News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The attorney Hamish hasn't filed the appellants' brief on the scheduled date, due on March 25th, 2024, in a different case (Wazee. Court of Federal Claims with judge Sweeney) than the case in the Lamberth court.

Pacer doesn't show it on its docket, with the docket updated.

Check it out yourself:https://www.pacermonitor.com/public/case/52102413/Wazee_Street_Opportunities_Fund_IV_LP_v_US

Because I don't have subscription to Pacer, I can't be 100% sure, but it usually works fine for all the cases.

This is important because Wazee was the first case that challenges the ongoing NWS 2.0 or Common Equity Sweep through the offset attached to the SPS LP increased for free every quarter (Image), equal to the Net Worth increase, brought up by the attorney Hamish Hume in an amended complaint.

Have a look to the amended complaint in this tweet:

NO GLIMPSE OF LEGALITY W/ LAMBERTH

— Conservatives against Trump (@CarlosVignote) March 20, 2024

Atty Hamish didn't challenge today's Common Equity Sweep. It'd hinder his claim of 1-day share price drop rebate on 3rd amdt-day.

To avoid be sued, NWS 2.0 brought up w/ Wazee(CFC) in amended complaint.Appeal due 3/25.#Fanniegate @TheJusticeDept https://t.co/QPwJTUOf1G pic.twitter.com/PXHIHYNBcd

A class action is superior to other available methods for fairly and efficiently adjudicating the controversy.

CORRECTION. Ackman didn't remove "re-privatization" from his GSE slide of this year, published on February.

At the time, I had a look to the bullet points and spotted that the sentence with "re-privatization" that was written at the bottom of the slide in black letters the prior year, was omitted.

Yesterday I checked it out and realized that Ackman had made the executive decision to "upgrade" it to the top of the slide, as a headline, and written with blue marking paint. This is why it went unnoticed.

This isn't just speculation because it involves felonies, like the coverup of statutory provisions, regulation and basic financial concepts (Making False Statements), an elaborate plan of deception for stock price manipulation and assault attempt on the ownership of FnF (Common stock. JPS holders have "other ownership interest"), colluding with the FnF management and the conservator with their Financial Statement fraud (SPS LP increased for free and its offset, absent from the Balance Sheets) providing the alibi and, the key for being liable for $4.8B in Punitive Damages among all the plotters, it's carried out through formal documents that have more influence on the market price than just an opinion on social media "free speech", regardless of being a letter to Pershing's shareholders, or Hindes with: "To my partners". It's an official statement with the pomp of a corporate document and written as executive of that corporation, that it's made publicly available by simply posting it online and not sent by private email or mail to each shareholder/partner as it should be.

The same with the court briefs (abuse of court process), articles in SA with an editor, posted later on all the financial websites for the stocks in question, books, financial analyses, etc.

Playing the fool isn't an option. Attorney for Berkowitz, Bhatti, Robinson, Collins and Rop, David Thompson, in a conference call hosted by Pagliara:

With respect to capitalization, I am not a regulatory lawyer. I am a litigator....That's being watched by a number of sofisticated lawyers...

Speculation? It's stock price manipulation/abuse of court process.

A compensaton of $4.8B in Punitive Damages has been requested to all those peddling the government theft story in formal documents, based on the coverup of statutory provisions, regulation and basic Financial concepts (Dividend, a distribution of earnings. Unavailable with Accumulated Deficit Retained Earnings accounts)

For instance, Bill Ackman has recovered the "re-privatization" in his latest letter with Pershing, that was removed from his latest GSE slide.

potential re-privatization in the event former President Trump is re-elected.

The foreclosure reports are included in the quarterly Earnings reports of FnF.

Not only FnF are required to post all available data under SEC rules for any Public Company, but also the management is compelled to post a comment about them.

The FHFA just lifts all their data from the reports with the SEC (10-K forms) and creates its own report several weeks later.

This is like HUD before the FHFA was established for the first time in 1992 (formerly known as OFHEO). HUD was mandated by law to require reports from the enterprises.

The deliquency rates are also shown in their monthly volume data on their websites. February file just posted in Freddie Mac.

Therefore, these quarterly FHFA reports are always outdated.

More evidence that we don't need this Federal Agency owned by the hedge funds, investment banks and special interest groups (Moelis, Urban Institute, CATO Institute, etc.)

It has limited powers and it does it all wrong:

-The PLMBS were barred in the Credit Enhancement clause of the Charter Act, just like today's CRT operations;

-Separate Account;

-Their NPL and RPL are being auctioned off to the hedge funds at bargain prices, instead of the Guaranty Mortgage Securitization business of taking possession of the collateral and bundling the RPL into UMBSs again;

-REO inventory sold to minority- and women-owned businesses, LGTB associations, Neighborhood Associations,...;

-REO inventory sold to a Goldman Sachs subsidiary (This subsidiary won all the sales of Fannie Mae in early conservatorship, thinking that we would never know that Goldman Sachs was the parent company)

-Etc.

This explains the "wards of the state" remark by the chamber investor Ackman, expecting good deals down the road from the FHFA (Utility Model)

Navy Hedge Fund continues to promote the hedge fund manager Alec Mazo's flawed diatribe.

First, he uses the Capital Reserve, an invalid capital metric in the FHEFSSA, instead of Core Capital, Total Capital, CET1 and Tier 1 Capital.

He follows Mnuchi-Calabria's "Capital Reserve End Date" in the 6th PA amendment of January 14, 2021 (when the Capital Reserve meets the capital requirements, instead of what is mandated in the FHEFSSA: Core Capital greater than the minimum Leverage ratio or Minimum Capital level, for the Capital Classification of Undercaptialized. A Total Capital greater than the Risk-Based Capital requirement, for the Adequately Capitalized threshold), as his "capital target to exit Conservatorship". All made up. If any, it's the flawed threshold CET1>3% of Total Assets, that Mnuchin and Calabria came up with, in the same PA amendment. This outsized threshold has been snubbed, as it's well above the ERCF that came into effect one month later, of Tier 1 Capital > 2.5% of Adjusted Total Assets (Leverage ratio), and way above the prior MANDATORY release in the FHEFSSA struck by Calabria's HERA (The Core Capital > minimum Leverage ratio, mentioned above).

Nowadays, we are using CET1 > 2.5% of ATA, for the FHFA's best interests (pursuant to the FHFA-C's Incidental Power) of the expulsion of the AT1 Capital instruments (redemption of the JPS at their Redemption Value, which coincides with their fair value under the Separate Account plan. In same series of JPS, the Redemption Value is slightly higher than the par value), as it wouldn't affect the ERCF (T1 = CET1 + AT1), and in the run-up to the annuncement of one of the 3 options in the 2011 UST Report to Congress, submitted at the request of the Dodd-Frank law, as "recommendations on ending the Conservatorships".

Secondly, the number $124B is wrong, not just because it's $125B, but also because it's pending the offset with the SPS LP increased for free, both absent from the balance sheets. Capital Reserve, $0.

Thirdly, he talks about the resumption of dividend payments, disregarding the rules, not only the Capital Classification of Adequately Capitalized as always, but also there is the Table 8: Payout ratio, in the recent Capital Rule, that requires a minimum of 25% of the Prescribed Capital Buffer.

Navy Hedge Fund adds something on his own:

Govt Conservatorship

More evidence that Berkowitz-Mnuchin(UST) kept the 11,000 documents secret, that gave response to the question RFP12 about the existence of the Separate Account plan, posted on the comment I'm replying to.

In this court brief, we see the first time that the Treasury missed the deadline to comply with the subpoena issued by judge Lamberth, with the requirement to produce the documents for the RFP12. A one week extension to August 2nd, 2019.

Judge Lamberth granted the prior motion:

.jpeg)

The Treasury department failed for a second time to produce the documents, now with its own deadline.

Then, Berkowitz moved to file a motion to compel compliance with subpoena to the Treasury department, and it's when on November 8th, 2019, Friday, judge Lamberth issued this order granting that motion. It doesn't appear in the screenshot, but here is when the judge requested to produce the documents "timely".

In August 2021, it's when Berkowitz withdrew this motion to compel compliance with subpoena to the Treasury. Screenshot posted before.

Therefore, if someone asks about the famous "11,000 documents" withheld for Privilege by the Treasury Department, we should ask Berkowitz or Mnuchin.

Or is it Trump, with the Agency documents found recently in his bathroom of Mar-a-Lago? Yikes!

Anyway, we don't need those documents because the Separate Account is what legalizes every action and it's set forth in the law, regulations and basic Finance.

So, keep them.

It's a summary of the Trump Administration in Fanniegate.

FACT: Mnuchin/Trump deliberately chose another capital distribution restricted, among the enumerated ones in the FHEFSSA statutory definition of capital distribution (12 USC § 4502(5)(A) 3rd one added by regulation: the Lamberth rebate: CFR 1229.13), a compensation to Treasury with SPS LP increased for free (number 1) and then, they refused to record them on the balance sheets, along with its corresponding offset that reduces Core Capital.

First, with Watt, $3B SPS LP increased for free on the 4th PA amendment of December 2017 when the "Applicable Capital Reserve" was increased to $3B again, like in the 3rd amendment (Then, reduced $600 million per year), when our negotiator on the Fanniegate hashtag warned them with a tweet, that the whole PA would be declared invalid as of December 2017, because the 3rd amendment established an "Applicable Capital Reserve" (minimum Net Worth) of $0, the rest swept to Treasury, and the Charter Act requires the management to have always a minimum Net Worth, without specifying more.

The 5th (Sept 2019) and 6th (Jan 2021) PA amendments with Calabria, increased this "Applicable Capital Reserve".

Later, the Mnuchin Treasury called on Congress to repeal all the definitions regarding capital in the FHEFSSA (source), to erase his tracks and also because he had implemented in the 6th PA amendment of January 14, 2021, another scheme, aiming to meet the capital requirements with the Capital Reserve mentioned before, instead of the capital metrics in the FHEFSSA (Core Capital; Total Capital), and the additions in the ERCF with the CET1 and Tier 1 Capital.

Mnuchin/Trump weren't aware that the adjusted Capital Reserve (amount of Net Worth above the Capital Stocks) has always been $0, because the SPS LP increased for free carries an offset that wipes out the Retained Earnings just built and FnF were just building SPS in their Net Worth.

So, in truth, they wanted to meet the capital requirements with gifted SPS.

Therefore, an invalid Capital metric and badly assessed. Who does that?!

If it wasn't enough, Mnuchin/Trump colluded with the former SEC chairman to disregard a SEC complaint filed by our negotiator on August 2020, denouncing the absence of these SPS LP increased for free from their balance sheets, commented yesterday.

Although the CRT operations began before, with Craig Phillips as counselor for the Treasury Department, they have ballooned exponentially and he is behind the CRT symposiums to transmit a sense of normalcy in these operations (it was followed by Bitcoin symposiums), attending the 2nd annual symposium along with Blackrock. These credit enhancement operations are barred in the Credit Enhancement clause of the Charter Act, and HERA only authorized the Treasury with its Capital Magnet Fund (source), not FnF.

A conservatoship wasn't meant to break the Charter Act.

The famous Trump letter is considered fabricated evidence, because it wasn't what the Supreme Court required for claiming "constitutional damages". It was later used by the attorney for Berkowitz, David Thompson, in the Collins and Bhatti cases. As such, the letter falls squarely in the felony of stock price manipulation (coverup of the laws, like all the litigants)

Last but not least, a deliberate attempt to conceal the Separate Account plan, after refusing to comply with the judge Lamberth's subpoena to the Treasury Department requirement that, in the Request for Input RFP12, requested all the documents that gave response to a question about the existence of a Separate Account plan that had repaid the obligations SPS under the guise of dividend payments, as per the statute (exception to the Restriction on Capital Distributions: 12 U.S. Code §4614(e)).

After many motions by the investor Berkowitz, who is friends of Mnuchin (both defendants in the retailer Sears bankruptcy), to compel compliance with this subpoena that began in 2019, because the Treasury failed to meet all deadlines, judge Lamberth simply removed the deadline and required to produce the documents "timely".

Berkowitz ended up in August 2021 requesting the withdrawal of the judge's subpoena, likely when he learned that there was a long way to resume the dividend payments under the Basel framework for capital requirements just approved in the ERCF or, likely, he was told that it'd be necessary even more time for a "membership cleansing" similar to the one carried out by the FHFA with the FHLBanks in a 2016 Final Rule (first proposed in 2010), and, if the separate account is unveiled, his 5 or 6 different series of JPS held, would still trade at a discount to par value (6% annual discount rate)

Judge Lamberth accepted his motion and now, he has a lot of explaining to do for the unfulfillment of his initial court order.

Let alone that now, the judge wants to give the JPS holders back dividends for this extended period of dividend suspension beyond what was estimated for its resumption (3Q2022 earnings reports), because of the FHFA's best interests (FHFA-C's Incidental Power) of "membership cleansing" or wind down the affairs of FnF with the JPS holders (holders of AT1 Capital instruments), which has made necessary more regulatory capital until CET1 > 2.5% of Adjusted Total Assets (Compliance with T1 Capital > 2.5% of ATA afterwards). That is, the redemption of the JPS before a Privatized Housing Finance System revamp is unveiled at the same time it's done the same with the Separate Account.

It's irresponsible to assert that POTUS has a say on the Conservatorships of FnF.

i expect biden will act

BREAKING NEWS. Mnuchin hired the former SEC chairman as advisor for his $NYCB deal at off market prices, as compensation for having disregarded a SEC complaint submitted on August 2020, denouncing the Financial Statement fraud in the enterprises (SPS LP increased for free and its offset, absent from the Balance Sheets), containing all the numbers and how the offset works out once the Additional Paid-In Capital account has been exhausted (an account used for the offset with the initial $1B SPS LP issued for free), citing SEC rules (reduction of Retained Earnings account. Core Capital).

This Financial Statement fraud is important because it would be another evidence to visually see how the Common Equity is held in escrow (for those reluctant to read the law in force that expressly states so with the prior 10% and NWS dividends, besides the repayment of the SPS. 12 U.S. Code §4614(e)), in order to comply with the FHFA-C's Rehab power and pursuant to the exception to the Restriction on Capital Distributions (gifted SPS as compensation to UST is a capital distribution as per the statute) in the July 20, 2011 CFR 1237.12: a capital distribution is applied towards the Recapitalization of FnF.

And not the current fraud with the invalid "Capital Reserve", evidence that the Federal Reserve is involved in Fanniegate, because it's the only one that uses this capital metric, called "Capital Surplus" in the balance sheet of the Federal Reserve System.

It isn't a coincidence that the lobbyist Bill Ackman is a member of the Investor Advisory Committee on Financial Markets at the Federal Reserve Bank of New York.

The FHEFSSA was enacted exclusively to assess the Capital standards in FnF. With an authority in HERA, the FHFA chose the Basel framework for capital requirements in its February 16, 2021 Capital Rule (ERCF), with the FHEFSSA still in force: Critical Capital level, Capital Classifications, etc.

We can't allow that two guys (Powell and Ackman) make everything up, using the interest rate policy (Monetary policy) to blackmail the society.

SEC complaint posted on this tweet:

MNUCHIN HIRED THE LAW FIRM THE FMR SEC CHAIR, CLAYTON, REJOINED TO, AS ADVISOR FOR THE $NYCB DEAL

— Conservatives against Trump (@CarlosVignote) March 26, 2024

SEC complaint 15976-876-848,Aug2020, trashed: Financial Stmt fraud→gifted SPS LP/its offset, absent from the B-Sheet.

Mistake: charge on Income Stmnt is🆗#Fanniegate @TheJusticeDept pic.twitter.com/Md8BjM5IR9

The lobbyist Bill Ackman and the Fannie_Mae CEO have been caught in, yet again, another conspiracy in the same week, just when the Democrats and Republicans were negotiating the Federal Budget.

But two posters received orders to say that the Pershing's letter was published on March 25, when it occurred on March 22, to not show that both were colluding with the same pitch the same week.

Hey, navy! Are you also writing with Nsfraudbuster over on stocktwits?

You bet!

It isn't just a flawed opinion. One of them is responsible for the Financial Statement fraud they are basing their opinion on: All the SPS LP increased for free as compensation to Treasury since the December 2017 4th PA amendment, and its corresponding offset with reduction of Retained Earnings account (Core Capital), are missing on the Balance Sheets.

The comment about the two interviews to the CEO of Fannie Mae last week, appears in one of the tweets cited below.

Both with the same song:

-FnF continue to build capital through retained earnings. FALSE.

-FnF hold x dollars in capital, referring to Capital Reserve, not the capital available in the ERCF: Total Captial, Core Capital, CET1 or T1 Capital. FALSE. Besides an invalid capital metric in the FHEFSSA, the actual Capital Reserve is $0, once the SPS LP increased for free and its offset, are posted on the balance sheets to solve the current Financial Statement fraud.

Finally, Bill Ackman in his letter praises the CEOs of FnF to later assert:

whom we have never met

Both companies remain wards of the state.

FHFA should have sufficient autonomy from the enterprises (during a 15-year conservatorship?) and special interest groups. Source.

Pershing's letter was posted on 3/22. Yet, it's today when we've learned about it in 2 message boards claiming that it was dated 3/25.

— Conservatives against Trump (@CarlosVignote) March 25, 2024

It's the CEO the one committing the Fin Stmnt fraud (gifted SPS absent from the Bce Sheet) later the CEO/Ackman base their opinion on.#Fanniegate https://t.co/oebZSNI109 pic.twitter.com/Mm0nEUPOte

You have stripped out the first explanation as to why the Class Action was illegal and also that the grounds of my take is the Rule 23 for Class Actions:

The share class $FNMA was excluded from the Class Action and that makes it illegal, because one of the prerequisites for Class Actions is that it puts an end to the controversy.

Breach of Rule 23(b)(3):

A class action is superior to other available methods for fairly and efficiently adjudicating the controversy.

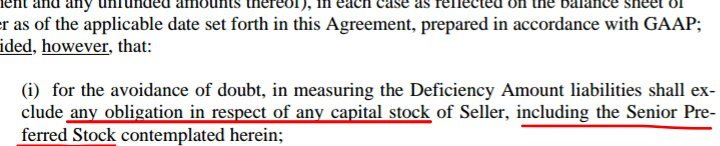

"Satisfying taxpayers bailout". It wasn't a loan but the purchase of securities (obligations in respect of capital stock. SPS), and it isn't "satisfied" but you have to repurchase them or redeem.

It can't be paid back as if by magic.

- The share class $FNMA was excluded from the Class Action and that makes it illegal, because one of the prerequisites for Class Actions is that it puts an end to the controversy.

Breach of Rule 23(b)(3):

A class action is superior to other available methods for fairly and efficiently adjudicating the controversy.

The pro se plaintiff says: "jury verdict certified", because he wants to transmit the idea that it can't be appealed, and the conservator would say that it has no other option than to disburse the amount that would allocate a fat bonus to the corrupt attorneys, estimated in $180 million (a cut of 30% of the total $600 million awarded) that, likely, in turn, will be allocated to all the attorneys in all the cases participating in the Fanniegate scandal since 2013.

Their prime felony is stock price manipulation sustained during 10 years and you need many participants that come and go, unless you are this pro se plaintiff that has a free pass in the D.C. courts, allowing him to file a new lawsuit every time that one gets dismissed, and with the DOJ attorneys always playing along.

Like the dividend declared in 2008 in Fannie Mae, but not paid on the day of conservatorship. Despite the Restriction on Capital Distributions covered up by the attorneys in court nowadays, it was finally disbursed arguing that it was "an outstanding obligation to be honored".

It was "certified", right?.

Anyway, the fact that the jury's award and the Plan of Allocation have nothing to do with the actual damage claimed in court (one-day share price drop the day of the 3rd amendment), blows the whole jury trial up, as commented yesterday.

Attempt to give back dividends to a Non-Cumulative dividend stock and to pay the attorneys for their con job.

***The cases in the Lamberth court are blown up***

This means that, even without a new trial, this case is dismissed regardless once the Separate Account plan is unwound.

All the lawsuits are meritless, as the dividend was impeccably suspended.

The tweet below confirms that everything was staged in the jury trial to give the holders of a Non-Cumulative dividend JPS, back dividends, and a case of camaraderie among the attorneys in the private sector and public sector (The DOJ and the SEC).

Something we already knew, with the so called "revolving door". The DOJ's Mooppan and the Solicitor General Francisco, rejoined their prior law firm Jones Day. The DOJ's Jody Hunt. The former SEC chairman, Clayton, rejoined his prior law firm too, now an advisor to Mnuchin in his $NYCB deal. Etc.

Let alone the FHFA that is directly using a private law firm in its conspiracy: "Mandatory dividends" said in the Lamberth court, in order to turn dividend payments into interest payments. Unaware that a dividend is a distribution of Earnings and you need a positive balance account in the Retained Earnings account (Balance Sheet: picture of a company at a determined date) in the first place. Let alone that it's a capital distribution restricted when FnF are undercapitalized (IN GENERAL).

Notice that the DOJ is a silent party in the Lamberth court. The DOJ wants its counterparty in the Govt theft story (Berkowitz's attorney, David Thompson, and the attorney Hamish Hume, who also represents the hedge funds) to get paid with funds taken from the enterprises, instead of the DOJ having to pay to all the Equity holders a compensation for Punitive damages out of its pocket.

The Lamberth rebate is another capital distribution restricted.

ACTUAL DAMAGE CLAIMED IN THE JURY TRIAL WAS STAGED

— Conservatives against Trump (@CarlosVignote) March 23, 2024

The one-day share price drop on 3rd amdt-day👇.

The jury awarded less($600mll)

Then, the Plan of Allocation switched it to a stake in the Share Class par value, to satisfy Lamberth's call for back divs.#Fanniegate @TheJusticeDept pic.twitter.com/zGbp5c8gjG

Conservatorship has nothing to do with the dividend payments.

After conservatorship, once dividends are restored,

Why does the CBO continue to talk about subsidies for mortgages?

In early conservatorship, it was criticized for what it calculated as "subsidy cost" in FnF for delivering a guarantee fee below the one it would charge the fully private sector, as required in the Charter Act (actions related to Secondary Mortgage Market operations: section Purposes). This cost was then charged on the Federal Budget.

But this is when FnF charged 28 bps g-fee on average and during the period increasing the guarantee fees through today that charge around 62 bps g-fee on new acquisitions, pursuant to the UST 2011 Report to Congress in light of the request by the Dodd-Frank law of "recommendations on ending the conservatorships".

Therefore, there is no subsidy anymore and subsequent "subsidy cost" on the Federal Budget.

Since then, the CBO turned into a branch of the investment banks, calling for the Warrant exercised, Equity restructuring, etc. Clearly, it isn't knowledgeable about the affairs during the conservatorship (laws, rules and basic finance dynamics) and I no longer read anything that comes from the CBO. This is like listening to a Chinese in a karaoke bar singing in English. I can't take no more!

On the other hand, the Office of Management and Budget (OMB) of the White House, treats FnF different. The accounting of FnF is simple: cash outlays and cash inflows.

However, you have posted what it looks like the CBO is continuing to charge a cost on the Federal Budget even without the prior "subsidy cost" caused by a subsidized guarantee fee, increasing the Deficit in $43.4 billion during a 10-year period.

The CBO continues to claim that it's "related to subsidies for mortgage loans purchased and securitized by Fannie Mae and Freddie Mac" without specifying what subsidy it's talking about, because there is none, and linking it to the Conservatorship, when it's a status that preserves their legal status of private shareholder-owned enterprises and FnF have been operating business as usual all along.

The Congressional Budget Office’s baseline includes $43.4 billion in mandatory spending during the FY 2023–FY 2032 period related to subsidies for mortgage loans purchased and securitized by Fannie Mae and Freddie Mac. Ending the conservatorships of Fannie Mae and Freddie Mac would reduce mandatory budget authority by $43.4 billion during the FY 2023–FY 2032 period.

Allies judge Lamberth/Parties curtail prospects of new trial, once they've realized that the Separate Account plan is for real.

Federal Rules of civil procedure. Rule 59 (b). Any motion for a new trial shall be filed no later than 10 days after entry of the judgment.

This way, they lock in the award after this deadline, as, arguably, any appeal can only be about the procedure.

At the same time, they extend the deadline to file the 60-day notice of appeal, by extending the moment it begins to run.

First, judge Lamberth extends the deadline for filing the attorneys' fees, from 14 days to 45 days. Later, he expressly points out that the period for the notice of appeals begins to run after filing the attorneys' fees.

This way, they make sure that the interest payments continue to accrue for a long time. They've secured a minimum of 105 days more of interest payments because, although Bradford is writing on Ihub with a different alias that the attorney Hamish is going to appeal, he won't do it because it'd be more interest payments. With the 105 days granted by judge Lamberth is enough, and with an appeal, it'd have been an extension caused by him. He is here just for the booty with the alibi provided by judge Lamberth.

Everything will happen while we wait for a final resolution by the conservator, working with Congress, as recommended by the Treasury in 2011 for the release from Conservatorship, at the request of the Dodd-Frank law. A 3-option Privatized Housing Finance System revamp.

With or without the judge's judgment, the interest payments would continue to accrue. This is why the suprising judgment has only one objective: the elimination of prospects of a new trial, that would be brought up after unwinding the Separate Account that strikes down their claim of damages, and to lock in the booty for the attorneys and JPS holders.

This is like the dividend already declared in Fannie Mae but not paid on the day of conservatorship. It was disbursed arguing that it was "an outstanding obligation to be honored". Now, without the possibility of a new trial and with the jury's verdict, they would claim the same, despite the fake damages.

For the $FMCC holders, the rebate is just a payment with their own money (Common Equity).

And the $FNMA holders were illegally excluded from the Class Action.

No one pays down debt as if by magic.

That's debt forgiveness, IMF-Argentina style.

The NWS dividend would be reinstated in the future as you claim, after Calabria-Muchnin's flawed "Capital Reserve End Date" in the January 14, 2021 PA amendment is met, but you cover up that the NWS goes on TODAY and FnF aren't being capitalized with regulatory capital as you claim, but with SPS (capital stock not recorded as regulatory capital).

So, the same as before. A Common Equity Sweep.

Common Equity = Net Income attributable to the common shareholders (Retained Earnings account on the balance sheet) + Other Comprehensive Income (AOCI on the balance sheet) = Comprehensive Income.

It has just changed the name: NWS 2.0. Instead through a dividend (NWS dividend), through the offset attached to the SPS LP increased for free that happens every time a company issues/increases stocks for free (without getting the corresponding cash): stock dividends, etc.

Like occurred with the initial $1B SPS LP issued for free on day one.

Two weeks after the 5th Cir. judge Willett's ruling, the NWS dividend was switched for the NWS 2.0 with the SPS LP increased for free in the same amount as the Net Worth increase in the period.

As a result, FnF aren't building regulatory capital ("not being capitalised") but SPS (capital stock not considered regulatory capital).

Not even "Capital Reserve" (amount of Net Worth above the Capital Stock) as the Fannie Mae CEO continuously repeats, because the same offset makes the Capital Reserve be $0 every quarter. An invalid capital metric under the FHEFSSA that uses Core Capital and Total Capital, and only used by the Federal Reserve System in its balance sheet (called Capital Surplus). With this invalid capital metric badly assessed, they want to meet the Calabria-Mnuchin flawed threshold "Capital Reserve End Date" (when the Capital Reserve meets the capital requirements). So, the numbers and the rules are made-up. This is beyond shenanigans.

You just need to have two eyes to see that these gifted SPS are absent from the balance sheet, because they don't want to post the corresponding offset in order to peddle the lie "FnF continue to build capital through Retained Earnings" (Ackman, Fannie Mae CEO, FHFA, etc.).

Then comes the Separate Account plan, because these gifted SPS are a capital distribution (statutory definition) restricted (U.S.Code §4614(e)) and the exceptions kick off to legalize this compensation to Treasury: for their Recapitalization (CFR 1237.12), that is, necessarily the Common Equity being swept to Treasury is held in escrow, which means that, at some point, it'll be unwound and the Comprehensive Income is back up.

We don't see this effect due to the Financial Statement fraud in FnF, but you can see it in the image above.

There are no excuses for not spotting the SPS LP absent from the balance sheet and Guido is simply a layman hired to peddle the plotters' slogans about FnF being "capitalised".

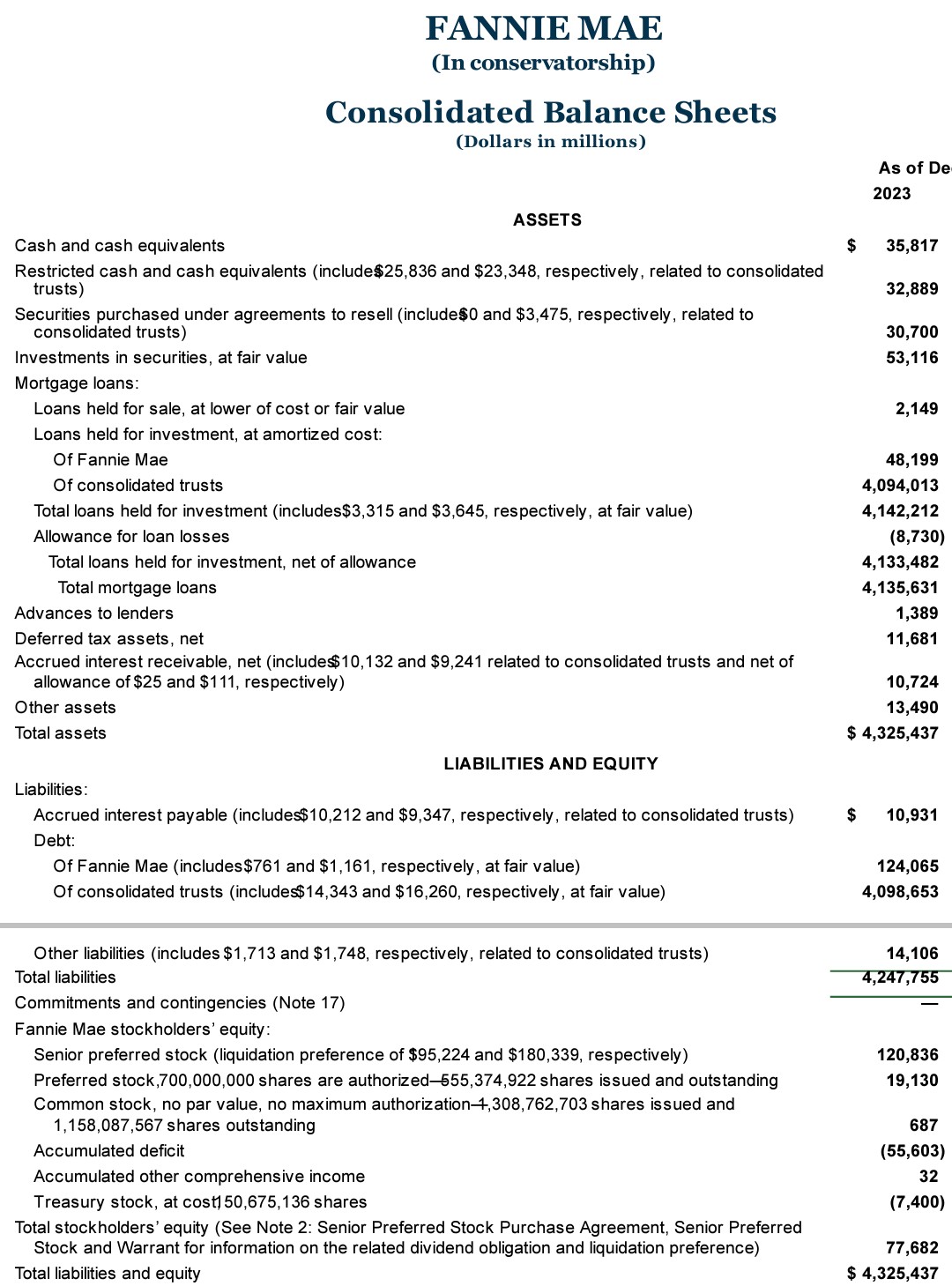

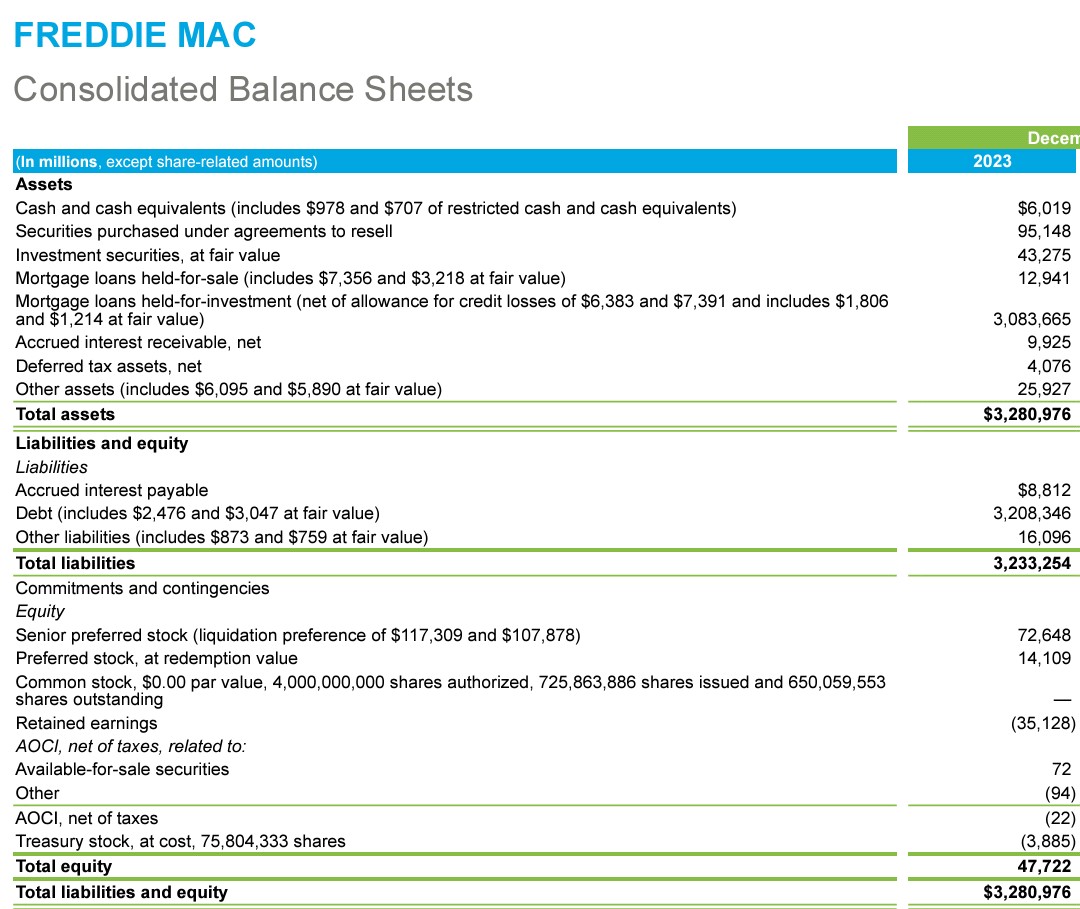

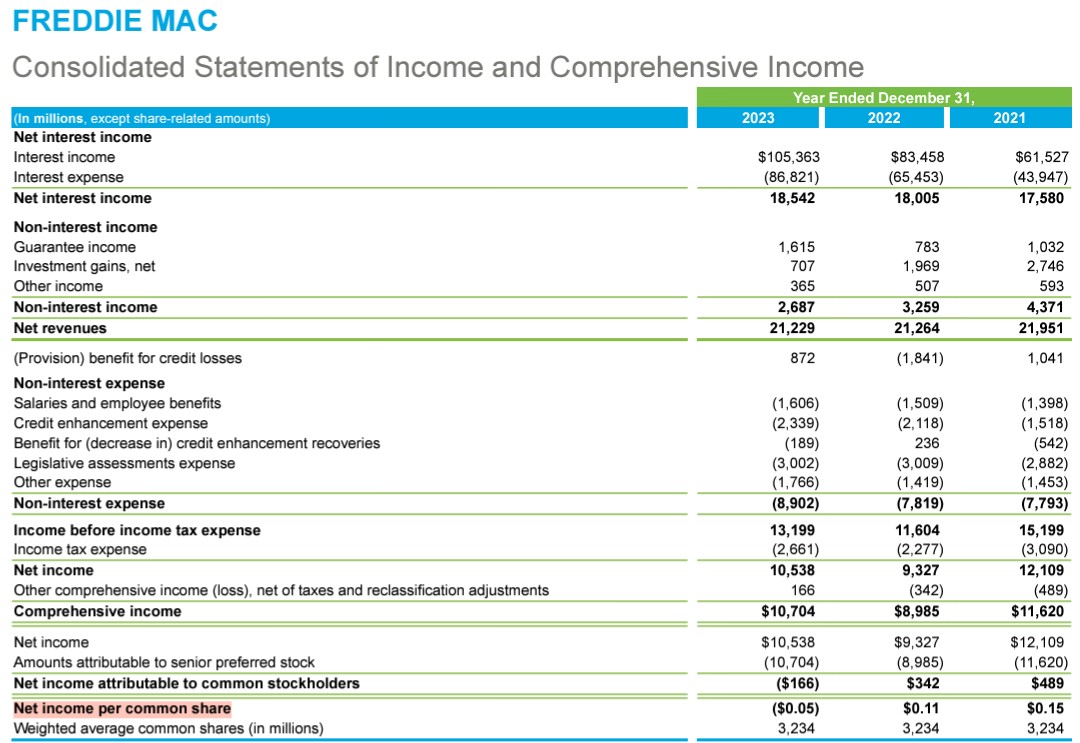

For instance, Freddie Mac always posts the same amount of SPS LP: $72.6B on its Balance Sheet, when the correct amount of SPS LP outstanding as of December 31, 2023, including the $3B SPS LP scheduled to be increased on March 31, 2024, is $120B.

That is, $47.7B SPS LP is absent from the Balance Sheet.

It means that, with $47.7B Net Worth as of December 31, 2023, once Freddie Mac posts the missing SPS and its offset, we'd see that it has been building SPS in its Net Worth, not regulatory capital (Retained Earnings).

This is why their ERCF tables with Core Capital, need to be adjusted for the pending reduction of Retained Earnings (Core Capital), increasing the capital shortfall.

In Freddie Mac, $47.7B lower.

Removing their statutory Critical Capital Level is another felony. FnF don't just remain "undercapitalized" as the FHFA director and Fannie Mae CEO repeat, precisely a quote taken from the Restriction on Capital Distribution by the way.

More like a Capital Classification of: A Hell Of A Lot Critically Undercapitalized.

Let alone that their adjusted Retained Earnings accounts stand at $-216B together. An account that absorbs the future (unexpected) losses and where the dividends are distributed from.

So much for "rehabilitate FnF", required by the Supreme Court and judge Willett: "any action within the enumerated powers" (Rehab).

"Give us reporting" says Roberts, a plaintiff of 2017, when he is accused of not reporting properly.

The stock price manipulation isn't about the stock market and the current stock prices that simply reflect what they see on the Balance Sheets and future prospects:

- FnF post $0 Net Income Atribuible to the Common Shareholders, that is, $0 EPS,

- The Warrant to purchase 79.9% common stock at $0.00001 per share,

- $318B SPS LP still outstanding,

- The FnF management and the conservator committing Financial Statement fraud with the SPS LP increased for free absent from the balance sheets.

-FnF auctioning off their NPL and RPL to the hedge funds at fire sale prices, instead of the normal mortgage business of taking possession of the collateral (property) and repackage the RPL into UMBSs again, respectively. Notice that this comes after their foreclosure prevention actions have been exhausted.

FnF can't be used to give business to the hedge-fund industry that works for JPM, Goldman Sachs, etc.

The stocks aren't "permanent options" as the controversial Ackman repeats in his GSE slides to justify the stock price, and later he pretends to be an options trader expert in his twits.

FnF don't "make $10 a share every year", as he claims, but $0, due to the ongoing Common Equity Sweep covered up by the plotters.

Being recapitalized while posting $0 EPS, is called "selling smoke", because the capital built is the common equity (Net Income + OCI = Comprehensive Income on the Income Statement. It turns into Retained Earnings account and AOCI once posted on the Balance Sheet.) that belongs to the shareholders and you have just posted $0 net income attribuible to the common shareholders.

It's the plaintiffs and Co the ones to blame for the stock price manipulation with their government theft story in court, as a result of not challenging the conservator's actions properly, in accordance to the law, regulation and basic finance.

In other words, the stock prices would have been very different had they uncovered the Separate Account plan, but watching the JPS trading at a discount to par value (estimated 6% discount rate over par value until the dividend is resumed -25% of the Prescribed Capital Buffer- Table 8 of the Capital Rule: Payout ratio) wouldn't have been pleasant if they compare it to a common stock that trades at x times the annual EPS and the real thing.

They rather attempt the assault on the ownership, even stuffing the Treasury with SPS LP for no reason (gifted SPS), betting on a swap Preferreds for Common Stocks.

For instance, this is what the judge for the 7th Circuit Court of Appeals stated for the dismissal of his lawsuit or, better said, it looks like the judge gave him a reprimand (words in brackets added by me):

The plaintiffs didn't establish that the NWS (dividend) contravenes that duty (conservator's power: put FnF in a sound and solvent condition)

Restricted Cash/Custodial Account:Funds already pledged you can't count on.

Cash and cash equivalents as of December 2023: $36B.

Screenshot taken from Fannie Mae's earnings report with the S.E.C.. The file appears messed up, nothing weird in the Fanniegate saga and its controversial CEO/President:

Quit posting false information and definitions, Guido: "Common Equity is the commons". Stick to your deranged tweets that promote your boss Pagliara's book: "We've been robbed! Weee!".

The source is always their 10-k reports with the S.E.C., yet you made it up:

$68.7 billion cash and equivalents as of 12/31/2023.

"We drew 119B from UST. Paid back 181B"→Add 78B gifted SPS. All capital distributions restricted.

— Conservatives against Trump (@CarlosVignote) March 20, 2024

"Investment"→in obligations SPS.

"Building C. through RE"→Adjusted for the offset w/ gifted SPS, $0.

"78B in Capital on Dec"→ERCF:-43B Core Capital (-121B adjusted)

😳#Fanniegate https://t.co/31Muyve7dc pic.twitter.com/ah34R9XvGf

I have never used Bradford's website before, until our website for court briefs, www.gselinks.com, shut down a few years ago, after a period of not being updated.

It was a better website than Bradford's because each court case had its file, so you can easily scour past briefs. You can't do that with Bradford's site because he just posts the briefs together in chronological order.

This is very important in these lengthy cases and the widespread misbehavior in court by all the plaintiffs and judges.

For instance,

- Gary Hindes removed all prior references to breach of statutory provisions ("FHFA's statutory mission to build capital") in an amended complaint, when he was told that the 10% dividend that he defends, was the same breach as the NWS dividend.

-Bryndon Fisher has filed a appeal but it turns out that it'd be a third appeal over the same case (looping) and about an issue already appealed himself and also appealed to the Supreme Court by the Fairholme plaintiff Andrew T. Barrett. Supposedly, because no brief electronically filed has been provided, just a google drive document.

-Or just yesterday, about the attorney Hamish Hume in one of the two cases in the Lamberth court (the other is the Fairholme case), he is also in the CFC with the Wazee case denouncing for the first time ever the current Common Equity Sweep concealed by the FnF management under orders of the conservator (SPS LP increased for free and its offset, are missing on the Balance Sheets. Financial Statement fraud. Another capital distribution restricted and the exceptions kick off: for the recapitalization, that is, another tool to hold the Common Equity in escrow like the Separate Account with the dividends to Treasury (applied towards the reduction of SPS in the first place), complying with the FHFA's Rehab power as well).

A NWS 2.0 that he covered up in the Lamberth court for his claim of fake damages (the dividend was impeccably suspended).

NO GLIMPSE OF LEGALITY W/ LAMBERTH

— Conservatives against Trump (@CarlosVignote) March 20, 2024

Atty Hamish didn't challenge today's Common Equity Sweep. It'd hinder his claim of 1-day share price drop rebate on 3rd amdt-day.

To avoid be sued, NWS 2.0 brought up w/ Wazee(CFC) in amended complaint.Appeal due 3/25.#Fanniegate @TheJusticeDept https://t.co/QPwJTUOf1G pic.twitter.com/PXHIHYNBcd

15 years into Conservatorship, Glen Bradford-LuLeVan still talks about their capital structure and even he says it wrong, because with today's $125B Net Worth and $318B SPS LP still outstanding, the JPS are wiped out, whereas the Cs are still necessary in order to monetize the remaining SPS after the corresponding 61% haircut.

Both haircuts boost the common stock valuation.

Known investors in preferred stocks, like Berkowitz, see a non-cumulative dividend Preferred Stock as a tool for the assault on the ownership of enterprises, instead of what this made-up hybrid financial instrument was meant to do: recorded in Core Capital due to its loss-absorbing capacity, Capital Adequacy-wise (by definition, like all other accounts therein). In other words, they are used by the financial companies to restore capital with the dividend suspended.

This is why the JPS get a higher dividend rate than the interest rate on similar obligations by the same issuer.

Bank CEOs play along, because these costly JPS are never redeemed, and they repurchase common stock instead, which is wrong too, because this is done when they don't know where to invest in their business.

But, for instance, $JPM with $116B worth of Treasury Stock (stock buybacks) on its balance sheet (a contra-equity account) that, once retired, it reduces the core capital (both Additional Paid-In Capital and Retained Earnings accounts), is beyond not knowing where to invest in.

At least, it should have repurchased its $27.4B worth of JPS instead.

It isn't a compensation to the shareholders because they rather see a 20% ROE on that amount, than a CEO, wannabe hedge fund manager, investing in the stock market.

The point is, there's been a Separate Account plan all along, in accordance with the law. Now it's when the JPS's fair value is their par value.

"IF THEY ARE WORTH ANYTHING"

— Conservatives against Trump (@CarlosVignote) March 19, 2024

For $FNMAS to be worth $25, the Cs would have a Mkt Cap of $201B in FNMA. $173B in FMCC (PER 10/12x)

He doesn't get that the par value is recovered once the div is resumed.

To that end, Common Equity has to be built first(T1 C.>2.5% of ATA)#Fanniegate https://t.co/WWLoVEXksU pic.twitter.com/WPcP3u1Wyu

All the Preferred Stocks are permanent securities, but redeemable at the option of the issuer, by definition.

Continuing with the idea of debentures in the post I'm replying to.

The SPS are no different, regardless of the 5th PA amendment of September 2019, where Mnuchin/Calabria wrote an "Optional pay down of SPS liquidation preference upon termination of the commitment", in an attempt to thwart the separate account plan.

Pointless. At the time, all the SPS LP corresponding to the draws from Treasury, was long gone (end of 2013/2014) as per the exception to the Restriction on Capital Distribution by statute, U.S.Code §4614(e), and the SPS LP increased for free as of December 2017, is used to hold the common equity in escrow in order to uphold both the FHFA-C's Rehab power and another exception to the Restriction on Capital Distributions: for their Recapitalization, CFR 1237.12 (Though this effect is concealed when this SPS LP and its offset -reduction of Retained Earnings account-, is missing on the balance sheets), and it'll be cancelled with the FHFA-C's Incidental Power: "Any action authorized by this section,....in the best interests of the FHFA".

Any action, like: "Just joking. Zing!"

Everyone must take a 9-box checklist polygraph test to see the extent of their involvement in the Fanniegate scandal.

A minimum requirement of 6 boxes is used for the scrutiny of those writing about FnF in formal documents, in order to prevent investors turned into lobbyists from tricking the society into their investment cases, and even abusing of court process to the same end, messing around with the retail investor for profits: court briefs, books, articles, GSE slides, financial analyses, personal blogs, etc.

By the way, a formal document is the one posted on a space publicly available, regardless of who it is addressed to (Gary Hindes: "to my partners") or whether that person has protected his tweets on Twitter, so only his followers can see them, like Rum just yesterday (the tweet below is a retweet of his tweet). It's still posted on a public space.

If you want to write to your partners, write them a private email. But then, don't post it online like Rum does with the emails from the attorneys.

Writing formal documents and posting them on a public space, always comes with liabilities. In Fanniegate, crippling liabilities.

6-BOX CHECKLIST ASSESSES PUNITIVE DAMAGES🆚THE PLOTTERS W/ THE GOVT THEFT STORY IN FORMAL DOCS

— Conservatives against Trump (@CarlosVignote) March 19, 2024

Accused of the felony of stock price manipulation,they double down w/ technical analysis while posting $0 EPS,$402B C.shortfall,...

3 more boxes for the #Fanniegate crew.@TheJusticeDept https://t.co/9P44uEmOA5 pic.twitter.com/A2op1UTUXF

You don't know the specifications of the security you purchased.

The underlying security in a Preferred Stock is an obligation.

The Treasury department also said so in the SPSPA:

The security "obligation" is a compromise of repayment, that is, a debenture that reflects the taxpayer's assistance, which must be paid back asap.

Subsection (c) any obligations of subsection (b) redeemable obligations, is the original UST backup of FnF in the Charter Act, at rates similar to Treasuries. It's included the SPS in this definition, also as a way to finance their operations as a last resort (either Equity or Debt) in the section Purposes, which is the one that specifies their (risky) Public Mission.

The lobbyist G.Hindes chatted with a top WH official in April 2022, he told us in one of his public letters, contending that the White House will lay out a plan in the next 18 months.

Presumably, with the former NEC Director, Brian Deese, also a former Blackrock executive.

I've been wrong before, stating that it was the other lobbyist Tim Pagliara the first to start with the slogan "White House Conservatorship", instead of FHFA Conservatorship (aiming to transmit the idea that it's the WH the one in charge of the release, when it's solely the conservator), with his first tweet of 2024 proposing the same scam of "Recap and release" for the next 18 months. It was Gary Hindes with this letter.

Pagliara came out with a new time frame, just when the prior 18-month deadline had passed.

This slogan comes at the time the third musketeer, Timothy Howard, felt very comfy last week with the NEC Director Lael Brainard when she was playing along with this slogan, and both also coinciding with the idea that the Biden Administration won't release them.

Howard on Brainard's statement at the Urban Institute headquarters:

I’m not surprised by this.

I wrote, “[T]his small publicized action on title insurance very likely also is a large silent message that the administration is not currently considering tackling the much bigger issue of removing Fannie and Freddie from conservatorship this year.” Yesterday, Brainard simply “said the silent part out loud.”

Section CONGRESSIONAL FINDINGS: FHFA should have sufficient autonomy from the enterprises (15-year conservatorship) and special interest groups (the 3 musketeers, Urban Institute, Moelis, the JPS holders, etc.)

unrelated to the (FHFA) Conservatorships (Rule of Law and basic Finance) and a Privatized Housing Finance System revamp, chosen for the release in a UST 2011 Report to Congress, at the request of the Dodd-Frank law.

More on my conversation with Pagliara, president of the phony Shareholders' Association Investors Unite, he set up to trick them into accepting his plan for the sacking of the enterprises, through the Warrant and stock offerings, as "incentives" for other rogue investors lying in wait. That is, secured deals.

HOW IT STARTED

HOW IT ENDED

He insulted me for no reason, because I was just defending the shareholders from this rogue chamber investor. Therefore, it wasn't justified his outburst, that would have been admissible if, for instance, I would continuously call the SPS "SPSPA" (Pagliara's clerk Glen Bradford), in order to pass the 4th PA amendment of Jan 14, 2021 (Justice Alito was the first to call it 4th, when it's the 6th, selling the idea that it was a game changer after the 3rd amendment in question, as suggested by the Solicitor General Perdogar in a last-minute brief) off as the 4th SPS certificate amendment of April 13, 2021. This way, it involves secretary Yellen in this flawed 6th PA amnt ("Capital Reserve End Date", CET1 >3% of ATA for the release, when the ERCF just requires TIER 1 Capital (JPS, included) > 2.5% of ATA, which was the prior mandatory release Undercapitalized: C.C. or T1 > 2.5% of ATA), because she was sworn in on Jan 26, 2021.

Or for filing frivolous lawsuits as a con job, covering up many statutory provisions and financial concepts, etc.

It seems that they can carry out a con job of epic proportions, but you can't call them "corrupts" because they get offended.

This is why they are continuously provoking us, to later claim:

Are you going to let him talk to me like that?!

Aren't you allowed to write "Pagliara"?

Tim P has hosted calls with the legal team in the past.

The government comes to me.

Guido switches between Pagliara and plaintiff Bryndon Fisher, as planned.

He complains about the Warrant but only if it's exercised, knowing that it's when the damage can't be reversed, ignoring that the damage on stock valuation is the moment it was issued in 2008 (EPS on a diluted basis).

In the meantime, this allows more time for his boss, Pagliara, to use it to negotiate with the government the same way the former Venezuelan president Hugo Chavez would say: "Appropriate it!" (79.9% stake in FnF).

Pagliara:

7. Biden will start the recap and release process, claim credit for solving the housing crisis, and appropriate the 100 billion warrant money to congressional districts in a variety of programs to address affordability but more importantly SUPPLY. This is the easiest big idea win available in the current election cycle.

The FHLBs are a government-sponsored enterprise. The government determines who can buy shares, when those shares must be sold, the price at which the shares are bought and sold, and the bulk of the rights that come from holding the shares. 3/

— Kate Judge (@ProfKateJudge) March 13, 2024

It isn't the first time that the plaintiff Joshua Angel calls me "Pagliara hater" with this alias, one of his 20+ aliases he uses regularly on Ihub.

If you are looking for a hater, look no further. My convo with Pagliara turned very ugly.

He even confessed being involved in the Fanniegate scandal at the highest levels, before the conservatorship began, June 8th, 2008.

6-box CHECKLIST template to assess Punitive Damages against the plotters peddling the government theft story in formal documents: court briefs in frivolous litigation, amicus briefs, letters, GSE slides, articles, books, financial analyses and even personal blogs, because the blogger can delete comments from other shareholders.

The reason why the stocks trade at rock bottom prices: it translates into $0 EPS every quarter, $402B capital shortfall over minimum Leverage capital requirement as of end of 2023 and the Warrant and $310B SPS LP still outstanding.

A formal document has a far-reaching influence, than an opinion on social media "free speech", despite that many social media influencers might face charges as well, when it's obvious that it isn't just a simple opinion, but they are the necessary accessories of the main plotters, for the felony they are accused of: stock price manipulation (Abuse of court process is added to those that have utilized the court for their investment case: called "the Trump trade" nowadays).

The total Punitive Damages respectfully requested, is $4.8B. The same amount as their necessary counterparty in the Govt theft story, the DOJ: "Yes, we stole it all!".

The 6-box checklist has been divided into 3 groups:

COVERUP OF STATUTORY PROVISIONS AND REGULATION

🔲1- Restriction on Capital Distributions (U.S. Code §4614(e) and CFR 1237.12) and its exceptions: for the reduction of SPS and for the Recapitalization.

🔲2- The FHFA-C's Rehab power, expressly stating that it means to build regulatory capital. It doesn't count if you claim it in court, but then, you take it back in an amended complaint (Gary Hindes)

🔲3- UST financing of their operations as a last resort at a rate similar to Treasuries, on any obligations, including the SPS.

🔲4- Fee Limitation of the United States, as part of the Charter Dynamics as well.

LIES

🔲5- Howard in his SCOTUS-amicus brief: "the SPS are non-repayable securities", repeated a dozen times and not written anywhere. The law expressly states that they can be reduced while they remain undercapitalzed, in the box 1.

FINANCIAL CONCEPTS

🔲6- Dividends, a distribution of earnings. Thus, unavailable earnings for distribution, out of an Accumulated Deficit Retained Earnings account.

These are the basic points, but the list can go on:

- For not challenging the security Warrant with the Authority of Treasury to Purchase Securities, to (iii) protect the taxpayer (collateral).

- Credit Risk Transfers (CRT) barred in the clause Credit Enhancement of the Charter Act. For instance, Howard insists that they don't make economic sense instead, which is trumped by the FHFA-C's Incidental Power. So, it's clear his intention to mislead the retail investor in their claim (a $19B refund in CRT expenses, net, has been requested).

- Concealing the Financial Statement fraud in FnF with the SPS LP increased for free and its offset, absent from the Balance Sheet since December 2017. We even have the case of the attorney for Berkowitz, David Thompson, that uses this fraud for his claim of constitutional damages in the Bhatti and Collins cases, because the "for cause" removal restriction prevented his wonderland scenario of the UST getting rich with gifted SPS and, at the same time, FnF are recapitalized, from happening sooner. This is false, as FnF aren't being recapitalized once the SPS LP increased for free shows up on the balance sheet.

Playing the fool isn't an option but an aggravating circumstance when assessing Punitive Damages. Attorney David Thompson: "I'm not a securities lawyer".

Only FHFA-C is in charge of the release from Conservatorship, working with Congress because of the UST's 3-option Privatized Housing Finance System revamp in a 2011 Report to Congress, chosen as "recommendations on ending the conservatorships", at the request of the Wall Street reform and Consumer Protection Act (The Dodd-Frank law).

The U.S. Congress didn't direct Pagliara to lay out his recommendations.

The Biden Administration can provide input, but it can't change the plan for the release, in motion since then (guarantee fee increases, Basel framework for capital requirements, the commingled securities for a Government- or private- catastrophic loss resinsurance) and DeMarco began to work on it right away.

The extended Conservatorship is evidence of this Privatized Housing Finance System revamp, because the FHFA has already made clear that it wants a "Membership cleansing", as seen in its 2016 Final Rule with the FHLBanks: ordered to wind down their affairs with the captive insurers in the next 6 years (hedge funds getting cheap funding from the FHLB system). This final rule was first proposed in 2010.

With an adjusted CET1 > 2.5% of Adjusted Total Assets (Separate Account), the JPS can be redeemed, still comply with T1 > 2.5% of ATA and, as of the recent 4Q 2023 Earnings report, the laggard Fannie Mae had a Capital Buffer > 25% of the Prescribed Capital Buffer for the resumption of dividend payments after this JPS redemption.

The stars are aligned and this is how FnF "wind down their affairs with them".

It's evidence because all possible prior thresholds for the release have been skipped:

1- At the discretion of the FHFA-C (prior FHEFSSA),

2- Prior mandatory release with Capital Classification Undercapitalized,

3- Resumption of dividend payment (laggard Fannie Mae with the 3Q2022 earnings report. $FNMAS's Fair Value chart),

4-CET1 >2.5% of ATA (laggard Fannie Mae with the 3Q 2023 earnings report)

We are in the last one.

5- Number 4 + Capital Buffer > 25% of Prescribed Capital Buffer (Fannie Mae, 4Q 2023 earnings report)

Although the Congress might disagree with the conservator acting "in the best interests of the FHFA" (Incidental Power), the redemption of the JPS is now a corporate decision.

It's clear the collusion to spread the slogan that it's the White House the one that decides about the release. It began with Pagliara in the tweet that you post, peddled also by his social media crew and, recently, the NEC Director Lael Brainard and Timothy Howard, adding both that the Biden Administration won't release them, thinking of the Trump letter, as seen in this comment from Howard posted on Ihub:

the administration is not currently considering tackling the much bigger issue of removing Fannie and Freddie from conservatorship this year.” Yesterday, Brainard simply “said the silent part out loud.”

The common stock par value was reclassified in the third quarter of 2008 earnings reports, to Additional Paid-In Capital account.

Then, it was reduced (which is a reduction of Core Capital and thus, a breach of the FHFA-C's Rehab power) with the following amounts:

- The $1B worth of SPS issued for free on day one. Like any other stock issued or increased for free (today's SPS LP increased for free, absent from the balance sheet to evade this operation. Financial Statement fraud), there is an offset that reduces the Core Capital.

Hank Paulson needed this gift on day one, not only to reduce the Core Capital and justify the conservatorship under the discretionary authority of FHFA with "(G) LOSSES: likely to incur (fabricated) losses that deplete all of its capital", but also to begin with another Securities Law violation with the SPS LP increases, instead of issuances and purchases, in order to skip the deadline in the temporary authority of Treasury to purchase securities/obligations of FnF, of December 31, 2009, with a high yield, necessary for the Separate Account plan (later the original rate similar to Treasuries is the one that prevails: assessed at a weighted-average 1.8% cumulative dividend rate on SPS, applying a 0.5% spread over Treasuries)

- The value of the Warrant ($2,304 million in Freddie Mac) to purchase 79.9% of common stock for $0.00001 per stock (A collateral of the SPS, to (iii) protect the taxpayer). Again, like any security issued for free, it carries an offset.

We see also one of the 7 securities law violations, because the value of the Warrant was also credited to the Additional Paid-In Capital account, when it should only be debited from that account.

HOW TO UNWIND IT

There is no need to put the value of the common stock par value back in its place once the Separate Account is unwound, because most of the companies operate with no par value common stock.

Not even back to Additional Paid-In Capital account, because the value that was eliminated, will be recovered once it's reflected on the Retained Earnings account that belongs to them.

All of them are part of the Common Equity.

It seems that Howard feels comfy with Brainard playing along.

Common stock par value and Common Equity are different things.

The Common Equity belongs exclusively to the common shareholders, also known as the Book Value of a common stock.

Hence, we calculate a Book Value Per Stock (BVPS).

It seems that you have never read that Book (Balance Sheet), because I already explained it to you here.

Even I calculated $JPM's Price to BV ratio for you: 1.8 times, knowing that you would never make it on your own.

FnF operate business as usual during Conservatorship.

A UST backup came to substitute their light capital requirements as a result of a subsided guarantee-fee.

Everything changed with the UST's 3-option Privatized Housing Finance System revamp in 2011, as "recommendations on ending the Conservatorship", at the request of the Dodd-Frank law.

Now, the UST backup is pointless and their Public Mission outdated.

Charter-revoked wording in the very 2011 Report to Congress.

FnF don't compete with the banks. FnF help them to off-load mortgages from their balance sheets, so they can continue to lend out.

FnF compete with others that have a securitization platform, like Blackrock.

The commingled securities were created to fuel competition, for those that lack a Securitization Platform and also in the sale of their products if the market requires Reinsurance by FnF.

This is why Blackrock is involved in the Fanniegate scandal, with the CRT (Craig Phillips) and sending people to the White House, like Brian Deese, to conceal the Separate Account plan. Just what you are doing, Bradford.

Notice that CSS could operate globally once it's IPOed, and Blackrock has huge business with the ECB's fraudulent activities across the board, and with other countries/governments.

Trump is the cheater (mastermind of the phase 3 in the Separate Account plan: SPS LP increased for free holds the Common Equity in escrow. It began with Watt-Mnuchin).

The shareholders' worst-case scenario (99.99% dilution).

Trump did write in his Nov. 21 letter that he plans to release the twins so that hard-working Americans will no longer be cheated out of their retirement savings.

It was an expense in Q3 of 2023 under accounting rules.

But, as capital distribution (an expense unrelated to the normal operations and, considered so by regulation), it's a restricted payment.

Restricted for a reason as pointed out before: build capital.

Yeah, we know. "Zing!" (FHFA-C's Incidental Power)