Tuesday, January 16, 2024 7:04:38 AM

Wazee is the only case that challenges the SPS increased for free (NWS 2.0) in an amended complaint.

This attorney is also in the Lamberth court, filing frivolous lawsuits over the same issue: he covers up the Restriction on Capital Distributions and its exceptions, both in the 12 U.S. Code § 4614 (e) (Reduce the SPS) and the July 20, 2011 12 CFR 1237.12 that "supplements and shall not replace or affect any other restriction on Capital distribution by statute" and that statute is the 12 U.S. Code § 4614 (e) mentioned before (A follow-on plan. For their Recapitalization: exception 1, 2, 3 and 4)

This makes sure that FnF cannot distribute capital in the best interests of the taxpayers because it'd break the Restriction on Capital Distributions by statute. The "best interests of taxpayer" in the CFR 1237.12 can only be the Recapitalization of FnF.

🚨The key: both the reduction of the SPS and the Recapitalization in a Separate Account are recapitalizing FnF. Because the SPS are repaid with cash, not under the guise of cash dividends. You are depriving FnF of recording the Core Capital in the first place (double-entry accounting cash-Retained Earnings)

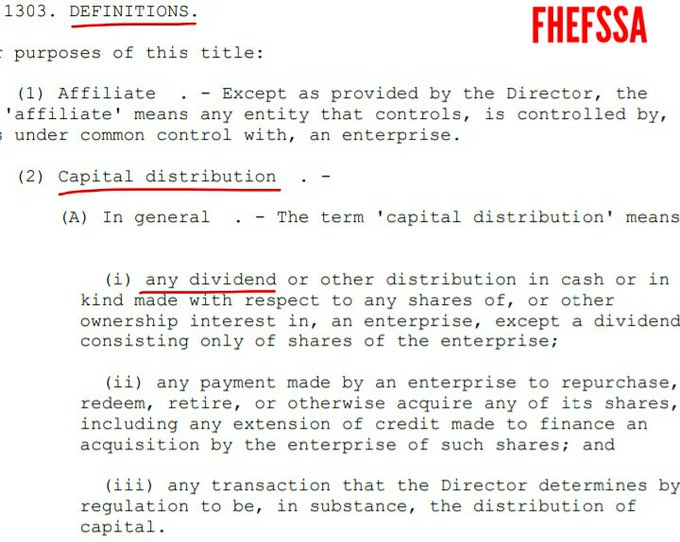

We can't allow the Fanniegate scandal to come down to a Sesame Street case, where we have to repeat over and over again the numbers 1, 2 and 3, with regard to the statutory definition of Capital distribution, amended also in the July 20, 2011 Final Rule, to include the payment of securities litigation judgment now in the Lamberth court covered up by the attorney Hamish Hume again.

Number 1. Any dividend and today's SPS LP increased for free in the absence of dividends.

Number 2. Stock buybacks and reduction of the Preferred Stocks.

Number 3. The payment of securities litigation claims (Lamberth court)

12 U.S. Code § 4502 (5)(A)

Amendment to include the Lamberth rebate in the number 3:

This tweet serves as appeal and it was sent to the DOJ.

WAZEE FILES NOTICE OF APPEAL

— Conservatives against Trump (@CarlosVignote) January 15, 2024

CFC case(Atty @ Lamberth court too)

In amended complaint,only one challenging today's NWS 2.0 (gifted SPS +offset,missing)

Another capital distribution restricted. It's applied twds Recap(CFR1237.12):Common Equity escrowed.#Fanniegate @TheJusticeDept pic.twitter.com/iBYeXpxeop

A Separate Account plan very similar to the one carried out by Sandra Thompson (FDIC) and DeMarco (GAO and UST) in the FHLBanks in 1989. With FnF, it continued for their recapitalization. Also, FnF cannot pay dividends (cumulative dividend on SPS). Restricted when they are undercapitalized. Whereas the FHLBanks paid interests. And the 0.299% spread over Treasuries was 10% in the FHLBs, whereas 50 bps spread in FnF (original UST backup of FnF) has been assessed at a weighted - average 1.8% cumulative dividend, latter netted out with the interests owed to FnF on the $150.9B due.

.jpeg)

Avant Technologies Engages Wired4Tech to Evaluate the Performance of Next Generation AI Server Technology • AVAI • May 23, 2024 8:00 AM

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM