Friday, March 22, 2024 5:07:31 AM

So, the same as before. A Common Equity Sweep.

Common Equity = Net Income attributable to the common shareholders (Retained Earnings account on the balance sheet) + Other Comprehensive Income (AOCI on the balance sheet) = Comprehensive Income.

It has just changed the name: NWS 2.0. Instead through a dividend (NWS dividend), through the offset attached to the SPS LP increased for free that happens every time a company issues/increases stocks for free (without getting the corresponding cash): stock dividends, etc.

Like occurred with the initial $1B SPS LP issued for free on day one.

Two weeks after the 5th Cir. judge Willett's ruling, the NWS dividend was switched for the NWS 2.0 with the SPS LP increased for free in the same amount as the Net Worth increase in the period.

As a result, FnF aren't building regulatory capital ("not being capitalised") but SPS (capital stock not considered regulatory capital).

Not even "Capital Reserve" (amount of Net Worth above the Capital Stock) as the Fannie Mae CEO continuously repeats, because the same offset makes the Capital Reserve be $0 every quarter. An invalid capital metric under the FHEFSSA that uses Core Capital and Total Capital, and only used by the Federal Reserve System in its balance sheet (called Capital Surplus). With this invalid capital metric badly assessed, they want to meet the Calabria-Mnuchin flawed threshold "Capital Reserve End Date" (when the Capital Reserve meets the capital requirements). So, the numbers and the rules are made-up. This is beyond shenanigans.

You just need to have two eyes to see that these gifted SPS are absent from the balance sheet, because they don't want to post the corresponding offset in order to peddle the lie "FnF continue to build capital through Retained Earnings" (Ackman, Fannie Mae CEO, FHFA, etc.).

Then comes the Separate Account plan, because these gifted SPS are a capital distribution (statutory definition) restricted (U.S.Code §4614(e)) and the exceptions kick off to legalize this compensation to Treasury: for their Recapitalization (CFR 1237.12), that is, necessarily the Common Equity being swept to Treasury is held in escrow, which means that, at some point, it'll be unwound and the Comprehensive Income is back up.

We don't see this effect due to the Financial Statement fraud in FnF, but you can see it in the image above.

There are no excuses for not spotting the SPS LP absent from the balance sheet and Guido is simply a layman hired to peddle the plotters' slogans about FnF being "capitalised".

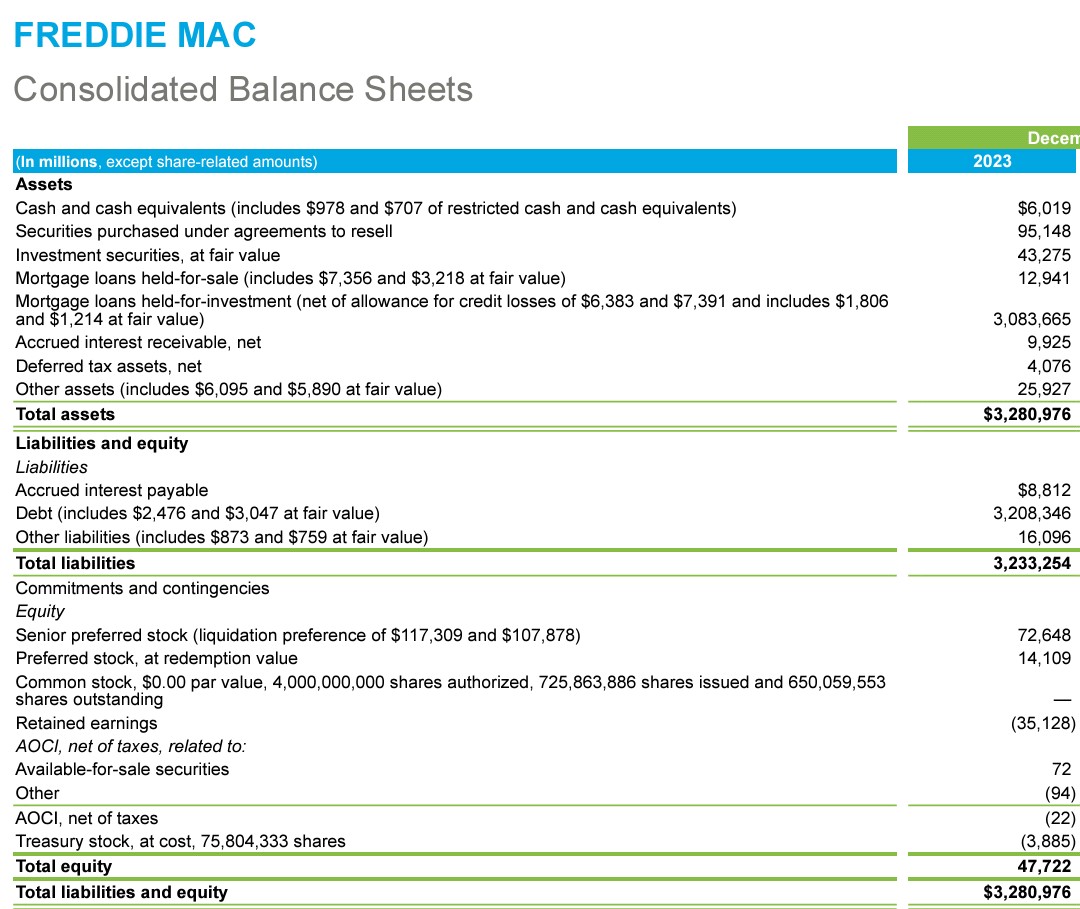

For instance, Freddie Mac always posts the same amount of SPS LP: $72.6B on its Balance Sheet, when the correct amount of SPS LP outstanding as of December 31, 2023, including the $3B SPS LP scheduled to be increased on March 31, 2024, is $120B.

That is, $47.7B SPS LP is absent from the Balance Sheet.

It means that, with $47.7B Net Worth as of December 31, 2023, once Freddie Mac posts the missing SPS and its offset, we'd see that it has been building SPS in its Net Worth, not regulatory capital (Retained Earnings).

This is why their ERCF tables with Core Capital, need to be adjusted for the pending reduction of Retained Earnings (Core Capital), increasing the capital shortfall.

In Freddie Mac, $47.7B lower.

Removing their statutory Critical Capital Level is another felony. FnF don't just remain "undercapitalized" as the FHFA director and Fannie Mae CEO repeat, precisely a quote taken from the Restriction on Capital Distribution by the way.

More like a Capital Classification of: A Hell Of A Lot Critically Undercapitalized.

Let alone that their adjusted Retained Earnings accounts stand at $-216B together. An account that absorbs the future (unexpected) losses and where the dividends are distributed from.

So much for "rehabilitate FnF", required by the Supreme Court and judge Willett: "any action within the enumerated powers" (Rehab).

Avant Technologies Engages Wired4Tech to Evaluate the Performance of Next Generation AI Server Technology • AVAI • May 23, 2024 8:00 AM

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM