Saturday, January 27, 2024 3:01:20 AM

Now that they have built up a TON of Cash reserves.

By the way, you remind me navy Hedge Fund with:

$100B+ cash Equity. Chooo Chooo.

Read the explanation in the tweet posted at the end.

FnF's capital is governed by the FHEFSSA.

The Capital Rule (ERCF) as well (FHEFSSA Capital Rule and not FHFA's), because it emanates from an authority granted in statutory provisions:

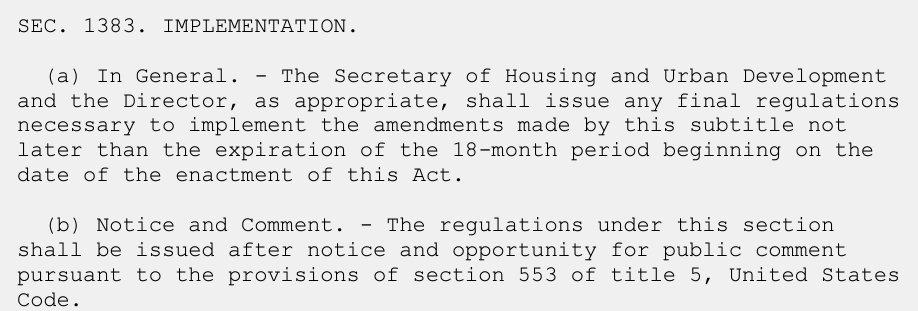

1- An authority of FHFA to come out with a new Risk-Based Capital requirement formulaic (Source), as the prior wording was struck by HERA. Calabria and Pelosi "forgot" to include the provision 18-month IMPLEMENTATION

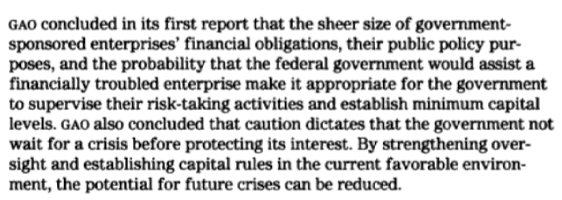

necessary always that an Agency is tasked with something by law, as seen, precisely in the FHEFSSA of 1992 that established capital metrics, capital levels, capital classifications and Prompt Corrective Actions, for the first time, and

at the request of a GAO report the year before.

Along with removing the provision MANDATORY release Undercapitalized (Core Capital > Minimum Leverage Capital requirement), they are evidence of concealment of the fact that FnF are building capital in a Separate Account.

The absence of IMPLEMENTATION provision is why the Capital Rule that came into effect on February 16, 2021 is called "back-end Capital Rule", that is, effective at the end of the typical Transition Period to build capital, given by an Agency when there are changes in the capital requirements (For instance, the Fed and FDIC have just given 3 years to build capital to the banks, starting in July 2025, for the proposed capital standards Basel III engame. So, 5 years in total. The FHA's MMIF was given 10 years by Congress to build a 2% ratio. Or the very FHFA pointed out with regard to the FHLBanks' capital building: "Within a reasonable period of time". It's been 12 years since the Treasury's Privatized Housing Finance System for the release of FnF from Conservatorship, at the request of the Dodd-Frank Law, and now, FnF have CET1 > 2.5% of Adjusted Total Assets, suitable for the redemption of JPS. Is 12 years a reasonable period of time or do we have to believe that FnF have an adjusted $-194B Core Capital (ERCF tables)? Critically Undercapitalized.)

2- An authority to change the percentages in the Minimum Capital requirement (Source), now known as Leverage Capital requirement. For instance, from 0.45% to 2.5% of MBS trusts, Basel framework.

3- An authority to establish additional capital (CET1 and Tier 1 Capital) and reserve requirements (Capital buffers). Watch the prior link.

It didn't change the Critical Capital level that remains as is, but the FHFA rather conceal this fact to peddle the lie of "rehabilitation". Not meeting a capital level called "critical" bothers them. This is why it's concealed.

The JPS holders still don't get what Regulatory Risk means and the fact that a JPS is a made-up financial instrument, precisely created exclusively to build capital when it's needed. Plus the overtime chosen by the conservator "in the best interests of the FHFA" (Incidental Power), for the expulsion of unwanted Equity holders (the same occurred with the FHLBs, when the hedge funds that used insurers to access low cost borrowing from the FHLBanks were called "captives", expelled in a 2016 rule, proposed in 2010)

Notice that the FHFA would like the battered FHLBanks to acquire FnF. So, the ownership of the FHLBanks is also linked to FnF's.

The expulsion of the JPS is why FnF have built a CET1 > 2.5% of ATA under the Separate Account plan.

FLAWED CAPITAL STANDARD. BADLY ASSESSED

— Conservatives against Trump (@CarlosVignote) January 26, 2024

The #Fed's C.Surplus is the amount of Net Worth above C.Stock, fixed at $6,785mll by law. Hence,DA(losses) fraud,to not deplete it.#Fanniegate

The plotters' C.Reserve=$118B. But $118B SPS LP absent from the Bce Sheets.

Hence,adjusted CR=$0 https://t.co/d6q7TMeSBS pic.twitter.com/C7CV7OoJzh

Avant Technologies Engages Wired4Tech to Evaluate the Performance of Next Generation AI Server Technology • AVAI • May 23, 2024 8:00 AM

Branded Legacy, Inc. Unveils Collaboration with Celebrity Tattoo Artist Kat Tat for New Tattoo Aftercare Product • BLEG • May 22, 2024 8:30 AM

"Defo's Morning Briefing" Set to Debut for "GreenliteTV" • GRNL • May 21, 2024 2:28 PM

North Bay Resources Announces 50/50 JV at Fran Gold Project, British Columbia; Initiates NI 43-101 Resources Estimate and Bulk Sample • NBRI • May 21, 2024 9:07 AM

Greenlite Ventures Inks Deal to Acquire No Limit Technology • GRNL • May 17, 2024 3:00 PM

Music Licensing, Inc. (OTC: SONG) Subsidiary Pro Music Rights Secures Final Judgment of $114,081.30 USD, Demonstrating Strength of Licensing Agreements • SONGD • May 17, 2024 11:00 AM