That is exactly the point of the Value Proposition.

If this sp can go to several dollars then what is the issue with waiting for more substantial potential validation and jumping in at .50 and gaining a safer multibagger? Waiting for lower risk to still obtain great gains seems like the better route.

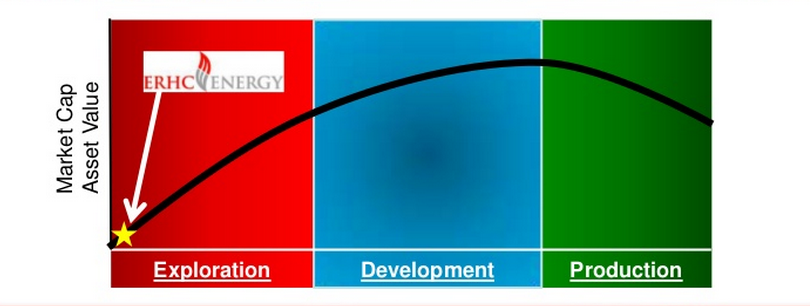

ERHE is not a "safer multibagger" at a higher shareprice. ERHE is actually higher risk when it has good drilling prospects and a higher share price valuation, not lower risk. Without finding oil, we saw exactly what happened to the share price when ERHE had good seismic studies, was near drilling and at a share price of .50 - .90 cents.

Those pre-drill highs were the highest risk bet, not the lowest risk. True for all exploration stage oil companies with limited drilling assets. That bet could have won big, and still could, but there was about a 10% chance of a commercial oil discovery in the JDZ. (Actually a zero % chance as there was no oil in the targets) Yet the bet from .10 to .90 was a repeat winner. Several 5 and 10 baggers, on an almost annual basis buying around this time of year.

The lower risk bet is the exploration run-up, from .10 to .50 or .90 is a 500% to 900% gain, and no oil discovery is needed. Many past examples, again, nearly annually. Alternatively, an increase from .50 to $2.5 likely requires a commercial oil discovery. (Although it can also come from a buy-out or multiple simultaneous explorations)

ERHE has run-up several times, 500% and 900% above the current share price based upon just the exploration stage. The mistake was thinking that it was reduced risk at .50 to .90 cents because the excitement and the targets were defined. Rather it was the run-up to the .90 cents from .10 that was the better, and lower risk bet.

There is no guarantee that this will occur again, I agree, and no guarantee that this is the lowest share price. Rather the share price is in what has historically been the Buy Zone during the period that 12 out of 12 years has had the annual low.

No guarantee of a repeat, but that is a pretty compelling pattern and record.

Only two of those years requires a smaller profit, or a wait, or double down if the targets are large. I plan to do an example spreadsheet on this.

The condition for another exploration phase run-up is now at exactly the early stage, asset acquisition and pre-exploration that have occurred in the past with ERHE.

But with Chad, and Kenya, and the EEZ, there are now multiple potential catalysts. Not just the one ultra-deepwater one which was also one of the first ultra-deepwater drills in the the Gulf of Guinea. Very slow and very high risk frontier geology!

But I absolutely agree we don't see much volume at the best buy zone around the annual lows when the risk is lowest, we see most of it when the share price is much higher, and the risk is the highest.

More investors will take the bet you are talking about. But understand that it is actually the higher risk bet. The science and actual statistics of exploration results is on my side. The prettiest seismic pictures in the world won't magically turn a gas or water deposit into oil. Nor does super high confidence by shareholders at that point lead to discoveries when the odds favour dry holes.

It is not understanding this that leads to disappointed shareholders. It is time for the ERHE longtimers to learn from experience IMO, and take some well earned profits when the herd of new investors comes stampeding in when all the pretty pictures are in pre-drill and both risk and the share price is at its highest.

Alternatively, sure there's lots of other stocks to choose from, but few with a repetitive history of 5 and 10 baggers off of the current share price, and with exactly the catalysts coming which has caused those big wins in the past.

Market Data

Market Data  Markets

Markets