News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Quit asking for

"fair treatment for all GSE JPS and Common shareholders".

A conservatorship isn't an "administrative bankruptcy", stated by the ambitious Mark Calabria, who had the conviction that he doesn't like private shareholders benefiting from a UST backup of congressionally-chartered private corporations.

Bankruptcy is for debt restructurings.

Conservatorship is meant for the financial rehabilitation of enterprises. This is why the management and BOD is expelled and it's appointed a conservator in their place, who needs the rights and powers from the shareholders as well, to carry out its statutory mission, otherwise they would oppose to every action, ASMs, etc.

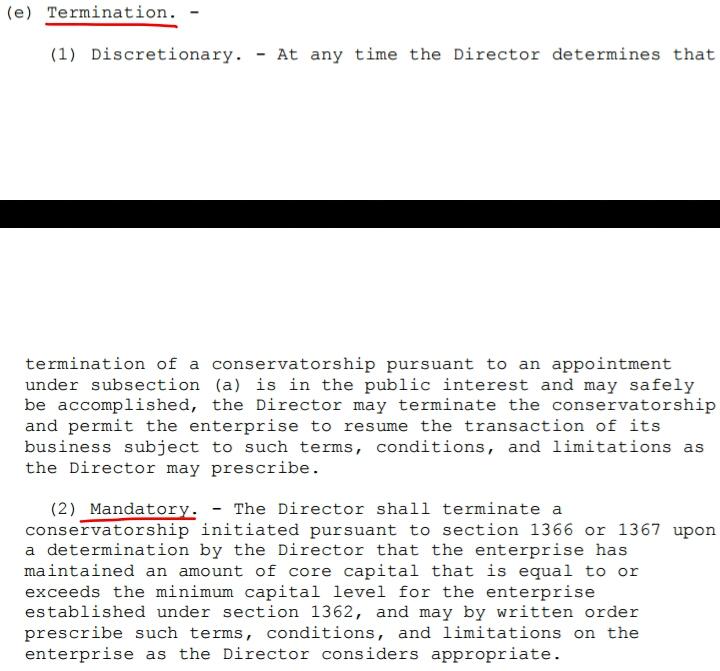

This is why there is a MANDATORY release Undercapitalized (Core Capital > Minimum Leverage Capital requirement). It can't overstep.

Calabria struck this MANDATORY release in the FHEFSSA with HERA.

It doesn't mean that, all of a sudden, now a Conservatorship is a state to induce bankruptcy or Receivership, 15 years into a Machiavellian plan of deception, because the key 2 points in the prior FHEFSSA conservatorship prevail, so don't think about repealing HERA and return to the prior FHEFSSA:

-Capital Restoration Plan.

-Restriction on Capital Distribution.

Today's FHEFSSA conservatorship, as amended by HERA, states the same in the conservator's Rehab Power: "Put FnF in a sound and solvent condition", when "soundness" is related to building regulatory capital,

Regarding the Restriction on Capital Distribution, HERA placed it at the end of the section Capital Classifications of the FHEFSSA, and it applies "IN GENERAL" when FnF are undercapitalized. Let alone in a Conservatorship for Critically Undercapitalized enterprises.

Calabria wanted the companies in Receivership in 2008. This is why he came up with a Final Rule entitled "Resolution Planning" in mid 2021, which is "Receivership scheming". Such a bad taste during a Deceivership.

Our enemy pro se plaintiff Joshua Angel, a JPS holder, continues his bad performance in the U.S. courts, requesting on Wednesday permission to amend his 4th complaint in the DC courts, navycmdr posted on Twitter.

An attorney chosen also for the Madoff case aiming to spin undervalued assets off to his gang. It can't be just a coincidence.

And who, in this board, pretends to defend the shareholders, asking now for debt forgiveness Argentina-style, so he can sneak a 10% dividend in a negotiation, where dividends are called "interests" to skip the Restriction on Capital Distributions, and calling it "contractual rate". It turns out that it's as "contractual" as the NWS dividend. Duh!. A negotiation controversial attorney Bryndon Fisher-style.

This is why kthomp19 brought up on Wednesday the themes of "administrative bankruptcy" by Calabria and the "legacy shareholders" by Pagliara.

We are dealing with an organized group.

The plaintiff Joshua Angel has to call the NWS dividend "NWS", because dividends are restricted and, because we cannot undo what's already been done, it's applied towards the exceptions to this restriction to legalize it, thanks to the FHFA-C's Incidental Power that authorizes this plan of deception. The same with the 10% dividend (Restricted and unavailable earnings for distribution as dividends).

"HERA" instead of the "FHEFSSA", so other provisions are concealed. For instance, that the capital requirements are met with Core Capital, currently adjusted $-194B, not with "Capital Reserve", which is an adjusted $0 by the way.

A negotiation cattle market-style, where no rule has existed before, as we can read in his daily comments on Ihub with his 20+ aliases.

Attempt to conceal the reality of the Separate Account plan, with assessments sent to Treasury under the guise of dividend payments, in accordance with the law, rules and basic finance.

The key: the original low cost financing of the operations by the Treasury (both debt and Equity), as a last resort (image below), in the Charter Act, prevails.

With CET1 > 2.5% of Adjusted Total Assets as of September 30, 2023, now the Charters can be revoked and Calabria's wish comes true.

Complying with the Fee Limitation of the United States in the Charter Act, that Calabria also conveniently forgot.

I thought that the rogue kthomp19 was "kthaput19" after being called out for attempting to mislead this board, stating that the statutory Restriction on Capital Distributions doesn't apply, because it says that it's for enterprises "classified Undercapitalized", when it states "undercapitalized" in general, and it starts with: "IN GENERAL". Source.

First of all, this rogue attorney doesn't understand that this restriction is a Prompt Corrective Action to rehabilitate a financial company. That is, to build capital. A financial concept. It was explained by the FHFA in the famous Final Rule of July 20, 2011 in relation to a response to the payment of Securities Litigation judgements, now in the Lamberth court, but it can be extended as an explanation of all the Conservatorship. Source.

Section in HERA that amended the FHEFSSA in question:

Unlike a different FHEFSSA restriction on capital distribution (an expense unrelated to the normal business of FnF) with the 4.2 bps sent to UST/HUD's Affordable Housing trusts, where it states "classified undercapitalized" (Source) and now, there aren't Capital Classifications. The reason why FHFA's Mel Watt lifted the suspension in December 2014, presumably when he declared FnF in solvent condition, complying with one of his statutory goals as conservator (Put FnF in a sound -capital- and solvent -debenture SPS- condition), and also, it's assumed that it was satisfied another specific exception to its restriction: "it wouldn't contribute to the financial instability of FnF", at a time when it's estimated that the laggard Fannie Mae ended the reduction of the SPS in full, in turn, pursuant to the exception (reduce the SPS) the different general Restriction on Capital Distributions mentioned before (Dividends, today's SPS LP increased for free and the Lamberth rebate)

It's estimated that Freddie Mac repaid its SPS one year earlier (watch my signature image below).

Therefore, the rogue attorney Kthomp19 lied about this general Restriction on Capital Distributions, mixing it up with the specific one on the 4.2bps.

The one in question is for undercapitalized enterprises, like today that "FnF remain undercapitalized" (Sandra Thompson). The grounds for a Separate Account.

Let alone his: "The SCOTUS authorized the NWS dividend" (knowing that the 2nd UST backup of FnF authorizes an infinite dividend rate on SPS), without pointing out that it also stated that it must "rehabilitate FnF", which means that, in reality, it authorized a Separate Account plan for the extortion of the enterprises in the meantime, that is what is rehabilitating FnF for real (Regulatory and statutory capital metrics; On the balance sheet, not "off-balance sheet" which, if any -MBS Trusts-, is consolidated on the balance sheet).

Yet on Wednesday, he started the "legacy shareholders" diatribe, a concept that doesn't exist, neither as financial term nor as legal term, the reason why all the members of the gang repeated it yesterday, at least ten times, seeking the "treat the stocks" peddled by Pagliara & Co: "Thanks for sharing", "Everyone must win", etc.. That is, all made up in a cattle market-style negotiation with the government.

Everyone will get what is entitled to according to the specifications of the security they bought. That is, stock valuation.

It's always "existing shareholders" in any event.

Plotters' invalid term "legacy shareholders" aims to pitch an invalid idea of stocks treated🆚stock valuation,OK'd w/ ST:"I defer to Congress"🆚prior "work w/ Congress".

— Conservatives against Trump (@CarlosVignote) February 1, 2024

It's "existing shareholder", awaiting the return of Powers/Rights in use by FHFA-C as I write this.#Fanniegate pic.twitter.com/CxJrd5vBvb

That 'European' is Glen Bradford, alias "European farmer LuLeVan".

Your in a discussion with a person ‘European’,

FNMA posts 2 consecutive monthly volume declines. FMCC, winning!

Annualized month-on-month growth in November and December:

Fannie Mae: -0.4% and almost flat.

Freddie Mac: +2.4% and +3.1%.

This slams all those in Wall Street promoting the idea of a combined FnF (Goldman Sachs, GS alumni Sandra Thompson with the FNMA HQ lease contract terminated this month, 5 years before the deadline "if it's significantly changed", the media published at the time it was signed, etc.)

It's been proven that there is a benefit from the competition between FnF.

This is because Fannie Mae found a new revenue stream with the extortion of money from Freddie Mac, under the guise of normal operations, with the commingled securities. A catastrophic-loss reinsurance that Freddie Mac is being forced to buy in order to sell its products, when there is no need. Latest: $105 billion, net, at 9.375 bps.

These "resecuritizations" unveiled by Freddie Mac in June 2022, are meant to bring in private capital in the Guaranty Mortgage Securitization business, helping them to sell their products (UMBSs) and compete with FnF on a level playing field.

It could be a Govt Catastrophic-Loss Reinsurance for the option 3 in the UST Privatized Housing Finance System revamp, chosen for the release from Conservatorship in 2011. Or private reinsurance for the options 1 and 2.

More ways to spin funds off to one company of the gang: now Fannie Mae. That's why the "deregulation segment in Fannie Mae", promoted by Goldman Sachs commented before, that secures good deals for them (sale of undervalued assets), and later this revenue stream makes up for the losses.

Other examples: CRTs, Bitcoin scam, IMF-Argentina spree,...

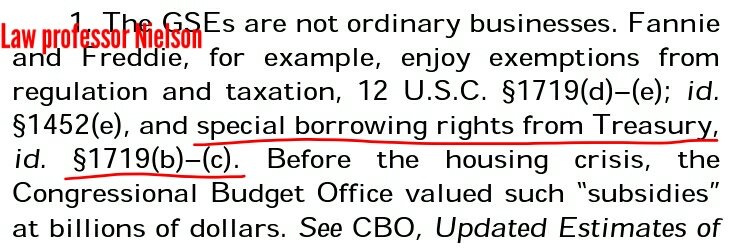

Goldman Sachs doesn't get that our only category is:

NOT ORDINARY BUSINESSES.

Supreme Court-appointed amicus:

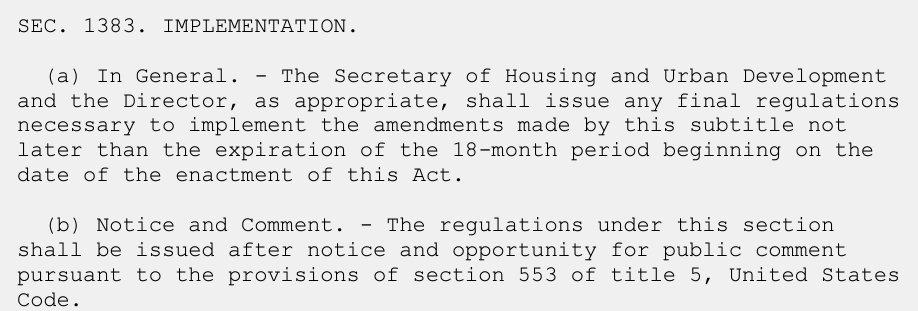

With "de-regulation (sic) category", Goldman Sachs covers everything up, beginning with the 2011 UST Privatized Housing Finance System endgame (guarantee fee increases, Basel framework,...), chosen for the release from Conservatorship, at the request of the Dodd-Frank law. A Report to Congress.

Then, the FHEFSSA capital metrics, as seen also in the BTIG report, a subsidiary of Goldman Sachs, commented yesterday. Etc.

This is why GS now comes out with "easing the Capital Rule" stance.

A two-pronged attack. Or one attack if it's the same conglomerate.

The problem isn't "deregulation", because today's Basel framework for capital requirements is an international standard, but the current adjusted $-194 billion Core Capital together.

The reason why there is a 20% Risk Weight floor to calculate the Risk-Based Capital requirement, which is the only addition by regulation albeit authorized by Basel rules, is because of the "Capital covers unexpected losses" that BTIG said it all wrong (commented as well), because it leads to a capital level for the long haul, and not subject to the current pristine portfolios in FnF, with an average Current LTV of 58%.

For that, there is a different analysis called Stress Test, published annually and required by the Dodd-Frank law.

Anyway, there is also a Minimum Leverage capital requirement higher than the Risk-Based Capital requirement. So, no matter how low the latter is (deregulation), the binding capital is still the Leverage ratio (Core Capital > 2.5% of Adjusted Total Assets).

This is why Howard only complains about the Risk-Based Capital requirement and conceals the other, pretending that it doesn't exist, so the problem of FnF now is only "deregulation", instead of the real problem which is a Separate Account plan and that $420B of core capital generated during Conservatorship is currently missing on their adjusted Balance Sheets.

Timothy Howard is behind this attack by Goldman Sachs/BTIG for sure.

Hand-in-hand with the plaintiff Joshua Angel entertaining the shareholders on the Ihub message board with his deranged posts using 20+ aliases, that make our heads spin.

A phone call from the DOJ will clear things up.

Now, GS forms part of the pot liable for $4.8 billion in Punitive damages as compensation to the Equity holders, along with all others that have written the government theft story in formal documents: Moelis and sponsors, Ackman, Howard, Pagliara, the plaintiffs, etc.

Collusion.

Rodney/Barron +20, is the plaintiff J.Angel writing flawed analyses.

I already warned the board that his objective is to tarnish the image of other posters that might be posting valid analyses and also, to make our heads spin.

Which is what you are attempting too, in your reply to him, so that only the frivolous lawsuits that have been filed so far, are valid.

repetition of groundless legal theories.

If you think their arguments have merit, you should file suit.

FnF forced to issue Warrant @0.00001ps for profit? GROSS!

It wouldn't make it to a movie. Get a grip.

The warrants are the equity ROI.

Shameful attempt to distort the Separate Account plan by the rogue plaintiff Joshua Angel, with one of his 20+ aliases on this board.

- Is it "NWS" or NWS dividend?

- Is it "interests" or dividends?

- Is it "HERA" or the FHEFSSA?

- Is the exception to the Restriction on Capital Distribution in the law "a refinancing option", or it simply requires to raise cash in the same amount of SPS reduction, which was satisfied when the Common Equity was increased at the same time? By the way, the same scheme in the Federal Reserve with their fraudulent Deferred Asset that substitutes the SPS: it's reduced as the Retained Earnings increases, so the remittances to Treasury can resume. What FnF have done with the SPS under the Separate Account plan (watch my signature image below with Freddie Mac)

In the end, what the gang attempts is what the controversial Bryndon Fisher already pointed out: "What if the NWS dividend hadn't existed?", as a way to pitch the payment of a 10% dividend. He still doesn't get that it's restricted too and the same breach of the FHFA-C's Rehab power, when rehab means to build regulatory capital in this world (soundness).

The NWS dividend existed, and you can't undo what's already been done.

The reality is that no actual dividend was ever paid to Treasury, with unavailable earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings account, and a capital distribution restricted. The exceptions in the law/CFR kicked off.

They were assessments sent to Treasury, misleading about it under the FHFA's Incidental Power: "Zing!".

Similar to the FHLB's Separate Account in 1989 by law, because now it's been extended for the Recapitalization.

Likewise, the paid shills yesterday with: "What if HERA hadn't existed?"

It's been an exceptional exercise of rulemaking to commit fraud with the enterprises and their Equity holders.

2008 HERA isn't to blame when it's been active rulemaking to the same end, with the July 20, 2011 CFR 1237.12 by DeMarco, that enabled the continuation of the Separate Account with capital distributions (deplete capital) for their Recapitalization (build capital), for the moment that the prior exception in the law, repaid the SPS in full.

And Trump and Mel Watt actively seeking all that is prohibited as well, to continue the plan of deception: the dividends stopped. Instead, SPS increased for free, which is the same. Another capital distribution number (1): a compensation with stocks, other than stock dividends. RESTRICTED. Then, another way to hold the Common Equity in escrow to legalize this payment.

Playing the fool is an aggravating circumstance when assessing the penalties for Punitive damages: "Mandatory dividends"; The almighty and omnipresent attorney David Thompson: "I'm not a securities lawyer"; "Sep-p-p...Separate whaa?"; "Interests"; "HERA"; Etc.

All comes down to Regulatory Risk and stock valuation.

Non-negotiable.

I didn't know that Howard now works for BTIG.

An investment bank owned by Goldman Sachs, by the way.

They repeat the same stance peddled by the controversial Howard:

-Howard has always repeated that the latest RFI on the recent LLPA changes, was about changes in the capital requirements and even he submitted a comment about it. Focus, it was LLPA changes.

-They don't know that Capital is meant to cover future unexpected losses, as the expected losses have already been fully reserved in the Allowance for Loan Losses (CECL Accounting standard since January 2020). The report requires a g-fee for the capital that covers expected losses.

-The guarantee fees aren't assessed based on a required ROE. Primarily, the ROE is distorted when there are JPS, as they have their return capped at their dividend rate (Fixed-income securities). Therefore, when you see that JPM has a ROE of 10%, it might be ROE of 20% (a normal ROE for a common stock) and the ROE of the JPS capped at a 7% dividend rate. You can't mix up apples with oranges, making JPS and Cs equivalent securities, which is what these people always attempt.

-Once again pointing out that the future earnings must be recorded as Capital. Clueless about basic concepts because all the exercise of Capital requirements is meant to know how a company can tackle future losses with the picture of the company TODAY (as seen on the Balance Sheet). Not in the future. Today. You can try a different theoretical exercise but then, it will be a second analysis because this one prevails. So, BTIG's Howard still doesn't understand what the capital requirements are for. The guy that repurchased FNMA common stock that reduces the core capital, to boost his EPS target bonus, as seen today ($7B Treasury Stock)

-The minimum Leverage capital requirement stands at $208B. Then, it's not $400B and later, $300B, as they point out. The capital buffers aren't a capital requirement. This threshold is met with Core Capital.

-The Core Capital as of September 30, 2023, stands at $-76B officially in their ERCF tables, and it drops to $-194B adjusted for the offset (reduction of Retained Earnings account) attached to the $118B SPS LP increased for free absent from the balance sheets. Yet, BTIG's Howard claims that their capital today is $100B+, which refers to the $118B Capital Reserve, notwithstanding that the Capital Reserve drops to $0 with the offset pointed out before. Above all, the Capital Reserve isn't a valid capital metric under the FHEFSSA. So, wrong capital metric and badly assessed. More evidence of con operation.

-Exercise the Warrant, without pointing out why this security was authorized in the law in the first place, as FnF are NOT ordinary businesses.

-Let alone that capital distributions are restricted (dividends and today's SPS LP increased for free)

These people aren't serious. Stock price manipulation.

No phone call from the DOJ yet, plaintiff Joshua Angel?

Then, you will understand what "SEPARATE" and "ACCOUNT" mean, necessary to uphold the law, rules and basic Finance.

Timothy Howard: "Separate Account? I don't know what that is."

Sep...pr, prrrrr...p, p,. ...Separate, whaaa?

.jpeg)

Beware of scammers that mix up the amendments of the SPS certificate (prospectus) with the amendments of the SPSPA.

Let alone Glen Bradford that calls the SPS "SPSPA".

The SPS certificate is usually amended a few weeks after a SPSPA amendment or whenever they want, because what the plotters call "4th amendment", is the 4th amendment of the SPS certificate dated April 2021, in light of the January 14, 2021 6th amendment of the SPSPA, called 3rd Letter Agreement, currently in force (the latest with regard to compensations to UST)

The plotters mess around with the names because secretary Yellen was sworn in on January 26, 2021, and thus, unrelated to the January 14, 2021 SPSPA amendment.

This is why they talk about the 4th (SPS Certificate) amendment, of April 2021, that didn't need the OK from Yellen.

Summary:https://www.fhfa.gov/Conservatorship/Pages/Senior-Preferred-Stock-Purchase-Agreements.aspx

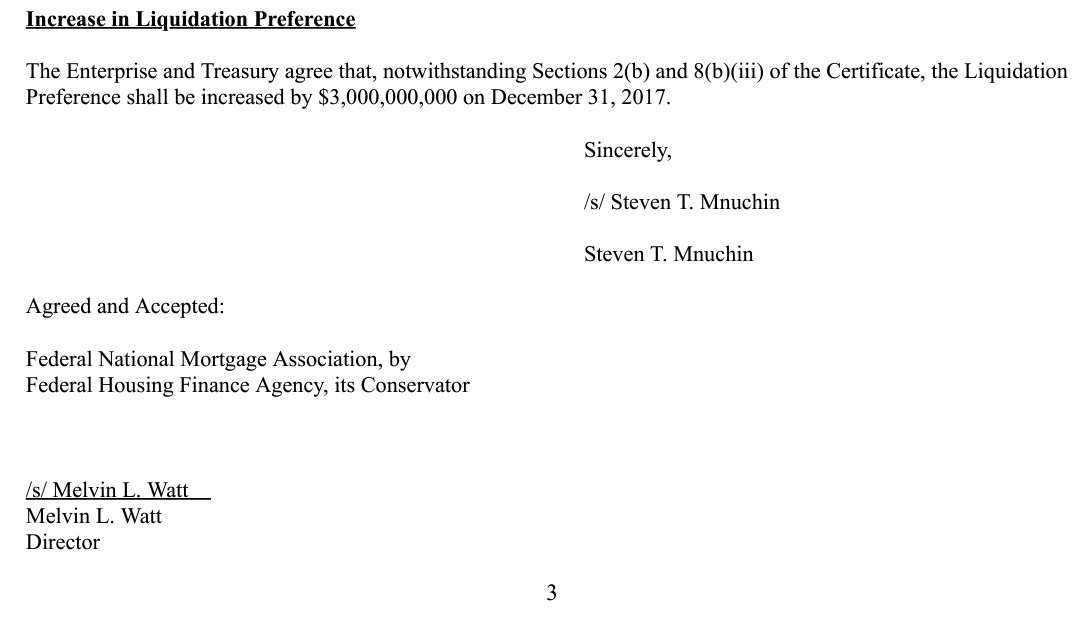

The September 2019 "Letter Agreement" would be the 5th amendment of the SPSPA, because there was one before, on December 2017 by the allies Watt-Mnuchin (concealed to seek constitutional damages for the "for cause" removal restriction), that kick-started the current Financial Statement fraud with a one-time $3B SPS LP increased for free out of the blue, absent from the Balance Sheets, along with its offset (Reduction of the Retained Earnings account)

With the 5th amendment, the SPS LP increased for free doesn't emerge as a result of the cumulative dividend when it isn't paid with cash, stipulated in a SPSPA covenant (the only way a LP can be increased, otherwise new SPS had to be issued for each draw from the UST). The thing is that the dividend was terminated, as a consequence of judge Willett's ruling in the Collins case 3 weeks before (5th Circuit en banc), contending that the conservator exceeded its powers. And it's a brand new compensation to UST, laid out in this brand new covenant:

Not a dividend but another capital distribution in its FHEFSSA definition (1) compensation with stocks, other than a dividend.

Then, the same Restriction on Capital Distributions and the same we do to legalize this action: it's applied towards the exceptions. In this case, for the Recapitalization (CFR 1237.12). That is, necessarily the Common Equity is held in escrow, which also complies with the FHFA-C's Rehab power (soundness). Easily seen with the aforementioned offset, had the SPS LP increased for free and the offset, been posted on the Balance Sheet.

Everything is adjusted (Image). So, nice try and now pay damages.

The moment that Mnuchin made clear in a press release that the dividends were terminated to all effects.

BOTTOM LINE

Trump and Mnuchin participated actively in the continuation of the Separate Account plan, both with Mel Watt and with Calabria.

All of them expect the Congress to undo what's already been done and "treat the stocks".

Or, the return of Trump to finish them off, along with holding up all other scams worldwide:

-Argentina-IMF spree.

-Fraudulent European Central Banks' Payment Systems Target2 and TIPS (External Positions)

-BOE's stamp on loans to foreigners.

-The S.E.C.-sponsored unbacked token scam.

-CRTs in FnF.

-Etc.

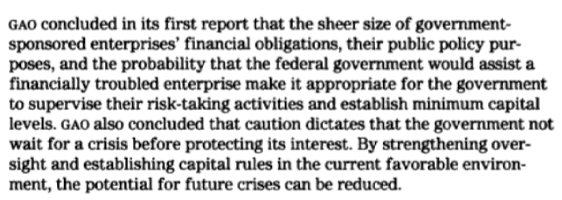

Can't you see that Geithner submitted a Privatized Housing Finance System for the release of FnF from Conservatorship, at the request of the Dodd-Frank law? Guarantee fee increases, Basel framework for capital standards, a 3-option Housing Finance System revamp.

The same as before. The only difference is that the FHEFSSA MANDATORY release Undercapitalized, stripped out, now is much higher (Basel Framework) and it isn't mandatory anymore.

Hence, the overtime aiming to get rid of the unwanted AT1 capital instruments (JPSs). And that's achieved only when the CET1 > 2.5% of the Adjusted Total Assets (Compliance with Tier 1 Capital > 2.5% of ATA later). A threshold fetched by the laggard Fannie Mae in the Q3 2023. It could have been done outside the Conservatorship but, somehow, the FHFA wanted to get rid of them before, "in its best interests".

The aspects that are lawful can't be "treated" with the stocks (the sought-after rebate). Only the unlawful parts with the enterprises, like the $151B cash refund and a posting in the Retained Earnings accounts.

The Equity holders are only entitled to a compensation for the Securities Law violations and the con operation in the U.S. courts.

The endgame is Charter revoked, as the UST backup of FnF will no longer be necessary. All their privileges would have been removed. That's the Privatized Housing Finance System.

Regulatory Risk.

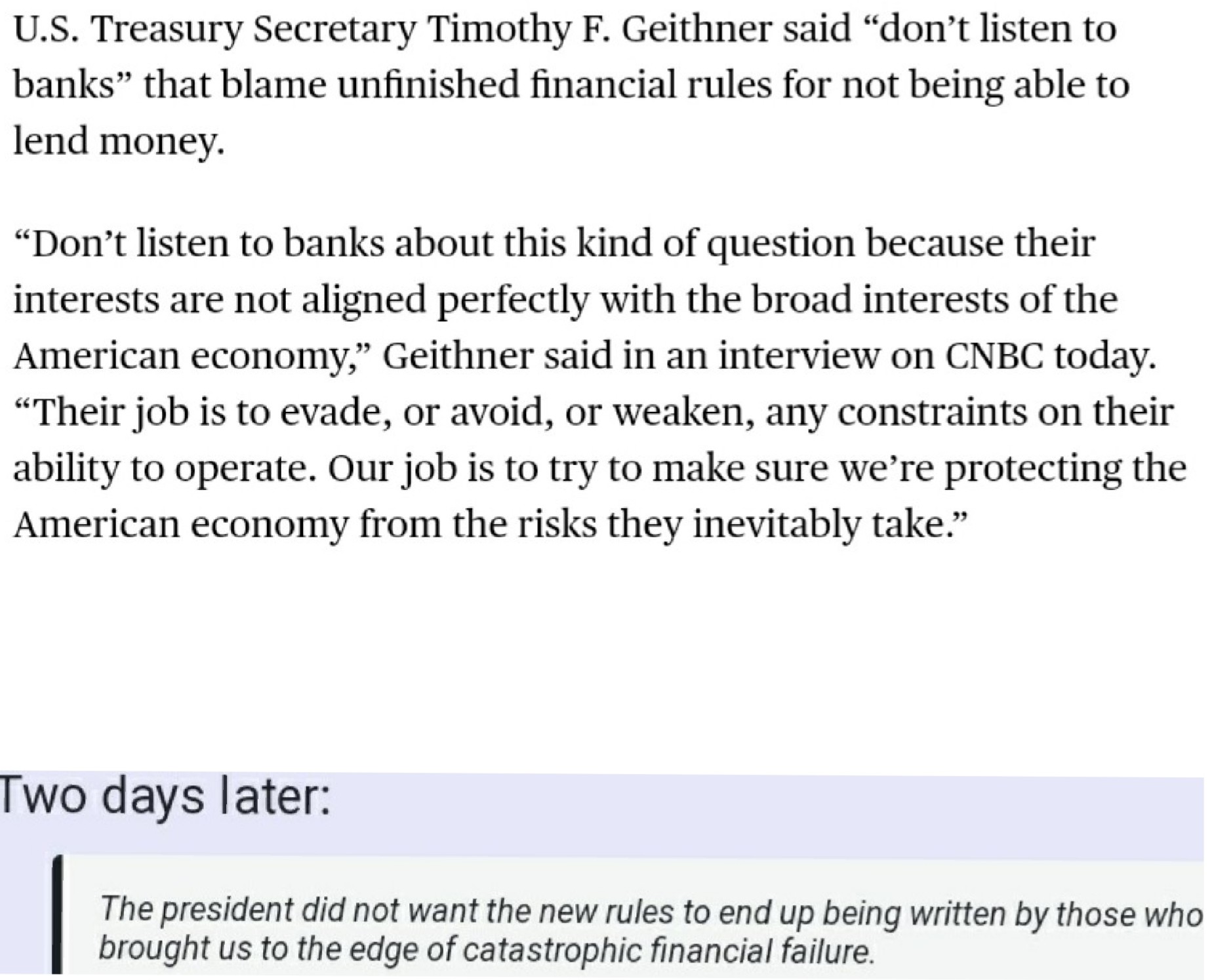

Seems a little like BS. Wasn't Geithner one of the architects of our current morass?

That's off-topic. Get a grip, Glen Bradford.

Don't listen to banks.

Don't listen to China.

Don't listen to Bloomberg/CNBC.

Treasury was wrong in its assertion that HERA, in an amendment of the Charter Act, granted it authority to purchase MBSs from Wall Street on the secondary market, in order to allow them to lock in the huge rally in price when the interest rates plummeted.

More trickery and evidence of attempt to twist the Charter Act, concealing the reality of a UST backup of FnF to finance their operations (MBSs in the TBA market or SPS), replica of the one since the Charter's inception at rates similar to Treasuries, that is the one we use in a final resolution (0.5% spread over Treasuries. A weighted-average 1.8% cumulative dividend on the SPS).

Explained in these two tweets:

Max TARP was $700B.

— Conservatives against Trump (@CarlosVignote) January 28, 2024

Down to $475B in the 2010 Dodd-Frank law.

They knew that the $221B in MBS till Dec 2009 that UST claims its authority in the Charter was about(inserted by HERA),was wrong.

It should've been TARP.

Charter =backup of FnF(MBS/SPS), not MBS held by BLK.#Fanniegate https://t.co/c2ufUoXzuS pic.twitter.com/bWLzqhJ1wW

When will the conservatorship end?

No genuine dispute remains on the fact of harm on the theory of plaintiffs were denied dividends that they otherwise were reasonably certain to receive.

.jpeg)

This bystandard doesn't know there is a Warrant prospectus.

And he had to ask:

Do you know what date the Warrants expire?

There aren't "11,000 secret documents". Everything is set forth in the law, rules and basic finance. And this isn't about "theories".

You've got it all messed up (HERA, TARP, the Charter Act,...), plaintiff Joshua Angel with your 20+ aliases on this board, with the objective to make our heads spin.

These 2 tweets give response to your jumble.

Why on earth would appear in the Charter an authority of UST to buy obligations on the secondary mkt?

— Conservatives against Trump (@CarlosVignote) January 27, 2024

That's unrelated to FnF.

2nd goal: to conceal that, with HERA's inclusion, now 2 homonymous UST backups of FnF in the Charter:"Authority of UST..." Low/high rates.@TheJusticeDept

It's called "UST backup of FnF". Keep the fancy names

"this looked like a guarantee or insurance policy"

The operations thereof shall be financed by private capital to the maximum extent feasible

The HERA legislation granted temporary authority to the Treasury to purchase obligations of the Enterprise

Their adjusted Capital Reserve is $0.

Now that they have built up a TON of Cash reserves.

$100B+ cash Equity. Chooo Chooo.

FLAWED CAPITAL STANDARD. BADLY ASSESSED

— Conservatives against Trump (@CarlosVignote) January 26, 2024

The #Fed's C.Surplus is the amount of Net Worth above C.Stock, fixed at $6,785mll by law. Hence,DA(losses) fraud,to not deplete it.#Fanniegate

The plotters' C.Reserve=$118B. But $118B SPS LP absent from the Bce Sheets.

Hence,adjusted CR=$0 https://t.co/d6q7TMeSBS pic.twitter.com/C7CV7OoJzh

The sacking of enterprises,unacceptable under the Rule of Law.

The Warrant was a SPS collateral if we...

This reply to navycmdr appears on the Freddie Mac board.

Here.

It's worth stressing that the taxpayer's assistance MUST be repaid asap.

Although the Preferred Stocks are permanent securities, they are always redeemable at the option of the issuer.

Although we don't have redemption dates with the SPS, unlike the JPS, they were simply reduced with the assessments sent to Treasury under the guise of dividend payments (restricted and unavailable earnings for distribution), in accordance with the Law (exception to the Restriction on Capital Distribution)

Mnuchin attempted to thwart the Separate Account plan, adding in the September 2019 SPSPA amendment, a new covenant "Optional Pay Down of Liquidation Preference Following termination of the Commitment".

Too late! (Besides ill-conceived, as the taxpayer's assistance must be paid down asap). The SPS LP corresponding to the draws from UST, was long gone.

Today's SPS LP increases for free (restricted) are part of the phase 3: another way to hold the common equity in escrow (for recapitalization: CFR 1237.12), through the offset attached. It will be unwound (FHFA-C's Incidental Power: "Zing!")

The Warrant was a SPS collateral if we want it to be a legal security.

One thing is their intention, which I already pointed out yesterday that it was to tumble the common stock price, as mentioned also in the FASB meeting minutes that you posted, so it mimics the initial collapse in the JPSs' fair value with the suspension of the dividend payment and they can peddle the idea that Cs and JPSs are equivalent securities for a conversion JPS to Cs.

Also, for the intention of assault on the ownership of FnF with the clause 2.1 "Shares assigned to any Person (BX, BKT, MS, JPM, Community banks, etc.)"

This way, the Treasury pays almost $0 for a 79.9% stake in FnF but, by Immaculate conception ("Assigned"), the banks and investment banks become owners of FnF overnight. What government policy is that? Don't expect to read it in the FASB meeting minutes with Sheila Bair (later she became chairman of the BOD of Fannie Mae to continue to provide cover for the UST-FHFA Machiavellian conservatorship).

And a different thing is where in the law is authorized the Warrant for the Treasury, because you seem to forget that everything surrounding FnF is statutory (decided, required and controlled by law), as congressionally-chartered private corporations, and it includes the relationship with the Treasury.

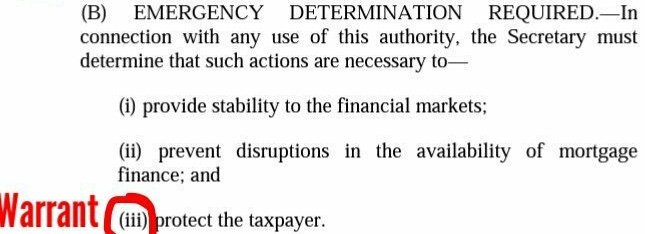

The temporary authority of Treasury in 2008, with regard to the purchase of securities like the SPS and the Warrant, had 3 prerequisites, after the determination of EMERGENCY (conservatorship), and the only one suitable for the Warrant, is (iii) to protect the taxpayer. A security that acts as protection, in this world is called collateral. That is, a guaranty that secures the repayment of a debenture (SPS, obligations in respect of Capital Stock)

Despite that this security was issued for free to evade this prerequisite on purchases. We considered it purchased at $0 cost. Instead, it was written that it was an "entry fee" or "commitment fee", that is, a higher compensation for the SPS, but they are barred in the Charter's Fee Limitation of the United States, both as fees and as a compensation worth 79.9% of a company (isn't it crazy?) for the funding commitment.

As always, we are here to legalize every action.

It isn't the first time that navycmdr and the rest of the plotters attempt to substitute the law in force for emails, statements in articles or press releases, or now, the minutes of a FASB meeting, most of them if not all, staged precisely to that end.

Zero sense of what the Rule of Law is about. This substitution is more of the same strategy of covering up of the law: the Trump Presidential Memorandum, an advisor called "Parrot", etc.

No one can come to the conclusion that it isn't a collateral, with the FASB minutes. As I've demonstrated, it can be both collateral and to tumble the stock price. You were ordered to write "NOT collateral", and you didn't know how.

I don't see in the law: "Authority of Treasury to get a Warrant with the objective to tumble the common stock price."

Keep the emails, the litigants' charts, statements, meeting minutes, etc. for yourself.

Maybe it's because of the numbers again (Sesame Street), like with the statutory definiton of capital distribution:

Number 1: (authorization to buy SPS)

Number 2: (authorization to buy SPS)

Number 3: to protect the taxpayer.

Spoiler alert: the Warrant is number 3.

And with the definition of capital distribution:

The Lamberth rebate is number 3 and dividends and SPS LP increased for free, number 1.

RESTRICTED when FnF are undercapitalized. The exceptions to the restrictions kicked off to legalize the capital distributions that went through:

-Reduce the SPS.

-Recapitalization (CFR 1237.12)

Hence, the Warrant (SPS collateral) should have been cancelled in late 2013 and late 2014, in FnF, resp., when their SPS were fully repaid, but a Separate Account plan has allowed the conservator to keep it "in the best interests of the Agency" (Incidental Power)

The FHFA is only interested in misleading the world in its alliance with the hedge funds and investment banks (Utility Model).

(*) 3-It wouldn't contribute to the financial instability (not stability) of FnF.

(Regarding the reason why the suspension of 4.2 bps was lifted on December 2014)

What the Supreme Court authorized is a Separate Account plan in the FHFA's best interest of misleading the world, because it MUST "rehabilitate FnF" at the same time, and "not in the best interests of FnF" on paper (Balance Sheets), as seen in their horrible ERCF tables, as justice Alito pointed out, paraphrasing the prior ruling over the same case and the same provision, the Incidental Power of the conservator, by judge Willett (5th Circuit Court) with: "Any action within the enumerated powers" (Source), which basically relates to the main Rehab power: put FnF in a sound and solvent condition.

Scroll down to learn what soundness and in solvent condition mean in a financial company.

Complying with the etymological definition of Incidental Power that the plotters want us to forget: without an express grant of authority, they are actions that help to fulfill the main Power.

And also, that the best interests of a regulatory Agency, with regard to the private corporations it oversees, it's related to activities: CSS, UMBS, commingled securities, etc.. It can't be monetary benefit, regardless that the rogue justice Alito, switched "best interests" for "beneficial to the Agency" to play the hedge funds' game of "Govt theft story" for stock price manipulation. Let alone the add-on "and the public it serves" remark that isn't written anywhere, but, in truth, it just allows Congress to keep the $15 billion owed to FnF in the MHA program, and FHFA can continue with the utilization of FnF for government policies: sale of loans to women- and minority-owned businesses, etc. Good for you! At some point it will have to stop.

When soundness in a financial company is related to capital levels, not the "rehab" made up by the CEO of Fannie Mae.

A laughable remark, because FnF today should be declared Critically Undercapitalized with a combined $-194 billion Core Capital, had the Critical Capital level been posted in the ERCF tables in light of the Capital Rule, because the FHFA is omitting this statutory capital requirement. HERA only allowed the FHFA to come out with a new Risk-Based Capital requirement, change the weights in the Minimum (Leverage) Capital requirement and add new capital metrics CET1 and Tier 1 Capital, but nothing about the Critical Capital level that remains as is.

So much for "rehabilitation".

An enterprise shall be classified as critically undercapitalized if—

(ii) does not maintain an amount of core capital that is equal to or exceeds the critical capital level for the enterprise;

12 U.S. Code §4614(a)(4)

Pagliara's footman, Guido, claims again that the Warrant only affects us when it's exercised, and it's not until then when the lawsuits should begin to pour in.

if ever taken to court after execution

FnF weren't part of TARP. They form part of the Charter Act.

You posted the same lunacy last week, pro se plaintiff.

Quit posting phony claims, aiming to tarnish other valid claims brought up.

It is pretty obvious to me that Treasury used TARP to fund the SPS.

11 million short volume, out of 27 million total volume.

It means that the short seller is covering up its prior position with 16 million stock repurchases.

There is only one person buying and short-selling the FnF stocks. The retail investor doesn't make any difference. The same person tasked by Geithner with bottom-fishing the stocks for the Treasury.

The "market maker".

The idea that all of a sudden there is a market frenzy and many investors pile up to purchase these stocks, is crazy.

Let alone that someone is short-selling, like the actor Kthomp19, alias Mr. Soopprise, who claimed to have a pair-trade short FNMA and long FNMAT, notwithstanding that later he mentions to have a large portion of his portfolio in FNMAS.

This attorney thinks that he can't take any crazy stance and defend it firmly and thus, it will be whatever he wants it to be.

This isn't a court room and Finance doesn't understand of shenanigans. This is why he hits a wall over and over again.

"Pair-trade" doesn't necessarily mean 2. It can be multiple securities as long as they have high correlation (similar risk exposure).

He thinks that his position in FNMAS is "off-balance sheet", like the $118B SPS LP absent from the balance sheets and its offset. Off-portfolio? ROFL.

The reality is that he had a pair trade: small short position in FNMA, and the bulk of his portfolio with a long position in JPSs.

Knowing that he is a compulsive liar, everything is a big lie and he has never shorted the stocks and only the market maker and its accomplices are doing it, driving the stock up and down at his will, accompanied by the Government theft story, the common stocks are "options", now "The Trump trade" peddled by Navy Hedge Fund with all his aliases, etc.

The plotters want to transmit the idea that there are random people shorting these stocks.

Who knows if he is now thinking of Failure-to-Deliver, in this beyond-Machiavellianism Conservatorship.

*** Judge Lamberth is feeling the heat ***

He is very busy nowadays.

J.LAMBERTH TAKES THE PLACE OF THE FHFA DTR

— Conservatives against Trump (@CarlosVignote) January 23, 2024

Contravening the will of Congress:"Demonstrated understanding of financial mngmt"

Lamberth:"Plaintiffs were denied divs that otherwise were certain to receive"

Conmen know the trick and pile up at his doorstep.#Fanniegate @TheJusticeDept pic.twitter.com/RL1dDbJYCm

The actor kthomp19 talks about "off-balance sheet SPS" again.

More shenanigangs like the other day with the Restriction on Capital Distributions, claiming that it's when FnF are classified Undercapitalized, when the law states "undercapitalized" and "IN GENERAL", like nowadays.

Sandra Thompson: "FnF remain undercapitalized...."

He claims that this restriction is void, since the FHFA suspended the Capital Classifications on day one.

But above all, he doesn't know the financial reasoning behind. It's restricted (Dividends, SPS LP increased for free, Lamberth rebate. Watch the statutory Definition of capital distribution numbers 1, 1 and 3, respectively.) to build capital (soundness). It isn't done to attack the Equity holders or to enrich the government with dividends just for it.

It's the stocks' role and the reason why the are recorded in regulatory Core Capital (loss-absorbing capacity capital-related).

So, FnF can't even set aside a reserve for the Lamberth rebate, as seen in Q3.

The SPS LP increased for free must be posted on the Balance Sheet, along with its offset that happens when someone issues or increases(fraud) stocks for free (stock dividends, stock compensation to employees, etc), as seen with the initial $1B SPS LP gifted to the UST, debited from the Additional Paid-In Capital account (Core Capital and CET1. A breach of the FHFA-C's Rehab Power).

Currently, all the SPS LP increased for free as of December 2017 ($118B) is absent from their Balance Sheet, which coincides with their Net Worth.

Once adjusted, we see that FnF are building SPS, not regulatory capital (the Retained Earnings built is wiped out with the offset attached to the gifted SPS LP), and the plotters want to meet the capital requirements with these gifted SPS.

Beyond Machiavellianism.

Even if these gifted SPS were "off-balance sheet", he claims that it doesn't affect FnF.

More shenanigans by this attorney, who reminds me a lot of the DOJ's Mooppan, who took a crazy stance and defended it firmly before the Supreme Court:

The 3rd amendment NWS dividend, was a typical renegotiation of obligations. Thus, within the FHFA's powers.

Off-balance sheet. Thus, it doesn't affect FnF.

Maximize taxpayer profit

For the Enterprise Value, you have to add the Preferred Stocks in the formula that you've pointed out:

Enterprise Value= Market Capitalization + Market Value of Debt – Cash and Equivalents

Hedge fund manager Donald Trump is a worst-case scenario.

A 99.9% dilution of the common shareholders.

The former POTUS showed us his true face when he promoted the farce of "Equity restructuring" in his letter that came out of the blue, restructuring peddled also by the hedge fund manager Bill Ackman in his Pershing letters, with "re-privatization" for the conversion of SPS to Cs, exercising the Warrant for the sale of more stocks to the hedge funds, plus more stock offerings to build capital, as today they want us to believe that FnF have a whopping $402 capital shortfall over Minimum Leverage capital requirement, after 15 years in conservatorship.

Donald Trump laid out his investment case in a letter written in November 2021 addressed to senator Rand Paul, when no one asked him for his opinion.

As commented yesterday, the SCOTUS didn't require a statement from Trump as hedge fund manager today, but as POTUS:

Suppose that the President had made a public statement expressing displeasure with actions taken by the FHFA Director Watt

The Supreme Court's decision asks what I would have done...

Former President Trump recently made such a statement in a letter,

It looks like the parties prepare a CHEVRON deference case out of the blue, in the Lamberth court, after reading the latest court briefs.

First, the FHFA's "oral motion" to defer entering judgment on Verdict-Day, which is obviously an attempt to conceal the reason behind, with the Restriction on Capital Distributions by statute.

Lamberth then required future briefs "on paper" and offered the court for "any dispute" that the parties might brief.

What dispute might he be thinking of, if the Proposed Final Judgment was already submitted by the partes and what is left, a Plan of Allocation, the Defendants have no say?

The latest evidence is the recent joint motion for a five-day extension of time to file the Plan of Allocation, scheduled for today, where the parties extensively talk about having disagreements:

The parties held a lengthy meet and confer via Zoom, in which they discussed multiple issues...

some areas of dispute that will need to be briefed before entry of a final judgment.

to narrow outstanding issues and brief any final remaining dispute(s) for the Court.

There is no point in writing a financial analysis in a company under a Machiavellian conservatorship, just to claim that the stocks have no value (YOU DON'T SAY? Let me guess. The outcome of a PER 14 times with the $0 EPS that FnF post every quarter, right? Or is it the $310B SPS LP outstanding? Etc.), where the conservator can "take any action authorized by this section, in the best interests of the Agency" (FHFA-C's Incidental Power), so it can do and undo whatever it wants if the endgame is "authorized by this section", which isn't the same as saying "FHFA has absolute discretion" (implied by Ackman in his letters with Pershing) or that "it can do whatever the hell it wants" (Bradford), when both wrongly quote the Supreme Court, because justice Alito started out with "a way to rehabilitate FnF" that blesses the Separate Account, and the same pointed out by judge Willett "any action within the enumerated powers".

They are the grounds for an External Position (Separate Account like in 1989 with the FHLBanks with ST and DeMarco too), and everything you see might not be the actual outcome, for someone that has read the rest of the legislation, regulation and knows basic Finance, like a dividend, distribution of Earnings.

The FHFA's best interests have been, thus, to mislead the world.

The coverup of all of the above is what Fanniegate is all about, like:

-Restriction on Capital distributions. Exceptions. U.S. Code §4614(e).

-FHFA-C's Power and Incidental Power.

-The low cost UST backup of FnF in the Charter Act.

-The Fee Limitation of the U.S..

-The Final Rule for the transparency of the conservatorship, on July 20, 2011, coinciding with the Time Limitation of the Acting Dtr DeMarco, that enacted the CFR 1237.12, that "(c) supplements and shall not replace or affect any other (the aforementioned) Restriction on Capital distribution by statute", meaning "follow-on plan" for the moment the SPS were fully repaid with the prior exception to this restriction (estimated at the end of 2013 and 2014 in Freddie Mac and Fannie Mae, respectively). Now the capital distribution (deplete capital) is authorized for their Recapitalization (build capital), a Separate Account wording, in either of the 4 exceptions, because it must uphold the restriction by statute, which is for Recapitalization as well (dividend suspended).

A Final Rule that also included the the payment of Securities Litigation judgments as capital distribution after amending its statutory definition, and "prohibiting" it in the preface of the rule, "at a time when the Agency is tasked with the rehabilitation", etc. It's the Lamberth rebate currently with a Plan of Allocation in the making, scheduled for today.

Another one that will come up with the: "But I believed...". That is, playing the fool, like Ackman with the 13D reports mentioned in my prior post.

No one in his right mind covers the FnF stocks, except KBW that was just hired to write the alibi in the form of financial analysis, and, with all the verbosity possible, it comes to the same conclusion laid out by the hedge fund manager Bill Ackman, among others, like the hedge fund manager Donald Trump, former POTUS, with his case of restructuring FnF laid out in the Trump letter, an example of "fabricated evidence" because the SCOTUS didn't ask for his opinion today, but a public statement when he was POTUS "showing displeasure with the FHFA Director's actions" and what he said was exactly the opposite during a rally with Real Estate professionals on May 17, 2019, the only time that he has talked about FnF publicly, other than the Presidential Memorandum:

We are doing well with them. Now, it's well managed. They are great people...have some really good people running it.

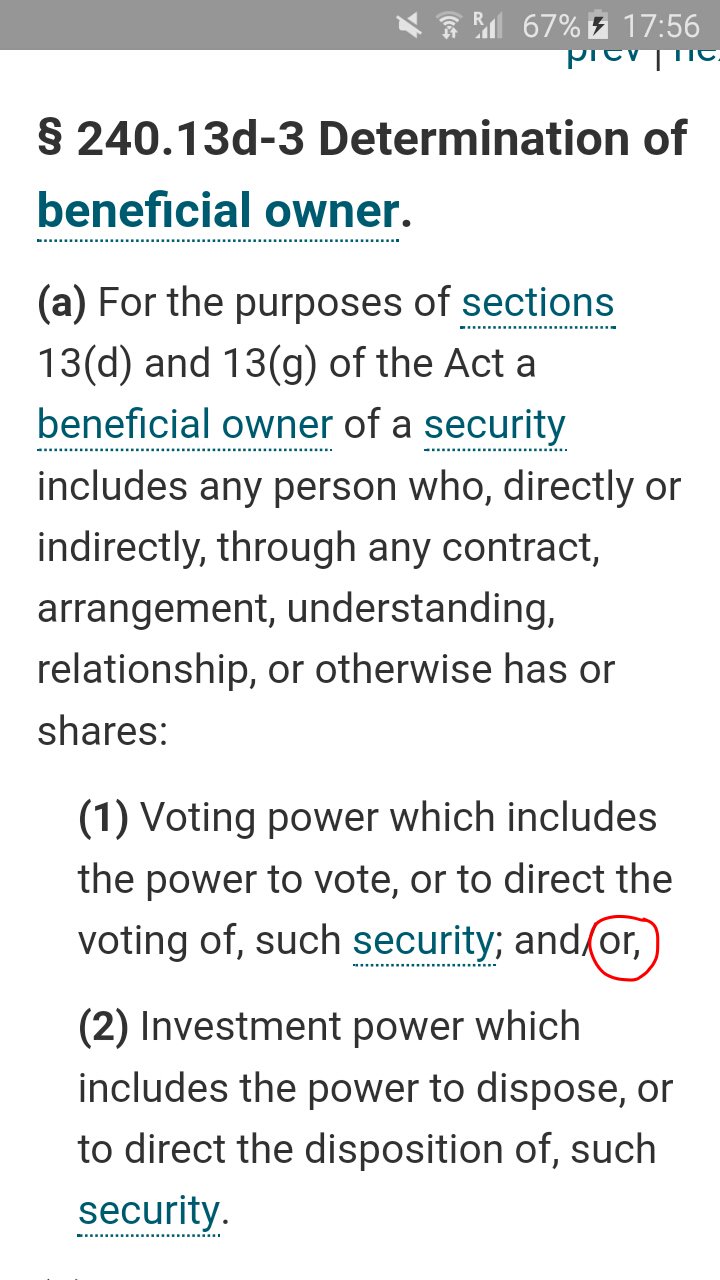

No. Ackman said that he believes that he can contravene S.E.C. rules and don't file future reports on Schedule 13D with beneficial ownership, according to Freddie Mac in its Earnings reports.

So, play the fool talking about what he "believes" as part of his strategy to bottom-fish the stocks, after hiring a bunch of crackpots on social media and in court, continuously downplaying expectations about the common stocks: "spspa conversion", "$100B+ cash Equity", "retained earnings, choo choo", "the Warrant affects only if it's exercised", etc.

He uses the excuse contending that "the common stock is not a voting security", despite that the definition of Beneficial Ownership clearly states that it's also the power to dispose of such security, which is our case in Conservatorship.

Play the fool is an aggravating circumstance when assessing the breakdown of penalities worth $4.8 billion for Punitive Damages, against those peddling the government theft story in formal documents: books, articles, letters to shareholders, court briefs, financial analyses, etc.

Your JPS valuation is to claim:"anti dilution protection", which is laughable since it forms part of the Net Worth and currently the JPS are worthless with only $118B Net Worth, but $310B SPS outstanding, including the ones absent from the Balance Sheets.

So, 100% dilution. That is, wiped out.

Mnuchin is a bond guy and he was thinking of a debt restructuring.

The SPS would need a haircut.

Both measures boost the common stock price.

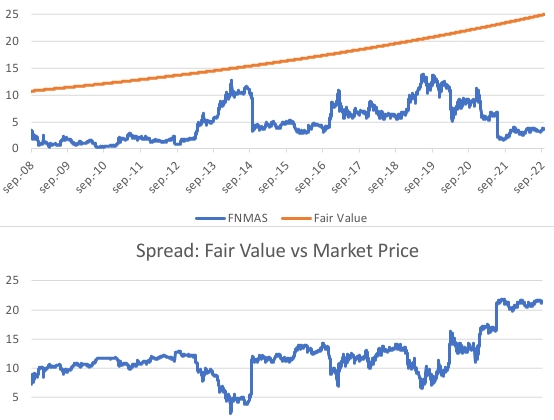

Watch the chart in my signature image below, with the evolution of the Net Worth in Freddie Mac (SPS + JPS + Common Equity) during Conservatorship and when the Cs and JPS started to have some value, under the Separate Account plan, which is the same chart as a normal Conservatorship.

Then, you'll get the par value for your stock because that's the stock's fair value today.

Fair Value calculated using a 6% discount rate to the moment that it's estimated Fannie Mae should have resumed the dividend payments under the Table 8 (Payout ratio) of the Capital Rule, as seen in this chart:

All you need to know about CHEVRON DEFERENCE in Fanniegate.

And regarding the Separate Account plan, it isn't deference either, but a case of ethics.

— Conservatives against Trump (@CarlosVignote) January 21, 2024

The so called "External Position", like the European Central Banks' Payment Systems Target2 and TIPS.@Bundesbank: "External position".

A global pandemic.@USTreasury pic.twitter.com/bDQSVFgyJe

Geithner: "Don't listen to banks...". Remember?

Don’t listen to banks…Their interests are not aligned perfectly with the broad interests of the American economy. Their job is to evade, or avoid, or weaken, any constraint on their ability to operate our job to make sure we’re protecting the american economy from the risks they inevitably take.

The president did not want the new rules to end up being written by those who brought us to the edge of catastrophic financial failure.

The banks seem poised to challenge their federal regulators requirements for holding yet more Capital: (todays WSJ): "Banks have spent more than a decade since the financial crisis showing relative deference to regulators. Now big banks have signaled they are considering legal action,...

The CEO of Fannie Mae was referring to the Separate Account.

That's why she talked about the rehabilitation of FnF.

Otherwise, under the ERCF tables, the financial condition of FnF is awful.

Let alone the adjusted numbers. Adjusted for the offset (reduction of the Retained Earnings account) when the SPS LP is increased for free every quarter.

A combined $402 capital shortfall over Minimum Leverage Capital requirement. Rehab?

Rehabilitation of FnF is considered the prerequisite laid out by justice Alito and judge Willett, when they interpreted the Incidental Power: any action "authorized by this section", also taking into account the etymological definition of "incidental" (without an express grant of authority, they help it to fulfill the main power), adding the Marxist-way "beneficial to the Agency and the public it serves" for the extortion of resources in the meantime, with the sale of loans with a debt forgiveness string attached, and REO inventory to Goldman Sachs & Co, Neighborhood Associations, women- and minority-owned businesses, etc., and mess around, because the law doesn't say "beneficial to the Agency" but "best interests", to transmit the idea of "monetary benefit" and play the conspirators' game of Govt theft story for stock price manipulation.

The interests of an Agency with regard to the companies it's regulating, are related to activities, not to take their profits away.

This is the key for the Separate Account plan, because those interests chosen by FHFA, have been to mislead the world holding the Common Equity in escrow. Good. But at same point the External Position has to be returned for the rehabilitation of FnF, which, in this world, occurs only on the Balance Sheet, unless you live in Europe with the large scale fraud in their Central Banks' Payment Systems Target2 and TIPS (Bundesbank: "External Position". Give me a break.)

If you refuse to watch the ERCF, then watch their Balance Sheets (concealed when the corrupt litigants submit to court their own manufactured charts, instead of the Balance Sheets. A picture of a company), with outstanding Accumulated Deficit in their Retained Earnings accounts, that are meant to absorb future (unexpected) losses. Capital Stocks don't absorb losses, they just offset a negative RE, so the Net Worth is positive avoiding bankruptcy (example: the effect of the SPS in early conservatorship. Watch my signature image below). This is why the issuance of stocks "fund the losses", they don't bear the losses (representative Hensarling called the SPS "taxpayer's losses"). By the way, what the Fed should have done instead of its surreal Deferred Asset: fund the losses with issuance of capital stocks.

What the Capital ratios are for: to cover future unexpected losses, as the expected losses have already been reserved (asset write-down, as seen in the Balance Sheets below) in the Allowance for Loan Losses, under the CECL accounting standard (it assumes that the loss already occurred. Yet, it might be recovered down the road -Benefit for loan losses, instead of Provision for loan losses-)

Although RE can be negative (caused by past losses), it's common sense to think of "Financial rehabilitation" in the sense of turning it around and have a positive balance again.

Let alone the payment of dividends. A distribution of Earnings, you need to have a positive balance in the first place to distribute it out (then, there are thresholds to meet. Table 8: Payout ratio)

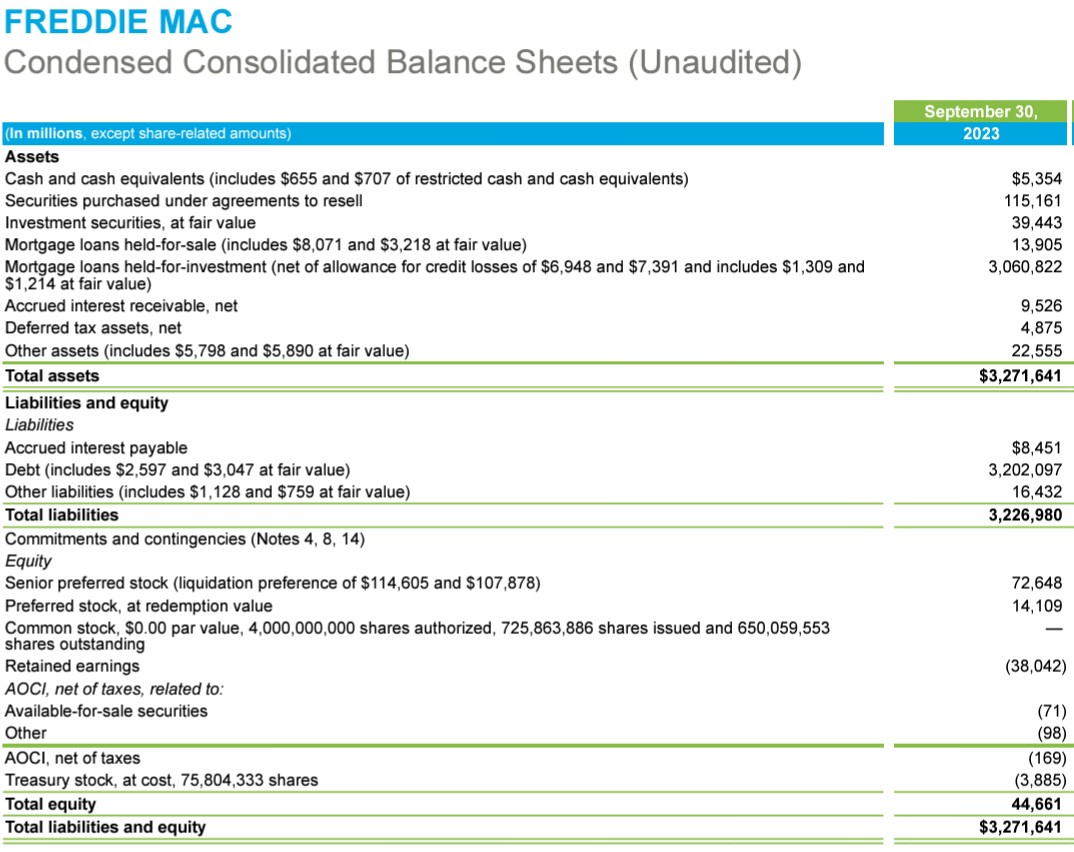

These are their Retained Earnings accounts as of September 30, 2023:

Official/Adjusted for offset attached to the gifted SPS ($ Billions)

$FNMA: -60/-134

$FMCC: -38/-83

This is the outcome when the SPS LP increased for free is posted on the balance sheet, as it should be (Financial Statement fraud), with the goal to peddle the lie of "FnF continue to retain earnings and build capital" (Ackman, Bradford, Sandra Thompson, etc.). Neither FnF are retaining earnings if it's later wiped out with the offset, nor they build regulatory capital (RE), but capital stock (SPS). A visual example of Common Equity (RE) held in escrow to uphold the law: the exception to the Restriction on Capital Distributions (Recap: CFR 1237.12) and the FHFA-C's Rehab power)

Freddie Mac:

The Retained Earnings accounts will be $236 billion combined with a posting, under the Separate Account plan and after retiring the Treasury Stock (stock buybacks).

Combined Equity (Balance Sheet) comprised of:

$0 par value Cs

$236B Retained Earnings accounts

$ current small amount of AOCI.

Common Equity calculated with the Accumulated Total Comprehensive Income in full (dividends suspended) + PLMBS lawsuit settlement, net of attorney fees + CRT expenses, net.

CET1 > 2.5% of the Adjusted Total Assets.

That's rehabilitation.