News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Bradford is a hippie that always diverts the attention from technical concepts because all he knows is to swap his stock for a different stock, like kids trading with baseball cards.

1st. FnF are in the business of making investments. So, the debate about MBS purchases is about the very existence of the Charter or try something else, because the latter was the objective during conservatorship since day one: to eliminate their advantages, enumerated here, and one of them was the usage of their low cost funding to boost profits in their investments held in the Retained Portfolio (on-balance sheet), as opposed to their mortgages bundled into MBSs and sold to investors, held in MBS trusts (off-balance sheet obligations). Their assets are split into Mortgage-related Investments portfolio (MBSs, mortgages) and Other Investments portfolio (Treasuries, cash,...)

So, the debate isn't about their current capital. You snuck Critically Undercapitalized to conceal the Separate Account plan, where FnF have excess of capital to redeem their JPSs.

Please explain to me how two critically undercapitalized (CET1) firms in conservatorship could even dream of making "investments"?

Sandra Thompson's charitable distributions from scarce corporate capital, which are actually a government function,

1st. The 60-day deadline expired on Friday October 13th.

If what you promoted here is true, judge Lamberth had 60 days to finalize the judgment.

I don't see any entry in the court docket.

An illegal Class Action and epitome of corruption, the DOJ rather let the case be trumped by the actual resolution of Fanniegate, than a judgment that could even end up in lawsuits against the DC court and the judge.

2nd. Another comment where you just copy-paste what an attorney in this conspiracy sends you by email.

There is no way that you could possible say this:

biased & mistrial eligible comments

You don't understand what affects Equity and what doesn't.

After my explanation of capital distribution, you reply insisting on your mistake, ignoring the difference between an investment for their Investment Portfolios and when they purchase their Equity stocks, a capital distribution.

I propose to double the penalties to those playing the fool in the Fanniegate scandal.

Glen Bradford is living the American dream: to work for a hedge fund manager in one of their scams to rip off investors.

Just like his buddy Navy Hedge Fund. The good cop - bad cop combo.

Yes. I wrote JPS instead of JPM twice.

No big deal!

Bradford, you write the typical reply from a financial illiterate attempting to discredit the author of a financial analysis.

Our negotiator hints that a new wave of economic expansion is possible, by simply eliminating the Capital Buffers all across the board.

What is a simple concept of "buffer" above the capital requirement, is now considered an increased capital requirement and an excuse to more than double or even triple it with the surcharge in the case of Global Systemically Important Banks (GSIB)

For instance, this is why JPS posted a CET1 of 14.3% when the capital requirement is just CET1 = 4.5% of RWA. This is because with the capital buffers, the total is 12% (estimated to be increased to 15% with the proposed capital standards now in place)

What it looks like is that JPM leads the future amendments to the capital requirements because Jamie Dimon doesn't want risk exposure, that is, invest in America, and not the other way around.

For instance, JPM posts $1.4T in cash and marketable securities, but the excess of High Quality Liquid Assets (HQLA) over the Liquidity needs that I guess refers to a 1-year period (Liquidity Coverage Ratio = 112%), is just $252B.

First, JPS should reinvest the $252B excess right away in assets with more risk exposure.

Second, figure out how to reduce the 1-year liquidity needs to increase this pot (For instance, offering 2-year or 5-year deposits, or issuing bonds beyond 1-year maturity)

So, more than $1T could be freed up to invest in assets with more risk, rather than currently invested in Treasuries, MBS or the fraudulent scheme of the Federal Reserve that grants the banks a 5.4% rate in reverse repo operations and also on Reserve Balances (IORB rate), when the latter has always been 0% for legal reserves.

First and foremost, the banks must comply with GAAP, because the Fed is to blame of the current accounting fraud with the investments in debt securities held in HTM Portfolios, instead of being recorded at fair value, either as Trading securities or AFS securities.

Along with the CECL accounting standard, all the expected losses would have been accounted for on a determined date.

Also, it's been proposed a change in the risk-weight of mortgages, because currently there is a flat 50% weight, instead of being related to the current LTV like FnF.

Then is when we start a debate about capital ratios to absorb unexpected losses.

With the Capital Buffers so high, it seems that you are protecting the actual capital from ever bearing losses, which is the reason why it exists to begin with, as any item is recorded as capital due to its loss-absorbing capacity. It's not a picture hung on the wall. And I'm referring mainly to the high yield Preferred Stocks, recorded as AT1 capital for a reason, they absorb losses with the dividend suspended upon undercapitalization. It can't be a security for the extortion of resources with a higher yield than similar obligations forever, for the enrichment of the institutional investors that usually buy these things. Because, another conundrum is why these JPSs are never redeemed at some point and substituted for Retained Earnings.

This way, the regulators focus on their job of overseeing Liquidity and Capital Levels, and to impose Prompt Corrective Actions upon:

-Undercapitalized: dividend suspended

-Significantly Undercapitalized: Capital Restoration Plan

-Critically Undercapitalized: Conservatorship for the financial rehabilitation and the management is ousted.

A prohibition to consider a Deferred Tax Asset valuation allowance is a must, the excuse used by Goldman Sachs' H.Paulson and the FHFA to reduce the capital in FnF big time in 2008 to increase the draws from Treasury. So much for rehabilitation.

A Capital Buffer would be useful to create a rule for the Payout Ratio and limit the amount of Net Income distributed to the Equity holders as dividend. For instance: a Capital Buffer equal to 100% of the capital requirement. Then, it's split in tranches for different payout ratios, like FnF today in their Table 8.

So, each financial institution will have the capital buffer it wants, based on the management's assessments about the future, not by low profile officials more interested in manufactured crisis to feed their cronies lying in wait or in making the banks buy Treasuries, so more Municipal jobs are created (first responders, etc.) A Soviet regime instead of a productive economy led by the private sector.

FRAUD W/ THE CAPITAL BUFFER

— Conservatives against Trump (@CarlosVignote) October 14, 2023

It isn't capital requirement as stated by regulators(FHFA IG)and banks:$JPM

CET1=4.5% RWA,called Regulatory Min instead of Max legal. It posts 14.3%🆚12% w/ Buffer.

Buffer useful for:

-7%? Start to increase risk exposure.14.3%? Moron

-For Payout ratio https://t.co/RaJ1e4awrJ pic.twitter.com/Ckf18pO9Da

No, Bradford. MBS purchases isn't a capital distribution, but investment.

What is restricted is capital distributions because it's when the capital affects Equity and it isn't regular expenses/investments result of operations.

Capital distributions:

1- Dividends and today's gifted SPS.

2- Stock buybacks

3- Payment of Securities Litigation judgments.

The grounds of the Separate Account plan, as #1 distributions have gone through and we applied them towards the exceptions in the law and CFR 1237.12 to legalize it (to reduce the SPS and recapitalization outside their balance sheets. The gifted SPS are simply a joke thanks to the FHFA-C's Incidental Power. All of them translate into Common Equity held in escrow). Besides, no dividend was available for distribution, out of an Accumulated Deficit Retained Earnings account. A dividend is a distribution of Earnings, whereas interest payments are expenses. Capital distribution vs No capital distribution.

It was extensively explained in this comment.

The phony MBA guy, Bradford, doesn't know basic financial concepts, even if those are written in the laws and regulations.

You are here to deceive and mess everything up. Playing the fool won't reduce your share of the $4.8 billion penalty required to the plotters (law firms, your boss Ackman, Pagliara, Howard, Moelis, etc)

There is a fine line between playing the fool and crazy talk, because the previous day you claimed that SPS and LP are two different securities, and also that the gifted SPS are in a separate account, when their absence is simply Financial Statement fraud.

Playing the fool is when you claim to don't understand something and crazy talk is when you just post gibberish.

how can FnF (while still in c'ship) spend capital on MBS repurchases when capital is so scarce that Lamberth can't even pay the plaintiffs in the jury trial?

It's $612 million for the plaintiffs versus tens of billions in MBS buybacks.

No. There isn't Retained Earnings if they are wiped out when, at the same time, the SPS LP is increased for free in the same amount, because it carries an offset (reduction of Retained Earnings) currently concealed with Financial Statement fraud (these gifted SPS are absent from the balance sheet)

"there is ONLY retained earnings" as I've said

— yes — they continue to retain earnings.

The Charter of FnF isn't about reducing the spread Treasuries-MBS yields in the secondary mortgage market.

This spread has widened reflecting the government bond spree in the Treasury Department, raiding the world savings for itself, so other asset classes have to offer higher yields to attract investors. It also affects the amount of lending by the banks, because the banks absorb the new issuances and have less money to lend, leading to a spike in rates.

It's an efficient financial market and it's stable.

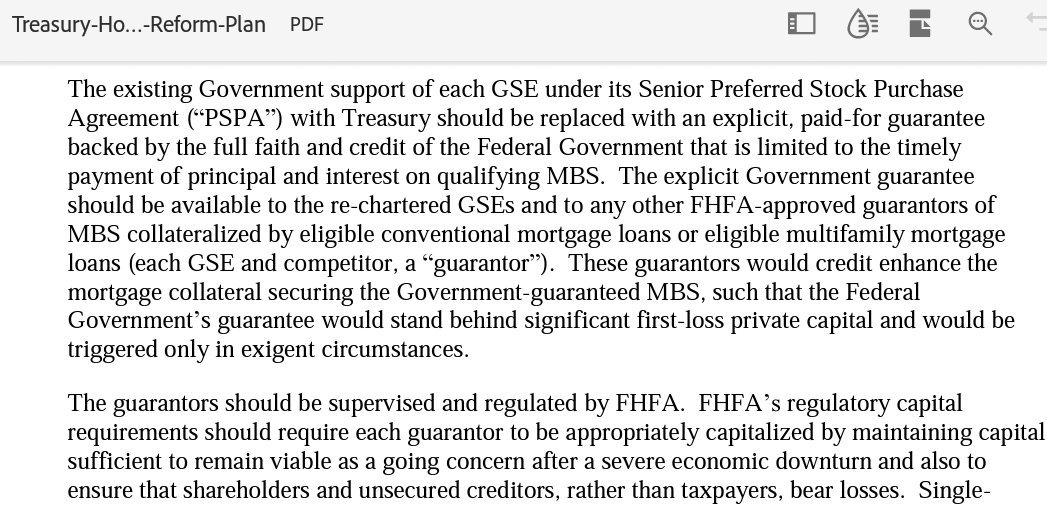

Once FnF are on the finish line 15 years later, the investors now want to keep the Charters, unaware that the Conservatorship endpoint options were related to a Privatized Housing Finance System (2011 UST-HUD Housing Finance System revamp)

The goal during conservatorship, thus, has been to remove all the advantages enjoyed by FnF and their shareholders:

-Wind-down their Investment Portfolios: FnF were accused of using their low cost funding advantages to build an investment portfolio and boost their profits. The SPSPA established a reduction of their Investment Portfolios (Retained Portfolios) first 10% per year, then it was increased to 15% per year in 2012, until they reached $250 billion maximum. This cap was decreased to $225 billion on December 31, 2022. This letter proposes to balloon their Investment Portfolios again.

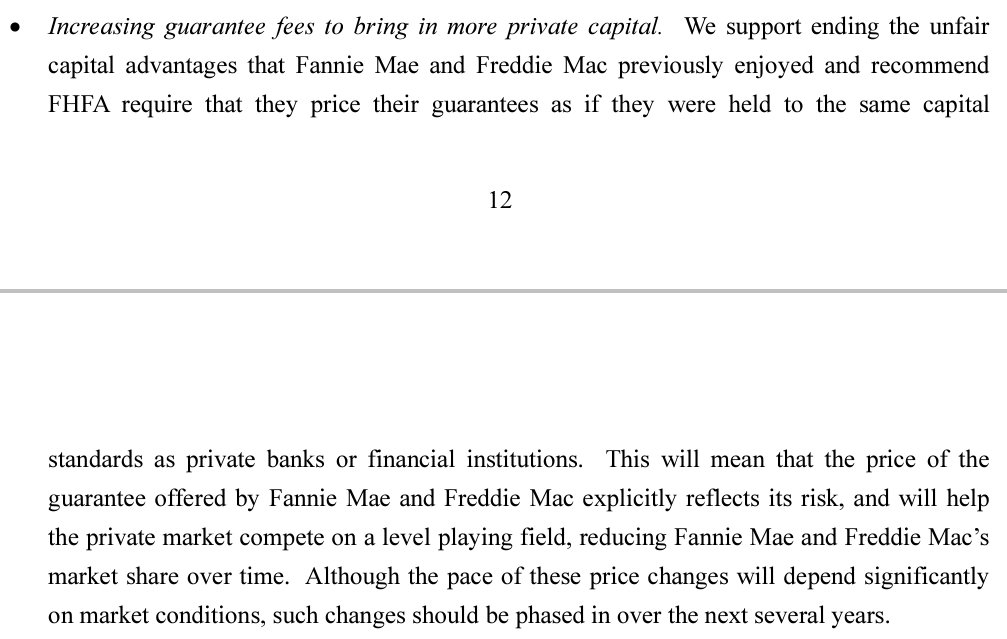

-Eliminate guarantee fee subsidies. The CBO formally accused FnF of delivering below private sector g-fees to increase their market share. It called it "subsidy cost" and it was charged on the Federal Budget.

-Eliminate their advantages on capital standards. For instance, the FHEFSSA required only a 0.45% of the off balance sheet obligations (MBSs) in the form of core capital. As explained in the aforementinoed 2011 UST-HUD Report to Congress, it was expressly pointed out that the guarantee fee increases had the purpose to hold FnF to the same capital standards as the private banks, that is, Basel framework for capital requirements. Source. Which is what has happened.

-Eliminate the Charter's UST backup of FnF as a last resort. Basel capital standards render this UST backup upon Capital deficiency (negative Net Worth) pointless.

-In the end, we are talking about revoking the Charters as endgame.

Now they see that their "Utility Model" for the extortion of resources out of FnF comes to an end and they are desperate to start the Charter of FnF over again. Too late. The Charter Act had a purpose when it was enacted and it was fulfilled. Nowadays, it's no longer necessary.

It was a Request for Input on pricing, not "pricing and capital" as Howard states. Primarily you must understand that it came out in light of the recent LLPA changes (upfront guarantee fee) and the manufactured controversy surrounding them.

Howard pioneered the complaints about the capital ratios in the comment submitted, stating that 4% plus capital is high, whithout specifying what was 4% of what, that led to his followers to claim that in the unrelated Proposed Rule coming up soon, the expectation is "change to 2.5% ERCF". Also, he is famous for the "bank-like", when Basel measures the same risk exposure regardless of the type of financial institution, and the Leverage ratio is far lower than the banks'.

And this is how you create buzz about a theme that isn't up for debate: Basel capital standards.

His objective is to distance the 2021 Basel framework for capital standards in FnF, from the 2011 conservatorship endpoint options chosen by the UST, with a Privatized Housing Finance System as a common feature, including the recommendation of g-fee hikes through today, both based on Basel.

So, people don't see that 2021 and 2011 are intertwined and the lengthy conservatorship turns out to be a simple Transition Period to build the increased capital requirements with the dividend impeccably suspended.

This is why the Capital Rule is called "back-end". It should have been announced in 2011, but they rather start the abuse of court process in an attempt to change the fate that was written.

Bradford-LuLeVan knew that the letter was addressed to Lael Brainard and not the other way around.

The thing is that if he can deceive two or three persons per day, he considers his job done and gets another check from a renowned hedge fund manager.

This is what the lengthy conservatorship is about: career scam artists at their finest.

Howard: "Separate Account? I don't know what that is."

FHFA attorney: "Mandatory dividends"

Berkowitz's attorney: "Implied contract"; "Constitutional damages".

Social media paid shills: "Expectation of 2.5% ERCF"

Etc.

Again with that bs, Bradford? It's always SPS LP.

There aren't two types of SPS.

Current status (estimated values):

SPS = $191 billion

LP = $300 billion

.jpeg)

The shareholders ❤️ the NWS dividend. Fastest speed for the Separate Account plan.

actual damage suffered by shareholders as a result of the NWS

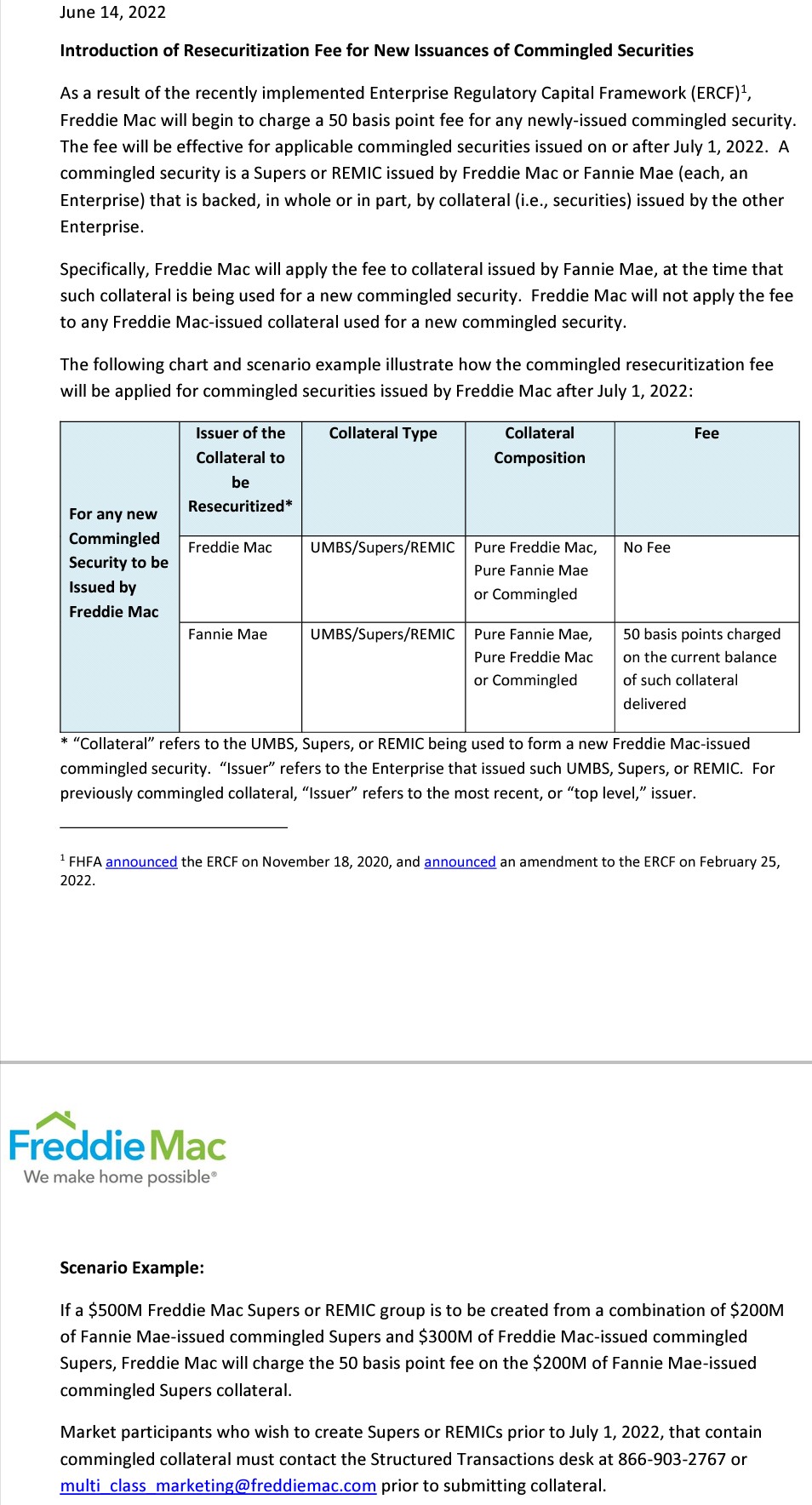

The Proposed Rule won't change the Basel framework for capital requirements, as I commented yesterday, but minor amendments like a risk-weight in the new security unveiled by Freddie Mac in June 2022 - Resecuritizations of commingled securities (Catastrophic-Loss reinsurance), etc. (Then, there was a RFI on pricing)

Yet more paid shills pile up (Robert from Yahoo, Alex Mazo, now FoFreddie) to claim that the ERCF will change to 2.5%. That's it. Without specifying what is 2.5% of what, because there are 8 combinations: CET1, T1 Capital, Core Capital, Total Capital and as % of RWA (Risk-Based) or % of Total Assets (Leverage ratio). This is why the ERCF data is presented with tables. Evidence that we are dealing with an organized group.

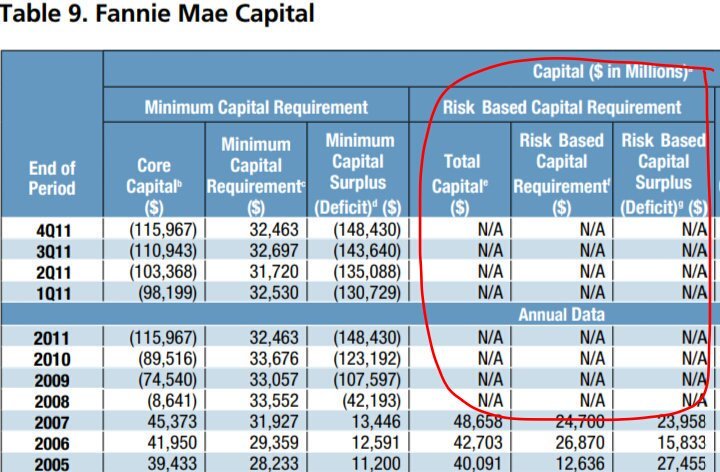

As I commented before, it seems that they want to alienate the Leverage ratio because it's the binding one (the highest), previously called Minimum Capital level in the FHEFSSA, by calling the Risk-Based capital requirement "Minimum Capital requirement", as always any requirement is called "minimum capital" for that variable. So, the ERCF table is reduced to one capital standard, instead of two, when the correct is three, as the statutory Critical Capital Level is absent from the ERCF tables (Don't meet a level considered critical, bothers for the FHFA director's propaganda "FnF remain undercapitalized", when the actual Capital Classification is Critically Undercapitalized enterprises. Adjusted $-194B Core Capital every quarter, to be precise.)

They attempt to distance the February 16, 2021 capital standards Basel framework adopted by the FHFA, renamed "back-end Capital Rule", from the 2011 Housing Finance System revamp chosen for the release by the UST, accompanied by guarantee fee hikes to the same endpoint: Basel framework ("capital standards in the private banks"). Hence, "back-end" Capital Rule that should have been unveiled within the typical 18-month period after the Risk-Based Capital requirement in the FHEFSSA was struck by HERA, directing the FHFA Director to come up with a new one ("The director shall", without a time frame). Primarily because you can't submit reports to Congress with data N/A. Conservatorship isn't an excuse. Just do it.

So, 2021 is linked to 2011 and they are after the Basel framework to prove it wrong.

Once proven that the Conservatorship turned into a Transition Period to meet the Basel capital standards, chosen for the release, the plotters are exposed, because this is the same organized group that initiated in 2012 the corrupt litigation that covers up the key statutory provisions and financial concepts, aiming to overshadow the aforementioned Privatized Housing Finance System endgame and the Transition Period to build capital typical every time that a Federal Agency imposes increased capital standards (For instance, recently the Fed and the FDIC gave the banks 5 years to meet the new capital standards and other rules. Or the Congress giving 10 years to the FHA for its 2% "economic net worth" ratio). In the end, they cover up that the dividend was impeccably suspended to build capital, as always, and that it's been concealed with a Separate Account plan similar to the 1989 statutory Separate Account with the FHLBanks (same assessments to a separate account. The difference is that the FHLBanks had to pay interests on RefCorp obligations at a time when they stood at a 10% rate and the remainder, reinvested in zero coupon bonds, reduced the obligation; Whereas with FnF, the dividends on SPS are suspended, so the whole assessment reduces the obligation SPS. Then, applied towards their recapitalization. Cumulative dividend with a small spread over Treasuries (weighted average 1.8% dividend rate. 5- and 6-year investments), is netted out with the interests on the $152B "credit due to FnF". Another difference is that with FnF, the assessment has been concealed under the guise of dividends to UST (Not actual dividends: restricted by law and unavailable funds for distribution as dividend, out of an Accumulated Deficit Retained Earnings account)

Notice that one of the 3 rounds of $4.8 billion in Punitive Damages requested by the Equity holders, is against this organized group counterparties of the DOJ in court for the Govt theft story, as opposed to the reality of the Separate Account plan.

On one hand we have these paid shills, on the other hand the big players with deep pockets behind: Moelis and the sponsors of its plan, Ackman, law firms, the plaintiffs, ACG Analytics, Pagliara, Howard, Rosner, financial analysts, etc.

It will be funny to see the breakdown of the $4.8B penalty.

Now, why don't you find another person claiming that there is expectation of 2.5% ERCF?

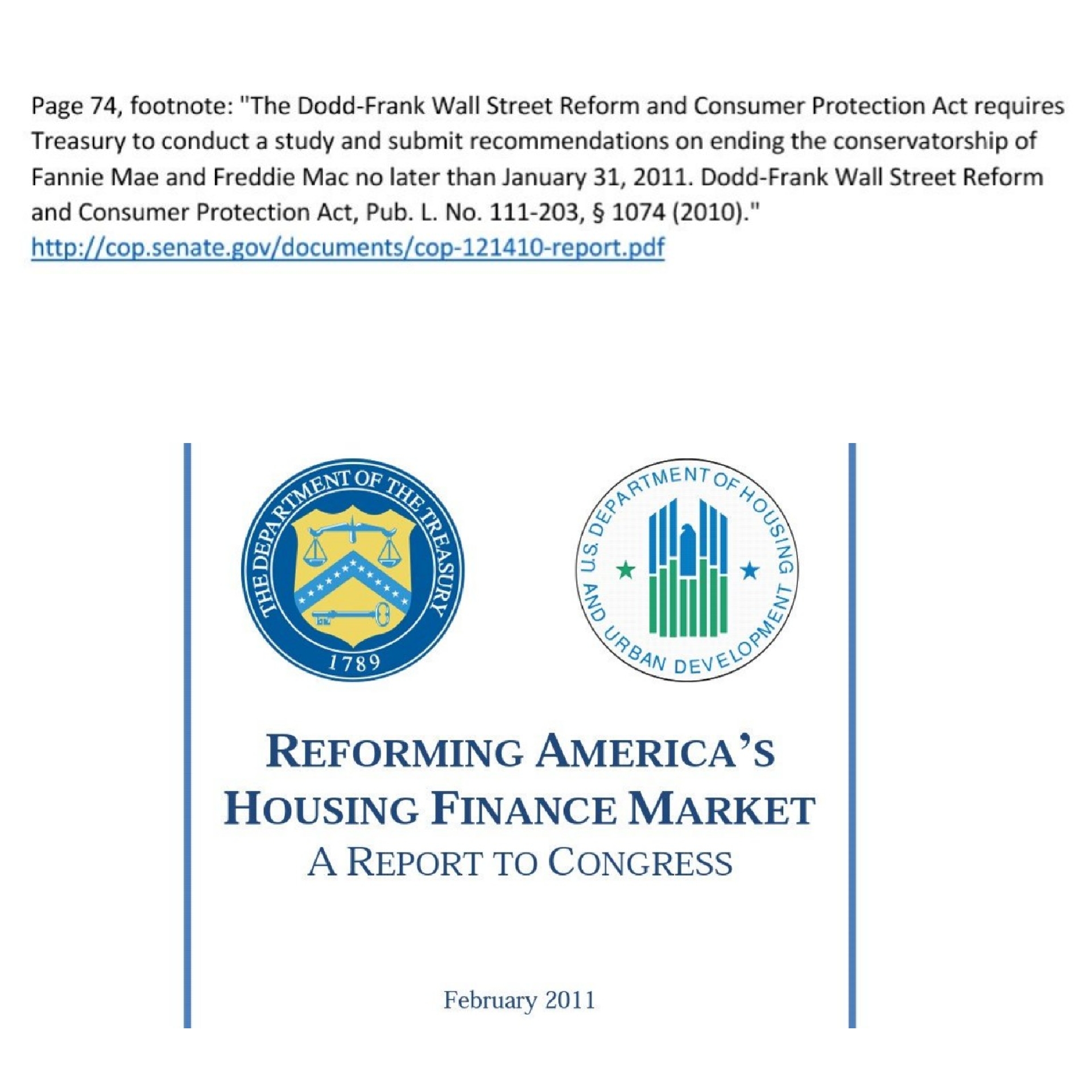

Don't miss this excerpt taken from the February 2011 Report to Congress by the UST-HUD, linking the guarantee fee hikes during Conservatorship to a Basel framework for capital requirements (adopted by the FHFA in 2021), which is also the endpoint of the Conservatorships with a Privatized Housing Finance System, as outlined in this report submitted at the request of the Dodd-Frank law.

Had the back-end Capital Rule been announced within the typical 18-month period (1992 FHEFSSA) since it was required by HERA ("The director shall"...without time frame), primarily because HERA struck the entire Risk-Based Capital requirement and, since then, it's N/A in the reports to Congress, the investors would have spotted the Separate Account plan from the onset, and would have snubbed the fraudsters with the Court cases, advocating the 10% dividend to UST and even requiring a dividend for themselves too.

Don't repeat the same post twice.⚠️TOS violation.

With the article that implies that the Capital Rule with Basel capital standards adopted by the FHFA for FnF, under an endgame Privatized Housing Finance System revamp chosen by the UST in 2011 for the release from Conservatorship, required by law, is up for debate. A big lie.

Yesterday I replied to your first post with 3 comments.

Now, do I have to repost my replies?

A judgment upholding the verdict is only expected by the plaintiff Joshua Angel, who writes here with more than 20 different ID's and often, animated conversations with himself, and also navy hedge fund, a JPS holder and member of the Pagliara's boys aiming to rip off the shareholders.

More abuse of court process by the DOJ-hedge funds allies.

A verdict is harmful to the shareholders' interests, as it advocates the 10% dividend and conceals the Separate Account plan that has repaid the SPS in full as of end of 2014 and has fully recapitalized FnF, even including the scenario of redemption of the JPSs, according to the law that they cover up and basic Finance.

We request a JNOV.

CORRECTION.There is a satellite Proposed Rule out there with minor amendments of the Capital Rule, like other amendments since it came into effect on February 16, 2021.

This time, it includes a risk-weight for the recent security "commingled securities", which is the Resecuritization, commonly known as Catastrophic-Loss Reinsurance. The grounds for the Housing Finance System revamp, either Govt- or Private-Catastrophic-Loss Reinsurance, with a g-fee already priced at 9.375bps.

Other minor changes, like a 0.6 risk multiplier on properties with government subsidies. Risk-weight on guarantee assets (FMCC's K-certificates in the Multifamily business) reduced from 100% to 20%.

We see that they are all credit risk assessment changes on assets that already had some credit enhancement among the enumerated ones in the clause Credit Enhancement, here, where the CRTs isn't included. Illegal.

2023 Proposed Rule.

The article is mixing up the Proposed Rule with the RFI, because it talks about a Proposed Rule on "pricing policies"..."price loans for nonbanks and depositories"..."comment letters on pricing", when only the RFI was related to pricing (upfront g-fee or LLPA)

The goal of the plotters is to transmit the idea that the Basel framework is up for debate. They don't like the idea of having used a conservatorship to increase the guarantee fees and ultimately, revoke the Charter, as explained in my prior comment. They rather keep the current Utility Model (secured deals through the extortion of resources out of FnF)

(*) complaints

It wasn't a Proposed Rule to begin with, but a Request for Input (RFP, not a comment period for a Proposed Rule) about the upfront g-fees (LLPA) recently updated, that even there was a question whether they should exist at all. So, the FHFA is clueless and it just pretends to be a busy regulatory Agency engaging in public debates, when there was no need.

Therefore, it had nothing to do with the Capital Rule and its Basel framework. The complains about Basel are low profile, because it's an international standard for the same risk exposure.

This is what happens when you don't want the prior UST backup of FnF "at rates that take consideration the Treasury yields as of the last day of the month preceding the purchase" and you don't want to subsidize the guarantee fee (FnF was accused by the CBO of delivering below private sector g-fees to increase market share and called it "subsidy cost" charged into the Federal Budget at the time), which was part of the Charter dynamics.

The goal during Conservatorship was to increase the g-fees, so FnF compete on a level playing field and in order to bring in more competition from the fully private sector, reducing their market share (shrink footprint)

This is an excerpt explaining it, taken from the famous 2011 UST-HUD Housing Finance System revamp with the ultimate endgame: a 3-option plan Privatized Housing Finance System chosen by the UST as "recommendations on ending the conservatorships, no later of January 31, 2011", at the request of the Dodd-Frank Act, explaining it:

Finally, the Credit Risk Transfers (CRTs) are unauthorized in the Charter's Credit Enhancement clause and likely a backdoor Commitment Fee to enrich the UST, which is also barred in the Fee Limitation clause. We are requesting a refund of the CRT expenses, net, as explained yesterday. More reasons why the Charter ought to be revoked.

No one should have the perception that will ever get $1 out of FnF while they remain undercapitalized

"Lamberth rebate" is fraud in every aspect you can think of. From an illegal Class Action with the absence of the FNMA holders, the fiction of "implied contract", disregard of the laws, phony economic harm, etc. and epitome of corruption, as the payment of Securities Litigation judgments sought, is restricted in the same statutory provision that they've covered up from the onset, that also bars the dividends and today's gifted SPS, and whose exceptions are the grounds of the Separate Account plan:

-Reduce the SPS: U.S. Code §4614(e)

-Recapitalization: CFR 1237.12

Inspector General makes ZERO mention of the UNANIMOUS

8-0 JURY TRIAL Verdict AGAINST the FHFA & TREASURY !

All the officials involved will agree with the Separate Account plan, because we are talking about breach of statutory provisions, which carries prison sentence. All of them covered up by the corrupt litigants, for which they owe us damages.

The evidence that the officials always wanted to make sure that they were upholding the law with every action, either directly or with a Separate Account knowing that the Incidental Power allows the conservator to lie about its actions if the endgame is the rehabilitation of FnF (Justice Alito's prerequisite) as an exit strategy, is found:

-The July 20, 2011 Final Rule "for the transparency of the conservatorship", snuck at the end a shocking surprise. It contemplated the scenario when the SPS are fully repaid with the trick in the law of the exception to the Restriction on Capital Distributions, under the guise of dividends,as it added up new exceptions: deplete capital in FnF for their Recapitalization ("to meet the Risk-Based Capital and Minimum (Leverage) Capital requirements"), that is, a Recap outside their Balance Sheets. This is a separate account wording.

Notice that July 20, 2011 is exactly the Time Limitation for the Acting Director DeMarco. We see the intentionality to make sure that the alibi is enacted in accordance with the law. We also can determine that they were thinking of the NWS dividend as the fastest speed to repay the SPS and they needed another exception to apply the assessments towards (not actual dividends but capital distributions under the guise of dividends)

-Mel Watt lifted the suspension of the 4.2 bps on new acquisitions funneled to 2 Affordable Housing funds managed by the UST and HUD, at the end of 2014. The law only allowed three cases when this payment is suspended. So, when it was lifted it only could be if the FHFA director considered that FnF have achieved some milestone regarding their "financial stability". That milestone can only be the fully repayment of the SPS at the end of 2014 in Fannie Mae (Freddie Mac one year earlier. Watch my signature image below) which is a variable to measure their solvent condition, as the SPS are obligations (debenture). More detail here.

The Separate Account plan is the alibi that legalizes every action. Other examples of alibis, are simple lies not backed up by the law, like Sandra Thompson's "CRT to protect the taxpayer", when it's unauthorized in the Credit Enhancement clause of the Charter Act, the taxpayer doesn't bear credit risk in FnF and even hinders the repayment of the SPS ("obligations in respect of capital stock": also in the SPSPA that you have pointed out), because CRT are expenses that should have been used to repay the SPS instead, hadn't been repaid many years ago, and kept as capital (Retained Earnings) for the soundness of FnF. Likely, a backdoor Commitment Fee to enrich the UST, etc. The sacking of FnF at its finest, with the former Blackrock and Morgan Stanley, Craig Phillips, once sued by the FHFA for selling toxic mortgages to FnF, turned into "counselor for the Treasury" to set up CRT symposiums and hold up this scam (Then, the Bitcoin symposiums popped up. A telltale sign). We request a refund of the amount net (deductable expenses at the time, now they pay taxes) and its posting in the Retained Earnings accounts.

They are officials and bankers attempting to make up for the losses in the money losing 1989 scheme with the FHLBanks, Funding Corp and RTC, with the taxpayer on the hook for a $48.8B losses caused by RTC's complex Public-Private Partnerships for the sacking of the taxpayer, and the scam of the officials back then: "the FHLBanks only had an obligation to pay interests", when that was Funding Corp, not the FHLBanks that had to pay down the principal of the obligation RefCorp.

It turns out that the officials back then, are the same individuals in Fanniegate: DeMarco (GAO and UST), Sandra Thompson (FDIC), Sheila Bair (FDIC, then chairman of the BOD of FNMA to transmit the idea that FNMA was included in the prior RTC scheme, that was managed by the FDIC) and Calabria (Senate staffer)

You learn first what a dividend is.

1st. Restricted when undercapitalized (to build capital obviously)

2nd. Unavailable funds for distribution, out of a Retained Earnings account (Equity) with Accumulated Deficit all along.

3rd. A breach of the conservator's Rehab power.

4th. In this world, mandatory dividend doesn't exist (FHFA's attorney), otherwise it'd be interests payments (expense). Then, it'd be a different security.

Therefore, what FnF sent to UST can't be called dividend because it can't be an actual dividend.

It was a capital distribution under the guise of dividend payment, that is applied towards the exceptions to the Restriction on Capital Distributions in the FHEFFSA (reduction of SPS), then the CFR1237.12 (Recapitalization)

The conservator's Incidental Power allows it to mislead (take any action...) if the endgame is the rehabilitation of FnF (...authorized by this section)

The goal is to legalize this action that shouldn't have existed.

Who in their right mind would pay dividends during a Conservatorship for Critically Undercapitalized enterprises, first 10%, then a NWS dividend? Someone carrying out a Separate Account plan, similar to the one in the 1989 scheme with the FHLBanks and with the same officials (DeMarco, Sandra Thompson)

Learn what a dividend is.

Explanation of the 3 rounds of Punitive Damages at a glance.

$4.8 billion each.

The third round corresponds to the peddlers of the Government theft story in formal documents, preventing the stocks from trading at their fair value all along. The actual damage, as the economic harm is fully redressed with the announcement of the Separate Account plan.

In the No Takings scenario, the DOJ is exempt from paying damages to the common shareholders (The first two rounds. The first is waived as a gift to the DOJ, not because there aren't Securities Law violations; and the second because the Deferred Income is recovered in full), reducing the price tag to a mere $1.3B each round, for the JPS holders.

The 3rd round can't be reduced. Accountability is the key in the Rule of Law.

3X PUNITIVE DAMAGES

— Conservatives against Trump (@CarlosVignote) October 8, 2023

-8 Securities Law breaches

-Deferred Income accounting

-Law firms &Co

0.5% IRR on the harm for real(Avg gap FV🆚Mkt Price =half JPS) 15 years =$0.97 in a $25pv JPS (Cs=$50pv JPS)

Breakdown$FMCC $1.3B

JPS=$0.5B$FNMA $2.2B

JPS=$0.8B#Fanniegate @TheJusticeDept https://t.co/sz2YTYk8rC pic.twitter.com/cxU3v27ynd

The rebel pro se plaintiff reposts all his thoughts refuted multiple times before, thinking that it will change the outcome.

-No commitment fee was ever assessed or collected. The initial SPS issued for free might well be considered a higher compensation to UST for the SPS, since the subsection (g) allows infinite rate. Then, cancelled due to subsection (c) original UST backup of FnF. The Warrant also issued for free, to skip the prerequisite on purchases of "(iii) to protect the taxpayer" (collateral). So, collateral it is, purchased at $0 cost.

-The SPS aren't new products. It's a security. No activity behind which is what makes a security a product. I explained it to your other you (Barron) once.

-The conservator isn't a trustee.

-The SCOTUS highlighted the prerequisite of "rehabilitation of FnF" with regard of the 3rd amendment. It didn't even mention the NWS dividend by name. Basically, the SCOTUS legalized the Separate Account plan for the extortion of their resources in the meantime. Everything but a dividend, as it is a distribution of Earnings (Core Capital), what rehabilitation is about.

-Shamefully echoing the CBO's take, clueless about the conservatorships of FnF. There is no Nationalization possible during a Conservatorship. Let alone barred in the Charter Act.

-You keep on covering up the laws in force, FHEFSSA and the Charter Act, as amended by HERA. It isn't HERA alone. For instance, the FHEFSSA would declare FnF Critically Undercapitalized as of end of June, 2023. Mnuchin's UST rushed to "recommend Congress to repeal the statutory definitions" (2019 UST Housing Reform plan)

-The repurchase of the SPS in the law isn't a refinancing option as you claim, since the cash required can be achieved through the increase in the Common Equity, which is what has happened (image below)

-You can't understand that a dividend is a capital distribution. Calling it interests to skip the restriction on dividends in the law, doesn't make it interests.

-And what about today's gifted SPS as compensation to UST and your beloved "Lamberth rebate", a payment of Securities Litigation judgment? Both are capital distributions too. Then, restricted in the law.

-A dividend can't possible be paid, out of an account Accumulated Deficit Retained Earnings. A dividend is a distribution of Earnings and you need a positive balance in that account, not just annual income which is the result of operations during a period of time. The actual picture of the company at a determined date, is the Balance Sheet, with the Retained Earnings account. You need to replenish this account before thinking of distributing dividends. Let alone considering all other restrictions: undercapitalized and Table 8 of the Capital Rule (Payout ratio = 0%)

Get a grip and pay us punitive damages for the conspiracy aiming to rip us off, jointly with the rest of your gang.

Separate Account (DOJ) + the peddlers of the government theft story (The Plaintiff Joshua Angel Gang), prevent the stocks from trading at their fair value.

The damage is, thus, the spread Fair Value versus Market Price.

$4.8 billion will do it.

Our negotiator rules out a Takings. Everybody calm down.

I already mentioned here, that the absence of the typical time frame to write regulation in order to uphold the requirement in an Act, melts everything down. Meaning a game changer.

The Separate Account is legal thanks to the conservator's Incidental Power.

A Takings of our stocks at their adjusted Book Value, legal as well.

But the fact that this plan of deception was enabled by an arbitrary act of the FHFA, by enacting the Capital Rule 13 years after HERA struck the Risk-Based Capital requirement and mandated the FHFA director to come up with a new one ("the Director shall..."), it would make it an opportunistic Takings (the UST would have taken advantage of this arbitrary decision of FHFA) and thus, it won't be feasible.

The FHFA adopted the Basel framework for capital requirements in its Capital Rule. Had it been within the 18-month period after HERA was enacted, as usual (1992 FHEFSSA), it would have been very close to the mandate on UST in the Dodd-Frank Act of 2010 to outline recommendations on ending the conservatorships ("no later than January 31, 2011"), and then, very close to the proposed 3-option Privatized Housing Finance System revamp, which also means Basel framework for capital requirements. So, the investors would have spotted the Separate Account plan from the onset, compelling the FHFA and the UST to make it public and thwarting the plan of acquiring the entire FnF on the cheap at the adjusted BV.

A No Takings is, therefore, a scenario of normalcy, taking into account also the PROHIBITION of UST to make profits with FnF, other than a rate with a small spread over Treasuries (UST backup of FnF)

"BACK-END" CAPITAL RULE ↑ CHANCE OF NO TAKINGS

— Conservatives against Trump (@CarlosVignote) October 7, 2023

Transition Period to build capital, adding up to normalcy, like the PROHIBITION to make profits (It snuck Legislative fees: $39B TCCA +$5B 4.2 bps)

JPS redeemed.

Deferred Income amortized in full.

No merger.

$150B refund.#Fanniegate pic.twitter.com/U83VJNevMu

If you reply to yourself, you are cray. You would be having conversations with yourself.

Other theme is when you refer to yourself in third person, which is a literary technic and it's adivised when writing in-depth financial analyses or in academic writing.

Send this message to your more than 20 or 30 different ID's on this board. But please, send private messages. You will have an entertaining morning!

How many rabbits are you going to pull out of your hat, pro se plaintiff?

That letter represents only your thoughts and you want to pass it off as the opinion of the Ihub board.

Your opinion refutted multiple times, like here about the CFR 1237.12.

You are also accused of covering up key statutory provisions like the cheap UST backup of FnF in the Charter Act (redeemable obligations SPS), expressly written as a last resort ("the operations shall be financed by private capital to the maximum extent feasible)" in the section Purposes, and in exchange for their Public Mission set forth in that section, or even the coverup that the laws in force are the FHEFSSA and the Charter Act, as amended by HERA, not HERA alone, and also accused of conspiracy to rip off the shareholders, advocating the 10% dividend to UST (barred and unavailable funds for distribution of dividend, out of an Accumulated Deficit Retained Earnings account)

You don't even know that the dividend was suspended to build capital and currently there is a compensation to Treasury in the form of gifted SPS (a capital distribution restricted and Financial Statement fraud with these SPS absent from the balance sheets)

the ongoing senior preferred dividend payments

We only read our negotiator's tweets on the #Fanniegate hashtag.

Bradford and navycmdr are owned by the hedge funds.

Leave them alone, will ya?

In addition, purchasers must offer delinquent borrowers a waterfall of loss mitigation options, including loan modifications, which may include principal forgiveness

We already had en banc and appeal to SCOTUS.

With the same case, Collins. And both had the same outcome, necessarily there is a Separate Account plan that complies with the FHFA-C's statutory mission (Power): put FnF in a sound and solvent condition, which Justice Alito called "the rehabilitation of FnF".

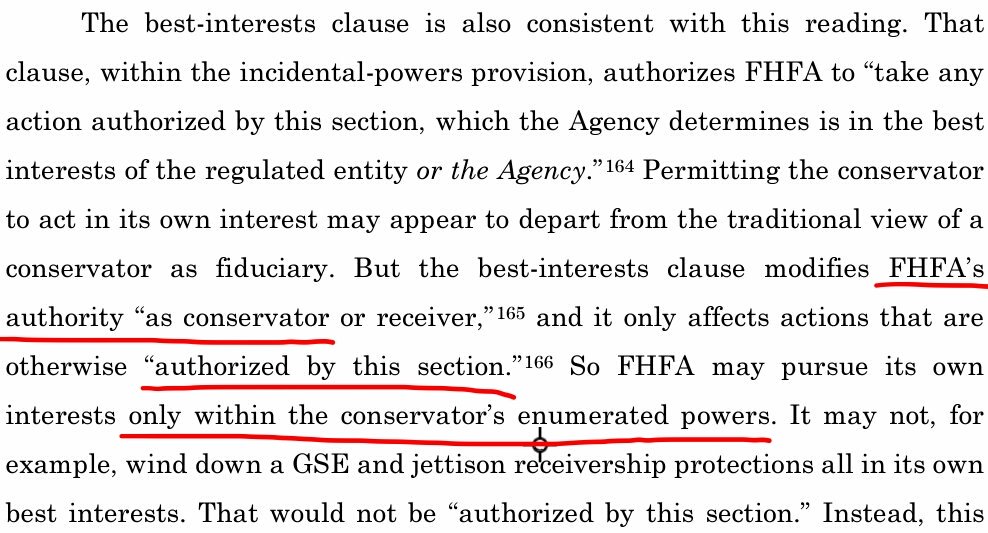

And both judges coincided in the interpretation of the Incidental Power as well. Justice Alito, in addition, interpreted the second part of the Incidental Power that Judge Willett (5th Circuit) missed. This is why it's been determined that both were synchronized:

Judge Willett stating that "take any action authorized by this section" means actions "within the enumerated powers" (Rehab)

and Justice Alito, after interpreting "authorized by this section" with "rehabilitate FnF", he followed up interpreting what "in the best interests of FHFA" means, with:

It may aim to rehabilitate FnF in a way that, while not in the best interests of FnF, is beneficial to the FHFA and, by extension, the public it serves.

In addition, non-performing loan buyers must offer delinquent borrowers a waterfall of loss mitigation options, including loan modifications, which may include principal forgiveness,

Navycmdr, a plotter JPS holder, harasses the UST.

Not the first time.

(more GOVT WASTE of $Taxpayers Dollars$)

This mistake in the HERA of 2008 melts everything down.

Pelosi (sponsor) and Calabria drafting HERA, forgot to include the typical time frame to write the regulation required in the Act.

Because it took the FHFA Director 13 years to write the required Capital Rule (effective February 16, 2021), primarily because it struck the entire Risk-Based Capital requirement, when it was granted an 18-month period in the FHEFSSA of 1992, the law that established capital ratios in FnF for the first time, makes the 15 years in Conservatorship a de facto Transition Period to meet the capital requirements, and de Capital Rule renamed "back-end Capital Rule" (unveiled at the end of the Transition Period)

Since then, we are just determining which metric to choose for the release and Adequately Capitalized after redeeming the JPS, with the Separate Account plan, seems to be the winner, under their motto: "Take no captives" (Takings by UST ; redemption of JPS by FnF)

The reason for the delay is simple: attempt to distance the Basel framework adopted by FHFA for capital requirements (for fully private corporations. Charter revoked), from the UST-HUD's Privatized Housing Finance System revamp chosen in 2011 by the UST for the release from Conservatorship, at the request of the Dodd-Frank law, so people would forget that both are intertwined and that FnF were in the Transition Period, for the plotters' Government theft story that aims for a different outcome.

Outcome in #Fanniegate of absence of time frame to write regulation(1992 FHEFSSA: 18-mth period)

— Conservatives against Trump (@CarlosVignote) October 6, 2023

De facto:

▪️15-yr Transition Period to meet C.levels.

In 1992:

- 4yrs for the Risk-Based C.(after initial 18 mths)

-Leverage: Phased in w/ an interim ratio reduced

▪️C.Rule "back-end" https://t.co/s16JMo2XRe pic.twitter.com/gMoIdkoiR8

*FANNIEGATE SUMMARY* Don't miss the response to representative Ogles posted yesterday, that serves as a summary of this conspiracy to rip off the shareholders of congressionally chartered private corporations.

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=172963035

The UST can make a profit of $312 billion with the Takings of our stocks and resale, after a refund of the amount due to FnF, $152B, which can be reduced to $150B, caused by the Asset-Liability matching principle.

Not bad knowing that the UST is prohibited to make profits using FnF, which was broken with the legislative fees: 10bps g-fee (TCCA fees) and 4.2bps on new acquisitions for the Affordable Housing Funds managed by the UST and HUD.

The ultimate amount of Punitive damages depends on whether the DOJ bails out its counterparty, the peddlers of the Government theft story in formal documents: Law firms, plaintiffs, Pagliara, Howard, Rosner, Ackman, Moelis, ACG Analytics, financial analysts, etc., accused of stock price manipulation and conspiracy, for the fact that they agreed with the payment of 10% dividend during the transition period to build capital (financial rehabilitation or sound condition), while FnF showed Accumulated Deficit Retained Earnings accounts (a dividend is a distribution of earnings. Not only negative balance, but also Payout ratio = 0% in the Table 8) and after the coverup of the Restriction on Capital Distributions. Etc.

It also depends on whether there is a Takings or not, as the common shareholders are excluded from the second round of $4.9 billion in Punitive Damages for the Deferred Income accounting (the upfront g-fee is, in truth, a Delivery Fee) if there isn't a Takings.

The first round of $4.9B serves as a settlement of the 8 Securities Law violations in conservatorship (the SPS are issued so that the stocks are dated, not "increased". Goal: skip the December 2009 deadline on purchases by UST for the infinite rate authorization subsection (g), the grounds of the Separate Account plan, as subsection (c) prevails: redeemable obligations SPS, that can be repurchased on the "open market", that is, in the separate account)

I would ban the DOJ from bailing out its counterparty in the third round of $4.9 billion, forcing it to go after the masterminds and sponsors instead, which could go as far as 1989 for those involved in the rip-off of RTC and the Funding Corp scheme, where, likely, the UST lost $48.8 billion in total ($30B invested in RefCorp obligations, plus $18.8B invested directly in RTC, required by law) and then, the same officials and investors in RTC's Public-Private Partnerships are using FnF to make up for their losses; Those that authorized the purchase of PLMBS in FnF, which are banned in the Charter's Credit Enhancement clause; Former Fannie Mae CFO Howard for the stock buybacks to boost his EPS target bonus, an investment unauthorized in the Charter Act that depleted Equity and core capital, both lacking when the crisis struck in mid 2008, prompting the conservatorship (ongoing damage in the line item Treasury Stock on the Balance Sheet). And, by the way, the one that authorized the initial issuance of $1B SPS for free, fined as well, as it reduced core capital: Additonal Paid-In Capital account, against the FHFA-C's Rehab power to begin with (Paulson needed $1B additional reduction of capital to justify the conservatorship)

The 3 rounds of $4.9B in Punitive Damages are secured, knowing that it's been a simple case of Transition Period to build capital (15 years), with a back-end Capital Rule (when it's announced and fully effective at the end of the typical Transition Period, as commented yesterday)

The back-end Capital Rule (it was unveiled at the end of the transition period when the rule came into effect) is evidence of the Separate Account plan.

The Federal Agencies always allow a transition period to meet the capital requirements.

Let alone Congress' 10 years to FHA.

In the tweet, it's pointed out the 5 years that the Fed and the FDIC have given to the banks for the recent proposed capital rule, until it becomes fully effective in 2028.

The Capital Rule of FnF came into effect on February 16th, 2021. Freddie Mac met the Adequately Capitalized threshold with the first quarter 2021 results, under the Separate Account plan.

After that, FnF entered the period to determine which threshold to choose for the release from Conservatorship, taking into consideration that it has to be met together.

I can't think of a more stringent threshold than becoming Adequately Capitalized after redeeming the JPS. That threshold is met with the results of third quarter of 2023 in Fannie Mae that was lagging ($1B Tier 1 Capital shortfall over Min Leverage Capital requirement as of June 30, 2023)

THE FED's🆕CAPITAL RULE, EVIDENCE OF FnF's SEPARATE ACCT

— Conservatives against Trump (@CarlosVignote) October 5, 2023

🆕requirement to record unrealized losses as AOCI,effective 2028:"Phased in over 3yrs starting July1,2025"

FnF: effective Feb16,2021.

Thresholds met in 1Q2021-3Q2023:

Adeq Cap?

25% Buffer?

Adeq Cap +JPS redeemed?#Fanniegate pic.twitter.com/aMtk9nE7VC

A bill "To require the Secretary of the Treasury to submit to the Congress completed proposals for the termination of the conservatorships".

A mandate to the Treasury Department that already had this mandate in the Dodd-Frank law and the options recommended were submitted in a Report to Congress "no later than January 31, 2011", with the typical delay by UST 11 days after the deadline, every time that Congress requires something to the Treasury Department. For example: Law: "Restrictions for electric vehicle tax credits no later than Dec 31, 2022". The UST on D-day: "March".

A 3-option plan based on a Privatized Housing Finance System.

In brief:

1- Privatized Housing Finance System + targeted assistance: FHA, USDA, VA.

2- 1 + Govt guarantee in crisis.

3- 1 + Govt Catastrophic-Loss reinsurance.

And DeMarco began to work hard on it right away:

Then, the CSP, UMBS, pilot programs with the States' HFAs, the February 16, 2021 Capital Rule that adopted the Basel Framework (international standard for fully private financial institutions), Freddie Mac unveiled the Resecuritizations on June 2022, a security that would enable the option 3 with a Govt Catastrophic-Loss reinsurance, but it could also be private reinsurance for the options 1 and 2, etc. It was first priced at 50 bps, but soon after it was rectified to the current 9.375 bps.

The first one that wanted to override this mandate by law was Trump, who used a Presidential Memorandum to give it some sort of legality, to request to the Secretary of the Treasury a Housing Reform plan.

In this Housing Reform plan of September 2019, the Treasury Department of Goldman Sachs' Mnuchin proposed the China-sponsored Govt Explicit Guarantee on MBSs.

This is why the FHFA first priced the Resecuritizations at 50 bps, thinking of China, but then, with 9.375 bps, it allows a Privatized Housing Finance System, because a Govt Catastrophic-Loss reinsurance is triggered only when the guarantor files for bankruptcy. So, the capital level in the guarantor is the "first-loss" protection.

Now, representative Andrew Ogles, once FnF are on the finish line (Fannie Mae was lagging with $1B Tier 1 Capital shortfall over Leverage Capital requirement on June 2023, under the scenario of redemption of JPS) comes up with the same requirement of recommendations on ending the conservatorship that Goldman Sachs' Mnuchin required in an amendment of the SPSPA, in an attempt to substitute the actual mandate in the Dodd-Frank law, but, instead of requiring it pursuant to a Presidential Memorandum, now representative Ogles requires it by law, so a report has to be submitted to Congress.

This SPSPA amendment of January 14, 2021, was signed 12 days before Secretary Yellen was sworn in. Mnuchin and Calabria were in a hurry to amend it, thinking that they are lawmakers sat at a table with the power of amending the Charter and the FHEFSSA through "agreements", rewriting it with whatever they wish for: commitment fees, etc. or even made-up financial concepts like "Capital Reserve End Date", when the Capital Reserve meets the capital requirements, instead of the capital metrics: core capital, Tier 1 Capital, Total Captial or CET1, as per Basel framework that sets the international financial standards.

Let alone that what they call "Capital Reserve", is the $111B SPS absent from the Balance Sheet (once they are recorded, the offset reduces the Retained Earnings just built, leaving only the SPS on the current $111B Net Worth). What lies behind is that they want to meet the capital levels building SPS.

This is why the Mnuchin's Treasury recommended to Congress in its Housing Reform Plan to repeal the FHEFSSA definitions, like the one that states that the core capital is the one that meets the Minimum Leverage Capital requirement for the capital classification of Undercapitalized. They don't want you to know that the current adjusted Core Capital stands at $-194 billion together (resulting in a $400B capital shortfall over Leverage capital requirement) and they rather choose their made-up "Capital Reserve" to meet the Leverage capital requirement. The definitions of financial concepts bother to the investment banks for their Rule of Plunder.

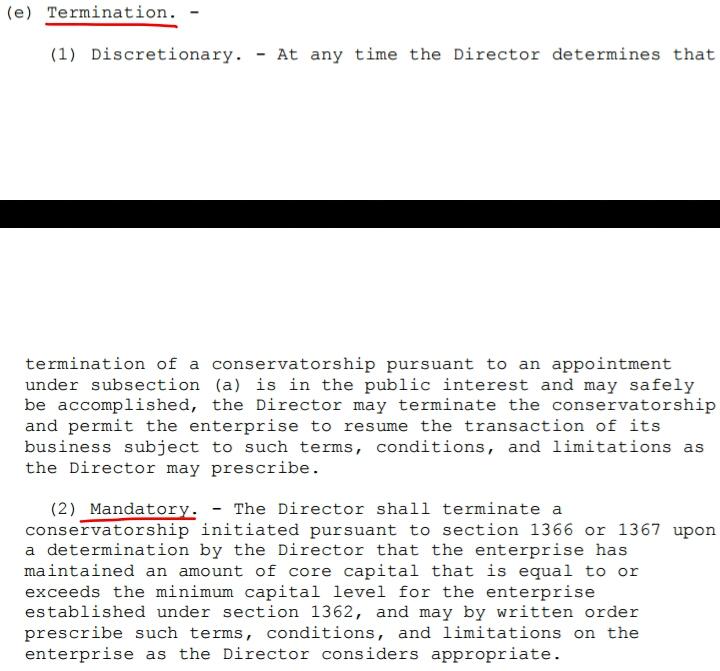

For the exact endpoint of conservatorship, knowing that it's a Privatized Housing Finance System and Basel framework, evidently it should be mandatory upon FnF become Undercapitalized again, which makes them Adequately Capitalized at the same time, as its threshold is lower, or it could be well before at the discretion of the FHFA Director with a Capital Restoration Plan, which hasn't been the option chosen because, as stated before, FnF have gone all the way through meeting the mandatory release Undercapitalized under the Separate Account plan.

Both endpoints were established in the FHEFSSA before being struck by HERA.

Fanniegate is all about coverups and attempts to substitute the law in force and financial concepts.

Notice that this copycat report about recommendations on ending the conservatorships requested in the Mnuchin's PA amendment, was also requested to Secretary Yellen in a House Financial Services Committee hearing by representative Warren Davidson a few months ago.

So, now representative Andrew Ogles wants this requirement in the PA by Goldman Sachs' Mnuchin, to rank equally to the real mandate by law in 2011.

The reality is that it's an attempt to substitute it, when they spotted that the endpoint is in the making according to the law (the rehabilitation of FnF, as stated by Justice Alito and judge Willett)

"Do you mind sharing the link?"

Check the Table 8 for dividend payments.

Payout ratio: the percentage of net income that a company distributes as dividend (preferred and normal dividend) to the Equity holders.

What's worse, the 2016 "Trump will save us" now, or a expectation to get the "Lamberth rebate"?

Does judge Sweeney know that you spend the day troubling the FnF shareholders here, with your more than 20 different IDs, Mr. Pro Se?

A judge rules that expert witness testimonies aren't evidence.

Trump said yesterday about the judge in Manhattan ruling over one of his cases.

It dynamites the Lamberth trial, filled with the so called "experts" as substitution for the law, making up damages with the share price reaction, when the damage is the dividend to UST in undercapitalized enterprises, a dividend paid out of unavailable funds for distribution (accumulated deficit Retained Earnings accts), the gifted SPS nowadays, the Warrant, etc. The goal was to make the JPS holders get back dividends, a swap JPS for Cs and prevent the FMCC holders from filing new lawsuits as they've been included in the illegal Class Action, where the FNMA holders were absent.

So many testimonies instead of the law, that this is why the one making up the whole staged trial came up with the idea of the jury asking for the HERA text on the last day (besides MBS data of 2011 and 2012. Joking, right?), pretending to have knowledge of the law, when the laws in force are the FHEFSSA and the Charter Act, as amended by HERA, and about rulemaking, the July 20, 2011 Final Rule that supplemented the Restriction on Capital Distributions with CFR 1237.12 and also, precisely, it was expressly included the payment of Securities Litigation judgments as one of the capital distributions restricted, by amending its definition. The determination of damages was the only task of the jury. Therefore, they missed key legislation and rulemaking for the verdict.

Let alone that leaving the decision to 8 individuals is outrageous, that looks more like expert witnesses but without the label of "expert". They are just called on this board: "8 random people".

This will backfire and judge Lamberth has no other option than to rule: "Judgment notwithstanding the verdict" (JNOV): the jury incorrectly applied the law in reaching its verdict.

E.g. SPSPA: "Conservatorship pursuant to Section 1367(a) of the FHEFSSA of 1992".

Expert witness is synonym of conflict of interests and, according to the Manhattan judge, it isn't evidence and now we will call it "fabricated evidence" in those cases where they showed up.

Notice that Trump is also accused of fabricating evidence in Fanniegate with the famous Trump letter that the attorney for Fairholme submitted in court in the Collins case, to later falsely allege that it's what the SCOTUS requested.

There is a big problem with these law firms fabricating evidence and other is covered up. Law firms that later hire Goofy's for social media propaganda, etc. They are required to pay us a compensation for Punitive damages.

Mr. Pro Se, quit posting the CFR 1237.12 that supplemented the Restriction on Capital Distributions in the law FHEFSSA, amended by HERA: U.S. Code §4614(e).

Are you supplementing it or bypassing it?

A July 20, 2011 Final Rule, coinciding with the date of Time Limitation of Acting Dtr DeMarco, that was meant to continue with the Separate Account plan once the SPS were fully reduced in the law, as now it allows to deplete capital (under the guise of dividends that weren't actual dividends) for their recapitalization (to meet the Minimum Capital and Risk-Based Capital requirements), which is a Separate Account wording right there. A recap outside their Balance Sheets.

CFR enacted 2 weeks before the FHFA announced a proper Recap plan for the FHLBanks in this press release, by the way, with the famous: "The FHLBanks fulfilled their obligation to pay interests", but they still have to repay the $30B principal of the RefCorp obligation, as Equity holders of Funding Corp. A $30B loss of the Treasury that, likely, subscribed to this obligation, reinvested in RTC. Plus an additional $18.8B that the Treasury invested directly in RTC, required by law. A $48.8B hole that the same officials back then (ST and DeMarco) are trying to offset with monies from FnF.

This usage of the Federal Register for conspiracies is unacceptable.