News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

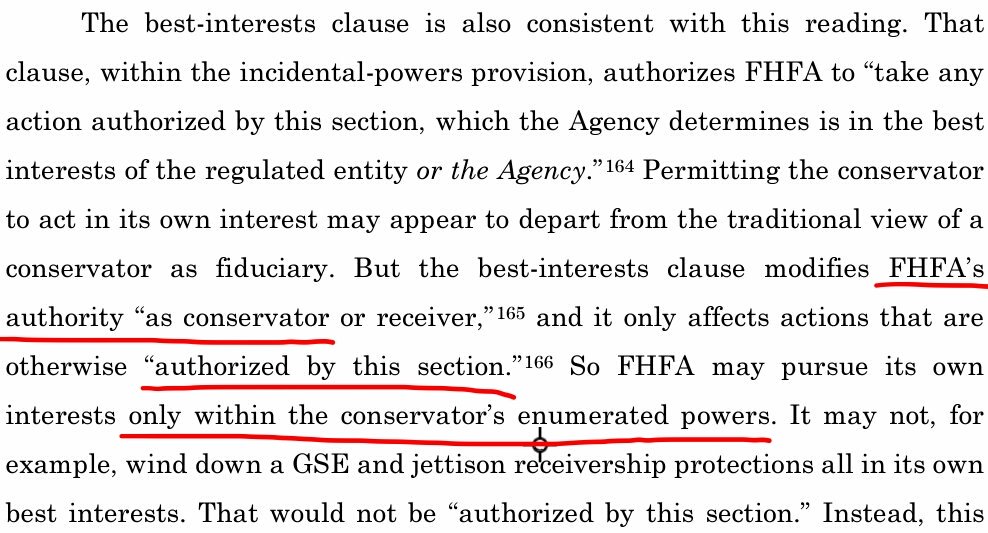

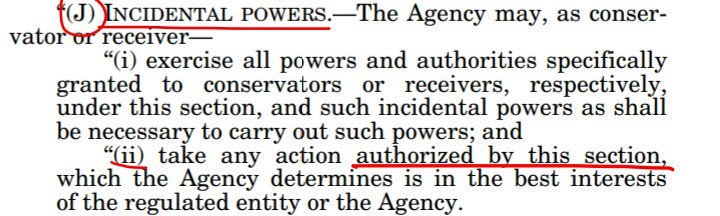

Justice Alito flagged the Separate Account plan, stressing the rehabilitation of FnF as prerequisite (adding: the Marxist way) in his interpretation of the FHFA-C's Incidental Power he based his opinion on. Although he didn't mention it, this "Rehab" is captured in the "authorized by this section" in the same sentence he was reading (the Rehab power), as explained by judge Willett in the prior en banc ruling, 5th Cir.: "Authorized by this section means any action within the conservator's enumerated powers".

This is why it's considered that both were synchronized.

You can read both quotes here.

You should have learned what Rehab means before filing your lawsuits, first with judge Lamberth (You were allowed to change the defendants in the Appellate Court to claim that the management should have stored the dividend on your non-cumulative dividend JPS) and now with judge Sweeney.

Also, you should have learned that they were interpreting an Incidental Power, that, by definition, are actions that help to fulfill the main power.

The rehabilitation in a financial company is related to restoring capital levels (Soundness) and related to the level of debt (Solvency. SPS, a debenture too). That is, put FnF in a sound and solvent condition (the FHFA-C's power)

This is why a dividend is restricted in the law FHEFSSA when a company is undercapitalized: it reduces the core capital. So, a breach of the FHFA-C's Power.

Also, you should have learned that a dividend is a distribution of Earnings and Retained Earnings is Core Capital.

You can't rehabilitate a company allowing dividend payments.

Then, in truth, the FHFA used its Incidental Power (any action...) to lie about these capital distributions that weren't actual dividends due to all of the above.

No actual dividend existed, nada, zero, nitchs.

Justice Alito upheld the Separate Account plan. He just tried to fool us with the objective to change the outcome.

You can only play the fool saying that you didn't know what Rehab means, to be relieved of accountability. It won't make a difference.

Others like Gary Hindes, chose to amend his lawsuit and remove the prior references to a breach of the conservator's Rehab power. This is because he was told that he can't challenge the NWS dividend using the FHFA-C's Rehab power as we can read in the screenshot, while defending at the same time the 10% dividend, as both reduce the same core capital and thus, the same breach of the Rehab power he was crying out loud.

This is why the SCOTUS was activated to use the Incidental Power to authorize the NWS dividend, but it failed again when Justice Alito started off his sentence with: "FHFA may rehabilitate FnF in a way....". All roads lead to Rome and the actions through the Incidental Power must be authorized in the Power.

There is only one way to rehabilitate a financial company and he, in truth, was authorizing the Rehab secretly, the Marxist way: beneficial to the FHFA and the public (a lengthy Conservatorship, more extortion of resources out of FnF to boost the finances of interest groups and cronies, etc.).

At some point, the Common Equity currently held in escrow, which isn't in the best interests of FnF as Justice Alito pointed out as well (Today, there is no rehabilitation whatsoever: awful ERCF tables; $-216 billion Retained Earnings accounts that absorb future losses; $302 billion SPS outstanding; Financial Statement fraud), will have to be returned to their Balance Sheet, for the Rehab in the real world, not in a Separate Account (Justice Alito's prerequisite), and then, FnF resume independent operations.

Justice Alito upheld the third amendment, NWS dividend, explaining magnificently that it was done to prevent the death spiral, that is, the 10% dividend prompted more draws from UST, more SPS, a higher dividend the next quarters and thus, a reduction of the UST funding commitment.

A NWS dividend is the fastest speed for the Separate Account plan.

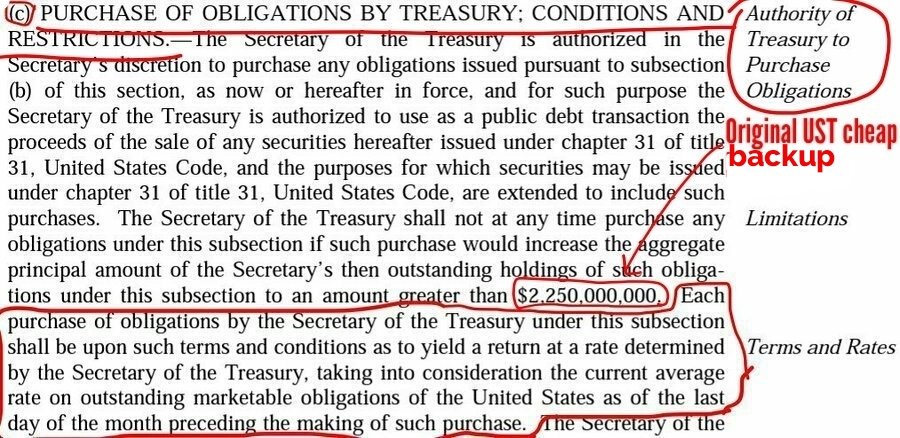

A NWS dividend is as legal as the 10% dividend (an infinite rate is authorized in the 2nd UST backup of FnF. Subsection (g)). And both, restricted. So, quit cherry-picking the dividend rate you want, because for that, we have the original UST backup of FnF, subsection (c), that takes into consideration the Treasury yields as of the end of the month preceding the purchase, estimated at a weighted-average 1.8% rate after applying a 0.5% spread.

Charter subsection (c): any obligation of subsection (b).

Subsection (b): redeemable obligations, such as SPS (Obligations in respect of Capital Stock)

A Separate Account plan has repaid the SPS using the exception (reduce the SPS, which is not a "refinancing option" as you claim, since the same cash required in the law was raised through the double-entry accounting with the increase in the Common Equity of FnF, as seen in my signature image below) to the Restriction on Capital Distributions in the FHEFSSA and thus, we don't have to wait to the SPSPA's OPTIONAL PAYDOWN upon termination of the funding commitment, if the SPS were fully repaid at the end of 2013 in Freddie Mac (image below) and end of 2014 in Fannie Mae, according to the law, which supersedes an agreement SPSPA, if you weren't aware of. So, quit bringing up an agreement between rogue Federal Agencies, because everything is being unwound to uphold the laws in force, and those laws are the FHEFSSA and the Charter Act, as amended by HERA. Not just HERA, otherwise you are covering up the rest of the law that wasn't amended by HERA.

You are a champion of deception, pro se plaintiff.

What's the point in agreeing with my statement that the capital distributions are forbidden (dividends, today's gifted SPS and the payment of damages), if later you agree with the NWS dividend. Deleting with Tipp-Ex "dividend", after NWS, won't change that it was a NWS dividend.

Then, calling the 10% dividend, "10% interest".

Let alone that you repeat on this board with you 30 different ID's: "THE LAW!", when no law is mentioned in your lawsuits.

Boooo!

You haven't responded to my question yet: How is judge Sweeney doing?

Day 22. Corrupt plaintiffs' plea deal negotiations resumed and continued to 9/5/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

The law isn't HERA but the FHEFSSA-Charter Act, as amended by HERA, pro se plaintiff with one of your 30 different ID's: HappyAlways, Barron, Vancmike, Fannie Heeeey, EternalPatience, stvupdate, etc.

The resolution of Fanniegate isn't about... "What if the NWS dividend hadn't existed". "What if...". Commonly known as do-overs.

The 10% and NWS dividends existed and they are forbidden when FnF are undercapitalized, besides there weren't funds available for distribution as dividend out of a Retained Earnings account with deficit all along.

We use the FHFA-C's Incidental Power (take any action...) to apply these capital distributions (no actual dividend payment) towards the exception in the law (reduce the debenture SPS) and, once fully repaid, for their Recapitalization in the CFR 1237.12, complying with the FHFA-C's Rehab power as well (solvent condition and sound condition, respectively)

That is, the legalization of all the FHFA-UST's actions with an Incidental Power that allows the FHFA to lie about it with a Separate Account. No do-overs.

You want to conceal the rest of the FHEFSSA and the Charter Act that wasn't amended by HERA:

- The original low cost UST backup of FnF, about purchases of any (subsection (c)) redeemable obligation (subsection (b)), such as SPS.

- Besides, the definitions of each capital requirement, to learn that they are met with Core Capital/Total Capital, not with the Net Worth as the plotters peddle all the time.

Meeting the Capital levels is what soundness is about, in the FHFA-C's Rehab power.

- Or even the Fee Limitation of the United States as part of the Charter dynamics.

How is judge Sweeney doing, pro se plaintiff?

No, pro se plaintiff. The Request for Input isn't about the Capital Rule and it isn't a Proposed Rule as I told you before.

The question that you are talking about, does not start a debate about the Capital Rule and whether it's high or low, which is what the plotters like you claim because they don't want their dividend to be kept by FnF to build capital and they are reluctant to realize that the FHFA has adopted the Basel Framework because we are heading to a Privatized Housing Finance System.

It's a Request for Input on pricing, in light of the recent LLPA changes.

The question that you are referencing to:

Should risk-based pricing be calibrated to the ERCF?

.jpeg)

Day 21. Corrupt plaintiffs' plea deal negotiations resumed and continued to 9/2/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

FHFA considers the existing FnF Equity holder a captive.

The expulsion of the unwanted shareholders is a longstanding goal by the FHFA with regard to the FHLBanks, enacted in a 2016 Final Rule, but it was an idea first floated in 2010 and the Proposed Rule came out in 2014.

The FHFA called those shareholders unrelated to housing finance "captives".

It gives the FHLBanks a grace period of 5 years to expel any captive from the membership ("Wind down the business with them". It could have kick-started the politicians' and officials' wind-down rhetoric with FnF, meaning the expulsion of the retail investor from the ownership of FnF and from the "other ownership interest" in the case of the JPS holders, with psychological warfare, including the utilization of the U.S. courts and social media)

It would explain why it was postponed through 2016.

2021 is when FnF became Adequately Capitalized under the Separate Account plan, as explained in the comment that I'm replying to.

But they realized that the existing Equity holder kept captive, bothers (unless you are a Community Bank holding JPSs: one-third of them owned JPSs in 2008), as the UST can't exercise its Warrant as scheme for the assault on the FnF ownership by the Industry, as first thought by FHFA and GS's Paulson (covenant 2.1. The shares after exercising the Warrant at $0.00001ps, can be assigned to any Person: BKT, GS, MS, JPM, FHLBanks, etc)

Then, the Supreme Court was activated, in yet another attempt to legalize all the illegal actions and as a way to get rid of the captives paying nothing. It didn't work either.

But we have reached the milestone that corresponds to a recapitalization of FnF to perfection. Under the Separate Account plan, the JPS could be redeemed at their fair value of par value, and FnF remain Adequately Capitalized afterwards.

This recapitalization needs all the capital generated during conservatorship. So, to the Separate Account plan, we have to add the sum from the PLMBS lawsuit settlement, a case brought by the FHFA as conservator on behalf of FnF, net of attorney fees and a refund of the CRT expenses, net (barred in the Credit Enhancement clause. Likely a backdoor Commitment Fee, barred too in the PROHIBITION clause)

The way to get rid of the common shareholders, is to buy the Cs out at their adjusted fair value, that, in the case of a Takings, it's the Common Equity or Book Value.

Adjusted BVPS as of end of June, 2023:

$FNMA = $108

$FMCC = $159

"We can't blame them for trying", you may say.

The reality is that both counterparties in the Fanniegate scandal: the DOJ-peddlers of the government theft story, will have to pay us the same penalty: $4.8B each, for Punitive damages and an all-in settlement of the 9 Securities Law violations during conservatorship (SPS increased instead of issued, to evade the 2009 deadline on purchases; Financial Statement fraud; flawed accounting standard with the Deferred Income, etc), one of them is stock price manipulation, which is what the government theft story was all about.

A voluntary payment in the case of the DOJ, that is compelled to advance the payments of its counterparty and then, figure out how it'll be broken down among the plotters.

FHFA's 2010-2016 RULE EXPELS UNWANTED FHLBANK SHAREHOLDERS

— Conservatives against Trump (@CarlosVignote) August 31, 2023

"5yrs to wind down its business transactions w/ any captive that it had previously admitted to membership"

FnF RECAPITALIZED TO PERFECTION FOR JPS REDEMPTION.

Adjusted Fair Values

JPS=par value

Cs=BV or PER 14.#Fanniegate https://t.co/R7G4PcZBOF pic.twitter.com/JQWaVoTXV6

The Request For Input was related to pricing, not the ERCF which is based on the international standard Basel Framework. So, it will never change. Get over it, pro se plaintiff. You and your more than 30 different ID's that you use on this board.

It was not a Proposed Rule, so it wasn't published on the Federal Register.

Then, we don't have to wait "4 more weeks", which is what it takes for the Publication Date on the Federal Register, had it been a Final Rule approved at an effective date.

You are always posting flawed analyses with Rodney, Vankmike, Barron, etc, to make the reader's head spin, in an attempt to discredit all other valid analyses, at the same time you request a settlement of your flawed lawsuit with judge Sweeney.

An opportunity requested by the FHFA Dtr's hedge funds guard, to complain about the Capital Rule because they refuse to accept that the JPS dividend suspension is all about the recapitalization of FnF, not just for the rehabilitation of FnF, but later the goalpost changed for recapitalization to perfection, to fulfill the 2011 UST-HUD's "recommendations on ending the conservatorships" at the request of the Dodd-Frank Law, with a Privatized Housing Finance System (Adoption of Basel Framework)

Financial illiterate attorneys can't understand the existence of financial instruments created just for capital adequacy matters, like a JPS. The reason why they are recorded in the Core Capital and Additional Tier 1 Capital (AT1) for the Capital ratio (soundness)

The Equity holders have suffered Regulatory Risk, as the capital ratios are remarkably higher than 2008 (For instance, 258% higher in the Risk-Based Capital requirement in Freddie Mac; let alone the Minimum Capital Level, from 0.45% to 2.5% of the off-balance sheet obligations -MBS Trusts-)

Goldman Sachs and Co want to keep at least one of them to continue the current extortion of the resources out of them, with good deals for the investment banks: sale of NPL and RPL, PMI claim pardoned, etc.

The Public-Private partnerships with RTC that saddled the taxpayer with a $30B loss in its investment in RefCORP bonds with the bailout of the FHLBanks in 1989, a scheme spearheaded by DeMarco and Sandra Thompson at the time, that saw an opportunity to use FnF to make up for the losses.

Day 20. Corrupt plaintiffs' plea deal negotiations resumed and continued to 9/1/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

Correction in the post that debunked "SPS, non-repayable securities".

A minor mistake when I called the SPS in early conservatorship "SPS increased for free", as they were increased 1:1 with the draws from UST.

"For free" occurs nowadays, when FnF don't get the corresponding cash for the SPS increased every quarter.

Timothy Howard, ex-FNMA CFO, is to blame for the Conservatorship ($7.4 billion Treasury Stock -stock buybacks- on the Balance Sheet, investments that contravened its statutory mission, reduces the Net Worth and the Core Capital) and now a member of Fairholme's legal team to keep on causing economic harm on the shareholders.

He now faces liabilities for his amicus brief in the Supreme Court.

Howard's EPS target bonus w/ Treas.Stock (buybacks) to blame for Conservtshp too(C.C.reduction)

— Conservatives against Trump (@CarlosVignote) August 31, 2023

LIES/DEBUNKED

-FHFA's suspension of c.classifications affected the FHEFSSA Restr on C.Distrib/https://t.co/kNvg8gqtu1

-SPS, non-repayable securities/https://t.co/TrpKgOGD8j#Fanniegate

Quit posting the useless court news. Not only all the lawsuits are meritless with the announcement of the Separate Account plan, as the dividend was impeccably suspended as per the JPS contract and the law, but also the law prevents the courts from taking any action that affects the conservatorships, 12 U.S. Code § 4617 (f).

The Fisher case was part of the related cases that were dismissed in the Appellate Court long time ago, and the appeal in the SCOTUS, snubbed.

So, now judge Sweeney happens to remember that Fisher filed a sealed lawsuit and requires him to file a redacted version no later that September 29, 2023.

Your assertion in other post that this case is still active, along with other scrambled lawsuits left over in the CFC, only shows that you've been put here by the government.

The point is that this case is NOT dismissed and is going though.

Day 19. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/31/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

BOOM. Our negotiator posts the official dates of earnings reports in which FnF achieved important milestones under the Separate Account plan, that are essential for the optimal stock valuation of both Cs and JPSs, otherwise we'd be talking about the dilution effect on Cs and discount to par value in the JPSs and more important, a fraudulent Conservatorship because currently FnF are NOT rehabilitated ($-216 billion in the Retained Earnings accounts that absorb future losses; $304 billion SPS that have to be paid back; Financial Statement fraud with the gifted SPS absent from the balance sheets,...). Breaking the fhfa-C's Rehab power, which was the prerequisite laid out by both judge Willett and Justice Alito (the Marxist way, he added)

The Separate Account plan is the same as a normal Conservatorship with the dividend suspended. The only difference is that it's being carried out secretly. So, both have the same chart shown in my signature image below.

Another reason why no one can say that the Separate Account plan isn't really happening.

It's time to snub all the attorneys stuck to Fanniegate with a crazy stance based on a Govt theft story, 10% dividend, gifted SPS in the same amount as the Net Worth increase in the quarter and so on and so forth.

FREDDIE MAC/FANNIE MAE

-1Q2021/4Q2021. Adequately Capitalized. Notice that FnF had to wait until they became Undercapitalized (met with Core Capital), as the Minimum Capital level was turned into a Leverage ratio, and now it's higher than the Risk-based Capital requirement that marks the Adequately Capitalized threshold.

-3Q2021/3Q2022. FnF met 25% of the Capital Buffer. Threshold for the resumption of the dividend payments (Table 8: Payout ratio. February 16, 2021 Capital Rule), that also marks the date when the JPS's fair value fetches its par value.

-4Q2022/(*)4Q2023. FnF met 25% of the Capital Buffer in the case that the JPS are redeemed by FnF.

(*) In this case, the reason why the FNMA holders might be hit with a small discount in the case of a Takings today by the UST at the BVPS.

Notice that the tweet has been updated to stress that there is no discount in the following resale of FNMA at PER 14 times, as it's contemplated an Accounting Standard change just after the Takings, for the amortization of the Deferred Income into earnings in one fell swoop.

This is harsh for the FNMA holders, but authorized in the famous fhfa-C's Incidental Power (best interests of FnF and FHFA). Otherwise the FNMA holders would vote against the redemption of the JPS now.

PER 14x NEEDS COMMON EQUITY 1ST

— Conservatives against Trump (@CarlosVignote) August 29, 2023

▪️1Q2021/4Q2021 FMCC/FNMA Adeq Capitalized(Total C.):no dilution in stock offerings.

▪️3Q2021/3Q2022:FnF met 25% C.Buffer(Tier1 C.). Div payment resumes→JPS=par value.

4Q2022/(*)4Q2023 upon JPS redemption.(*)Slight discount now on FNMA.#Fanniegate pic.twitter.com/SOOSjfNdRq

No where is written that SPS are non-repayable securities.

It must be expressly written in the certificate of designations. The same for the case of conversion to commons, specifying the conversion ratio, which doesn't exist either. The same occurs with the JPS.

The SPSPA only states that the dividend can't be used to repay the SPS, which is obvious. The thing is that no actual dividend existed. No dividend was ever disbursed, because it's forbidden when FnF are undercapitalized in the FHEFSSA Restriction on Capital Distributions. None dividend, zero, nada, nichts. Auchtung!

The SPS have a cumulative dividend, which means that at some point, it'll be suspended and it's accumulated.

Mandatory dividend doesn't exist in this world, which transforms a dividend into interest payments, as the Wall St law firm representing the FHFA has stated in court.

A dividend is a distribution of earnings to the Equity holders after calculating the Net Income with the income and expenses from operations (like interests). Therefore, a dividend appears on the tables Change in Equity or Net Worth Activity in their earnings reports, because earnings are otherwise retained on the Balance Sheets (A Retained Earnings account is Equity and Core Capital). This is why a dividend is considered a distribution of capital (FHEFSSA definition of capital distribution: any dividend). So, it couldn't have been possible paid, out a Retained Earnings account with deficit all along. So, two reasons why they weren't actual dividends.

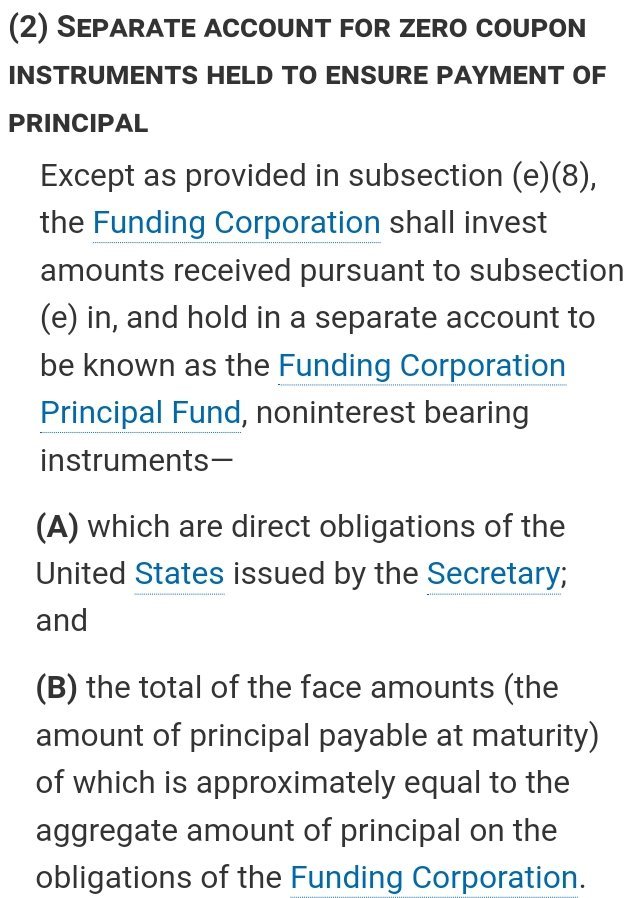

In fact, the reduction of the SPS is the only exception to this Restriction on Capital Distributions (image below)

Therefore, if the law states that no dividend was ever paid, the capital distributions to UST that have gone through, have been applied towards the reduction of the SPS, as per the exception in the law (Later on, for their Recapitalization in a separate account was added in the CFR 1237.12), under the guise of dividends. This way, the FHFA-UST's actions are legalized, avoiding do-overs.

The fact that the Incidental Power of the conservator allows it to "take any action authorized by this section, in the best interests of the FHFA", this plan of deception with a Separate Account is the first thing that anyone should have come up with, taking into account that we are dealing with the same officials that carried out a similar plan in the 1989 bailout of the FHLBanks by Congress, under a statutory section entitled "Separate Account", for the repayment of the principal of the obligation RefCORP with the taxpayer, with an allowance that was first applied for the payment of interests (there was also a UST backup worth $300 mll, to make sure that they pay the interests on this obligation. Section: "Treasury backup"). By they way, they could skip the allowance if they reported losses in a quarter. But with FnF, these officials were more interested in swelling the SPS and the capital distributions were the reason of the losses, draws from Treasury and more SPS increased for free, increasing the dividend amount the next quarters and an increased public outcry at the time (it occurred in 11 quarters in early conservatorship. Explained here) and, for instance, representative Hensarling calling the SPS "taxpayer's losses" as part of the plan to spook the retail investor as well. He was then hired by UBS.

Currently, the entire allowance disbursed by FnF is applied only for repayment of the obligations SPS (all the preferred stocks are obligations in respect to Capital Stock, that is, fixed-income securities), as the SPS pay dividends, not interests, and they are forbidden.

The same occurs with the current SPS increased for free. Another capital distribution restricted that reduces the core capital and thus, also barred in the FHFA-C's Rehab power like the dividends mentioned before. This is concealed with Financial Statement fraud in FnF (These gifted SPS are missing on the balance sheets in order to evade posting the corresponding offset with reduction of the Retained Earnings account). It's considered a joke "in the FHFA's best interests". In truth, the Common Equity is held in escrow (if there was no Financial Statement fraud) like with the dividends and, at some point, it'd be unwound.

Finally, actually, the SPS are redeemable securities. Because there are 2 UST backups of FnF in the Charter Act with the same name: "Authority of UST to purchase obligations", with the surprising addition by HERA of one that can fetch an infinite rate and in an infinite amount (Subsection (g))

As the UST backup since the Charter's inception is the one that prevails (Charter dynamics), we use the second UST backup to accomodate a resolution of Fanniegate that complies with the original.

The one inserted by HERA was used in the SPSPA for a Separate Account plan (10% and NWS dividends are, thus, legal, although later they weren't actual dividends but capital distributions) and it was also useful for the approval in the SPSPA of a $200B funding commitment that de facto updated the obsolet limit of $2.25B in the original bailout, established more than 50 years ago when Fannie Mae had only $15B in debt outstanding (an update that should have been done by Congress in the first place, instead of enacting HERA)

We also look at the original UST backup to learn that the SPS are redeemable securities, because this subsection (c) states that the UST is authorized to purchase any obligation of the subsection (b), and this subsection (b) specifies that they must be: redeemable obligations.

The Separate Account plan legalizes every action and upholds the original dynamics. For instance, the PROHIBITION of United States to make profits off the securities and assets of FnF, except the rate on redeemable obligations established in the subsection (c). The infinite rate inserted by HERA in the subsection (g), doesn't appear as exception to this prohibition for a reason: it was never meant to be the ultimate rate.

The plotters cling to HERA and the SPSPA to avoid these conundrums when you watch the legislation with all the amendments included, as seen today if you download the FHEFSSA and the Charter Act.

Heavy penalties for those peddling the Govt theft story in formal documents, including Howard who showed up in the SCOTUS as amicus curiae to repeat a dozen times that the SPS are non-repayable securities and now he sends this guy Kthomp19 to repeat the same lie. Kthomp19 also calls the existing shareholder "legacy commons". Another attorney with an evident lack of knowledge in finance that covers up the Restriction on Capital Distributions and its exception, Rehab power, etc.

Day 18. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/30/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

Not even $1 will come out of FnF, in what looks more like an attempt by the DOJ attorneys to compensate their colleagues attorneys for the plaintiffs, for their job of covering up the laws, Finance and even Securities Law violations during Conservatorship, and give back dividends to the non-cumulative dividend JPS.

The dividend was impeccably suspended according to the law, yet there is always someone complaining about the lack of dividends, a suspension that has more to do with the capital requirements, not just the Conservatorship itself, as these are 258% higher than 2008 in the case of the Risk-Based Capital requirement in Freddie Mac, for instance. Although both issues are intertwined, since the UST chose a 3-option plan as "recommendations on ending the Conservatorship", at the request of the Dodd-Frank law "no later than January 31, 2011", that has one thing in common: a Private Housing Finance System, with the option 3 expressly stating "stringent capital requirements". A Private System, end point of Conservatorship (no UST backup of FnF anymore, that is, the Charter is revoked), is why the FHFA adopted the Basel Framework for capital requirements, an international standard for the same risk exposure, so it's not "bank-like" if FnF have different risk exposure. In the one that isn't risk-based, it's below "bank-like", as the Leverage ratio is Tier 1 capital greater than 2.5% of Total Assets in FnF, and 4% for the U.S. banks and 3% in Basel.

An option 3: Govt catastrophic-loss reinsurance, that is achieved with the new product unveiled by Freddie Mac on June 2022: Resecuritizations, already priced at 9.375 bps. Though, it might be private reinsurance, and then, we'd be talking about the option 1 or 2.

So, no one can say they didn't see it coming once the Separate Account is unveiled: endpoint, rehab power through the incidental power (take any action...), etc.

A made-up hybrid financial instrument, non-cumulative dividend JPS, recorded in Core Capital for its loss-absorbing capacity in capital matters, like all other items inside Core Capital. For which they get a higher dividend rate than the interest rate on similar obligations by the same issuer.

The Fanniegate scandal can't come down to attorneys illiterates in financial matters, attempting to sort out its resolution tailoring a kind of wish list, even including a compensation to the government snitches working for the DOJ, using funds taken from the enterprises or the common stocks.

Navy commodore asks again why there is no judgment, when I've already explained it to him here a few days ago.

He is unaware that the Wall St law firm representing the FHFA, instead of the DOJ, requested a motion to defer the judgment and everything melted down, as the FHEFSSA's Restriction on Capital Distributions not only bars this payment of Securities Litigation claims as the FHFA likely pointed out in the oral motion, but also any dividend and today's SPS LP increased for free.

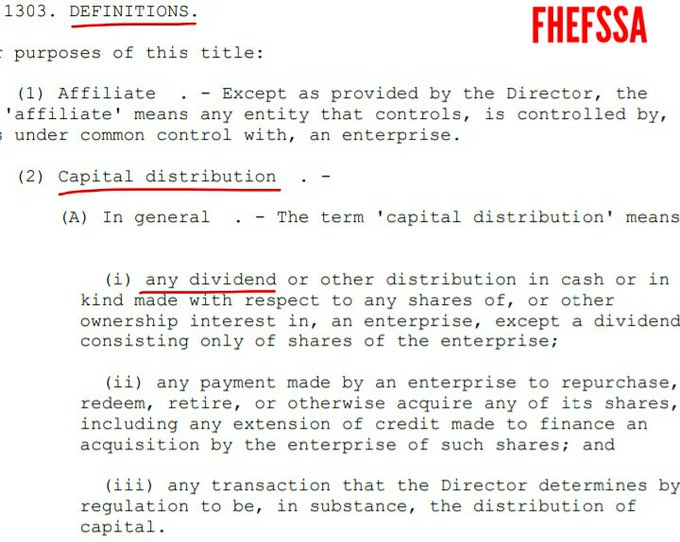

(See the definition of capital distributions CFR 1229.13 that added up this item Payment of Securities Litigation Judgments in #3, to the 12 U.S. Code § 4502 - Definitions (5) Capital distributions)

The reason why it was an oral motion: it's all about covering up this restriction, a Prompt Corrective Action, by both counterparties: DOJ/FHFA - The plaintiffs.

Obviously, the suspension of capital classifications didn't affect the Restriction on Capital Distributions, continuing with the last point laid out yesterday contending that it didn't affect the FHEFSSA section Capital Classifications, because this statutory provision was placed by HERA at the end of this FHEFSSA section, as shown below.

Neither they are "FHFA guidelines" nor it affected this section, yet we see how Howard, a member of Fairholme's legal team (in the comment posted by @stockanalyze that I was replying to), claims otherwise in what looks like a last-minute desperate attempt to avoid crippling penalties for having gone to the SCOTUS as amicus curiae to claim that the SPS are non-repayable securities, because his comment comes out after years spent simply covering up this basic Prompt Corrective Action (along with the rest of his gang: the DOJ and all other plaintiffs and the company peddling the government theft story). A Restriction on Capital Distributions that anyone with a minimum knowledge in Finance knows beforehand, so it doesn't need to be written in a law, and whose exception (reduce the SPS), that continued with the CFR 1237.12 exceptions that supplemented the prior exception (for recapitalization), are the grounds of the Separate Account plan, in the FHFA's best interests.

A $4.8 billion penalty on each counterparty (DOJ - government snitches) will do it.

Day 17. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/29/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

FHFA suspended the capital classifications during Conservatorship.

Related to the declaration of:

-Adequately Capitalized

-Undercapitalized

-Significantly Undercapitalized

-Critically Undercapitalized.

They aren't "regulatory guidelines" as the controversial Timothy Howard claims in your post. They are statutory capital classifications.

This is the FHFA's statement:

The objective of the FHFA was to avoid a declaration of Critically Undercapitalized with the 3Q2008 earnings reports through today, with an adjusted $401B capital shortfall over Minimum (Leverage) Capital requirement (FHFA keeps refusing to publish the Critical Capital level, estimated at $23B together in 2023)

On the other hand, it also avoids the conflict (and liabilities) of having had to declare FnF Adequately Capitalized with the 3Q2021 results, under the Separate Account plan according to the law. Which could make this statement from FHFA on day one of conservatorship, a telltale sign of the intention to carry out a Separate Acct plan with the necessary absence of the capital classifications, and with the bailout in 1989 of the FHLBanks in DeMarco's and Sandra Thompson's rear mirror. A bailout where the UST lost $30B in its investment in RefCORP bonds because these officials thought that, with the quarterly allowance, the FHLBanks only had to pay interests, not the principal of the obligation. A failed bailout that enriched Wall Street with numerous Public-Private partnerships.

The end of the paragraph, with "capital requirements aren't binding", has more to do with what has already been explained about "may" in the conservator's power and "best interests of FHFA" in its Incidental Power, that allows the FHFA to increase the risks in FnF or activities that increase the losses, like building the CSP, etc.

It doesn't affect its statutory mission of the rehabilitation of FnF through building capital (soundness) with "put FnF in a sound and solvent condition".

It didn't affect the publication of the statutory capital requirements in their earnings reports with the S.E.C. every quarter since day one through today. However, the Critical Capital level has been missing all along and also today in the ERCF tables, which is a felony. The Risk-Based Capital requirement formulaic was struck by HERA, so it couldn't have been published until the new Capital rule in February 16th, 2021, remember that it was withheld on purpose through regulation until January 1st, 2022, so that representative French Hill asked ST in July 2022 about the FHFA 2021 Report to Congress, with the new Capital Rule absent. The FHFA 2022 Report to Congress? This time, Rep. Hill and McHenry scheduled the hearing with ST's testimony two weeks before the scheduled release of the report.

It didn't affect the FHEFSSA section Capital Classifications, where it's explained the definitions of each capital classification, useful to learn that the Minimum (Leverage) Capital requirement is met with Core Capital, and the Risk-Based Capital is met with Total Capital, which slams nowadays the scammers that claim that it's met with their Net Worth that they call Capital Reserve (SPSPA's amendment by Calabria-Mnuchin, 12 days before Sec. Yellen was sworn in: "Capital Reserve End Date"), notwithstanding that the these definitions are seen on the ERCF tables nowadays.

Then, with the ERCF tables absent from the FHFA Report to Congress, they can throw numbers at the wall. For example, the exchange ST- representative Blaine: "$100B vs $300B", ignoring that $100B was their Net Worth, not the regulatory capital. And the $300B was the official capital needs or capital shortfall over the capital requirement at the time ($297B, the official number in their ERCF tables), not the capital requirement. Typical: create confusion. Is it HERA or the FHEFSSA?... On bitcoin. Is it a commodity or a security?

Also known as playing the fool.

HERA didn't replace the FHEFSSA. Guido is here to mislead the retail investor under the orders of his boss, the hedge fund manager Tim Pagliara.

For instance, he insists once again that FnF have to repurchase the Warrant, which was issued for free and it's deemed an illegal collateral according to the law.

2008 HERA amended the 1992 FHEFSSA and the Charter Act.

So, now you have to download the FHEFSSA, a law created just for the soundness of FnF, establishing Capital ratios for the first time, corrective actions, the definitions of financial concepts that the scammers hate (definition of capital distribution, ....), etc., and the Charter Act, to see the laws with the amendments already included.

It takes more time to write your lie in the form of question (typical confusion from the scammers: On bitcoin. Is it a commodity or a security?), than typing "2008 HERA" on a search engine, 15 years later, where you would see that HERA is all a mess, with "the FHEFSSA is amended by striking X for X"; "by inserting..."

As seen with the Restriction on Capital Distributions.

Day 16. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/28/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

*** THE DOJ HAS A PROBLEM OF ATTITUDE ***

It's time to take the ball away from the DOJ and its accomplices, the peddlers of the government theft story in formal documents (some social media influencers will be in trouble too)

I don't know what this DOJ attorney was thinking of, in the brief filed on Friday in response to the government snitch Bryndon Fisher.

Have a look:

.@TheJusticeDept's ATTITUDE

— Conservatives against Trump (@CarlosVignote) August 27, 2023

Emphasis on HERA instead of FHEFSSA/Charter Act.

"FnF lost the right to...

-exclude the Gov from their property":3 prerequisites on purchase of securities expired in 2009.

-complain about FHFA's interests":actions authorized by this section.#Fanniegate https://t.co/1oeK9pLOYn pic.twitter.com/qoNNuzyrZB

Robert and Bryndon Fisher are two Don Quijotes fighting windmills that they imagine to be "Nationalization".

Bryndon, page 2-3: "Although HERA conferred broad authority on FHFA as conservator to conduct the business of the Enterprises, including permitting FHFA to consider both the interests of the Enterprises and the interests of the public, that authority is necessarily limited by the Constitution."

Day 15. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/27/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

"Verdict certification" doesn't exist, navy commodore. A JPS holder.

You mean a judgment/court order issued by a judge, which was deferred due to the FHEFSSA's Restriction on Capital Distributions (Dividends, today's gifted SPS and the payment of Securities Litigation claims in the Lamberth's court)

A verdict is a simple statement by 8 ordinary citizens, that doesn't take effect until the judgment.

With "certification" you want to transmit the idea that the judge will simply sign off on whatever the jury came up with in the verdict, when the odds are that the judge will issue a "judgement notwithstanding the verdict" (JNOV), that is, entering a judgment in favor of the losing party, arguing that the jury incorrectly applied the law in reaching its verdict. It's well known that the jury asked for the HERA text, when the laws pertaining to FnF are the FHEFSSA and the Charter Act, as amended by HERA.

You are here just to promote the court news, thinking that, this way, the plaintiffs have the upper hand in the resolution of Fanniegate.

What the market is actually expecting is the announcement of the Separate Account plan according to the law, plus a heavy penalty on the plotters, both the DOJ and the peddlers of the govt theft story in formal documents (plaintiffs, amicus curiae, law firms, the Moelis Gang, etc)

Verdict Certification plus Award of additional Interest due anytime ....

volume is completely ridiculous with recent COURT event ...

until it happens ... GSEs only move on NEWS

Clarification: 0.5% was the spread over Treasuries (Remember that for the FHLBs, it was 0.299% in 1989 -GAO report-) to calculate the ultimate dividend rate on SPS, once the Separate Account plan comes to an end with the "Rehabilitation of FnF" (prerequisite from Justice Alito and judge Willett, known as "The synchronized"). This spread is the UST's Net Interest Yield that takes into consideration its cost of funding. The Net Interest Income earned by UST in the cheap bailout of FnF and in exchange for their risky Public Mission.

The amount that is netted out with the interests that UST owes to FnF on the $152.3B due, is the whole cumulative dividend assessed at a weighted-average 1.8% dividend rate on the UST's quarterly investments in SPS, "taking into consideration the Treasury yields at the time" (which means that it's applied a spread over Treasuries, as per the Charter Act dynamics) and partial repayments (as per the exception to the FHEFSSA's Restriction on Capital Distributions), until the SPS were fully repaid, estimated in late 2013 and late 2014, in FMCC and FNMA, respectively.

Until the Charter Act is revoked, it's legally binding in its entirety, not just the amendments inserted by HERA. The same occurs with the FHEFSSA.

FnF are not ordinary businesses.

The conservator's Incidental Power "take any action authorized by this section", wraps it all up.

The infinite rate on SPS inserted by HERA in the Charter Act, the grounds for the SPSPA, wasn't included as exception into this other provision entitled "Fee Limitation of United States". Pelosi/Calabria's HERA didn't dare to amend it with "PROHIBITION, except an infinite rate". Huh? A telltale sign that the infinite rate inserted by HERA was meant for a Separate Account plan (with the 1989 FHLBs' bailout by Congress entitled: "Separate Account for the repayment of the RefCORP obligation with the taxpayers", in the rear mirror) and was never meant to be the ultimate rate. They thought they can get away with it with judicial maneuvers.

Day 14. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/26/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

$4.8B, a compensation for real in damages for real.

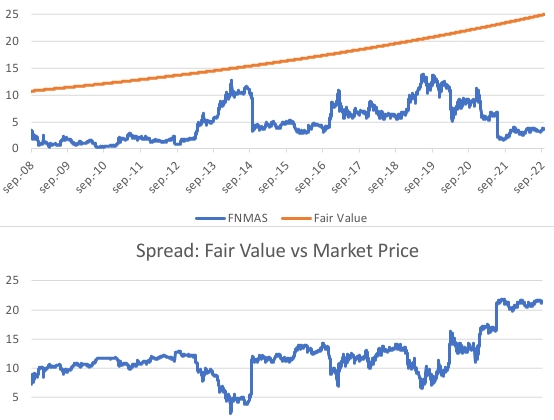

Damage: the Separate Account plan prevented the stocks from trading at their fair value all along. Therefore, the damage is the spread Fair Value vs Market Price. It's been calculated an average spread for the 15 years of deception, using FNMAS (a $25 par value JPS), the most liquid series among all the series of Preferred Stocks issued by FnF. Actual number $12 through September 2022, when it's estimated that the fair value would have fetched the par value with the resumption of the dividend payments. As of today, the average is estimated at $12.5, half its par value.

This is a real damage provoked by both counterparties in the Fanniegate scandal: the DOJ and the peddlers of the government theft story ("We've been robbed!") in formal documents: books, articles, court briefs, financial analyses, letters, etc (the plaintiffs, Howard, Ackman, Bradford, law firms, Moelis and the sponsors of its infamous plan, etc). Which will suffer the same penalty, by the way ($4.8B)

Now, the real compensation. Because the economic harm of loss, on both Cs and Ps, is fully redressed unveiling the Separate Account plan, I'm talking about Punitive damages (deterrence). It's estimated that the Treasury earned a 0.5% rate (Net Interest Yield) in the bailout of FnF under the Charter Act ("take into consideration the Treasury yields as of the end of the preceding month to the purchase"), netted out with the interests owed to FnF on the $152B due. Now, I'll be a loss for its misbehavior.

The amount of interests on $12.5 during 15 years using a 0.5% compound interest rate, sum $0.97 today.

For a $50 JPS, it's $1.94.

The Cs' fair value is subject to more variables than a JPS (straight forward: a 6% annual discount rate to par value). Then, the Cs match a $50 JPS in damages.

This amount represents a 0.254% annual rate if the calculations are made with the par value. Which is how we can now assess whether this amount requested is high or low. A 0.25% rate on a JPS is extremely low, but assessed with thoughtful criteria.

Breakdown of the $4.8 billion worth of compensation (estimation):

Fannie Mae

Ps: $752mll

Cs: $2.2B

Freddie Mac

Ps: $533mll

Cs: $1.3B

On the other hand, the plaintiffs with a fiction claim (breach of implied contract) attempt to make up for the lawful suspension of their non-cumulative dividend on JPS, stipulated in their contract with FnF, calculating a false damage with the one-day stock price reaction to the third amendment and that the Equity holders love it, as the fastest speed for the Separate Account plan that reduced the SPS and recapitalized FnF under the guise of restricted dividend payments and even without available funds for its distribution (accumulated deficit Retained Earnings accounts)

The fact that the "doctor" that calculated the interests used a simple interest rate (Left. Table circulating on the internet), when in the financial world, it's always a compound rate, denotes that these expert witnesses are brought for their confict of interests, like the medical doctor Mason in question, who worked for a consulting firm with links to China. Source.

On the right, it was submitted yesterday both simple and compound interest rate, after the attorney representing the Hedge Funds, Hamish Hume, saw that I was using a compound rate.

A law and regulation are distinct. CFR1237.12/CFR1237.13.

Another rabbit pulled out of the plotters' hat: Saying "law" when talking about two pieces of regulation enacted with the July 20th, 2011 Final Rule "for the transparency of the conservatorship". An excuse to sneak the CFR 1237.12 that surprisingly added up another exception to the FHEFSSA's Restriction on Capital Distributions (as amended by HERA) when FnF are undercapitalized, that has the same effect as the restriction itself: the Recapitalization of FnF. It enabled this Recap through a capital distribution, which means that the capital exits the Balance Sheet, but necessarily has to be held in a separate account "to meet the Minimum and Risk-Based Capital levels". It was necessary for the case when the SPS were fully reduced under the guise of dividend payments (estimated in late 2013 in Freddie Mac, as seen in my signature image. End of 2014 in Fannie Mae), so that FHFA and UST can continue to distribute capital that otherwise would be forbidden. That is, a Separate Account plan authorized in the FHFA-C's Incidental Power: "Take any action authorized by this section", with a Rehab power of "restoring FnF to a sound and solvent condition", so forget that FHFA-UST can steal the profits (core capital) from FnF in the public interest, because it'd break this power, which is the prerequisite of "Rehabilitation of FnF" laid out by Justice Alito, synchronized with Judge Willett in the prior enbanc hearing in Collins (5th Circuit), who stated that "authorized by this section" means "any action within the enumerated powers". That is, its Rehab power.

Both the word "may" in the Power and "best interest of FHFA" in the Incidental Power, is related to other activities different from stealing the capital once it's built. For intance: building the CSP, UMBS, or even activities that increase the risk, etc. Today, FnF are not rehabilited but in the worst financial condition possible. Explained here.

A company restricts dividends because Retained Earnings is Core Capital, as a dividend is a distribution of earnings.

HERA states:

This statutory restriction -IN GENERAL- complies with the FHFA-C's Rehab power (statutory mission): put FnF in a sound and solvent condition, both soundness (Recap) and solvency (reduce the obligations SPS)

Just so that you know, a law can't be overriden using regulation. This is why I've written Recap in all the 4 exceptions, including "in the public interest" as pointed out before.

As stated in the same regulation:

(c) This section is intended to supplement and shall not replace or affect any other restriction on capital distributions imposed by statute or regulation.

except to the extent the Director determines is in the interest of the conservatorship.

Day 13. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/25/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

5th Circuit, Collins case and Fairholme's atty, again?

More court news until the attorney for Berkowitz, the omnipresent (Robinson, Fairholme, Bhatti, Rop, Collins) almighty David Thompson, achieves "the government has to come to me" at a negotiation table, he pointed out in a Conference Call hosted by Pagliara. The endgame of the abuse of court process and coverup of the laws in the Fanniegate conspiracy by the hedge funds.

A 3 judge panel in the 5th Circuit will learn about this case again, when judge Willett (prior enbanc hearing. 5th Circuit) and Justice Alito, seem sycronized when the former explained what "authorized by this section" was about (any action within the enumerated powers) in the FHFA-C's Incidental Power, and the latter highlighted the prerequisite of the rehabilitation of FnF, which is the FHFA-C's Power in question: put FnF in a sound and solvent condition.

It's called FHFA-C's Rehab power for a reason.

An explanation about what judge Willet and Justice Alito actually said, was posted yesterday.

When the Fanniegate scandal seemed resolved, with the evidence of a Separate Account plan by rogue officials, now, the Collins case returns to the 5th Circuit Court of Appeals seeking damages for the unconstitutionality of the FHFA director. The "for cause" removal restriction is constitutional to begin with, as explained by the law professor Nielson, who represented the FHFA when he was appointed by the Supreme Court, arguing that the Charter Act and the FHEFSSA, make the FHFA director have LIMITED POWERS, thus, it doesn't break the Separation of Powers doctrine. A Charter Act concealed by the parties all along.

The dramatic part in this case is that the Fairholme's attorney seeks damages based on a Financial Statement fraud in FnF (the SPS increased for free since December 2017 are missing on the Balance Sheets, to evade posting the offset with reduction of Retained Earnings -Core Capital- that would slam their slogan of "FnF continue to build capital"), orquestrated by FHFA's Sandra Thompson, who arrived to the FHFA in March 2013 as Deputy Director in charge of Capital policy ($402 billion capital shortfall over Leverage Capital requirement as of end of June, 2023) and behind the "blame DeMarco" rhetoric spread by her Hedge Funds guard.

The attorney uses this Financial Statement fraud to claim that the "unconstitutional" removal restriction prevented that the current scenario where the UST gets rich with the gifted SPS every quarter and, at the same time, FnF are recapitalized, from happening sooner, as Mel Watt would have been fired before.

That wonderland scenario is just a bunch of lies, based on the Financial Statement fraud in FnF. The adjusted Core Capital remains stuck at $-194 billion every quarter due to the offset mentioned with the gifted SPS, once they are posted on the Balance Sheets.

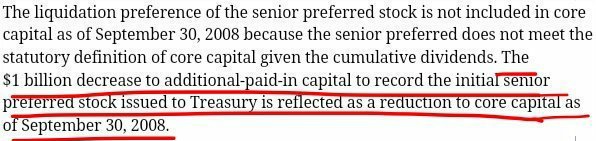

The same offset with reduction of Core Capital was seen with the initial $1 billion worth of SPS issued for free on day one of Conservatorship, debited from the Additional Paid-In Capital account (Common Equity too), now exhausted.

Can you imagine that this same attorney, at the same time he is concealing this Financial Statement fraud seeking damages in Collins, later is trying to settle this fraud directly with FnF confidentially, knowing that Fairholme and FnF are parties in the Lamberth's court, and awaiting the release from Conservatorship, when the management recovers its powers for this settlement?

Without powers (transferred to the conservator), FnF can't be parties in any legal proceedings. A telltale sign that the FnF management and the FHFA are eager to settle their fraud confidentially.

SPS and SPS LP, the same/// HERA? It's FHEFSSA.

2 topics:

- It's not the first time that someone tries to make a distinction between SPS and SPS LP, in order to justify that there is $111 billion SPS LP that is missing on the balance sheets (Financial Statement fraud)

Like LuLeVan yesterday:

The only "separate account" is the Liquidation Preference because it is not included in the balance sheets, which show only the SPS.

Day 12. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/24/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

Navy commodore unaware that the sham trial was uncovered.

It's been explained the reason why the Wall Street law firm representing the FHFA requested to judge Lamberth the deferral of the judgment: the payment of securities litigation claims is prohibited in the FHEFSSA's Restriction on Capital Distributions when FnF are undercapitalized.

So, the FHFA tries to avoid the announcement that the payment will be withheld. People would begin asking questions as to why, etc

This is why it was requested through an oral motion: to continue to keep this statutory provision from the public, as among the capital distributions restricted, are also any dividend and today's SPS LP increased for free every quarter.

A coverup of the law by all other plaintiffs and the company, in collusion with the government to share the booty, peddling the Government theft story

The grounds of the Separate Account plan with the exceptions to this restriction, laid out in the same provision.

Why don't you mention this oral motion of deferral?

This response is rather addressed to the attorney that sends you emails, and you later repost here, passing them off as your own comments.

The Separate Account plan for the repayment of the principal of the obligation with the taxpayer, was a statutory provision in the 1989 FHLBanks' bailout scheme by the Congress.

You'd better don't laugh at it. $BOOM

If you write what the SCOTUS said, make sure to post a quote with what it really said and not

what SCOTUS "actually said"

It may aim to rehabilitate FnF in a way that, while not in the best interests of FnF, is beneficial to the FHFA and, by extension, the public it serves.

Day 11. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/23/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

BOOM. Our negotiator renews the call for amortization into earnings of the $67.8 billion worth of Deferred Income (upfront g-fees already collected) in one fell swoop, currently recorded as Debt. So, useless for the Net Worth (stock valuation) and to meet the capital requirements.

It doesn't affect the resolution of the Separate Account plan according to the law:

-$152.3B cash refund from UST-FHFA.

-$228B posting as Retained Earnings account.

FnF would resume the dividend payments and it's when the JPSs' fair value would fetch their par value.

It benefits the UST in the case of a Takings of our stocks at the BVPS and resale to other players, as it'd get the Deferred Income, net, as a windfall, through a higher resale price. Plus, the corresponding extra tax income that year.

FnF have accumulated so much capital, 15 years into conservatorship, that, in the case of Freddie Mac, it could redeem the JPS in full, still be Adequately Capitalized and even meet 25% of the Prescribed Capital Buffer. But this isn't the case for Fannie Mae. It turns out that the Buffers are met with Tier 1 capital, which is $12B less than the available Core Capital, and thus, the redemption of its JPS would leave it $1B short of the Leverage Capital requirement. This is the moment when the amortization of the Deferred Income into earnings would come to the rescue.

Although the JPS would trade at their par value as pointed out before, with a restated dividend rate, there is a possibility that they could trade below it, just due to the effect of the stock overhang (too many people willing to realize profits). Also, investing jointly with hedge funds isn't the best investment decision: there is risk of stock price manipulation with these illiquid stocks with the excuse of the stock overhang and whatever the gang comes up with again.

Besides, the redemption of the JPS boosts the common stock valuation (adjusted EPS) and thus, the sale price if in the first point I've mentioned that a Takings today would end up in the resale of FnF to bigger players. Another benefit for the UST if that's the case. Otherwise, the existing shareholder captures this benefit.

In the thread cited, is included the prices under this scenario of redemption of JPS, with the adjusted EPS and Privatized Housing Finance System scenario.

The problem with the accounting of the Deferred Income, is that FHFA is mixing up the revenue earned with the concept that FASB (accounting standards council) calls "performing obligations", defined as a promise of future delivery of the product or service.

FHFA might think that "performing" is like FnF that may or may not pay the claim depending on how the loan performs. Also, it's mixed up with the prior Guaranty Income/Obligation accounting, also income that was recorded as debt, but it stopped upon the consolidation on the Balance Sheets of the MBS Trusts in early conservatorship. And I'm wondering whether this consolidation was meant to set aside the "guaranty obligation" accounting, how is it possible to end up with the same accounting standard, now renamed "Deferred Income".

Or, simply, the FHFA has used its Incidental Power as conservator to deprive the Equity holders of the benefits of this upfront g-fee recorded in their Net Worth, by opting out of adopting the new Revenue standard as of 2017, which can't be authorized as it's been done with the Separate Account plan and blessed by the Supreme Court, when Justice Alito read the Incidental Power as the rehabilitation of FnF, the Marxist way (beneficial to the Agency and the public: the extortion of their resources with loan sales when the PMI claim is pardoned, REO inventory sold to neighborhood associations, etc.)

The service that FnF provide (guaranty service) is delivered and the MBS holder benefits from it, on day one. This is why it's Revenue earned and the accounting standard the FHFA is applying, must be changed for this 2014 new Revenue Recognition standard, that came into effect in December 2017.

This violation of its Incidental Power secures the compensation for damages requested for the Equity holders to the DOJ ($4.8 B) that also settles the 8 securities law violations during conservatorship, and it matches the one demanded to the plotters peddling the Government theft story.

FHFA CAN'T USE ITS INC POWER TO OPT OUT OF ADOPTION OF 2014🆕REVENUE RECOGNITION STANDARD

— Conservatives against Trump (@CarlosVignote) August 22, 2023

ASC 606, effective in Dec 2017.

Benefit of 💯% Guaranty service (control) transferred to the MBS holder on day one.

❎Deferred Income

☑️Revenue earned.#Fanniegate@TheJusticeDept @FAFNorwalk https://t.co/ZVhG4nFzUZ pic.twitter.com/t32mSXmS0t

Fairholme's Bryndon Fisher and Howard keep on covering up the law and basic concepts in Finance, like the fact that a dividend is a distribution of earnings and impossible to pay out if there is a negative balance (deficit) in the Retained Earnings accounts (a change in Equity: a dividend ends up being de facto debited from RE)

This is why any dividend is a capital distribution. Restricted in the FHEFSSA's Restriction on Capital Distributions, as amended by HERA Subtitle C - PROMPT CORRECTIVE ACTION.

Today's SPS LP increased for free every quarter and the payments of Securities Litigation claims (added to the definition of capital distributions in (3) CFR1229.13, are capital distributions too.

Then, RESTRICTED. PROHIBITED. BARRED. ACHTUNG!

Because the payments to UST existed, we can't say that they were actual dividends, as they are prohibited while undercapitalized by law.

Instead of bringing them to Justice accused of violating the law, there is another statutory provision that authorizes the conservator to lie and carry out a different plan behind the scenes: The conservator's Incidental Power: "Take any action authorized by this section,...."

Whatever it wants if the endpoint is the rehabilitation of FnF. Taking in account that it may take actions that reduce the profitability in the best interests of FHFA ("May" also in the FHFA-C's Power), but it's not an authorization to be excused from complying with its Power, neither with "may" nor with the "best interests", that is, once the capital is built, it's kept by FnF (or this Common Equity is held in escrow and lie about it if you wish. Just so that you know, at some point in time, it will be returned to their Balance Sheets, for the normal functioning of a corporation). It's called Retained Earnings (Core Capital) for a reason.

Then, you can't claim that there is a non-repayment provision of the SPS, because that's related to the dividend to UST, and no actual dividend existed but capital distributions under the guise of dividends.

Actually, the law authorizes the capital distributions for the repayment of the SPS (An exception to this restriction)

The problem with the "and" in the exception "(A) and (B)" was recently solved by simply acknowledging that the intention of the legislator was to raise fresh cash in the same amount as the redemption of the SPS and he didn't know that by building Common Equity (Comprehensive Income + OCI), there is also cash accounted for, due to the double-entry accounting. This is how the SPS were reduced with cash, at the same time the Common Equity increased and as seen in my signature image below.

In 2011, the FHFA added up another exception: a capital distribution (deplete capital) for .... wait for it... for their recapitalization (build capital: "Meet the Risk-Based capital and Minimum Capital requirements") in the CFR 1237.12 (Separate Account wording right there)

Above all, it would comply with the conservator's Rehab power: "Put (restore) FnF in a sound (build capital) and solvent (reduce the obligations SPS. Debentures) condition". Another statutory provision covered up by the plaintiffs and Co.

Hence, no one can say that nowadays FnF have been rehabilitated, with:

- $-216 billion Retained Earnings accounts. The only account that absorbs future losses.

- $304 billion SPS outstanding that will have to be paid back.

- $-194 billion Core Capital.

- $402 billion capital shortfall over Minimum Leverage Capital requirement.

You can't claim that the SPS are converted to Commons and that's it. Problem solved. Primarily, the Net Worth is only $111 billion and the rest of SPS are wiped out. Secondly, you must acknowledge that the FHFA-C has failed in its Rehab power, which would put into question the entire conservatorship. The "for cause" removal restriction of the director that was constitutional, is activated and the Fanniegate trials would kick off. Unless, it's announced the Separate Account plan: the Common Equity is held in escrow. The FHFA has lied to us all along.

Then, the dividend rate on SPS was authorized in a provision inserted by HERA in the Charter Act, with the same name as another one just above it in the Charter, with a rate that "takes into consideration the Treasury yields as of the end of the month preceding the purchase", also known as cheap UST backup of FnF, in exchange for their Public Mission.

This is why the plotters repeat "HERA, HERA, HERA". (Even the alleged jury asked for the HERA text). So, you don't see the Charter Act in its entirety with the original cheap UST backup of FnF.

So, quit repeating like mad that there is a 10% contractual rate. FnF aren't governed by contracts between Federal Agencies to begin with. It must uphold the laws in force. Again, the Incidental Power allows the conservator to mess around with the dividend rates, and eventually, its Rehab power and the special borrowing right from UST must be respected.

Finally, the Fee Limitation of the United States clause, tells us the Charter dynamics (the spirit of the Charter): the UST can't make profits off the securities and assets of FnF, other than the a low rate on redeemable obligations, in exchange for their Public Mission (section Purposes). Although it's been broken with the TCCA fees, HERA's 4.2 bps to UST/HUD and, likely, the CRT expenses (prohibited in the Credit Enhancement clause too) that might be being syphoned off to UST.

Numerous attorneys and social media influencers, funded by the hedge funds, play the fool over and over again. The thing is that the coverup of a material fact is a crime of Making False Statements, stock price manipulation and, in court, abuse of court process.

Day 10. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/22/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.

FHFA is well aware of the existence of a Prompt Corrective Action upon undercapitalization of the enterprises, but it refuses to acknowledge it publicly.

In this screenshot taken from the latest Final Rule that amended the ERCF, published in the Federal Register, the FHFA responds to the comments submitted by stakeholders and other people interested in the subject.

It explains what the capital buffers are for: a cushion of capital to prevent falling into undercapitalization territory, when a prompt corrective action kicks off.

But we see again how the FHFA is reluctant to mention which prompt corrective action it's talking about, because it's the Restriction on Captial Distributions (HERA subtitle C - Prompt Corrective Action) covered up by the Government and by those peddling the Government theft story, aiming to arrange a different outcome using the companies as a bargaining tool.

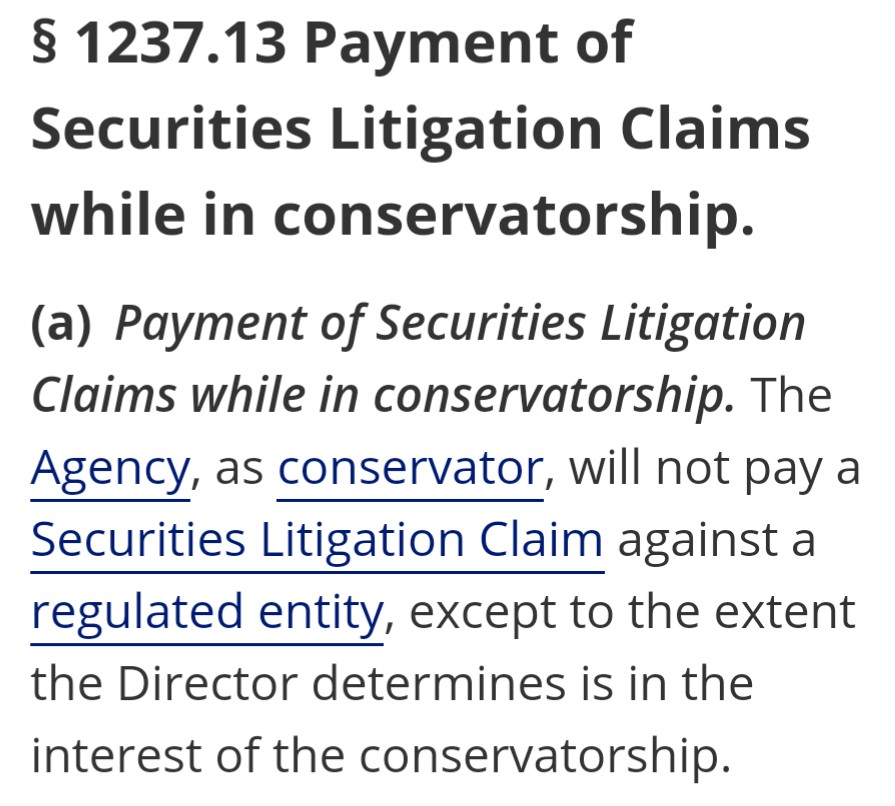

We saw it also in the July 20, 2011 Final Rule "for the transparency of the conservatorship", where in the CFR 1237.13, the FHFA stated that the payment of securities litigation judgments are barred in conservatorship, without outlining the true reasoning behind, which is no other than the FHEFSSA's Restriction on Capital Distributions.

The true reasoning was outlined in the preface of this rule:

This is the reason why the Wall Street law firm representing the FHFA, requested to judge Lamberth in an oral motion, to defer the judgment in the recent trial, because it would have to announce that this payment is prohibited with the restriction in the law mentioned.

So, the conservatorship is all about the coverup of this statutory provision, among others like the cheap UST backup of FnF, Fee Limitation of U.S. and the FHFA-C's Rehab power (Recap), by the FHFA/DOJ and their counterparty, the plotters peddling the Govt theft story.

15 years and counting.

It turns out that the coverup of a material fact is a crime of Making False Statements, for which we request a compensation for Punitive Damages worth $4.8 billion each.

Day 9. Corrupt plaintiffs' plea deal negotiations resumed and continued to 8/21/2023 at 10 A.M. in the S.E.C. headquarters in DC, accused of stock price manipulation and the crime of Making False Statements for the coverup of many statutory provisions and financial concepts, in a conspiracy of attempt to rip off the shareholders.

The plaintiffs and all others peddling the Government theft story in formal documents (books, articles, etc), are expected to plead GUILTY.