News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Wanna see who MAGNA is? Watch this- it explains it all (same IMO as Asher, Daniel James, KBM Worldwide, etc essentially (all "convertible debt, floorless or "toxic" cash-for-convertible-shares lenders)- all being utilized by Bioheart for "toxic" convertible debt financing deals, see most recent 10-Q and 10-K filings of BHRT)

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Pretty amazing story. This is the guy behind Magna and "what they do" and how they do it.

Remember, Bioheart just inked a $205K/$305K "note" with this guy and his penny lending firm Magna and then BHRT also filed a recent share registration statement with the SEC to also use a $3 million "line of credit" product that this Sason guy and his firm "Magna" invented/created- and from what I've read via some simple Google research, it's a notorious share price crusher to penny stocks that make use of it. (everything about Bioheart's recent "financing" deals making use of the guy "Sason" and his company "Magna" is all in BHRT's most recent SEC filings and also some PR's)

Fascinating IMO.

LOL Quote, "yes biilions saved-- suffering eliminated-- due to dr Lanza"

What?? When and where did these fantasies happen?

WHERE is this happening exactly and via what FDA or similar approved OCAT products/services being sold and utilized on human patients for "treatments" etc?

Is there even one source such as a major medical insurance carrier or major hospital HMO chain or similar that has documented these imaginary "$billions saved" because they are using some kind of imaginary "dr Lanza" product somehow?

I would love to read more about this in detail, exactly where and how these "billions saved" are happening.

Oh, and where exactly the "suffering eliminated" stuff is taking place too. I'd love to find out more about that myth too.

Quote, "Millions of patients need what the OCAT-Lanza-Team has accomplished. It's sort of like the "Cats Meow" OCAT"

What? What products does OCAT and this supposedly incredible "team" have for sale and available and FDA or Euro approved and proven safe with efficacy in humans and available now to use in patients today? Is there a list available? What physicians, clinics, hospitals are using these imaginary products and what major medical insurance companies are paying for them?

The common stock has lost about 98% of its value since trading public- that means most holders (other than self enriching insiders) probably have nothing but "beer and peanut" money left IMO. The insiders by contrast are living large and get to self-vote their own pay increases, never ending flow of free stock shares and options and have a near "miracle" like, seemingly uncanny ability to sell and dump their free shares into every near term "pop" or high on the stock. They're drinking the $500 a bottle stuff while the 98% loss "beer and peanuts" club is waiting for the next PR "carrot" to be dangled- 10 yrs of this.

My "beer and peanuts" 6 cents worth.

Thoughts? BMAK is back sitting on the Ask in their "parking place" with a 10K share block at .0097. Which tells me, IMO this is not going above 1 CENT as long as they're there.

Also, CDEL has showed up heavy as late, CDEL is also an MM often linked to dilution IMO via reading up on various stock boards on I-Hub and similar.

I see weakness and continued down pressure. The volume was practically nothing when BMAK pulled off the Ask for a few days, the instant they came back on the volume went way high yesterday- nearly all of it to the downside/sell-side and with the Bid getting pinned down close to .009

Stock is RED this AM with both the Bid and Ask getting pushed down as both BMAK and CDEL sit on the Ask. There is no up-trend even beginning yet, let alone established per any standard charting methods I'm aware of. The 50 DMA is above the 200 DMA (inverted) which means the stock is in technical weakness- it would need to break above the 200 DMA then on high volume and get the 50 DMA back above the 200 DMA and trending up before any reversal is in place IMO.

Bid/Ask both dropping this AM

0.0087 / 0.009 (10000 x 10000)

http://www.otcmarkets.com/stock/BHRT/quote

Continual use of common stock dilution and continual use of toxic, convertible debt financing deals (See any latest BHRT 10-Q/10-K SEC filings: Asher, Daniel James, Fourth Man, KBM Worldwide and Magna, etc aka floorless, toxic, death spiral, etc) has negative consequences to the common stock long term IMO. The SEC seems to have the same opinion in their write-up on "convertible debt":

http://www.sec.gov/answers/convertibles.htm

My .0087 cents

BS, "FWIW, I mention this as rumor seems to be building that one of the Major Pharma's has an interest in $OCAT's Blood Platelet technology to rebuild white blood cell count following strong chemo."

A "rumor"? And it "seems" to be "building"? Where's it "building" and who's "building" it?

I've not heard of any "rumor" of some "major Pharma" being interested in OCAT anything blah, blah, blah??

What proof is there of a "rumor"?? "rumors" are a dime a dozen to create and start and make up about anything? I heard a "rumor" Walmart is very interested in OCAT as Walmart opened a very big store down the road "somewhere" kinda near where OCAT headquarters is located- the rumor is that Walmart "might" maybe sell stem cell stuff at a big discount one day. That's what I heard- my friend told me I think.

Total nonsense that "big pharma" is blah blah OCAT IMO.

Quote: "Nasdaq sells buys, are watched by the SEC and electronic executed unlike the OTC where hand entries are used to execute as well as their Naked Shorting on Phantom Shares. Shorting on the Nasadq are "Covered Shorting" and accounted for. "

NOT true. The SEC does not sit and "watch trades"- that's not what they do. The first, or front line defense for "trade monitoring" is the DTC (Depository Trust Corp) a fairly secretive and extremely powerful- quasi govt entity that is essentially the "clearing house" of all public traded markets in the U.S.. They "monitor" and "close" and balance out all daily trading activity via all MM's and broker-dealers on all U.S. markets DAILY, processing BILLIONS if not a TRILLION trades or more. They can "freeze" or "chill" a stock of which they suspect trading problems, imbalances, manipulation, etc. They work in concert with the SEC but are not thee SEC. DTC monitors OTC and listed stock trades- it makes no difference.

Then there is FINRA which is also closely linked to the DTC and then the SEC and they also "monitor" and check daily trading and regulate broker-dealers and MM's etc. They would also be reporting to the SEC "suspicious" activity and have front-line defense capabilities to stop trading etc via reporting issues to the SEC. If one remembers, when OCAT botched their first try on the uplist in DEC 2014, they landed on the FINRA "daily list" for several days, maybe a week or more.

The SEC is the last people to get involved and only once a major investigation is launched or serious suspicious activity is suspected or insider trader or other serious level offenses are suspected and likely to be able to be proven. The SEC DOES NOT sit and "monitor" daily trades- that's not their role.

Also, SHORTING OF ALL TYPES, naked or otherwise, LIVES ON THE NASDAQ and it's a myth to say otherwise. Simply 100% not true. There is probably more professional level shorting and hedge funds that do nothing but short stocks (naked or covered) on the NASDAQ than anywhere else- and it's usually done via HFT (high frequency trading software auto-bots) making use of the various sub electronic networks that make up the Nasdaq and it's not "monitored" by the SEC- BILLIONS of trades a day popping off and often in nano seconds each.

That entire initial quoted statement is simply NOT TRUE or even close to accurate.

It's SIMPLE MATH. Got any links to PROVE it's NOT ACCURATE, or is that simply a bunch of pure BS CONJECTURE?

What, the insiders and Northstar LLC all decided to "sit this one out" and not vote? LOL !!

Quote, "Yeah right..."it shows that most common shareholders didn't even cast a ballot"

YES, that's exactly what the simple math show. Exactly correct.

The avg largest total votes cast was about 670 million votes. 500 million of those are Northstar LLC right off the top.

That's 670 - 500 = 170 million left. Another 40 million or so are Northstar LLC common shares. Now that's 170 - 40 = 130 million.

Then, from the last filed 10-K, PAGE 77, the insiders hold about another 84 MILLION shares outside of the Northstar LLC structure- meaning held as common shares.

That's now 130 million - say 80 million = 50 million.

THAT IS IT. Out of 600 MILLION plus common shares O/S, "maybe" 50 MILLION non insider votes were cast. THAT IS THE MATH. MATH DOESN'T LIE.

50 million / 600 million = .08 X 100 = 8% approx of common O/S shareholders cast a vote. MATH.

A) There's more than 585 million insider voting shares (add up all Northstar LLC preferred share votes, plus Northstar LLC non preferred share votes, plus all the shares held by the insiders outside of Northstar LLC- it's a whole lot more than 585 million)

b) When one subtracts out the insider votes from each total votes cast- it shows that most common shareholders didn't even cast a ballot (O/S share count - common shares held by insiders - the Northstar preferred share voting block count = not many non-insiders even cast a vote). The vast, vast majority of the total vote count in each case is the insider held voting block. Thus again, it MADE NO DIFFERENCE who voted other than the insiders- the die was cast with or without the public (non insider votes) being cast or not- they make no difference.

It makes no difference what the ratio of the "for" or "against" non insiders vote count was- they had no power to sway anything one way or another. It makes no difference- it's a moot point.

Sure it is- and it's MISSING about 75% of the rest of the story IMO. It's "selectively" chosen info- leaving out a tremendous amount of other key info that tells a much, much, much different, less "rosy" picture of the harsh realities of their dire financial situation.

This is the key two pages- the "statement of operations" and their "balance sheet" - one needs ALL the info on those pages to "see" the full picture and reality of their financial situation- and then toss in the "GOING CONCERN WARNING" to round it out.

Most recent filed 10-Q, PAGE 12:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

MUCH better "picture" IMO than some single slide in a power point stack- of a few carefully selected bullet points. MUCH better to me. I like to read the WHOLE STORY, the entire SEC filing and all the goodies contained therein.

My .009 cents worth

LOL quote, "Respectfully, as a shareholder of Bioheart since 2008, I am grateful you are not in his position. I voted for his raise, and would do so again. His salary, as well as Ms. Comella's, is not a concern of mine...outside entities that influence the stock price are."

Uh, the common share holders of this company don't have a controlling vote power over ANYTHING. Thus, unless an insider- "I voted for his raise" makes zero sense?

Northstar LLC alone controls over 500 MILLION share votes (20 million preferred shares w/ 25:1 voting rights). Add in the other insider which per the last filed 10-Q hold over 82 MILLION more shares (outside their Northstar holdings) and then Northstar holds another 40 million or something shares of common (I'd need to check latest filings).

Thus it's folly to believe that the common public shareholders "vote for" or have a say in ANYTHING related to this company. It's simply not true. Insiders hold 100% majority voting power and IMO have set that up and maintain it that way "by design" as they continually issue themselves more shares or increase the Northstar LLC voting rights (from 20:1 to 25:1) to insure that as the ever increasing, non-stop share dilution occurs they never lose their majority vote and can never be out-voted on anything.

As an example- just read the wording from a fairly recent SEC filing involving a "proxy" issue to increase the available shares from 950 MILLION to 2 BILLION shares. They stated right in the document- we voted ourselves, we passed it ourselves and your (the public shareholder's) you vote is NOT NEEDED nor is it even requested or wanted. That is the reality.

http://www.sec.gov/Archives/edgar/data/1388319/000114544314000633/d31331.htm

"Ratification of the increase of the authorized shares of capital stock of the Company from nine hundred and fifty million (950,000,000) shares of common stock and twenty million (20,000,000) shares of preferred stock, both $.001 par value respectively, to two billion (2,000,000,000) shares of shares of common stock and twenty million (20,000,000) shares of preferred stock, both $.001 par value respectively, effective as of the filing of an amendment to the Company's Articles of Incorporation with the Florida Secretary of State."

And did they need any public shareholder "vote"???

PAGE 3:

"The elimination of the need for a meeting of stockholders to approve this action is made possible by Florida Statutes which provides that the written consent of the holders of outstanding shares of voting capital stock, having not less than the minimum number of votes which would be necessary to authorize or take such action at a meeting at which all shares entitled to vote thereon were present and voted, may be substituted for such a meeting. In order to eliminate the costs involved in holding a special meeting of our stockholders, our Board of Directors voted to utilize the written consent of the holders of a majority in interest of our voting securities. This Information Statement is circulated to advise the shareholders of action already approved by written consent of the shareholders who collectively hold a majority of the voting power of our capital stock."

And PAGE 2:

"This notice and information statement (the “Information Statement”) will be mailed on or about April 17, 2014 to the stockholders of record, as of April 16, 2014, to shareholders of Bioheart, Inc., a Florida corporation (the “Company”) pursuant to: Section 14(c) of the Exchange Act of 1934, as amended. This Information Statement is circulated to advise the shareholders of action already approved and taken without a meeting by written consent of the holders of a majority of the Company’s outstanding voting common and outstanding voting preferred stock, specifically, management and one non-solicited shareholder, representing 597,553,092 voting capital shares (including 20,000,000 preferred shares that have 25 for 1 voting rights or 500,000,000 voting shares) (62% of the Company’s issued and outstanding voting stock as of the Record Date). Pursuant to Rule 14c-2 under the Securities Exchange Act of 1934, as amended, the corporate action described in this Notice can be taken no sooner than 20 calendar days after the accompanying Information Statement is first sent or given to the Company’s stockholders. Since the accompanying Information Statement is first being sent or given to security holders on April 28, 2014 to the corporate action described therein may be effective on or after May 19, 2014.

Please review the Information Statement included with this Notice for a more complete description of this matter. This Information Statement is being sent to you for informational purposes only.

WE ARE NOT ASKING YOU FOR A PROXY AND YOU ARE REQUESTED NOT

TO SEND US A PROXY."

LOL, no public shareholder (non insider, no Northstar LLC, non "one other" majority holder named above in that document) VOTED FOR ANY PAY RAISE. They can vote and pass any pay raise they want and someones vote supposedly having an imaginary "approval" of it here is comical IMO. They don't need those votes to pass anything- they do it all one their own. Just the way it is and they set it up they way on purpose IMO. Vote away- it makes no difference IMO.

The 10-K will also show things like LOSS FROM OPERATIONS, "going concern" warnings if appropriate, poor cash on-hand liquidity issues, debt and very importantly- MASSIVE continued on-going dilution of the common stock shares (PAGE 1 of the 10-K will give the most current O/S share count, further down in the 10-K will be the "fully diluted" share count), etc.

I would never IMO refer to a single "power point" slide to try and gauge anything really relevant about the true health or lack of health about a pubic traded stock company. The 10-K filing will probably be 60 plus pages in length- and IMO needs to be read cover to cover to fully understand the true condition of the company. The first 10 pages or so - will present the company "financials" which are the fastest way to get a snap-shot of the true financial condition of the company (balance sheet, statement of operations, statement of cash flows, etc).

Here are some key points/pages from the last filed 10-Q, prior qtr showing many issues with the company's lack of financial health- despite top line "revenues".

Those IMO are some of the things one will find in a 10-K and should look for.

Also, look for statements like this from the Sr. Mgt and auditors: Last 10-Q, PAGE 12:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time.

The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern."

Things like that- that's what's in a 10-K. Again, probably 50 to 60 plus pages of reading- and IMO should be read cover to cover.

Good luck to all

"It's happening"??

What exactly is happening? The Bid is buried below .009 at .0088 and the stock is getting crushed again for the most part today?

It's only trading in a ultra wide spread Bid/Ask with the Bid being pinned to the mat.

BMAK has 10K shares parked on the Ask at .0098 which means it ain't going above that today- they have it in a head lock.

So what exactly is "it" that's "happening"? Just another day mostly in the RED on very high volume- and a Bid going nowhere?

0.0088 / 0.0097 (165000 x 114025)

http://www.otcmarkets.com/stock/BHRT/quote

BMAK is back- just slid into position, 10K share block at .0098, one level off 1st position on the Ask, they're normal "parking place"

Right as they come down the Level II to park their 10K share block- the Bid side drops and shares move down. (and NO, the Bid has not been "continually moving up"? Where is that happening? It's been stuck at about .0089, .009 max for going on 2 weeks with drops to the .008 range several time. Aka lower lows and lower highs continually, "ratcheting" down in stair-steps)

Looks like .0098 is it now then for the day then? Looks like maybe .01 or so has been set as the "cap" at least for now by MM BMAK . This has been the pattern for months- a few "breathing" days on very low volume and then BMAK comes back.

Notice, the volume took a large spike this AM to over 600K shares (it barely traded anything yesterday) and as soon as that volume came in, is when BMAK appears.

The Ask just got stacked much heavier over the Bid also.

22K shares left on the Bid (about $200 bucks worth) and next level is .0085 again it looks like for now.

0.0093 / 0.0096 (22000 x 309000)

Look like IMO that the dilution MM's are still sitting hard on it and as present as ever.

http://www.otcmarkets.com/stock/BHRT/quote

1) There is ZERO proof that they have "cured blindness" or are even "about to cure blindness"? HAS NOT HAPPENED. They're barely out of the starting gate in an FDA approval process in which there's about 1000 ways to get tripped up and fail along the way- and that's after 15 yrs of "working" on this. 18 people in a micro-trial is nothing. They're just now entering the "tough part" the much larger phase II trials with placebo arms and all- and that's where most clinical trials get tripped up and fail and wash out. They're on about the 5 yrd line right now and have a 95 yard drive left to try and make the goal line- and it's against the toughest opponent one will ever face, the FDA team.

Year 2020 for a "maybe" on an FDA approval per their own insider's comments. Well documented fact.

2) Those "negative goggles" or whatever they're called- are called REALITY GLASSES that allow people to see the REAL 98% LOSSES to the common shares to date and the REAL SEC violations still being paid off out of current shareholder dilution and the REAL dilution of a stock that went to 3 BILLION plus shares while hitting a price of a literal 5 CENTS.

This isn't some fairy tale story coming true yet- they're running on fumes and dilution at this point and have yet to declare how they're going to come even remotely close to funding the plans they have on the table in front of them at this immediate point in time- just getting their needed "trials" started, let alone even completed.

I wear the REALITY GOGGLES and don't own a pair of "negative goggles" or whatever they're called?

LOL, quote, "10-K and CC on time"

Wow, so now they get extra credit or something for just making their duly required SEC FILINGS "ON TIME"??

That now counts as like an "accomplishment" or something?

Every public traded company is required to file their 10-K's and 10-Q's ON TIME when due? What's the big deal about that happening?

"revenues" haven't and didn't "change" anything in BHRT's situation so far as is being claimed numerous times?? Not IMO. Where is proof of that?

WHY despite the ole "revenues" blah, blah, blah claims is the stock sitting at and hitting near its ALL TIME RECORD LOWS? How does that "work"? Why did they tap toxic, convertible debt financing deals as recent as Oct 2014 for pittance amounts of cash like $25K and $38K (see last filed 10-Q the Daniel James Management toxic note and the KBM Worldwide toxic note- horrible terms and mega steep share discounts on floorless, 100% toxic dilutive note financing deals. Then Magna was also added on a "note" to keep cash coming in) Why? When this imaginary scenario supposedly exists where "revenue" is now supposedly "funding" their operations and blah, blah which is NOT happening?

Stock just went RED today also. Bid sinking to .0091 (now .0092) The Bid hasn't moved up at all, despite the volume falling off to near nothing- there's little or no buying interest in the stock at this point. Crossing the 50 DMA is not the technical indicator that matters- it's the 200 DMA that matters, as the 50 DMA and 200 DMA are inverted right now. It would need to break above approx. .02 on very high vol to even begin to be in a technical reversal. It's traded a big $120 bucks worth or so, so far today (now just bumped up a bit to maybe $7,500 bucks but Bid didn't move- trading the spread again) . It traded maybe $1,200 bucks worth total, something like that for an entire trading day yesterday. There's no "big buying" or "accumulation" going on or whatever?

What "changed" supposedly? They didn't generate any cash via "revenues" that could be used to pay down debt, fund a trial, or LOL be used to "buy back shares"?? They finished the last quarter, despite the ole "top line" ole "revenues" with a grand total of $46K CASH left to their name (bording on insolvency for all intents and purposes and their own 10-Q filed GOING CONCERN WARNING in that same filing said so). That's despite cutting R&D spending to essentially nothing- barely $3K a month and that is NOT "funding any trials" of any phase (I, II, or III) that's for sure IMO. It would be impossible to fund trials on that pittance. So despite not funding any trials they still took a LARGER LOSS FROM OPERATIONS in the first 9 months so far of 2014, larger than in 2013 and again, finished the last qtr with a whopping $46K bucks left on-hand.

The only "Debt reduction" was NOT done via using any internally generated cash? It was done by 1) Convincing one old, old creditor to allow them to discharge, aka "write off" a debt they never paid back (Willian Beaumont Hospital, whatever the exact name was) and then b) Via allowing some ole Northstar LLC insiders to do "debt to equity swaps". That is IT when it comes to "debt reductions". They, BHRT, never generated any cash internally and then used it to "pay down debt" or whatever else was claimed in some post? DID NOT HAPPEN. Even in the last 10-Q, the most recent- they, BHRT were just living off of dilution financing and also paying common bills via issuing millions of shares of dilutive common stock for common items like "accounts payable" and similar- as they HAD NO CASH to pay those bills, despite the ole "revenues" blah, blah, blah.

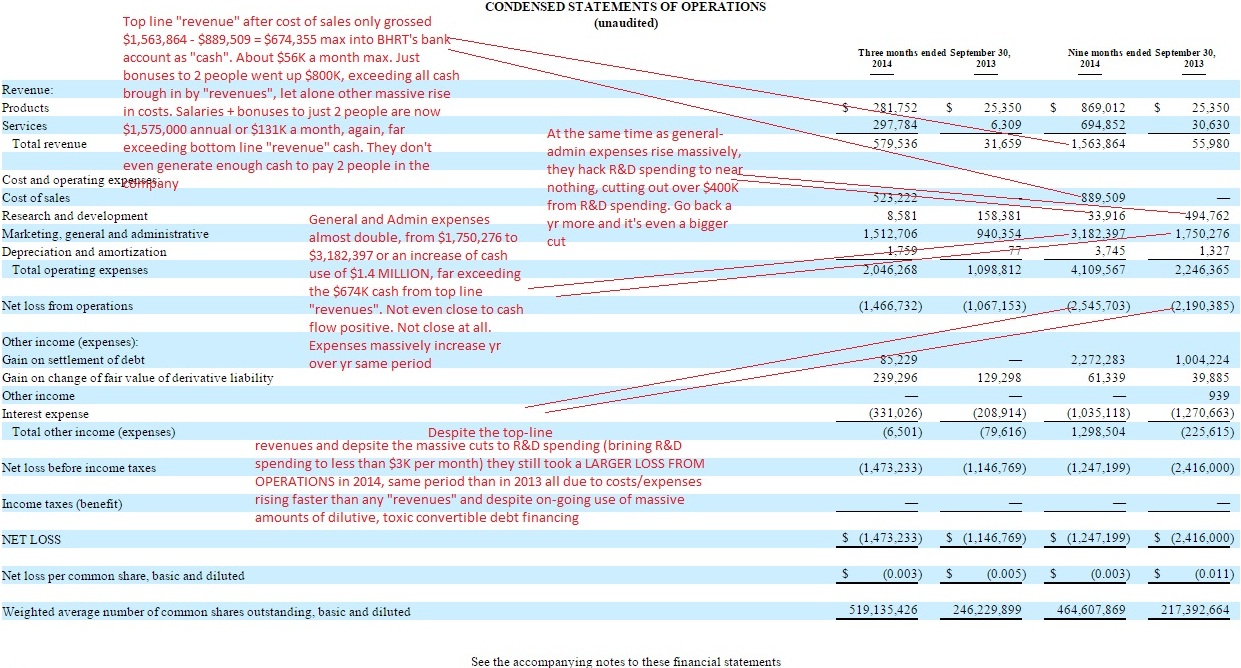

From the last filed 10-Q, showing the massive rise in EXPENSES off-setting any top line "revenues" and thus making their LOSS FROM OPERATIONS larger this yr so far than last yr:

There was a greater LOSS from operations because EXPENSES EXPLODED UPWARD and also the gross margin on top-line revenue that past qtr was a dismal approx. 10%. They made almost nothing to bank on the "revenues" - it was eaten up in cost of sales.

From the same 10-Q, most recently filed, PAGE 12:

"NOTE 2 — GOING CONCERN MATTERS

The accompanying unaudited condensed financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. As shown in the accompanying unaudited condensed financial statements, during nine months ended September 30, 2014, the Company incurred an operating loss of $1,247,199 and used $747,184 in cash for operating activities. As of September 30, 2014, the Company had a working capital deficit (current liabilities in excess of current assets) of approximately $10.0 million. These factors among others may indicate that the Company will be unable to continue as a going concern for a reasonable period of time. The Company’s existence is dependent upon management’s ability to develop profitable operations and to obtain additional funding sources. There can be no assurance that the Company’s financing efforts will result in profitable operations or the resolution of the Company’s liquidity problems. The accompanying statements do not include any adjustments that might result should the Company be unable to continue as a going concern.

"

"liquidity problems" is the nice way IMO to say teetering on insolvency (lacking enough timely cash being on-hand to pay your bills as they come due, aka often leading to BK). Nothing "changed" in their dire financial condition IMO because of top-line "revenues" as their expenses grew faster and ate of the ole "revenues".

Same 10-Q filing, most recent PAGE 26 (TOXIC financing continues to be used for survival- NOT "revenues" generating internal cash to fund any trials or "buy back shares" LOL !"

"KBM Worldwide

On October 6, 2014, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc., for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).

The Note bears interest at the rate of 8% per annum. All interest and principal must be repaid on July 8, 2015,. The Note is convertible into common stock, at holder’s option, at a 45% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts.

Daniel James Management

On October 3, 2014, the Company entered into a Securities Purchase Agreement with Daniel James Management, Inc., for the sale of a 9.5% convertible note in the principal amount of $25,000 (the “Note”).

The Note bears interest at the rate of 9.5% per annum. All interest and principal must be repaid on October 2, 2015. The Note is convertible into common stock, at holder’s option, at a 47% discount to the lowest daily trading price of the common stock during the 10 trading day period prior to conversion. In the event the Company prepays the Note in full, the Company is required to pay off all principal and accrued interest at 150%, and any other amounts."

So a company is going to use TOXIC, floorless, convertible debt financing or a Magna dilutive "credit line" to borrow money to then "buy back" their own shares - aka using more dilution to buy-back the very dilution shares they just issued? What? That's the equivalent of using credit card "A" to max it out to pay down credit card "B" for a while? That never accomplishes anything?

Same 10-Q filing, the latest filed, showing common stock being issued out in the millions and millions of shares to pay what would be "common" business bills and obligations as the company HAD NO CASH of their own to pay those bills when due- and that's despite cutting over $400K out of the R&D budget and then finishing that last qtr with $46K total dollars cash left in their bank account:

PAGE 27:

"Subsequent issuances

On October 3, 2014, the Company issued 514,886 shares of its common stock as payment of $70,521 interest on its Northstar (related party) debt.

In October 2014, the Company issued 1,818,182 shares of its common stock in settlement of $20,000 of convertible debt.

In October 2014, the Company issued 1,293,103 shares of its common stock in settlement of $15,000 of convertible debt.

In October 2014, the Company issued 2,260,764 shares of its common stock in settlement of $18,000 of convertible debt and accrued interest of $2,120.

In October 2014, the Company issued 552,846 shares of its common stock in settlement of $5,500 of convertible debt and accrued interest of $1,300.

In October 2014, the Company issued an aggregate 2,773,549 shares of common stock for consulting services.

In October 2014, the Company issued 538,875 shares of common stock in settlement of accounts payable."

What? All that "revenue" blah, blah and they're paying their bills by issuing out common stock NOT USING CASH as any business would normally do? Why? Why would that be?

Top line "revenues" haven't "changed" a thing in their dire financial condition IMO or the fact they're basically running/existing as a share dilution machine. None. Oh, and they issued out $800K in "cash" bonuses to just 2 of the "4 full time employees" at the company (see latest 10-Q PAGE 23, $500K cash bonus to Tomas and $300K cash bonus owed to Comells, now being carried as debt "notes" owed w/ interest) thus they issued an IOU for those bonuses, earning interest- as they didn't have the CASH ON HAND despite the ole "revenues". Those bonuses will get paid first IMO before any cash goes to any ole "trials" or whatever. Same old, same old the way I see it.

My 2 cents.

Quote, "If we're taking bets I'd say $2.47 million."

Sounds like it would take insider trading or similar info to get that kind of accuracy? Most company's can't even predict their own numbers to that kind of accuracy until they actually "close the books" via final numbers.

How would it be possible to know sales to within 2 numbers after the decimal? Not $2.46 million and not $2.48 million - but EXACTLY $2,470,000 dollars? Based on what criteria unless it's coming from the inside IMO?

Again, unless the company has already rolled up their own final numbers for the qtr- I'd be surprised if they can even give that kind of accuracy until all accounts receivables are booked, any pending payments are deemed to be "booked as revenue" or not (one has to read the company SEC filing details on specifics as to when they "book" certain revenues- at time of sale, or when payment arrives, or other various methods)

I don't see how knowing that number would be remotely possible unless it's already known inside the company IMO.

Bigger question IMO- who cares about "revenues"? Are expenses still outgrowing revenues and will the company take a bigger loss from operations this year over 2013, as they have so far up through the Sept 2014 10-Q quarterly filing. "revenues" really make no difference if the cost of sales and then higher SG&A expenses have eaten it all up as happened essentially so far for the first 9 months of the year- despite R&D being cut by a huge $400K plus. The operational loss through Sept 30th was larger yr over yr for 2014 than in 2013.

How much massive dilution has occurred - new O/S share count. And how much more toxic debt financing has been utilized if any and has the Magna credit-line been tapped yet and for how much and are common bills still being paid by issuing out 10's of millions of shares of common, dilution stock as is the norm per all most recent 10-Q and 10-K filings (stock issued for stuff like accounts payable, "consulting" or "related party debt" or "services rendered" etc). Those will be the first things I'll be looking for in the 10-K. They have a much bigger impact IMO than just top line "revenue". Last qtr, the cost of sales ate up most of the revenue- the gross margin was like only 10%.

My 2 cents. I don't see how one "guesses" 2 places after a decimal point- seems impossible to me w/o some "help", like maybe an inside line or some data given ahead of time?

I agree. I'm holding in the pattern also. I just got a feeling there's a lower entry point available.

I'd rather miss 10% to the upside than get caught being able to enter 10% or 20% lower or more (if they dilute large IMO) later. It's harder to gain it back on the way up. 50% down means one needs a double (100% gain) to get back to break even.

Holding pattern for me, just orbiting the race track pattern, waiting for the signal to enter the break- can refuel here and wait it out as needed. Keeping the powder dry.

Buy when the blood it running in the streets- like the big boys. Like Gastro has been commenting- the entire market is getting pounded, so probably no hurry to jump on anything here at this point. Let the dust settle on the potential rise in interest rates (which I doubt much will happen, 1/4 basis point if the even do it), Euro/Greece stuff, oil prices, dollar strength and all the other gremlins that have the markets barfing up all over.

Kinda unfortunate timing IMO for little ole OCAT to make it on the Nasdaq right as the raging bull market starts to burp n hiccup a bit. End of 2014 would of been much better- but OCAT getting financing will trump all other cards IMO anyway- either to the upside (good financing deal) or to the downside (weak, highly dilutive financing) - but I'm pretty certain they know with 100% surety they gotta make a visit to the "big money man" here soon- or show their hand and cards as to how they pay for trials going forward, else, folks are gonna go to the sidelines IMO.

We'll see.

Over 1 hour, $100 bucks worth traded

It's gone ill-liquid IMO, practically dormant it seems.

No buyers willing to step in here even at sub once CENT.

Can't move a stock much when there is no volume, no buyer's willing to come to the table.

$100 bucks traded in an hour? That's pretty impressive.

Bid/Ask is still stacked totally to the sell side- so it would need a lot of buying activity to get it moving even slightly in the other direction IMO.

0.0091 / 0.0099 (161000 x 962320)

They even dropped the Bid now a tad lower to .0091 and no takers on the Ask at .0099 in over an hour.

Like watching paint dry.

(OK, after 1.5 hours into trading day they put on a whopping total 28K shares traded now- approx $275 big ones worth. The paint just dried a micro tad, wow)

Trading on the huge, 10% plus spread again.

Bid hasn't budged at all and over 1 million shares still parked on the Ask for sale around .01, all of which would need to get sucked up before this moves at all. Yesterday, when anything got bought off the Ask- they just piled on some more to the sell side, keeping it stacked with 1 million plus shares at .01 or .0099

Volume is a whopping 10K shares this AM to move it "up" 10% plus. (that like $100 bucks worth, if even that. Wow !!)

0.0091 / 0.0099 (160000 x 880320)

http://www.otcmarkets.com/stock/BHRT/quote

So again today- the volume is anemic and the Bid isn't moving up and it's stacked heavy to the Ask, sell-side.

Not much going on here IMO. Barely any volume and no real buying pressure at all- just a big spread and flat-lining. 10K shares trade ($100 bucks worth) and then it sits.

$6.07, Wow ! Solid RED on higher than avg vol already for this early in trading day.

Looks like a trip into the $5's again may be in the on-deck circle here.

Wow, the ole magic of the Nasdaq "uplist" just hasn't panned out much yet it seems? And the ole "article" has been out there long enough for any "big money investors" to have read it cover to cover at least a few times by now.

This stock apparently has bigger issues putting the down pressure on it still? Not sure what- just dilution and overhang? Or the OTC transfer perhaps takes more than a name change and a new logo before the "big money" buys into the new "story" and make over and all?

They pulled the offer but have yet to say how they're gonna fund this thing going forward, especially a large, expensive phase II trial. It seems like until that gets answered (big dilution or net, etc) - then this is just floating around with no anchor or hooks to grab into yet IMO.

Too much uncertainty and the markets hate uncertainty.

"Anyone still buying this junk?" ??

Well by the looks and reality of any chart and the present SUB ONE CENT price- not much net buying going on IMO. It hit near its all, all time low in 2015 already, dipping to .007 (just missing the .0063 low of Dec 2013), yes 7/10ths of ONCE CENT.

And is now languishing for months as a sub ONE CENT stock with a market cap barely holding $5 million with current debts of more than $10 million.

So I'd say no, not any evidence of much net buying at all. The stock has been in a sustained, 9 month plus, unbroken downtrend with a few "up" blips along the way but a trend that is steady down and unbroken and still no sign of any reversal or even a slight uptrend when I read the chart.

And all that is despite numerous amounts of "PR" and "big news" and "presentation slide shows" and a "conference call" and all the rest- and nothing has remotely turned it to an uptrend yet.

My 2 cents.

Thanks farview,

I think that's who/what I was thinking of when trying to remember who/what else might still be holding some large blocks of potential share "overhang" out there.

That's the name I was looking for I think- the "Aarsonson, et. al." potential shares. As you stated, maybe fully liquidated but does anyone know, and/or still holding millions and are they sellers, longs, "working" the stock for their own advantage, etc.

Yep, I think that was the one I'd read about. So Lincoln of course. Then this Aaronson in the millions of shares - so those two combined, who knows? Could be all kinds of down pressure or potential dinking around with the shares in large blocks for self "motives" perhaps, etc

LOL, "Champagne and yachts"??

It's barely budged up to ONE CENT today on lower than avg volume so far- no real big buying pressure has stepped in here at all today that I can see? It's been all stacked to the sell side and is even "flat-lining" (trading slow and ill-liquid, going 1/2 hour or more w/o a single share trading many times today).

The Bid/Ask has been stacked to the Ask, sell side all day w/ shares piling on to the Ask each time any were bought. It's still sitting with about a million shares stacked on the Ask at .01 as it was since the AM and only 1/2 hour is left in the trading day.

The Bid/Ask both just dropped with 1/2 hour left to go today and it hasn't traded a share in about 30 minutes (oops, just posted a trade now after about 30 plus minutes now and it's on the lowered Ask, .0093)

0.009 / 0.0093 (388156 x 120000)

http://www.otcmarkets.com/stock/BHRT/quote

Big drop right there on both Bid/Ask meaning no strength or conviction or follow-through buying that I can see today?

Yachts or used Yugos?

elysse, I just have a gut guess that Lincoln is constantly unloading. Also, they still have some other share "overhang" (can't remember the names- related to the legal stuff and one other old deal I think?) and perhaps they keep unloading too?

Every blip into any strength and someone steps right back down on it- today is pretty decent volume to the downside, so I don't think this is just Joe Q. Public selling in here, although it could be buyers over $8 just throwing in the towel, but I don't think that accounts for this much sell side volume.

Someone has this thing pinned in a range and has for a long, long time - which IMO is most often then only 2 possibilities usually:

1) The dilutive finance house these companies get involved with or

2) Pro short desks, aka hedge funds and similar

I think it's too early on the Nasdaq for the pro shorts to be all over this yet (but I'd not be surprised if it's not already on their radars- they have auto-bots that sniff out weak stocks and then they plaster um via pro, often automated shorting algo's- welcome to the "new" automated Wall Street) but that leaves Lincoln most likely IMO.

Dilution, good ole dilution might be all this is. Ole dilution never fails wherever it goes in my experience. The greatest stock price killer probably ever invented, even more damaging than shorts piling on. A near, never ending flow of shares that just can't be vacuumed up fast enough being sold by people who make money via a dilution formula that for all intents and purposes makes them the "house" in Vegas- meaning they never lose and always profit when they sell. Big bucks in dilution lending- huge bucks.

My 2 cents

Can't hold that Bid up at all it seems and the Ask just keeps getting stacked deep with sell shares.

Bid moved up for a blip to .0099, then CDEL got back on it again w/ the same 40K block plastering it back to .0093

The Ask went to 1.7 million with only 10K shares on the Bid, looked like they chewed up the Ask a bit down to only 800K left or so, then it just got re-stacked back to 1.5 million on the Ask. Someone looks to be selling into this strength today- trying to get around .01 or .0099 from any takers. They keep loading that Ask up to over 1 million shares each time.

Still just trading on the spread then it looks like- no real strong buying pressure or ability to move the Bid up and sustain it IMO.

0.0093 / 0.01 (40000 x 1572478)

http://www.otcmarkets.com/stock/BHRT/quote

Quite a bit of the buys are popping off under the Ask, moving it back to .0099 each time. Not strong buying pressure. Volumes picked up a tad - wait and see here where this goes.

Looks like it's CDEL "working" both sides today- which is what happened for a good part of Friday before BMAK slid back down in the 2nd half of the day, parking a 10K share block on the Ask. Will be very interesting today IMO to see if BMAK stays clear of one level off the Ask or off the Ask all together, at least backed way out to .05 like now, which means they're really not "making a market" this AM on the stock.

Interesting.

BMAK did the exact same thing on Friday, moved off to .05, only to slide right back down with their daily 10K share block by mid-day.

I haven't seen any "loading"- as the higher volume days have all closed RED that I'm aware of? Friday being a perfect example. Closing red means net selling- not accumulation or "loading" by anyone, it's "un-loading" which is the opposite IMO.

Again, this so far is a lower volume "blip-up" as has happened several times in the past few months (sell/dump days have been 3 million shares on the low side and closer to 4/5 million shares on most "avg" days now). A few moments in time does not maketh a trend. Avg daily vol is now up at 2.5 million shares a day- it'd need to break that and much more in the green for many days to really start setting a trend. 1.3 million on the Ask, sell side all need to go first and Bid move up before it goes anywhere that I can see.

Way to early to "call" a trend here IMO. Friday AM looked "better" too- only to get bulldozed by mid-day with an explosion of volume to the red side and then ole BMAK, the 10K share block moved right back to sitting on the Ask the rest of the afternoon, never getting "filled", never disappearing- just sitting there as the "daily cap" as I now see it.

Way too early here IMO and not much volume to any upside yet. And a key thing- the Bid barely moves lately, if at all. It's stuck- as it's been for months. The Bid would need to move up rapidly to match the Ask on any real strong "up-trend" or heavy buying day. It's parked at .0093 or .0094, the Bid right now, which means to me the MM's just have it trading on a wide open spread again (10% spread minimum), not any real strength. The MM's are just fishing for some buyers to take a bite at that 10% spread IMO. It's done this too many times to count just since start of 2015- but never set a trend yet, not even close.

My 2 cents.

Journal articles, when not backed by a mountain of cash- which is what clinical trials cost, don't get "buy recommendations" from my past experience.

CASH IS KING on Wall Street and OCAT has not attracted any "big cash" infusions at this point- the "article" didn't amount to much IMO.

Also, it's a very, very tiny 18 person phase I. Just barely out of the starting gate for a medical/clinical trials based company at this point. This would normally not even be public traded most likely at this point- it would be backed by big name, high quality venture firm money (Menlo park boys or even the MA venture "corridor" money in their own backyard, or similar) and then they'd take it IPO in the phase II usually and this thing would be sitting with like $60 to $100 million cash at that point, totally debt free, with a relatively low O/S share count and so forth.

That's how it's usually done if backed by "big" and "smart" money venture firms. OCAT right now is out hunting for cash and needs a mountain of it to move forward in any serious way- they're a 1000 miles from the finish line and need a lot of bucks to have even a shot a making the journey.

My 2 cents.

Quote: "Looks like the 50MA will be touching the current price soon. This could indicate a 50MA breakout soon. I will load, thank you."

Problem is, the 200 DMA and 50 DMA are inverted right now- the 200 DMA is above the 50, which is a sign of extreme technical weakness. Also, any slight "up" days like right now (the day isn't over) the volume has been low/weak, the sell days having 4 to 5X the volume or more of any of these little "blip" ups when it's trading on the spread. The Bid is just slightly "up" this AM, but barely moved above the red-line from Friday. Nothing much happening here- no volume, no big buying interest as of yet.

This would need to break above the 200 DMA avg right now, not the 50 DMA to start any kind of actual up-trend or reversal. It's not even close yet. The 200 DMA is clear up at .019 and it's gotta get there and get the 200 DMA back under the 50 DMA if a "technical chart" pattern approach wants to be used- as a buy signal or technical indicator of any start of a solid up-trend.

It's just breathing a bit today IMO as BMAK has pulled way off the Ask, same as they did end of last week, only to slide back on it by mid-day Friday, sending it red. Also, CDEL (another pretty notorious dilution MM) is now sitting, "bracketed" on both the Bid/Ask this AM. They also appeared heavy end of last week when BMAK had moved way off the Ask w/ their daily 10K share block. We'll see- but I don't think BMAK will be gone for good at this point- they did this several times over the past month alone, the "breathing day" I call it. Like maybe Magna, or Asher or whoever it is that BMAK moves shares for is perhaps sliding off the Ask or done converting perhaps for a few days.

There's 1.3 million plus shares on the Ask at 1 CENT they'd have to work through before this goes anywhere. That same block of 1 million plus was parked there all of Friday last week too.

Heavily tilted towards the Ask, sell-side but no big volume coming in to buy it up:

0.0093 / 0.01 (40000 x 1385578)

http://www.otcmarkets.com/stock/BHRT/quote

Don't see any sign of a reversal or uptrend yet IMO. Volume bars along bottom of the chart are the most telling to me. They're very high on the sell/dump days and much lower vol on any "up" blips so far. Been this way for pretty much all of 2015 so far now when I look at that chart.

My 2 cents

Quote: "And what would they base a "Buy" recommendation on???"

My thoughts EXACTLY. "big firms" who give "buy recommendations" (Citi, UBS, Goldman, whoever) don't usually give big ole "buy recommendations" on cash poor, no product, no sales, no "big financing" deal(s), living off of Lincoln dilution "credit line" based companies, not that I'm aware of?

Especially (6 CENT pre R/S split) companies just a few weeks off the OTC who's stock is going nowhere as of right now?

Like the question above states- "buy recommendation" based on what criteria exactly? The common stock has lost about 98% of its value too date- and is sitting where it was at least 3 or 4 yrs ago, unchanged. What's the "buy" part all about exactly?

They got a tiny phase I under their belt right now, very little cash, no phase II even started yet and about 5 yrs minimum (per their Sr Mgt's own words) 5 yrs to a "possible" product and FDA approval and nowhere near enough cash via their present dilution funding line to carry them much past 1 yr, if even that, w/o even providing funding for a large, FDA quality phase 2 trial.

I don't think the big "analyst houses" are exactly all over this one just yet IMO.

Quote, "So if BHRT went bk these people we are talking about would be 1st in line to get money repaid before commons?"

IMO, 100% absolutely of course. Always that way for holders of "loans/debt" versus equity holders. Always.

Read the Northstar LLC "lien" agreement- they hold rights to everything this company has for all intents and purposes and are a "secret" structured LLC, meaning no one in the public is even fully certain who all the members of the LLC are. It says so right in the lawsuit filing- that part of their discovery process is to figure out who else "might" be part of Northstar LLC as the SEC filings of BRHT always say something like, "Made up of certain BOD members and "other" shareholders and/or guarantors" (some wording similar to that - see SEC filings) aka the mystery guarantors IMO. As far as I know- Bioheart has never stated who they all are- who ALL the "members" are that have a stake or ownership rights to Northstar LLC.

But yes, read the balance sheet- there's $10 million in current "debts" and at least $2 million or more of that is for example "accounts payable" - those are like vendors, people doing recent business with the company, etc. They would ALWAYS make a first claim to any monies in a BK proceeding and as "creditors" would always be ahead of equity (stock) shareholders.

Bioheart has no assets for all intents and purposes (about $250K worth as of last SEC filings) so it really makes no difference anyways- they have no cash left to pay anyone in the event of a default and nothing to sell or liquidate to generate even a fraction of what it would take to make even a tiny dent in paying anyone back - they don't really own anything (no real estate buildings, no plant and equipment, nothing really of value- just look at their assets, about $250K listed). There'd be nobody getting paid back IMO if this goes BK, there's nothing there to pay anyone with. They're in debt up to their eyebrows, cash poor and relying on finance houses like Magna who I'd guess get first dibs probably along with "accounts payable" and especially Northstar LLC per the "lien" security agreement.

Look at BK filings for even mega corps (not sub ONE CENT penny stocks)- the bond holders usually even only end up with pennies on the dollar- as the companies were upside down in debt, which is how they ended up BK in the first place. Equity holders (aka common stock) never get anything- the stock literally goes worthless in nearly all cases. "If" the company even manages to emerge years later from BK- they typically issue new stock and the old stock is rendered worthless- often even pensions and other obligations get wiped out (airlines had it happen many times: Delta, Continental, Northwest etc resulting in pilot union lawsuits to try and reclaim their pensions owed - I know a good pilot friend who was part of a big suit when his airline went BK, Captains w/ 25 yrs suddenly watching their pensions go up in smoke, sorry no money left to pay you). MCI/Worldcom, Enron, Lehman, Nortel, Tyco, Delphi, recently Radio Shack, GM, Chrysler, practically every airline that ever was- what did the common shareholders get left for table scraps in the end? Usually nothing in most every case. Bondholders and creditors first- and they usually settle for pennies on the dollar- a fraction of the face value of the debts they're owed, always.

Just read the SEC filings:

Examples:

Last filed 10-K, PAGE 25:

We will need to secure additional financing in 2014 in order to continue to finance our operations. If we are unable to secure additional financing on acceptable terms, or at all, we may be forced to curtail or cease our operations.

As of March 24, 2014, we had cash and cash equivalents of approximately $211,632.80 and a working capital deficit of approximately $13.4 million. As such, our existing cash resources are insufficient to finance even our immediate operations. Accordingly, we will need to secure additional sources of capital to develop our business and product candidates as planned. We are seeking substantial additional financing through public and/or private financing, which may include equity and/or debt financings, research grants and through other arrangements, including collaborative arrangements. As part of such efforts, we may seek loans from certain of our executive officers, directors and/or current shareholders. We may also seek to satisfy some of our obligations to the guarantors of our loan with Seaside National Bank & Trust, or the Guarantors, through the issuance of various forms of securities or debt on negotiated terms. However, financing and/or alternative arrangements with the Guarantors may not be available when we need it, or may not be available on acceptable terms.

If we are unable to secure additional financing in the near term, we may be forced to:

· curtail or abandon our existing business plan;

· reduce our headcount;

· default on our debt obligations;

· file for bankruptcy;

· seek to sell some or all of our assets; and/or

· cease our operations.

If we are forced to take any of these steps, any investment in our common stock may be worthless.

"

Last 10-K, PAGE 28 (The Northstar "Lien" - they, Northstar effectively own pretty much everything this company has, could have, or might have for all intents and purposes IMO)

"On October 1, 2012, the Company and Northstar entered into a limited waiver and forbearance agreement whereby the Company agreed to issue 5,000,000 shares of Series A Convertible Preferred Stock and 10,000,000 of common stock in exchange for $210,000 as payment towards outstanding debt, default interest, penalties, professional fees outstanding and due Northstar. In addition, the Company executed a security agreement granting Northstar a lien on all patents, patent applications, trademarks, service marks, copyrights and intellectual property rights of any nature, as well as the results of all clinical trials, know-how for preparing Myblasts, old and new clinical data, existing approved trials, all right and title to Myoblasts, clinical trial protocols and other property rights. In addition, the Company granted Northstar a perpetual license on products as described for resale, relicensing and commercialization outside the United States. In connection with the granted license, Northstar shall pay the Company a royalty of up to 8% on revenues generated."

I mean read that and ponder it- Bioheart could go belly up IMO, and then the Northstar LLC members IMO would/could walk away with essentially EVERYTHING that's "Bioheart the public traded company" including even all results to clinical trials, etc and then just re-start under some new name company and pick right back up where they left off. That's the way I read that statement above- I mean what's not in that list that would be "owned" or of any value to Bioheart that Northstar now doesn't have the rights too?

A "lien" - like what a mortgage holder gets on your house when they make you a loan. THEY OWN THE HOUSE until paid off- not you. That's what a "lien" means- and read what Northstar has a "lien" on- pretty much everything that is Bioheart, the public traded company. I've always wondered how that's even legally possible- and am now fascinated to see this suit essentially claiming the same thing or question the same thing. Now does a tiny group of insiders set up a small, private LLC (Limited Liability Company) who's "headquarters" is a residential "house" (per the Florida Secretary of State filings) a "house" apparently of one of the BOD members in rural MN and then "sign over to that little group" all the rights to ownership to pretty much all the technology, future sales, any assets, all intellectual property (if any even exists for this company?) of a public traded stock company? How is that possible?

Same 10-K, most recent, PAGE 77 (the mystery of who even makes up the membership of Northstar LLC, there's some secret, un-named "members" never named as far as I know). Read the lawsuit- it's alleging "breach of fiduciary duties" of the BHRT Sr Mgt and BOD and this is one of the specific reasons per reading the claims- you can't set up a secret sub corporation and then give it control and rights of ownership to the assets of a public traded stock company? How is that possible and that's what the lawsuit is asking per my reading of the complaint. The suit is saying that's a "breach of fiduciary" duties of the Sr. Mgt and BOD to have set that up and grant if the "lien" and all- they just can't do that according to the suit per the legalities and transparency required of public traded stock companies- that's what the suit is alleging and wants a judge to rule on.

PAGE 77: (not all the Northstar members are ever even listed- so who's the mystery members that hold all this power over a public traded company, BHRT?)

"Excludes Northstar Biotechnology Group, LLC (“Northstar”), owned partly by certain directors and existing shareholders of the Company, including Dr. William P. Murphy Jr., Dr. Samuel Ahn and Charles Hart."

Notice the wording- "owned PARTLY BY"? Ok, then who owns the OTHER PARTS? Who's the mystery owners and why are they never named? It's a public stock company- how can their be secrets?

Then, the lawsuit is filed by Brenda Leonhardt and suddenly they, Northstar Biotech LLC file documents (public of course) with the State of Florida Secretary of State and suddenly change control and location of Northstar LLC to some guy in MN "Gregory Knutson" (not sure on spelling, see filing documents) and he's shown as being an owner of some "construction company" in rural MN. So now BOD Chuck Hart is no longer listed as running Northstar- which at least Chuck Hart is a sitting Board Member of Bioheart- so there's at least some sense to it perhaps- but now some "guy" who's a construction company owner per public records- now he's in charge of Northstar LLC and the 500 MILLION plus votes it holds and controls over the public traded company Bioheart- 20 million preferred stock shares with 25:1 votes each over common stock votes. 500 MILLION voting right- like they just handed the keys to the car IMO to "some guy" that as far as I'm aware of- no one as a public shareholder has a clue as to who he is, or why he now runs Northstar and the control it has over Bioheart- and Bioheart of course is saying nothing about it, as per standard operating procedure IMO

http://search.sunbiz.org/Inquiry/CorporationSearch/SearchResultDetail?inquirytype=EntityName&directionType=Initial&searchNameOrder=NORTHSTARBIOTECHGROUP%20L120000248400&aggregateId=flal-l12000024840-bd33dc0c-23e3-4df8-9590-ecf4bbbe3d0d&searchTerm=northstar%20biotech&listNameOrder=NORTHSTARBIOTECHGROUP%20L120000248400

That's the LLC filings for Northstar Biotech- all LLC's or Corps must be on file with the Secretary of State in which they exist.

Now, here's the latest document they filed- removing BOD Chuck Hart as being the "Managing Director" (or President or whatever title they use, of the LLC, and inserting this new guy, Gregory Knutson?) What sense does that make? Why did this happen now? Why's it not at least Sam Ahn who's an M.D. and a sitting BOD member or someone like him- why isn't he "Managing Director of this Northstar LLC "thing" they created? Instead a "construction company" guy in rural MN now has the managing power over it all? What? Why?

http://search.sunbiz.org/Inquiry/CorporationSearch/GetDocument?aggregateId=flal-l12000024840-bd33dc0c-23e3-4df8-9590-ecf4bbbe3d0d&transactionId=l12000024840-46773435-d124-47a2-a180-a768590a4a43&formatType=PDF

Title Manager : Knutson, Gregory

Ham Lake, MN

http://www.whereorg.com/g-e-knutson-construction-8294240

There's a public record with the EXACT address now listed as "Northstar Biotech, LLC "headquarters" or "main contact" per the Florida Secretary of State website and it's Gregory Knutson a "concrete construction" company in some small town in MN. Who is that guy and why does he now sit as "controlling manager" of a high tech biotech public traded company via a "lien" given to a tiny LLC and over 500 MILLION voting share rights per 20 million preferred stock shares over which he now has the controlling vote power? How does that "work"?

Here's the latest SEC filed "ownership shares" document for Northstar Biotech LLC and sure enough- it says right on it, that "Gregory Knutson" now has the "voting control rights" to the 20 MILLION preferred shares of Bioheart stock which at 25:1 voting rights if 500 MILLION plus votes- as Northstar also holds shares of common stock.

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000029/d31977.htm

From that SEC filing:

"Names of reporting persons: Northstar Biotech Group, LLC"

" Greg Knutson, Chairman of Board of Managers, is deemed to have voting and dispositive power"

Same SEC filing:

" Shared dispositive power: 52,368,582 capital shares (32,368,582 shares of common and 20,000,000 preferred (each share of preferred stock has voting power equal to twenty-five common shares)"

Again, in the past it was always Chuck Hart, who at least sat on the Board of Directors of Bioheart. Who is "Greg Knutson" of MN? Why is he now running and got the voting control power to Northstar Biotech LLC and all the power it has over the public traded company known as Bioheart? How does all that "work" or make any sense IMO?

It just gets more bizzaro IMO as it goes along. I'll be fascinated to see where this lawsuit goes if the local Florida biz press follow it- to see if it indeed "peels back the layers" on the ole Northstar LLC onion.

I find it very fascinating IMO. I never understood Northstar existing from day one. Don't see how it's even possible when this is a public traded stock company.

My 2 cents. IMO, shareholders (and it says so right in the 10-K filing) likely get the goose egg, nothing in the event this company goes into default on any of their large debts, goes BK or whatever. Almost always the way it works, always IMO.

Quote, "What was the breach in contract for the suit to be filled? Did BHRT miss a payment or extend the duration of the terms, I am just not sure I understand the merit behind the lawsuit? They handed money over to a start up company and what were they expecting?

"

They LOANED MONEY as CREDITORS and were expecting to GET PAID BACK- like how it works in the world of loans and creditors and debts? Where is it that it says "they handed over money to a start up company"???? Did B of A just "hand over money" to a start up and expect no repayment of the DEBT? Is that how banks work? Cause this money is related to bailing out the original original "Bluecrest" loan and B of A for a loan going bad (and the Bluecrest loan is in this mix too I think, but LOANS, aka debt, not charitable gifts or donations to a start up or whatever?) Loans, debt mean one expects to get paid back- they weren't buying stock or equity in the company as risk takers. Debt is always in first position over equity. For example, in a BK proceeding, Bond holders, aka "debt" holders are always paid back first before one cent ever goes to any stock/equity holders. It's why stock share holders almost never get a cent in a BK proceeding- as all the bond holders and other "creditors" (accounts payable, vendors, equipment loans, whatever-anyone owed a payment) always get paid first out of any money left in the BK proceeds and stock/equity holders are always paid last, which usually means nothing. Debt/loans are not "money just given"- they are loans with expectations as creditors of being paid back.

http://www.bizjournals.com/southflorida/stories/2010/07/26/daily1.html

That's the time frame of the B of A loan going into default, which is in the mix of all this and why the Leonhardts are "on the loan" to B of A as "guarantors" in the first place- it's a big, complicated series of BHRT teetering on BK at the time and then the Leonhardts acting as "guarantors" and creditors using their own assets and money- not GIFTS, but loans/debt IMO.

Thus, if one reads the lawsuit as filed, all allegations are answered pretty crystal clear IMO. It's alleging they (Bioheart) "subordinated" her (Leonhardt) w/o rights to do so and also then paid off many other creditors ahead of her, including insiders via the creation of some insider run "thing" the LLC corp, known as Northstar Biotech LLC (who they, BHRT then granted a "lien" to essentially everything BHRT owns, could own, might ever own, etc) but excluded her from that too- and the suit is even alleging the validity of how an LLC such as Northstar can even exist- as it's like a tiny private company within a public traded company- essentially being given total control and rights to everything the public company has or ever could have. I personally never understood how Northstar LLC and the "lien" thing and all was even legally possible for a public traded company- it makes zero sense to me, IMO.

http://lawsuitpressrelease.com/wp-content/uploads/2014/12/Leonhardt-v.-Bioheart.pdf

That's then entire initial suit as filed- on a public site. It's all in there- what they, the plaintiffs, are alleging and filing for. Not confusing IMO?

They, Bioheart, paid off her ex husband's (Howard Leonhardt) portion of the debt owed and then "subordinated" her and have never paid her- it's pretty cut n dry IMO. Just read the suit filing- it's all in there? What's confusing or not clear?

They, the Leonhardt's when married didn't just "hand a bunch of money to a start up", that's nonsense, LOL? They acted as creditors and "guarantors" to a very specific loan that BHRT needed to stay out of default related to a public traded stock company, Bioheart- they were creditors, not "handing out gifts or charity"? Where is that written? If that was the case then why is BHRT carrying the DEBT (it's listed ON THEIR BALANCE SHEET UNDER LIABILITIES/DEBTS) why carry it then "on their books" to this day? Why didn't they just discharge it and write it off then if it's got no merit as a valid debt obligation, is not owed, is frivolous or whatever? No such thing as company's carrying "phantom debts" on their books from an audited accounting standpoint? That debt of $1.5 million "subordinated debt, related party" is there, and has been there since the 2010 time frame as alleged in the suit, and is there "on the books" for a reason IMO and landed on their balance sheet for a reason- it wasn't some "they just gave um money" deal? Else, WHY is it booked under DEBTS OWED on their own balance sheet? Why?

It's not confusing at all IMO. They paid her husband back using stock and warrants, they paid back a bunch of debts to Northstar LLC members, aka "insiders" (BOD members and a few others) and they haven't paid her- and she wants to get paid back for a debt/loan that she made to BHRT while married to her husband, then CSO/CEO of the company prior- who was paid back his portion, while she's gotten nothing on her 50/50 split portion post divorce, spelled out in the BHRT 2010 10-K filing (the divorce splitting of the Leonhardt BHRT loan/debt, PAGE 68, yr 2010 10-K filing) in pretty plain English IMO.

My 2 cents. Pretty clear cut to me.

BS IMO, "Woops, Shawn Collins... Does anyone on this board know who Shawn Collins is and his relationship to BHRT? Not Ryan. I saw Shawn Collin's name posted on another board, but could not make out what the person was saying was his involvement in the company. Can anyone share any info? "

"on another board" but then no link to this imaginary "other board" where all this is said? Really?

Link to the "other board" so all can read it and then maybe "share any info". Else, IMO the claimed info above doesn't exist on some "other board". Link, or it's not there to me.

Quote, "What were the specifics terms of the loan? How long did the filings say until they needed to be paid back?"

I'm not the company accountant or CEO or working for them- how would I know?

I do know the exact amount and description of the original loan is right on the most recent Bioheart 10-Q filing, "subordinated related party debt, $1.5 million"- that matches exactly what the lawsuit filing reads as the original principal owed and the exact wording of the email exhibit from then company "controller" Angel or whatever the name is, that's attached to that lawsuit filing that on the public link.

http://lawsuitpressrelease.com/wp-content/uploads/2014/12/Leonhardt-v.-Bioheart.pdf

Latest 10-Q filing, most recent quarter, PAGE 4:

Then, one can go back to the 2010 10-K filing and see the original debt/loan described via the wording of the "Leonhardt divorce" being described- and it states pretty clearly to me that they admit she had a "debt" owed her and also her then husband. As part of the divorce they then "equally split that debt" and Howard Leonhardt former CEO decided to take shares of common stock for his 50% portion (meaning IMO they paid him, meaning the original debt and them acting, the Leonhardts acting as creditors was confirmed and real, else why did they pay Howard Leonghardt his 50% owed as a large block of shares for his portion?) and Brenda Leonhardt appears to have retained her debt as "owed" and was willing apparently, to wait to be paid and let it accrue interest. The suit is apparently alleging (per my reading of it) that Bioheart then "subordinated" her without rights to do so, putting her in 2nd place to a bunch of other creditors- and then paid off a bunch of other people, including Northstar LLC, aka "insiders" as her loan/debt of $1.5 mil plus interest owed just sat never getting paid, sitting as "subordinated" and being carried forward endlessly on the books- that's my read on it.

Here's the 10-K wording from 2010, affirming again, IMO what the suit is alleging- that she indeed "inherited" via the divorce process, 50% of a debt owed to her and her husband, then CEO and CSO Howard Leonhardt.

http://www.sec.gov/Archives/edgar/data/1388319/000114544311000484/d28195.htm

2010 10-K filing, PAGE 68:

"In February 2010 the Company’s Chief Science and Technology Officer and his spouse filed divorce papers. Pursuant to the divorce, their jointly owned shares and their ownership of the loan to Bioheart which they hold as a result of their payment of $3 million of principal and related interest to Bank of America on behalf of Bioheart, would be divided equally between them. As a result, the Chief Science and Technology Officer’s common shares were then reduced to 2,513,840 and his percentage shareholding of the Company to 13.8%, with his former spouse assuming ownership of the same number of common shares and percentage shareholding of the Company. Their commonly owned loan and related interest, as of March 29, 2010, $4,140,201, was been equally split. The Chief Science and Technology Officer on March 29, 2010, elected to convert his portion of the loan and related interest to restricted common stock and warrants. As a result, Howard Leonhardt, the Company’s Chief Science and Technology Officer, as of March 31, 2010, owns approximately 22 % of the Company."

Right there in plain language IMO. $3 million split 50/50 is the $1.5 million carried on the 2014 10-Q filing as "subordinated, related party debt" in the amount of $1.5 million. All interest owed would be on the "accrued expense" line entry or some similar other line entry than the original principal amount of the loan. One can see that even back in 2011 when that above 10-K was filed, the total owed to the two was already up to $4,140,201 due to fees, expenses and already accruing interest.

Looks like it's all there "on the books" as alleged to me? I don't see anything frivolous or confusing IMO? Pretty clear cut seems to me.

Of course they (the defendants) will file/filed a "motion" to dismiss. Has or did it happen? No, not as of yet. It's law 101 basics. The defendants will always file numerous motions for dismissal.

Nothing new or meaningful about that IMO. It's done in every case, always.

Look at the date on that article link about the "motion to dismiss"- it's dated Jan 2015. Was the case "dismissed" or motion granted as of today, March 7th 2015? Doesn't look like it to me?

As stated, those "retained attorneys" for the remainder of Bioheart BOD members on that clerk of the court site, several of them were just filled in within about the past 2 weeks. As I checked that site a few weeks back and BOD member Ahn and at least one other Bioheart BOD member had no counsel listed or filled in on that chart (just blank, no attorney listed or "retained", now all are filled in as having "retained counsel")- maybe they were hoping for a quick dismissal and thus didn't sign-on or hire counsel immediately and it appears the "motion to dismiss" hasn't happened yet, and now it's heading into mid March. So perhaps that's why they've now fully "lawyered up" and retained counsel IMO.

Again, that link to that article about the defendants counsel saying they will seek to "dismiss" is from early January. It's old info.

https://www.clerk-17th-flcourts.org/Clerkwebsite/BCCOC2/OdysseyPA/CaseSummary.aspx?CaseID=7862332&hidSearchType=party_case&DisplayCitation=no&CaseNumber=CACE14021256&SearchType=

$2 million plus lawsuit against Bioheart for alleged failure to pay back a creditor/debts seems to be moving ahead- it looks like to me.

http://lawsuitpressrelease.com/investors-sue-bioheart-inc-millions-unpaid-debt

http://lawsuitpressrelease.com/wp-content/uploads/2014/12/Leonhardt-v.-Bioheart.pdf