Monday, January 08, 2024 2:49:27 AM

I think that FNMA is rebuying it's [sic] own stock shares.

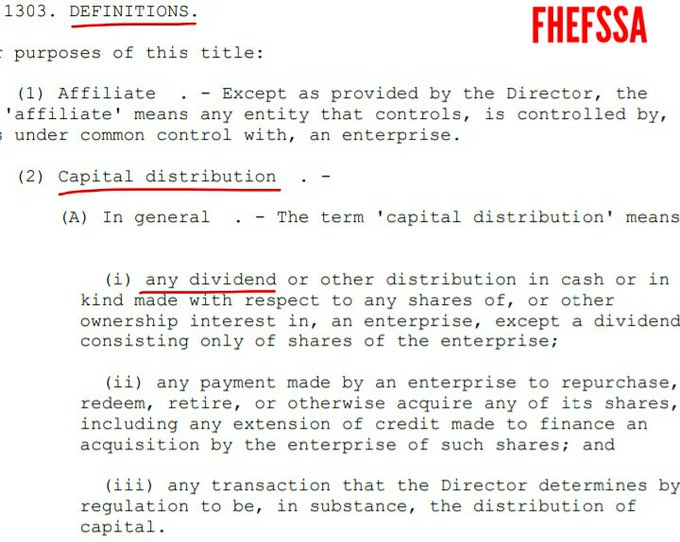

A capital distribution number 2.

12 U.S. Code § 4502 (5)(A)

This restriction is when FnF are undercapitalized IN GENERAL.

But, in the case of the Preferred Stocks, there is an exception in the law that has been used for the repayment of the SPS, with the exception (B) and the exception (A) that requires to raise cash in the same amount, it was achieved with the double-entry accounting when the Common Equity increased.

Net Worth increase = Total Comprehensive Income = Comprehensive Income (Retained Earnings account) + OCI (unrealized losses. AOCI account.)

Watch my signature image below to see how it worked in Freddie Mac.

This double-entry accounting Cash - Common Equity is what was sent to UST with a (phony) dividend.

If someone wants to repurchase SPS, it's done only with cash.

Remember that the corrupt litigants, besides agreeing with the 10% dividend, only required a refund of the excess cash payment, not the second leg of the double-entry: a posting in the Retained Earnings account (Core Capital) for the full Common Equity Sweep (Net Worth).

$0 Core Capital recovery with the frivolous lawsuits. Now they start begging for debt forgiveness, Zambia- and Argentina-style.

12 U.S. Code § 4614 (e)

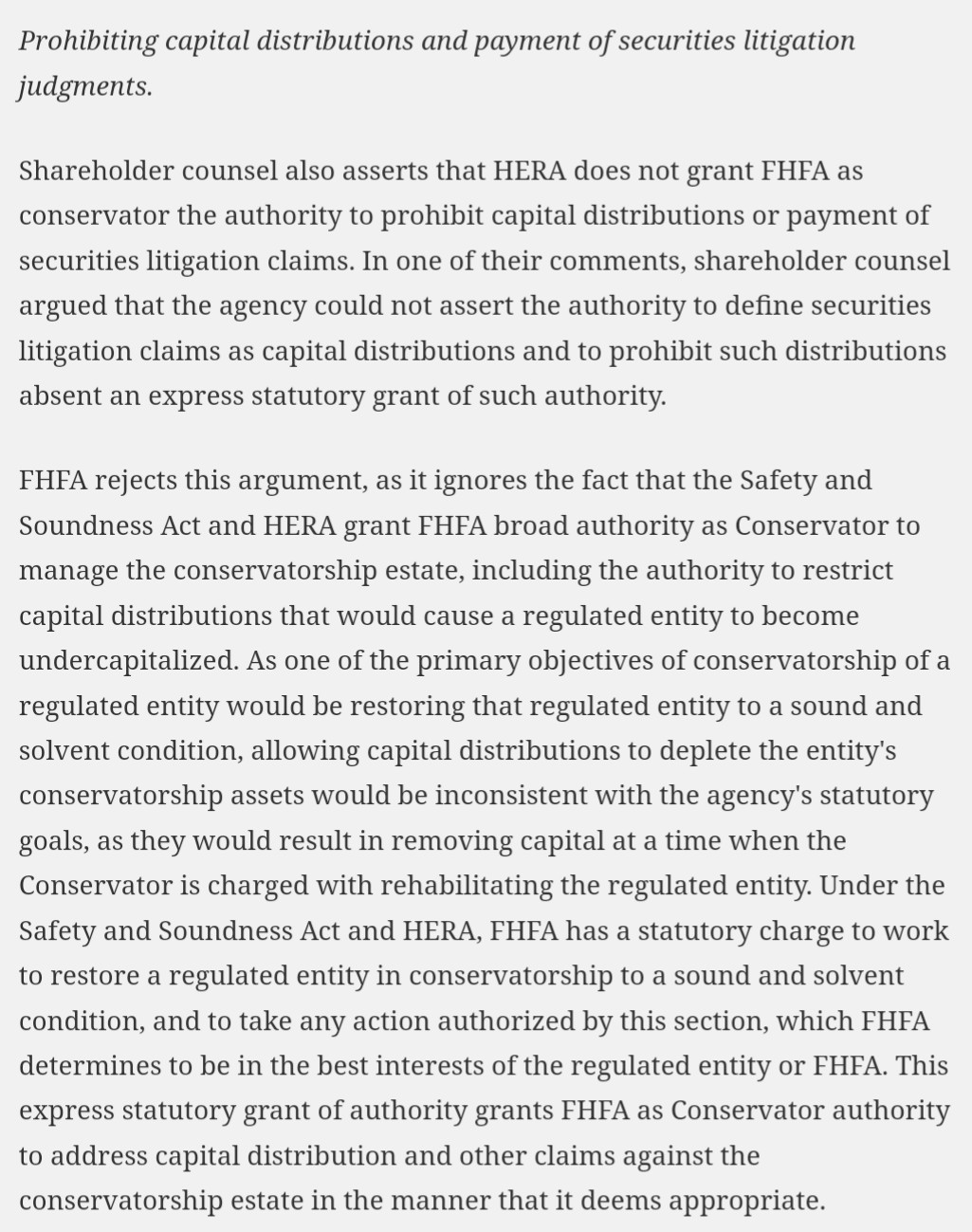

This definition of Capital Distribution was amended by FHFA in the July 20, 2011 Final Rule (12 CFR 1229.13) and we can read in the law that it was done with an express grant of authority, to include the payment of Securities Litigation judgments as number 3, now in the Lamberth court.

Then, the FHFA's afterthought through regulation (CFR 1237.13)

"...except to the extent the Director determines is in the interest of the conservatorship"

, is considered a bad joke, as presumably the FHFA director was referencing to its Incidental Power as conservator, which doesn't allow it to break the law at its will as most people wish for (another example, the CRTs are barred in the Credit Enhancement clause), because "any action in the best interests of FHFA" must be "authorized by this section", and it'd break its "statutory goal" (Rehab power), as the FHFA director pointed out, precisely for its prohibition, in the preface of the same Final Rule:

This amendment of the definition of capital distribution, at a time when there was no litigation, is considered a trap set by DeMarco to lure all the bad actors into frivolous lawsuits, that would, at some point, uncover what they've been covering up all along jointly with their counterparty, the DOJ attorneys, that the dividends and today's gifted SPS are capital distributions restricted too (definition of capital distribution number 1), and necessarily, the exceptions kicked off to make them lawful (reduction of SPS and recapitalization off-balance sheet), whether they want it or not.

More evidence if we see that there were no Earnings available for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts (adjusted $-216 billion as of September 30, 2023)

A Separate Account plan, in the best interests of FHFA (and the Treasury), 1989 FHLBanks-style:

.jpeg)

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM

VPR Brands (VPRB) Reports First Quarter 2024 Financial Results • VPRB • May 17, 2024 8:04 AM