News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

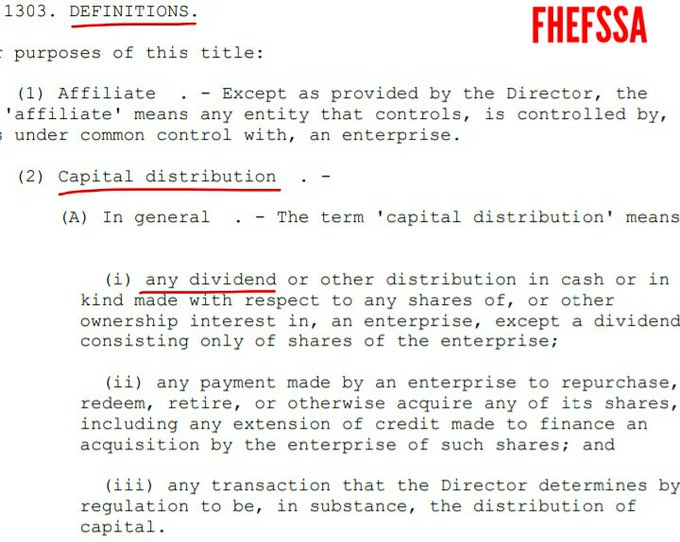

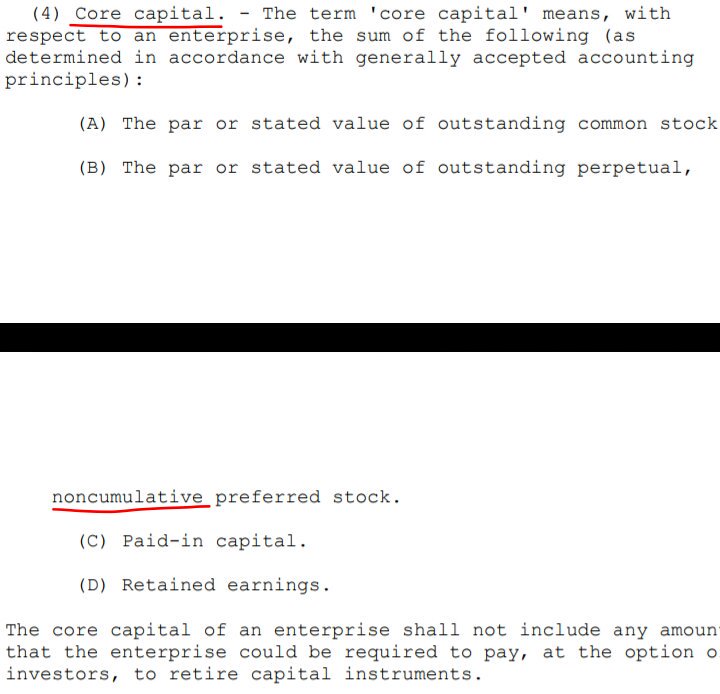

"Regulatory policy": ST, responsible for the absence of the Critical Capital level in the ERCF.

HERA amended the FHEFSSA's Risk-Based Capital requirement, the Minimum Leverage Capital level and allowed the FHFA to include new capital metrics like the CET1 and the Tier 1 Capital, along with the concept of Capital Buffers, but nothing about the Critical Capital level that remains as is: 1.25% of the Retained Portfolio and 0.25% of the off-balance sheet obligations (MBS Trusts), which is met with Core Capital.

The Critical Capital level triggers a Conservatorship, established for Critically Undercapitalized enterprises.

Now it's when

"regulatory policy, capital policy and financial analysis".

President, CEO and serves on Fannie_Mae's board of directors.

You can't make this shit up.

The same person holding the job of President and CEO has always been controversial and it's discouraged, as the President serves as a balance position to counter the power of the CEO.

The CEO is in charge of long-term goals.

The President is in charge of the corporate picture: costs, marketing, etc.

But a CEO serving on the BODs is even more controversial. The BOD oversees the management. This can't be done if a CEO is in the same table with other board members.

It could be one of the reasons of the Financial Statement fraud in FnF, with the SPS LP increased for free and its offset, absent from the Balance Sheets since December 2017 (not the initial $1B SPS LP issued for free and its offset with reduction of Additional Paid-In Capital account -Core Capital-)

, in order to peddle the lie of "FnF continue to build capital through retained Earnings", later echoed by the hedge fund managers like Bill Ackman and his clerk, Bradford, along with the FHFA director, ST.

We are witnessing how the CEOs of both FnF grab more power in order to conceal this fraud that, in turn, would unveil the prior Separate Account plan with the dividend payments, as both divs and SPS LP increased for free are capital distributions restricted, and the exceptions kick off to legalize them. It works as follows:

- Pay down the SPS (U.S. Code §4614(e)) and recapitalization outside the balance sheets (CFR 1237.12), with the dividends (assessments sent to the Treasury)

- Common Equity held in escrow, with the SPS LP increased for free, as we can see in this image:

Also in compliance with the FHFA-C's Rehab power.

We see that FnF build Capital Stock (SPS) not regulatory capital, and not even the FHEFSSA-invalid capital metric "Capital Reserve" (Capital Surplus in the Federal Reserve System).

Don't expect the FHFA to bring it up, with its long track record of breaking the laws: PLMBS, CRTs, artificial losses, etc. Actually the FHFA is behind this fraud, knowing that ST arrived at the FHFA in 2013 as Deputy Director in charge of "regulatory policy, capital policy and financial analysis". Jackpot!

The PLMBS rallied after FnF were placed in Conservatorship, as we can see in this image, the trough date was three months later, then, a rally in price to the extent that Freddie Mac commented in a report, that it will halt the pace of PLMBS sales.

Freddie Mac posted in the 3Q2010 results an increase of $3,947 million in AOCI (Accumulated Other Comprehensive Income: unrealized losses in AFS securities. Equity), "primarily resulting from fair value improvements on available-for-sale securities". In other words, the PLMBS market was improving dramatically.

Maybe many billions worth of write-offs would have been avoided in the prior years, had they kept the position, or this sale at fire-sale prices was planned.

It seems that she made up this quote:

Another year later, at the end of 2007, defaults on private-label MBS were so high that the market was shut down entirely,

With CET1 >2.5% of ATA, the time has come.

CAN'T YOU SEE IT'S A CAPITAL DISTRIBUTION RESTRICTED?

(SPS LP increased for free as compensation to the UST in the absence of dividends).

Just like the dividend payments. Both number 1.

Then, we use the Incidental Power ("any action", like lying) to legalize this action applying it towards the EXCEPTIONS:

-Pay down the SPS. U.S. Code §4614(e),

-The exception added in "the supplemental" on July 20, 2011 CFR 1237.12 (Recapitalization in a separate account, either in the exception 1, 2, 3 and 4, because it (c) supplements and it shall not replace or affect the Restriction on Capital Distribution by the statue posted in the prior point.

A restriction on Capital distribution is meant for the recapitalization (the Capital is built internally). FnF can redeem the SPS and, at the same time, build capital. Double-entry accounting (cash - Retained Earnings acct: you pay down the SPS with simple cash. The Retained Earnings acct stays. Watch my signature image below)

This is why a recapitalization in a Separate Account (outside their balance sheets) CFR 1237.12 supplements the Restriction on Capital Distributions by statue that is meant for the recapitalization too. A follow-on plan.

In the end, they've been assessments sent to the UST in the form of capital distributions, no actual dividend was ever paid (Besides unavailable Earnings for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts) and no SPS LP was ever intended to stay (instead of lying, like the dividends, a joke "in the best interests of the Agency"), as the evidence seen because they are absent from the Balance Sheets.

If you continue to play the fool, you will end up wearing diapers.

Jesus!

A Conservatorship for the rehabilitation of financial companies can't end up with people pleading the 5th amendment of the constitution, like this corrupt litigant that just seeks to be in the limelight, turning himself into a savior:

We are trying to save the companies

If the FHA's MMIF and GNMA cease to exist, the government can free up $145B in the FHA and $31B with Ginnie Mae, for government spending.

With the recent LLPA changes in FnF, this upfront g-fee was aligned with the FHA, to the extent that in some cases, even FnF charge a lower fee.

For instance, in First-Time homebuyers; LTV >95%; credit score <680 (FHA's 74% mkt share), same fee FnF-FHA with credit scores <640, but FnF are cheaper in the range 640-679.

Since Bill Ackman's "economy shutdown" call,

home prices are up 47% and rents are up 20%.

The bill is co-sponsored by your boss, Tim Pagliara.

I have been involved in every aspect of this issue at the highest levels for 9 years.

Ongoing 3rd phase of the Separate Account plan.

The Common Equity (Retained Earnings acct) is swept to UST the moment it's substituted in the Net Worth (Equity) for SPS LP increased for free (we can't see this effect either in this table and in the Balance Sheets, because all this SPS LP increased for free and its offset, are missing. Financial Statement fraud).

Necessarily, this CE is held in escrow, pending unwinding this operation (A joke "in the best interests of the Agency": FHFA-C's Incidental Power), in order to uphold:

-The exception to the Restriction on Capital Distributions. CFR1237.12: recapitalization.

-FHFA-C's Rehab power (CET1)

The deadline is the latest May 23rd, or 30 days after a motion filed under the Federal Rule of Civil Procedure has been resolved by the court, like the controversial motion for JMOL under Rule 50(b) submitted by the FHFA (55 pages), after an oral motion 50(a) during trial (Thus, (b) can't have the same evidence presented to the jury for deliberation in the motion (a)).

Guess what, this motion hasn't been resolved yet.

Judge Lamberth has deadline of Thursday, May 23rd.

They post $0 EPS every quarter. Can't you read?

Didn't you ask for court news?

The revelation of the attorneys’ fees and nontaxable costs and expenses, better known as "the fat bonus" for their con job, is being postponed to the maximum by the allies: FHFA, the litigants and judge Lamberth.

The felony already happened with the jury award. This "Lamberth rebate" was included in the definition of capital distribution with the famous Final Rule of July 20, 2011 (CFR 1229.13 shown in the tweet below), thanks to an express grant of authority by statute in the number 3:

The FHFA doesn't have authority to override the law that states that capital distributions are restricted.

That's not what "in the best interests of the Agency" is about (FHFA-C's Incidental Power), because it isn't meant to turn a Federal Agency into an outlaw. Secondly, it isn't "authorized by this section" (FHFA-C's Rehab Power).

The key: it would expose the other capital distributions during Conservatorship:

-Dividends.

-SPS increased for free in the absence of dividends.

Both, number 1 in the definition of capital distribution.

Which makes us come to the conclusion that they've been assessments in the form of capital distributions, applied towards the exceptions in the law (pay down the SPS - statute- and recapitalization in a separate account - CFR1237.12-) in order to legalize those payments that went through despite the restriction.

An attempt to mimic the assessments sent into a Separate Account plan invested in zero coupon Treasuries, to reduce the principal of the RefCorp obligation, besides interest payments ($300mll annuity), in the 1989 FHLBs' bailout by Congress @ a rate with a 0.299% spread over Treasuries (GAO report).

With FnF, dividends are restricted, so the entire assessment was applied towards the reduction of the SPS.

THE ALLIES FHFA-LITIGANTS-LAMBERTH AFRAID OF UNVEILING THE FAT BONUS TO THE UNSOPHISTICATED ATTYS

— Conservatives against Trump (@CarlosVignote) May 7, 2024

30% cut?

14days Rule,swapped for

45days:May23

Or

30days after a motion. Hence the surreal JMOL pending.

The felony was the award: a capital distribution #3,restricted.

#1?#Fanniegate pic.twitter.com/EmetX7YLUe

You already posted Fisher's tweet and I already replied to you, here.

Fisher, Pagliara and Howard are the, what you call, "leaders" you work for.

No ordinary shareholder follows the frivolous litigation.

Analysis of the liquidity in FnF.

In the midst of a banking crisis caused by a liquidity and solvency crisis, it's worth having a look to this analysis posted every quarter since many years ago.

Fannie Mae has reduced its Restricted Cash in Q1 from $33B held since long time ago, to $21B, reinvested in Securities Purchased under Agreements to Resell. This is why its Liquidity ratio increases from 3.5 to 3.8.

This analysis is also key if the shareholders are proposing a Leveraged Buyout of FnF.

A Liquidity ratio of 1 to cover a credit crunch event, is a normal ratio.

Then, their business requires more liquidity to repurchase delinquent loans from their MBS Trusts, that won't be recovered until the end of the Loan Modification trial period where, if it succeeded, the loans are bundled into MBS again (RPL), instead of being sold to Goldman Sachs & Co at a deep discount like nowadays, or, in NPL, the sale of the collateral after taking possession (taking into consideration the rebel states, where the courts delay the foreclosures).

Assuming that the Restricted Cash is pledged for the redemption of the JPS, we could be talking about $80B in Freddie Mac and $75B in Fannie Mae of spare Liquidity that can be monetized for the acquisition of the common stocks (the Private Equity firms use debt to acquire the companies and later they use the Assets to service the debt. In this case, due to spare Liquidity, they pay off the debt on day one).

With less Assets, FnF aren't leveraged if, at the same time, FnF redeem their JPS which are obligations (debentures recorded in Equity).

RESTRICTED CASH AND CUSTODIAL ACCOUNTS.

— Conservatives against Trump (@CarlosVignote) May 6, 2024

Screenshots: pic.twitter.com/DR3Bvyzq08

It's funny that neither the low profile WSJ Editorial, always with the "taxpayer's risk" when it's null in FnF, as it only buys obligations SPS from companies that buy mortgages with maximum 80% LTV at origination, which took 5 and 6 years for FnF to pay them down (exception to the Restriction on Capital Distributions), respectively, and as a result of fabricated losses, nor Meredith Whitney, mention that the proposal by Freddie Mac is a Personal loan at a whopping 9.5% rate, and with the collateral valued at all time high.

Double risk increase.

Likely, this was the reason why the CEO of Freddie Mac, with 30+ years of experience in mortgage finance, resigned effective March 15th, before it was unveiled.

This product has nothing to do with a mortgage, like a cash-out refinancing as a result of refinancing the entire UPB of the mortgage when interest rates are low.

On the other hand, the shareholders proposed many years ago, that FnF could repurchase the second-lien mortgages that were a business stolen by the banks, as they used the collateral owned by FnF.

This collateral-sharing was the reason of the robo-signing case in 2009-2010, where the banks (mortgage servicers) wanted to foreclosure on fast, in order to protect their second-lien mortgages, disregarding that a first mortgage gets paid first.

It's estimated that currently, there are $2+ Trillion second-lien mortgages outstanding at low rates, with the collateral owned by FnF.

This could free up the battered balance sheets of the banks, that could start lending again or boost their sound condition, currently with hidden unrealized losses (unaccounted for in Equity, either with change in AOCI or fair value change reflected later in the Retained Earnings account).

(*) Commingled securities since 2022, not 2020.

Anticapitalism was summoned during the Senate hearing, organized by the chairman, senator Brown, and the Goldman Sachs alumni, Sandra Thompson.

ST was very interested in highlighting that only "mom-and-pop businessmen" invest in their Multifamily business (Apartment buildings for rentals), when their Charter Act doesn't distinguish between small and large investors, as long as the clause Credit Enhancement is upheld (currently violated with the CRTs, and before, with the PLMBSs).

In the Multifamily business, Freddie Mac, which is the lead player (Fannie Mae catched up in volume a few years ago), issues K-certificates, which are comprised of bonds guaranteed by other players (just like the Commingled securities in the single-family business since 2020), which complies with the number 3 in the Credit Enhancement clause.

The last turn was senator Brown, who used the Senate and his position as Chairman, to bring to the town square one of his fellow neighbors of his home town, accused of being a businessman, and he set him on fire, for all the world to see.

Clearly, they aimed to prevent FnF from being acquired by Private Equity firms.

The sellers of business to FnF can't become owners of FnF.

Neither the banks that originate mortgages, nor Warren Buffett who owns Clayton Homes, the largest builder of manufactured housing and modular homes in the United States.

A question of conflict of interests, regardless that their BODs include builders, required by law.

FnF include the acquisitions of mortgages secured by manufactured homes since 2018.

But I'm sure there are many other Private Equity firms willing to own FnF.

As long as they acquire our stocks at their fair value, either directly or through an intermediary (the Treasury department buys us out at the stocks' Book Value), I'm good with that.

The JPS aren't part of a takeover, as they are redeemed by FnF at their fair value of par value.

Finally, remember that their huge Other Investments Portfolios, the most liquid mortgage-related Investments and the swelled Restricted Cash in Fannie Mae ($33 billion), facilitate a Leveraged Buyout of FnF, using most of those assets to finance the acquisition.

No, scammer. Both ideas are written in different sentences, separated by a full stop.

Fannie Mae says that:

Available capital excludes the stated value of the senior preferred stock.

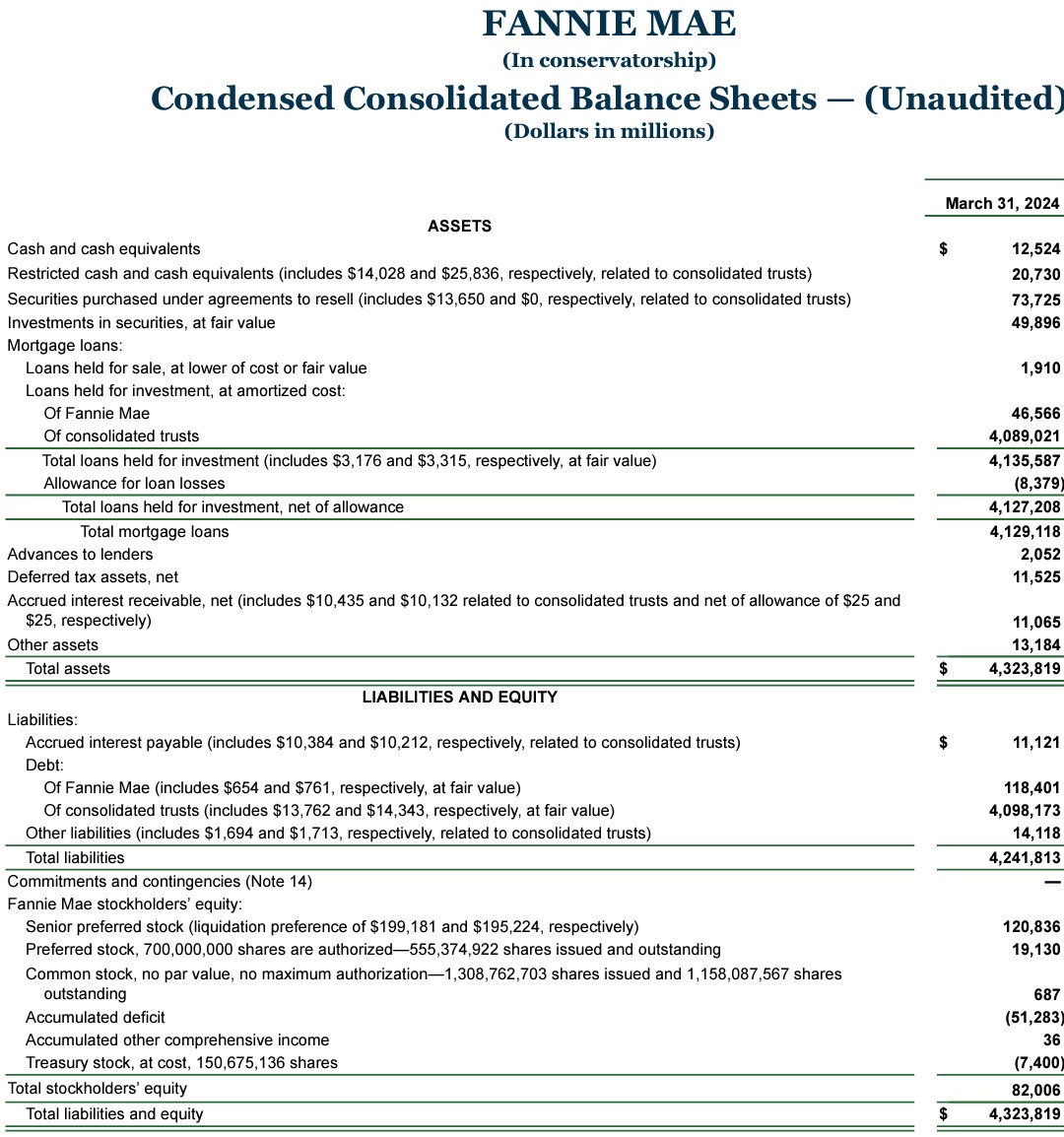

we had positive net worth under GAAP $82 billion

Deferred Tax Assets are deducted from capital to the extent they exceed 10% of common equity.

More evidence of a conspiracy FHFA-C and the Plaintiffs.

The unsophisticated lawyer from Ihub, is Mr. Pro Se, who also participated in the Madoff scandal, in charge of the bankruptcy to spin undervalued assets off to themselves.

The same accusation against Mnuchin and his buddy, Berkowitz, in the U.S. courts, as Defendants in the bankruptcy of the retailer Sears they were executives from (they forced the retailer to take out loans they granted personally, knowing that the retailer couldn't pay it back, with a huge collateral attached. Source: lawsuit).

Now, it's been spotted that FnF and the pro se plaintiff calculate the capital metrics the same way, not how the Basel Committee on Supervision (FHFA Capital Rule) and FHFA regulation 12 CFR 1240.20(b), assess it, with the sum of its components.

Certainly, this financial illiterate plaintiff (or how the attorney for Berkowitz, David Thompson, calls himself "unsophisticated lawyer" after pointing out that he is not a regulatory lawyer, but a litigator), couldn't have come up with the formulaic himself, that attempts to pass the Net Worth off as regulatory capital.

Both follow the instructions from the conservator, FHFA director Sandra Thompson, in charge of, precisely, regulatory policy, capital policy and financial analysis, since she arrived as deputy director in 2013.

Both currently parties in the Lamberth court with an "implied contract" claim (fiction), because they are reluctant to unveil the Separate Account plan (explained in the link provided in my prior comment) in accordance with the law and basic finance.

They rather play the fool.

That's the Capital Rule.

— Conservatives against Trump (@CarlosVignote) May 3, 2024

Then,FHFA outlined the definition of CET1 in regulation 12CFR1240.20(b)

It consists of the sum of the following elements:

Common share par value, less Treasury Stock(stock buybacks)

Additional Paid-In Capital acct

Retained Earnings acct(limit in DTA)

AOCI

The shareholders already filed a S.E.C. complaint in August 2020, denouncing the SPS LP and its offset with reduction of Retained Earnings account, absent from their balance sheets.

Posted at the end of this comment.

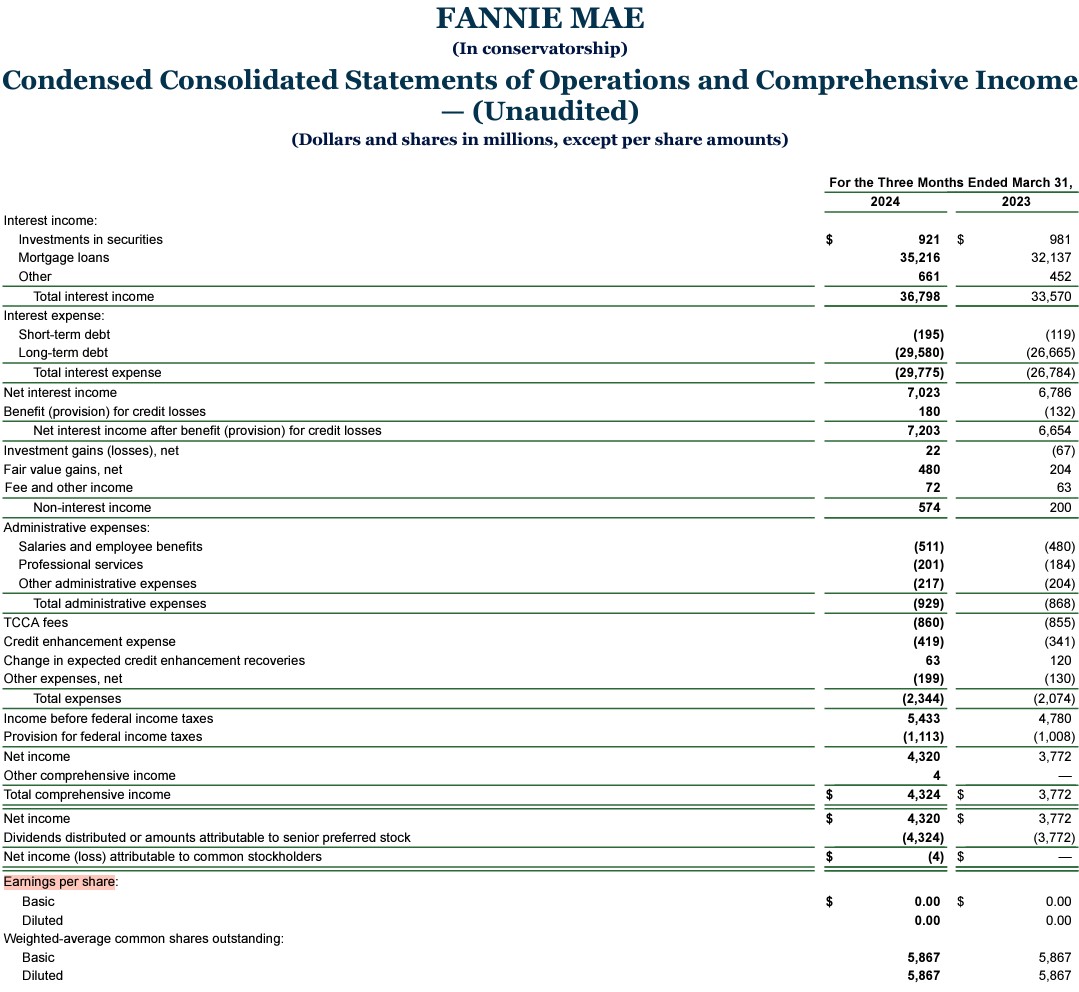

Important clarification: the charge on the Income Statement that makes FnF post $0 EPS every quarter, is correct.

There was a theory at the time, that the SPS LP increase for free was only an Equity transaction (balance sheet) and thus, it can't appear on the Income Statement.

Later, it's been rectified and their Income Statements are correct.

A SEC complaint doesn't understand of White House administrations or congressmen that come and go.

Don't mix up the Separate Account plan with your add-ons, Mr. Pro Se.

Crazy stuff with your 30+ aliases, with the objective to tarnish the image of those that truly post in-depth analysis: "spsa an illegal contract", "illegal actions of treasury to appropriate 200 billion in taxpayer debt", etc.

An by the way, the U.S. banks have the same Basel framework and the same capital requirements as FnF with the Risk-based capital ratios (RWA): CET1=4.5%; Tier 1 capital=6%; Total Capital=8%.

With the Leverage ratios (adjusted total assets), the banks have more stringent capital requirements: Tier 1 capital=4%, whereas 2.5% in FnF.

FnF calculate the capital metrics 'upside down', that is, they take a different concept (Net Worth or Equity) and subtract different items unrelated to the capital metric that you are calculating (SPS).

I already called the plaintiff Mr.Pro Se out, when he did the same 3 days ago, posting:

Net Worth

-SPS

-some portion of the DTA

= unaware that he was calculating Tier 1 Capital in his reply, and not the Core Capital that I was talking about with its statutory definition. He simply copy-pasted the script he had received beforehand.

This is Freddie Mac. Fannie Mae does the same:

Their objective was to conceal the components of each capital metric, so people don't see that FnF have $-84B Accumulated Deficit Retained Earnings account combined, shown on the Balance Sheets , but it's important to see it here as a component of the capital amount that later is required a minimum through regulation and statute ($-216B RE with the offset -Reduction of Retained Earnings- attached to the $132B SPS LP increased for free), an account tasked with absorbing future (unexpected) losses and a gauge of the rehabilitation in a financial company (RE is Core Capital for the capital ratios). Justice Alito's prerequisite to allow the Separate Account plan through restricted capital distributions: "Rehabilitate FnF in a way...".

This isn't a coincide. FnF calculated it correctly in early Conservatorship, and, for instance, this is how I learned that the Treasury Stock (stock buybacks) reduces the common stock par value when calculating the Core Capital.

FnF and this unsophisticated plaintiff, received instructions to change how to report the formulaic of the capital metrics.

Remember that Sandra Thompson arrived to FHFA in 2013 as Deputy Director, in charge of "overseeing regulatory policy, capital policy and financial analysis". Everything that is being put into question since long time ago (The Capital Reserve is what has to meet the capital requirements; SPS LP increased for free and its offset, are missing in the Balance Sheets; formulaic of the capital metrics, etc)

They all receive instructions from the same big players.

And who doesn't.

First, it wasn't Mnuchin. Secondly, the SCOTUS wasn't informed that the NWS had ended.

Mnuchin sent SCOTUS a letter stating that he and Calabria had ended the NWS. One of the justices even referenced that letter.

the enterprise will compensate Treasury through increases in the (SPS) liquidation preference rather than through variable cash dividends.

The conservator has limited powers. You are repeating the take by Bill Ackman, who implied that the SCOTUS said FHFA has absolute discretion (Source).

O Ackman’s clerk, Bradford:

With your quote:

4617f bars courts from questioning the actions of a conservator. As it should.

A Common Stock represents a legal claim on all the future EPS

The fraudsters want to become more Communist than China.

Existing common shareholders do not own the companies at all. They have no economic rights and no voting rights. Nothing.

Kphut19, a financial illiterate repeating the same lies over and over again.

The SPS LP increased for free is

off balance sheet

Bryndon Fisher already filed an appeal with a Derivative Takings case (on behalf of FnF) after insisting to judge Sweeney, because it could only appeal the lead plaintiff (Fairholme) and not the 11 related cases. But he loves to be in the spotlight.

Then, the same claim was appealed to the Supreme Court with Andrew Barrett individually (Fairholme plaintiffs).

Everything denied, because Justice Alito already said that necessarily, there is a Separate Account plan for the rehabilitation of FnF, if you know what that means.

Anyway, this unsophisticated lawyer still doesn't understand that a Direct claim and a Derivative claim are, in essence, the same claim. Because what is swept is the Common Equity that belongs to the common shareholders.

INCOME STATEMENT

Net Income of FnF

+Other Comprehensive Income (OCI)

= Comprehensive Income (Net Worth increase), is the amount of SPS LP increased for free.

BALANCE SHEET: the quarterly numbers of the Income Statement posted before, are Accumulated here for the picture of the company.

Accumulated Retained Earnings account

Accumulated Other Comprehensive Income (AOCI)

Both are used to calculate the Common Equity, also known as the Book Value of a company that belongs to the Commons:

+Common Stock par value

-Treasury Stock (stock buybacks)

+Additional Paid-In Capital

+Accumulated Retained Earnings account

+AOCI

We see how the Common Equity is swept to the Treasury, when the Common Equity generated in the quarter is substituted for SPS in the Net Worth.

The figure of Net Worth under GAAP doesn't change.

Same Financial Statement fraud: SPS LP increased for free and its offset with reduction of Retained Earnings in the same amount, are missing in their Balance Sheets.

If Fannie Mae states that

we had positive net worth under GAAP $82 billion.

we had positive net worth under GAAP $82 billion.

BOOM. Fannie Mae meets market expectations of $0.00 EPS.

YEEEEEEEEEE!

Beware of the fraudsters that take the Net Income to calculate the EPS, instead the Net Income Attributable to common shareholders after the payment of dividends or other compensation to Preferred Stocks, in order to conceal the ongoing Common Equity Sweep (NWS 2.0).

The Common Equity generated in the quarter (Net Income + Other Comprehensive Income), is the Net Worth increase in the quarter that later is used to assess the compensation to the Treasury.

Reminder: this compensation is another Capital Distribution (number 1 in its statutory definition), just like dividends (#1 too), and thus, restricted.

Common Equity held in escrow, in order to uphold the CFR 1237.12 (we use the exception to this Restriction on Capital Distribution to legalize it: for the recapitalization) and the fhfa-c's Rehab power as well.

EPS at the bottom of the image.

By the way, we see how judge Willett, in the previous screenshot, claimed that FnF had returned to sound condition at the time, referring to the return to profitability, when, in a financial company, soundness is related to the capital levels.

That is, RETAINED earnings (Core Capital).

Adjusted $-216B Accumulated Deficit Retained Earnings account combined as of end of December 2023 and stuck every quarter at that amount with the ongoing Common Equity Sweep (Common Equity held in escrow though, in accordance with the law)

Which reminds me of the 6th Circuit Court of Appeals in the Robinson case with the omnipresent attorney for Berkowitz, David Thompson, with the judge also mistaking sound condition for "the return to profitability, even if a large portion of that profit was sent to Treasury's coffers".

Besides, mistaking solvent condition for the UST's Funding Commitment, when it refers to solvent condition on their own, not with the existence of a UST's Funding Commitment, which existed since the Charter's inception (limited to $2.25B that had to be updated to carry out their Public Mission)

Let alone the judge's radical view, contending that "FnF likely should not return to business as usual". No one asked him for his opinion.

And "nothing in HERA's text requires the FHFA to return the Companies to business as usual", the reason why was appointed a conservator in the first place, the expulsion of the prior management, and with a Power that directs the conservator to restore (put) FnF to a sound and solvent condition. With "may" an imperative in statutes, once the capital has been generated.

This is why the judges are barred from making decisions about FnF. Lack of understanding of financial matters, which is a statutory requisite to become FHFA director and thus, the conservator of FnF.

Rogue officials are using the Judiciary to provide the alibi, and legalize what isn't stated in the law and basic Finance and has ended up with judge Lamberth openly admitting that he wants to grant back dividends to the Non-Cumulative dividend JPS, while FnF remain undercapitalized.

Everybody wants dividends when they are restricted for the recapitalization of FnF: RETAINED EARNINGS.

They should learn that a dividend is a distribution of Earnings in the first place. That's the point. Besides unavailable funds with Accumulated Deficit Retained Earnings accounts.

.jpeg)

"every circuit ***to review*** 4617f"

#FANNIEGATE ATTYS BRING 4617f UP AGAIN

— Conservatives against Trump (@CarlosVignote) April 29, 2024

Courts step in if FHFA exceeds its powers.

Willett's half-baked ruling amending Sweeney's ("authorized by this section" deleted)said YES w/ the NWS div, in a Hindes-moment(the 10%div too)

Alito corrected Willett:"Rehab FnF...Can't you read?" pic.twitter.com/2nBGuAxvJ3

You have calculated TIER 1 Capital, when I'm talking about Core Capital.

Similar, but different. Evidence that you can't follow the arguments.

I'm not going to explain more because, if you don't understand what you write, you can't understand my explanation.

Someone sent you the script.

Fannie Mae is not reporting under GAAP because it's accused of Financial Statement fraud (SPS LP increased for free and its offset, are missing on the balance sheet)

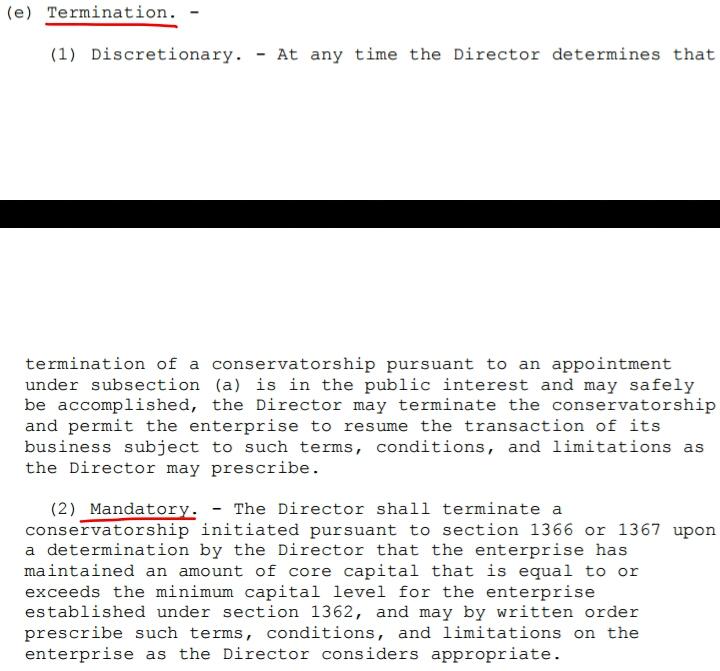

Significantly undercapitalized? How about Critically Undercapitalized with Deficit Capital available?

Fannie Mae had a GAAP positive net worth of $78 billion at YE23, the Enterprise Regulatory Capital Framework excludes the stated value of the senior preferred stock ($120.8 billion), as well as a portion of deferred tax assets, resulting in the Company being significantly undercapitalized.

Now, hit this wall: Definition of Core Capital 12U.S.Code§4502(7)

This is the FHEFSSA, not the U.S. Code:

Retained Earnings account is core capital. The only account that absorbs the future (unexpected) losses (the other Loan Loss Reserve -ALLL- is for expected losses -CECL accounting standard-. ALLL shows up as Asset writedown, that is, it assumes that the loss already occurred. Though it isn't true and that's why it's recorded as Tier 2 Capital for the Total Capital that has to meet the Risk-Based Capital requirement)

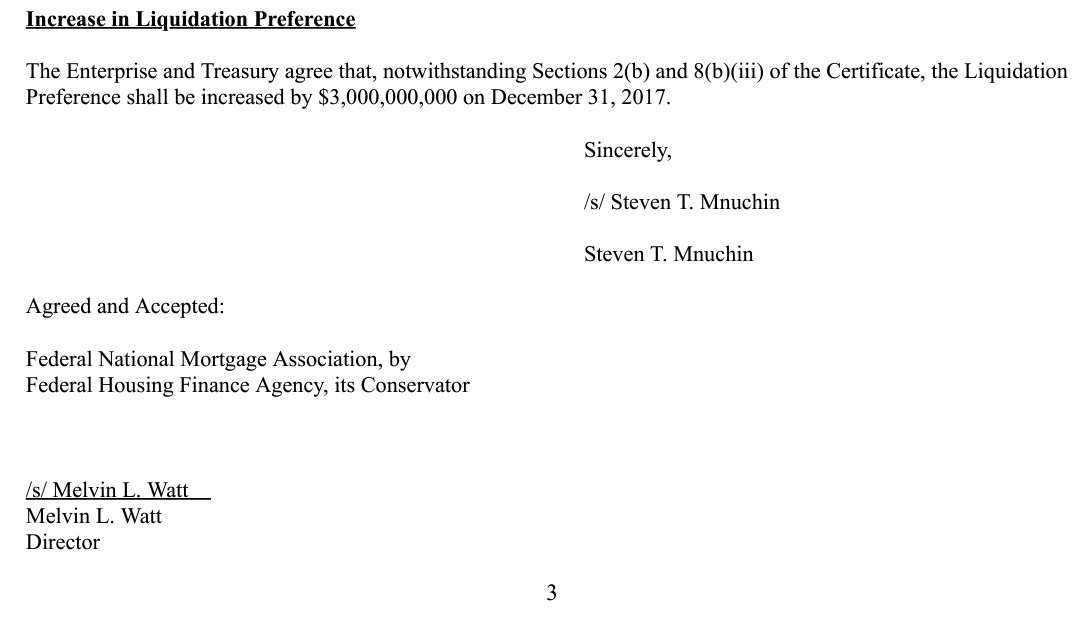

Today, the Retained Earnings accounts stand at an adjusted $-216B ($-91B officially on their Balance Sheets), adjusted for the offset (reduction of Retained Earnings) for the $125B worth of SPS LP increased for free (without getting the corresponding cash) since December 2017, with the masterminds of this 3rd phase of the Separate Account, Mnuchin/Trump, when they agreed with the FHFA director at the time, Mel Watt, on $3B gifted SPS on December 2017, when the Applicable Capital Reserve was raised to $3B.

Then it continued with Calabria on the September 2019 PA amendment and the latest, on the January 2021 amendment with the fraudulent concept "Capital Reserve End Date": when the capital requirements are met with Capital Reserve, and badly assessed, because of the offset mentioned (adjusted CR = $0)

It's the Core Capital the one that meets the Minimum Leverage Capital requirement, as per the definition of Capital Classification of Undercapitalized.

An adjusted $402B core capital shortfall as of end of 2023.

So much for "rehabilitation".

Mnuchin/Trump and Watt simply looked up the definition of capital distributions posted before, which are restricted, and when judge Willett called them out, unware that there is a Separate Account plan behind and in a half-baked ruling commented before, stating, about the NWS dividend, "that kind of liquidation exceeded the powers of the conservator", 3 weeks later they picked a different compensation to UST, notwithstanding that it's the same Common Equity Sweep as before, as we can see in:

- The Income Statement: Net Income less dividends or other compensation to UST, equals $0 Net Income Attributable to Common Shareholders. That is, $0 EPS.

- The Balance Sheet: here we can't see it here, because this SPS LP increased for free and its offset, are missing (Financial Statement fraud). But have a look to this adjusted Net Worth activity table, to see how it plays out. The Common Equity is always held in escrow, in order to uphold the Rehab power.

In the best interests of the Agency: mess around, in a conspiracy with the crooked litigants and Co.

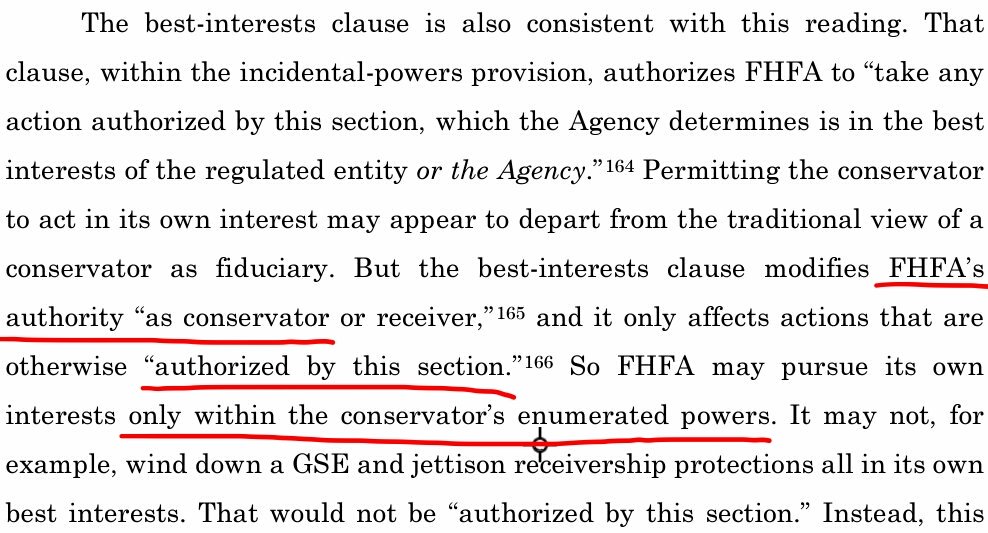

You shamelessly conceal that the UPMOST judge, justice Alito, began his interpretation of the FHFA-C's Incidental Power: "Rehabilitate FnF in a way....".

By the way, this comes after judge Sweeney's interpretation of this provision, deleted the words "authorized by this section", so she could read "take any action in the best interests of the FHFA", ending up with "the FHFA is the government". She was called out and renamed "The Tipp-Ex Queen", and it's when the big boys stepped in to give a proper interpretation of the written text. Primarily because take their capital away is NOT authorized by this section (a breach of the FHFA-C's Rehab power, knowning that "may" is imperative in legislation, once the capital has been generated, and not a choice. Already commented.)

Justice Alito was just making clear what judge Willett stated in a prior ruling (5th Cir.) over the same Collins case and regarding the same provision: "Any action within the enumerated powers".

Therefore, the savy Justice Alito simply looked for the FHFA-C's Powers, something that judge Willett missed, and determined that it's about the rehabilitation of FnF, when he read: "Put FnF in a sound and solvent condition", because he knows that the soundness in a financial company is measured with the Capital levels, where the Retained Earnings are recorded as Core Capital. And solvency (ability to meet the obligations) is suitable for the reduction of the SPS (obligations in respect of Capital Stock) and restore their capital levels as well.

Both are, precisely, the exceptions to the Restriction on Capital Distributions.

Then, we can come to the conclusion that the Restriction on Capital Distributions is a tool to achieve the FHFA-C's Rehab power.

This is why the FHFA's Power is also called "the Rehab power" or the "Recap power".

You have just posted justice Alito's add-on "and the public it serves" in your piecemeal approach (The Tipp-Ex gang), that stretches the interpretation of the FHFA-C's Incidental Power, useful to use FnF for government policies and to put an example, it would allow the Congress to keep the estimated $15B it owes to FnF for managing Obama's Making Home Affordable program (HAMP and HARP), that even made FnF advance the payments to borrowers and servicers (banks), with the promise that they would be reimbursed for this cost with TARP funds, but it didn't happen.

Also, the utilization of the hedge funds as a tool for government policies, after Trump approved the debt forgiveness plan (the short-sales that DeMarco prohibited), forcing FnF to sell their NPL and RPL to the hedge funds at a deep discount, because it contains a clause that includes debt forgiveness, and with the collateral (properties) valued sky high given away. This is an incentive to prompt manufactured crisis.

Fannie Mae. Sale of RPL:

purchasers must offer delinquent borrowers a waterfall of loss mitigation options, including loan modifications, which may include principal forgiveness, prior to initiating foreclosure on any loan. Source.

You continue to hit the wall of the Restriction on Capital Distributions and its exception (pay down the SPS) U.S.Code §4614(e), along with the exception added in "the supplemental" on July 20, 2011 CFR 1237.12 (Recapitalization in a separate account, either in the exception 1, 2, 3 and 4, because it (c) supplements and it shall not replace or affect the Restriction on Capital Distribution by the statue I began this comment with, which is meant for the recapitalization as well, because when you pay down the SPS, you are recapitalizing FnF at the same time, as the SPS are pay down with normal cash and they aren't core capital, whereas the posting on Retained Earnings stays, Core Capital)

At the same time, the FHFA is complying with its Power of Recapitalization and also improving their Solvency with the reduction of SPS.

"(May) put FnF in a sound and solvent condition".

When "may" is imperative once the capital has been generated, and it's only to give the conservator some leeway to carry out activities or actions (upholding the law, obviously. It wasn't turned into an outlaw Agency).

The Restriction on Capital Distributions is written in stone.

The same as the penalty on all those individuals that have covered it up in formal documents: court briefs including Amicus briefs, GSE slides, "letters to my partners", articles, books, etc., as long as these documents are publicly available

The obsession to conceal the FHEFSSA, so that the definitions regarding capital go unnoticed, is of epic proportions.

Like the very Mnuchin's Treasury Department:

Something that people should have learned beforehand, in order to make decisions about FnF, that's why to become FHFA director is required a deep understanding in financial matters.

The judges are providing the alibi to not unveil the Separate Account plan. That is, playing the fool with the pomp of a black robe.

Now, hit this wall too. CAPITAL DISTRIBUTION: Dividends, today's SPS increased for free and the Lamberth rebated added later in #3 through regulation CFR 1229.13.

FACT: The authority of UST was about the PURCHASE of securities, and it hasn't purchased even one security.

No one has ever wondered how is this even possible.

It all began with the issuance of $1B worth of SPS free of charge (1 million stocks at $1,000 per stock), with the objective to reduce the Core Capital in the same amount (It carries an offset: it reduced the Additional Paid-In Capital account. Source) and justify the Conservatorship with (G) LOSSES: Likely to incur losses that deplete capital.

Since then, all the SPS LP corresponding to the draws from the UST (1:1) has been increased and that's a Securities Law violation because the securities must be dated at the time the company raises fresh cash, and necessary for the deed of purchase (necessary for the capital gains tax, etc).

Other theme is that, for reporting purposes, they can be unified in one security if they have the same price and characteristics.

The objective was to skip the deadline on the "TEMPORARY" second UST backup of FnF inserted by HERA with unlimited yield SPS, of December 31, 2009, because the deadline refers to the authority on PURCHASES mentioned, and there's been none.

The Warrant is another security that was issued for free on day one, in an attempt to override the prerequisite on PURCHASES by the UST of (iii) to protect the taxpayer (collateral). Once spotted, collateral it is. Collaterals aren't allowed in the original Fee Limitation of the United States ("PROHIBITION...."), this is why Calabria/Pelosi's HERA continues to raise our eyebrows.

This is one of the 7 Securities Law violations that need to be settled and also it serves as Punitive Damages that the Equity holders require to the DOJ. Although the common shareholders waive this claim in the case of "as is" and "takeover" resolution of Fanniegate, not in the case of a Takings at BVPS.

The same with the second round of Punitive Damages due to the Deferred Income accounting, in the case that it's allowed to amortize it into Earnings in one fell swoop without the existing shareholder ($61B Deferred Income together as of end of 2023, is recorded as Debt, not Equity. $42B in Freddie Mac alone)

The third round of Punitive Damages, is against the plotters of the government theft story in formal documents: court briefs, books, articles, etc., for the cover-up of many statutory provisions (Restriction on Capital Distributions; "May" recap is imperative once the capital is generated; etc.) and financial concepts (Dividends, a distribution of Earnings, unavailable with Accumulated Deficit Retained Earnings accounts).

2- SPS LP increased for free since December 2017 and its offset, are missing on the balance sheets (Financial Statement fraud)

3- Fannie Mae posted a charge on the Income Statement, when no SPS LP was required to be increased in the 1Q2020 Earnings report.

4- Stock price manipulation.

5- The value of the Warrant was credited to Additional Paid-In Capital account.

6- Dividends paid out of an Accumulated Deficit Retained Earnings account (for the Separate Account plan).

7- CRTs. Although it's a breach of the Charter Act (Credit Enhancement clause: not among the enumerated ones), it's included here to simplify and because it can also be considered a Securities Law violation. A credit enhancement operation in mortgages where the credit event is the credit loss, is a scam, because it occurs after the company carries out costly foreclosure prevention actions. For instance, Freddie Mac's STACR DNA or HQA notes. Whereas the credit event that triggers the claim of payment in the STACR DN or HQ notes, is serious delinquency. Since 2015, Freddie Mac only issues the former.

They are an excuse to make FnF pay an outstanding annual rate of return on these debt notes, currently between 9%-13% rate (Source: Earnings reports).

The CRTs look more like a continuation of the fraud in early conservatorship, with their 30-year zero coupon callable Medium Term Notes, redeemed at a 5% and 6% annual rate of return soon after they were issued, as a way to extort money from them, commented on Friday showing documentary evidence.

With the CRTs they made a mistake.

$19B in CRT expenses/recoveries is due because it's barred in the Charter Act, no questions asked.

Team work: Guido posts flawed analyses and I call him out.