| Followers | 843 |

| Posts | 122982 |

| Boards Moderated | 9 |

| Alias Born | 09/05/2002 |

Saturday, February 18, 2012 11:47:45 AM

CLF Reports 4Q11 Results

[Since CLF pre-announced its 4Q11 results on 1/26/12 (#msg-71437952), the PR below from 2/15/12 was anticlimactic. GAAP EPS was $1.30 (including a non-cash asset-impairment charge) for 4Q11 and a record $11.48 (!) for the full year 2011. CLF re-iterated the 2012 outlook given in the 1/26/12 PR; although CLF’s guidance excludes EPS, it includes enough detail for investors to produce a good EPS estimate based on an investor’s expectations for iron-ore prices. CLF expects China’s 2012 steelmaking output to be 730M tonnes, a 7% increase from 2011.

I commented in #msg-72282431 on the ballooning cost estimates for CLF’s chromite assets in Ontario.]

http://finance.yahoo.com/news/Cliffs-Natural-Resources-Inc-prnews-474293466.html?x=0

›15-Feb-2012 4:30pm CLEVELAND, Feb. 15, 2012 /PRNewswire/ --

• Full-Year Revenues Hit a Record $6.8 Billion, with Net Income Attributable to Cliffs' Shareholders Increasing 59% to a Record $1.6 Billion, or $11.48 Per Diluted Share

• 2011 Cash from Operations Reaches Record $2.3 Billion

• Global Iron Ore Sales Volume Reaches 40 Million Tons

Cliffs Natural Resources Inc. (NYSE: CLF) today reported fourth-quarter and full-year results for the period ended Dec. 31, 2011. Record full-year revenues of $6.8 billion increased $2.1 billion, or over 45%, from the previous year. Full-year operating income increased to $2.3 billion, up 85% from $1.3 billion in 2010. Net income attributed to Cliffs' shareholders was $1.6 billion, or $11.48 per diluted share, up from $1 billion, or $7.49 per diluted share, in the prior year.

Joseph Carrabba, Cliffs' chairman, president and chief executive officer, said, "Cliffs delivered an exceptional performance in 2011, a year highlighted with the transformational acquisition of Consolidated Thompson. With a significant organic pipeline of growth in both iron ore and metallurgical coal, Cliffs is well positioned for continued momentum in 2012 and beyond."

2011 Highlights

In addition to achieving record-breaking financial results, Cliffs accomplished several milestones, enhancing the Company's growth profile and increasing financial flexibility. These included:

• Completing the C$4.9 billion (including net debt) acquisition of Consolidated Thompson, an emerging world-class iron ore producer in Eastern Canada, along with implementing the long-term capital structure to finance the deal;

• Increasing the quarterly cash dividend rate by 100%;

• The addition of Cliffs Natural Resources to the Fortune 500 listing;

• Being ranked No. 7 on the 2011 Barron's 500 America's Top Companies List;

• Advancing its safety program "Road to Zero" by reducing year-over-year injury rates across the organization by 15%; and

• Executing a global reorganization, by realigning management responsibilities for worldwide production and commercial sales.

Fourth-Quarter Consolidated Results

Consolidated fourth-quarter revenues were $1.7 billion, a 17% increase compared with $1.4 billion in the same quarter last year. The improvement was driven by higher sales volumes and increased exposure to seaborne market pricing. Consolidated sales margin increased slightly to $496 million, from $483 million in the same period of 2010. During the fourth quarter of 2011, the Company incurred higher cost of goods sold driven by the increased sales volumes, along with higher stripping, labor and electricity costs in certain business segments.

In the fourth quarter, Cliffs' consolidated operating income decreased to $370 million, from nearly $400 million in the prior year's comparable quarter. This was driven by the relatively flat sales margin indicated above, and the previously disclosed $28 million pre-tax goodwill impairment charge related to the coal operations that Cliffs acquired from INR Energy in 2010.

Fourth-quarter 2011 net income attributable to Cliffs' shareholders decreased 52% to $185 million, or $1.30 per diluted share, from $384 million, or $2.82 per diluted share, in the fourth quarter of 2010.

* Excludes revenues and expenses related to freight, which are offsetting and have no impact on sales margin.

** Cash cost per ton is defined as cost of goods sold and operating expenses per ton less depreciation, depletion and amortization per ton.

Fourth-quarter 2011 U.S. Iron Ore pellet sales volume was 7.8 million tons, a 20% increase from the 6.5 million tons sold in the fourth quarter of 2010. The increase was primarily attributed to stronger demand for iron ore pellets driven by slightly higher North American steel industry capacity utilization of approximately 74%, compared to 69% in the fourth quarter of 2010.

U.S. Iron Ore fourth-quarter 2011 revenues per ton increased over 20% to $120.37, compared with $99.46 during the fourth quarter of 2010. The increase was due to stronger year-over-year iron ore pricing driven by pricing mechanisms contained in certain supply contracts that provide increased exposure to more favorable seaborne market pricing. Last year, Cliffs sold more volume under supply agreements containing formula-based pricing mechanisms that have less exposure to seaborne iron ore pricing. The impact of this was offset by sales mix shifts and, to a lesser extent, retroactive provisional pricing adjustments recorded during the fourth quarter of 2011.

Cash cost per ton in U.S. Iron Ore was $66.34, up 12% from $59.27 in the year-ago quarter. The increase was driven primarily by higher supply and maintenance spending, electricity rates and stripping activity.

*Cash cost per ton is defined as cost of goods sold and operating expenses per ton less inventory step-up costs, purchase price adjustments, and depreciation, depletion and amortization per ton.

Fourth-quarter 2011 Eastern Canadian Iron Ore sales volume was 1.9 million tons, a 70% increase from the 1.1 million tons sold in the fourth quarter of 2010. The increase was primarily driven by approximately 1.2 million tons of incremental iron ore concentrate sales volume from the Bloom Lake Mine. Offsetting the incremental sales from Bloom Lake were decreased year-over-year production and sales from Wabush Mine. This was attributed to a number of crusher, dryer and other equipment outages that resulted in lack of pellet availability.

Eastern Canadian Iron Ore fourth-quarter 2011 revenues per ton were $123.83, down 18% from $151.52 in the prior year's fourth quarter. The revenue-per-ton decrease was driven by product mix and lower sales rate premiums for pellet products versus the prior year's comparable quarter. Fourth-quarter 2011 sales mix was comprised of approximately 60% iron ore concentrate sales from Bloom Lake Mine versus last year's fourth quarter, which was comprised exclusively of a premium pellet product.

Cash cost per ton in Eastern Canadian Iron Ore was $102.41, up 9% from $94.29 in the year-ago quarter. The increase was primarily driven by the production challenges at Wabush Mine noted above, which led to lower fixed-cost leverage and approximately $9 per ton of unplanned maintenance and repair spending. Offsetting this was lower cash costs from Bloom Lake Mine of $75 per ton during the fourth quarter of 2011, including an estimated $8 per ton unfavorable impact from Cliffs' decreased production at Bloom Lake Mine to adjust for the mine's fourth-quarter shipping schedule.

* Cash cost per metric ton is defined as cost of goods sold and operating expenses per less inventory step-up costs, purchase price adjustments, and depreciation, depletion and amortization per ton.

Fourth-quarter 2011 Asia Pacific Iron Ore sales volume decreased 31% to 1.8 million tons, compared with the prior-year quarter. The decrease was due to the combination of a planned shutdown at the port related to its expansion project, weather-related timing of two shipments and, to a lesser extent, industrial action within the logistics network in Western Australia.

Revenue per ton for the fourth quarter of 2011 decreased slightly to $130.18 from $135.42 in last year's fourth quarter. This was driven by weaker year-over-year pricing for seaborne iron ore, as average spot pricing for 62% iron ore (C.F.R. China) was 11% lower during the fourth quarter of 2011 than the prior year's comparable average.

Asia Pacific Iron Ore's fourth-quarter cash cost per ton increased 34% to $69.22 from $51.75 in last year's fourth quarter. The increase was primarily due to lower fixed-cost leverage, higher mining costs and unfavorable foreign exchange rates compared with the year-ago quarter.

* Excludes revenues and expenses related to freight, which are offsetting and have no impact on sales margin.

** Cash cost per ton is defined as cost of goods sold and operating expenses per ton less depreciation, depletion and amortization and other non-cash expenses per ton.

*** Depreciation, depletion and amortization for 2010 includes certain non-cash acquisition-related costs.

For the fourth quarter of 2011, North American Coal sales volume was 988,000 tons, slightly higher than the 928,000 tons sold in the prior year's comparable quarter. The increase was driven by significantly higher sales and production volumes from Pinnacle Mine. Slightly offsetting this was lower year-over-year sales volume from Oak Grove Mine due to severe weather that damaged the above-ground operations during 2011. Underground mining operations continued during the quarter, resulting in the Company stockpiling 1.9 million tons of raw coal (or 740,000 tons of clean coal equivalent) at quarter end.

North American Coal's fourth-quarter 2011 revenue per ton increased 11% to $125.10, compared with $112.50 in the fourth quarter of 2010. The increase in revenue per ton was due to a higher proportion of sales of low-volatile metallurgical coal products versus 2010's comparable quarter.

Cash cost per ton decreased 17% to $98.38 from $118.00 in the comparable quarter last year. This decrease was primarily attributed to the significantly lower cash costs per ton of $94 achieved at Pinnacle Mine during the quarter driven largely by higher production in the fourth quarter of 2011.

Sonoma Coal and Amapa

In the fourth quarter of 2011, Cliffs' share of sales volume for its 45% economic interest in Sonoma Coal was 360,000 tons. Revenues and sales margin generated for Cliffs were $58.9 million and $16.3 million, respectively. Revenue per ton at Sonoma was $163.78, with cash costs of $80.80 per ton.

Cliffs has a 30% ownership interest in Amapa, an iron ore operation in Brazil. During the fourth quarter of 2011, Amapa produced approximately 1.3 million tons and earned equity income of $9.6 million for Cliffs' share of the operation.

Capital Structure, Cash Flow and Liquidity

At Dec. 31, 2011, Cliffs had $522 million of cash and cash equivalents. During the quarter, Cliffs repurchased the one million shares remaining under the authorized share repurchase plan approved by Cliffs' Board of Directors in August 2011. At year end, Cliffs had acquired a total of four million shares at an average weighted cost of $72 per share and a total investment of approximately $290 million.

At Dec. 31, 2011, the Company had $3.6 billion in long-term debt and no borrowings drawn on its $1.75 billion revolving credit facility. For full-year 2011, Cliffs reported depreciation, depletion and amortization of $427 million and generated a record-breaking $2.3 billion in cash from operations.

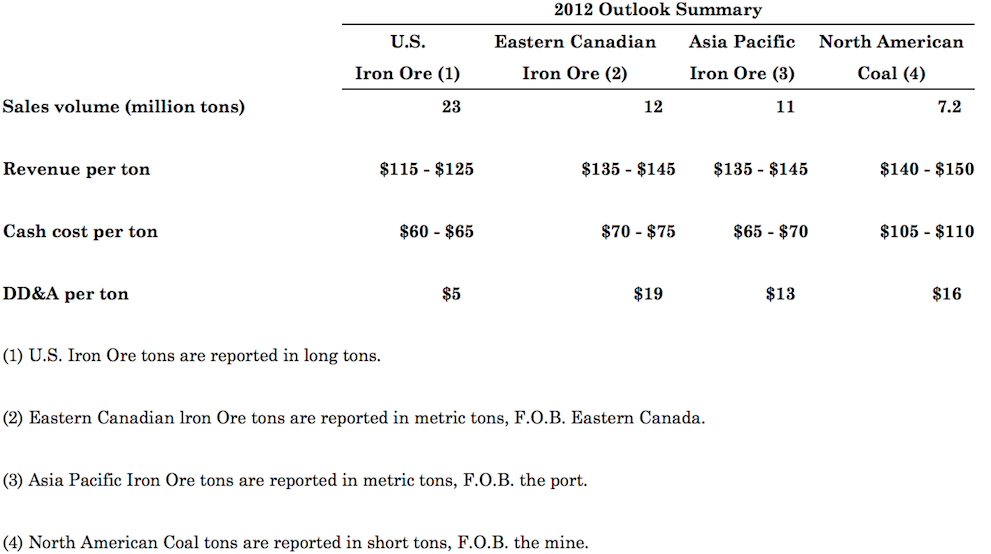

Outlook

Cliffs is maintaining its 2012 business segment outlook, which was previously disclosed on Jan. 26, 2012. Assumptions in this outlook include an average 2012 spot price for 62% Fe seaborne iron ore of approximately $150 per ton (C.F.R. China).

The table below summarizes the 2012 outlook by business segment.

Outlook for Sonoma Coal and Amapa (Metric tons, F.O.B. the port)

Cliffs has a 45% economic interest in Sonoma Coal. For 2012, the Company is maintaining its equity sales and production volume expectations of approximately 1.6 million tons. The approximate product mix is expected to be two-thirds thermal coal and one-third metallurgical coal. Cash cost per ton is expected to be approximately $110. For 2012, depreciation, depletion and amortization is expected to be approximately $14 per ton.

Cliffs expects Amapa to contribute over $30 million in equity income in 2012.

SG&A Expenses & Other Expectations

Cliffs' full-year 2012 SG&A expense expectation is approximately $325 million. The year-over-year increase in SG&A expense is primarily driven by an increase in growth-related corporate projects.

The Company expects to incur cash outflows of approximately $165 million to support future growth, comprised of approximately $90 million related to exploration and drilling programs and approximately $75 million related to its chromite project in Ontario, Canada.

For 2012, Cliffs anticipates a full-year effective tax rate of approximately 25%. In addition, Cliffs expects its full-year 2012 depreciation, depletion and amortization to be approximately $620 million.

2012 Capital Budget Update and Other Uses of Cash

For 2012, based on the Company's outlook, Cliffs anticipates generating cash flow from operations of approximately $1.9 billion.

Cliffs is also maintaining its previously disclosed 2012 capital expenditures budget of approximately $1 billion, comprised of approximately $300 million in sustaining capital and $700 million in growth and productivity-improvement capital.‹

[Since CLF pre-announced its 4Q11 results on 1/26/12 (#msg-71437952), the PR below from 2/15/12 was anticlimactic. GAAP EPS was $1.30 (including a non-cash asset-impairment charge) for 4Q11 and a record $11.48 (!) for the full year 2011. CLF re-iterated the 2012 outlook given in the 1/26/12 PR; although CLF’s guidance excludes EPS, it includes enough detail for investors to produce a good EPS estimate based on an investor’s expectations for iron-ore prices. CLF expects China’s 2012 steelmaking output to be 730M tonnes, a 7% increase from 2011.

I commented in #msg-72282431 on the ballooning cost estimates for CLF’s chromite assets in Ontario.]

http://finance.yahoo.com/news/Cliffs-Natural-Resources-Inc-prnews-474293466.html?x=0

›15-Feb-2012 4:30pm CLEVELAND, Feb. 15, 2012 /PRNewswire/ --

• Full-Year Revenues Hit a Record $6.8 Billion, with Net Income Attributable to Cliffs' Shareholders Increasing 59% to a Record $1.6 Billion, or $11.48 Per Diluted Share

• 2011 Cash from Operations Reaches Record $2.3 Billion

• Global Iron Ore Sales Volume Reaches 40 Million Tons

Cliffs Natural Resources Inc. (NYSE: CLF) today reported fourth-quarter and full-year results for the period ended Dec. 31, 2011. Record full-year revenues of $6.8 billion increased $2.1 billion, or over 45%, from the previous year. Full-year operating income increased to $2.3 billion, up 85% from $1.3 billion in 2010. Net income attributed to Cliffs' shareholders was $1.6 billion, or $11.48 per diluted share, up from $1 billion, or $7.49 per diluted share, in the prior year.

Joseph Carrabba, Cliffs' chairman, president and chief executive officer, said, "Cliffs delivered an exceptional performance in 2011, a year highlighted with the transformational acquisition of Consolidated Thompson. With a significant organic pipeline of growth in both iron ore and metallurgical coal, Cliffs is well positioned for continued momentum in 2012 and beyond."

2011 Highlights

In addition to achieving record-breaking financial results, Cliffs accomplished several milestones, enhancing the Company's growth profile and increasing financial flexibility. These included:

• Completing the C$4.9 billion (including net debt) acquisition of Consolidated Thompson, an emerging world-class iron ore producer in Eastern Canada, along with implementing the long-term capital structure to finance the deal;

• Increasing the quarterly cash dividend rate by 100%;

• The addition of Cliffs Natural Resources to the Fortune 500 listing;

• Being ranked No. 7 on the 2011 Barron's 500 America's Top Companies List;

• Advancing its safety program "Road to Zero" by reducing year-over-year injury rates across the organization by 15%; and

• Executing a global reorganization, by realigning management responsibilities for worldwide production and commercial sales.

Fourth-Quarter Consolidated Results

Consolidated fourth-quarter revenues were $1.7 billion, a 17% increase compared with $1.4 billion in the same quarter last year. The improvement was driven by higher sales volumes and increased exposure to seaborne market pricing. Consolidated sales margin increased slightly to $496 million, from $483 million in the same period of 2010. During the fourth quarter of 2011, the Company incurred higher cost of goods sold driven by the increased sales volumes, along with higher stripping, labor and electricity costs in certain business segments.

In the fourth quarter, Cliffs' consolidated operating income decreased to $370 million, from nearly $400 million in the prior year's comparable quarter. This was driven by the relatively flat sales margin indicated above, and the previously disclosed $28 million pre-tax goodwill impairment charge related to the coal operations that Cliffs acquired from INR Energy in 2010.

Fourth-quarter 2011 net income attributable to Cliffs' shareholders decreased 52% to $185 million, or $1.30 per diluted share, from $384 million, or $2.82 per diluted share, in the fourth quarter of 2010.

* Excludes revenues and expenses related to freight, which are offsetting and have no impact on sales margin.

** Cash cost per ton is defined as cost of goods sold and operating expenses per ton less depreciation, depletion and amortization per ton.

Fourth-quarter 2011 U.S. Iron Ore pellet sales volume was 7.8 million tons, a 20% increase from the 6.5 million tons sold in the fourth quarter of 2010. The increase was primarily attributed to stronger demand for iron ore pellets driven by slightly higher North American steel industry capacity utilization of approximately 74%, compared to 69% in the fourth quarter of 2010.

U.S. Iron Ore fourth-quarter 2011 revenues per ton increased over 20% to $120.37, compared with $99.46 during the fourth quarter of 2010. The increase was due to stronger year-over-year iron ore pricing driven by pricing mechanisms contained in certain supply contracts that provide increased exposure to more favorable seaborne market pricing. Last year, Cliffs sold more volume under supply agreements containing formula-based pricing mechanisms that have less exposure to seaborne iron ore pricing. The impact of this was offset by sales mix shifts and, to a lesser extent, retroactive provisional pricing adjustments recorded during the fourth quarter of 2011.

Cash cost per ton in U.S. Iron Ore was $66.34, up 12% from $59.27 in the year-ago quarter. The increase was driven primarily by higher supply and maintenance spending, electricity rates and stripping activity.

*Cash cost per ton is defined as cost of goods sold and operating expenses per ton less inventory step-up costs, purchase price adjustments, and depreciation, depletion and amortization per ton.

Fourth-quarter 2011 Eastern Canadian Iron Ore sales volume was 1.9 million tons, a 70% increase from the 1.1 million tons sold in the fourth quarter of 2010. The increase was primarily driven by approximately 1.2 million tons of incremental iron ore concentrate sales volume from the Bloom Lake Mine. Offsetting the incremental sales from Bloom Lake were decreased year-over-year production and sales from Wabush Mine. This was attributed to a number of crusher, dryer and other equipment outages that resulted in lack of pellet availability.

Eastern Canadian Iron Ore fourth-quarter 2011 revenues per ton were $123.83, down 18% from $151.52 in the prior year's fourth quarter. The revenue-per-ton decrease was driven by product mix and lower sales rate premiums for pellet products versus the prior year's comparable quarter. Fourth-quarter 2011 sales mix was comprised of approximately 60% iron ore concentrate sales from Bloom Lake Mine versus last year's fourth quarter, which was comprised exclusively of a premium pellet product.

Cash cost per ton in Eastern Canadian Iron Ore was $102.41, up 9% from $94.29 in the year-ago quarter. The increase was primarily driven by the production challenges at Wabush Mine noted above, which led to lower fixed-cost leverage and approximately $9 per ton of unplanned maintenance and repair spending. Offsetting this was lower cash costs from Bloom Lake Mine of $75 per ton during the fourth quarter of 2011, including an estimated $8 per ton unfavorable impact from Cliffs' decreased production at Bloom Lake Mine to adjust for the mine's fourth-quarter shipping schedule.

* Cash cost per metric ton is defined as cost of goods sold and operating expenses per less inventory step-up costs, purchase price adjustments, and depreciation, depletion and amortization per ton.

Fourth-quarter 2011 Asia Pacific Iron Ore sales volume decreased 31% to 1.8 million tons, compared with the prior-year quarter. The decrease was due to the combination of a planned shutdown at the port related to its expansion project, weather-related timing of two shipments and, to a lesser extent, industrial action within the logistics network in Western Australia.

Revenue per ton for the fourth quarter of 2011 decreased slightly to $130.18 from $135.42 in last year's fourth quarter. This was driven by weaker year-over-year pricing for seaborne iron ore, as average spot pricing for 62% iron ore (C.F.R. China) was 11% lower during the fourth quarter of 2011 than the prior year's comparable average.

Asia Pacific Iron Ore's fourth-quarter cash cost per ton increased 34% to $69.22 from $51.75 in last year's fourth quarter. The increase was primarily due to lower fixed-cost leverage, higher mining costs and unfavorable foreign exchange rates compared with the year-ago quarter.

* Excludes revenues and expenses related to freight, which are offsetting and have no impact on sales margin.

** Cash cost per ton is defined as cost of goods sold and operating expenses per ton less depreciation, depletion and amortization and other non-cash expenses per ton.

*** Depreciation, depletion and amortization for 2010 includes certain non-cash acquisition-related costs.

For the fourth quarter of 2011, North American Coal sales volume was 988,000 tons, slightly higher than the 928,000 tons sold in the prior year's comparable quarter. The increase was driven by significantly higher sales and production volumes from Pinnacle Mine. Slightly offsetting this was lower year-over-year sales volume from Oak Grove Mine due to severe weather that damaged the above-ground operations during 2011. Underground mining operations continued during the quarter, resulting in the Company stockpiling 1.9 million tons of raw coal (or 740,000 tons of clean coal equivalent) at quarter end.

North American Coal's fourth-quarter 2011 revenue per ton increased 11% to $125.10, compared with $112.50 in the fourth quarter of 2010. The increase in revenue per ton was due to a higher proportion of sales of low-volatile metallurgical coal products versus 2010's comparable quarter.

Cash cost per ton decreased 17% to $98.38 from $118.00 in the comparable quarter last year. This decrease was primarily attributed to the significantly lower cash costs per ton of $94 achieved at Pinnacle Mine during the quarter driven largely by higher production in the fourth quarter of 2011.

Sonoma Coal and Amapa

In the fourth quarter of 2011, Cliffs' share of sales volume for its 45% economic interest in Sonoma Coal was 360,000 tons. Revenues and sales margin generated for Cliffs were $58.9 million and $16.3 million, respectively. Revenue per ton at Sonoma was $163.78, with cash costs of $80.80 per ton.

Cliffs has a 30% ownership interest in Amapa, an iron ore operation in Brazil. During the fourth quarter of 2011, Amapa produced approximately 1.3 million tons and earned equity income of $9.6 million for Cliffs' share of the operation.

Capital Structure, Cash Flow and Liquidity

At Dec. 31, 2011, Cliffs had $522 million of cash and cash equivalents. During the quarter, Cliffs repurchased the one million shares remaining under the authorized share repurchase plan approved by Cliffs' Board of Directors in August 2011. At year end, Cliffs had acquired a total of four million shares at an average weighted cost of $72 per share and a total investment of approximately $290 million.

At Dec. 31, 2011, the Company had $3.6 billion in long-term debt and no borrowings drawn on its $1.75 billion revolving credit facility. For full-year 2011, Cliffs reported depreciation, depletion and amortization of $427 million and generated a record-breaking $2.3 billion in cash from operations.

Outlook

Cliffs is maintaining its 2012 business segment outlook, which was previously disclosed on Jan. 26, 2012. Assumptions in this outlook include an average 2012 spot price for 62% Fe seaborne iron ore of approximately $150 per ton (C.F.R. China).

The table below summarizes the 2012 outlook by business segment.

Outlook for Sonoma Coal and Amapa (Metric tons, F.O.B. the port)

Cliffs has a 45% economic interest in Sonoma Coal. For 2012, the Company is maintaining its equity sales and production volume expectations of approximately 1.6 million tons. The approximate product mix is expected to be two-thirds thermal coal and one-third metallurgical coal. Cash cost per ton is expected to be approximately $110. For 2012, depreciation, depletion and amortization is expected to be approximately $14 per ton.

Cliffs expects Amapa to contribute over $30 million in equity income in 2012.

SG&A Expenses & Other Expectations

Cliffs' full-year 2012 SG&A expense expectation is approximately $325 million. The year-over-year increase in SG&A expense is primarily driven by an increase in growth-related corporate projects.

The Company expects to incur cash outflows of approximately $165 million to support future growth, comprised of approximately $90 million related to exploration and drilling programs and approximately $75 million related to its chromite project in Ontario, Canada.

For 2012, Cliffs anticipates a full-year effective tax rate of approximately 25%. In addition, Cliffs expects its full-year 2012 depreciation, depletion and amortization to be approximately $620 million.

2012 Capital Budget Update and Other Uses of Cash

For 2012, based on the Company's outlook, Cliffs anticipates generating cash flow from operations of approximately $1.9 billion.

Cliffs is also maintaining its previously disclosed 2012 capital expenditures budget of approximately $1 billion, comprised of approximately $300 million in sustaining capital and $700 million in growth and productivity-improvement capital.‹

“The efficient-market hypothesis may be

the foremost piece of B.S. ever promulgated

in any area of human knowledge!”

Discover What Traders Are Watching

Explore small cap ideas before they hit the headlines.