Thursday, October 05, 2023 2:45:25 AM

A mandate to the Treasury Department that already had this mandate in the Dodd-Frank law and the options recommended were submitted in a Report to Congress "no later than January 31, 2011", with the typical delay by UST 11 days after the deadline, every time that Congress requires something to the Treasury Department. For example: Law: "Restrictions for electric vehicle tax credits no later than Dec 31, 2022". The UST on D-day: "March".

A 3-option plan based on a Privatized Housing Finance System.

In brief:

1- Privatized Housing Finance System + targeted assistance: FHA, USDA, VA.

2- 1 + Govt guarantee in crisis.

3- 1 + Govt Catastrophic-Loss reinsurance.

And DeMarco began to work hard on it right away:

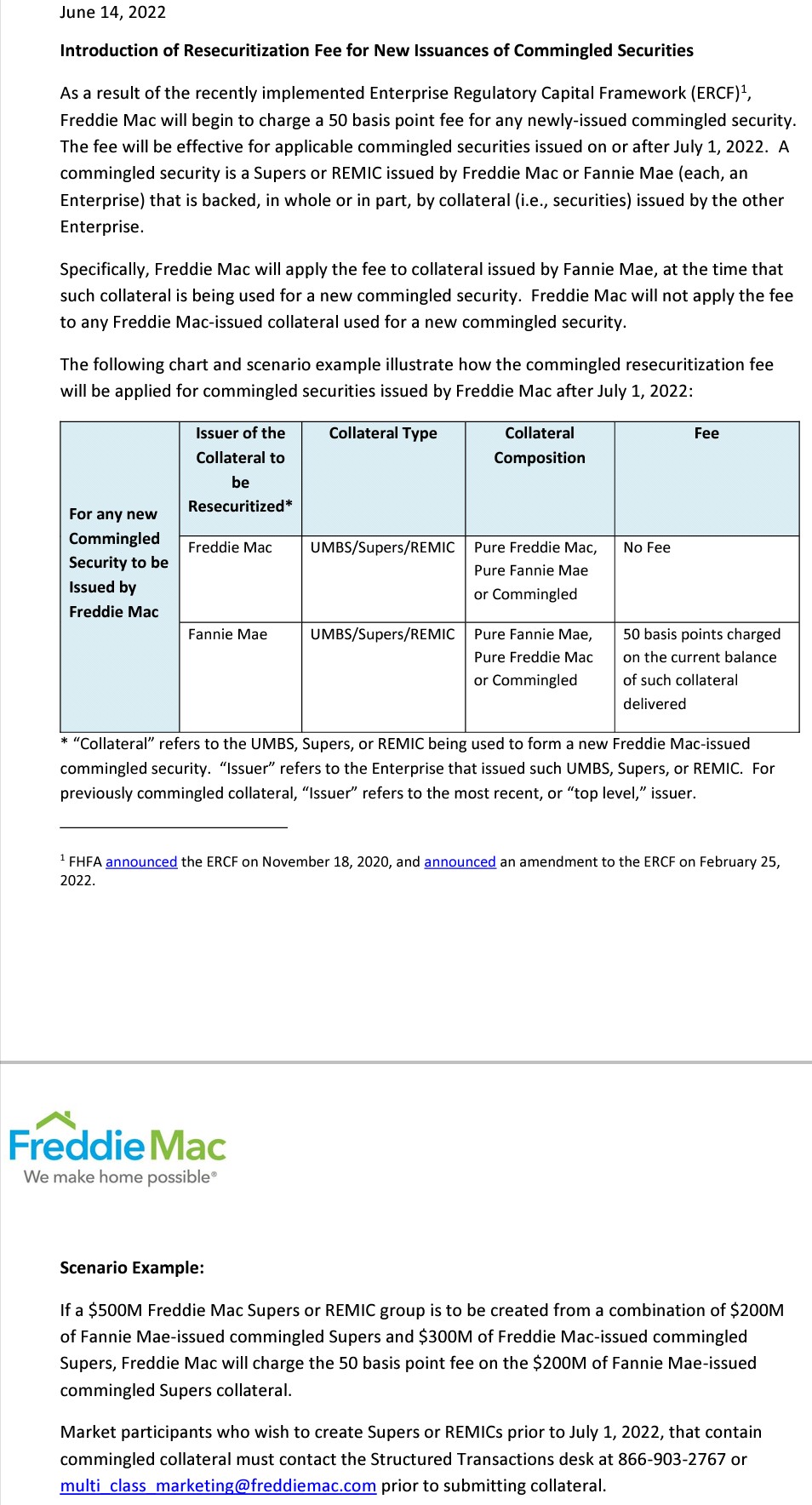

Then, the CSP, UMBS, pilot programs with the States' HFAs, the February 16, 2021 Capital Rule that adopted the Basel Framework (international standard for fully private financial institutions), Freddie Mac unveiled the Resecuritizations on June 2022, a security that would enable the option 3 with a Govt Catastrophic-Loss reinsurance, but it could also be private reinsurance for the options 1 and 2, etc. It was first priced at 50 bps, but soon after it was rectified to the current 9.375 bps.

The first one that wanted to override this mandate by law was Trump, who used a Presidential Memorandum to give it some sort of legality, to request to the Secretary of the Treasury a Housing Reform plan.

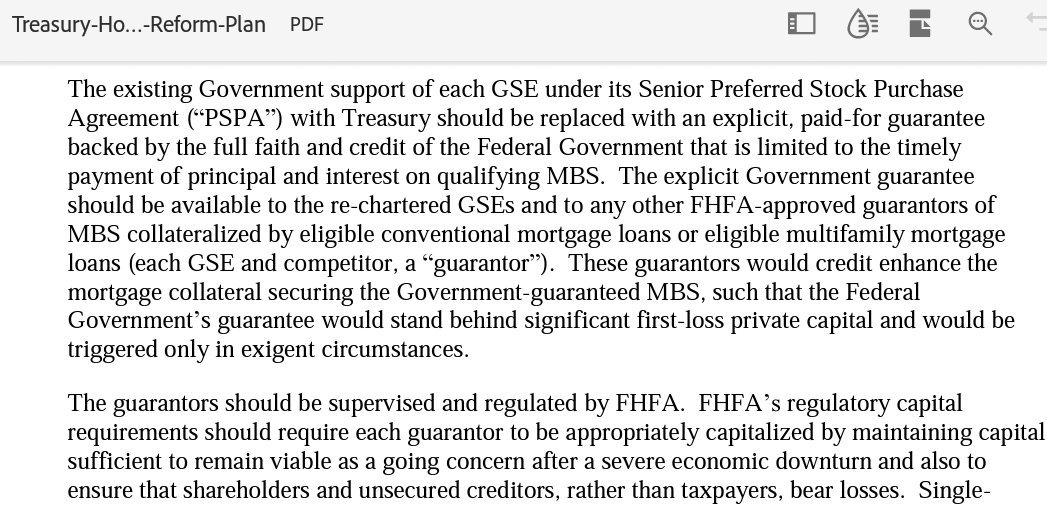

In this Housing Reform plan of September 2019, the Treasury Department of Goldman Sachs' Mnuchin proposed the China-sponsored Govt Explicit Guarantee on MBSs.

This is why the FHFA first priced the Resecuritizations at 50 bps, thinking of China, but then, with 9.375 bps, it allows a Privatized Housing Finance System, because a Govt Catastrophic-Loss reinsurance is triggered only when the guarantor files for bankruptcy. So, the capital level in the guarantor is the "first-loss" protection.

Now, representative Andrew Ogles, once FnF are on the finish line (Fannie Mae was lagging with $1B Tier 1 Capital shortfall over Leverage Capital requirement on June 2023, under the scenario of redemption of JPS) comes up with the same requirement of recommendations on ending the conservatorship that Goldman Sachs' Mnuchin required in an amendment of the SPSPA, in an attempt to substitute the actual mandate in the Dodd-Frank law, but, instead of requiring it pursuant to a Presidential Memorandum, now representative Ogles requires it by law, so a report has to be submitted to Congress.

This SPSPA amendment of January 14, 2021, was signed 12 days before Secretary Yellen was sworn in. Mnuchin and Calabria were in a hurry to amend it, thinking that they are lawmakers sat at a table with the power of amending the Charter and the FHEFSSA through "agreements", rewriting it with whatever they wish for: commitment fees, etc. or even made-up financial concepts like "Capital Reserve End Date", when the Capital Reserve meets the capital requirements, instead of the capital metrics: core capital, Tier 1 Capital, Total Captial or CET1, as per Basel framework that sets the international financial standards.

Let alone that what they call "Capital Reserve", is the $111B SPS absent from the Balance Sheet (once they are recorded, the offset reduces the Retained Earnings just built, leaving only the SPS on the current $111B Net Worth). What lies behind is that they want to meet the capital levels building SPS.

This is why the Mnuchin's Treasury recommended to Congress in its Housing Reform Plan to repeal the FHEFSSA definitions, like the one that states that the core capital is the one that meets the Minimum Leverage Capital requirement for the capital classification of Undercapitalized. They don't want you to know that the current adjusted Core Capital stands at $-194 billion together (resulting in a $400B capital shortfall over Leverage capital requirement) and they rather choose their made-up "Capital Reserve" to meet the Leverage capital requirement. The definitions of financial concepts bother to the investment banks for their Rule of Plunder.

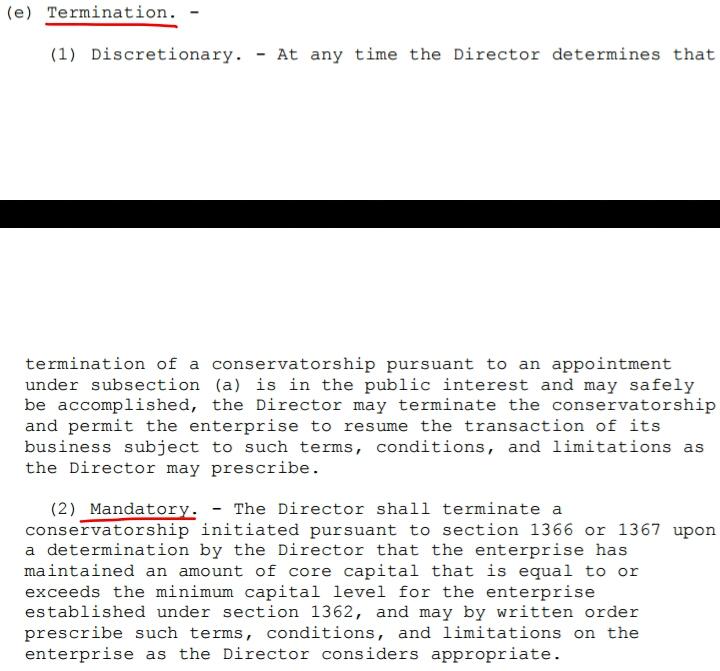

For the exact endpoint of conservatorship, knowing that it's a Privatized Housing Finance System and Basel framework, evidently it should be mandatory upon FnF become Undercapitalized again, which makes them Adequately Capitalized at the same time, as its threshold is lower, or it could be well before at the discretion of the FHFA Director with a Capital Restoration Plan, which hasn't been the option chosen because, as stated before, FnF have gone all the way through meeting the mandatory release Undercapitalized under the Separate Account plan.

Both endpoints were established in the FHEFSSA before being struck by HERA.

Fanniegate is all about coverups and attempts to substitute the law in force and financial concepts.

Notice that this copycat report about recommendations on ending the conservatorships requested in the Mnuchin's PA amendment, was also requested to Secretary Yellen in a House Financial Services Committee hearing by representative Warren Davidson a few months ago.

So, now representative Andrew Ogles wants this requirement in the PA by Goldman Sachs' Mnuchin, to rank equally to the real mandate by law in 2011.

The reality is that it's an attempt to substitute it, when they spotted that the endpoint is in the making according to the law (the rehabilitation of FnF, as stated by Justice Alito and judge Willett)

Simple Stock Loans Announces Unique Solutions For Investors Looking for Alternative Liquidity Amidst Recent Small Cap Rally Sep 6, 2024 9:30 AM

Reliant Coffee Debuts at #271 on the Inc. 5000 List of Fastest Growing Companies - Coffee Service Industry Disruptor Brews Up Exponential Growth Sep 5, 2024 11:51 AM

VAYK Confirms Receiving Revenue from First Airbnb Property with 1.4 Million Annual Revenue Goal • VAYK • Sep 4, 2024 9:34 AM

Mawson Finland Limited Expands Known Mineralized Zones at Rajapalot: New Lens Intercepts 21.75 m at 5.25 g/t Gold & 515 ppm Cobalt • MFL • Sep 4, 2024 9:02 AM

Integrated Ventures Acquires 51% Stake In GetTrim.Com (TM), Telemedicine Platform With Focus On Expansion Into Booming GLP-1 Powered Weight Loss Market • INTV • Sep 4, 2024 8:45 AM

Avant Technologies Announces Strategic Review Process Intended to Maximize Shareholder Value • AVAI • Sep 4, 2024 8:00 AM