News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The stocks won't be "treated" at all, upon resolution of Fanniegate and release.

Both classes will be equally treated at release also, just based on what has happened for 15 years.

the government would otherwise earn nothing at all.

FHFA already prohibited this payment of Securities Litigation judgment.

A capital distribution, restricted, inserted in the FHEFSSA (U.S.Code §4614(e)) with an amendment in HERA's Subtitle C: Prompt Corrective Action. This is why the FHFA (and everyone else) calls this restriction "prompt corrective action" as well, in its rulemaking. For instance, Capital Rule:

A Final Rule where the FHFA amended the FHEFSSA's definition of capital distribution to include this case (Number 3)

Final Rule, July 20, 2011, "for the transparency of the conservatorships". Preface:

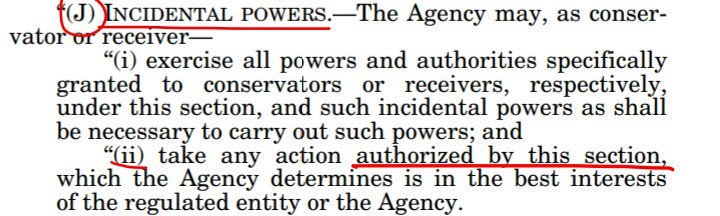

The fact that the FHFA, through rulemaking, (CFR 1237.13) later added a funny afterthought to authorize it ("...except to the extent the Director determines is in the interest of the conservatorship"), is struck down for shenanigans (the CFR 1237.12 with more exceptions to the restriction (1, 2, 3 and 4: for their Recap in a Separate Account), "supplements and cannot replace or affect" the FHEFSSA's Restriction on Capital Distribution, and the actions in the best interests of FHFA (FHFA-C's Incidental Power), must be "authorized by this section", which this case is not: breach of the FHFA-C's Rehab power)

Also, it gave answer as to when the Equity holders might expect the resumption of dividend payments. It includes the Treasury's SPS, obviously.

The fiction of "implied contract" in the Lamberth court is, precisely, about the lack thereof. Later on, the Adequately Capitalized threshold was substituted for the Table 8: Payout ratio, in the new Capital Rule: now, additionally, it's necessary to fetch 25% of the Capital Buffer.

More evidence that judge Lamberth hasn't read the regulation pertaining to FnF that the attorneys cover up, jointly with their paid shills on social media.

Finally, the Limitation on Court Action (U.S. Code 4617(f)) precludes the court from taking any action until the Fanniegate scandal is over with the return to the equity holders, management and the Board of Directors, of the rights and powers transferred to the conservator momentarily, to help it fulfill its mandate (Voting Right, ASM, etc), where fiduciary duties arose (actions on our behalf, that may or may not be in our best interests, like a Separate Account plan, but there are other duties. The conservator wasn't given carte blanche. Any action "authorized by this section" or as justice Alito claimed "rehabilitate FnF..." the Marxist way, for the extortion of resources using the investment banks for public policies, in the sale of NPL and RPL at a deep discount to capture the debt forgiveness string that Trump approved; REO inventory sold to Neighborhood Associations, women-owned businesses, etc.)

Good, but once the capital is generated, it's kept (Retained Earnings). Which bars today's NWS 2.O (Common Equity Sweep through the gifted SPS and their offset). In accordance with the law, the Common Equity is held in escrow.

It isn't the first time that you put words in my mouth that I didn't say.

You are Bradford.

And you don't have integrity.

No, it hasn't changed. NWS 2.0 (Common Equity Sweep)

Held in escrow though.

This follow up comment against the Warrant highlights that the BOD of Freddie Mac amended the bylaws unlawfully to enable the issuance of this Warrant.

Because it occurred on September 4th, 2008, one day before FnF were placed in conservatorship and thus, it should have required two-thirds shareholder consent to do it.

Our negotiator filed a complaint with the S.E.C., within the Statute of Limitations: TCR1329318575775.

This comes in addition to the fact that the Warrant is a legal (to protect the taxpayer)-illegal (Fee Limitation) collateral, and also void (non-transferable in the clause 7, can be transferred in the clause 2.1), for the assault on the ownership of FnF by Wall Street and the community banks, paying nothing (ownership by Immaculate conception. Shares "assigned".)

We just have to expose the shenanigans, like calling the Warrant "investment" in the UST's website.

Who on earth calls something received for free "investment"?

So on and so forth.

Likewise the shenanigans from the attorneys and renowned investors.

By the way, there was a death spiral, as DeMarco said. That's why the NWS dividend was necessary. Our hero. He fooled both sides of the aisle engaged in the Wind-down and Nationalization rhetorics, respectively. Both sides working together with the law firms, chamber investors (Pagliara-Maxine Waters, etc.) and the social media paid shills where you come from, "asleep" Bradford.

Now, it's time for the Separate Account to come to the surface.

It has been explained a thousand times, so don't play the fool asking how all the SPS have been repaid and FnF fully recapitalized.

15 years in the making.

How do you envision the elimination of the "separate account" in practice? Will there be any conversions? Like converting LP (fully or partially) to commons?

No, thanks. We stick to the Separate Account as per the law and basic Finance.

You fool no one, Bradford-LuLeVan.

Once again, Guirdo lies with the Warrant prospectus that provides a definition of "Fair Market Value", related to the Market Price and it's commonly known as VWAP: volume-weighted average price. In this case, it's used the closing price and the period of the most recent 20 trading days.

The Warrant Prospectus doesn't explain what this concept is for, because it doesn't contemplate the case of cashing-in the Warrant through differences: 20-day VWAP - Exercise Price. The Warrant had other objective as explained below: the assault on FnF by the banks and Wall Street.

The VWAP data for one trading day is used a lot by traders.

This has nothing to do with FnF and the broad scheme of conservatorship. To begin with, neither the UST is a trading desk, nor it's a Moelis-like restructuring shop. The role of the UST in the Charter Act is very limited.

Guido wants to pass this "Fair Market Value" off as the "Fair Value" that we calculate for the stock valuation.

Read the definition of fair value as per warrant agreement

The warrant exercise price is NOT FAIR VALUE!

Why don't you go on vacation with your caravan and without internet access?

Your girlfriend could recite your famous poems with nonsense that you write here regularly, like this one yesterday.

It would be like this:

mkt sets the price - mkt defines value

YTD Chart is all you need for FACTs

Dec 7th will be another total FHFA ZERO

like All the other FHFA gov Conf Zeros

Biden Admin is doing ZERO on GSEs

Biden has Israel / Hamas / hostages

Ukraine / China - Taiwan / budget

Holiday recess & a pile of MUCH

MORE PRESSING issues to deal with

before "any" action on Fannie / Freddie ...

Gov "only" takes last minute action on

a Crisis "when they have to" ...

FACT - there's no Fannie / Freddie "crisis"

in the meantime - Fannie & Freddie have

retained earnings & next Court events

for shareholder relief ... FACT

Saying "Receivership is off the table" is off the table, with 15 years into Conservatorship, yet we have the usual suspects like Bradford and his partner, Navycmdr, saying yesterday that Receivership is off the table.

They belong to the same gang that wants to downplay expectations for the common stocks, thinking that, in the meantime, the JPS will get a better deal out of pity and with frivolous lawsuits, than otherwise would be with a normal conservatorship and what lies behind, a Transition Period to build capital (Regulatory Risk), pursuant to the UST's "recommendations on ending the Conservatorships", at the request of the Dodd-Frank law of 2010. That is, Basel framework for capital requirements endgame.

What the litigants are doing in court is called "stock price manipulation", for which they have to pay us Punitive Damages. So, nice going.

Only the ambitious Calabria has mentioned Receivership twice before, during Conservatorship:

FIRST.

Another one with the "Back to the future" stance, disregarding the fact of a conservatorship status since 2008, like the hedge funds in court that has led to a capital shortfall similar to the one in 2008: now there are 16 years left to become Adequately Capitalized again and resume the dividend payments (Illegal. In the absence of Separate Acct), versus 14 years in 2008 (Separate Acct plan)

A Receivership is when there aren't prospects of financial recovery, which it has been proven that it wasn't the case of FnF in 2008. So, Receivership was off the table in 2008.

If you induce a bankruptcy, which is what Calabria would like to see, with a series of schemes to misrepresent their financial condition, like recently the SPS LP increased for free out of the blue, in the same amount as the Net Worth increase in the quarter, it's not that FnF need a Receivership, the thing is that you are a crook. The Separate Account plan comes to solve this issue, as it legalizes every action whether they want it or not, and puts FnF in a sound and solvent condition in accordance with the law. In the prior example: For the recapitalization of FnF and pursuant to the CFR 1237.12, these gifted SPS are a joke (capital distribution, restricted) thanks to the FHFA-C's Incidental Power ("in the best interests of FHFA"), that is, in truth, it's holding the Common Equity in escrow (recapitalization, an exception to the restriction), through the offset attached, pending unwinding this operation at some point down the road (operation concealed when these gifted SPS and the offset, are absent from the balance sheets. A Financial Statement fraud that needs to be settled with an all-in settlement or Punitive Damages)

SECOND. Enacting a Final Rule in 2021, precisely, for a Receivership, under the nickname "Resolution Planning Rule", to mimic their failed scheme of 1989, Resolution Trust Corp (RTC), managed by the FDIC, where the UST lost $48.8 billion in Public-Private Partnerships with Wall Street, that no one can say they didn't see it coming. $30 billion invested through the purchase of the RefCorp bond issued by the FHLBanks, that is still outstanding, and $18.8 billion the UST invested directly in RTC required by law.

This is why these people are happy when they see the shareholders calling for "resolution of Fanniegate", thinking that resolution means Receivership, when resolution means also "solution to a problem".

There is nothing wrong with enacting rulemaking for a Receivership. The problem comes with the timing (during a conservatorship), under a Separate Account plan and with a regiment of paid shills in court and on social media that want to harm the economic interests of the shareholders, in favor of the JPS holders, and, last but not least, colluding with the DOJ to that end (share the booty approach)

Navycmdr never learns.

Dude, one cannot write daily comments that refute your statements, but later, you keep on posting the same lies over and over again.

FACT: 4 yrs ago Congress didn't have Sept 18th 2023 Bill H.R. 5549

to require Sec of Treasury completed proposal to "terminate the conservatorships"

Navycmdr, with "just the facts", is a government snitch.

Because he advocates the current $118B Net Worth and balance sheet with $312.5 billion SPS LP outstanding.

A shill for the hedge funds JPS holders' diatribe that seeks a "restructuring a là Goldman Sachs", that is, with what Calabria said in his book about what Mnuchin said he wanted: the JPS are swapped for Cs with the same haircut as the SPS, when the balance sheet indicates that the JPS would be wiped out instead.

Navycmdr, part of the judicial front to peddle their case, conceals the reality of multiple violations of statutory provisions and also justice Alito and judge Willett's guidelines with "rehabilitate FnF"....the Marxist way (authorization of sale of NPL, RPL, REO inventory to Goldman Sachs and Co at a deep discount) and judge Willett with "any action within the enumerated powers".

The financial rehabilitation has only one meaning: "Put (restore) FnF in a sound and solvent condition" (the FHFA-C's power)

Today, FnF are in the worst financial condition ever. But the government shill under the orders of chamber investors, loves it:

-$312.5 billion SPS outstanding

-$-216 billion Retained Earnings accounts tasked with absorbing future losses. It needs to have positive balance for that and also to distribute earnings as dividend. So, no dividend was ever possible in the last 15 years.

-$-194 billion Core Capital. A $402 billion capital shortfall over Minimum Leverage capital requirement.

-The SPS LP is increased for free every quarter out of the blue, in an amount equal to the Net Worth increase. Berkowitz's attorney, David Thompson, even sought damages in the 5th circuit (Collins case), because the "for cause" removal restriction prevented this from happening sooner, selling the idea that this is a good deal for FnF that are being recapitalized and also it enrichs the government. The truth is that FnF are building SPS, not regulatory capital (concealed with financial statement fraud: gifted SPS and their offset -reduction of Retained Earnings- absent from the balance sheet), and this attorney and his client are just snake oil salesmen. They just need a government snitch posting happy emojis on the internet, and the chamber investors like Pagliara or Hindes in his disastrous letters that just change the headline, so he can write one every week. These are others that I recommend: "Nice and easy. Nice and easy." And "That's not good."

On the other hand, the reality of the Separate Account plan that upholds all the statutory provisions the corrupt litigants have covered up, and a plan that has already been carried out by the same people (ST at the FDIC since 1990 and DeMarco at GAO, the auditor) in the law entitled SEPARATE ACCOUNT commented yesterday in the post that proves it using the method PATTERN ANALYSIS.

You need financial knowledge in the first place, to carry out this analysis.

Under this plan, the CET1 would be 2.6% of the Adjusted Total Assets as of end of September, 2023, which means that FnF can redeem the JPS and then, they would comply with the threshold Tier 1 Capital > 2.5%.

Beware of these shills with the "everything is fine" and they never mention financial concepts, like their ERCF tables with huge capital deficits, other than $118 billion Net Worth without knowing what it means (It's owned by the Treasury, government shill. The JPS and Cs are wiped out in a restructuring)

Navycmdr writes a poem that no one can take seriously, peddling the same lies, like "Retained Earnings" and "shareholder relief" from the courts with all the frivolous lawsuits, attempting to conceal the fact of a Separate Account.

You will fail because you've been a paid shill for the hedge funds' Government theft story that has decimated the share prices, as counterparty of the DOJ in court, and for which it's been requested that your gang pay us $4.8 billion in Punitive Damages, and the DOJ another $4.8 billion.

Do you get now what the "you will fail" remark by KengKong means?

It's not about Receivership as you claim due to your obsession to cause emotional harm on the shareholders, like with your other alias LuLeVan: "the stocks will halt trading".

You'll get the full par value for your JPS, either in cash or the market price, in light of the 15 years into Conservatorship.

Dividend suspended upon undercapitalization (Regulatory Risk). Get over it.

PATTERN ANALYSIS: 6 ways to hold the Common Equity in escrow.

This analysis of data or logs is used to solve complex issues, like Fanniegate.

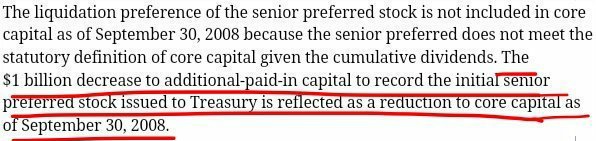

In the second way, with gifted SPS, it should have been added the initial $1 billion SPS increased for free in each GSE that, unlike the others that I will refer to next, it does appear on the balance sheet, debited from the Additional Paid-In Capital account (Common Equity held in escrow)

The interpretation of the relationship between the actions, leads us to assert that there has been a Separate Account plan, in accordance with the law and basic Finance:

-Put FnF in a sound and solvent condition (FHFA-C's power)

-Using the exceptions to the Restriction on Capital Distributions (FHEFSSA and CFR 1237.12): dividends, gifted SPS, stock buybacks and the payment of Securities Litigation judgments.

-No earnings available for distribution as dividend all along.

-Low cost UST backup in the Charter Act.

-CRT operations, illegal in the Charter Act.

We saw the visual effect of "Common Equity held in escrow" in the prior screenshot.

Here is another example to spot it visually, with this adjusted table of Freddie Mac (SPS increased for free out of the blue, in an amount equal to the Net Worth increase, a new compensation to UST after the dividend to UST was suspended with judge Willett's en-banc ruling in the 5th Cir., to build regulatory capital. A big lie. It was all part of the same scheme: uphold the law, but lie about it "in the best interests of the Agency")

Hence the $-194 billion Core Capital combined every quarter since September 2019. FnF are building SPS, not regulatory capital, concealed with Financial Statement fraud (the gifted SPS are missing in the balance sheets)

MORE WAYS TO HOLD COMMON EQUITY IN ESCROW

— Conservatives against Trump (@CarlosVignote) November 17, 2023

-PLMBS settlement on behalf of FnF: $25.5B

-CRT operations: $18B,net

Barred in the Charter's Credit Enhancement clause.

Foreclosure prevention actions bail investors out.

C.C.

Likely,Commitment Fee,barred in the Fee Limitation.#Fanniegate https://t.co/BAPQtvb7lh pic.twitter.com/D5IrArm2eo

No "water boy". The Request for Input on pricing was related to the recent LLPA changes (upfront g-fee)

It wasn't related to the Capital requirements and a Federal Agency is never tasked with establishing a "targeted rate of return".

No respondent, except the plotter Timothy Howard, asked about the issues mentioned by Alec Mazo in that tweet.

Everyone talked about the LLPA, like me.

You, a JPS holder, keep on promoting the hedge fund manager Alec Mazo.

There is nothing scheduled "by December 31st".

You posted the email that you have just received, either from Pagliara or from the attorneys. You play both hands so you receive more checks. Am I wrong?

Look! 📬️ You've got mail!

The common stocks' fair value was calculated with the adjusted annualized Q3 2023 EPS, adjusted for a Privatized Housing Finance System (no TCCA fees, no CRT expenses) and after unwinding the Separate Account plan (no Warrant, no SPS outstanding, $150B refund, ...), besides fully reserved for expected losses, ALLL (adjusted for the Benefit/Provision for loan losses)

It was calculated a PER 14 times.

On top of that, it was assumed that the Accounting Standard of the upfront g-fee, is changed, so the fair value captures the value of the Deferred Income, net ($51.2 billion combined)

Then, you can agree or disagree about whether Q3 2023 was an earnings report representative to calculate such fair value, should it need further adjustments, because we had strong Derivative gains (partially offset with investment losses and fair value losses) and a high yield on reverse repo operations with the Fed. On the other hand, low amortization of deferred income with lack of refinancings and, in a takeover, absence of control premium that otherwise would be. So, pretty much it stays as is.

There is also a fair value in the case of Takings: adjusted Common Equity as of September 30, 2023.

And, finally, a target price or how the stocks should trade on the stock market or heading to, in the absence of takeover or takings, with a forward PER 14x (with the estimated 2024 EPS)

Those that throw numbers, like $22.5 for FNMA, likely are JPS holders that can't withstand that a common stock is valued at a price much higher than their JPSs.

Our negotiator rips into the ambitious Mark Calabria.

Who said that he and the Goldman Sachs' alumni, Sandra Thompson, could create a parallel Charter with FnF?

Now, the FHFA and the UST will have to recall all the insurance premiums paid ($18B, net), though, likely they were syphoned off to UST under the Mnuchin's slogan: "The taxpayer be appropriately compensated". Good, but he is talking about a different Charter, because in this one, it's barred.

Ambitious Calabria is a tool of BLK,etc

— Conservatives against Trump (@CarlosVignote) November 21, 2023

The FHFA-C's Inc.Power, backed up by the word "may" in its Power, that gives it some leeway in managing the conservatorship👇doesn't mean that it can break the law.

CRT, likely syphoned off to UST (Mnuchin's Commitment Fee)

Anyway,$18B due. pic.twitter.com/2lJqwiiqFf

Trump, accused of attempting to supplant the law in force with a new manufactured scheme.

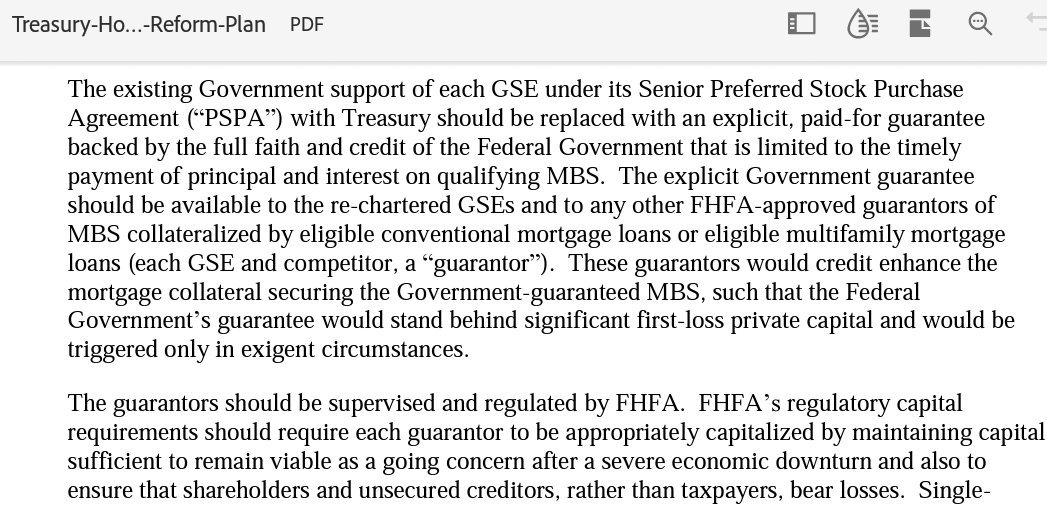

The September 2019 Mnuchin's Treasury Housing Reform plan was released pursuant to a Presidential Memorandum.

Mnuchin outlined his vision for America with a China-sponsored Government Explicit Guarantee on MBS.

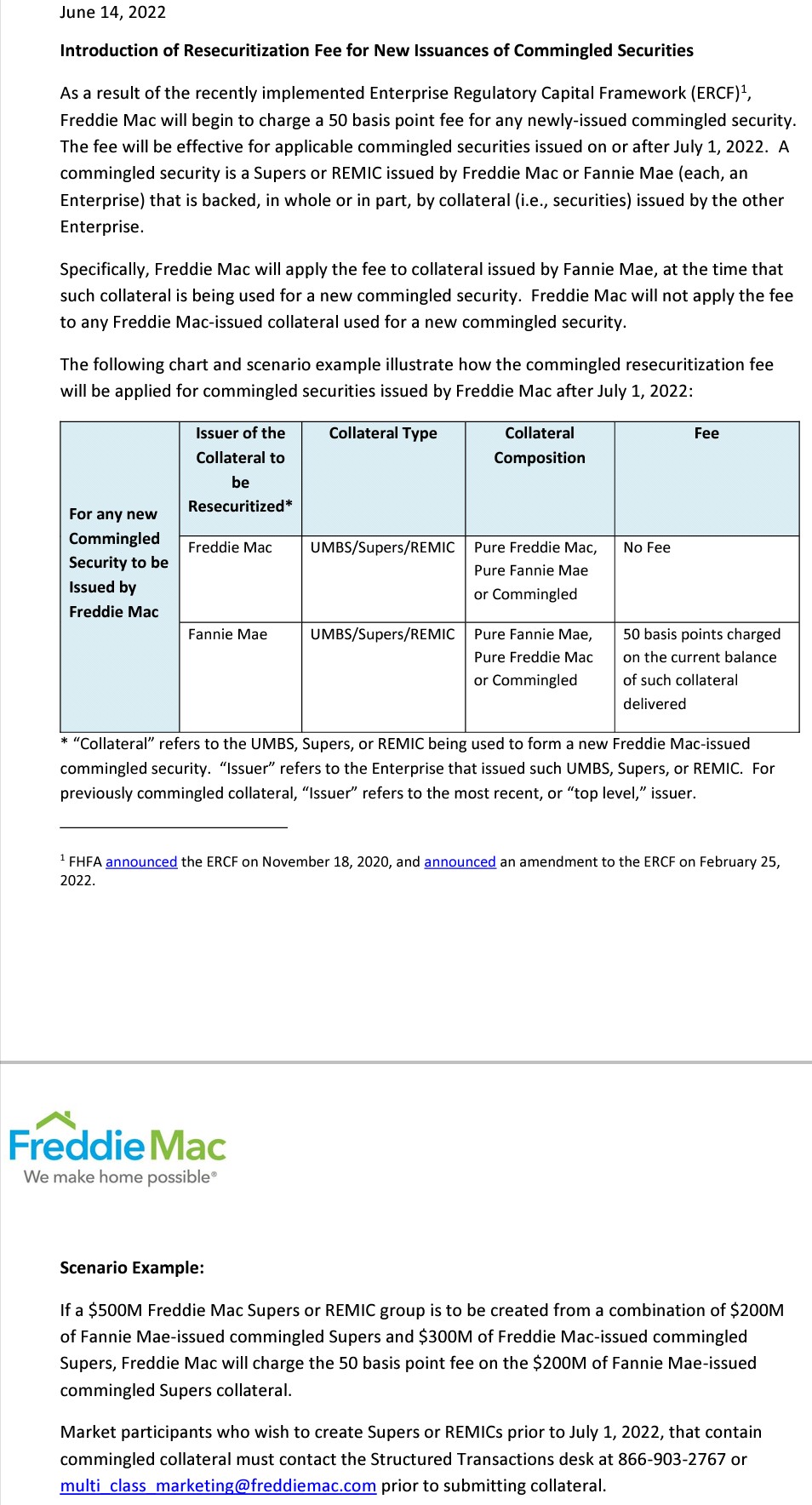

This is why the FHFA first priced the Resecuritizations in FnF, unveiled by Freddie Mac in June 2022, at 50 bps. Later it was changed to 9.375 bps when they realized that the Trump Administration got it all wrong in its broad alliance with China, because Trump was just attempting to substitute the plan for the release of FnF in the making since 2011.

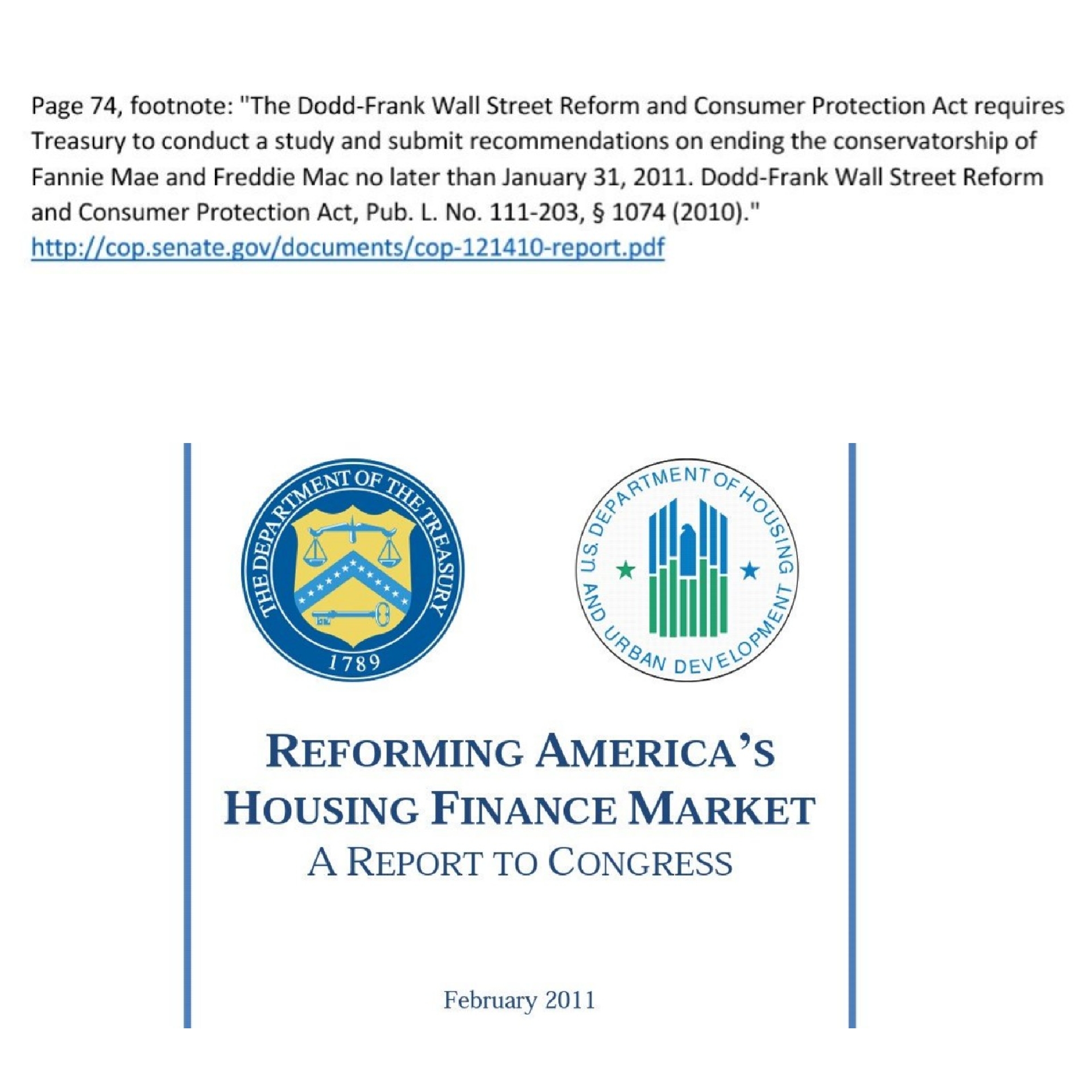

The U.S. Treasury and HUD submitted a Housing Finance System revamp on February 2011, with a Report to Congress 11 days after the deadline, which is typical in the UST, at the request of the Wall Street Reform and Consumer Protection Act of 2010, better known as the Dodd-Frank law (the same law that makes FnF and the banks release an annual Stress Test), as "recommendations on ending the Conservatorships, no later than January 31, 2011".

The reason why Trump, China and Goldman Sachs concealed it, is because the 3 options outlined, have one thing in common: a Privatized Housing Finance System, which means that the guarantors are subject to the Basel framework for capital requirements or, as the option 3 states: "Stringent capital requirements".

In brief:

1- Privatized Housing Finance System + targeted assistance: FHA, USDA, VA.

2- 1 + Govt guarantee in crisis.

3- 1 + Govt Catastrophic-Loss reinsurance.

DeMarco began to work on it right away:

Then, the CSP, UMBS, CSS, pilot programs with the States' HFAs and, finally, the Resecuritizations unveiled by Freddie Mac in June 2022 that allows the option 3 with a Govt Catastrophic-Loss Reinsurance, which means that the MBSs are still guaranteed by the private guarantors and the Reinsurance is triggered upon bankruptcy of the guarantor.

It can be private reinsurance and then, we would be talking about either option 1 or 2.

This is why the FHFA repriced the Resecuritizations to 9.375 bps.

The idea that Trump wanted to put an end to the conservatorship is laughable, when he imposed the NWS 2.0 (the Common Equity is still being transferred to the UST, through the offset -reduction of Retained Earnings- when the SPS LP is increased for free in the same amount as the Net Worth increase in the quarter. This effect is concealed when the gifted SPS are missing on the balance sheets.) and he just wanted to supplant the law in force and the ongoing process for the release from conservatorship required in the Dodd-Frank law and the Separate Account plan in accordance to the law from the onset, because he also called for a swap SPS for Cs ("reprivatization" slogan peddled also by Bill Ackman) and exercising the Warrant (an illegal collateral in the Charter Act)

But the plotters are insatiable and they insist on their plan to supplant the original mandate by law.

So, because it was a requirement by law and submitted in a Report to Congress, whereas the Mnuchin plan was unveiled pursuant to a simple Presidential Memorandum, the plotters directed a rookie representative to introduce the bill HR 5549 on September 18, 2023: "To require the Secretary of the Treasury to submit to the Congress completed proposals for the termination of the conservatorships of Fannie Mae and Freddie Mac", a replica of the mandate in the Dodd-Frank law of 2010.

More "back to the future", like those calling for a "restructuring" in FnF today, thinking that we are still with $400 billion capital shortfall like in September 2008.

BOMBSHELL. The Lamberth court aims to replicate what happened in 2008 with a dividend on the JPS that was declared before FnF were placed in Conservatorship, but not paid.

At that moment, the Restriction on Capital Distributions applied and the dividend was suspended.

It turns out that, according to a Fannie Mae press release, because this dividend was declared before, they made up the idea of "an outstanding obligation to be honored" as an excuse to break the law, even before the record date September 15, 2008. The press release follows up stating that the conservator and, surprisingly, the Treasury Department, authorized this dividend payment for September 30, 2008.

In the Lamberth court, phony proceedings have been stretched to the maximum, ending up in a sham trial, so the final order falls pretty close to a final resolution of Fanniegate but it has to be before, so, even though this resolution renders the original claim meritless, the FHFA and the UST will claim again that it's "an outstanding obligation to be honored".

They aren't interested in a resolution of Fanniegate, just in this Securities Litigation claim that acts as a back dividend on a non-cumulative dividend JPS and the payday for the corrupt attorneys.

The evidence is that Fairholme asked about the existence of a Separate Account plan in 2019, that is, whether the dividend to UST was, in truth, an assessment applied towards the reduction of the obligation with the taxpayer, SPS (screenshot with the RFP12 in the tweet below) and, after multiple breaches of the subpoena to Treasury to comply, Fairholme withdrew the motion to compel compliance with the subpoena that would have given response to the existence of the Separate Account plan (brief seen in the tweet)

It's imperative to put an end to Fanniegate before the judge's final order, so the judge will have no other option than to declare a Judgment Notwithstanding the Verdict (JNOV) and no obligation emerges with regard to the fiction of implied contract.

FHFA,PLAINTIFFS & LAMBERTH SEEK "AN OUTSTANDING OBLIGATION TO BE HONORED", BEFORE THE #FANNIEGATE RESOLUTION THEY THWARTED IN 2019

— Conservatives against Trump (@CarlosVignote) November 20, 2023

Just like the div on JPS declared,but not paid. UST illegally gave OK on 9/30/2008.

RFP12 asked about a Separate Acct plan.Withdrawn.@TheJusticeDept pic.twitter.com/R1Ig4hLxim

When the FHFA suspended the capital classifications, explained yesterday, it stated that the capital requirements aren't binding during conservatorship, which is a misleading statement because they are thresholds necessary to comply with its power: "put FnF in a sound and solvent condition", and also, the fact that there was a mandatory release Undercapitalized, that, although struck by Calabria with HERA, is evidence of the financial rehabilitation process during conservatorship. Restore capital levels to a minimum, or before at the discretion of the FHFA Director. A conservatorship isn't a state to make the FHFA Director become the CEO of the enterprises during 15 years, as the current management and the BOD don't have powers, regardless that this fact is being concealed to transmit a sense of normalcy in this state. For instance, FnF are parties in the Lamberth court, illegally signing all the court briefs.

It has more to do with the word "may" in the conservator's power ("May put FnF..."), jointly with the "take any action authorized by this section, in the best interests of the Agency" in its Incidental Power.

So, they are always binding and it can only mean that the FHFA has some leeway during conservatorship to fix their operations because it's supposed that the companies are bleeding or, as Freddie Mac explained better what "may" and the FHFA-C's Incidental Power might be about:

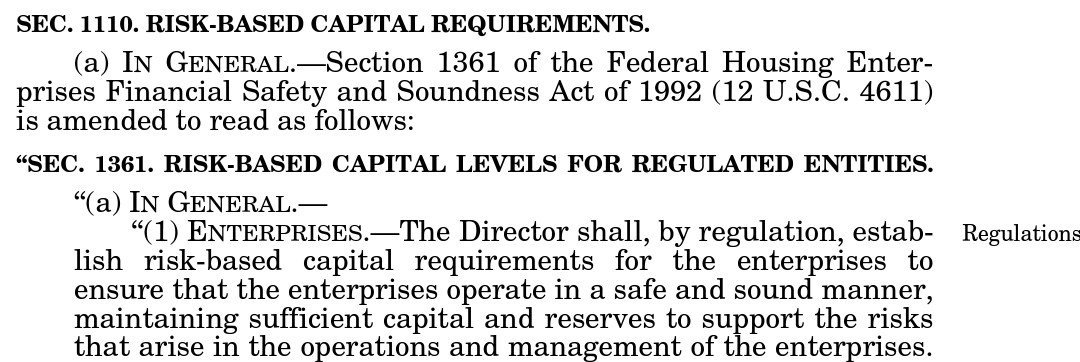

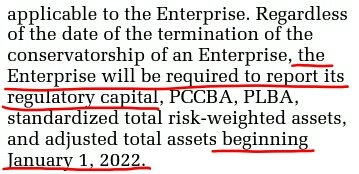

By the way, I guess you noticed that the amendment of HERA of the FHEFSSA's Minimum (Leverage) Capital requirement, was related to "revise" the existing percentages (1992 FHEFSSA), but until then, FnF have been posting the figures with the old requirements every quarter in their SEC filings and also in the FHFA Reports to Congress, because they are statutory, regardless of the FHFA's "not binding" remark. So, the game between Calabria withholding the publication of the ERCF tables until January 1st, 2022, despite being effective since February 16th, 2021, and the congressmen French Hill and McHenry, of keeping the ERCF tables from the Congress (now in the 2022 Report to Congress) at the time of the annual testimony of the FHFA director, so congressmen make up the figures in a convo with Sandra Thompson: "$100B vs $300B. I'm a former examiner", said one of them ($100B was the Net Worth at the time, not the Core Capital, and $300B was the official capital shortfall, not the Minimum Leverage Capital requirement. Adjusted $400B capital shortfall over $207B capital requirement), is pointless, because there is always the Minimum (Leverage) capital requirement with the old percentages, posted every quarter since day one.

There is nothing new "as of the passage of HERA", as the low profile DOJ attorneys peddle all the time, but a continuation of the FHEFSSA (and the Charter Act with the old low cost UST backup), as amended by HERA.

Agreed. Navycmdr said that it was judge Lamberth's Final Order, when in reality it was a Proposed Final Order filed by the parties.

Totally misleading.

He posted this lie here and also on Twitter: "overnite final order".

FHFA suspended the capital classifications, not the FHEFSSA's section Capital Classifications.

This is evidence of a Separate Account plan, because it simply relieves the FHFA of having to change the Capital Classification all along, first from Critically Undercapitalized to Significantly Undercapitalized, then to Undercapitalized and finally, Adequately Capitalized.

Therefore, the Separate Account plan is kept secret.

We can read below that it was done "in the best interests of the market", which is an addition it made up, to the "in the best interests of FnF or the Agency" set forth in the conservator's Incidental Power.

This is because the Conservatorship is being used to grant good deals to the investment banks and hedge funds, in the sale of NPL, RPL and REO inventory.

No. The Restriction on Capital Distributions is when it makes FnF be undercapitalized in general. It doesn't say "the regulated entity would become classified Undercapitalized pursuant to section 1364 (a)(2)".

And it starts with "IN GENERAL".

Besides, it's set forth in the FHEFSSA with an amendment of HERA in its Chapter: "Prompt Corrective Action".

So, as always, it isn't HERA as you claim, but the FHEFSSA.

The Conservatorship was imposed because it's laid out in the SEC. 1367. AUTHORITY OVER CRITICALLY UNDERCAPITALIZED REGULATED ENTITIES.

(a) APPOINTMENT OF THE AGENCY AS CONSERVATOR.

So, the preservation of capital is of supreme importance and the restriction on capital distribution is a prompt corrective action for a reason. That's why the dividend payment (a distribution of Earnings -Core Capital-) was suspended on day one. It was not imposed on a whim by the conservator, as the low profile attorneys seem to suggest.

And this is why a Non-Cumulative dividend JPS is recorded in the Core Capital (loss-absorbing capacity capital related). And why a JPS gets a higher dividend rate than the interest rate on similar obligations from the same issuer (risk of dividend suspension). Whereas the SPS are not regulatory capital.

It's pathetic to see how you, another attorney, cite khtomp19 as source of your statement, instead of citing the law or posting a screenshot of the law.

Kthomp has explained this before. And I think this explanation is correct.

The regulatory capital requirements aren't demanded in HERA, but in the 1992 FHEFSSA, the law enacted exclusively for the safety and soundness, establishing capital ratios for the first time, and requested in a GAO (auditor of the FHLBanks' failed RTC and Funding Corp scheme with DeMarco) report the year before, by the way.

More evidence that khomp19 is the former DOJ attorney Mr. Soopprise, because the DOJ is also obsessed with HERA to conceal the FHEFSSA: "As of the passage of HERA...."

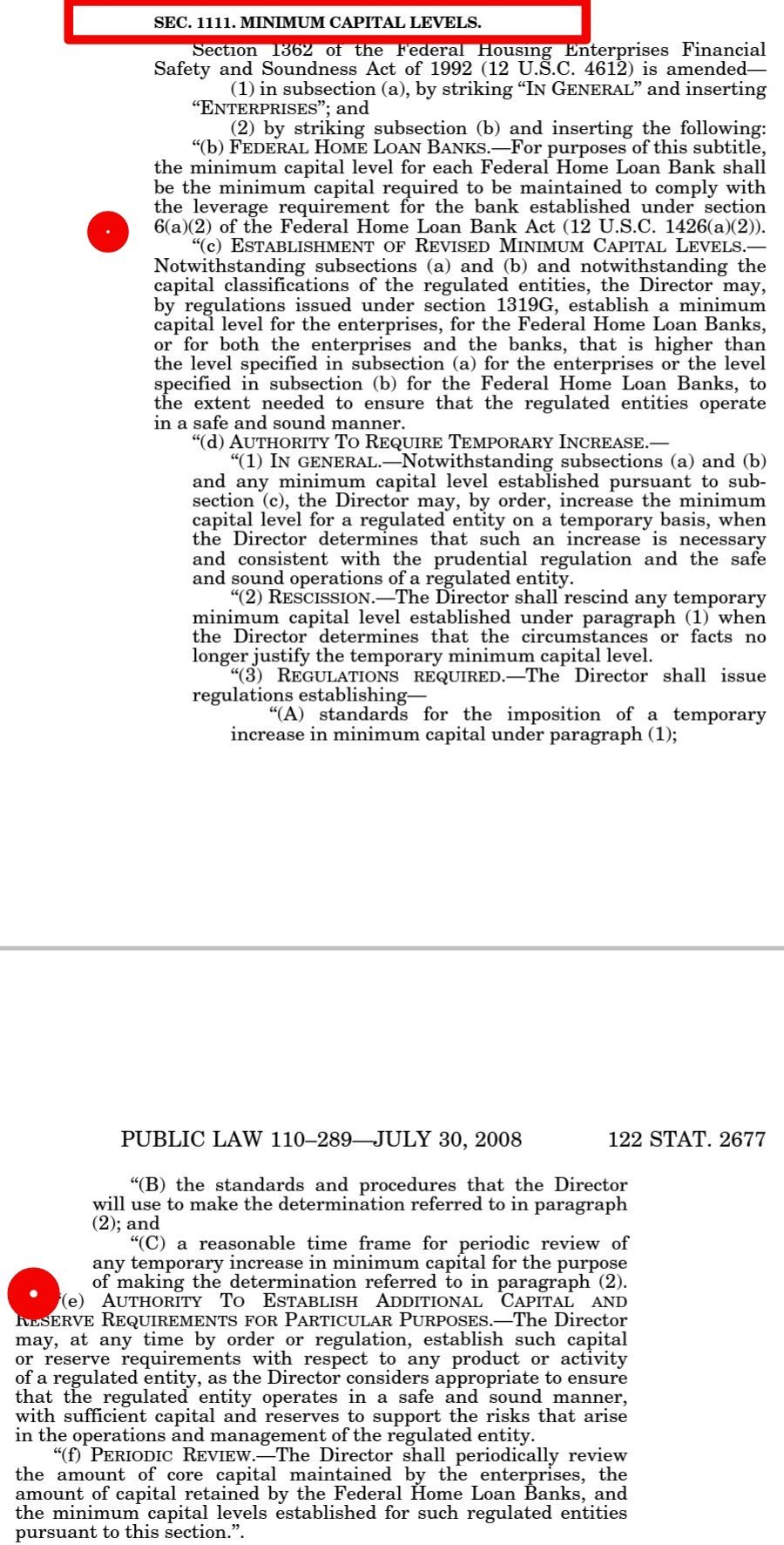

It's a law passed by Congress (HERA) that directs the FHFA Director to issue regulatory capital requirements. There are two types of capital requirements: risk-based and minimum.

One thing I don't know is why Lockhart and DeMarco never issued capital standards, or why Watt waited until his term was almost over to do so. At least Calabria fulfilled this requirement, though his final rule wasn't published until 20 months after he took office.

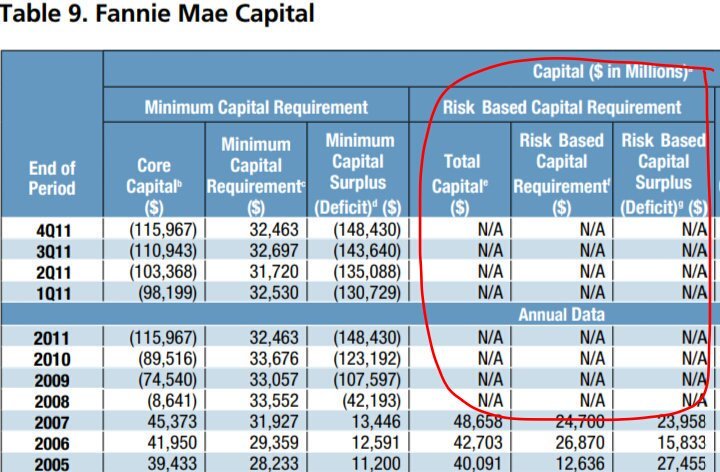

Screenshot shows the moment FHFA prohibited this payment of Securities Litigation judgment, in the Preface of the July 20, 2011 Final Rule that amended the definition of capital distribution in the FHEFSSA, to include this case.

The FHFA stressed that it was applying the Restriction on Capital Distributions in the FHEFSSA (U.S. Code §4614(e)), which was "supplemented and shall not be affected or be replaced", by the CFR 1237.12 enacted in this same Final Rule, for the phases 2 and 3 of the Separate Account plan: capital distributions (deplete capital) for their recapitalization (build capital) outside their Balance Sheets.

The reader should be aware that this same screenshot is being used as a masterpiece of explanation of the conservator's role and endgame.

In the case of Commons, it's our own money (Common Equity) being distributed. So, no big deal. The shareholders have the same wealth before and afterwards. It's like a dividend payment.

On the other hand, in the case of the non-cumulative dividend JPS, it's our own money too. So, the JPS holders are stealing from the shareholders' pockets in broad daylight, because this payment is restricted.

FHFA's Sandra Thompson now shows outrage for the idea that valuable regulatory capital of the Government-Sponsored Enterprises will be allocated to the corrupt attorneys, and she requires to see the plaintiffs' proposed plan of allocation beforehand.

Also, it proves the fact that she has the intention to commit a felony: this payment of Securities Litigation claims, is a capital distribution, restricted when FnF are undercapitalized. Once spotted, it uncovers the Separate Account plan, as dividends and today's SPS LP increased for free, are also capital distributions restricted in the same statutory provision, U.S. Code §4614(e). Thus, the exceptions to this restriction kicked off. The outcome is that the Common Equity is held in escrow and the Equity holders didn't suffer any damage, other than Punitive damages. But it wouldn't be the case for this payment.

This happens when you use the United States courts, colluding with hedge funds that act as counterparty in the phony court proceedings, in a plan to save the image of the FHFA (The use of courts for a PR campaign), in its clear Separate Account plan according to the law, a plan that already happened in the past with both ST and DeMarco (1989 bailout of the FHLBanks: statutory provision entitled Separate Account) and corroborated by justice Alito ("Rehabilitate FnF", which has only one meaning in a financial company, adding the case for actions that may increase losses or risk "beneficial to the public", instead of the text as it's written: "in the interests of the FHFA". So playing with the word "beneficial" and "Federal Agency/the public", but the Incidental Power he was referring to, was never meant to authorize taking their regulatory capital away. That's not "authorized by this section") and judge Willett (5th Cir.) that explained what justice Alito missed, in a prior ruling over the same case ("Any action within the enumerated powers": Rehab power)

This is why it's been determined that both judge Willett and judtice Alito were synchronized. One interpreted the first part of the Incidental Power ("Take any action authorized by this section,...."), the latter the second part ("...in the best interests of FnF or the Agency"). But both parts must be considered together.

The conservator saw an opportunity to use this Incidental Power for a Separate Account plan that is financially rehabilitating FnF, and mislead about it "in its best interests".

Good for you! At some point, the conservatorship will be over, the Separate Account, unwound, and the powers and rights returned to the Equity holders, the management and the BOD, as usual.

ST NOW OUTRAGED: PLAINTIFFS OMITTED A PLAN OF ALLOCATION

— Conservatives against Trump (@CarlosVignote) November 18, 2023

The attys demand fees +nontaxable costs taken from the FnF's coffers,for collaborating in a campaign to save:

-The FHFA's image after a Separate Acct plan

-@TheJusticeDept's vicarious liability

-Back divs on JPS.#Fanniegate https://t.co/lEWcGP2OUL pic.twitter.com/WEhFRBYwlf

The settlement is about the 8 Securities Law violations during Conservatorship, as part of Punitive Damages required to the DOJ and also, to the corrupt litigants, since the current economic harm is fully redressed once the Separate Acct plan is unveiled.

The Separate Account plan and the Govt theft story is all the same and it had the purpose to prevent the stocks from trading at their fair value all along.

8 Securities Law violations:

1- SPS increased, instead of issued, aiming to skip the December 2009 deadline on purchases in the Temporary authority of Treasury in the Charter Act (UST backup) in the case of high yield SPS. The ultimate goal was to use this high yield for a Separate Account plan, since the original low cost funding prevails.

2- The SPS increased for free are missing in the Balance Sheets. Financial Statement fraud. Goal: peddle the lie of "FnF continue to build capital through Retained Earnings" (Ackman). It carries an offset that wipes out the Retained Earnings just built.

3- A charge on the Income Statement equal to the SPS increased for free, in order to post always $0 EPS.

4- Fannie Mae posted this charge in the 1Q2020 results, when no SPS was increased for free.

5- Stock price manipulation.

6- Dividends paid out of unavailable funds for distribution. Although part of the Separate Account plan, FHFA has used a Securities Law violation to that end.

7- The value of the Warrant was credited to Additional Paid-In Capital account.

8- CRT operations, barred in the Charter's Credit Enhancement clause and a scam to misrepresent their financial condition, not suitable for collateralized loans.

PUNITIVE DAMAGES :

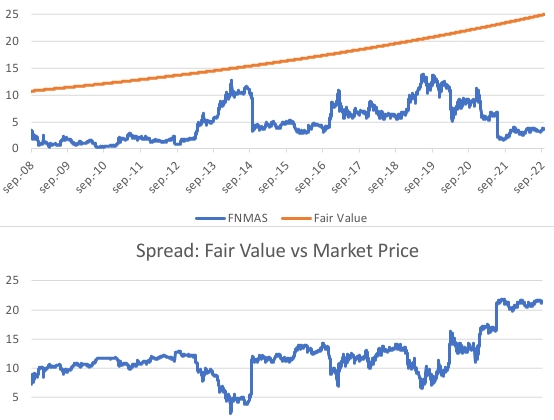

A 0.5% compound rate, IRR (taken because it's also the spread over Treasuries chosen in the UST backup) on the average spread Fair Value versus Market Price (equal to half a JPS) during 15 years = $0.97 on a $25 par value JPS.

A common stock matches the amount for a $50 par value JPS.

The flawed accounting standard chosen for the upfront g-fee (Deferred Income) that should have been renamed Delivery Fee, could mean a third round of Punitive Damages ($4.8B each)

"AIG is not a comparable", says the attorney FOFreddie.

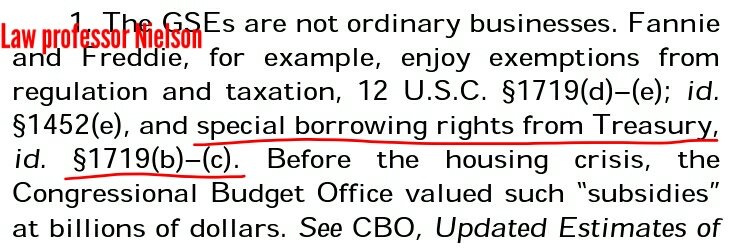

Really? Isn't it better to say that it's because FnF ARE NOT ordinary businesses? They are congressionally-chartered private corporations with a UST backup in exchange for their Public Mission that no longer exists: no g-fee subsidized anymore, the Duty to Serve geografically is what any company is after nowadays, and the countercyclical role is about secondary market operations in a financial crisis, unnecessary during an economic crisis as seen in the COVID crisis.

Law professor Nielson, who represented the FHFA in the Supreme Court when the FHFA was declared illegally structured, spotted the UST backup right away:

The section Purposes of the Charter Act, where the Public Mission is set forth, states what could be considered that the UST backup is only as a last resort, which is what has happened upon capital deficiency in FnF in early conservatorship (See my signature chart below), after FnF had tapped the private capital market for funds with massive issuances of both JPS and Common Stocks, which could be what in the end lies behind the Purpose #2. So, FnF did their part in the Charter.

The operations are financed by both Debt and Equity. FnF needed Equity. The authority of UST in the law, is a UST backup of FnF "at rates that take into consideration the Treasury yields as of the end of the month preceding the purchase" (subsection (c)), and it's about purchases of any (subsection (b)) redeemable obligations, such as SPS (obligations in respect of Capital Stock, as stated in the SPSPA)

It's time to get rid of all the attorneys surrounding Fanniegate.

Do they understand what Prompt Correction Action means? And why the JPS is recorded in Core Capital (due to the non-cumulative dividend feature or loss-absorbing capacity capital-related). By the way, they should begin learning that the law in force is the FHEFSSA if all HERA did, is to amend the FHEFSSA and the Charter Act, and even the FHFA that was created by HERA but as successor of OFHEO created in the FHEFSSA, something that judge Sweeney and the Federal Circuit ignore.

Imagine reading this chapter of HERA entitled Prompt Corrective Action and later claim that the law in force is HERA, instead of the FHEFSSA.

Chapter concealed by the parties and the judges in court. Maybe it's the "Prompt" what they don't understand. Or is it "Corrective"? Is it "Action"? Let alone what comes next "capital distribution" despite its definition set forth in the FHEFSSA (There you are! That's why they conceal the FHEFSSA. Concealment of the financial definitions, as requested by the Mnuchin's Treasury in the UST Housing Reform, "Treasury recommends Congress to repeal the statutory definitions (Source)", like Total Capital, capital distribution, Undercapitalized, Core Capital, etc), plus the supplemental section enacted in a Final Rule on July 20, 2011 by DeMarco, coinciding exactly with his Time Limitation as Acting Director, for the continuation of the Separate Account plan, but his time capital distributions applied towards the Recapitalization (outside the balance sheets: Separate Account wording. CFR 1237.12), to capture the moment when the SPS were fully repaid with the phony dividend to UST (10% and NWS dividends). Assessments in the form of capital distributions, not actual dividends (restricted and unavailbe earnings for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts)

The cram-down people wipe out JPS, plaintiff Joshua Angel.

What part didn't you understand when I said that their Net Worth is $118 billion, but $304 billion SPS oustanding?

You people think that you can use your frivolous lawsuits to give up the company to the Treasury, thinking that later you will be rewarded with a good deal for the JPS in a swap for Cs and even back dividends in the Lamberth court.

Finance doesn't understand of shenanigans, like the assumption that it will be just because Calabria said in his book that Mnuchin said he wanted it.

Now, you all will have to pay the Equity holders Punitive damages for stock price manipulation, and anyone peddling the same government theft story in formal documents (Pagliara's book, etc). $4.8 billion.

Is this why judge Sweeney maintains your lawsuit artificially active?

I will rephrase the part of Deferred Income in the prior post, with regard to the upfront g-fee that should have been renamed "Delivery fee":

(the ones that pay this fee, the banks, aren't the beneficiaries of the guaranty service)

BOMBSHELL. The FHFA takes advice from our negotiator and declines to file the proposed order of final judgment, that was requested by judge Lamberth, knowing that it would translate into an intent to commit a felony: a capital distribution, restricted when FnF are undercapitalized.

The key: it uncovers the Separate Account plan carried out since day one, because the dividend payments and the SPS LP increased for free as compensation to UST, are also capital distributions.

The FHFA has been repaying the SPS and recapitalizing FnF, with assessments sent to UST (all of it, as dividends are restricted. Cumulative dividend on SPS though), just like the FHLBanks in their 1989 statutory provision entitled: Separate Account, although they shamelessly use it to pay only interests, instead of using it also for repayment of the principal of the RefCorp obligation at maturity with the excess amount. The FHLBanks applied this excess amount "Credit due to FHLBanks", towards reducing the period of interest payments of the 40-year RefCorp obligation, as Funding Corp paid only interests, leaving the principal of the obligation unpaid (The FHLBanks are the Equity holders of Funding Corp, the entity that issued the 40-year bond), as set forth in the statutory provision (invested in zero coupon Treasuries, so it matches the principal of the RefCorp obligation at maturity)

With FnF, the assessments sent to UST were in the form of capital distributions, under the guise of dividends and gifted SPS (deception thanks to the FHFA-C's Incidental Power), which are restricted and cannot exist, using the exceptions to the Restriction on Capital Distributions in the law (U.S. Code §4614(e)) and the July 20, 2011 CFR 1237.12, besides the fact that they weren't actual dividends if there weren't earnings available for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts (A company needs to replenish this account in the first place.)

A negotiation is about posting thoughtful in-depth financial analyses, that render the other negotiators' lawsuits, meritless.

A level playing field. This is why the litigants and their shills on social media are annoyed with the idea that there is another negotiator.

#BOOM. THE PARTIES SUBMIT A MOTION FOR A 3-DAY EXTENSION OF TIME TO FILE A PROPOSED ORDER

— Conservatives against Trump (@CarlosVignote) November 15, 2023

It seems that the @FHFA was told that there are rules.#Fanniegate $FNMA $FMCC $FNMAS https://t.co/ewQOcagWFf pic.twitter.com/XRl7K0Teyp

kthomp19 applies "Finance for attorneys",i.e., all made up.

The JPS are valued at par value in Equity regardless of the market price, but they ARE NOT part of the Net Worth if there is $304B SPS outstanding, but only $118B Net Worth. It was explained in this reply.

He adds a new lie in this post:

The market price of the juniors has absolutely nothing to do with FnF's capital levels.

BOOM. FnF have more room for Reserve release "Benefit for Loan Losses" with their Allowance for Loan Losses, ALLL (A Loan Loss Reserve for expected losses, required in the CECL accounting standard)

The Capital Rule states that there is a 0.6% of RWA limit in the amount of ALLL that can be Tier 2 Capital, for the calculation of the Total Capital that has to meet the Risk-Based Capital requirement.

.jpeg)

The conservator has violated this rule in the ERCF tables, because FnF record the entire ALLL ending balance as Tier 2 Capital.

We've seen in FnF a reduction of the ALLL in the last two quarters and, likely, we will see more in the coming quarters or later on, though there is no obligation to bring the ALLL within the Tier 2 Capital limit.

Just the idea that the ALLL is overblown, makes the Capital ratios (for unexpected losses) shine.

But the shareholders rather see the reserve in the CET1 (Retained Earnings. Net Worth) than in ALLL (asset write-down: it assumes that the credit loss already occurred)

For instance, as of September 2023, Freddie Mac records the entire ALLL $7.4B ending balance as Tier 2 Capital, with data taken from the ERCF table and the FHEFSSA definition of Total Capital, TC = Core Capital + ALLL general reserve (not against specific assets) aka Tier 2 Capital, yet there is a $5.8B limit.

The plotters hate the FHEFSSA, to impose their "Finance for attorneys".

Mnuchin:

More detail:

FULL ALLL: TIER2 CAPITAL & OVERBLOWN

— Conservatives against Trump (@CarlosVignote) November 15, 2023

More Common Equity held in escrow.

After spotted,ALLL reduction 2 qtrs in a row,in favor of Retained Earnings(CET1,NW)

ALLL: Tier2 limit >0.6%RWA,though FHFA breaks its rule to conceal an outsized ALLL:$B

FNMA 8.7>8.1

FMCC 7.4>5.8#Fanniegate https://t.co/eV1mSgJ8QC pic.twitter.com/pVI3ISwH6B

Hindes announces more letters part of "Finger-counting Finance" and the "Finance for attorneys" series, aiming to rip off the FnF shareholders, after one of his latest was even sent to the Secretary of the Treasury.

Latest:

-"What are they waiting for?"

-"When do we get our companies back?"

Coming up:

-"Why would you do that?"

-"Can you believe it?"

-"You don't say?"

-"Yes sir. It sounds like a plan."

-"Meet you in the middle."

-"$100B+ cash equity. Rum commodore said so."

Gary Hindes should read more and write less.

He conceals the existence of a scheme with assessments sent to Treasury, in the form of capital distributions and under the guise of dividend payments (restricted and unavailable earnings for distribution as dividend, with accumulated deficit Retained Earnings accounts. So, no actual dividend was ever paid because it cannot exist), using the exceptions to the Restriction on Capital Distributions in the law, U.S. Code §4614(e).

The FHFA-C's Incidental Power allows it to mislead during the process of rehabilitation of FnF.

A NWS dividend was necessary because the 10% dividend prompted the capital deficiency, draws from UST and more SPS (death spiral)

The Net Worth is never a variable to measure the soundness in a financial company, but the Core Capital, CET1, etc, where is included the Retained Earnings account that absorbs future unexpected losses (Capital ratios)

Remember that the expected losses are already covered by the Loan Loss Reserve (CECL accounting standard), in the form of Allowance for Loan Losses (Asset write-down) worth $7.4B and $8.7B in Freddie Mac and Fannie Mae, respectively, as of end of September, 2023, that could be released down the road if the management's expectations change, as witnessed the last two quarters, for instance.

ALLL isn't, therefore, recorded in the Net Worth, but it's recorded as TIER 2 Capital for the Capital ratios (the Total Capital that has to meet the Risk-Based Capital requirement), with some limitations, because, theoretically, they are expected losses and the assets already written down.

So, we need the Capital ratios, not the Net Worth, since FnF are building SPS in their Net Worth, when they increase the SPS LP for free in the same amount as the Net Worth increase in the quarter, and SPS don't absorb losses. These people think they found the geese that laid the golden eggs, increasing the Net Worth with gifted SPS (currently concealed, as these gifted SPS are missing on the Balance Sheets. Financial Statement fraud)

This is why the most important piece in the capital structure, the CET1, exists, where Retained Earnings is included. JPS are AT1 Capital ("the others") and the SPS aren't even considered regulatory capital due to its cumulative dividend feature (no loss-absorbing capacity)

SPS LP increased for free as compensation to UST, is another capital distribution (read the definition in the FHEFSSA) restricted, that falls squarely within the prior scheme of using the exceptions to the restriction. In this case, for the recapitalization (CFR 1237.12) with the Common Equity held in escrow with the offset (reduction of Retained Earnings) attached to this SPS LP increased for free. The image shows how the Common Equity is escrowed, pending unwinding the operation (FnF don't post these gifted SPS on the Balance Sheet, to evade showing this operation with the offset)

Their Adjusted Retained Earnings accounts stand at $-217B together.

But $236B with the Separate Account plan.

The scammers seek to undermine the Common Equity. The don't know that the JPS need the Common Equity in the first place, to recover their par value once FnF resume the dividend payments (Adequately Capitalized +Table 8: Payout ratio)

Nobody with half a brain mentions Nationalization during Conservatorship.

Sick. I said that you lie,Bradford. Not the SCOTUS.

Bradford continues to lie about what the SCOTUS said, here

and with the alias LuLeVan:

according to Scotus, the FHFA can do whatever it wants,

Huge adjusted capital shortfall($402B combined)over Min Leverage C.requirement, is driven by the Retained Earnings accts w/ Accumulated Deficit:

— Conservatives against Trump (@CarlosVignote) November 12, 2023

Official/Adjusted($B)

FNMA: -60/-134

FMCC: -38/-83

RE, only acct that absorbs future (unexpected) losses, not capital stock.#Fanniegate https://t.co/io1Qr07Fw4 pic.twitter.com/AjFQXuM1WL