News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

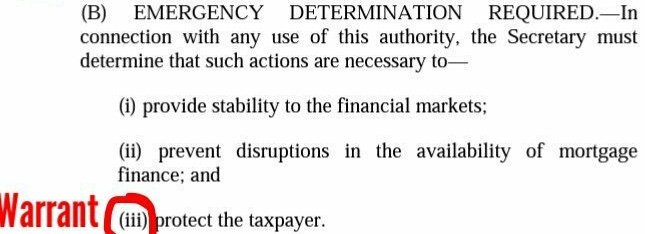

The purchase of securities by the UST, like the Warrant, had to comply with any of the 3 prerequisites under a temporary authority that expired in December 2009 inserted by HERA into their Charters.

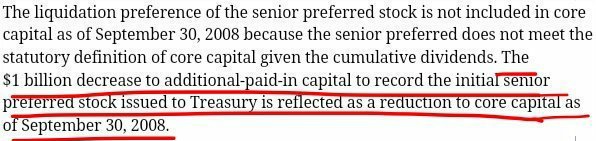

This is why we consider the Warrant as collateral of the investment in SPS, regardless that it wasn't a purchase if the UST got it for free. We consider it purchased at no cost (another example of gifted security: its value was debited from the shareholders' pockets: Additional Paid-In Capital account -Core Capital-, another breach of the FHFA-C's Rehab power. Although, at the same time, surprisingly it was credited to APIC too, one of the 9 Securities Law violations)

Anyway, even as collateral, it's barred in the Charter's Fee Limitation clause:

PROHIBITION OF UNITED STATES.... No fee or charge, collected or assessed, with regard to the assets or securities of FnF.....except the rate in the original cheap UST backup of FnF.

"May" in the Power and the Incidental Power, intertwined.

Fanniegate is a case of breach of multiple statutory provisions and financial concepts, and the judiciary and corrupt litigants with their social media "Goofies", providing the alibi with misinterpretations and coverups.

It has led to a case of "restructuring" with proposals of resolution that look more like kids that, instead of trading with baseball cards, exchange stocks. No skills are necessary, this is why Bradford is redoubling his efforts using LuLeVan and The Man With No Name.

They still don't get what the rehabilitation of a financial company means. Even judge Willett and Justice Alito coincided in stressing this fact of rehabilitation of FnF as stated in the law (any action authorized by the FHFA-C's Rehab power. "May" isn't an authorization to be excused from complying with "Rehab", once the capital is built -Retained Earnings-, but related to other activities, conservatorship-related or not, like the preps of a Housing Finance System revamp: CSS, CSP, UMBS, etc), but the Goofies have "gold fever" and only see an opportunity to make up for their losses getting common stocks trading at rock bottom prices and discounting the fraud all across the board.

There are multiple subcommittees that tackle Housing matters, both inside the Housing and Banking committee and the Financial Services committee, in charge of overseeing the operations of FnF and their conservatorships, but I've never heard from a politician any complaint about the breach of statutory provisions or the fact that the Core Capital was deep in the red in their quarterly S.E.C. filings since early Conservatorship, but the opposite. For instance, they've been openly delighted about how profitable was being a conservatorship for the taxpayer (Senator Brown). With an adjusted $-216 billion in their Retained Earnings accounts, FnF have not been rehabilitated.

The idea that they couldn't have overseen the FHFA, since Congress hasn't received a FHFA Report to Congress with the ERCF tables yet, is ridiculous. This is why the same Capital Rule effective February 16, 2021, directed FnF to keep the ERCF tables secret till January 1, 2022, and why rep. French Hill and rep. McHenry scheduled the 2023 testimony of the FHFA director one week before the expected release of the 2022 FHFA Report to Congress that would show the ERCF tables for the first time.

Without the ERCF tables, they can make up the numbers. Rep. Blaine in the hearing: "$100B vs $300B". Sandra Thompson: "You got it!". When it's "$-90B vs $207B". A $297B capital shortfall. He claims that $300B is the capital requirement instead of capital shortfall. And $100B is their Net Worth, $103B to be precise. $-90B is their Core Capital.

This is why the FHEFSSA is concealed. So you don't know that the Undercapitalized threshold is met when the core capital is greater than the minimum (Leverage) capital requirement (The definitions of each Capital Classifications, that the Mnuchin's UST recommended Congress to repeal, in the 2019 Housing Reform plan)

Rep.Blaine:"The threshold for exit is $300B". No, $300B is the capital shortfall, the threshold is $207B, the Minimum Leverage Capital requirement (mandatory release in the prior FHEFSSA, struck by HERA), as of end of March 2023. And by the way, the adjusted figures are: "$-193B Core Capital vs $207B", adjusted for the $103B gifted SPS that carry an offset that reduces the Retained Earnings accounts (core capital). A $400 capital shortfall over Min. Leverage Capital requirement.

So, Rep. Blaine didn't want to download the earnings reports with the ERCF tables, so he can now claim that he didn't have the 2022 FHFA Report to Congress in time for the hearing.

Don't tell me that it's the funding structure of the FHFA the cause of the problem of lack of oversight.

I see collusion Congress-FHFA.

A clear case of misrepresentation of their financial condition to fish in troubled waters. Even Financial Statement fraud (gifted SPS hidden on the Balance Sheet in plain sight), is being concealed by both parties shamelessly colluding in this scandal. Let alone concealing the laws FHEFSSA and the Charter Act with the cheap UST backup of FnF and a Fee Limitation of United States. These people truly think that everything inside suddently vanishes.

The penalty on the corrupt litigants and their crew peddling the Government theft story, is of supreme importance. $4.8 billion, the sum requested by the Equity holders in Punitive damages. The same amount from the DOJ ($1.94 per $50 par value JPS and common stock)

BOTTOM LINE

The reality is that the FHFA director has complied with all the statutory provisions so perfectly, that even he has made use of its Incidental Power (secondary power) as conservator to that end: The Separate Account plan.

Navy, the board's Goofy, creates ID's to later reply to himself:

"thx navy"

"Awesome Navy"

This crackpot has to explain his daily posts about more buyers than sellers when the stock goes up or the contrary.

Great urinalysis!

Insane.

Just so you know, under no circumstance $1 will come out of FnF.

The corrupt litigants have made up phony damages defrayed by FnF, as kind of back dividends that would make up for their losses with the dividend suspended and through an illegal Class Action with the absence of the FNMA holders.

All monies in damages will be paid by the DOJ as vicariously responsible of the FHFA's actions and they are Punitive damages, as the harm of loss is redressed with the announcement of the Separate Account plan (a posting of $228B in their Retained Earnings accounts after the Treasury Stock -stock buybacks- is retired, and a cash refund worth $152.3B)

Navy Hedge Fund is a JPS holder. You also write with Patswil and Stockprofitter.

The spokesperson of the Moelis Gang still doesn't understand that entering the judgment was deferred, at the request of the FHFA, because the payment of Securities litigation claims is a capital distribution, and thus, RESTRICTED when FnF are undercapitalized. Just like the dividends and today's gifted SPS handed out to Treasury every quarter, which exposes the Separate Account plan with both the 10% and the NWS dividends, then the gifted SPS which are holding the Common Equity in escrow as well (concealed with Financial Statement fraud, as these SPS are absent from the Balance Sheets), and starts the prosecution of the litigants and Co.

You don't like the rules, do you.

You've got mail! Another check has just arrived.

Howard always cheating. He can't say

“Separate account” (I don’t know what that is)

.jpeg)

Why on earth do you post the CFR with an excerpt taken from the law FHEFSSA with the duty of the FHFA director as regulator (which is different to the authority now as conservator by the way: Put FnF in sound and solvent condition), instead of going to the source, the law FHEFSSA?

To ensure that:

FnF operate in a safe and sound manner, including maintenance of adequate capital and internal controls

Howard and Stevens haven't read the Charter Act dynamics yet, where FnF can't buy MBS or any asset, unless it complies with the clause Credit Enhancement.

FnF are forbidden to buy any security or underlying mortgage, where the mortgage exceeds 80% of the value of the property that secures it (Maximum 80% LTV). The property is the collateral of the mortgage, but FnF are compelled to sell NPL and RPL and even the REO inventory, to their cronies instead.

Unless, this security or underlying mortgage has one of these credit enhancement operations:

(i) The portion of the mortgage (credit risk) that exceeds 80% LTV, is guaranteed by an insurer (The borrower buys PMI)

(ii) The seller retains a participation in the mortgage of more than 10%.

(iii) The seller guarantees 100% the mortgage against default.

This is why the PLMBS were illegal and thus, subject to mispricing in the run-up to the 2008 financial crisis, and fraud (PLMBSs sold to FnF with fraudulent information. For instance, the lawsuit filed by the FHFA on behalf of FnF about a $202 billion PLMBS portfolio and against 18 financial institutions)

For the same reason, the current Credit Risk Transfers (CRTs) are illegal, as it's not a valid credit enhancement operation among the ones enumerated. The shareholders are requesting a refund of the CRT expenses, net (turned into Retained Earnings. The Core Capital that protects FnF) and it's been included in the assessment of BVPS in the case of a Takings or, otherwise, part of the $152B cash refund from UST-FHFA. Likely, the CRT expenses are a backdoor Commitment Fee, barred in the Fee Limitation clause of the Charter Act.

The mortgage-related investment portfolio filled with these illegal PLMBS (more than $1 Trillion), had to be reduced 10%/15% per year when conservatorship began.

The mispricing of these securities was one of the reasons of the conservatorship (AOCI line item in Equity. Unrealized losses), this is why Howard's assertion that "those portfolios were extremely profitable" is laughable.

Once in Conservatorship, these PLMBS skyrocketed.

The Resecuritizations is a security that would fill the void, complying with the Credit Enhancement (iii) (Too bad that the Charter is no longer necessary, as we are bound for a Privatized Housing Finance System). It's the so called "catastrophic-loss reinsurance", where a guarantor bundles the UMBS guaranteed by other guarantors into "Supers", sold to investors, and the insurance claim isn't paid until the guarantor files for bankruptcy. It can be Government reinsurance or private.

The security was launched by Freddie Mac in June 2022 and it was priced at 9.375 bps.

It can be used for the option 3 in the 2011 UST-HUD Housing Finance System revamp, with a Government Catastrophic-Loss Reinsurance. Or private reinsurance for the options 1 or 2.

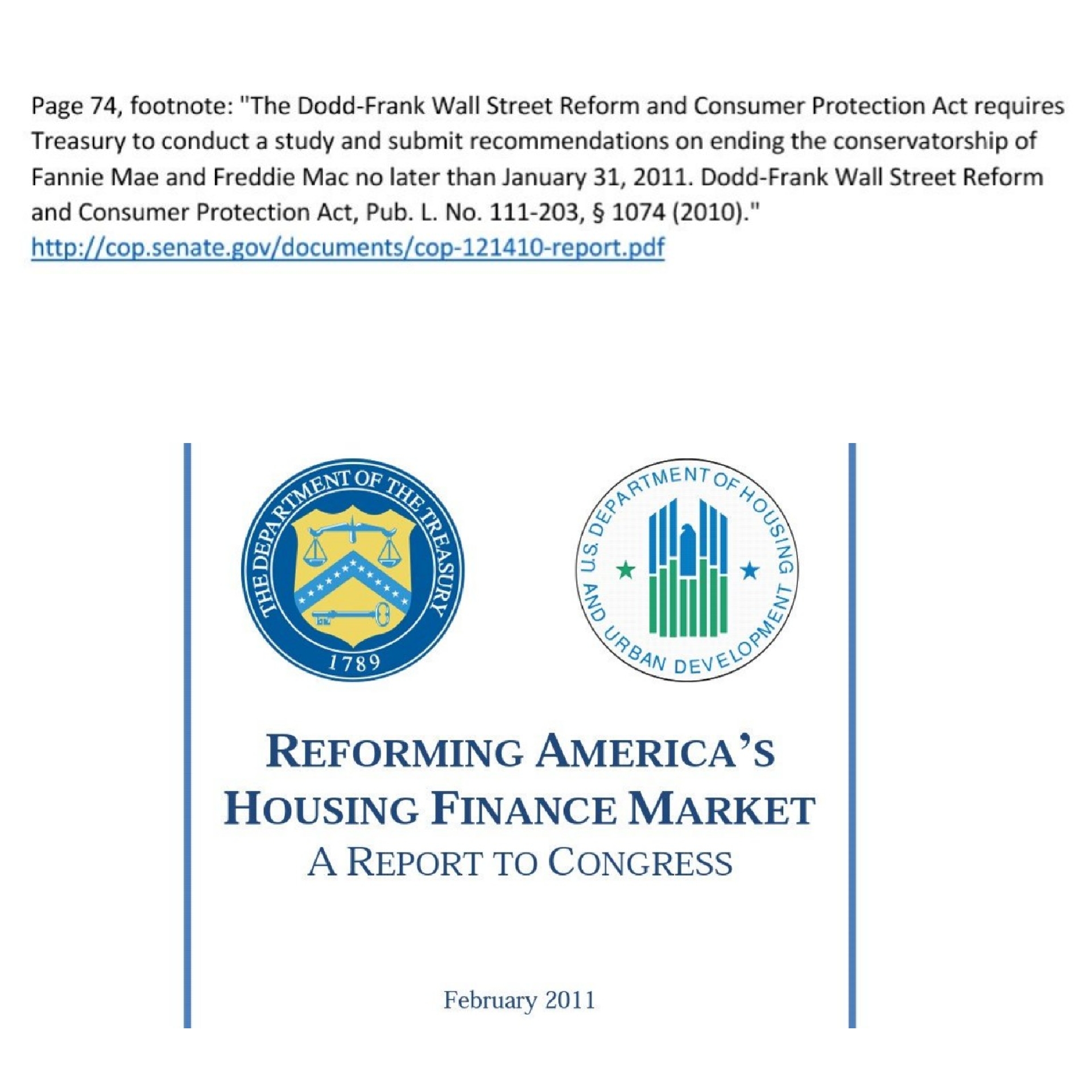

A 3-option plan as "recommendations on ending the conservatorships, no later than January 31, 2011", at the request of the Dodd-Frank law.

The 3 options imply a Privatized Housing Finance System, with "stringent capital requirements", known as Basel framework. Hence, the February 16, 2021 Capital Rule (ERCF)

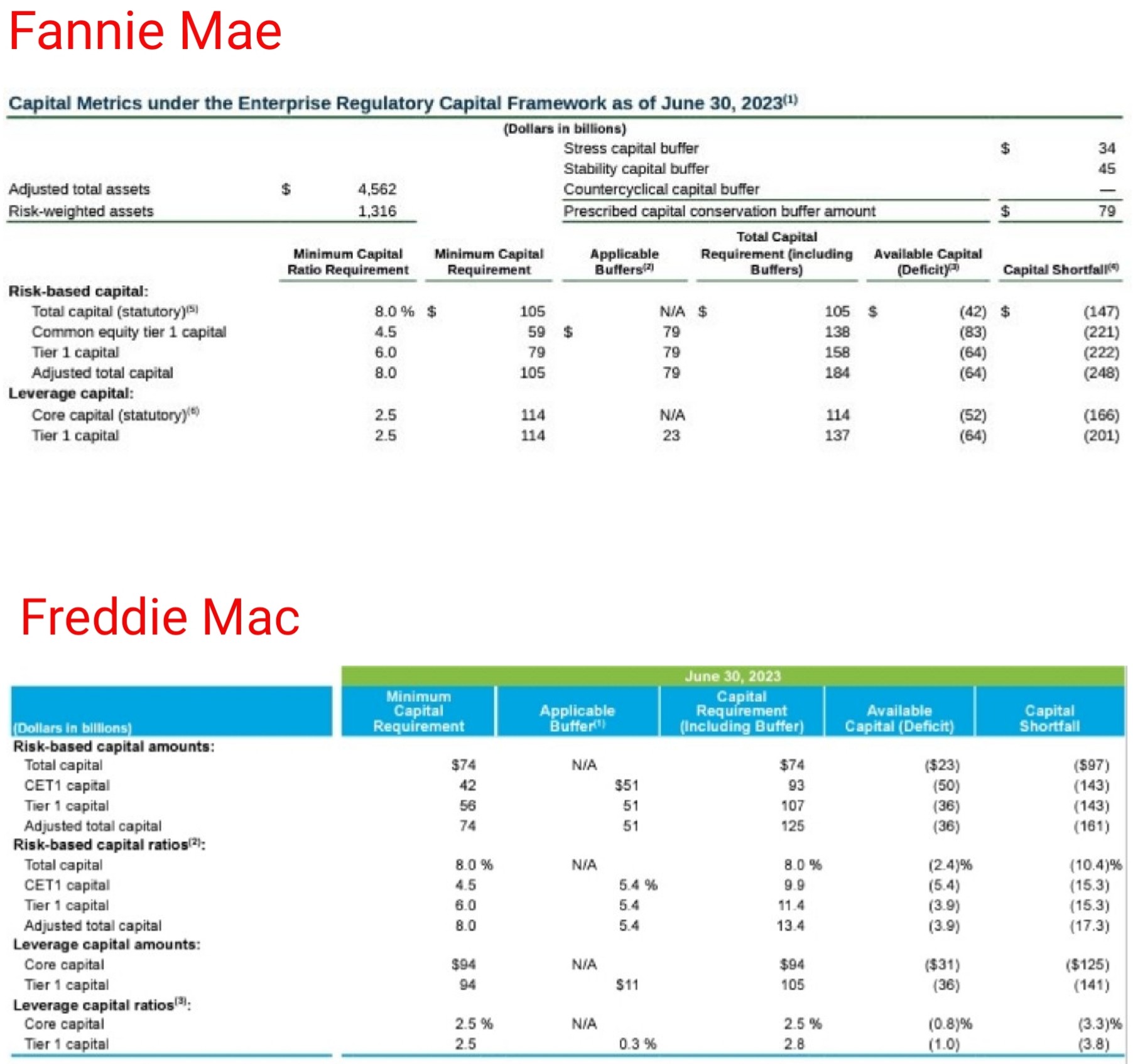

FnF would meet all the capital requirements even after the redemption of the JPS (Fannie Mae $1B short of Tier 1 Capital for the Leverage ratio, but as of end of June, 2023. No big deal today, end of Q3). Also taking into account that it's expected the amortization of the Deferred Income into earnings in one fell swoop, with an Accounting standard change.

Therefore, the UST backup of FnF upon "Capital deficiency" (negative Net Worth) is no longer necessary and the Charter would be revoked. Also, the Charter's Public Mission isn't necessary, as FnF no longer subsidize the guarantee fee thanks, in turn, to the UST backup of FnF, and their countercyclical role in the Secondary Mortgage Market as stated in the section Purposes (Step up buying mortgages. It isn't about refinancings and loan modifications.) is only in a financial crisis, not in an economic crisis. This is why the plotters attempted a banking crisis in 2023 after having been allowed by the Federal Reserve in a Schedule for the U.S. banks about how to fill out a Balance Sheet (FR Y-11. Schedule Balance Sheet reporting. General instructions. December 2020), to commit Accounting fraud with the unrealized losses (AOCI) in their investments in debt securities, unaccounted for, as they are held in HTM portfolios (unlike FnF for their PLMBS portfolios, commented above). Thus, there are only 2 options, not 3 as the Fed pointed out in the Schedule, for the valuation of investments in debt securities. It seems that this problem will be solved on October 1st, with the new Capital requirements by the Fed, as they tackle these unrealized losses that don't show up in Equity.

The prior liquidity crisis attempt in December 2018 with Mnuchin-Powell (Mnuchin phoned 6 bank CEOs, etc) failed. Powell, in this second attempt, suceeded, but not with FnF that have their interest rate risk hedged and their investments valued at fair value.

Bradford, you are the only one that talks about reverse split.

Here with LuLeVan.

IPO, etc, as mandated by your boss Bill Ackman.

Another check is coming for you and Patswil/Navy Hedge Fund.

Navy Hedge Fund once again acting as spokesperson for the corrupt attorneys.

The informaton about the scheduling in the Lamberth court was already made public on August 31.

So, we already knew that next Monday, it's scheduled a brief.

The attorneys want to pass the delay in the judgment as a period of discussion about the prejudgment interests, when the reality is that the judge doesn't have to hear from the parties on this issue and they attempt to cover up that the delay was caused by the ORAL MOTION TO DEFER ENTERING JUDGMENT by the FHFA's Wall Street attorney on the verdict-day.

This is because he realized that the payment of this Securities litigation judgment is restricted when FnF are undercapitalized in the famous FHEFSSA's Restriction on Capital Distributions, as the FHFA added this item to the definition of capital distribution through the 2011 Final Rule in the 12 CFR §1229.13, and authorized in the law to do it.

Thus, the FHFA's attorney sought to keep this restriction from the public with the delay, that would have exposed that capital distributions are also dividends and today's gifted SPS as compensation to UST in the absence of dividends (read the definition posted above), and the Separate Account plan would have had to be unveiled, that is using the exceptions to this restriction (reduce the SPS and recapitalization) to comply with the FHFA-C's Rehab Power.

Bill Ackman is the enemy of the shareholders and always in favor of the JPS holders, calling the common stocks "options", calling for a "Privatization", lying about what the SCOTUS said implying that FHFA has absolute discretion in its actions, when Justice Alito talked about "the rehabilitation of FnF" endgame, paraphrasing his colleague judge Willett when he interpreted the "authorized by this section" (within the enumerated powers -Rehab-) in the prior en banc ruling.

The rehabilitation in a financial company is about capital levels and debt levels, that is, build capital and reduce the obligations with the taxpayer (SPS)

It's not just the return to profitability.

Retained Earnings is core capital.

Ackman will keep his mouth shut knowing that there is a 4-box Checklist Template for coverups of the law, as a scrutinity of those making public comments on FnF in formal documents (peddlers of the Government theft story, aiming to tumble the stock prices), plus a box for the coverup of financial concepts, like Dividends, a distribution of Earnings (unavailable funds for distribution, out of a Retained Earnings account with Accumulated Deficit all along. Latest: adjusted for the offset for the gifted SPS, $-216 billion combined)

The odds are that Ackman is just holding a stake in FnF Common Stock on behalf of others.

So, he is another hedge fund manager pursuing stock offerings in FnF, as a scheme of secured deals for many years to come.

Pro se plaintiff, aren't you ashamed for calling a dividend rate "coupon"?

The FHEFSSA provision for the repayment of SPS isn't a refinancing feature in the law. The law states that it's for the REDUCTION of these obligations, as the exception to the Restriction on Capital Distributions (Dividends, today's gifted SPS to UST and the compensation for Securities litigation judgments currently in the Lamberth's court)

The exception is A and B, and A compels to raise cash with the issuance of any security, like common stocks, JPS or other obligations, in an equivalent amount, and had it been Equity stocks, the dividend is suspended as well. So, it can't be refinancing, but repayment option.

But the legislator didn't know that, due the double-entry accounting when the Common Equity increases (Retained Earnings + Other Comprehensive Income) the cash required was already raised and this is how FnF have repaid the SPS as the Common Equity increased, as per the intent of the legislator, which is legally binding as well.

As seen in my signature image below.

By the way, FnF have never had a problem of cash, since the SPS funded manufactured accounting losses (DTA valuation allowance, initial $1B gifted SPS, provisions set aside for modified loans)

So, no need to raise fresh cash with issuance of new securities. Although FnF issue tonnes of obligations daily, like the 30-year zero coupon callable MTN.

This controversial pro se plaintiff has always denied the existence of this statutory restriction on capital distributions, and laughed at me years ago for bringing it up on the Yahoo board, where he also wrote with 20+ different IDs, like on Ihub nowadays, and now he repeats it daily. Too bad that you didn't mention it in your lawsuit with Lamberth and now with Sweeney. Now you'll have to pay us damages for the coverup not only of this provision but the entire FHEFSSA and the Charter Act.

This is why now reading you repeat "APPLY THE LAW!" is laughable.

BOOM. Our negotiator puts forward a 4-box Checklist Template for scrutiny of the peddlers of the Government theft story ("We've been robbed!"), that is what really has decimated the stock prices.

A 5th box with the lie of: SPS, non-repayable securities, was added up only for Timothy Howard, as the only person that has asserted it in a formal document (his Amicus brief in the Supreme Court). Berkowitz's amicus, as a member of his legal team.

His personal blog is considered a formal document, because it doesn't satisfy the prerequisite of social media post, to be exempt from scrutiny (without the "community" characteristic)

PS. It isn't enough with having written the FHFA-C's Rehab Power. It must be expressly written that "Put FnF in a sound condition" means Recapitalization.

4 boxes to detect the coverup of statutory provisions.

Another box could be considered for the coverup of the financial concept of a dividend, a distribution of earnings. Unavailable funds for distribution, out of a Retained Earnings account with Accumulated Deficit all along.

SPOILER ALERT: All the plaintiffs tick all the boxes.

The case of the hedge fund manager Gary Hindes is more dramatic, because he amended his first lawsuit in order to remove these prior references to a breach of the FHFA-C's Rehab power that would have saved him from, at least, ticking that box and having to pay us an outsized compensation for damages.

LIE

— Conservatives against Trump (@CarlosVignote) September 11, 2023

☑SPS,non-repayable: W/ divs,but no actual div existed(Restricted & unavailable funds)

COVERUP

☑Restr on C.Distr.;Exceptions: reduce SPS/Recap

☑Cheap UST backup as a last resort (redeemable obligation)

☑FHFA-C's Rehab Power

☑🇺🇸's Fee Limitation.#Fanniegate @TheJusticeDept pic.twitter.com/iWJYUo2erc

Howard lies. 1st.The release is established in the law.

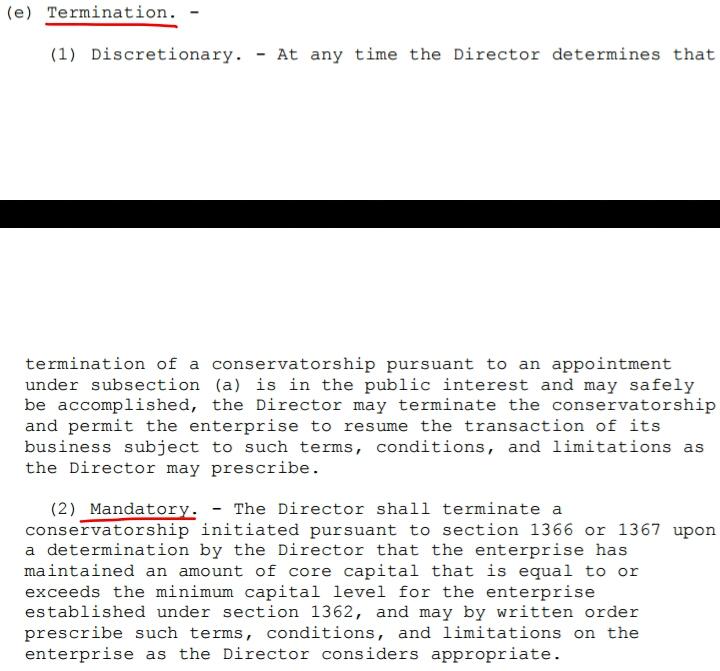

Although the mandatory release Undercapitalized (Core Capital > Min. Leverage Capital requirement (now 2.5% of Total Assets); or, with the new metric Tier 1 Capital > 2.5%. It implies that FnF have to build capital. Soundness. Rehab.) in the FHEFSSA, was struck by HERA,

...there is another law (Wall Street Reform And Consumer Protection Act, aka Dodd-Frank law) that required the UST to come out with "recommendations on ending the Conservatorships, no later than January 31, 2011", and it submitted a report to Congress along with HUD with a Housing Finance System revamp with 3 options for a Privatized System as the endpoint, which means Basel Framework for capital requirements or, as the option 3 states: "Stringent capital requirements" and thus, the Charter is revoked as the UST backup of FnF will no longer be necessary.

FHFA has been working hard since then, starting out soon after with these new initiatives:

Then, the UMBS, CSP, ....Resecuritizations, first priced at 50 bps to fulfill China's plan (Govt Explicit Guarantee) that I will comment next, but soon after it was switched for 9.375 bps that fulfills the original 2011 Housing Finance System plan, as this security enables the option 3: Govt Catastrophic-Loss reinsurance. Lastly, the Capital Rule (ERCF) adopting the Basel framework for the fully private sector as expected.

Trump and Mnuchin attempted to supplant this mandate by law, with Trump requesting to Mnuchin a new Housing Reform plan unveiled in September 2019, pursuant to a Presidential Memorandum, that envisioned a China-sponsored Housing Finance System with a Government Explicit Guarantee on MBS.

The attempt to supplant the 2011 mandate by law and subsequent Privatized Housing Finance System report to Congress, was also seen when Mnuchin claimed in his plan that:

Applicable law does not prescribe a specific end point for the conservatorship.

January 2021 letter agreements between former FHFA Director Calabria and former Treasury Secretary Mnuchin, specifying that neither can be released from conservatorship until they hold “tier 1 capital” (core capital, less junior preferred stock and a percentage of their deferred tax assets) equal to 3.0 percent of adjusted total assets.

Fannie and Freddie must hold 4 percent-plus “bank-like” capital irrespective of the risks of the mortgages they guarantee

Bradford = LuLeVan = The Man With No Name.

Obsessed with disregarding the law and harass the common stocks.

There won't be a resolution that changes the actions that have been taken.

A 10% dividend is as legal as a NWS dividend (subsection (g) unlimited yield on SPS), the fastest speed for the Separate Account plan, as it stopped the death spiral (the 10% dividend prompted capital deficiency)

It was not an actual dividend if it's restricted (like today's gifted SPS) and unavailable funds for distribution as dividend, out of a Retained Earnings account with Accumulated Deficit all along.

The FHFA-C's Incidental Power allows it to lie and send assessments with capital distributions under the guise of dividends, applied towards the exceptions of this restriction in the law + CFR1237.12.

Any resolution aims to uphold every single action by the FHFA and UST, not to change the past: "What if the NWS dividend had't existed? The SPS would have been repaid,..." and so on and so forth.

Bradford is another guy that uses multiple ID's, like the pro se plaintiff and navy cmdr.

The WSJ Opinion doesn't know that FnF are private shareholder-owned enterprises and that a Conservatorship preserves this status.

The taxpayer doesn't bear credit risk in FnF, even holding redeemable obligations in FnF (SPS) recorded in Equity. Long gone by the way.

An obligation is a compromise of repayment.

Who reads the WSJ?

It's the opposite: complaint for not being expropriated in 2012, when the Argentinean government acquired only a 51% stake.

The case is a breach of the YPF statutes that required a Takings/tender offer for the entire company when someone holds a 51% stake.

The relief is, thus, the full Taking of the remaining stake at the same terms as the initial 51% stake.

This has nothing to do with FnF in a Conservatorship, where they have repaid the obligation SPS and recapitalized through a Separate Account, according to the law and Finance, similar to the 1989 bailout of the FHLBanks, as I already told you, here.

Neither the Conservatorship nor the Charter Act, allow a Nationalization by taking the profits away, as the SCOTUS made clear with "the rehabilitation of FnF" endgame, which is the restoration to a sound and solvent condition (capital levels Basel framework and reduce the obligations with the taxpayer, respectively)

The Conservatorship terminates with FnF resuming independent operations.

If there is a Takings today at the stocks' adjusted fair value, it will be considered hostile.

Navy commodore is a Hedge Fund.

The only resolution will be administrative, as mandated by the law, and taking into account the Conservatorship since day one.

The SPS LP can't be written down as if by magic. That is, not only for no reason, but also not contemplated in any statutory provision pertaining to FnF.

This is what Fisher called for: a resolution cattle market-style, with two people sat at a table choosing from a Menu: a little bit of this, a little bit of that. Also known as: "What if...."

The repayment of the SPS is contemplated in the law FHEFSSA, as amended by HERA, as an exception to the Restriction on Capital Distributions when FnF are undercapitalized, which is what has happened with the phony dividend, as it's restricted and there weren't Earnings available for distribution as dividend, out of a Retained Earnings account with Accumulated Deficit all along (Balance Sheet = picture of a company)

So, no actual dividend was ever paid, but a capital distribution under the guise of dividend payment.

This is like the FHLBanks in their 1989 bailout: they had to pay an annual assessment and if it's more of the annual annuity that was used to pay interests, it was called "credit to the FHLBanks", and it was applied towards the reduction of the principal of the obligation in a statutory provision entitled: SEPARATE ACCOUNT, with monies invested in zero coupon Treasuries. This is what is written in the law, although they likely simply paid interests and the UST lost the $30B invested in the RefCORP obligation.

With FnF, the entire assessment was used to repay the principal of the obligation SPS, as dividends are..............RESTRICTED.

So, it was not an actual dividend but an assessment in the form of capital distribution, thanks to the FHFA-C's Incidental Power that allows it to lie ("Take any action...") if the endgame is the rehabilitation of FnF ("...authorized by this section")

Restore FnF to a sound (Recap) and solvent (reduce debenture SPS) condition (the FHFA-C's Rehab Power)

A dividend payment is NOT an interest payment.

You can't claim "mandatory" dividend (FHFA attorney) so that a dividend is turned into interest payments.

A dividend is a distribution of Earnings. Thus, a Change in Equity, as Retained Earnings is Equity and Core Capital, subject to restrictions when FnF are undercapitalized.

Interests are expenses, like personnel costs, etc., with no restrictions.

A SPS pays dividends, not interests.

Cumulative dividend though. It's been assessed at a weighted average 1.8% dividend rate, with a 0.5% spread over Treasury yields in each quarterly investment (0.299% spread in the 1989 FHLB bailout -GAO report-), pursuant to the original and prevailing cheap UST backup of FnF in the Charter Act since its inception. It's netted out with the amount of interests due to FnF on the $152.3 billion cash that the UST and FHFA owe to them.

Once the SPS were fully repaid (late 2013 and late 2014, in Freddie Mac and Fannie Mae, respectively), the FHFA had already contemplated this case when years before (July 20, 2011 Final Rule, coinciding with the Acting Dtr Time Limitation) it enacted the CFR 1237.12: capital distributions (deplete capital) applied towards their recapitalization (in a separate account obviously). Quote: "to meet the Risk-Based Capital requirement and Minimum Capital level".

The same occurs with the current compensation to UST with gifted SPS: both a capital distribution (restricted) and a breach of the FHFA-C Rehab Power (it prevents the recapitalization of FnF, concealed with Financial Statement Fraud, as these gifted SPS are absent from the Balance Sheets, in order to don't post the offset with reduction of Retained Earnings)

Hence, the Core Capital remains stuck every quarter since September 2019 at $-194 billion.

Because there isn't an assessment that exits the balance sheet, this new scheme is considered a "joke" instead of a Separate Account, thanks to the same FHFA-C's Incidental Power.

The Common Equity (Retained Earnings + AOCI) is held in escrow as well and, eventually, it will be returned to the Balance Sheets with the cancellation of these gifted SPS.

We can't allow these rogue lawyers to change the rules, making all up with kind words.

Fake. That's NOT what the Supreme Court requested, pro se plaintiff with one of your 30+ different ID's on this board (Barron, Vancmike, Rodney, HappyAlways, EternalPatience, etc):

show us where trump made concerted efforts or spoke about getting them out of conservatorship when he was president

expressing displeasure with actions taken by a Director and...asserted that he would remove the Director if the statute didn't stand in the way.

That statement from Trump goes against the plaintiffs, because the SCOTUS required a statement "expressing displeasure with actions taken by a Director and...asserted that he would remove the Director if the statute didn't stand in the way".

Because it was a constitutional claim abou the "for cause" removal restriction declared unconstitutional (It's consitutional by the way, in congressionally chartered private corporations: LIMITED POWERS)

But Trump does exactly the opposite:

We are doing well with them. Now, it's well managed.They are great people....They have some really good people running it.

MORE EVIDENCE OF A CORRUPT ORGANIZATION COMPRISED OF ATTORNEYS.

Collins was ALREADY remanded from the Supreme Court to a District Court for possible damages caused by the "for cause" removal restriction of the Director, declared unconstitutional, based on the lie already commented: FnF, the geese that laid the golden eggs (SPS and Recap, at the same time). This restriction prevented it from happening sooner, firing Watt before.

This is why the attorney for Berkowitz, David Thompson, now in Collins and everywhere, brought up the Trump's letter, so he could peddle the idea of "reprivatization" as a trump card that Trump had as the resolution of the Fanniegate scandal, that is, the Warrant exercised and the SPS switched for Common Stocks.

The stocks tumbled as a result.

We also can read in the lawsuit that the attorney claims that the SCOTUS required a statement from Trump to claim damages.

But the SCOTUS stated "had the president made a public statement...", not that now, Trump, a civilian, has to write a letter stating what he would have done and that it will be used in court by his buddy Berkowitz and Co. That's crazy and, secondly, fabricated evidence.

What lies behind is a MAFIA of attorneys working for renowned hedge fund managers and investment banks, bottom fishing the stocks.

Including the S.E.C. and the DOJ attorneys.

A compensation for Punitive Damages after the Separate Account plan is unwound, is of supreme importance.

Boy! This is a Conservatorship, not Nationalization. Hello?

Your attempts to pass a Conservatorship off as Nationalization, only shows that you want to rip off the shareholders.

It's pretty obvious that you are here paid by the hedge funds to repeat the slogan of Nationalization over and over again.

A lie repeated a thousand times, is still a lie.

Our powers and rights are transferred to the conservator to help it fulfill its statutory mission. It's not a Nationalization for the control of enterprises, Argentinean YPF-style.

Not only a Conservatorship bars a subtle nationalization attempt, as the Supreme Court stated with "the rehabilitation of FnF" as the endgame according to the law, paraphrasing his colleague judge Willett that interpreted the "authorized by this section" when the Incidental Power states: "Take any action authorized by this section", with "actions within the enumerated powers" (the Conservator's Rehab Power), but also the Charter Act bars the UST from any attempt to make profits using the securities and assets of FnF, as part of the Charter dynamics.

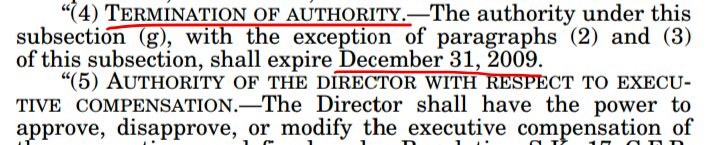

Nothing changed "as of the passage of HERA", as the DOJ attorney stated in his recent reply to Fisher, with the subsecton (g) a TEMPORARY authority that expired on December 31, 2009, and taking into account the rest of the laws.

Besides, the purchase of securities had the purpose of 3 prerequisites. The objective was never the taking of the property of FnF, as the DOJ attorney stated.

A redeemable obligation in the original UST backup of FnF, means that the intention of the legislator is that the UST can't overstay in FnF.

A Takings should be duly announced and our stocks taken away. The fair compensation for our stocks is their fair value today, adjusted for all the unlawful actions (Fake NWS dividend for Rehab. Remember? Otherwise a capital distribution restricted, barred and unavailable Earnings for distribution out of an Accumulated Deficit in their Retained Earnings account). That is, under the Separate Account plan up and running since day one, as seen in my signature image below. It's not a resolution today changing the past, with "What if...." as some people nowadays come up with.

The stocks' fair value is their Book Value, which in the case of the Cs is the Common Equity and in the case of the JPS, is their par value, taking into account that FnF would have been Adequately Capitalized and the dividend resumed (When the Tier 1 Capital met 25% of the Prescribed Capital Buffer. Table 8) since the 3Q2022 earnings report in the case of Fannie Mae and one year before in the case of Freddie Mac.

Consistent with the idea that in a Takings, at least the UST has to return to their Equity holders their money (Book Value)

A retrospective Nationalization doesn't exist. So, a Takings price today is assessed with the Book Value as of end of June, 2023, as shown in their adjusted Balance Sheets, adjusted for all the operations to misrepresent their financial condition, like the absence of the PLMBS lawsuit settlement and the CRT expenses, barred in the Charter's Credit Enhancement clause and a breach of the FHFA-C's Rehab Power. The "protect the taxpayer" rhetoric is a big lie. The taxpayer doesn't bear credit risk to begin with and FnF are protected building Capital, not paying for insurance.

A Takings in the middle of a Conservatorship would have been considered an opportunistic Takings. So, now that FnF should be released under the Separate Account plan, it's the moment to do it, otherwise the UST-FHFA refund the $152B cash due and FnF resume independent operations, when FnF would start trading at a PER 14 times or greater if there is Accounting Standard change in the Deferred Income.

In the meantime, the Common Equity keeps on being earmarked for the common shareholders as usual.

SPS, JPS and Cs are NOT products of FnF.

A product is a merchandise put up for sale as part of a business activity.

FnF aren't in the business of selling these securities.

This is why I made clear that a product is linked to an activity.

A SPS is a security, not a product (activity)

You are doing great as a stand-up comedian, for the moment when you have to play the fool before S.E.C. and DOJ attorneys and FBI agents specialized in organized crime.

A SPS is a security, not a product (activity)

If the law contemplates any (Subsection (c)) redeemable obligation (Subsection (b)), it means "any" . It includes SPS.

The key is "redeemable" (at the option of FnF): the UST can't overstay either as Debt holder or Equity holder.

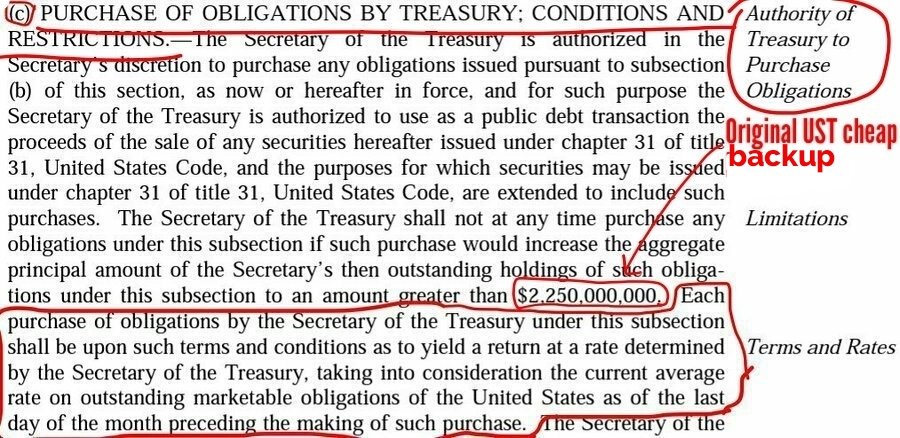

A MBS isn't the type of obligations the UST is authorized to purchase under the subsection (c) of the Charter, at a rate similar to Treasury yields (UST cheap backup of FnF)

Congress granted ONLY PURCHASE OF OBLIGATIONS (MBS)

FnF, the geese that laid the golden eggs.

The stocks rallied after more evidence comes out about the existence of a corrupt organization comprised for attorneys and their paid shills on social media, peddling that FnF are currently ripe for being released from Conservatorship and praising the FHFA, when the reality is that they are in the worst financial condition ever (breaking the SCOTUS' "Rehabilitation of FnF" prerequisite), subject to raqueteering activity all across the board.

A $4.8 billion penalty on each counterparty (Peddlers of the Govt theft story in formal documents and a voluntary payment in the case of the DOJ, necessary to settle the 9 Securities Law violations during conservatorship) is of supreme importance.

Obviously, the hedge fund manager Gary "call me Biden's friend" Hindes had to come to the party yesterday, here.

IN THE RUN-UP TO FRIDAY'S CON OPERATION, PAID SHILLS POP UP

— Conservatives against Trump (@CarlosVignote) September 7, 2023

Corroborating "FnF, the geese that laid the golden eggs(SPS +Recap)."For cause" restriction→Constitutional Damages.

-"Continued retention of earnings":ex-FMCC CEO;@ICBA

-NWS stop in 2019

-Decisive turnaround.#Fanniegate https://t.co/xu0wD1YBQY pic.twitter.com/Vs3qtTnCWt

What are they waiting for? Certainly not to his letter claiming that "the purpose of Conservatorship is to retore FnF to financial health". The conservator's power: Put FnF in a sound and solvent condition, by building capital and reducing the obligations with the taxpayer, respectively.

Which wouldn't be fulfilled as of end of June, 2023:

- Adjusted Core Capital = $-194 billion. A whopping $400 billion Capital shortfall over Min Leverage Capital requirement.

-$304 billion SPS outstanding.

-$-216 billion in their Retained Earnings accounts tasked with absorbing future losses.

-Financial Statement fraud with the gifted SPS absent from the balance sheets.

It seems that this hedge fund manager wants them back but severely damaged, just like all other plaintiffs: Bryndon Fisher, etc. This is why he talks about government's profits to lure the White House into his plan.

The odds are that FnF have been recapitalized to perfection, under the Separate Account plan and according to the Law. When the level of capital is such, that allows the redemption of the JPS at their par value and FnF remain Adequately Capitalized.

This way, the existing holder of ownership interest (Cs) and "other ownership interest" (JPS), considered "captives" by the FHFA (like some unwanted FHLB members expelled recently), are released from their captivity. The way to expel the common shareholders is with a Takings at the adjusted BVPS. Then, the UST resells the Cs at a PER 14 times, for instance.

The time has come.

Freddie Mac would have more than 25% of the Capital Buffer afterwards.

Fannie Mae $1B short of Tier 1 Capital as of end of June (Undercap, restricted, but we can make an exception being so close to the end of the quarter)

Then, it's expected that they will be allowed to amortize the Deferred Income into earnings in one fell swoop, which would be earmarked for building Capital Buffers or, distributed as dividend to the shareholders (holders of common stock) taking into consideration the resulting percentage of total Capital Buffer, to determine the limit in the Payout ratio (Table 8 of the Capital Rule)

Hindes fools no one.

"The continuing retention of earnings"

as retained earnings continue

In the run-up to FRIDAY's con operation by the attorney D.Thompson (Collins case. Also the attorney for Berkowitz, Rop, Bhatti, Robinson), it's necessary a paid shill corroborating his stance in court:

**Our negotiator responds to the ICBA's blog post**

(Tweet below)

Notice that the ICBA President stated in 2010:

It's estimated the Community Banks own between $15-20 billion in GSE junior prfd. shares (42%-56% of total outstanding), and affects to almost one third of the 5,000 Community Banks of the Association.

Another shameful post like in 2011,when it called for the sacking of FnF:"Infrastructure, including personnel,...transferred to new co-ops".

— Conservatives against Trump (@CarlosVignote) September 6, 2023

Pro 10%div/Warrant(BARRED: Charter's cheap UST backup/Collateral)

Adj.$-216B Retained Earnings. Rehab?@ICBA is owned by GS &Co.#Fanniegate https://t.co/H3CQuphnTL pic.twitter.com/iJYrCGrGAd

FHFA has worked hard to satisfy the Basel Framework for Capital requirements it adopted, as mandated by the U.S. Treasury that established a Privatized Housing Finance System (which means FnF's Charter, revoked, because the UST backup of FnF would be pointless) in a Report to Congress, as "recommendations on ending the Conservatorship, no later than January 31, 2011", at the request of the Dodd-Frank law.

The "post conservatorship world" that you point out, is already written in stone with the aforementioned UST's 3-option plan for Housing Finance and now it's up to Congress to choose which is the ultimate option.

DeMarco kick-started it soon after, outlining the grounds for this Housing Finance System revamp:

Then, the CSP, UMBS, pilot programs with the States' Housing Finance Agencies (HFAs) and, in June 2022, Freddie Mac unveiled the Resecuritizations for the option 3: Government Catastrophic-Loss Reinsurance, priced at 9.375 bps. Or private reinsurance and thus, option 1 or 2.

The same law, Dodd-Frank, that requires FnF to post an annual Stress Test. Another binding law covered up by the gang DOJ-Plaintiffs.

Capital Rule effective February 16, 2021. It came out too late, because HERA didn't put a time frame when it struck the Risk-Based Capital requirement in the FHEFSSA and authorized the Director to change the Minimum Leverage Capital requirement. It has taken 13 years to copy-paste the Basel Framework, yet it kept the ERCF tables secret till January 1, 2022, so they don't show up in the FHFA 2021 Report to Congress.

Anyway, we didn't need the exact capital requirements while FnF had a long way to become fully Recap. It has never been an issue, although I had to start posting my estimation years before.

FHFA refuses to post the statutory Critical Capital level, more evidence that the Charter will be revoked, since in a post conservatorship world, FnF would be bound just by Basel, not by the FHEFSSA anymore.

Also, it's being carried out twisted, since the FHFA Director hints that the Capital requirements are met with the Net Worth called Capital Reserve, not with the regulatory Capital metrics the FHFA has just approved.

Let alone the Financial Statement fraud (gifted SPS absent from the Balance Sheets, in order to don't post the offset with Reduction of Retained Earnings, like occurred with the initial $1B SPS issued for free, debited from APIC at the time) with the objective to don't see that the adjusted available capital is far lower than the figures reported, already deep in the red (adjusted $-194 billion Core Capital combined)

A felony that you continue to provide the coverup, again in this post:

a growing leash of retaining earnings which the gses are meant to eventually break and go recap and release

In the run-up to FRIDAY's con operation by the attorney D.Thompson (Collins case. Also the attorney for Berkowitz, Rop, Bhatti, Robinson), it's necessary a paid shill corroborating his stance in court:

Mnuchin's NWS stop in 2019

a decisive turnaround that opened the way to recap/release.

as retained earnings continue

Yessir! You are getting it.

Corrupt plaintiffs plea deal negotiations resumed and concluded.

In a turn of events, both parties at the negotiation table (the DOJ and the Plaintiffs) plead GUILTY, for the coverup of the key statutory provisions and financial concepts.

Those peddling the Government theft story in formal documents are added up (Moelis and the sponsors of its plan to steal from us: John Paulson and BX; ACG Analytics; Pagliara; Howard; Bradford; Ackman; Financial Analysis Firms, etc.)

A $4.8 billion penalty on each counterparty in Punitive damages to the Equity holders (0.5% interest rate on the average spread Fair Value vs Market Price, during 15 years)

$1.94 in a $50 par value JPS and Common Stock, each.

It also settles the 9 Securities Law violations during Conservatorship.

CORRECTION: The section in the Charter enabling JPS, is the SEC.303, not 304(b) pointed out yesterday.

Though both overlap, as a JPS is an obligation (in respect of Capital Stock) and for the Capitalization (SEC.303), Basel requires the Preferred Stocks to be REDEEMABLE (callable) at the option of the issuer, which is what the SEC.304(b) is about: Redeemable obligations.

This is why all the series of JPS are redeemable stocks.

The bottom line is that the SPS (Equity) could have been purchased through subsection (b) redeemable obligations, and (c) at a rate similar to Treasury yields, as a cheap UST backup of FnF as a last resort, a feature contemplated in the section Purposes (Public Mission) of the Charter Act, as the operations can be financed both with Debt and Equity.

Not with (g) unlimited rate, inserted in the Charter by HERA (the bazooka requested by Paulson, as he stated in his book), trampling the Charter dynamics.

We use the unlimited rate (10%/NWS dividends) for the Separate Account plan, as dividends are restricted and there weren't Earnings available for distribution, out of a Retained Earnings account with deficit all along. There you go!

I'm talking about checks. The same check that makes you claim that FHFA is making progress, because you aren't talking about the Separate Account plan. You are just praising the FHFA and its Director once again, thinking that it will change the outcome.

Like peddling that FnF are retaining earnings, when they are wiped out with the offset attached to the SPS increased for free in the same amount.

You are cheering up this con operation with kind words, when also later there is concealment, as FnF aren't recording these gifted SPS (Financial Statement fraud) in order to don't post the offset with reduction of Retained Earnings.

Then, the attorney for Berkowitz, David Thompson, thanks to this Financial Statement fraud, seeks Constitutional Damages in court (Collins case. Next Friday), as the "for cause" removal restriction prevented this wonderland scenario where the UST gets rich with gifted SPS and FnF are recapitalized, from happening sooner firing Watt before.

This scenario is a bunch of lies, once the gifted SPS are recorded on the Balance Sheets.

YOU'VE GOT MAIL!

I uploaded the wrong screenshot with the subsection (g)

There you are.

Same subsection that enabled JPS, declares the SPS redeemable obligations.

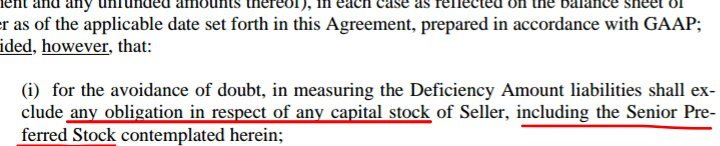

Obligations in respect of Capital Stock (SPSPA)

The Charter Act since its inception, gave UST in the subsection (c) the authority to purchase at a rate similar to Treasury yields, any of the obligations authorized in the subsection (b), which are redeemable obligations, such as JPS and SPS.

Redeemable obligations that can be repurchased "at any time and at any price" in the "open market", which is what FnF have done with the Separate Account plan, using the exception to the Restriction on Capital Distributions in the FHEFFSA.

Another important factor, these redeemable obligations must be redeemable at the option of the issuer, as seen with the JPS.

It was not until the amendment of the SPS Certificate of Designations, effective September 30, 2019 (in light of the September 27, 2019 SPSPA amendment), when it was incorporated for the first time:

3. Optional Pay Down of Liquidation Preference. Following termination of the Commitment. By that time, the SPS were already fully repaid long time ago (estimated at the end of 2013 in Freddie Mac. End of 2014 in Fannie Mae) with the aforementioned exception to the Restriction on Capital Distributions, like dividends.

Calabria and Mnuchin read that the Separate Account plan made sense and tried to thwart it. Then, the SCOTUS was activated. Both attempts failed.

The remaining SPS would be the $111B SPS increased for free, considered a joke by the Conservator, as they reduce the Core Capital and a breach of its Rehab Power (we don't see this effect due to the Financial Statement fraud in FnF: these gifted SPS are absent from the Balance Sheets, in order to avoid posting the offset with reduction of Retained Earnings account) and thus, the Common Equity is held in escrow awaiting unwinding this operation with the cancelation of these gifted SPS, that are also barred in the same Restriction on Capital Distributions that bars the dividends to UST, pointed out before, besides the payment of securities litigation claims.

This is part of the Charter dynamics in exchange for their Public Mission that makes them take on more credit risk and not properly compensated.

When things go sour, the government and the Congress can't void this UST backup that enables FnF to get low cost funding on the market, by inserting just below it in the Charter Act, with HERA, another subsection (g) with a Temporary Authority of UST to Purchase Obligations at an unlimited rate and in an unlimited amount, instead of simply having updated the obsolete $2.25B limit, set 60 years ago, when Fannie Mae had only $15B of Debt.

Then, skip the December 2009 deadline on purchases, with the Securities Law violations of SPS "increased", so there's been no purchase. Evidence of trickery.

In a final resolution, we blend everything together, not like the plotters that cling only to the amendments incorporated by HERA and the SPSPA, disregarding the rest of the law, making the original conditions prevail.

Conservatorship preserves their status as private corporations.

I'm not surprised to see that you and Bradford agree with Goldman Sachs' Mnuchin, contending that FnF will be "reprivatized" again, instead of saying "FnF will resume independent operations with the release from conservatorship".

Plenty of enemies on this message board, paid by the hedge funds and investment banks, that are making a killing.

YOU'VE GOT MAIL! The check has arrived.

Of course! Bradford agrees with his buddy navycmdr.

Both JPS holders and the subordinates of the hedge fund managers Bill Ackman and Tim Pagliara, respectively, that peddle the Government theft story and cover up the Financial Statement fraud in FnF with their slogan:

Navy commodore yesterday:

as retained earnings continue

Lamberth can't enter a court order. Judgment deferred due to the Restriction on Capital Distributions, like this payment of securities litigation judgments (CFR 1237.13)

Now they fake that the delay is due to the debate about prejudgment interests.

But capital distribution (Definition: CFR 1229.13) is also any dividend and today's SPS increased for free as of Sept 2019 and a onetime handout on December 2017, that wipe out the Retained Earnings that you were referencing to. Then, restricted too and the corrupt litigants' coverup of this restriction all along, is exposed.

We are waiting for an Administrative resolution.