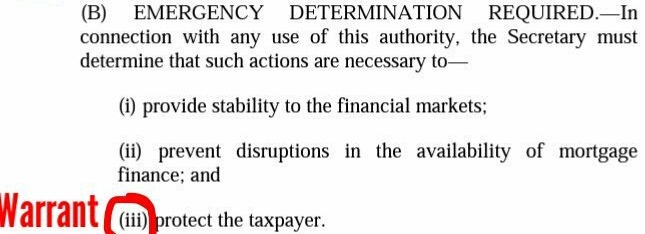

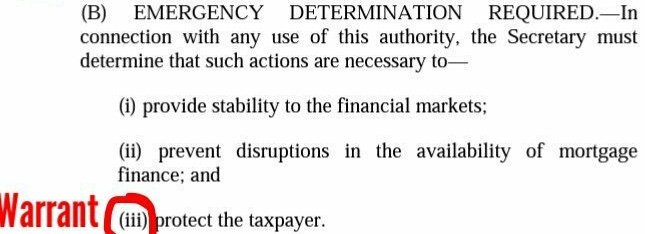

It seems that Fisher doesn't know that a collateral is a guaranty that ensures the repayment of a debenture (the underlying security in a Preferred Stock, is an obligation. Perpetual, but always redeemable at the option of the issuer.), like in our case, a collater "to (iii) protect the taxpayer". A security issued for free to evade this prerequisite on purchases by UST.

I know Colin’s brought the wrong case in front of SCOTUS for takings. I have gone around and around today .

People keep changing the subject of my posts rather agree they could take many options .

My posts today again were about the Governments self dealing for its best interests and disregard for shareholders.

I thank you for your knowledge and posts and agree a lot of your posts but let’s not go off in another discussion or direction other than all I stated was today . I’ve kept on topic and everyone else keeps changing the subject.( the Governments shady actions towards Fannie and Freddie and shareholders.

and how if they release them on what terms.