Saturday, September 09, 2023 3:01:09 AM

Your attempts to pass a Conservatorship off as Nationalization, only shows that you want to rip off the shareholders.

It's pretty obvious that you are here paid by the hedge funds to repeat the slogan of Nationalization over and over again.

A lie repeated a thousand times, is still a lie.

Our powers and rights are transferred to the conservator to help it fulfill its statutory mission. It's not a Nationalization for the control of enterprises, Argentinean YPF-style.

Not only a Conservatorship bars a subtle nationalization attempt, as the Supreme Court stated with "the rehabilitation of FnF" as the endgame according to the law, paraphrasing his colleague judge Willett that interpreted the "authorized by this section" when the Incidental Power states: "Take any action authorized by this section", with "actions within the enumerated powers" (the Conservator's Rehab Power), but also the Charter Act bars the UST from any attempt to make profits using the securities and assets of FnF, as part of the Charter dynamics.

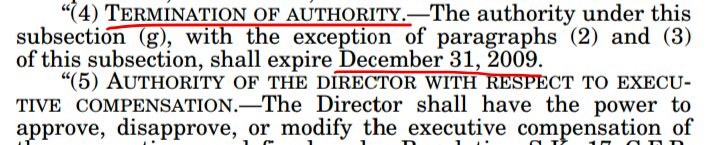

Nothing changed "as of the passage of HERA", as the DOJ attorney stated in his recent reply to Fisher, with the subsecton (g) a TEMPORARY authority that expired on December 31, 2009, and taking into account the rest of the laws.

Besides, the purchase of securities had the purpose of 3 prerequisites. The objective was never the taking of the property of FnF, as the DOJ attorney stated.

A redeemable obligation in the original UST backup of FnF, means that the intention of the legislator is that the UST can't overstay in FnF.

A Takings should be duly announced and our stocks taken away. The fair compensation for our stocks is their fair value today, adjusted for all the unlawful actions (Fake NWS dividend for Rehab. Remember? Otherwise a capital distribution restricted, barred and unavailable Earnings for distribution out of an Accumulated Deficit in their Retained Earnings account). That is, under the Separate Account plan up and running since day one, as seen in my signature image below. It's not a resolution today changing the past, with "What if...." as some people nowadays come up with.

The stocks' fair value is their Book Value, which in the case of the Cs is the Common Equity and in the case of the JPS, is their par value, taking into account that FnF would have been Adequately Capitalized and the dividend resumed (When the Tier 1 Capital met 25% of the Prescribed Capital Buffer. Table 8) since the 3Q2022 earnings report in the case of Fannie Mae and one year before in the case of Freddie Mac.

Consistent with the idea that in a Takings, at least the UST has to return to their Equity holders their money (Book Value)

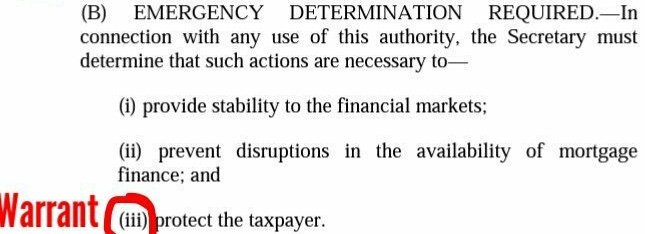

A retrospective Nationalization doesn't exist. So, a Takings price today is assessed with the Book Value as of end of June, 2023, as shown in their adjusted Balance Sheets, adjusted for all the operations to misrepresent their financial condition, like the absence of the PLMBS lawsuit settlement and the CRT expenses, barred in the Charter's Credit Enhancement clause and a breach of the FHFA-C's Rehab Power. The "protect the taxpayer" rhetoric is a big lie. The taxpayer doesn't bear credit risk to begin with and FnF are protected building Capital, not paying for insurance.

A Takings in the middle of a Conservatorship would have been considered an opportunistic Takings. So, now that FnF should be released under the Separate Account plan, it's the moment to do it, otherwise the UST-FHFA refund the $152B cash due and FnF resume independent operations, when FnF would start trading at a PER 14 times or greater if there is Accounting Standard change in the Deferred Income.

In the meantime, the Common Equity keeps on being earmarked for the common shareholders as usual.

Last Shot Hydration Drink Announced as Official Sponsor of Red River Athletic Conference • EQLB • Jun 20, 2024 2:38 PM

ATWEC Announces Major Acquisition and Lays Out Strategic Growth Plans • ATWT • Jun 20, 2024 7:09 AM

North Bay Resources Announces Composite Assays of 0.53 and 0.44 Troy Ounces per Ton Gold in Trenches B + C at Fran Gold, British Columbia • NBRI • Jun 18, 2024 9:18 AM

VAYK Assembling New Management Team for $64 Billion Domestic Market • VAYK • Jun 18, 2024 9:00 AM

Fifty 1 Labs, Inc Announces Acquisition of Drago Knives, LLC • CAFI • Jun 18, 2024 8:45 AM

Hydromer Announces Attainment of ISO 13485 Certification • HYDI • Jun 17, 2024 9:22 AM