News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

You are a lawyer, pro se plaintiff Joshua Angel.

It seems that you have difficulties in comprehending written texts.

I'm talking about both the interlocutory appeal by Fairholme and the 11-related cases acting in concert, as judge Sweeney stated in her Opinion being appealed (Watch the screenshot in the tweet attached), that was followed up by Fisher's weird motion to certify interlocutory appeal, with 2 questions that were stolen from Fairholme's 6 controlling questions of law in the interlocutory appeal already submitted, and, secondly, the appeal in the Supreme Court to review the prior appeal, submitted by some of the related cases. For instance, Cacciapalle case now in the Lamberth Court too, and Owl Creek case, submitting the same question posted below, and other petitions where individual plaintiffs within a case filed separately (Andrew T. Barrett and Fairholme)

So, 4 petitions in total as far as I'm concerned.

https://www.supremecourt.gov/Search.aspx?FileName=/docket/docketfiles/html/public\22-100.html

https://www.supremecourt.gov/Search.aspx?FileName=/docket/docketfiles/html/public\22-98.html

https://www.supremecourt.gov/Search.aspx?FileName=/docket/docketfiles/html/public\22-97.html

https://www.supremecourt.gov/Search.aspx?FileName=/docket/docketfiles/html/public\22-99.html

All of the above, about a Taking case.

I'm not talking about the appeal in the Supreme Court in the Collins case, years before, that you mention.

Fisher lost his opportunity to file an appeal in the Supreme Court on time, maybe because his questions were already filed by other plaintiffs in related cases. So, he thought that he had lost yet again another opportunity to be in the spotlight and pretend to be a "Fanniegate hero", like our other enemy Glen Bradford that calls himself that.

The reason for the rally on Friday was the mounting evidence of rigged litigation by the parties from the beginning: the JPS holders and the FHFA, with the DOJ in between.

The latest, it's a fact that judge Lamberth required a plan of allocation on December 21st and there's been none.

Now, the plaintiffs' plan of allocation has been postponed until two days before the scheduled appeal by the plaintiff Bryndon Fisher, on January 19, 2024.

Bryndon Fisher intends to appeal in the Federal Circuit the recent Final Judgment by judge Sweeney. But, it turns out, that his case has already been appealed twice before.

First, with the lead plaintiff Fairholme's interlocutory appeal (intermediate) in the Federal Circuit, where Fisher was one of the 11 related cases. Due to his insistence, Fisher filed a motion to certify interlocutory appeal with two of the 6 controlling questions submitted by Fairholme in its appeal "that would also dispose of the Fisher and Reid cases", he claimed.

Fisher was then allowed to file Amicus briefs in the Federal Circuit to be in the spotlight. Now we know why.

Finally, the Fairholme plaintiffs filed an appeal in the Supreme Court separately, to review the Federal Circuit decision. Always about a Taking case. The petitions were denied.

The Fisher case has already been dealt with conclusively (disposed of) or terminated.

The DOJ seeks a declaration of Taking during a Conservatorship of congressionally-chartered private corporations and it has in place numerous tricks. For instance, the poster "Robert from Yahoo bd" on Ihub crying out loud daily that there is been a Nationalization by DeMarco. Breach of implied contract in the Lamberth court. Then, Byndon Fisher in the CFC readies another appeal.

There's been a Separate Account plan in accordance with the law instead.

It seems that the DOJ attorneys have seen the common stock valuation with the adjusted fair values in the different possible scenarios, one of them a Taking but announced today at the adjusted Book Value per stock (the JPS aren't part of a Taking, as they are redeemed by FnF at a fair value of par value), and the fact that the UST and FHFA owe FnF $150.9 billion, plus Punitive Damages for the Equity holders.

FISHER TO APPEAL A FINAL ORDER AFTER INTERLOCUTORY APPEAL(Fed.Cir.)& SCOTUS

— Conservatives against Trump (@CarlosVignote) December 24, 2023

Sweeney only allowed lead plaintiff Fairholme to appeal(+11 related cases)

Fisher,amicus brief.

Besides,his motion to certify interlocutory appeal stole 2 of 6 questions from Fairholme's brief.#Fanniegate https://t.co/ahDVtOyj7c pic.twitter.com/8PQZdzK5Rh

If you are going to spread false rumors, at least write it properly.

Minimum required or limit?

a leak of new GSE Capital Rule limits ?

Boy! Quit saying that there are "regulatory guidelines" prohibiting dividends, pro se plaintiff Joshua Angel.

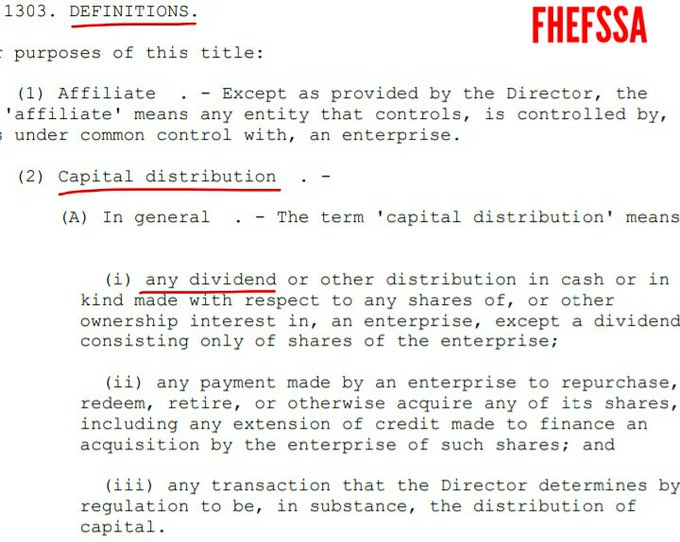

It's a statutory provision in the section "Prompt Corrective Action" of HERA, that inserted it in the FHEFSSA, entitled: Restriction on Capital Distributions, U.S. Code §4614(e):

1- Any dividend and today's SPS LP increased for free.

2- Stock buybacks and redemption of Preferred Stocks.

3- The payment of Securities Litigation judgment in the Lamberth court.

With exceptions: like the reduction of Preferred Stocks (exception B) while increasing capital in the same amount (exception A. With the Net Worth increase, FnF increased the Common Equity in the same amount as the reduction of SPS. Watch the image below) and, in the July 20, 2011 Final Rule (coinciding with the time limitation of the Acting Director DeMarco), a recapitalization in a Separate Account (CFR 1237.12). External Position, a global pandemic.

Fannie Mae and Freddie Mac's regulatory guidelines would have prohibited the companies form paying dividends to the Treasury while severely under-capitalized, but the FHFA suspended those guidelines

No. It states "undercapitalized", not "classified Undercapitalized under its definition in the subsection (a)(2) of this section", in the first sentence of the Restriction on Capital Distributions. U.S. Code §4614(e).

You already said it and I debunked it, but you don't care.

Also, it starts with "IN GENERAL", which reminds me Sandra Thompson in the Congress and the FHFA reports, stating that FnF are undercapitalized, in general as well.

A distribution of capital would also break the FHFA-C's Rehab power ("put FnF in a sound condition"), as Calabria reminded us:

It denotes that you don't know about financial matters. You intend to distribute capital when they are Significantly Undercapitalized or during a Conservatorship for Critically Undercapitalized enterprises.

Zero sense of what a restriction on capital distribution is for: to build capital.

You simply read the sentence unaware of the financial meaning behind. This is why you always use the trick of deleting words to fit your narrative, unaware of the fallout. For instance, shamelessly removing the "authorized by this section" in the FHFA-C's Incidental Power.

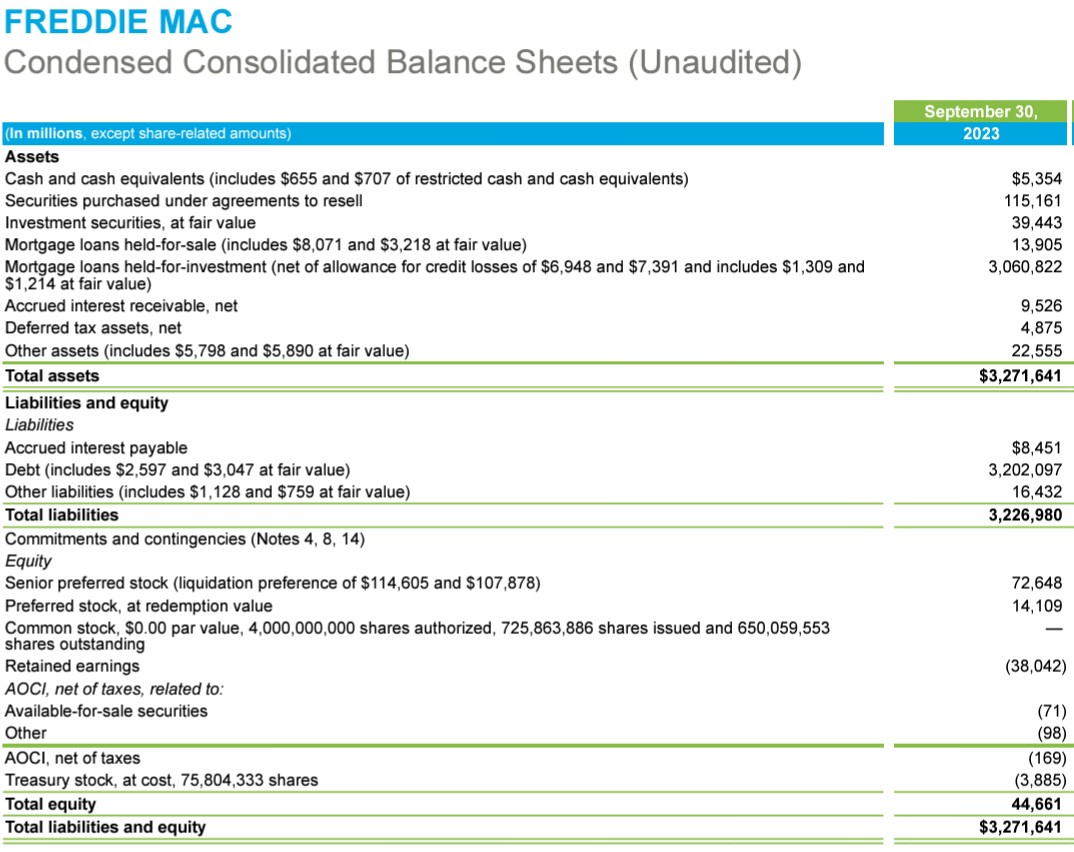

FHFA suspended the Capital Classifications in 2008. Evidence of Separate Account plan from the onset, as not only it's relieved now from having to declare FnF Critically Undercapitalized ($-76 billion Core Capital officially as of Sept 30, 2023; $-194 billion adjusted Core Capital with the offset for the $118 billion SPS LP absent from the Balance Sheets), but also, under the Separate Account plan, having had to change the Capital Classifications each time, first from Critically Undercapitalized to Significantly Undercapitalized, then Undercapitalized, and now Adequately Capitalized.

It would have exposed that the FHFA is now concealing their statutory Critical Capital level in their ERCF tables.

No problem! The Treasury of Mnuchin recommended Congress to repeal the statutory definitions with regard to capital. In the definition of each Capital Classifications, it explains that the capital requirements are met either with core capital or total capital.

They rather make up their own rules, and they intend to meet the capital requirements with the Net Worth. A NW built with the SPS LP increased for free absent from the balance sheets. A fraud that the attorney for Berkowitz, David Thompson, not only defended in court but he also sought a compensation for constitutional damages: the "for cause" removal restriction prevented this Wonderland scenario from happening sooner (Collins case).

Beware of FFFacts. He repeats that this payment of a Securities Litigation claim, isn't a capital distribution.

the definition of a capital distribution does not meet the standard in this type of judgment.

It depends on the stock's fair value at the time.

Or are you going to sell below it?

A fixed-income security without a "coupon payment", trades at a discount to "face value", discounting the time period till "maturity".

In our case, till FnF resume the dividend payments calculated as a percentage of the par value. It's when the fair value fetches the par value.

The resumption of the dividend payments is determined by the Table 8: Payout ratio. So, above the Adequately Capitalized threshold that was before (now, minimum 25% of the Capital Buffer)

It was estimated that Fannie Mae surpassed this threshold with the 3Q 2022 Earnings report, under the Separate Account plan. Freddie Mac, one year earlier.

All the securities have fundamentals, otherwise they have a collateral to back it up. Unbacked crypto like bitcoin, doesn't exist.

The Common Stocks represent a legal claim on future profits after the payment of dividends to JPSs, and also on the Retained Earnings account.

Now, FHFA is withholding the release till CET1 > 2.5% of Adjusted Total Assets, in order to redeem the JPS and later FnF meet the Tier 1 Capital >2.5% of Adjusted Total Assets (ERCF), and meanwhile, try the assault on the FnF ownership (Common Stock) by the SPS and JPS with shenanigans in court. They are annoyed with the Charter Act and a Privatized Housing Finance System revamp, but it's their role.

Blame FHFA and the plaintiffs. Up to two years of delay of stock valuation at par value.

Just because FHFA didn't want "captives" as FnF shareholders, unrelated to Housing Finance. The same occurred with the FHLBanks in a 2016 final rule, where some members were expelled. Proposed Rule in 2010.

It looks like the litigation was rigged by the parties from the onset, to try the shenanigans in court, aiming to change the fate.

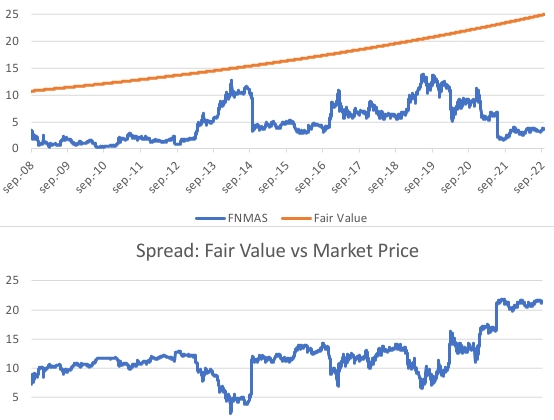

This is the chart of FNMAS with a 6% discount rate.

You sound ridiculous with:

To be quite honest, there's a very good chance I will liquidate a sizable chunk of my position once it gets to 50%+ PAR.

Bombshell! The reason why the Plan of Allocation has been postponed.

The plaintiff Bryndon Fisher is urged to withdraw his appeal with a Taking case.

He works for the DOJ. There has been no Taking. Conservatorship.

If any, a Taking must be properly announced today and our stocks taken over at their adjusted fair value.

The JPS aren't necessary for a Taking (no Voting Rights). So, either they stay in the capital structure or they are redeemed by FnF at their fair value of Redemption value (corporate decision), as they would no longer be necessary as AT1 Capital and Core Capital.

The hedge funds, JPS holders, are annoyed with the stock valuations. Sorry but this what fundamentals is about. Buy bitcoin if you want a scam.

ST BAILS

— Conservatives against Trump (@CarlosVignote) December 22, 2023

It was required a joint/separate Plan of Allocation(PA).Capital distribution.

Switched for ST filing a reply in opposition to PA,postponed after Jan19 @TheJusticeDept's Bryndon Fisher's scheduled appeal,switching Conservatorship for Taking of private property.#Fanniegate https://t.co/27BE0V8WAl pic.twitter.com/Uwe9E1xIzf

Another "overnite Final Order" like the prior Proposed Order?

🤡

HERE is the Final Order Allocation Plan

You conceal that Alito started out with "rehabilitate FnF".

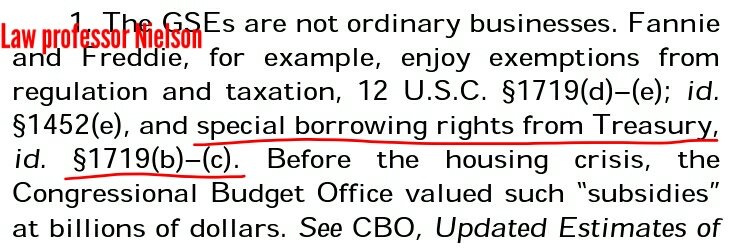

Blowaccount spewing his ignorance. FnF aren't ordinary businesses.

Law professor Nielson, SCOTUS-appointed amicus, who spotted the original UST backup of FnF:

FnF didn't get funds from the TARP fund, but the Charter Act.

UST backup as a last resort, written in the same section where is set forth their Public Mission:

UST backup limited to $2.25B but de facto updated in the 2nd UST backup of FnF in 2008, at an up toa an infinite rate and in an infinite amount, and subsequent amount in the SPSPA fact sheet. Useful for the Separate Account plan through assessments to Treasury under the guise of dividends. The exceptions to the Restriction on Capital Distributions kicked off.

The original rate prevails, estimated in a weighted average 1.8% cumulative dividend rate on SPS. It's netted out with the interests on the $150.9 billion owed to FnF.

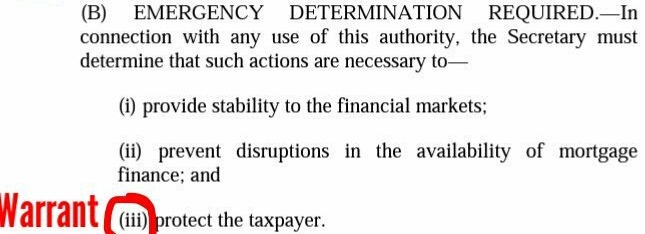

A Warrant, issued for free, authorized only to (iii) protect the taxpayer (collateral). The exercise price of $0.00001ps confirms that it was a collateral.

Although, a collateral is barred in the Fee Limitation clause.

We know that the real reason was the assault attempt on the ownership of FnF by Wall Street and the community banks, in the clause 2.1: Shares assigned to any Person: MS, BLK, etc.

The Warrant is non-transferable (clause 7), but the right to receive the shares can be assigned, mentioned before. It turns out that that right is the Warrant itself, so you are making it transferable and later you claim that it's non-transferable. What it is, is void to begin with. GS's Paulson didn't want to see the Treasury selling 80% of FnF to the bankers at $0.00001ps, and he made the whole thing void.

Blowaccount sounds a lot like Guido, Pagliara's footman, who, in turn, is the Chamber investor for representative Maxine Waters (same slogan recently Guido-MW: "Federal Government conservatorship"), because Guido is the only person in the world that has mentioned that the Warrants have a fair value in the prospectus, mistaking it for what it really states : "Market Fair Value", for a settlement through differences that isn't contemplated in the prospectus. So, a pointless definition of MFV.

Guido has always followed up with a Treasury web site informing of the Treasury warrants and the banks, stating that they were allowed to buy them back.

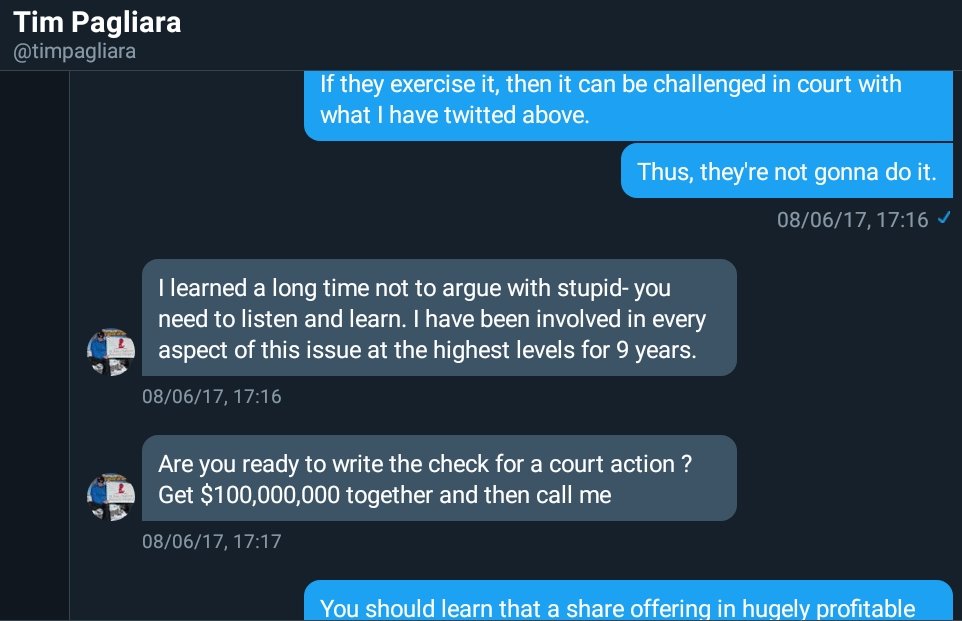

Pagliara, the plotter in chief.

I have been involved in every aspect of this issue at the highest levels for 9 years.

A senior Federal Judge in Washington demanding an alibi, in the case that the co-conspirators (hedge funds and the rogue Federal Agencies FHFA and UST) want him to continue using the U.S. courts for their plan of assault on two congressionally-chartered private corporations and their sacking.

Just when you thought that the Fanniegate scandal can't go lower.

The DOJ shouldn't allow the parties to file the required Plan of Allocation, aka distribution of capital. Restricted.

Bummer!

LAMBERTH SEEKS THE ALIBI "I KNEW NOTHING"

— Conservatives against Trump (@CarlosVignote) December 20, 2023

Allegedly, he learned of a restricted capital distribution in oral motion on V-day→Judgment DEFERRED.

Now, he needs

-ST in the Plan of Allocation.

-"Written" report.

-Here to help "if the parties have concerns"#Fanniegate @TheJusticeDept https://t.co/W6DBER7Plf pic.twitter.com/AMQG64D5Zp

SUMMARY at a glance: Fanniegate scandal/Adjusted Fair Value of the stocks.

EFFICIENT MKTS HYPOTHESIS HAS NOT BEEN SATISFIED

— Conservatives against Trump (@CarlosVignote) December 17, 2023

Mkt Value=Fair Value assuming the stocks discount all available info.

Not in #Fanniegate:

-Fivolous lawsuits concealing statutory provisions & financial concepts

-Unlawful acts: CRT,barred; gifted SPS,absent; W,collateral.

👇hidden https://t.co/mqKqepNE0p pic.twitter.com/CnM4gd82TG

The "restructuring" is called 15-year Conservatorship. Wake up.

Lmfao. They will uplist when they get restructured

BOOM. Judge Lamberth caught preparing his alibi in Fanniegate.

The felony already occurred. Due to his order granting prejudgment interests award, in light of the jury's verdict, FnF have already had to deplete their capital by setting aside a Reserve in "other expenses" in the Q3 Earnings reports, which breaks the Restriction on Capital Distributions and the FHFA-C's Rehab power.

His only defense, like many others, is playing the fool: "I knew nothing".

In his latest court order, not only he compels FHFA's Sandra Thompson to file either a joint plan of allocation or in a separate report, when a Defendant has no say in a plan of allocation, as the Plaintiffs stated in their latest brief, but also the judge seeks to emphasize that the court is here to help:

if the parties have concerns for which they seek resolution by the court,....

the parties shall submit a written report

Are you sure you don't have something else to tell me?

About capital distributions being restricted when FnF are undercapitalized?

Look, you are going to ruin my career and reputation. I need a brief I can use as a certificate that exonerates me. Because I also heard that any dividend and today's SPS LP increased for free, are also capital distributions.

Have you ever heard of a Separate Account? No? Does 1989 FHLBanks ring a bell? When did you arrive to the FDIC? 1990? Didn't the FDIC manage the failed RTC (Public-Private Partnerships), where the FHLBs invested in, through a RefCorp bond purchased by the UST?

Oh my! We're all going down!

Please, submit a written report.

There is no Commitment Fee. Go back to sleep.

Remember that we are here to legalize every action, not just to cry out loud.

A Warrant to (iii) protect the taxpayer.

The dividend was impeccably suspended.

SPS increased for free, a joke in the best interests of the Agency.

Etc.

We just need the SCOTUS to highlight "rehabilitate FnF".

Justice Alito simply legalized the Separate Account plan, which isn't beneficial to FnF "on paper", as we can see in their awful ERCF tables, but the "rehabilitate FnF" occurs in an "External Position", a global pandemic about off-balance sheet exposures (Europe Payment Systems, the Fed's Deferred Asset conceals the UST's SPS that should have funded the losses, etc)

It's beneficial to the Agency and the public (he claimed), as far as "interests" are concerned, in the sense that it enables the extension of conservatorship for the extortion of their resources on a great scale, with the sale of loans with a debt forgiveness clause attached and REO inventory to special interest groups, like Goldman Sachs gobbling up through a subsidiary all the REO inventory sold by Fannie Mae.

The Separate Account isn't that difficult to see it if you know to read plain English: a capital distribution (deplete capital) is authorized if it improves the regulatory capital (build capital). So, a Separate Account (External Position) wording right there, that

"supplements (follow-on plan) and shall not replace or affect the restriction on capital distribution by statute U.S.Code §4614(e) (a capital distribution that reduces the SPS: First phase of the plan)"

We can't wait for you to understand that capital distributions are restricted.

Any dividend, today's gifted SPS and the payment of Securities Litigation judgments are capital distributions.

Justice Alito's prerequisite of "rehabilitation of FnF" has not been satisfied.

Pay us damages, pro se plaintiff.

Don't expect the SCOTUS to know what capital is.

What was important is that justice Alito understood that the conservator must rehabilitate FnF, and that only means to restore capital levels.

Why don't you create another thread with all your aliases, but, this time, explaining how you are going to pay the Equity holders your portion of the $4.8 billion requested in Punitive Damages, plaintiff Joshua Angel?

This way, you stop for a few minutes harassing the shareholders on this board, downplaying expectations.

The DOJ is compelled to address our claim about the frivolous lawsuits spree.

LLPA reduce cross-subsidization, yet you reply with the slogan

cross subsidizing higher credit and default risk by those mortgagors with lower credit and default risk?

BOOM. The plain language controls. Therefore, quit peddling fictitious claims about an "implied contract", that the attorneys send you by email.

Their take isn't a peripheral consideration but an outright fiction.

Any dividend, today's gifted SPS and the very payment of Securities Litigation judgment in question, are a breach of the statutory provision Restriction on Capital Distributions and, in the 2021 Capital Rule, a breach of the Table 8: Payout ratio.

A dividend payment is also a breach of financial concepts, as the Retained Earnings account where the dividend is distributed out, turned negative fast (Accumulated Deficit).

A breach of the conservator's Rehab power as well.

It's not what "may" in the conservator's Power and its Incidental Power: "best interests of the Agency", are about.

You are annoyed because the dividend on your JPSs is kept by the enterprises and it's all that matters for the stock valuation of this fixed-income security.

Sorry, but this is what your security recorded in Core Capital is for: Recapitalization.

A dividend suspension is authorized in the contract.

Recorded in Core Capital (loss-absorbing capacity) and Equity, for Capital adequacy matters, as stated in the contract as well. Otherwise it would have been recorded in Debt along with similar obligations issued by FnF. But in that case, don't expect to get the current high "coupon" in interest payments, as it was meant to offset the risk of dividend suspension when it's Equity.

You talk about

shareholders' objectively reasonable expectations

.jpeg)

No genuine dispute remains on the fact of harm on the theory of plaintiffs were denied dividends that they otherwise were reasonably certain to receive.

.jpeg)

Is now renaming the Conservatorships "Taking of private property" the slogan of the plotters?

NWS is a clear case of illegal taking of private property.

Payment of Securities Litigation judgments, a capital distribution too.

A capital distribution aka dividends is not the same thing as a judgment being required to be paid.

Clarification: 13-year gap between the requirement by law of a new Risk-Based Capital requirement, plus other changes, and the Capital Rule (2008-2021)

With a FHEFSSA 18-month Implementation section, a Capital Rule would have coincided with the mandate by Dodd-Frank law of recommendations on ending the conservatorships (2010) and subsequent February 2011 UST-HUD Privatized Housing Finance System, which means Basel framework as well ("Stringent capital requirements")

Now, FHFA is focused on a Housing Finance System revamp and how to get rid of the unwanted AT1 Capital holders (JPS). Under the Separate Account plan, they must be redeemed by FnF for cash at their redemption value.

FHFA is conspiring with the hedge funds that filed frivolous lawsuits in court, to get rid of them with a swap JPS for Cs, jointly with the DOJ with its SPS.

This is a debate about the endpoint, not about the conservatorship process where FnF must be rehabilitated regardless, with the Restriction on Capital Distributions as a Prompt Corrective Action.

An Efficient Market assumes that the stocks discount all available information. Then, the market value is the fair value of the stocks.

But this doesn't happen with the FnF stocks.

Fanniegate is all about the concealment of the key statutory provisions and financial concepts in frivolous lawsuits and the shills on social media, besides outright illegal actions to the same end: misrepresent their financial condition. For instance, the Charter-unauthorized CRT operations or the SPS increased for free absent from the Balance Sheets (Financial Statement fraud) because it would wipe out your big lie of "Retained Earnings", and make FnF post $0 EPS every quarter. Calculate the fair value with that!

And the most important concealment of all: that the 2021 Capital Rule is intertwined with the 2011 UST Report to Congress with a Privatized Housing Finance System for the release from conservatorship, demanded in the Dodd-Frank of 2010.

Yesterday I commented that the absence in the FHEFSSA of the typical section 18-MONTH IMPLEMENTATION is key in the plan of concealment, as it would have avoided the 11-year gap between the requirement by law of a new Risk-Based Capital requirement, plus an authority to introduce changes, and the date of publication of the Capital Rule.

Also, my comment denounces the 3 posters that aimed to conceal that the 2021 Capital Rule exists; But then, there is Navy Hedge Fund, in charge of concealing the first leg of the overall Conservatorship: the actual mandate to Treasury by law in 2010, in your four-part sequel "Navycmdr never learns". A mandate to establish the endpoint of the Conservatorship with a 3-option Housing Finance System revamp, that we are heading to since then. Latest, the Capital Rule was amended (Federal Register publish Date: November 30th, 2023) to include the case of Commingled Securities (Resecuritizations). A security that was unveiled by Freddie Mac for the first time in June 2022, and suitable for the Government Catastrophic-Loss Reinsurance in the third option of the 2011 3-option plan for the release. Although it can be private Reinsurance for the options 1 and 2.

An important concealment, because it demonstrates that the conservatorship turned out to be the typical Transition Period to build capital, given to any financial company that has its capital rule amended (like the 5 years for the banks with the recent changes by the Federal Reserve/FDIC and the 10 years that the Congress gave to the FHA)

Just in case you know nothing about the FHFA-C's Rehab power and the Restriction on capital distribution to the same end. Besides the prior Mandatory Release Undercapitalized in the FHEFSSA, that also implies a recapitalization process, struck by Calabria/Pelosi's HERA.

Though, FnF could have been released well before at the discretion of the Director, but it seems we are heading to the scenario of clean Housing Finance System revamp, getting rid of the unwanted JPS holders (AT1 Capital instruments) for sure, and for that, it's necessary a CET1 > 2.5% of Adjusted Total Assets. A threshold that the laggard Fannie Mae met with the 3Q2023 earnings report.

Pending what to do with the existing shareholder: either a scenario of Takings/resale to players in Housing Finance; "as is" or a takeover at a price that includes the Deferred Income, net.

It seems that your Happy Emoji reality of

$DAMAGE AWARD $ALLOCATION $PLAN & $RETAINED $EARNINGS

Fourth part in the sequel to "Navycmdr never learns".

Entitled: "I'm back! 🤡"

Navy Hedge Fund attempts to supplant the actual mandate to Treasury with the endpoint of the Conservatorship: Privatized Housing Finance System (which means Basel framework for capital requirements), at the request of the Dodd-Frank law of 2010:

Require Treasury to conduct a study and submit recommendations on ending the Conservatorships, no later than January 31, 2011.

Are you pretending that the Capital Rule doesn't exist?

Isn't it crazy?

FNMA hitting 2.5% net worth absent SPSPA capital requirements in 2025.

Navy commodore is a shill for the hedge funds' frivolous lawsuits.

This is why he repeats that only the court news will move the share price, when it's precisely the opposite. The corrupt litigation has tumbled the stock price because it didn't recover even $1 of regulatory capital, out of a $400 billion capital deficit over Minimum Leverage capital requirement in FnF, shamelessly concealing that what FnF sent to Treasury is regulatory capital (dividend, a distribution of earnings), not simple cash, as we saw when they simply requested a refund of $29 billion is cash. FnF have tonnes of cash on the balance sheet, but a $400 billion capital deficit.

Therefore, it's all about sophisticated investors like Fairholme, Perry Capital, Pagliara, Hindes, Ackman, etc, along with rogue attorneys, playing the fool in order to conceal the reality of a Separate Account plan.

Timothy Howard:

Separate Account? I don't know what that is.

The NWS dividend, a typical renegotiation of obligations. Thus, within the FHFA-C's powers.

A Nationalization isn't authorized in a Conservatorship, unless the stocks are formally acquired at their fair value at the time, which hasn't happened.

With so many operations to misrepresent their financial condition (the Credit Risk Transfer operations, illegal in the Charter Act: Credit Enhancement clause; a Warrant to protect the taxpayer or illegal in the Fee Limitation of U.S.; etc.), we should talk about adjusted fair value.

A fair value in a Takings has a minimum amount of the Book Value per stock or Common Equity per stock, which is consistent with the idea of Charter cutoff date, staging a liquidation, as proposed by Mark Calabria.

What Robert is doing is stock price manipulation.

Among the definitions re Capital: Definition of Capital Distribution.

1-Dividends and today's SPS increased for free.

2-Stock buybacks.

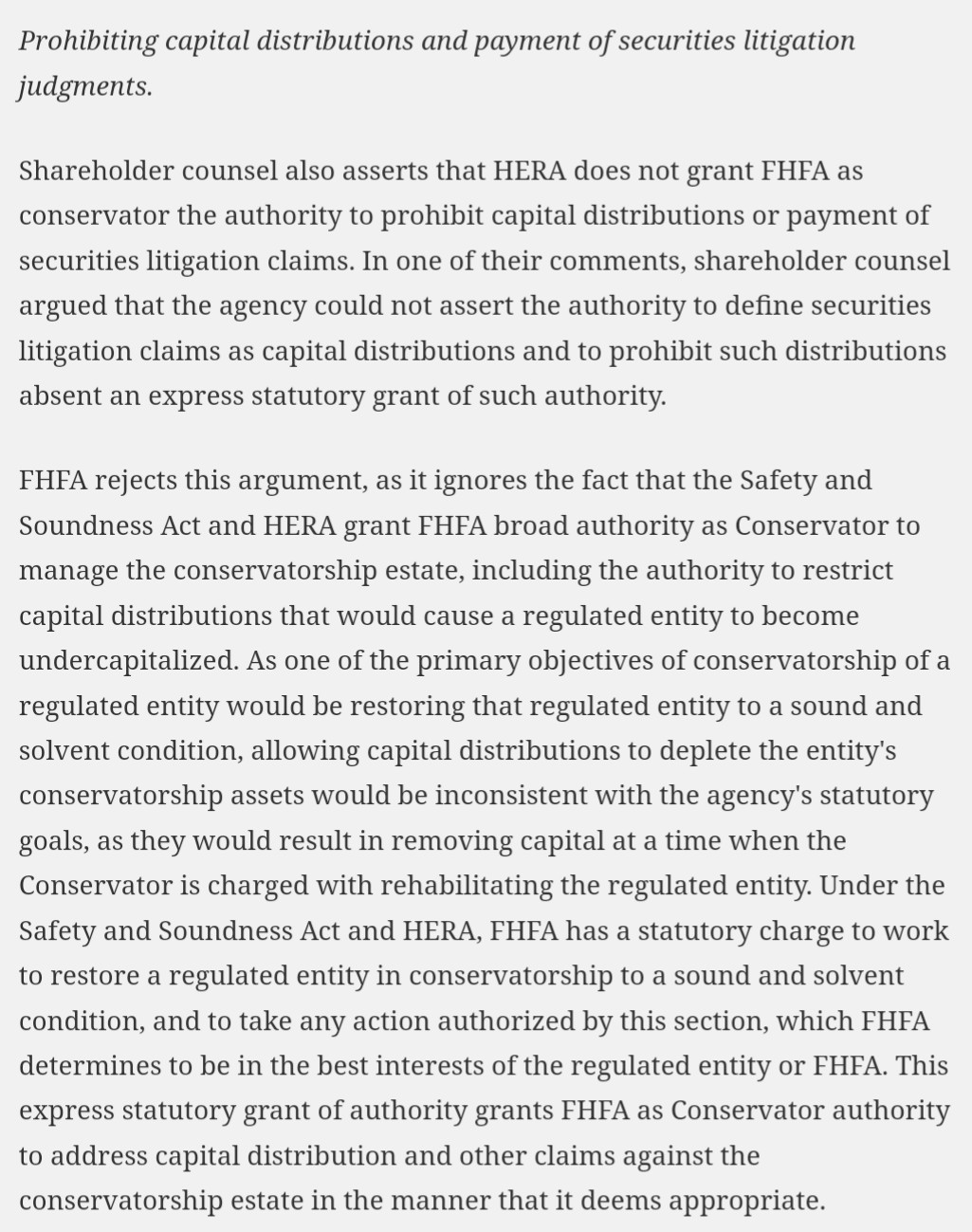

3-Payment of Securities Litigation judgment, included by the FHFA with an express grant of authority, through the 12 CFR 1229.13.

RESTRICTION ON CAPITAL DISTRIBUTIONS

The FHFA already prohibited the payment ordered in the Lamberth court because of this restriction, and it can't be overridden with

"...except to the extent the Director determines is in the interest of the conservatorship"

kthomp10 obsessed with HERA for concealment of the FHEFSSA and the Charter Act.

Just like the DOJ attorneys: "As of the passage of HERA....."

Coincidence?

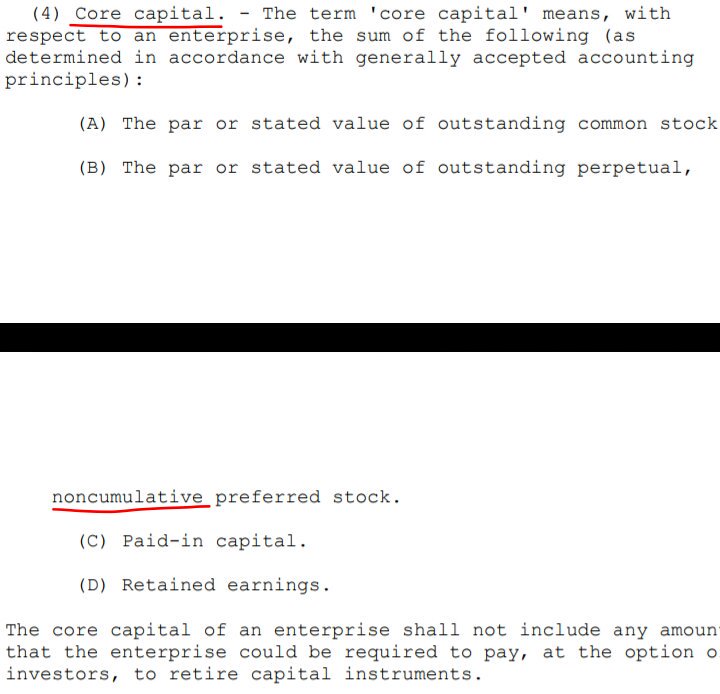

They don't count towards core capital because HERA's definition of core capital doesn't include cumulative preferred shares.

Felony in the U.S.District Court for the district of Columbia.

Judge Lamberth's latest court order granting award of prejudgment interest must be rescinded.

The restriction of this payment uncovers all other capital distributions during Conservatorship (dividends and SPS increased for free) restricted too, and what is known as the Separate Account plan that legalizes them.

THERE'S BEEN A FELONY IN THE LAMBERTH COURT

— Conservatives against Trump (@CarlosVignote) December 14, 2023

Payment of Securities Litigation judgment,a capital distribution(12CFR 1229.13)restricted to...build capital. Not disbursed yet,but you can't set aside a reserve(CE,escrowed) that has already deprived of capital.

🆕BVPS,unch.#Fanniegate https://t.co/g3MqnSqjTN

Fisher is an attorney. Then, clueless about financial matters.

The resolution of FnF isn't about "What if .... hadn't existed?"

Every action has existed and what we are doing is to legalize them with the Separate Account plan, which is the same as saying that it's been a normal Conservatorship with a simple dividend suspended to everybody, including the SPS, obviously (Equity).

Besides, his math is wrong.

He still doesn't understand the concept of dividend (distribution of earnings out of the Retained Earnings account in the balance sheets. A balance sheet is the picture of a company at a determined date. You can't pay dividend with an Accumulated Deficit Retained Earnings account. It's not interest payments) or the concept of Restriction on Capital Distribution to build capital.

There was no actual dividend payment during Conservatorship by any stretch of the imagination, but an assessment in the form of capital distribution and under the guise of dividend payment.

Also taking into account that it would comply with its Rehab power and carried out thanks to its Incidental Power: "any action authorized by this section, in the best interests of the Agency."

Assessments applied towards the exceptions to the Restriction on Capital Distributions in the law and the CFR (reduce the SPS and recapitalization), as seen in my signature image (Freddie Mac), 1989 FHLBanks-style (extended version with a Recapitalization plan. Full assessment applied towards reduction of SPS + recap, as dividends are restricted.)

Finally, there is no "originally agreed upon dividend" because the only contract with the Treasury is called Charter Act. The SPSPA is a simple fact sheet.

He doesn't understand that FnF are congressionally-chartered private corporations with a special rate on a UST backup of the enterprises in exchange for their Public Mission (section Purposes) as a last resort (seen in the section Purposes as well), that is the one that prevails (weighted-average 1.8% dividend rate), knowing that the dividend on SPS is cumulative.

No one can say they didn't see it coming, as everything is set forth in the law and basic Finance. This is why we don't need Treasury documents.

Bryndon Fisher is another one covering up the key statutory provisions and financial concepts in court. How is that even possible?

The "Finance for attorneys" (trickery, coverups, harassment, lies, play the fool, etc.), must be put to rest.

The rogue 94-year-old pro se plaintiff switches FnF for the brokerage firm Schwab, to justify his assertion already dismissed, contending that

Senior Preferred Stock is a product by definition.

Quit lying, pro se plaintiff. Ain't no refinancing option.

You keep on repeating the same lies. But a mistake in court with your two lawsuits, is very costly.

Lately: "the SPS are products". It only shows that you don't know what you are talking about. A security needs an activity to be considered a product, and thus, an special authorization by the FHFA director, publication in the Federal Register, comment period, etc. This is why with the lack thereof, you end up saying that the SPS are illegal.

Also, there are activities that aren't products. Everything is stated in the law that you are reading. So, you are just messing around to later claim: "it's complicated".

Therefore, a SPS isn't a product but a simple security and it's been considered one of the "any redeemable obligation" (in respect of capital stock (Source SPSPA. Equity) for the original UST backup at special rates (Subsection (c)(b) in the Charter Act) as a last resort (Section Purposes: "Operations financed by private capital to the maximum extent feasible") and the ones with high yield, duly authorized to purchase/no-purchase (SPS LP increased➡️fraud) by the Treasury under the prerequisites (i) and (ii).Source, suitable for the assessments in a Separate Account plan, FHLBanks-style.

I already explained it once to your other alias, Barron. But you rather go rogue, repeating it at least 10 more times and you want me to reply to your posts rebutting it each time, right? Which I refused, until today. The latest with Rodney citing "our friend Barron".

With regard to your comment that I'm replying to, the same repetitive lie you post about the reduction of SPS set forth in the law. And, by the way, for which Howard faces charges stating a dozen times in his SCOTUS amicus brief that the SPS are non-repayable securites.

It's NOT a refinancing option, because the objective of the lawmakers is to maintain the same capital as before, or increase it. That's what a Restriction on Capital Distributions is for. It's not a fancy name. Also, pursuant to the conservator's power: Put FnF in a sound and solvent condition (Build capital and reduce the debentures SPS, respectively. So, this Restriction on Capital Distribution and its exception, was spot on during a Conservatorship) and preserve and conserve assets. So, increase and/or preserve capital and reduce debentures (even more if it's an obligation with the taxpayer: SPS), is the way to go. That's called financial rehabilitation.

The exception A that you point out, is achieved when FnF repaid the SPS with cash, at the same time as the Common Equity increased (Retained Earings account. Core Capital). Double-entry accounting. There you are, the required increase in capital in the same amount as the reduction in the SPS for the exception B. So, the intent of the lawmakers was satisfied and there is no need to issue new shares or obligations.

Finally, your other slogan. Can't you read that it's always the FHEFSSA as amended by HERA? Not HERA alone as you claim, that just inserted the amendment in the FHEFSSA.

Where is the ball? Are you going to say again the catchy phrase: "it's complicated"?

How many times did I post these screenshots taken from the statute just for you?

I already denounced you misbehavior, rogue pro se plaintiff. Here, posted just two weeks ago:

Wait a few days for the plaintiff Joshua Angel to post the same lies with one of his 30 different aliases (HappyAlways, EternalPatience, Fannie heyyyy, nagoya, Rodney, Barron, stvupdate, 5 bagger, etc), refuted over and over again (interest rate; HERA; 4 exceptions in the CFR 1237.12 to conceal the ones by statute U.S.Code §4614(e); refinancing option; PA, a contract; etc.)

This is the bread and butter during conservatorship with all the commissioned social media celebrities and attorneys that post here regularly.

The fraudsters file frivolous lawsuits, to later claim that the court news drive the stock price.

Berkowitz:

The stake in Fannie/Freddie pfds was reduced by ~40% during H1 2023 following a court loss in January.

The draws from Treasury were $191B, not $193B.

3rd step unwinding the Separate Account: Treasury Stock, retired.

$150 billion cash refund from the UST and the FHFA, plus a posting in their Retained Earnings accounts of the Common Equity held in escrow ($236 billion)

BV ($B) FMCC/FNMA:106/130

— Conservatives against Trump (@CarlosVignote) November 5, 2023

-1.2/19.5 Beginning bce 6/2008

+80/94 Acc Total Comprehensive Income, adjusted for these Accounting Change charges:

4/2009: 5/3

1/2010: -11.7/3.3

1/2020: -0.24/-1.1

+9.3/9 CRT,net(RE)

+18.7/6.8 PLMBS settlement:73%/27% based on AOCI in 6/2008.#Fanniegate https://t.co/EmZTYgahAE

Continued retention of earnings is the main one i watch

Treasury doesn't participate in listen-only mode roundtables, like Sandra Thompson attending a council meeting in the Town Hall of Pagliara's home town. Allegedly, because I haven't seen any image of the event.

What is Pagliara up to next?

Does Deputy Secretary Adeyemo know? Because he already had a roundtable about the subject at the NYSE, less than three months ago.

The reason this is important $fnma #fanniegate is because it picks up at Treasury where FHFA left off at Franklin TN. Sandra Thompson lit the torch there and now it is going nationwide. https://t.co/78DsGGWdFL

— Fanniegate Hero (@DoNotLose) December 12, 2023