Friday, January 19, 2024 1:53:44 AM

I'm not surprised to learn that there is a Bloomberg article endorsing "recapitalization and release". The recapitalization has already happened. 15 years in the making.

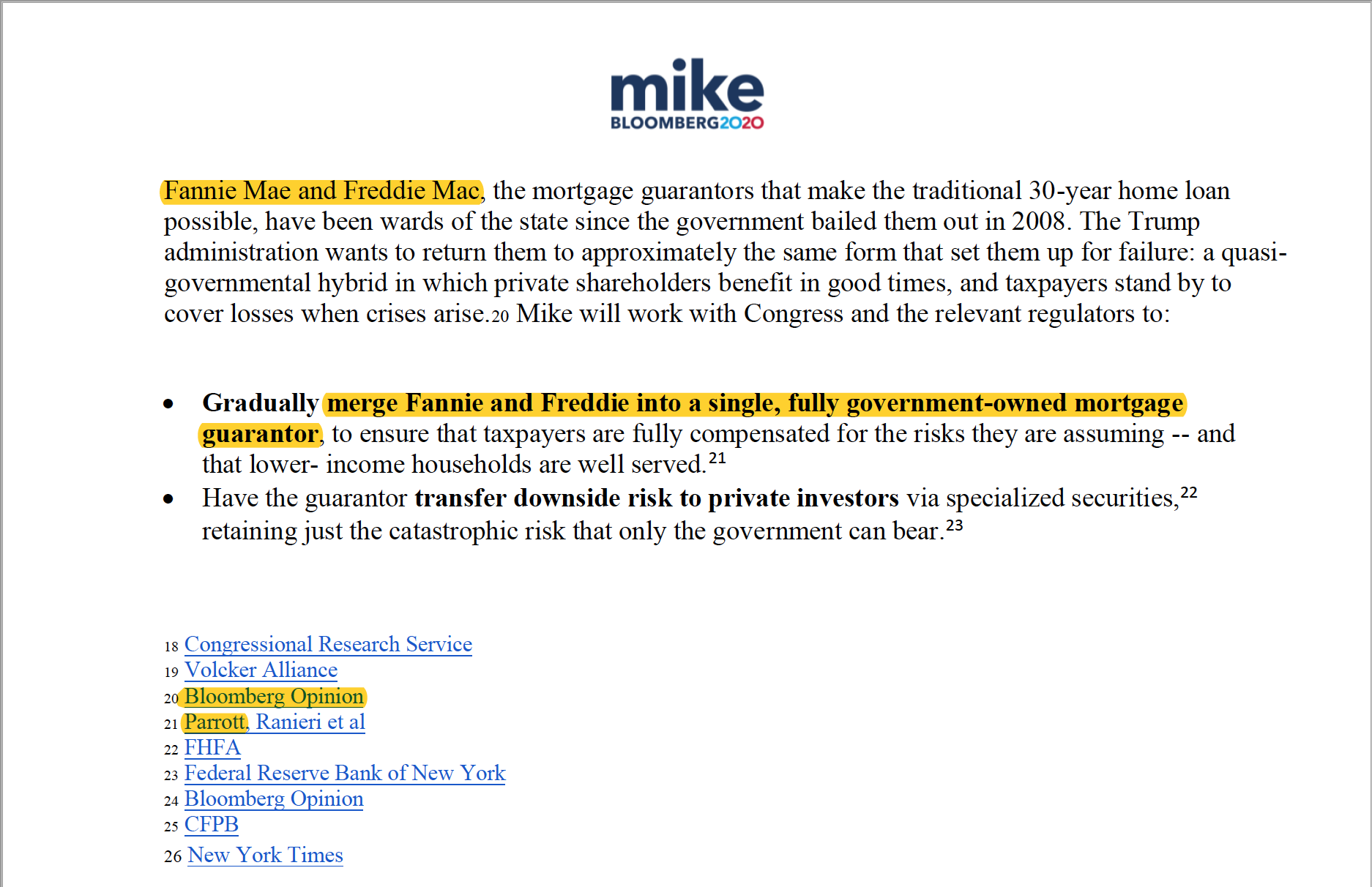

We know that Michael Bloomberg proposed a merger FnF and the nationalization of FnF thinking of China (as if this was even an option), with a Government Explicit Guarantee on MBSs. The United States isn't the Communist China.

Bloomberg is skewed toward the Wall Street firms that pay him the Bloomberg Terminal subscription rates that have made him billionaire. So, he owes them big time.

It's not a coincidence that the Bloomberg's take about a merger FnF, is the same as the Wall Street executives, according to their spokesperson, Gasparino, in 2010:

The report citing Wall Street sources said that the two mortgage firms will be combined into one agency.

Gasparino was the first one to conceal the mandate to the Treasury in the Dodd-Frank law of 2010, of "recommendations on ending the conservatorships, no later than January 31, 2011". And the subsequent UST's 3-option Privatized Housing Finance System endgame of Conservatorship.

Gasparino said that regulators purposely did not include Fannie and Freddie in the recent Dodd-Frank financial regulatory reform package due to a number of issues.

Article that echoes Gasparino's pro-Wall Street stance, here.

Also, it isn't a coincidence that two days ago we learned that Fannie Mae has terminated the lease contract it had for its headquarters in Washington DC.

The day the lease contract was signed, it was published that it comes with "the ability to exit a lease early in the event Fannie Mae is significantly changed".

The Goldman Sachs alumni, Sandra Thompson, attempts to force a merger FnF, as mandated by Wall Street, at the same time that she is colluding with them in the Lambeth court to settle the Fanniegate scandal as a Govt theft story case, when that's not what has happened and it's against the Supreme Court's stance "rehabilitate FnF" -the Marxist way, for the extortion of FnF in the meantime and a Separate Account, but the rehabilitation must be satisfied when the External Position (Common Equity held in escrow) is posted on the Balance Sheets, as Justice Alito's and judge Willett's prerequisites: "authorized by this section" remark.

This way, today's adjusted $-216 billion Accumulated Deficit Retained Earnings accounts combined, turns into a posting of $236B, after the retirement of the $11B Treasury Stock (stock buybacks).

The CET1 deep in the red today (ERCF tables pursuant to the 2021 Capital Rule) turns into a CET1 > 2.5% of Adjusted Total Assets, enabling the redemption of the JPS at their redemption value (par value). Their fair value today, as it fetched the par value when it was determined that the dividend payments could have been resumed, under the Table 8: Payout ratio, of the same Capital Rule (regulatory capital > 25% of their Capital Buffers). For instance, that threshold was met with the Q3 2022 in Fannie Mae. One year earlier in Freddie Mac. But the non-cumulative dividend was kept suspended under the conservator's Incidental Power. The odds are that the FHFA wanted to get rid of unwanted Equity holders, unrelated to Housing Finance, like occurred with the FHLBanks expelled through regulation, after being called "captives". Source.

Finally, it's worth remembering Geithner's tough stance against Wall Street on regulation, in July 2011, a few months after his Privatized System Housing Finance reform, endgame of Conservatorship, and at a time when China's VP Wang Qishan was pressuring him to enact a Govt Explicit Guarantee (Bloomberg Charlie Rose's interview Geithner-Qishan in May 2011. With a petrified face, Qishan said to Geithner: "Housing hasn't been addressed yet"):

Don’t listen to banks…Their interests are not aligned perfectly with the broad interests of the American economy. Their job is to evade, or avoid, or weaken, any constraint on their ability to operate our job to make sure we’re protecting the american economy from the risks they inevitably take.

And two days later:

The president did not want the new rules to end up being written by those who brought us to the edge of catastrophic financial failure.

Source.

Nowadays, we should say: "Don't listen to banks and Bloomberg".

The single security UMBS, is a standardized product to boost its liquidity, so more competitors step in. It has nothing to do with a single entity.

The commingled securities allow to bring in more competition as well.

The more Utility Model, the more manipulation of the economic cycles and secured deals for the hedge funds under the guise of normal operations, for the extortion of a single entity, that I guess, will happen to have many Goldman Sachs alumnis serving at the BOD, like Freddie Mac in 2008.

Zero sense of the current legal status of FnF, private corporations in a Conservatorship. FHFA Conservatorship, but it could have been anyone before HERA. This slams Rep. Maxine Waters' and her chamber investor's, Pagliara (through his subordinate Guido), stance: "Federal Government Conservatorship", in an attempt to switch it for a Nationalization.

Or a NYT reporter: "Their name starts with Federal, no?"

They know that, in the Separate Account in accordance with the law, they will have to pay us damages for stock price manipulation.

No one wants to pay damages, but they should have thought about it in the first place.

Panther Minerals Inc. Launches Investor Connect AI Chatbot for Enhanced Investor Engagement and Lead Generation • PURR • Jul 9, 2024 9:00 AM

Glidelogic Corp. Becomes TikTok Shop Partner, Opening a New Chapter in E-commerce Services • GDLG • Jul 5, 2024 7:09 AM

Freedom Holdings Corporate Update; Announces Management Has Signed Letter of Intent • FHLD • Jul 3, 2024 9:00 AM

EWRC's 21 Moves Gaming Studios Moves to SONY Pictures Studios and Green Lights Development of a Third Upcoming Game • EWRC • Jul 2, 2024 8:00 AM

BNCM and DELEX Healthcare Group Announce Strategic Merger to Drive Expansion and Growth • BNCM • Jul 2, 2024 7:19 AM

NUBURU Announces Upcoming TV Interview Featuring CEO Brian Knaley on Fox Business, Bloomberg TV, and Newsmax TV as Sponsored Programming • BURU • Jul 1, 2024 1:57 PM