Friday, March 22, 2024 3:52:08 AM

The stock price manipulation isn't about the stock market and the current stock prices that simply reflect what they see on the Balance Sheets and future prospects:

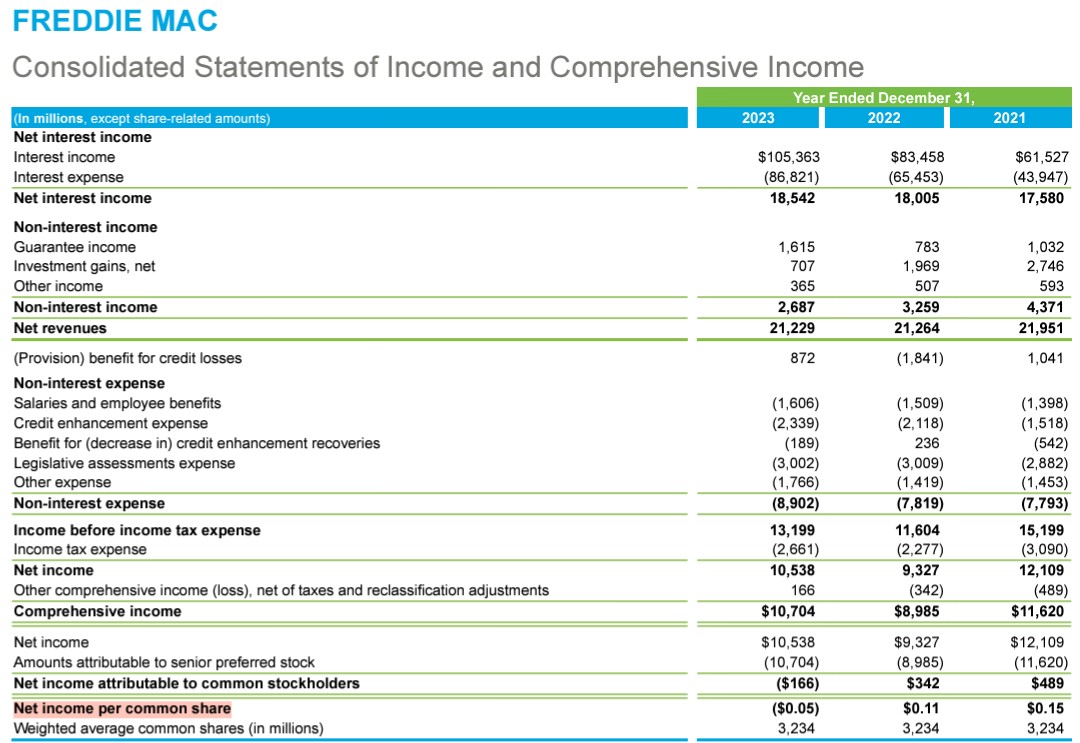

- FnF post $0 Net Income Atribuible to the Common Shareholders, that is, $0 EPS,

- The Warrant to purchase 79.9% common stock at $0.00001 per share,

- $318B SPS LP still outstanding,

- The FnF management and the conservator committing Financial Statement fraud with the SPS LP increased for free absent from the balance sheets.

-FnF auctioning off their NPL and RPL to the hedge funds at fire sale prices, instead of the normal mortgage business of taking possession of the collateral (property) and repackage the RPL into UMBSs again, respectively. Notice that this comes after their foreclosure prevention actions have been exhausted.

FnF can't be used to give business to the hedge-fund industry that works for JPM, Goldman Sachs, etc.

The stocks aren't "permanent options" as the controversial Ackman repeats in his GSE slides to justify the stock price, and later he pretends to be an options trader expert in his twits.

FnF don't "make $10 a share every year", as he claims, but $0, due to the ongoing Common Equity Sweep covered up by the plotters.

Being recapitalized while posting $0 EPS, is called "selling smoke", because the capital built is the common equity (Net Income + OCI = Comprehensive Income on the Income Statement. It turns into Retained Earnings account and AOCI once posted on the Balance Sheet.) that belongs to the shareholders and you have just posted $0 net income attribuible to the common shareholders.

It's the plaintiffs and Co the ones to blame for the stock price manipulation with their government theft story in court, as a result of not challenging the conservator's actions properly, in accordance to the law, regulation and basic finance.

In other words, the stock prices would have been very different had they uncovered the Separate Account plan, but watching the JPS trading at a discount to par value (estimated 6% discount rate over par value until the dividend is resumed -25% of the Prescribed Capital Buffer- Table 8 of the Capital Rule: Payout ratio) wouldn't have been pleasant if they compare it to a common stock that trades at x times the annual EPS and the real thing.

They rather attempt the assault on the ownership, even stuffing the Treasury with SPS LP for no reason (gifted SPS), betting on a swap Preferreds for Common Stocks.

For instance, this is what the judge for the 7th Circuit Court of Appeals stated for the dismissal of his lawsuit or, better said, it looks like the judge gave him a reprimand (words in brackets added by me):

The plaintiffs didn't establish that the NWS (dividend) contravenes that duty (conservator's power: put FnF in a sound and solvent condition)

The judge made our case against the plaintiffs and Co.

The plaintiff didn't point out that a dividend is a capital distribution restricted (it depletes capital) and that the conservator's Rehabilitation power is about building capital (soundness) in a financial company (capital levels).

This is exactly the box 1 in the 6-box checklist that contains the minimum requirement to not be considered a plotter writing formal documents.

All of them will put 5 ticks and Timothy Howard 6, because the box number 5 was created just for him.

Avant Technologies Engages Wired4Tech to Evaluate the Performance of Next Generation AI Server Technology • AVAI • May 23, 2024 8:00 AM

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM