From the 9-8-16/PR-CC, Q2(10-31-16) Revs coming Monday will "be in excess of $20mm". Peregrine's Op.Cash.Burn for Q1(7-31-16) was $9.6mm (vs. Net Loss of $12.4mm) - see http://tinyurl.com/jydtkoy . With Avid's GP% running around 47% and depending on how much "in excess" of $20mm revs are, it'll be interesting how close we come to Positive Cash Burn for Q2. We'll find out Monday around 4:30pm!

Updated PPHM REVS-BY-QTR TABLE, now thru FY17'Q1(qe 7-31-16), per the 7-31-16 10-Q ( http://tinyurl.com/jmy77g3 ) issued 9-8-16.

• Total Revs since May’06: ($179.2mm/Avid + $24.1mm/Govt + $2.5mm/Lic.) = $205.8mm

• 9-8-16: FY'17 (May'16-Apr'17) Avid revs guidance $50-55mm (Committed B/L=$71mm).

• Deferred-Revs at 7-31-16 total $21.5mm, UP from $10.0mm at 4-30-16.

• Cust.Deposits at 7-31-16 total $21.7mm, DOWN from $24.2mm at 4-30-16.

• Inventories at 7-31-16 total $25.3mm, UP from $16.2mm at 4-30-16.

• Avid’s Gross-Profit over last 4 qtrs: $19.2mm on revs of $40.6mm (GP%=47%)

• Recall, Avid Rev$ from Gov’t DTRA Contract work (6/30/08 – 4/15/11, totaling $24.15mm), went into GOVT-REVS, not AVID-REVS, in the Financials.

Avid’s website: http://www.avidbio.com

AVID PROFITABILITY (GROSS*) BY QTR:

QTR Avid-Rev$ CostofMfg$ Gross-Profit$ GP%

FY15Q4 4-30-15 9,308,000 4,758,000 4,550,000 49%

FY16Q1 7-31-15 9,379,000 4,608,000 4,771,000 51%

FY16Q2 10-31-15 9,523,000 4,741,000 4,782,000 50%

FY16Q3 1-31-16 6,672,000 3,896,000 2,776,000 42%

FY16Q4 4-30-16 18,783,000 9,721,000 9,062,000 48%

FY17Q1 7-31-16 5,609,000 3,062,000 2,547,000 45% <=low due to 3rd-party testing delays.

FY17Q2 10-31-16 “we remain on track to gen. revs in excess of $20mm in Q2.” <=to report 12-12-16.

9-8-16 CC/Q&A, CFO Paul Lytle:

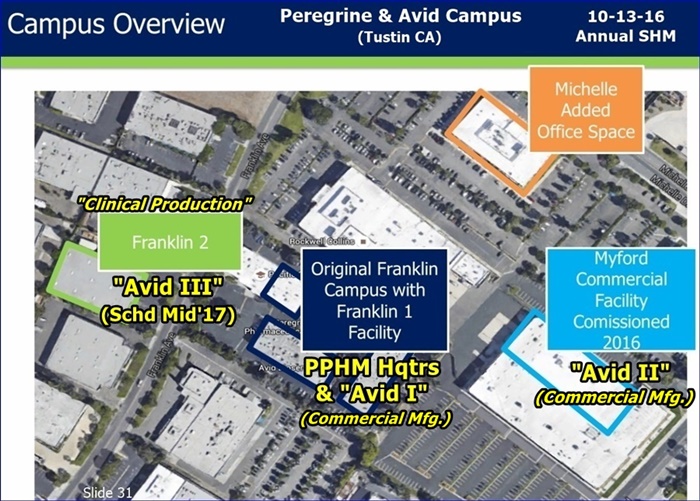

“We recognized $44mm in revenues during FY16 (fye 4-30-16) and that all came from our original Franklin facility. In March this year, we commissioned our new Myford facility, which is built for late stage Phase III clinical & commercial production. We are currently going through the motions of multiple process validation runs and those runs right now are built into our financial projections of the $50-55mm, with our goal of turning those process validation runs, which is the final step before submitting something to the FDA under preapproval inspection in terms of producing commercial quantities for those clients. So this year is really a building year in terms of building those process validation runs for our clients, and then we’re hopeful that those will turn into commercial supply needs in future FY’s.” http://tinyurl.com/jydtkoy

...Avid II (Myford) revenues were coming in as of 9-8-16, albeit via “mult. process validation runs” for clientS (<=note plural per PL). We don’t know when the FDA allows those to turn into Commercial Runs, but the trendline on Avid II revenue contributions to total Avid revenues is clearly UP – they’ve told us “up to $40mm per year” when Avid II is really humming.

Market Data

Market Data  Markets

Markets