Tuesday, September 12, 2023 3:20:53 AM

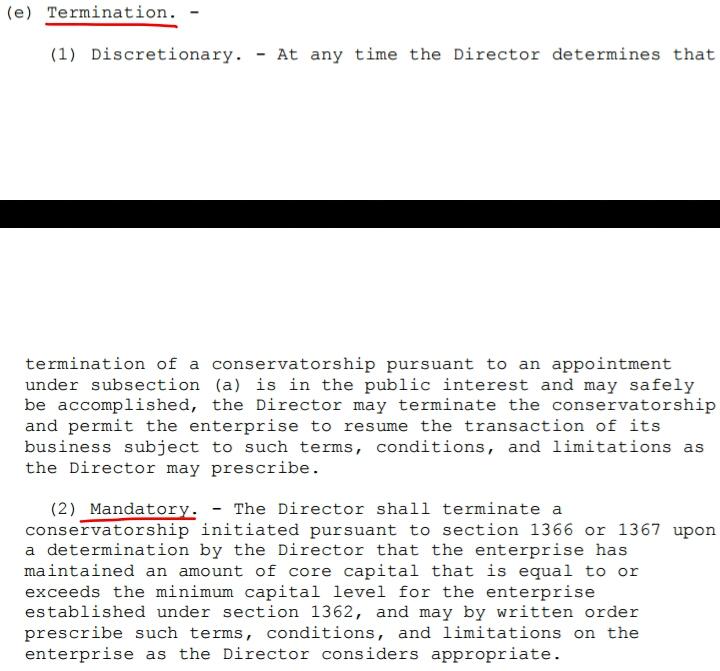

Although the mandatory release Undercapitalized (Core Capital > Min. Leverage Capital requirement (now 2.5% of Total Assets); or, with the new metric Tier 1 Capital > 2.5%. It implies that FnF have to build capital. Soundness. Rehab.) in the FHEFSSA, was struck by HERA,

...there is another law (Wall Street Reform And Consumer Protection Act, aka Dodd-Frank law) that required the UST to come out with "recommendations on ending the Conservatorships, no later than January 31, 2011", and it submitted a report to Congress along with HUD with a Housing Finance System revamp with 3 options for a Privatized System as the endpoint, which means Basel Framework for capital requirements or, as the option 3 states: "Stringent capital requirements" and thus, the Charter is revoked as the UST backup of FnF will no longer be necessary.

FHFA has been working hard since then, starting out soon after with these new initiatives:

Then, the UMBS, CSP, ....Resecuritizations, first priced at 50 bps to fulfill China's plan (Govt Explicit Guarantee) that I will comment next, but soon after it was switched for 9.375 bps that fulfills the original 2011 Housing Finance System plan, as this security enables the option 3: Govt Catastrophic-Loss reinsurance. Lastly, the Capital Rule (ERCF) adopting the Basel framework for the fully private sector as expected.

Trump and Mnuchin attempted to supplant this mandate by law, with Trump requesting to Mnuchin a new Housing Reform plan unveiled in September 2019, pursuant to a Presidential Memorandum, that envisioned a China-sponsored Housing Finance System with a Government Explicit Guarantee on MBS.

The attempt to supplant the 2011 mandate by law and subsequent Privatized Housing Finance System report to Congress, was also seen when Mnuchin claimed in his plan that:

Applicable law does not prescribe a specific end point for the conservatorship.

More deception and attempt to cover up the 2011 mandate, because it was precisely the UST the one in charge of putting an end point, at the request of the Dodd-Frank Law.

It doesn't mean that the FHFA has to wait till the day the Congress has to choose which of the 3 options is the ultimate Privatized Housing Finance System, where the Charter would be pointless, both the UST backup and their Public Mission is no longer necessary (Charter, revoked)

SECOND LIE. Howard claims that the release is established in the PA amendment by Mnuchin-Calabria that, one month before the effective date of the Capital Rule (February 16, 2021) came out with the rule: release from conservatorship when the CET1 > 3% of Total Assets.

Calabria should have looked at the prior mandatory release Undercapitalized in the FHEFSSA, that he helped to abolish when he crafted HERA: Tier 1 > 2.5% of Total Assets, because now he wants the release with a higher percentage of Total Assets and, secondly, with CET1 that doesn't include the JPS (Additional Tier 1 Capital). Tier 1 Capital = CET1 + AT1.

Howard, in his blog post, lies with this rule proposed by the Mnuchin's UST: Tier 1 Capital > 3%, and thus, only the percentage would be overstated with the prior 2.5%, when the truth is that Mnuchin proposed to be met with CET1, and thus, a more stringent capital requirement in both sides of the formulaic. Later he provides the correct information in brackets, subtracting the JPS, writing the wrong definition of Tier 1 Capital because he was writing the definition of CET1.

January 2021 letter agreements between former FHFA Director Calabria and former Treasury Secretary Mnuchin, specifying that neither can be released from conservatorship until they hold “tier 1 capital” (core capital, less junior preferred stock and a percentage of their deferred tax assets) equal to 3.0 percent of adjusted total assets.

Mnuchin was more interested in a conversion of the JPS from his buddy Berkowitz and Co, to Common Stock, to boost the CET1, and he didn't realize that his proposal was way overstated. Howard, a member of Berkowitz's legal team, attempted to cover it up.

THIRD LIE.

Fannie and Freddie must hold 4 percent-plus “bank-like” capital irrespective of the risks of the mortgages they guarantee

The capital requirement not based on risk is called Leverage Capital requirement, formerly Minimum Capital requirement.

It's Tier 1 Capital > 2.5% of Adjusted Total Assets, not 4% "bank-like".

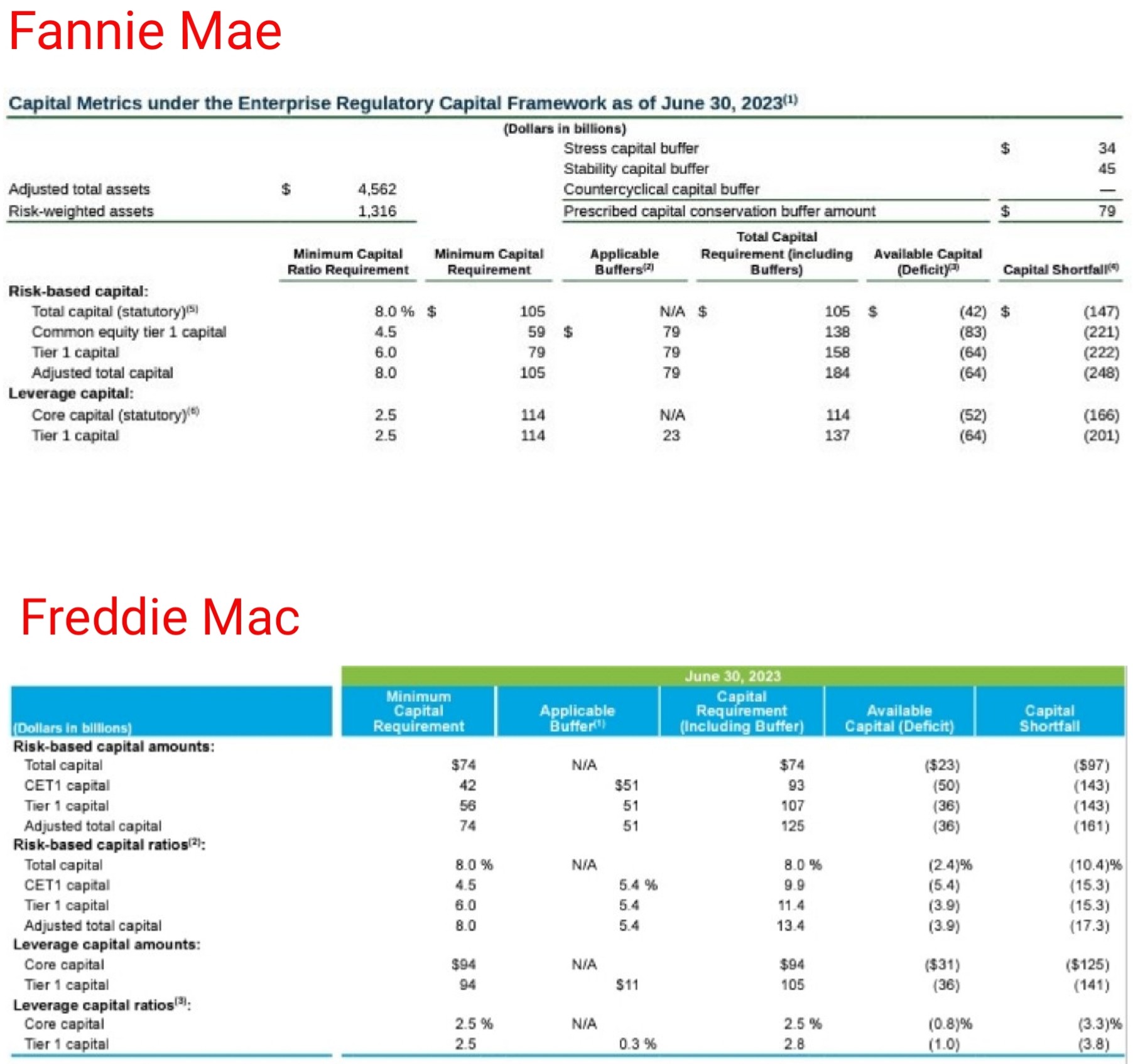

Not only the Capital Buffer isn't a capital requirement, but even if we consider it, we see in the ERCF tables that it's:

Freddie Mac: 2.8%

Fannie Mae: 3%

For the U.S. banks and without the Capital Buffer, it's 4%.

In the Basel Framework (an international standard), it's 3%, also without buffers.

This compares with 2.5% in FnF.

So, the 4% is wrong and the "bank-like" too.

Remember that Howard was the former FNMA CFO expelled from the company for cheating. Accounting fraud to boost his EPS target bonus.

He also repurchased $7.4 billion worth of common stock to that end (they aren't accounted for, for the EPS) that still shows up on the balance sheets as reduction of Equity (called Treasury Stock) and reduction of Core Capital (it reduces the common stock par value)

Likely, it was one of the reasons for the conservatorship. Fannie Mae would have had $7.4 billion more Core Capital in the absence of this investment contrary to the company's statutory Public Mission (Charter Act)

He was allowed to keep the ill-gotten money the S.E.C. accused him of.

I think we know the answer as to why.

Treasury Stock (buybacks)

VAYK Exited Caribbean Investments for $320,000 Profit • VAYK • Jun 27, 2024 9:00 AM

North Bay Resources Announces Successful Flotation Cell Test at Bishop Gold Mill, Inyo County, California • NBRI • Jun 27, 2024 9:00 AM

Branded Legacy, Inc. and Hemp Emu Announce Strategic Partnership to Enhance CBD Product Manufacturing • BLEG • Jun 27, 2024 8:30 AM

POET Wins "Best Optical AI Solution" in 2024 AI Breakthrough Awards Program • POET • Jun 26, 2024 10:09 AM

HealthLynked Promotes Bill Crupi to Chief Operating Officer • HLYK • Jun 26, 2024 8:00 AM

Bantec's Howco Short Term Department of Defense Contract Wins Will Exceed $1,100,000 for the current Quarter • BANT • Jun 25, 2024 10:00 AM