News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Never say "govt motion". A Wall Street law firm represents the FHFA in court.

ARNOLD & PORTER KAYE SCHOLER LLP

Wall Street law firm means that its clients are Wall Street firms.

Also, FHFA, an independent agency of the Federal Govt and sued as conservator of two private corporations.

Anyway, as Federal Agency, the government is vicariously liable for all its actions and the DOJ foots the bill.

This is why we cannot trust this Wall Street law firm when it requests to submit a motion for Judgment as a Matter of Law (JMOL) under Rule 50(b), which is the prior Judgment Notwithstanding the Verdict (JNOV).

Primarily because the deadline has passed:

No later than 28 days after the entry of judgment—or if the motion addresses a jury issue not decided by a verdict, no later than 28 days after the jury was discharged.

The shareholders call on the SEC to probe Bloomberg over lack of controls in the data submitted by financial analysts.

FnF post almost $0 or negative EPS every quarter and, all of a sudden, KBW submits an estimation of $2.89 and $2.4 for 2024 and $3.7 for 2025.

KBW is required to submit its projection of financial statements, not an investment case with assumptions of scenarios.

Attempt by Bloomberg to conceal the existence of a Common Equity Sweep that, in turn, would unveil the prior Common Equity Sweep with the dividends, as a scheme to hold the Common Equity in escrow too.

Both are capital distributions (Dividends and today's SPS LP increased for free. 12 U.S.Code §4502(5)(A)), restricted (Also the Lamberth rebate: CFR 1229.13). The exceptions to the restriction kicked off:

-To pay down the SPS. U.S. Code §4614(e)

-For the recapitalization. CFR 1237.12

Bloomberg follows other attempts, like Bill Ackman and his clerk, Bradford, along with the FNMA CEO and the very FHFA, with: "FnF continue to build capital through retained earnings."

Zero regulatory capital built: it's stuck at an adjusted $-194B Core Capital combined every quarter.

This is stock price manipulation, as the stocks trade according to what they see on the Income Statements and Balance Sheets (adjusted $402B Core Capital shortfall over minimum Leverage capital requirement; $310B SPS still outstanding; Warrant), and not what this organized group says.

$4.8B in Punitive Damages will do it.

.@SECGov OUGHT TO PROBE @BLOOMBERG OVER LACK OF CONTROLS

— Conservatives against Trump (@CarlosVignote) April 12, 2024

EPS always $0 because the Net Income Attributable to Common Shareholders is $0 due to the ongoing Common Equity Sweep.

2025 EPS $0

CE held in escrow as per the exception to the Restr on Capital Distr+Rehab Power.#Fanniegate https://t.co/iMqe48OQ6z pic.twitter.com/nN089AcLlk

(*)The Net Worth increase is the Comprehensive Income in the quarter, calculated with the sum of Net Income (not the Net Income Attributable to Common Shareholders) + OCI. Taken from the Income Statement.

I was thinking of what will be the ultimate increase in the NW of the Balance Sheet (Net Worth activity table) after the payment to Preferreds.

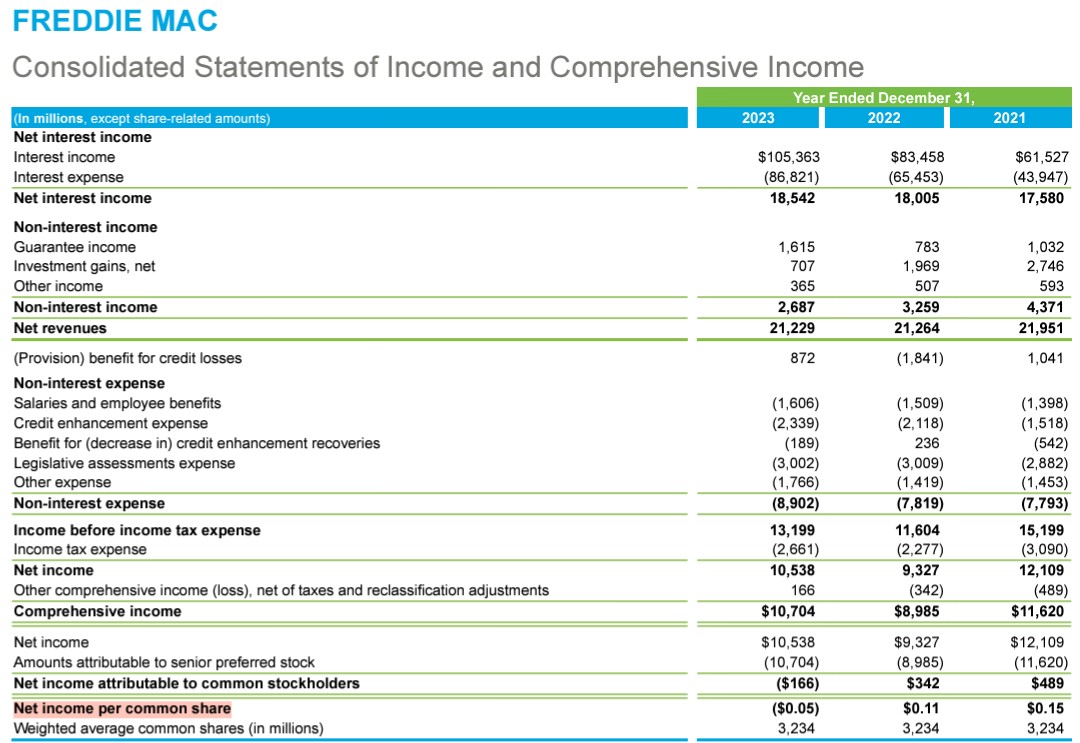

Better read what Freddie Mac says.

Income Statement.

The EPS is always $0 due to the ongoing Common Equity Sweep: SPS LP increased for free in the same amount as the Net Worth increase in the quarter. This gifted SPS LP is absent from the Balance Sheet, along with its offset (Financial Statement fraud).

The estimation for the 1Q2024 is $0.

The estimation for the FY2024? $0

An so on and so forth.

The "Net Income attributable to the common shareholders" that is used to assess the EPS = Net Income of FnF - Preferred Stock dividends or other compensation to Preferreds, such as SPS LP increased for free.

This is why it's close to $0. The amount subtracted is the Net Worth increase (Net Income attributable to the common shareholders + Other Comprehensive Income, that is, change in their unrealized losses in AFS securities, very small in FnF because they use mostly Fair Value valuation instead)

This Net Income attributable to the common shareholders, plus the OCI, is the Comprehensive Income. It's later posted on the Balance Sheet (Retained Earnings account and AOCI, respectively). Both, Common Equity in the Net Worth.

A Common Equity Sweep or, I should say, the Common Equity is held in escrow, in order to uphold the exception to the Restriction on Capital Distributions CFR1237.12 (for Recap) amd the FHFA-C's Rehab power.

This image captures the moment.

When a financial company is authorized to submit its projection of financial statements in Bloomberg, KBW can't make assumptions about future events (SPSPA amendments, a future bidding war for our shares, etc.). That would be an investment case in the reports it sells to its clients in roadshows.

Tremendous error by Bloomberg which, evidently, lacks controls.

This is part of the Fanniegate conspiracy, nowadays with the "everything is fine", transmitting a sense of normalcy and pointing out that FnF could even resume the dividend payments if they are released as is.

The SEC and the UST ought to probe Bloomberg over how financial companies submit input.

(*)$178B profit assumes that the UST collects their Deferred Income, net ($48B), in the case that there is an Accounting Standard change (the Upfront g-fee or LLPA, is renamed Delivery fee), through a higher PE multiple in the resale price.

Then, the prospective buyers are the ones that amortize the Deferred Income, gross ($61B), in one fell swoop, and it's when they recover the overprice paid through a special dividend if they wish, when the PE ratio drops. This is why the PER 10 and 12 times, are effective PERs.

Christopher Whales is clueless about FnF matters and he is just annoyed about the share price, which reminds me the plaintiff Joshua Angel who writes on this board with 30+ aliases, always obsessed with the fact that a common stock is worth more than his JPS, once the numbers are adjusted. This is something that he can't withstand. Either he throws numbers at the wall: $10, $20, always below his JPS par value, or he claims that a common stock is worth $1,500, to portray the shareholders as lunatics.

The problem of being so clueless is that your take could well have been written by a kid.

Whales doesn't even know that the SPS are no par value Preferred Stocks, when he calls for monetizing the SPS at their par value.

This is because he has never read a document about FnF: Charter Act, FHEFSSA, HERA, SPSPA, SPS certificate, etc.

All he knows was learnt on the streets.

He comes again with the slogan that President Biden is the one that releases FnF from conservatorship, disregarding that it's a FHFA Conservatorship and the FHFA is an independent agency of the Federal Govt, not subject to the direction of any other Agency, waiting for the direction of Congress, as the UST recommended a Privatized Housing Finance System for the release (guarantee fee increases, 3-options, etc.) in 2011, at the request of the Dodd-Frank law.

The laws, regulation and financial concepts are for grown-ups. This is why he is just a kid, like Bradford with:

These two companies have a net worth that increases every day. At some point it has to mean something.

HEY KID!

— Conservatives against Trump (@CarlosVignote) April 12, 2024

-MBS aren't gteed by the U.S.

-FHFA's control of Conservtrshp, not govt's. FnF operate business as usual: UST backup of their operations

-Funding Commitment Fee, barred(CRT,too)

-Charter revoked(2011 UST Plan)

-Max Credit rating:CET1>2.5% of ATA(Separate Acct)#Fanniegate https://t.co/2ibY2SUmOL

The UST can make an honest $178B profit with FnF, by acquiring our stocks at their adjusted BVPS and resell them with a PER stock valuation.

Too bad that $152B was already taken away from the enterprises: $110B SPS overpayment, $19B CRT expenses, net (Charter-unauthorized credit enhancement operation), and the $25B settlement of the PLMBS lawsuit, net of attorney's fees (the cash refund is $2B lower than the sum, in order to comply with the Asset-Liability matching principle when everything is unwound: $244B posting in their Retained Earnings accounts; Treasury Stock, retired. The UST got lucky).

Therefore, it'd only have $26B available for new investments or debt forgiveness across the board.

SUMMARY

$178B profit with a Taking + resale.

+$42B in TCCA fees (10 bps guarantee fee funneled to UST under the TCCA. Now, BBB Act)

+$5B allocated to 2 Affordable Housing funds managed by HUD and UST (4.2 bps on new acquisitions)

+$15B owed to FnF as managers of Obama's Making Home Affordable program (estimation too)

TOTAL = $240B

A pretty decent windfall knowing that the Treasury Department is forbidden to make money using the assets and securities of FnF in the Charter Act, other than the rate on the original UST backup of FnF since the Charter's inception (estimated at a weighted-average 1.8% cumulative dividend on SPS. It's netted out with the interests on the $152B it owes to FnF)

Also taking into consideration that Ginnie Mae kept the special assistance functions when it was spun off from Fannie Mae in 1968.

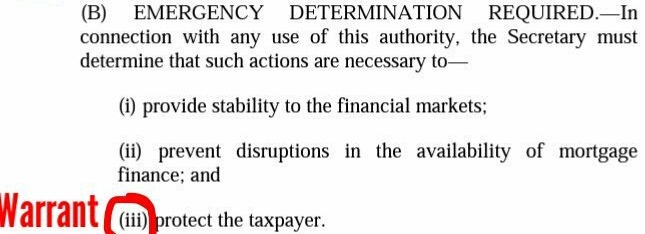

Pagliara talks about the Warrant gotten at no cost, and he calls it "investment", disregarding the reason why this security was authorized in the first place: to (iii) protect the taxpayer (collateral).

The exercise price of $0.00001 per share is evidence in itself of being considered as collateral of the investment in SPS.

Let alone the "shares assigned to any Person" clause 2.1 of the prospectus, for the assault on the ownership paying nothing, better than paying a Price Earnings Ratio of 10 and 12 times, for FNMA and FMCC, or even greater.

That's NOT our LIBOR interest rate lawsuit.

That's a settlement with the Exchange-Based Plaintiffs that transacted in LIBOR-based Eurodollar futures or options on exchanges.

https://www.usdliboreurodollarsettlements.com/

We are among the ones called OTC plaintiffs with direct claims. Those that transacted in interest rate swaps, for hedging the interest rate risk. Due to lack of popularity of this product as a result of this scandal, we have today's banking crisis with the massive unrealized losses unaccounted for (Liquidity and Solvency Risk in bad times), because the unrealized losses aren't the problem in themselves.

There is also the Class Action Plaintiffs, those with economic harm due to LIBOR-based investments: currencies, bonds, deposits, derivatives, etc.

We are talking about the well-functioning of the financial markets and the LIBOR case should go to trial and get treble damages. No settlement whatsoever.

It seems that there is a business with the banks committing fraud and the attorneys settling for maximum the loss incurred, which was the profit for the bank. So, a fraud at no cost for the "try again later", and a big payday for the attorneys.

Beware of "Boris the Spider".

I have a very good idea about who is behind this alias. He regularly writes with 2 aliases on this board, even bashing the Lamberth's fat bonus with an alias pretending to be a foreign guy, in order to pump his lawsuit in court, because he always loves to be in the limelight.

He fuels speculation of a settlement to solve a dispute with the crooked Fanniegate plaintiffs.

The famous negotiation: "The government comes to me", stated by the attorney for Berkowitz, the "unsophisticated lawyer" David Thompson, he told us. Basically recognizing that he is a financial illiterate, thinking of his defense strategy if he is called out one day: Capital distribution? Never heard of that; I don't understand. Ask the sophisticated lawyers for an answer. I'm just a litigator; Etc..

The link to the Conference Call hosted by Pagliara was posted yesterday, to listen to both remarks.

The lawsuits can be expensive indeed. Crippling liabilities arise.

But it can be expensive,...

... and the less prepared you are, the more expensive it will be.

With respect to capitalization, I am not a regulatory lawyer. I am a litigator....That's being watched by a number of sofisticated lawyers...

This Restriction on Capital Distributions in the FHEFSSA (U.S.Code §4614(e)), was later supplemented (which means there was intent to carry out a "follow-on plan") and shall not replace or affect it (clause (c) below), with the CFR 1237.12 of the July 20, 2011 Final Rule, when the FHFA director foresaw that, with the coming NWS dividend, the SPS will be fully repaid fast and it was needed another exception to apply the assessments towards: Deplete capital (capital exits the balance sheets) is authorized if it recapitalizes FnF (build capital), which is Separate Account wording right there, through regulation.

Notice that this Final Rule was enacted two weeks before the FHFA announced a proper Recapitalization Plan for the FHLBanks, that is, on-Balance Sheet.

Though, in this press release we see that the FHFA has a huge problem with the financial statements, as alibi for having written a Separate Account (outside their Balance Sheets. Financial Statement fraud) through regulation with FnF.

Separate Retained Earnings account on the Balance Sheet doesn't exist by any stretch of the imagination.

Let alone a Separate Restricted Retained Earnings account.

All forms part of the same pot and the capital requirements are enough restriction to not allow the shareholders to take it away through a special dividend or stock buybacks that deplete it. But you can't write "separate restricted Retained Earnings account". This obsession with "separate accounts" was an alibi for Fanniegate, carried out outside their balance sheet (External Position, Bundesbank-style with the ECB's Payment System Target 2. The FHFA and ECB's Draghi had the same advisor, Goldman Sachs).

Quit posting your flawed analysis of the Restriction on Capital Distributions.

The grounds of the Separate Account, you have spent 10 years laughing at me for highlighting it, Mr.Pro Se. A statutory provision that you have covered up in the Lamberth and Sweeney courts.

Since a few months ago, you post it from time to time with the goal to sneak a few lies:

-In HERA indeed, but what it did is to insert it in the FHEFSSA. Then, it's no longer in HERA.

-It's not a "refinancing option of the SPS", but a way to reduce/pay down the SPS for good.

The requirement in the exception (A), is to get the same amount of dollars either issuing shares or obligations. So, FnF can issue debt obligations to reduce the SPS. Different securities. Then, it's not a refinancing option but a new security. The intent of the lawmakers is to get the same amount of cash at the same time, and that's satisfied when FnF increased their Common Equity (Net Worth) that carries a double-entry accounting with cash. This way, FnF have reduced the SPS as the Common Equity increased, then swept with the assessments sent to Treasury under the guise of dividend payment (restricted and unavailable earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings accounts), as seen in the signature chart below with Freddie Mac.

By the way, this is how the Federal Reserve will reduce its Deferred Asset (Latest, $161B): as the Common Equity (Retained Earnings) increases. This is why the trick (fraud) of "Deferred Asset" (accumulated losses) is a substitution for SPS.

The deferred asset is the amount of net earnings that the Federal Reserve Banks need to realize before remittances to the US Treasury resume.”

In essence allows the trustees of Fannie and Freddie to go to the market at any time to raise new capital,

FHFA declared the Critical Capital level ............IRRELEVANT.

On day one of Conservatorship.

At the time, it was understandable because it talked about the "critical capital trigger" that triggers a conservatorship, "during the conservatorship period".

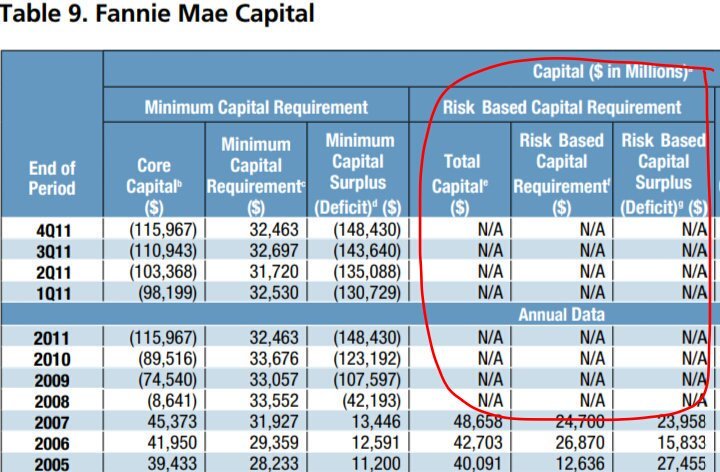

This is why FnF have only published their Minimum (Leverage) Capital level and capital shortfall (deficit) with the Core Capital, every quarter since day one (statutory) in their Earnings reports (10-k form filed with the SEC).

This is Freddie Mac:

HERA struck the FHEFSSA's formulaic of Risk-Based Capital requirement, so N/A until the FHFA comes up with a new one.

FHFA Report to Congress:

At some point, the Critical Capital level must be published. Mainly in the ERCF in light of the Capital Rule that came into effect on February 16th, 2021, as commented before.

But not meeting a capital level called "critical" bothers to the plotters in their slogan of "FnF have been rehabilitated", which is what requires Justice Alito and judge Willett, in their interpretation of the FHFA-C's Incidental Power.

What the judges were doing was explaining the Separate Account plan.

Justice Alito: Rehabilitate FnF in a way, not in the interests of FnF with awful ERCF tables, but in the best interests of the FHFA.

Judge Willett: "Any action within the enumerated powers".

And Justice Alito's add-on: "...and the public it serves", not written in the law, so that the UST can keep the estimated $15B owed to FnF in TARP funds, for being used as managers of Obama's Making Home Affordable program (MHA guidelines). TARP was deemed a success at the time, just because it owed big money to FnF (only $3B disbursed out of $30B obligated). Also, for the sale of NPL and RPL to the hedge funds at bargain prices, sale of REO inventory to minority- and women-owned businesses, LGTB associations, Neighborhood Associations, etc.

At some point, this Separate Account that resembles the statutory wording of the one with the FHLBanks in1989, will have to be unwound to see their financial rehabilitation for real on the Balance Sheets.

This is the reason of their con job: this capital threshold no longer exists. And pointing out HERA, so you will never find it out if it's located in the FHEFSSA.

The FHFA's flag is upside down.

Capital Classifications are set forth in the FHEFSSA of 1992, not in HERA which simply amended the FHEFSSA and the Charter Act. HERA isn't a law in itself if it just states:

"Section .....of the FHEFSSA is amended by inserting..... after subsection ...." Etc.

All of a sudden, you have deleted the 4th Capital Classification: Critically Undercapitalized.

12 U.S. Code §4614(a)(4)

An enterprise shall be classified as critically undercapitalized if—

(ii)does not maintain an amount of core capital that is equal to or exceeds the critical capital level for the enterprise;

Outside of conservatorship, i.e. once FHFA is forced to give FnF capital classifications as required by HERA, FnF will have to be classified as "significantly undercapitalized" by 12 USC 4614(a)(3)(A)(ii) if they don't meet the minimum capital requirement.

Book Value Per Share as seen on the balance sheets.

I've already explained how the Common Equity is calculated in any financial company, with the data taken from the Balance Sheets, with an example of JPM.

Also, I continuously repeat that their Retained Earnings accounts are still deep in the red. Then, everything has to be adjusted for the offset (reduction of Retained Earnings account) attached to the SPS LP increased for free ($-216B Accumulated Deficit Retained Earnings accounts combined).

What is new, is that it's been found a financial website that posts the BVPS, because, as it's negative, most of the websites post N/A.

The BVPS is useful to calculate the Price to BV ratio, as a reference for stock valuation (JPM =1.8)

Book Value is just a reference because it's what the shareholders would get if the company were to be liquidated or, in our case, useful to stage the Charter revoked as a cut-off date.

This is why, in our case, the adjusted BVPS is what is required in the case of a Taking by the UST, instead of other stock valuation methods like the PE ratio.

All the Common Equity generated by FnF is held in escrow, including the one syphoned off to UST with the illegal CRT operations (unauthorized in the Credit Enhancement clause) or the settlement of the PLMBS lawsuit. They want the UST to buy our stocks on the cheap.

Everything will be adjusted.

The tweet provides a link to see how the Common Equity has been calculated in FnF in order to unwind the Separate Account plan (Premise: no dividend to anyone), starting with the beginning balance as of June 30, 2008, adjusting their Balance Sheets.

BOOK VALUE/TANGIBLE BOOK/COMMON EQUITY PER SHARE

— Conservatives against Trump (@CarlosVignote) April 7, 2024

Under the Separate Acct plan:$FNMA =$116$FMCC =$170

Assessed:https://t.co/m36B9LyRI2

🚨As seen on the Bce Sheets, pending the adjustment for the offset(↓RE)with the SPS LP increased for free:

FNMA=$-54

FMCC=$-60

DIY👇#Fanniegate https://t.co/IpbjkPlsd0 pic.twitter.com/L3B0HSa1is

BVPS ADJUSTED FOR THE "EXTERNAL POSITION": FINANCIAL STMNT FRAUD

— Conservatives against Trump (@CarlosVignote) April 8, 2024

Like the #ECB's Payment Sys,#BOE,...

It began w/ Mnuchin/Trump-Watt's PA amnt,Dec 2017 ($3B Capital Reserve/$3B gifted SPS)

Same advisor, $GS.

Everything is deprived of its value/meaning: unbacked crypto.#Fanniegate https://t.co/jhIiyOyRpd pic.twitter.com/Pcdwm9qnAO

You call the dividend on SPS "commitment fee" to fit your narrative, contending that there is a Limitation on Fees by the United States, in the Charter Act.

No commitment fee on the UST's Funding Commitment was ever assessed or collected. So, shut up.

There is only the initial $1B SPS LP issued for free and the Warrant, that, in some documents, is called "initial commitment fee".

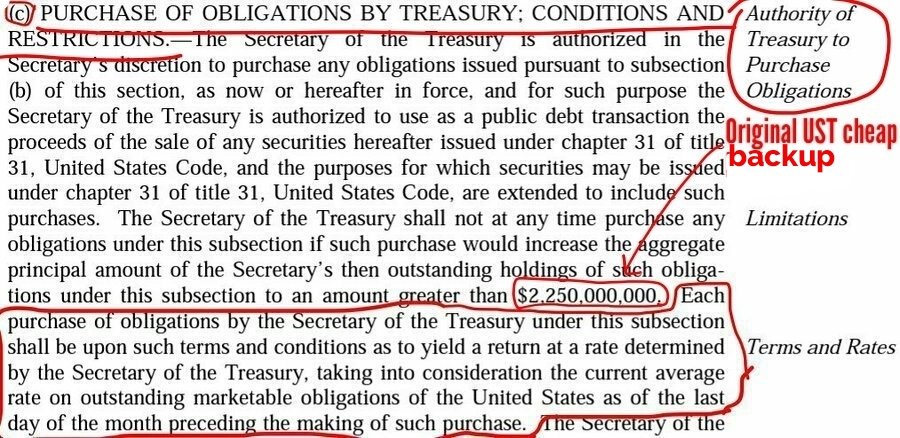

This is why we fix it by considering these gifted SPS a higher compensation to UST, thanks to the provision that allowed a 10% and NWS dividends, subsection (g), the second UST backup of FnF inserted by HERA into the Charter Act of Fannie Mae.

This higher compensation is later unwound, in order to uphold the original UST backup of FnF at rates similar to Treasuries, subsection (c) (any obligations of subsection (b) redeemable obligations, including the SPS), which is the exception in the Fee Limitation of the United States that you have written.

No provision of this subsection shall affect the purchase of any obligation by the Secretary of the Treasury pursuant to subsection (c) of this section.

The fact that Hamish Hume filed the motion for extension of time to file the appeal with Wazee, the same day judge Lamberth filed the Final Judgment (March 20th), is evidence of the plot pointed out, about this attorney hiding the Wazee appeal to use it in a negotiation in the Lamberth court (fat bonus, the fiction of damages due to breach of "implied contract", etc.).

"Gimme the booty and I let the Wazee case die, or else!"

The Fanniegate attorneys protect the Lamberth's fat bonus worth $180mll (a 30% cut of $600mll awarded)

Firstly, it was their ally, the judge, obsessed with granting back dividends to a Non-Cumulative dividend stock.

No genuine dispute remains on the fact of harm on the theory of plaintiffs were denied dividends that they otherwise were reasonably certain to receive. (Source)

"With respect to capitalization, I'm not a regulatory lawyer. I'm a litigator...That's being watched by a number of sofisticated lawyers"

VOID

— Conservatives against Trump (@CarlosVignote) March 31, 2024

1-Breach of Rule 23(b)(3)

2-No harm: Div impeccably suspended

3-Award+Plan of Allocation unrelated to initial claim(3rd amdt-day share price drop)

4-Rebate restricted too

5-Case🆚FHFA,but its Dtr was dismissed as Defendant in her official capacity.#Fanniegate @TheJusticeDept https://t.co/fdA2qIFbxu pic.twitter.com/N0HCWzKxEi

FnF's loss due to LIBOR manipulation tops $3B in audit (the FHFA-IG office).

Source.

Then, how on earth did you come up with $400B in losses in all the 220 plaintiffs involved?

I doubt that the FDIC, as receiver for 38 small banks, can even top the $3B of FnF, yet you claim that Washington Mutual alone will get $100B.

Also, you claim that

Fannie freddie get 5-10b

Close of fact discovery: April 4, 2024, as scheduled.

This is why the Liaison counsel asked the judge to skip it:

to take a limited number of depositions following the close of fact discovery on April 4, 2024.

*** Scheduling Order in the LIBOR antitrust case ***

Posted at the bottom of the comment.

It doesn't say "Discovery closed 10 days earlier than scheduled", as you claim.

It closed as of April 4, 2024, as scheduled.

In the letter, the Liaison Counsel just requested to:

take a limited number of depositions following the close of fact discovery on April 4, 2024.

Plaintiffs request no additional changes to the Scheduling Order (Doc. 3687).

04/05/2024***NOTICE TO COURT REGARDING STIPULATION OF VOLUNTARY DISMISSAL Document No. [4003] Stipulation of Voluntary Dismissal was reviewed and referred to Judge Naomi Reice Buchwald for approval for the following reason(s): the plaintiff(s) filed their voluntary dismissal and it did not dismiss all of the parties or the action in its entirety. (Text entry; no document attached.)

The last date in the Scheduling Order: January 2025.

Next week is Libor week.

FHFA is an independent agency of the Federal Government.

As conservator, FHFA is even more independent:

FHFA has limited powers, as it's still subject to the FHEFSSA and the Charter Act. The reason why we request a refund of the CRT expenses, net (deductible expenses, now they pay income tax), illegal in the Credit Enhancement clause.

The Supreme Court didn't say

FHFA has nearly unlimited power through HERA as ruled on by the supreme court in the Collins case.

the president of the United States has, in all accounts, unilateral control (all three constitutional branches) of Fannie Mae and Freddie Mac.

The settlement worth $25.5B of the PLMBS lawsuit brought by the conservator FHFA on behalf of FnF, in a case against 18 financial institutions and a $202B PLMBS portfolio, has not been recorded on their Financial Statements and then, swept to the UST as you claim.

Just look up their financials from 2013 through 2017. You’ll see amounts they received in settlements. I on vacation and can’t provide you with the PDF files.

LIBOR case: the judge sides with the defendants.

The judge discourages the LIBOR litigation that pursues treble damages in a trial, in favor of a settlement for a fraction of the actual loss incurred.

With words like "complexity", "What loss?" or "difficulty in proving a 16-bank conspiracy".

There is no complexity in the interest-rate swaps. Treble damages are necessary to protect this product in the future (the cause of today's banking crisis with the massive unrealized losses in Debt instruments in the U.S. banks, that remain unaccounted for)

The loss has already been assessed in more than $3 billion in FnF, by an auditor (the FHFA-IG office). Link.

As far as conspiracy is concerned, the intent by a panel of banks was clear and they had an active participation. The fact that the crime existed, is evidence of an agreement.

The $FNMA CEO could be eager to settle the LIBOR antitrust claim with her former employer, $JPM, for peanuts, after watching her very active recently spreading the known lies of "FnF build (regulatory) capital", "FnF have been (financially) rehabilitated", etc., publicly, as FnF would need to be released first, so the managements recover the powers.

This is an excerpt taken from the judge's order that approved the Barclays and Citigroup settlements in August of 2018, in favor of a settlement for a fraction of the losses:

A future court award of treble damages would be recorded as Common Equity (Retained Earnings account). Until then, the existing shareholder doesn't have a legal claim on that amount.

Libor antitrust claim: A voluntary dismissal yesterday of one plaintiff and one defendant, Citigroup, but the California Public plaintiffs sued a panel of banks. Therefore, it's still a plaintiff.

If a settlement isn't made public, it's because of this antitrust claim, which means that they were actions that harm competition. That is, a 16-bank conspiracy.

With an antitrust claim, we are talking about treble damages.

The state of California has a lot of explaining to do with this voluntary dismissal of a case brought by several cities and public entities.

Citigroup settled the Libor litigation with several plaintiffs in 2018.

In 2019, the city of Philadelphia settled with Citigroup too, and it also sued a panel of banks.

It's not just the FDIC and Freddie Mac. Hello?

They are 223 plaintiffs (3 cities, pension funds, etc.) suing 119 banks, some of them have the same parent company. For instance J.P. Morgan Bank Dublin PLC and J.P. Morgan Markets Ltd, appear jointly with the parent company JPMorgan Chase Bank. This is why the number of banks is swelled.

The reason why in the docket entry with a letter sent to the judge, appears the FDIC and Freddie Mac, is because they share the same attorney:

James R. Martin

Zelle LLP

Fannie Mae is represented by a different law firm.

But the attorney James R. Martin signs the letter also as Liaison Counsel for the Direct Action Plaintiffs, which means that he was chosen by the judge to represent all the plaintiffs that already had multiple lawsuits dispersed, and have been gathered in this case.

This is why he sent a letter to the judge as Liaison counsel, not as attorney for the FDIC and Freddie Mac.

The letter is also signed by another attorney that has formed a class action with other plaintiffs: Co-Lead Counsel for the OTC Plaintiffs and Liaison Counsel for the Class Plaintiffs.

Link to the court docket: https://www.courtlistener.com/docket/4349421/in-re-libor-based-financial-instruments-antitrust-litigation/?order_by=desc&page=1

You fool no one.

FDIC on behalf of 20 failed banks and Freddie Mac suing 16 big banks...

FnF lost more than $3B as a result of the banks rigging the interest rate Libor, "according to internal memos by the auditor of the Federal Housing Finance Agency", referring to the FHFA-IG office and reported by Bloomberg in December of 2012.

FnF could be awarded treble damages.

Treble damages are a type of punitive damage that rewards the victim three times the number of actual damages.

"Plaintiffs FDIC as Receiver for "Federal Home Loan Mortgage Corp" (FMCC)"

The Federal Deposit Insurance Corporation as Receiver, The Federal Home Loan Mortgage Corporation.

The court system was a tool for 24/7 court news, required by the Hedge Funds, Private Equity firms and Investment Banks to,

First, peddle the government theft story, that is what has decimated the share prices,

Secondly, deprive the laws and the financial concepts of its meaning, or directly, cover them up, for the slogan "FHFA can do whatever the hell it wants", and everything boils down to a case of "Equity restructuring", also called "re-privatization".

Thirdly, transmit a sense of normalcy that conceals the Machiavellian terms during the conservatorships. The "everything is fine", "there is light at the end of the tunnel" or "a fresh start" initiated with Mnuchin's remark: "We've got to get them out of government control", referring to the conservator. Followed up by paid shills with "FnF continue to build capital through retained earnings", while posting $0 EPS every quarter like before, when it's precisely Retained Earnings the Net Income attributable to the common shareholders to calculate the EPS that shows $0.

Or even nowadays, thinking that everything is sorted out by simply asking for the SPS be cancelled (debt forgiveness), or a haircut and then a conversion to common stocks, so that the JPS mimic this swap with the same terms and conditions, as stated by Mnuchin according to Calabria in his book (no actual records exist because the goal is just to maintain the threat of dilution, for stock price manipulation)

Holy cow! Bradford, the self-proclaimed "Fanniegate hero" and his boss, Bill Ackman, are involved in every aspect of Fanniegate mentioned above.

The DOJ is compelled to take up the complaints on social media, by the retail investor, in a clear case of abuse of court process, where the retail investor's interests haven't been defended properly.

The key: the usage of formal documents and made publicly available by simply posting them online.

The truth they have so far revealed is that the court system is corrupt in favor of government fraud and deception. This is of course my opinion

The Letter Agreements can be called SPSPA amendments, but you can't call the latter "SPS certificate" because they are DIFFERENT documents.

You keep on posting the SPS certificate of designations and calling it "SPSPA", punk.

Every stock has its Stock certificate of designations, that, in the case of the JPS, is called "prospectus" or directly, "contract".

This is why the 3rd Letter Agreement, is the 6th SPSPA amendment.

3rd SPSPA amendment, August 2012 (NWS dividend).

4th SPSPA amendment, December 2017 or 1st Letter Agreement.

5th SPSPA amendment, September 2019 or 2nd Letter Agreement.

6th SPSPA amendment, January 14, 2021 or 3rd Letter Agreement.

It's not my fault that someone came up with the bright idea of start calling them "Letter Agreements", thinking that, because it isn't called "PA amendment", the Statute the Limitations isn't reset, when, if it's an amendment of the terms and conditions on how the Treasury gets compensated, it's called "PA amendment".

The one in question (the 6th) it's not "the 4th amendment", mentioned by Justice Alito, who paved the way for the scammers to call the 4th amendment to the SPS certificate that came up weeks later (April 2021) without the presence of the UST secretary because it's an automatic deed, "4th SPSPA amendment". What you keep on doing.

What we are debating on, are the SPS Purchase Agreement amendments. The binding documents. Not the SPS certificate of designations that is amended as a result.

You have been caught in a conspiracy to involve secretary Yellen in the flawed 6th SPSPA amendment (Calabria-Mnuchin) and in turn, in all the prior PA amendment scheme, jointly with Guido, but you chose to play the fool as exit strategy, rogue plaintiff Mr. Pro Se (no other says "Broken record" and you always have a desire to reply to my posts with a turd, after being called out for your lies).

*** Timeline of the Fanniegate scandal ***

Nothing has been done by chance. This is why the FHFA Final Rule in 2016 for the FHLB membership cleansing, that was first proposed in 2010, gave 5 years to the FHLBanks to "wind down their affairs with the captive insurers".

It's 2021 when FnF became Undercapitalized (a percentage of the Adjusted Total Assets -Leverage ratio-), which makes them Adequately Capitalized because the threshold (a percentage of the RWA -Risk-Based Capital requirement-) is lower in FnF.

But the FHFA realized that, at the time, the JPS couldn't be redeemed at par value and, even when their fair value fetched their par value with the estimated resumption of dividend payment later on, it couldn't be done either, as the JPS are Core Capital and thus, if they are redeemed, FnF wouldn't meet the ERCF.

It's not until CET1 > 2.5% of Adjusted Total Assets when the JPS can be redeemed and then, continue to meet the ERCF with Tier 1 Capital > 2.5% of Adjusted Total Assets.

Wait! Because the FHFA wanted to meet another threshold, which is 25% of the Prescribed Capital Buffer after the redemption of the JPS, for the normalcy in FnF with the resumption of dividend payment, upon announcement of the Privatized Housing Finance System chosen for the release by the UST in a 2011 Report to Congress, at the request of the Dodd-Frank law: "Recommendations on ending the Conservatorships".

The last threshold possible was met by the laggard Fannie Mae with the 4th quarter Earnings report released a few weeks ago. After that, we are in unchartered (Act) territory. There are no more thresholds under the Separate Account plan.

CONGRESS GAVE FHA 10YRS TO BUILD 2% CAPITAL

— Conservatives against Trump (@CarlosVignote) April 2, 2024

2011: UST chose Basel.

FMCC/FNMA

10yrs: 1Q2021/4Q2021 Adeq Capitalized(no dilution)

3Q2021/3Q2022: 25% C.Buffer→Div resumes(JPS=par value)

3Q2022/3Q2023:CET1>2.5% ATA→JPS redeemed

Laggard 4Q2023: JPS redeemed +25% C.Buffer#Fanniegate pic.twitter.com/QoN2r3YeBK

You post the 4th amendment to the SPS certificate.

Dated 04/13/2021.

Not the 4th amendment to the SPSPA. Hello?

The SPS certificate is amended a few weeks after a SPSPA amendment (if considered necessary) to simply reflect the changes already approved.

The one that you mention, 4th SPS certificate, occurred in light of the 6th SPSPA amendment, dated 01/14/2021, agreed on by Calabria and Mnuchin, that includes all the known flawed aspects:

-Capital Reserve End Date.

-Release when CET1 > 3% of Total Assets.

-NWS dividend would resume in the future.

-Warrant exercised

-Stock offerings.

It's been denounced that those that call the 4th SPS certificate amendment, "4th SPSPA amendment", like you, attempt to include secretary Yellen in the Fanniegate scandal, because she was sworn in on 01/26/2021 and thus, unrelated to the flawed 6th SPSPA amendment of 01/14/2021.

Justice Alito kick-started this plan of deception aiming to involve secretary Yellen, when he called this 6th amendment of the SPSPA, "4th amendment", and sold as a game changer by the way, tricked by a letter sent by the solicitor general Perdogar "retain capital", when it's the same Common Equity Sweep as before.

He could have called it "3rd Letter Agreement" or "6th SPS amendment", but never "4th amendment" because that was the 4th amendment of the SPS certificate.

Here is a breakdown of all of the above:https://www.fhfa.gov/Conservatorship/Pages/Senior-Preferred-Stock-Purchase-Agreements.aspx

Then, there is Bradford calling the SPS "SPSPA" to the same end, but it's because he lives in a different planet.

spspa conversion.

"Fully capitalized".... "NWS resumes". A bunch of lies.

Fully capitalized.

NWS resumes.

The peddlers of the government theft story owe us $4.8B in a compensation for Punitive damages.

The plaintiff Bryndon Fisher is included.

the $$ they stole

The grown-ups talk about laws, regulation and financial concepts.

Your separate account plan that you say by its own existence makes the lawsuits frivolous— i wonder if you would agree that — if it does not exist then the lawsuits would then have merit —

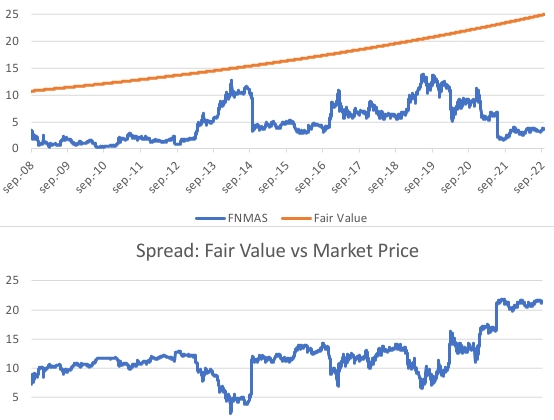

(*) $12 is an average in the spread Market price - Fair Value through the 3Q2022. Estimated $12.5 through today. Half the par value of $FNMAS.

(*) "5- and 6-year investments in SPS" in Freddie Mac and Fannie Mae, respectively, not the maturity because the SPS LP was "increased" in different quarters and also it's been considered the partial repayments through the exception to the statutory Restriction on Capital Distributions (U.S.Code §4614(e)), with the assessments sent to Treasury, under the guise of dividend payments (unavailable earnings for distribution as dividend, out of Accumulated Deficit Retained Earnings accounts -Balance Sheets-).

This is why it's mentioned a "weighted average" cumulative dividend rate (1.8%), "taking into consideration the Treasury yields as of the end of the month preceding the purchase", as per the original UST backup in the Charter Act, de facto updated with the SPSPA, which emerged in light of the authority of UST in the homonymous second UST backup inserted by HERA in the Charter Act by the ambitious Calabria/Pelosi for a Separate Account plan and the massive plan of deception attached.

The SPS complied with the authority of UST (i) and (ii):

The original rate on "any" (subsection (c)) "redeemable obligation" (subsection (b)), including the SPS (the preferred stocks are obligations in respect of Capital Stock and redeemable at the option of the issuer), is the one that prevails, primarily because it's permanent, whereas the other was temporary (deadline December 31, 2009).

Let alone because it's part of the Charter Act dynamics:

-As a last resort and in exchange for their Public Mission (section Purposes)

-The United States can't use FnF as piggy banks to make profits using their assets and securities, other than the rate similar to Treasuries mentioned before.

The litigants still don't understand that FnF are not ordinary businesses, but congressionally chartered-private corporations.

The law professor Nielson, Supreme Court-appointed amicus representing the FHFA in the Collins case, spotted the original UST backup of the enterprises right away. The hedge funds and investment banks forgot to pay him off too.

All the lawsuits are meritless with the Separate Account plan. That is, every single action has been lawful and the very Separate Account plan is lawful too, thanks to the "best interests of the FHFA" in the FHFA-C's Incidental Power: "Any action authorized by this section, ...".

It means that the litigation ends instantly.

As an attorney, Hamish Hume knows there is years of litigation ahead.

The 2 docket entries about DeMarco, are dated March 21, 2022.

The motion filed by him impersonating a FHFA employee, was a motion for summary judgment at the same time Fairholme filed its own motion.

Case Fairholme vs FHFA in the Lamberth court.

Therefore, it occurred before Fairholme filed in October 17, 2022 a motion to dismiss the FHFA director Sandra Thompson as defendant, in her official capacity (Screenshots posted before). Exactly on the day the first jury trial started out.

I wonder whether this invalidates the whole thing (two jury trials)

An institution can't defend itself. There has to be always the maximum executive as defendant to represent it, acting in his official capacity.

There's been two trials without the FHFA director as defendant.

The desire of Sandra Thompson that the Conservatorship doesn't exist (when it was the FHFA Director the one that appointed FHFA "conservator"), blame DeMarco for any past troubles, and therefore, she is only the director of the FHFA as regulator, so she can replicate HUD an stage that she is following orders from the White House, could backfire.

The Lamberth trial is annulled and HUD will take the place of FHFA, once the Charter Act is revoked, in a Privatized Housing Finance System chosen for the release in 2011 by the UST (a Report to Congress required by the Dodd-Frank law): increasing the guarantee fees, 3-option Privatized Housing Finance System revamp, commingled securities for a Catastrophic-Loss Reinsurance, etc.

Navy Hedge Fund "Hi Ron"-Attorney Hamish sent emails each other frequently.

For instance, here with Samuel Kaplan, a partner in the same law firm.

Now, he stages that he is no longer friend of this attorney, due to his threat "the government will appeal" recorded in audio tape and made public online when the market was already closed, yet Navy Hedge Fund is crying out loud hysterically to make his point. Dude, get a grip.

The court cases are irrelevant during a Conservatorship to begin with.

Because the hedge funds own the FHFA, now the hedge funds dare to talk on behalf of the government, telling us that it will appeal. They even disregard that the FHFA is an independent agency of the Federal Government and that it was acting as conservator in an "implied in fact contract claim" against the issuers of the securities (FnF), because it was a claim that emerged from the retention of securities (This is why the award is taken from the enterprises), as explained by the FHFA in the preface of the famous July 20, 2011 Final Rule (This payment was declared a capital distribution. CFR 1229.13, thanks to an express grant of authority by statute 12 U.S.Code §4502(5)(A), like dividends and today's SPS LP increased for free), where it stressed that this payment of securities litigation judgment is PROHIBITED, arguing, precisely, that it would violate two of the statutory provisions covered up by all the litigants, and the grounds of the Separate Account plan (This masterpiece serves as explanation of the entire Conservatorship):

-Restriction on Capital Distributions.

-FHFA-C's Rehabilitation power: Put FnF in a sound and solvent condition.

This payment isn't up to the conservator's discretion as it claimed later (CFR 1237.13), presumably with the CFR 1237.12, primarily because this one expressly states in (c) that it supplements and shall not replace or affect the statutory Restriction on Capital Distribution (U.S.Code §4614(e)).

A capital distribution is restricted when FnF remain undercapitalized. End of the story. There are no "superpowers". A conservatorship isn't meant neither to break the existing laws in force, nor to create a shadow Housing Finance System.

It's obvious that the FHFA won't appeal because it's been a frivolous lawsuit brought by the hedge funds in collusion with the FHFA, aiming to blame DeMarco and conceal the Separate Account plan, in order to hold up their government theft story.

Sandra Thompson urged Berkowitz (Fairholme Funds) to remove her as defendant in a case against the FHFA where she is the director.

Then, DeMarco, who is no longer an employee of the FHFA, was compelled to appear in court and file briefs on behalf of FHFA.

This is beyond abuse of court process. It's a con operation.

BREAKING NEWS. The attorney Hamish requested an extension of time to file the appeal with Wazee, that was due on March 25, to May 24.

PACER isn't updating the Wazee docket properly, as seen in the screenshot posted yesterday. Have a look below to JUSTIA instead.

Wazee is another Class Action, but in the Court of Federal Claims with judge Sweeney.

Wazee is a case that, for the first time, challenges the ongoing NWS 2.0 (Common Equity Sweep), brought up by the attorney Hamish Hume in an amended complaint.

The attorney Hamish Hume is using this case to make up for the flaws in his case in the Lamberth court that would declare the Class Action illegal, commented yesterday: breach of Rule 23(b)(3) of the Federal Rules of Civil Procedures, that outlines the prerequisites for Class Actions:

A class action is superior to other available methods for fairly and efficiently adjudicating the controversy.

WHAT THE ATTY HAMISH FILED WAS A MOTION FOR EXTENSION OF TIME TO FILE THE APPEAL ON 5/24

— Conservatives against Trump (@CarlosVignote) March 29, 2024

The PACER Wazee docket isn't updating properly.

Afraid of filing the appeal that would derail the Class Action in the Lamberth court: it didn't end the controversy.#Fanniegate @TheJusticeDept https://t.co/Ej2mnyeRhF pic.twitter.com/YoFsJwTwxt