Sunday, March 24, 2024 4:37:13 AM

After conservatorship, once dividends are restored,

This is the theory, because we know that, nowadays, under the Separate Account, the dividends are kept suspended thanks to the conservator's Incidental Power "in the best interests of the FHFA", because it's carrying out a "membership cleansing". FHFA saw an opportunity when the UST attached the release from conservatorship to a Privatized Housing Finance System revamp in its 2011 Report to Congress required by the Dodd-Frank law.

The driver of dividend payments is the capital levels and thus, capital classifications, as expressly written by the FHFA in the preface of the famous 2011 Final Rule "for the transparency of the conservatorship":

Since the Capital Rule that came into effect on February 16, 2021, the Adequately Capitalized threshold (Total Capital > Risk-Based Capital requirement) for the resumption of dividend payments isn't enough.

The Table 8: Payout ratio (percentage of the Net Income that can be distributed to the Equity holders as dividend) states that now, additionally, it's required a minimum of 25% of the Prescribed Capital Buffer.

This is the estimation of the moment $FNMAS would have resumed the dividend payments, if it wasn't because of this extended version of Conservatorship to fulfill the FHFA's interest of winding down (redemption) the AT1 Capital instruments (JPS)

This is useful to calculate its fair value all along, because a JPS is a fixed-income security nowadays without a dividend payment (just like FnF's 30-year zero coupon callable Medium Term Notes), applying a 6% annual discount rate to this milestone that marks the moment the fair value reaches its par value again.

With the 3Q 2022 earnings report (the chart was first calculated with the statutory Core Capital, when the Capital Buffer is calculated only over the Tier 1 Capital, which is a little bit lower than the Core Capital, that's why the delay in the chart)

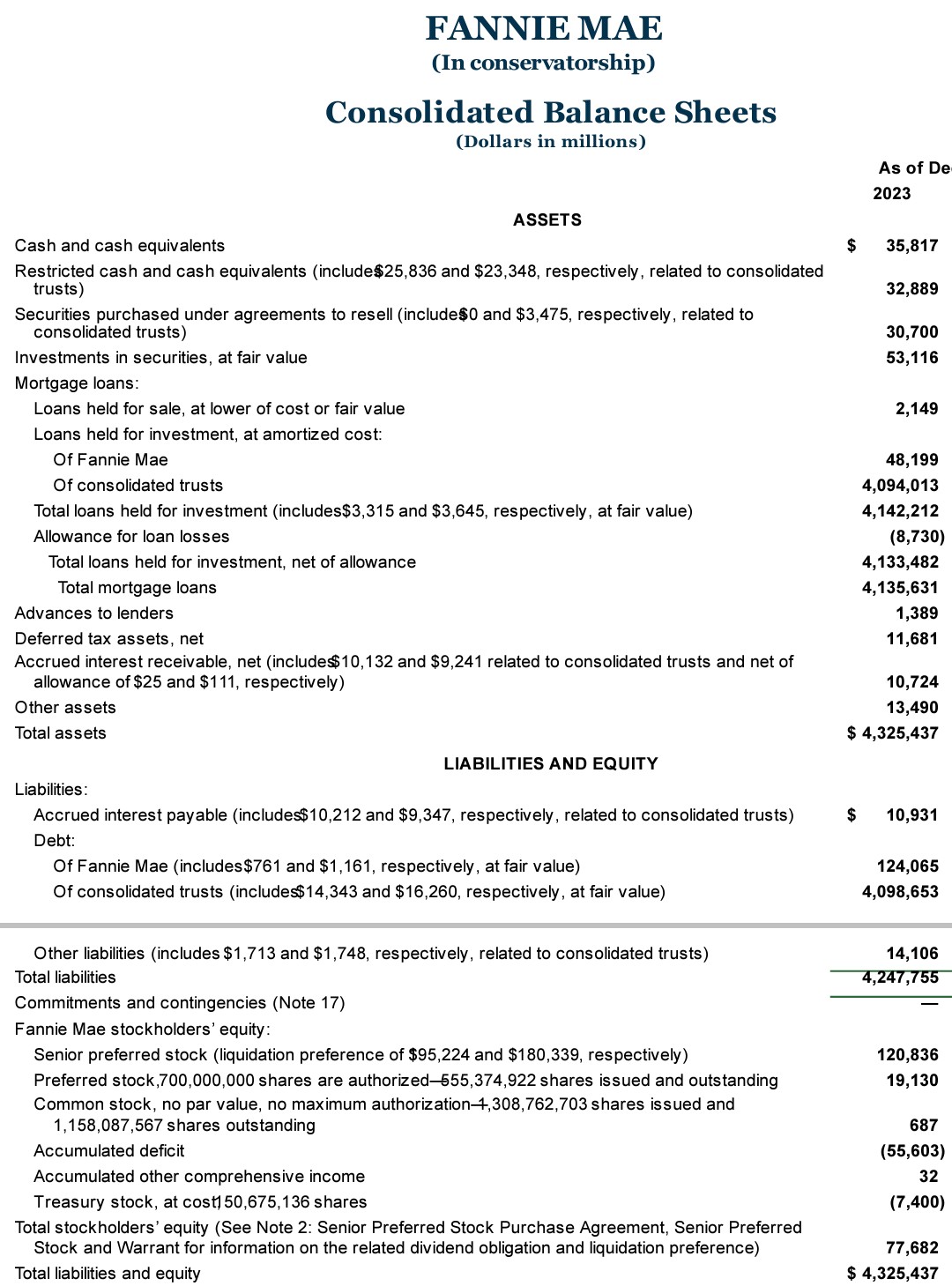

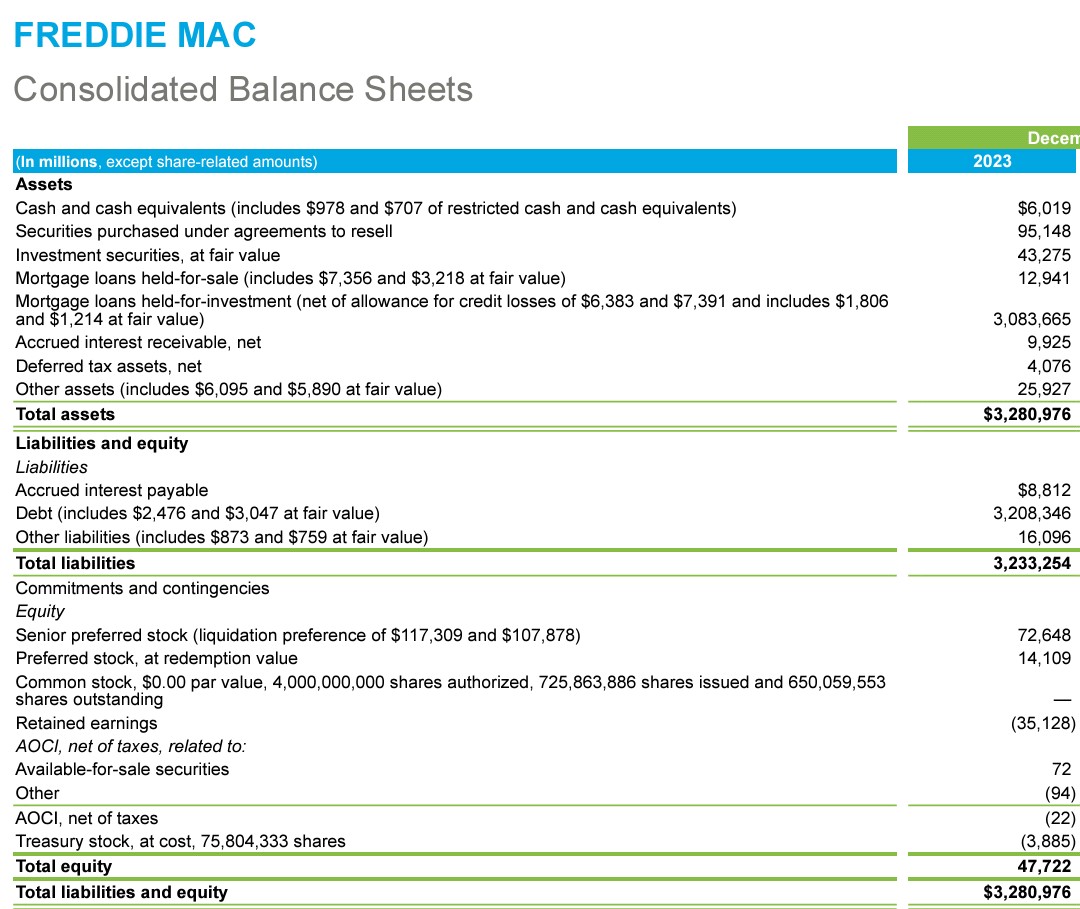

Remember that you need a positive balance account on the Accumulated Retained Earnings accounts in the first place, in order to distribute them out, yet FnF still post Accumulated Deficit Retained Earnings account, worth $-91B officially posted on their Balance Sheets, but we know that there is Financial Statement fraud with the $125B SPS LP increased for free and its $125B offset (precisely, reduction of Retained Earnings account) absent from the balance sheets.

Once this fraud is sorted out, their Accumulated Deficit Retained Earnings accounts stand at $-216B together.

Besides for dividend payments, this account is also meant to absorb the future (unexpected) losses.

So much for the "Rehabilitate FnF", required by the Supreme Court and also judge Willett (5th Cir.).

You just need two eyes to spot their Retained Earnings accounts on their balance sheets.

Fannie Mae: $-55.6B

Freddie Mac: $-35.1B

An adjusted Core Capital shortfall over Leverage capital requirement of $402B. Then, apply the 25% of the Prescribed Capital Buffer on top of that.

Way to go to start thinking about dividend payments, unless the Separate Account plan is unveiled: CET1 > 2.5% of Adjusted Total Assets on December 2023, allowing the redemption of the JPS and then, meet the ERCF with Tier 1 Capital > 2.5% of ATA.

Thus, complying with the FHFA's best interests of expulsion of the JPS holders (AT1 Capital).

ZenaTech, Inc. (NASDAQ: ZENA) Launchs IQ Nano Drone for Commercial Indoor Use • HALO • Oct 10, 2024 8:09 AM

CBD Life Sciences Inc. (CBDL) Targets Alibaba as the Next Retail Giant for Wholesale Expansion of Top-Selling CBD Products • CBDL • Oct 10, 2024 8:00 AM

Foremost Lithium Announces Option Agreement with Denison on 10 Uranium Projects Spanning over 330,000 Acres in the Athabasca Basin, Saskatchewan • FAT • Oct 10, 2024 5:51 AM

Element79 Gold Corp. Reports Significant Progress in Community Relations and Development Efforts in Chachas, Peru • ELEM • Oct 9, 2024 10:30 AM

Unitronix Corp Launches Share Buyback Initiative • UTRX • Oct 9, 2024 9:10 AM

BASANITE INDUSTRIES, LLC RECEIVES U.S. PATENT FOR ITS BASAFLEX™ BASALT FIBER COMPOSITE REBAR AND METHOD OF MANUFACTURING • BASA • Oct 9, 2024 7:30 AM