Wednesday, January 03, 2024 2:54:00 AM

The law doesn't authorize the sacking of private corporations during a Conservatorship and under the Charter Act.

What Pagliara is doing with that tweet, is stock price manipulation.

The judges haven't authorized it either (judge Willett and justice Alito), with some exceptions, for instance, the U.S. Court of Appeals for the Sixth Circuit.

The same court that omitted the count of 210 days under the FVRA (Rop case. Berkowitz's attorney, David Thompson), because it coincided exactly with the Final Rule July 20, 2011, that enables the 2nd and 3rd phases of the Separate Account plan "a capital distribution for Recap", CFR 1237.12, and where DeMarco set a trap declaring in 2011 that the Lamberth damages are a capital distribution too, that would uncover 12 years later, that the other capital distributions (a financial concept that has been covered up in court all along), like dividends and gifted SPS, are restricted too when FnF are undercapitalized (IN GENERAL)

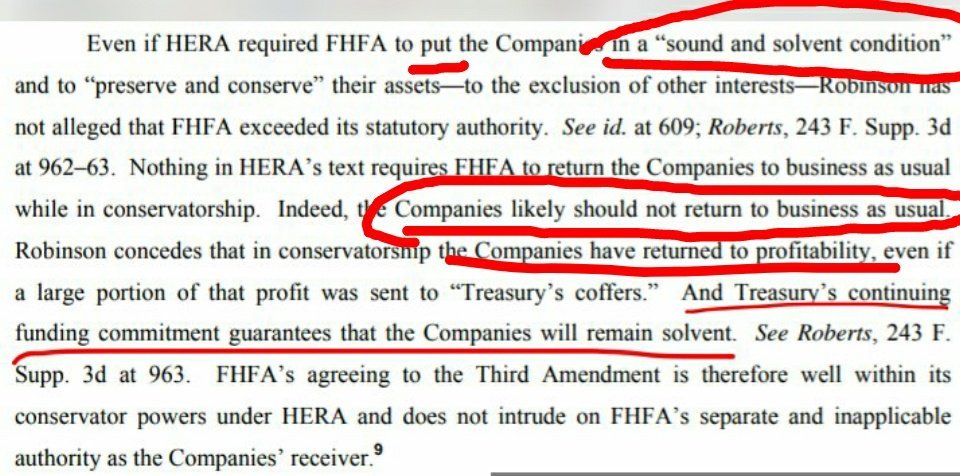

This court, with the important Robinson case (2017. Berkowitz's attorney, David Thompson, again), claimed that "put in a sound condition" in the FHFA-C's Rehab Power, was achieved with the return to profitability, "even if a large portion of that profit was sent to 'Treasury's coffers'". Unaware that, in a financial company, the soundness is measured with the capital levels, where the earnings must be retained by the enterprises in order to be recorded as Core Capital or CET1 Capital.

Likewise with the "put in a solvent condition", the judge claimed that it's achieved with the Funding Commitment from the UST (emanating from the Charter Act by the way: Authority of Treasury to Purchase Obligations), when it's measured with financial ratios, like Debt/Ebitda; Liquidity ratios,... and it includes the reduction of the obligations SPS as well, a debenture with the taxpayer that has to be paid back asap, which is what has been done with the assessments sent to Treasury under the guise of dividends, as per the law (a NWS dividend, the fastest speed to that end, as the 10% dividend prompted a death spiral)

Let alone that "put" means "to restore", and these judges even dared to claim that "the Companies likely should not return to business as usual". No one asked for their opinion on this subject.

The "may" word preceding this Rehab power, is some leeway related to activities that may incur losses or increase risk. The same with the "take any action authorized by this section, in the best interests of the Agency" of the Incidental Power, as explained by Freddie Mac.

It's not an authorization to break the law at its will.

There is a reason why to became FHFA Director, it's required by law knowledge in financial matters and the mortgage market.

The same reason why the courts are precluded from taking actions that affect the conservatorships. U.S. Code 4617 (f).

With an adjusted $402 billion capital shortfall over Minimum Leverage capital requirement, Sandra Thompson has a lot of explaining to do.

Let alone an adjusted $-216 billion Accumulated Deficit Retained Earnings account to absorb future "unexpected" losses and pay dividends.

The Warrant is a security that was authorized "to (iii) protect the taxpayer", regardless that it was issued for free to avoid this prerequisite on purchases by UST. Barred in the Fee Limitation, both as collateral or as a higher compensation on the funding commitment. Therefore, an illegal collateral.

An exercise price of $0.00001ps confirms that it had the purpose of collateral of the SPS (a guaranty for the repayment of the debenture SPS. Hence the "to protect the taxpayer"), although the true purpose was the assault on the ownership by Wall Street and the Community Banks, paying nothing, through the covenant 2.1: shares assigned to any Person (BLK, JPM, MS, BX, GS, etc.)

They become owners of FnF one day by immaculate conception.

What Pagliara is doing with that tweet, is stock price manipulation.

The judges haven't authorized it either (judge Willett and justice Alito), with some exceptions, for instance, the U.S. Court of Appeals for the Sixth Circuit.

The same court that omitted the count of 210 days under the FVRA (Rop case. Berkowitz's attorney, David Thompson), because it coincided exactly with the Final Rule July 20, 2011, that enables the 2nd and 3rd phases of the Separate Account plan "a capital distribution for Recap", CFR 1237.12, and where DeMarco set a trap declaring in 2011 that the Lamberth damages are a capital distribution too, that would uncover 12 years later, that the other capital distributions (a financial concept that has been covered up in court all along), like dividends and gifted SPS, are restricted too when FnF are undercapitalized (IN GENERAL)

This court, with the important Robinson case (2017. Berkowitz's attorney, David Thompson, again), claimed that "put in a sound condition" in the FHFA-C's Rehab Power, was achieved with the return to profitability, "even if a large portion of that profit was sent to 'Treasury's coffers'". Unaware that, in a financial company, the soundness is measured with the capital levels, where the earnings must be retained by the enterprises in order to be recorded as Core Capital or CET1 Capital.

Likewise with the "put in a solvent condition", the judge claimed that it's achieved with the Funding Commitment from the UST (emanating from the Charter Act by the way: Authority of Treasury to Purchase Obligations), when it's measured with financial ratios, like Debt/Ebitda; Liquidity ratios,... and it includes the reduction of the obligations SPS as well, a debenture with the taxpayer that has to be paid back asap, which is what has been done with the assessments sent to Treasury under the guise of dividends, as per the law (a NWS dividend, the fastest speed to that end, as the 10% dividend prompted a death spiral)

Let alone that "put" means "to restore", and these judges even dared to claim that "the Companies likely should not return to business as usual". No one asked for their opinion on this subject.

The "may" word preceding this Rehab power, is some leeway related to activities that may incur losses or increase risk. The same with the "take any action authorized by this section, in the best interests of the Agency" of the Incidental Power, as explained by Freddie Mac.

It's not an authorization to break the law at its will.

There is a reason why to became FHFA Director, it's required by law knowledge in financial matters and the mortgage market.

The same reason why the courts are precluded from taking actions that affect the conservatorships. U.S. Code 4617 (f).

With an adjusted $402 billion capital shortfall over Minimum Leverage capital requirement, Sandra Thompson has a lot of explaining to do.

Let alone an adjusted $-216 billion Accumulated Deficit Retained Earnings account to absorb future "unexpected" losses and pay dividends.

The Warrant is a security that was authorized "to (iii) protect the taxpayer", regardless that it was issued for free to avoid this prerequisite on purchases by UST. Barred in the Fee Limitation, both as collateral or as a higher compensation on the funding commitment. Therefore, an illegal collateral.

An exercise price of $0.00001ps confirms that it had the purpose of collateral of the SPS (a guaranty for the repayment of the debenture SPS. Hence the "to protect the taxpayer"), although the true purpose was the assault on the ownership by Wall Street and the Community Banks, paying nothing, through the covenant 2.1: shares assigned to any Person (BLK, JPM, MS, BX, GS, etc.)

They become owners of FnF one day by immaculate conception.

Recent FNMA News

- Fannie Mae Reports Net Income of $3.7 Billion for First Quarter 2026 • PR Newswire (US) • 04/29/2026 11:24:00 AM

- Fannie Mae Releases March 2026 Monthly Summary • PR Newswire (US) • 04/28/2026 12:30:00 PM

- Fannie Mae Plans to Report First Quarter 2026 Financial Results on April 29, 2026 • PR Newswire (US) • 04/27/2026 12:00:00 PM

- Fannie Mae Announces Credit Score Model Updates to Advance Credit Score Modernization • PR Newswire (US) • 04/22/2026 05:02:00 PM

- Fannie Mae Releases February 2026 Monthly Summary • PR Newswire (US) • 03/26/2026 08:05:00 PM

- Fannie Mae Announces Results of Tender Offer for Any and All of Certain CAS Notes • PR Newswire (US) • 03/02/2026 02:00:00 PM

- Fannie Mae Releases January 2026 Monthly Summary • PR Newswire (US) • 02/26/2026 09:05:00 PM

- Fannie Mae Announces Tender Offer for Any and All of Certain CAS Notes • PR Newswire (US) • 02/23/2026 02:00:00 PM