Monday, January 15, 2024 3:12:05 AM

"We're waiting for Congress to decide the future of the GSES."

Robert continues to play the fool and drama queen "DeMarco stole all of our money!", saying that he knows nothing about the reasoning behind those words, it's complicated,.... Cover-ups is the bread and butter during conservatorship.

A few hours before and in numerous occasions, I had explained why all the FHFA Directors have repeated the same slogan:

Remove their privileges" was written in the very 2011 UST Report to Congress, in light of the "recommendations on ending the Conservatorships", at the request of the Dodd-Frank law of 2010, and with regard to a second privilege removed "Ending the capital advantages"...

For the new the Basel framework (a back-end Capital Rule: effective after the Transition Period to build capital, not before as usual), FnF needed to charge a level of guarantee fees that reflect their risk.

Source.

The UST recommended guarantee fee hikes to that end. Source.

Because this Report to Congress included a Housing Finance System revamp, bound for a Privatized System, in light of "recommendations on ending the Conservatorships", this is why the conservator repeats that it has "deferred to Congress the release from Conservatorship".

FHFA's DeMarco began to work on this Housing Finance System revamp right away: Congress hearing. May 25th, 2011.

The reason why Freddie Mac unveiled in June 2022 the Commingled Securities or Resecuritizations, which is a Catastrophic-Loss Reinsurance because the payment of the claim occurs upon bankruptcy of the other guarantor, as explained, for instance, in the Option 3 (image below) with regard of a Government Catastrophic-Loss Reinsurance. But it can be private Reinsurance for the options 1 and 2.

It wasn't unveiled to make FnF buy each other's UMBSs like nowadays, but to bring in new competitors.

Because we are at a point beyond what is a reasonable pilot program, what ST is doing nowadays with the commingled securities, is transferring revenues from one guarantor to the other under the guise of normal operation when there is no need, also known as extortion, which is what lies behind numerous schemes nowadays: CRTs, unbacked cryptocurrencies to raid the people's life savings, etc.

Another U.S. Federal Agency-sponsored scam.

Commingled securities as of November 2023 (monthly volume files):

Freddie Mac has issued $111B worth of resecuritizations using the collateral of Fannie Mae. $217B the other way around.

The net effect is that Freddie Mac is paying to Fannie Mae 9.375 basis points on $106B annually. Money tossed in the bin because there is no need for Freddie Mac to pay for reinsurance to sell its products (UMBSs).

Because these commingled securities aren't accounted for in their Guarantee Portfolios, it explains the bad numbers of volume posted by Fannie Mae (annualized -0.4% MoM in November, versus +2.4% in Freddie Mac)

The inexperienced CEO of Fannie Mae has found a new revenue stream with the extortion of resources in Freddie Mac, and there is no need to compete.

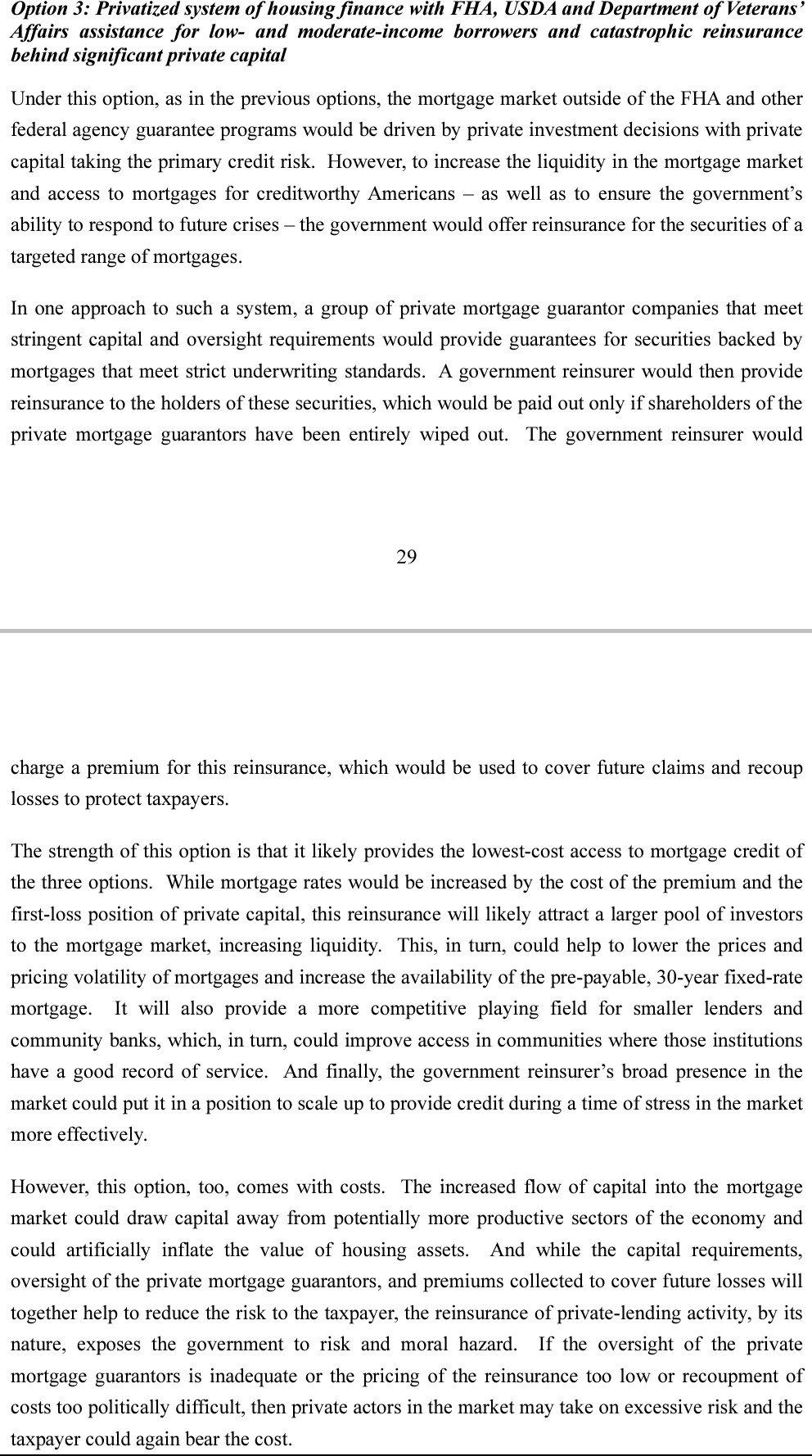

2011 UST's 3-option plan in brief:

1- Privatized Housing Finance System + targeted assistance: FHA, USDA, VA.

2- 1 + Govt guarantee in crisis.

3- 1 + Govt Catastrophic-Loss reinsurance.

Option 3:

Avant Technologies Engages Wired4Tech to Evaluate the Performance of Next Generation AI Server Technology • AVAI • May 23, 2024 8:00 AM

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM