News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

This isn't about throwing ideas at the wall.

The resolution of Fanniegate is upholding the law, rules and basic financial concepts.

1st. The Separate Account plan.

2nd. A refund of the CRT expenses, net (barred in the Charter Act, both in the Credit Enhandement clause and the Fee Limitation clause in the case of operations with the Treasury)

3rd. A refund of the PLMBS lawsuit settlemenent on behalf of FnF, net of attorney fees.

The only negotiation possible is about the compensation for Punitive Damages:

It's been requested a 0.25% IRR on a JPS par value, during 15 years.

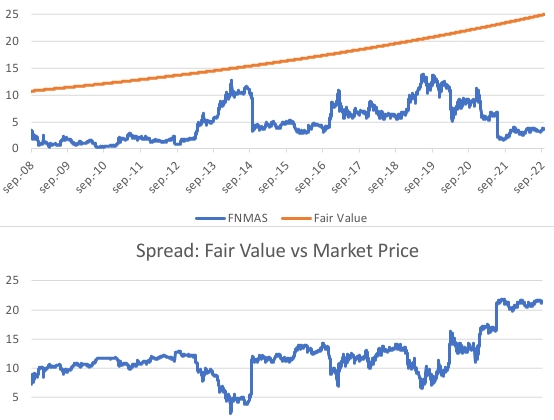

Calculated with a rate of 0.5%, because it's the spread over Treasuries under the Charter's original UST backup of FnF, for the estimated total 1.8% cumulative dividend on SPS that the UST has earned, until the SPS were fully repaid (end of 2013/2014). And an interest rate on half a JPS par value, which coincides with the average spread Fair Value vs Market Price, the real damage caused: the Separate Account plan prevented the stocks from trading at their fair value all along.

The amount of interests is $0.97 per $25 par value JPS. A common stock matches a $50 par value JPS because their fair values are closer.

Then, there are three rounds:

1- Agaist the DOJ for the 8 Securities Law violations during conservatorship: SPS increased instead of issued, to evade the December 2009 deadline on purchases; Stock price manipulation; Gifted SPS and their offset, absent from the balance sheet; Etc.

2- Against the DOJ again: the Deferred Income accounting. There was an accounting change in early Conservatorship with the consolidation of the MBS trusts that eliminated the prior accounting of Guaranty Obligation, but the FHFA later chose the same scheme with the Deferred Income. It should have been called Delivery Fee (before the product is launched) instead of upfront g-fee, and problem solved. It's valuable core capital already collected, that remains recorded on Debt. In a financial company, this is unacceptable, as it's subject to regulatory compliance with regard to capital levels.

The common shareholders waive these two claims in the case of resolution "as is" or "takeover" scenarios, not in "Taking", for having chosen the option more favorable.

3- Against the corrupt litigants that filed frivolous lawsuits covering up many statutory provisions and financial concepts. Also against their accomplices writing about a phony Govt theft story in formal documents, aiming to tumble the stock prices. This way, "everyone would be standing shoulder to shoulder", as Pagliara said when he shamelessly asked for a swap JPS for Cs, as a result of both stock classes trading at rock bottom prices, when each stock class has its own stock valuation, an the common stocks are affected by the Warrant and the Separate Account, not about the suspension of dividend payments, because they are kept by FnF and that's Common Equity.

You can't change the financial concepts and trample the Rule of Law, just because you are annoyed with the outcome. If someone has a problem with stock valuation, please attend a Finance Course, like everyone else has done before.

Can you imagine that the corrupt litigants are now in charge of "negotiating" a resolution with the FHFA? After both have deprived the Rule of Law of its meaning, with the frivolous lawsuits and crooked judges playing along, so now they stage a negotiation "cattle market-style" without any binding rule. The shareholders can throw in a cow and two goats.

Or is it a chess game? "Gimme this and I give you that. If you do this, I do that. ....You do that... I do that. ...Do that...do that. Dothatdothat..."

Or is it a tennis match: "Match point now in the Lamberth tennis court", where is scheduled for January 10th the sought-after "negotiation table" with the attorney for Berkowitz, David Thompson, achieving his plan: "The government has to come to me", a remark made in a conference call hosted by Pagliara many years ago (tape removed from the internet)

Hundreds of pages of legislative wording, rulemaking and financial concepts thrown in the bin.

Now we play in the Mob's playground: lawlessness. Everything has been covered up or twisted, that has ended up with the accessories claiming on social media that the conservator "can do whatever the hell it wants".

Finally,🚨this comment from the plaintiff Bryndon Fisher might have sounded the alarm at the DOJ and the SEC.🚨

It could be the reason why the litigants have filed so many frivolous lawsuits in the U.S. Courts. They are mercenaries that just seek a big check in a negotiation with the Government, knowing that the Government has unlimited resources.

Brydon Fisher proposed to settle the Collins case before the Oral Arguments at the Supreme Court.

The attorneys are negotiating their check, nothing about the rehabilitation of FnF. This is why a penalty for Punitive Damages is of supreme importance (deterrence)

By the way, is it me or Ace Trader sounds a lot like the plaintiff Bryndon Fisher? He always claims that Collins brought the wrong claim because he is smarter and he can file a better lawsuit than the Fairholme Plaintiffs. Also he seeks a Cattle Market-style negotiation with the Government and, the last clue, he seems always annoyed with other posters, even when they agree with him. For instance, in this reply to a poster, to point out the same that the poster had said, but he makes it look like both were in disagreement.

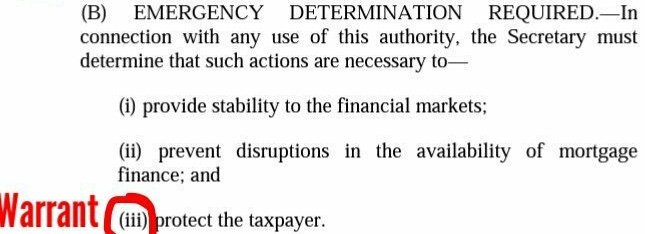

It seems that Fisher doesn't know that a collateral is a guaranty that ensures the repayment of a debenture (the underlying security in a Preferred Stock, is an obligation. Perpetual, but always redeemable at the option of the issuer.), like in our case, a collater "to (iii) protect the taxpayer". A security issued for free to evade this prerequisite on purchases by UST.

I know Colin’s brought the wrong case in front of SCOTUS for takings. I have gone around and around today .

People keep changing the subject of my posts rather agree they could take many options .

My posts today again were about the Governments self dealing for its best interests and disregard for shareholders.

I thank you for your knowledge and posts and agree a lot of your posts but let’s not go off in another discussion or direction other than all I stated was today . I’ve kept on topic and everyone else keeps changing the subject.( the Governments shady actions towards Fannie and Freddie and shareholders.

and how if they release them on what terms.

5th part in the sequel to "Navycmdr never learns".

Entitled: "scroll all the way down, babe."

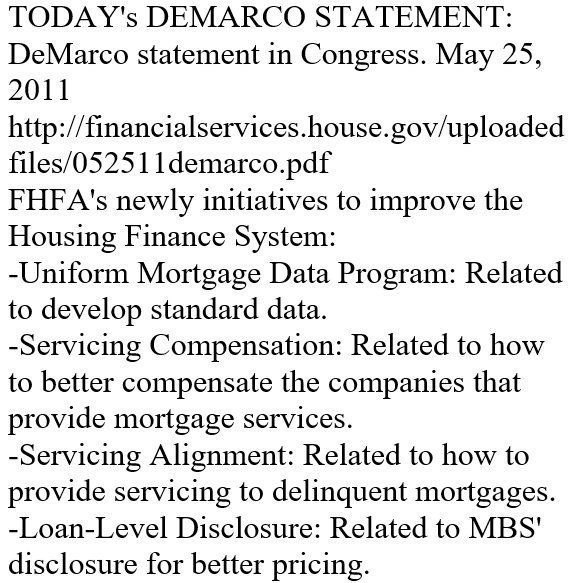

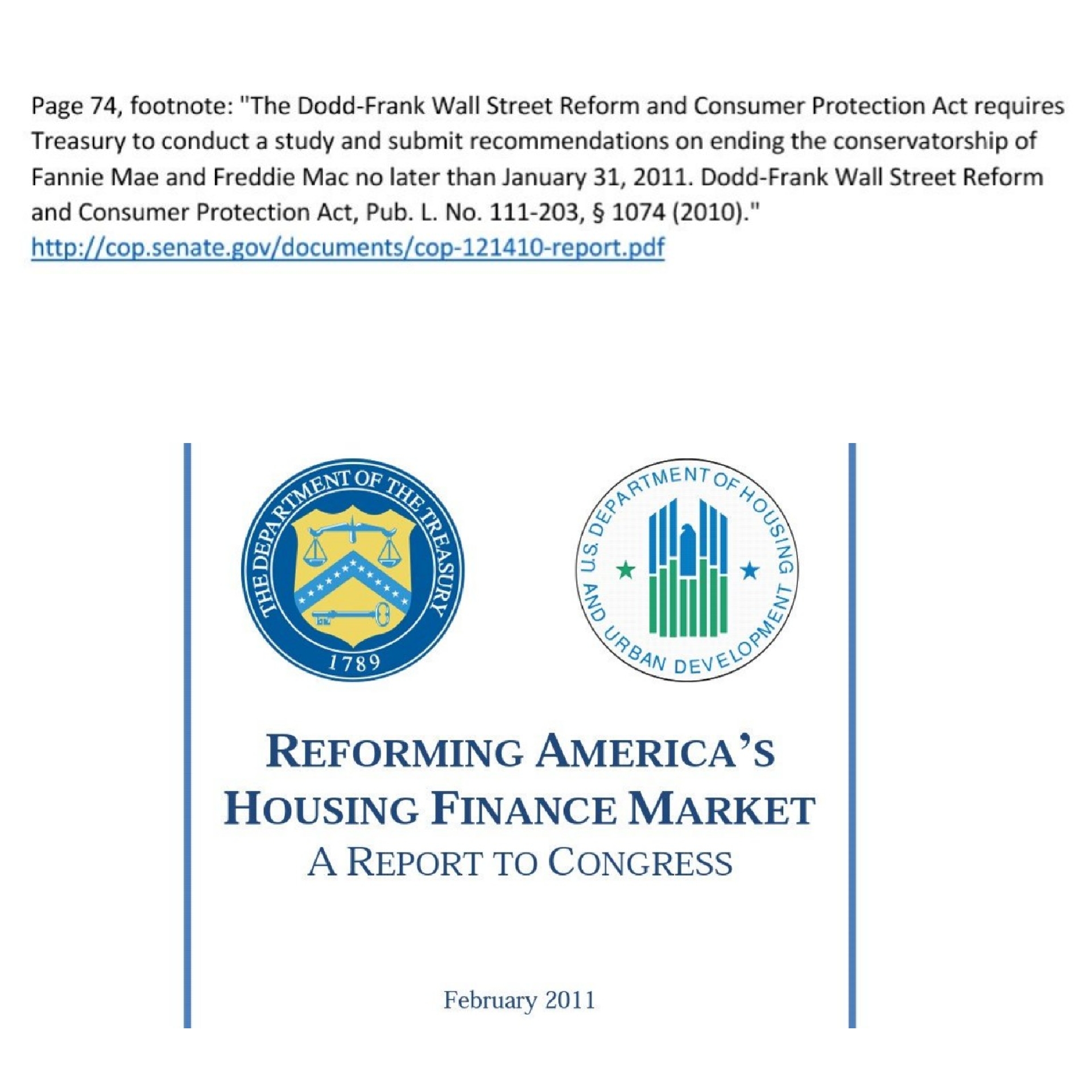

Once again, navycmdr attempts to supplant the actual mandate of release in the Dodd-Frank law of 2010, and subsequent Privatized Housing Finance System end point of conservatorship that the UST came up with in February 2011 (both images posted below), for a series of bills introduced in Congress in 2016 and 2023.

It renders the conservatorship as a typical Transition Period to build capital and the 2021 capital rule labelled "back-end", thanks to the lack of the required 18-month IMPLEMENTATION section, as seen in the FHEFSSA for the first capital ratios in 1992:

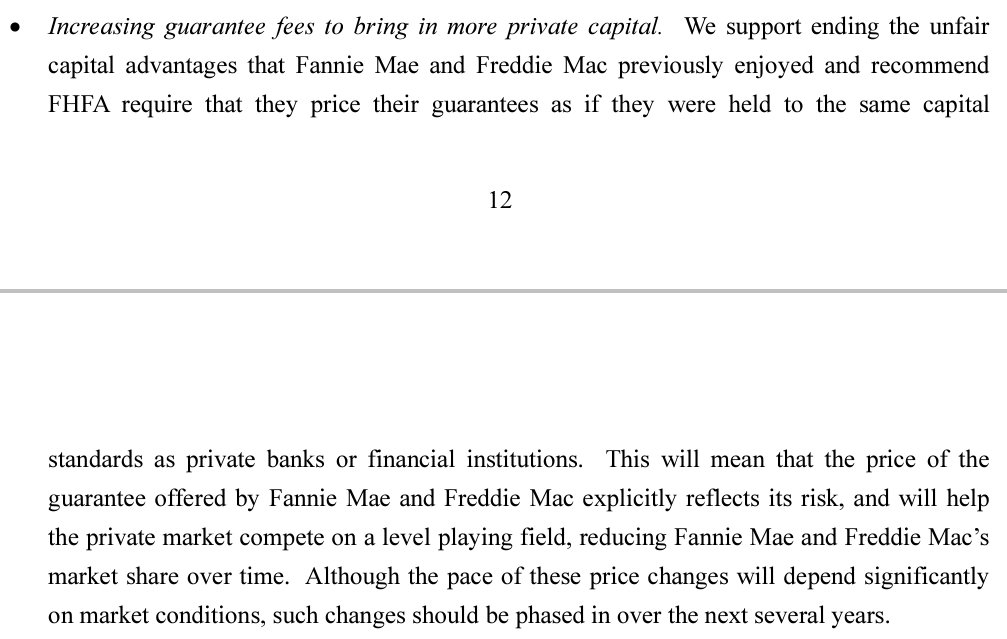

The g-fee hikes meant to that end, recommended by the Treasury "as if they were held to the same capital standards as private banks", which means Basel framework, stipulated in the 2011 Report to Congress:

All the U.S. officials have been building on it: CSS, UMBS, Basel framework, commingled securities, etc., and DeMarco began to work on it right away:

Obviously, this translates into a Charter revoked scenario, as it renders the UST backup of FnF, pointless, along with their Public Mission.

The conspirators don't like it. This is why they claim that there is expectation of amendment of the capital requirements Basel framework for fully private financial institutions, our end point.

Just yesterday, Guido submitted this question to the FHFA web site:

1) When are you going to publish the updated capital requirements for Fannie Mae and Freddie Mac?

The allocation of a one-time 4.2 bps on new acquisitions to 2 Affordable Housing Trusts managed by the UST and HUD, is a capital distribution too (an expense unrelated to the business activities or an operation that affects the Equity), but they have their own restrictions in their own statutory provision of the FHEFSSA, as amended by HERA, unlike dividends and gifted SPS that fall under the U.S. Code §4614(e): restricted upon undercapitalized IN GENERAL.

These exclusive restrictions for the 4.2bps explain the obscurantism surrounding the conservatorships, so that these payments can go through.

Suspension upon:

- Classified Undercapitalized. Capital Classifications suspended during conservatorship.

- When a Capital Restoration Plan is in place, necessary in the case that FnF were released before the MANDATORY release Undercapitalized, at the discretion of the Director (Struck by HERA, this threshold is still considered regardless).

- And the 3rd reason for the suspension of these payments, is another evidence of the Separate Account plan, because Mel Watt lifted the suspension during conservatorship on December 2014, and it's only possible if he determined that it doesn't contribute to the financial instability of the enterprises, at a time when, according to the law, Fannie Mae repaid the last SPS outstanding (Freddie Mac one year earlier as seen in my signature image below) under the guise of dividend payments to UST (restricted and unavailable funds for distribution as dividend with Accumulated Deficit Retained Earnings accounts) and this repayment of the debenture with the taxpayer (SPS) added up to a solvent condition.

These legislative fees, like the TCCA fees (10 bps guarantee fee syphoned off to UST as well), sum a total estimated in $46B during conservatorship, shouldn't have been enacted because they are barred in the Fee Limitation of the United States in the Charter Act.

The key is that these payments don't contravene other statutory provisions, as they have their own restrictions. Unlike the 2nd UST backup of FnF at unlimited yields, that contravenes the original low cost UST backup "at rates that take into consideration the Treasury yields as of the end of the month preceding the purchase".

And the restricted dividends and gifted SPS that went through, I've already told you that we are here to legalize the actions, not to cry out loud that they are unlawful. These payments are part of the famous Separate Account for the reduction of SPS and recapitalization, whether they want it or not, because it's what makes them lawful.

A few years ago, I stopped requesting a refund of the legislative fees.

Now, they are useful in the case of Fanniegate resolution "as is" or "takeover" of FnF by bigger players at the stocks' fair value, without a "Taking" of our stocks at book value beforehand, because the UST would make $0 in profits (cumulative dividend on SPS is netted out with the interests owed to FnF on $150.9B due), and we can reply that, along with the amount of the Making Home Affordable programs, called "Obama's programs" but defrayed by the Equity holders of FnF, estimated at $15 billion, the $0 in profits turns into a $61B windfall for the UST that shouldn't have existed under the Fee Limitation of the U.S., so it appeases tensions in lawmakers that still don't understand that FnF are not ordinary businesses.

All of the above is set forth in the law and it's been explained on this board before. More evidence that you haven't read the laws and regulations in force, pro se plaintiff, and you are writing here daily like mad and filing lawsuits in the Lamberth and Sweeney courts.

The DOJ is compelled to address our claim on social media against all the frivolous lawsuits that are the reason why the stocks trade at rock bottom prices, and others peddling their Govt theft story in formal documents, based on the cover-up of statutory provisions, regulation and basic financial concepts (dividends, a distribution of earnings from the Retained Earnings accounts): books, court briefs, letters to investors, articles, financial analyses, etc., plus their sponsors behind the scenes, others are publicly known, like BX and John Paulson, the sponsors of the Moelis Plan.

$4.8 billion will do it.

The DOJ, hit with two rounds of $4.8B as well, accordingly (relieved in the two scenarios mentioned in the case of common stocks), could earn big money penalizing these conspirators as well, regardless that they have worked hand-in-hand with them to share the booty with Wall Street.

-We've been robbed!

-Yes, we stole it all! Arrr!

The taxpayer doesn't understand of these conspiracies to rip off the shareholders.

Let alone, those to blame for the Banking crisis. Those that chose the HTM portfolio accounting in investments in debt securities, instead of AOCI (accumulated unrealized losses in Equity) or Fair Value change, it doesn't comply with GAAP, that requires assets to be valued at the market price if there is one, like this case. They are the large banks that didn't have the surreal "AOCI opt-out election": 12 CFR §324.22 (b)(2), and instead, the FDIC regulation requires that they "must deduct identified losses" (deduct losses of AOCI from CET1, if they weren't recorded beforehand as Fair Value change reflected later in the Retained Earnings account) in the 12 CFR §324.22 (a)(9).

Expected posting of $236B on the Retained Earnings accounts, not $228B that was the prior quarter (as of June 30, 2023)

After calling his boss "coward", Guido promotes his boss' will, about a conversion of JPS into common stocks.

3) conversion of jps to commons at ratios extremely detrimental to commons.

Howard talks about the CET1>3% of Total Assets for the release from Conservatorship written in the January 14, 2021 PA amendment, by Mnuchin and Calabria.

It was clearly meant to encourage a conversion of the non-convertible JPS of Mnuchin's buddy, Berkowitz, for Common Stocks, and the assault on the ownership of FnF (Common Stock).

An overblown figure for these reasons:

- 3% and CET1, are much higher than the minimum capital required in the ERCF: Tier 1 Capital > 2.5% of Adjusted Total Assets (Leverage ratio. Image below). First, a 3% instead of 2.5% and, secondly, Tier 1 includes the JPS (Tier 1 = CET1 + AT1). Too stringent, outside an ERCF that was about to come into effect (February 16, 2021). Therefore, Mnuchin and Calabria knew that the threshold was overblown and they thought that no one would notice it. Also, enacted 12 days before secretary Yellen was sworn in.

-The threshold mentioned before: Tier 1 Capital > 2.5% of Adjusted Total Assets, was a MANDATORY release in the FHEFSSA (Source. Core Capital is similar to Tier 1 Capital) before being struck by Calabria's HERA. Therefore, Calabria knew quite well that CET1 > 3% of ATA is an overblown threshold.

It's been de facto snubbed.

The laggard Fannie Mae met a more reasonable CET1 > 2.5% of ATA with its Q3 2023 Earnings report, under the Separate Account plan in accordance with the law, that, not only assumes that there was no dividend all along (calculated simply with accumulated Total Comprehensive Income + the charges for 3 Accounting Standard changes), but also a refund of the PLMBS lawsuit settlement in a case against 18 financial institutions, plus a refund of the $18 billion worth of CRT expenses, net (a scam and illegal operations)

CET1 > 2.5% of ATA is an important milestone because it enables the redemption of the JPS at their fair value equal to redemption value, because, afterwards, FnF would still meet the ERCF with a Tier 1 Capital > 2.5% of ATA.

It's achieved the FHFA's will of getting rid of unwanted Equity holders (a carbon copy of the FHFA 2010-2016 plan for the FHLBanks, with the expulsion of "captives". Source), though the Congress might disagree and choose an "as is" scenario instead, where the existing Equity holder stays.

Anyway, because this is an ongoing Conservatorship (non-stop), the redemption of JPS is now a corporate decision, and the JPS holders must go. More if, afterwards, there is an amortization of the entire Deferred Income in one fell swoop ($65 billion, gross, currently recorded as Debt.) that would help to build Capital Buffers for the Leverage ratio (for the Risk-Based capital requirement, it's estimated that they would start out with 13% of the Prescribed Capital Buffer in Fannie Mae, and 46% in Freddie Mac.)

The ERCF (Capital Rule Basel framework) is all that matters, not Mnuchin and Calabria conspiring all day long, jointly with other chamber investors on social media and the U.S. Courts.

Credit Risk Transfers, likely a backdoor fee to UST (barred in the Fee Limitation of the United States)

FNMA's new revenue stream with the extortion of FMCC.

First, the Credit Risk Transfers, likely a backdoor fee to UST (barred in the Fee Limitation of the United States)

Now, the commingled securities.

It's time to hold the advisors accountable: BLK, JPM and GS. The usual suspects.

THE REASON OF $FNMA'S -0.4% TOTAL MORTGAGE PORTFOLIO IN NOV$FMCC's +2.4% MoM.

— Conservatives against Trump (@CarlosVignote) January 4, 2024

FNMA found a🆕revenue stream w/ the extortion of resources out of FMCC in commingled securities,unaccounted for in its Guarantee Portfolio.

An inexperienced CEO seized control of Presidency.#Fanniegate https://t.co/jkpkUMUz1R

Higher g-fee and Resecuritizations are meant to bring in more competitors.

— Conservatives against Trump (@CarlosVignote) January 4, 2024

The payment of claims occurs upon bkrpt of the other guarantor.

F vs F, pointless.

It's beginning to look like another scheme for the extortion of resources under the guise of normal operations, CRT-style. pic.twitter.com/MOvse6qsK8

There's something when FOFreddie praises all our enemies, that makes it sound freaky.

The SCOTUS began: "It may aim to rehabilitate FnF..."

This is the "authorized by this section" of the FHFA-C's Incidental Power, in "take any action authorized by this section, in the best interests of the Agency", that the prior ruling by judge Willett made clear that it refers to actions "within its enumerated powers" (May put FnF in a sound and solvent condition), that is, along with the word "may" in its Power, it's some leeway with regard to activities commented yesterday with the explanation from Freddie Mac: CSS, the preps for a Housing Finance System revamp, the UMBS, sale of NPL and RPL as part of a business decision, not government policies, etc.

What Justice Alito really did, is to legalize the extortion of resources out of private corporations during a conservatorship managed by the FHFA or the FDIC (same statutory wording of the conservator's Incidental Power in the banks' FDI Act), with the addition not written in the law of "and by extension, the public it serves", so that the Treasury can keep the $15 billion it owes to FnF for managing the Making Home Affordable (MHA, which included HAMP and HARP) program, under TARP and "Treasury contracts", we learned of after the FHFA-IG complained about FnF not being reimbursed for the costs (heavy handouts to borrowers, mortgage servicers and the holders of the mortgages)

Likewise, justice Alito, unaware that always plain language controls, with this add-on, he legalized other programs that utilized FnF for government policies during a conservatorship: sale of loans to women-owned businesses, minority-owned businesses, neighborhood associations, etc.

As seen, for instance, in this screenshot taken from a FHFA report during Mel Watt's tenure:

By the way, Mel Watt famous for the: "CRT, responsible innovation" that is taking capital away from FnF, which sounds a lot like representative Maxine Waters recently with: "safe financial innovation", that can be assumed that she was talking about the bitcoin scam.

It can never be the extortion of their profits, because that's the Core Capital necessary for the "rehabilitation of FnF", Justice Alito's prerequisite.

Today, FnF have an adjusted $-216 billion in their Retained Earnings accounts, meant to absorb future "unexpected" losses and pay future dividends.

Let alone that capital distributions are restricted...., if you know what that means.

This man called his boss "coward"! Staged. 🤡

In charge of promoting his book: "We've been robbed!"

It's all about stock price manipulation.

The idea that the banks won't buy 30-year securities anymore, just because now they are compelled to record the unrealized loss on Equity (AOCI line item), like anyone else does, is insane.

There have been two problems with the U.S. banks that are interrelated: Wrong loss on Assets and a hidden capital hole.

-Liquidity crisis: debt securities in Held-To-Maturity portfolios, valued at amortized cost with a small write-down, just like a loan. It's only allowed either a loss on fair value (volatility in earnings) or a loss on AOCI (directly on Equity). Thus, there are two categories, not three as the Federal Reserve claims on a Schedule on how to fill out a Balance Sheet.

-The hidden hole in Equity that has popped up in 2023. The accumulated losses on debt securities mentioned before, should have been funded the last years (asset sales, issuance of stocks, Prompt Corrective Actions like dividends and stock buybacks suspended). The problem has been FDIC rulemaking that authorized them an AOCI opt-out election, when calculating the CET1 = Retained Earnings + AOCI (accumulated unrealized losses) + common stock par value - Treasury Stock (buybacks) + APIC.

CET1 = CE + regulatory adjustments.

The FDIC has some explaining to do.

BOTTOM LINE

The key: all of the above is related to a bank that is not "an advanced approaches FDIC-supervised institution", that may make a one-time election to opt out of recording AOCI.

That is, for banking organizations with assets between $100B and $700B (Categories III and IV)

This will change with the proposed changes in the capital requirements, now in place with a comment period: "Basel III framework endgame".

There won't be opt-out election. Those banks will be required to include the full AOCI on the CET1, phased in during a 3-year transition period, beginning in July 1, 2025.

This is about a flawed rulemaking (AOCI opt-out election) for the regional banks and Medium- and Small-sized banks, but unrelated to the large banks (Category II and GSIBs) that simply broke the rules (Trump's famous deregulation rhetoric), because they didn't have this election.

So, the large banks will have higher capital requirements as well, but it's because they are catching up with the compliance with the rules they broke.

Rogue bankers, as seen in the latest earnings report of JPM, want to pass the new proposal Basel framework endgame, off as a brand new rulemaking with a transition period for GSIBs beginning in 2025, when they were already subject to these requirements.

Deregulation, break the laws, external position (off-Balance Sheet; off-Federal Budget),.... The Age of Plunder.

DISCLAIMER: It's my understanding after reading the proposed Basel III endgame.

The law doesn't authorize the sacking of private corporations during a Conservatorship and under the Charter Act.

What Pagliara is doing with that tweet, is stock price manipulation.

The judges haven't authorized it either (judge Willett and justice Alito), with some exceptions, for instance, the U.S. Court of Appeals for the Sixth Circuit.

The same court that omitted the count of 210 days under the FVRA (Rop case. Berkowitz's attorney, David Thompson), because it coincided exactly with the Final Rule July 20, 2011, that enables the 2nd and 3rd phases of the Separate Account plan "a capital distribution for Recap", CFR 1237.12, and where DeMarco set a trap declaring in 2011 that the Lamberth damages are a capital distribution too, that would uncover 12 years later, that the other capital distributions (a financial concept that has been covered up in court all along), like dividends and gifted SPS, are restricted too when FnF are undercapitalized (IN GENERAL)

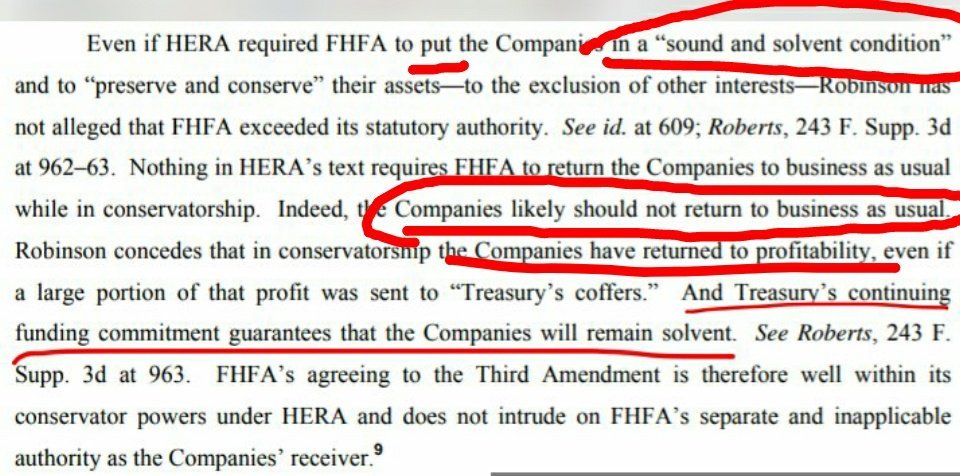

This court, with the important Robinson case (2017. Berkowitz's attorney, David Thompson, again), claimed that "put in a sound condition" in the FHFA-C's Rehab Power, was achieved with the return to profitability, "even if a large portion of that profit was sent to 'Treasury's coffers'". Unaware that, in a financial company, the soundness is measured with the capital levels, where the earnings must be retained by the enterprises in order to be recorded as Core Capital or CET1 Capital.

Likewise with the "put in a solvent condition", the judge claimed that it's achieved with the Funding Commitment from the UST (emanating from the Charter Act by the way: Authority of Treasury to Purchase Obligations), when it's measured with financial ratios, like Debt/Ebitda; Liquidity ratios,... and it includes the reduction of the obligations SPS as well, a debenture with the taxpayer that has to be paid back asap, which is what has been done with the assessments sent to Treasury under the guise of dividends, as per the law (a NWS dividend, the fastest speed to that end, as the 10% dividend prompted a death spiral)

Let alone that "put" means "to restore", and these judges even dared to claim that "the Companies likely should not return to business as usual". No one asked for their opinion on this subject.

The "may" word preceding this Rehab power, is some leeway related to activities that may incur losses or increase risk. The same with the "take any action authorized by this section, in the best interests of the Agency" of the Incidental Power, as explained by Freddie Mac.

It's not an authorization to break the law at its will.

There is a reason why to became FHFA Director, it's required by law knowledge in financial matters and the mortgage market.

The same reason why the courts are precluded from taking actions that affect the conservatorships. U.S. Code 4617 (f).

With an adjusted $402 billion capital shortfall over Minimum Leverage capital requirement, Sandra Thompson has a lot of explaining to do.

Let alone an adjusted $-216 billion Accumulated Deficit Retained Earnings account to absorb future "unexpected" losses and pay dividends.

The Warrant is a security that was authorized "to (iii) protect the taxpayer", regardless that it was issued for free to avoid this prerequisite on purchases by UST. Barred in the Fee Limitation, both as collateral or as a higher compensation on the funding commitment. Therefore, an illegal collateral.

An exercise price of $0.00001ps confirms that it had the purpose of collateral of the SPS (a guaranty for the repayment of the debenture SPS. Hence the "to protect the taxpayer"), although the true purpose was the assault on the ownership by Wall Street and the Community Banks, paying nothing, through the covenant 2.1: shares assigned to any Person (BLK, JPM, MS, BX, GS, etc.)

They become owners of FnF one day by immaculate conception.

Fat-finger error: $402B capital shortfall, not $492B.

Those calling for the release, are gibbering.

Gary Hindes, "Stephan" which is how Howard calls David Stevens, to later state:

Separate Account? I don't know what that is

Its current capital is $74 billion

It turns out that the Law states otherwise.

Those payments are restricted. Besides, no dividend was ever possible to disbursed, out of an Accumulated Deficit Retained Earnings account (Dividend, a distribution of earnings. A capital distribution. They are not interest payments.)

I would break the FHFA-C's Rehab Power as well, like the initial $1B gifted SPS (offset: reduction of Additional Paid-In Capital account, Core Capital).

Therefore, the FHFA and the UST have been carrying out a Separate Account plan, similar to the one established by law in the 1989 bailout of the FHLBanks, Section: "SEPARATE ACCOUNT for the reduction of principal of the obligation RefCorp". Source. Assessments reinvested in zero coupon Treasuries after the payment of interests, which is the same as today where the UST is the custodian of the funds. All of it, as dividends are restricted. So, the full assessment is applied towards the reduction of the obligation SPS ("Obligation in respect of Capital Stock": SPSPA).

They decided that it would continue with a Separate Account for the recapitalization ("it supplements...."), with the same assessments as before, enabled in a Final Rule (CFR 1237.12) enacted two weeks before the FHFA unveiled a proper Recapitalization plan for the FHLBanks with the same assessments as before. But it was on-Balance Sheet Recap plan. With FnF was an off-Balance Sheet Recap plan (External Position)

Why did the FHFA treat FnF and the FHLBanks different?

The key: the FHFA-C's Incidental Power allows it to mess around and mislead, applying those assessments towards the exceptions to the restriction: reduction of SPS and for the recapitalizition. The latter enacted by DeMarco on the Time Limitation day as Acting Director (CFR 1237.12), so he wanted to make sure that this ongoing plan is lawful.

More importantly, FHFA's DeMarco forged the exit strategy in that Final Rule, declaring that the payment of Securities Litigation judgments is a capital distribution (CFR 1229.13 number 3, with an express grant of authority in the FHEFSSA, number 3), at a time when no litigation existed. There is no authority of FHFA-C to approve this or other capital distributions in its Incidental Power, regardless of the FHFA's best interests, because that's not "authorized by this section" (Rehab Power) written in the same sentence and omitted by judge Sweeney (judge Willett and justice Alito agreed that it's about the rehabilitation of FnF). A time-bomb that has exploded now in the Lamberth court, where the damages cannot be paid as they are restricted, just like all other capital distributions when FnF are undercaptialized(IN GENERAL): dividends and today's SPS increased for free (number 1 in the FHEFSSA's definition of Capital Distribution posted before).

The cover-up of these statutory provisions is a felony of Making False Statements and also, stock price manipulation.

If it's done in formal documents (Howard's SCOTUS amicus brief with "SPS, non-repayable securities"; Pagliara's book, court briefs, etc.), they also will have to pay us Punitive Damages ($4.8 billion)

The point is that we must legalize every action, whether they want it or not, not to cry out loud all the felonies committed "We've been robbed!" ; "$420B worth of Core Capital is gone, either with $301B dividend sent to UST and $118B SPS increased for free that carries an offset", or to come out with "What would have happened if the NWS dividend hadn't existed?", like the plaintiff Bryndon Fisher, because it existed.

The $420B is the Common Equity held in escrow, in accordance with the law, in an ongoing plan of deception. Watch my signature image below to see a normal Conservatorship under the Charter Act, or a FHFA conservatorship adjusted for the Separate Account plan (A Common Equity Sweep). Same image in both cases.

Boy! Capital distributions are restricted. PROHIBITED.

Preface of the July 20, 2011 Final Rule:

Also, FHFA explained that the suspension of dividend payments is related to Capital Adequacy matters. It isn't restricted on a whim:

HERA inserted this amendment in the FHEFSSA: Restriction on Capital Distributions.

Navy Hedge Fund posts false numbers.

I took me 10 seconds to download the S.E.C. filing with the 2006 Earnings report and see that, as of December 31, 2006:

-Interest-only ARM: 9%

-Subprime loans: 2.2%

And you have posted 18% and 23%, respectively.

I reckon that there has never been Interest-only fixed rate mortgages.

You cite as source the "Fannie Mae financial reports", but I'd like to know who sent you the image.

This is an actual screenshot of the report:

Besides, the company assures that:

We did not participate in large amounts of these non-traditional mortgages in 2004, 2005 and 2006.

SPSPA +amendments are fact sheets emanating from the law/regulations.

The latest, the July 20, 2011 Final Rule enabling the 2nd phase and 3rd phase of the Separate Account plan, commented in my prior post.

So, all the following amendments emanated from this rule and every quarter there are violations of this Final Rule, that is telling you that a capital distribution must be applied towards the recapitalization, unless the FHFA and the UST unveil the Separate Account plan.

Quit peddling the breach of contract, with a dividend that was impeccably suspended. Get over it.

Moving foreword, every quarter that the LP and warrants remain will create a new breach of contract. It is not hard to figure out. The Gov has acknowledged this by not appealing the jury verdict.

The "damage" arose from the retention of a security.

These are the exact same words written in the preface of the famous July 20, 2011 Final Rule "for the transparency of the Conservatorships", where the FHFA talks extensively about the payment of Securities Litigation judgments.

Then, the issuer of those securities is the one to pay the claim of breach of "implied contract" (fiction), not the FHFA as you claim:

FHFA doesn’t have money to pay the compensation.

The Constitutional 210-day clock (FVRA) ended on July 20, 2011.

$402B Capital shortfall: NO release and NO Lamberth damages.

Capital shortfall over Minimum Leverage Capital requirement.

Yet, you peddle the idea of release as a kind of settlement of the damages.

The

"Just my opinion"

These are ALL the SPS increased for free:

-Initial $1 billion SPS issued for free, debited from the Additional Paid-In Capital account (Core Capital), on September 2008.

Then, all other SPS that are missing on the Balance Sheets along with their offset (Financial Statement fraud) and part of the same Separate Account dressing that is meant to make someone end up with: "It's complicated", also known as "regulatory gibbering" that the plotters accompany "doing the twist", as seen in the comment that I'm replying to.

It is kind of difficult to understand.

Starting 2021

"Seeking Alpha are Hedgie’s Shill"

Correction: the initial SPS were $1 billion, not 3.

It's plain English language, plaintiff Joshua Angel. You use💩fan.

It's a brand new compensation to UST, written in a brand new covenant.

We call it NWS 2.0 to differentiate it from the NWS dividend.

But the same Common Equity Sweep, as seen in the image posted before about Freddie Mac Adjusted Net Worth Activity.

UST press release at the time :

The same occurred with the initial $3 billion SPS issued for free. But these SPS and the corresponding offset, do appear on the Balance Sheets.

It's been always a Common Equity Sweep.

(The tweet below is a reply to your comment)

In either of the three phases of the Separate Account plan:

1st. 10% dividend.

2nd. NWS dividend.

3rd. SPS LP increased for free in the absence of dividend to UST. The Common Equity is swept to Treasury again, through the offset attached to the gifted SPS that are missing on the Balance Sheet, as we can see in this image with Freddie Mac. By they way, there is a typo because it should say Total Comprehensive Income, instead of Comprehensive Income, though they are the same figure or similar, since OCI is always $0 or very small.

The Retained Earnings accounts stand at $-216 billion as of Sept 30, 2023 FnF together, adjusted for the offset mentioned before ($-118 billion reduction of Retained Earnings).

$-98 billion Accumulated Deficit Retained Earnings accounts officially posted on their Balance Sheet (pending recording the SPS LP that is missing. Financial Statement fraud):

Freddie Mac Balance Sheet.

Fannie Mae Balance Sheet.

This account is the only item that really absorbs the future "unexpected" losses, meaning that this account bears the losses. The Capital Stocks do not bear losses, but they offset a negative RE account, so the resulting sum maintains the Net Worth with positive credit.

The Common Equity Sweep has prevented this account from being replenished and then, to continue its build-up, for the normal functioning of a financial company. This is why it's assumed that this Common Equity generated in Conservatorship, is held in escrow, in order to uphold the law:

-FHFA-C's Rehab Power.

-Restriction on Capital Distributions. Exceptions.

Besides the fact that no dividend was ever possible with a negative Retained Earnings account (Dividend, a distribution of earnings.)

Thanks to the FHFA-C's Incidental Power that allows it to mess around, if the endgame is the rehabilitation of FnF. A prerequisite outlined by judge Willett and justice Alito.

So, the Separate Account comes to force them to uphold the law and rehabilitate FnF, regardless of all their twists.

Timothy Howard, Guido, navycmdr with "the capital requirement is a limit" instead of a "minimum" required, Glen Bradford: "the SPS on the balance sheet", omitting the SPS absent from the balance sheet (Oooops!), among others, love to do the twist, pretending that FnF are in a good financial condition now.

What was swept to UST was the NW increase, comprised of (Income Stmnt):

— Conservatives against Trump (@CarlosVignote) December 29, 2023

-Comprehensive Income(Net Income)

-Other Comprehensive Income.

That later is accumulated on the Bce Sheet, resp.:

-Retained Earnings

-AOCI

Both accounts make up the CE.

A Common Equity Sweep.

Nowadays,NWS 2.0 pic.twitter.com/wOjLzFumF5

Exactly. 'Why' is the question. You are showing progress.

So why is it on the balance sheet of the audited financials.

English much? You took the idea in the bathroom,Guido.

No one should have expectations of getting Lamberth damages.

JPS should pay PAR plus Lamberth damages.

Bradford, you are clueless about stock valuation. Lol

For Equity stock valuation, watch the Net Worth first.

According to the FNMA balance sheet.

Is Timothy Howard behind the widespread typo "ECRF"?

It's Enterprise Regulatory Capital Framework (ERCF), which is how the FHFA calls the February 16, 2021 Capital Rule.

The last two days, I realized that navycmdr and FOFreddie wrote the same typo "ECRF".

Using the search engine of Ihub, we can see all the users that have written the same typo on the Fannie Mae public message board.

It all began with a user posting a comment from Timothy Howard on his blog, on May 15th, 2023, where he uses ERCF-ECRF intermittently: https://investorshub.advfn.com/boards/read_msg.aspx?message_id=171923683&txt2find=ecrf

Then, we see that the ones that write this typo are always people that peddle the lie about expectation of ERCF changes. So, it's an organized group that has the same objective.

We know that Howard is the one that began the idea of ERCF changes out of the blue, with a 2.5%, without specifying what is 2.5% of what. Which is the same stance spread by the gang.

FoFreddie:

Could the run up be in advance of a 2.5% ECRF?

The Separate Account plan is on everyone's desk, because it's set forth in the laws in force, FHEFSSA and Charter Act, as amended by HERA, plus the most relevant regulations, like the 2011 Final Rule "for the transparency of the Conservatorships".

So, you just have to download them in your computer.

There are a series of restrictions and exceptions.

Let alone have a minimum knowledge in Finance, like dividends, a distribution of earnings. There is no such thing as "mandatory dividends", as the Wall Street law firm representing FHFA stated in the Lamberth court.

The first restriction on dividends, is that you need, ar least, a positive balance Retained Earnings account, to pay out (Adjusted $-216 billion as of September 30, 2023 together). Then, there are thresholds to meet.

The Separate Account renders all the lawsuits, meritless.

The joke's on you.

The screenwriters of FANNIELAW & FREDDIEORDER, a comedy remake sitcom and parody of the famous American drama television series LAW & ORDER, went on strike for disagreement about the course of events and guidelines, with President Biden portrayed as a tyrant and with the attorneys Rebecca Musarra, a renowned Human Rights advocate, and Bryndon Fisher, in the role of Shareholders' Rights advocate, coming to the rescue with a Takings case that gives FnF away to the government.

This is the President of the Association of Screenwriters:

The storytelling is caca and no one believes it.

Capital distributions are restricted.

No. Navy commodore spread lies, about "market expectations" on ERCF changes on December 31st. It was not "his opinion" as you falsely claim with another lie.

He was called out for spreading the same lie on Sunday:

a leak of new GSE Capital Rule limits ?

Don't spread lies, navy commodore. Caca.

new ECRF Rule - expected before Dec 31st !

Really? That's Bryndon Fisher's defense, knowing that you are the de facto spokesperson for Pagliara and Fisher?

That he could have done it better. So, all comes down to a fight about who is a better attorney, notwithstanding that our negotiator on #Fanniegate is requesting penalties on all the attorneys and plaintiffs, plus the sponsors, for stock price manipulation and making false statements, for the cover-up of multiple statutory provisions and financial concepts (Restriction on Capital Distributions, original UST backup of FnF, FHFA-C's Rehab power, etc.), besides a conspiracy to rip off the shareholders.

Fairholme didn't make a convincing case and even ruined a sure dunk for Fisher in the COFC.

FISHER SEEKS TO BE IN THE SPOTLIGHT

— Conservatives against Trump (@CarlosVignote) December 25, 2023

Derivative Taking claim was already dealt with several times:

-J.Willett/J.Alito:"Rehabilitate FnF"(Separate Acct)

CFC-related cases:

-Interlocutory appeal

-Plaintiff Barrett(Fairholme)filed Derivative Taking claim @ SCOTUS👇

Denied.#Fanniegate https://t.co/AtqspKqUUx pic.twitter.com/cuerNTlvuf

Yeah,yeah,...but you'll be humiliated again if you repeat that the payment of Securities Litigation judgments isn't a capital distribution restricted, exposing the Separate Account plan from the beginning (with unavailable funds for distribution as dividend, as assessments sent to Treasury to reduce the SPS and Recap, and today's SPS LP increased for free that holds the Common Equity in escrow as well.)

An External Position.

DeMarco set a trap in the 2011 Final Rule.

The conservator's Incidental Power allows it to mess around.

You are doing great!

You are wrong and an embarrassment.

You keep on concealing that it was nws DIVIDEND.

A capital distribution, restricted. Just like today's SPS LP increased for free and the payment of securities litigation judgment in the Lamberth court.

The same occurs with the frivolous lawsuits that conceal these facts.

The breach of implied contract is, thus, fiction.

The Separate Account plan legalizes every single action.

Any comment, plaintiff Bryndon Fisher?

The Supreme Court already DENIED a Derivative Takings claim.

Spot on! I posted yesterday that the plaintiff Bryndon Fisher might be preparing a third appeal illegally, when he saw that his "innovative stance" about a Derivative claim on behalf of Fannie Mae that he is peddling all the time (on Twitter and Ihub as well. Also borrowing Guido from Pagliara, to praise him and echo his stance), was already taken by other plaintiff of the related cases, in a question presented in the Supreme Court.

Fisher lost his opportunity to file an appeal in the Supreme Court on time, maybe because his questions were already filed by other plaintiffs in related cases. So, he thought that he had lost yet again another opportunity to be in the spotlight and pretend to be a "Fanniegate hero", like our other enemy Glen Bradford that calls himself that.