Friday, April 26, 2024 1:25:07 AM

Let alone to set up a parallel Housing Finance System with them, called "GSE Reform".

CRT is only authorized the UST with its portion (Capital Magnet Fund) of the 4.2 bps allocated to two Affordable Housing Funds managed by HUD and the UST. Source.

The CRT is a normal bond used as an excuse to make FnF pay interests, that began with a steep 5% - 6% rate, which looked like the fraud in early conservatorship with their 30-year zero coupon callable MTNs, where FnF paid an outstanding rate when they were redeemed soon after being issued.

Now, they include arrangements in these back-end CRT "Bonds" (after FnF had carried out foreclosure prevention actions to bail out these CRT investors), and thus, it serves at the will of a random FHFA director whether he requires the payment of claims or not (Utility Model).

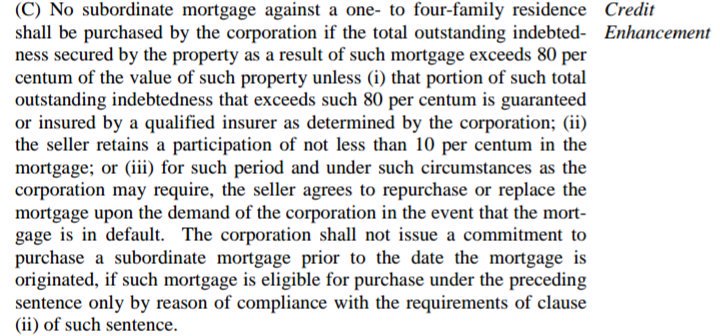

On the other hand, the PMI required to borrowers with LTV >80%, and today's Commingled Securities (Catastrophic-Loss Reinsurance or resecuritizations) 100% insured by other guarantors against default, are authorized CRT operations (number 1 and number 3 in the clause Credit Enhancement of the Charte Act, respectively)

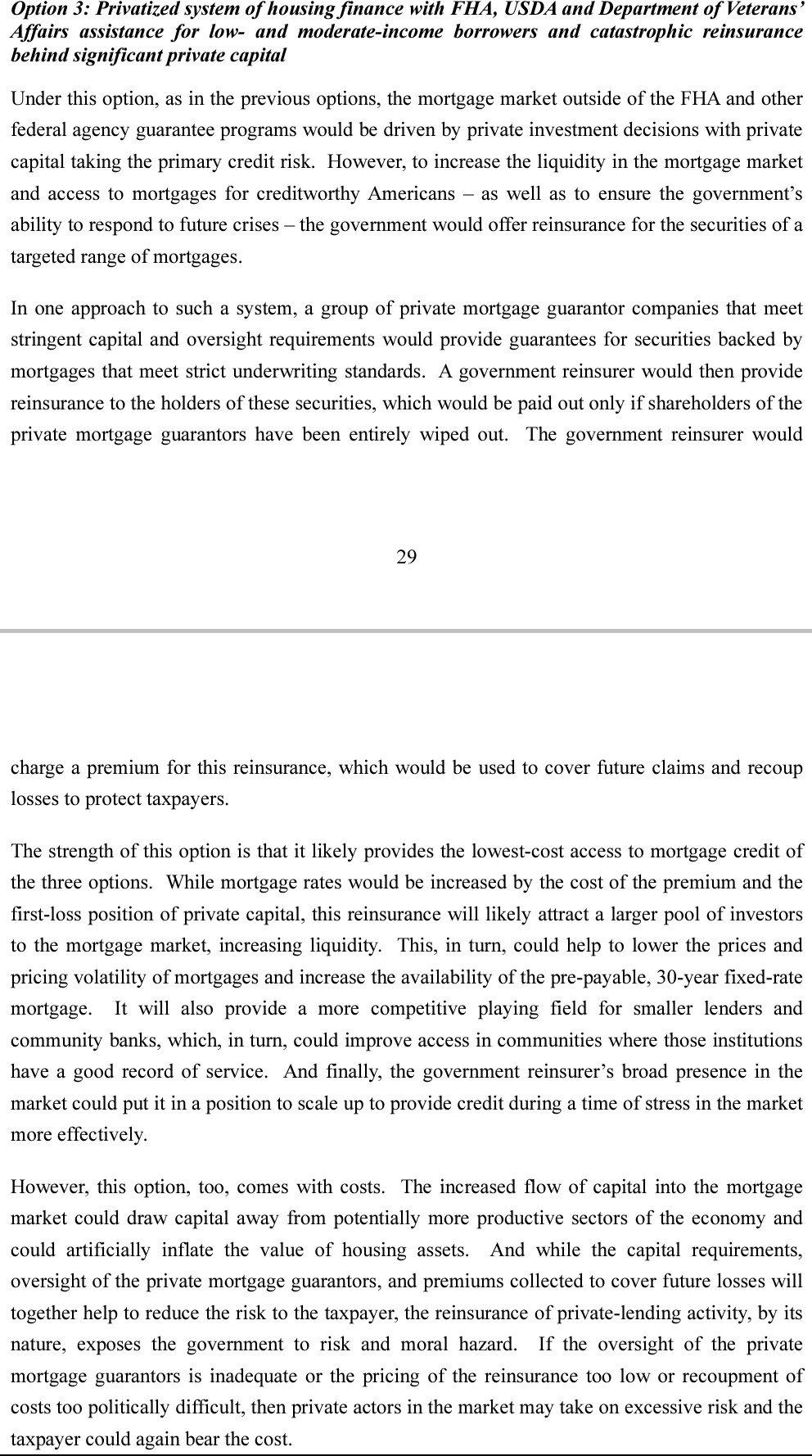

It's precisely, the Commingled Securites or Catastrophic-Loss Reinsurance, a new product for the 3-option Privatized Housing Finance System revamp, chosen by the UST in 2011 for the release from conservatorship, at the request of the Dodd-Frank law, because the option 3 is a Government Catastrophic-Loss Reinsurance and this product enables it:

This product can be used for a private Catastrophic-Loss Reinsurance as well, and then, we would be in the option 1 or 2.

It wasn't created to make FnF reinsure each other's UMBSs. Currently a pilot program, but, at some point, it has to be announced one of the 3 options.

This product was unveiled by Freddie Mac in June 2022 (Source. Notice how it's written that it began with a price of 50 bps. One week later, the FHFA changed it for 9.375 bps to better reflect the 2011 UST plan we are bound for, and not the ill-conceived Mnuchin's 2019 Plan with a Government Explicit Guarantee on MBSs)

It isn't the same a MBS with Govt Catastrophic-Loss Reinsurance and a MBS with Govt Explicit Gtee. In the first one, the credit risk is covered by private guarantors. It's activated once it files for bankruptcy.

Today, the MBS is guaranteed by FnF and there is only a cheap UST backup of FnF upon negative Net Worth. That's it. The "MBS with a Govt Implicit Gtee" is an attempt to conceal the reality of a UST backup of FnF.

The FHFA has a tendency to deviate from the normal course and it corrects itself, or, sometimes, it needs help.

The PLMBS was a product not authorized in this clause (Unlawful. Lack of credit enhancement operation) and it was one of the reasons for the conservatorships.

This time, the rogue FHFA can't be authorized to break the law again at its will, regardless that JPM, the Mnuchin Treasury Department and Mike Bloomberg (included in his electoral manifesto posted yesterday) love the CRTs. Barred in FnF.

The grounds for a Housing Finance System revamp ("GSE Reform") was initiated by FHFA's DeMarco, in light of the 2011 UST plan for the release, that included g-fee hikes, Basel framework for capital requirements: "capital standards that cover the risk as if it was held by the banks" (Mel Watt attempted to deviate from this course in his proposed Capital Rule, and he was corrected by Calabria),...., that would end up with the removal of the most privilege of all: the Charter's UST backup of FnF (Charter revoked).

ST TRIES TO OVERSHADOW DEMARCO AS MASTERMIND OF REFORM

— Conservatives against Trump (@CarlosVignote) April 25, 2024

In her written testimony.

DeMarco(written testimony, May 2011)unveiled the preps of a Privatized Housing Finance Sys revamp, chosen for the release by the UST in a Report to Congress 3 mths earlier: g-fee hikes,...#Fanniegate https://t.co/mgjrPMllgX pic.twitter.com/TDKYNXTug4

Avant Technologies Equipping AI-Managed Data Center with High Performance Computing Systems • AVAI • May 10, 2024 8:00 AM

VAYK Discloses Strategic Conversation on Potential Acquisition of $4 Million Home Service Business • VAYK • May 9, 2024 9:00 AM

Bantec's Howco Awarded $4.19 Million Dollar U.S. Department of Defense Contract • BANT • May 8, 2024 10:00 AM

Element79 Gold Corp Successfully Closes Maverick Springs Option Agreement • ELEM • May 8, 2024 9:05 AM

Kona Gold Beverages, Inc. Achieves April Revenues Exceeding $586,000 • KGKG • May 8, 2024 8:30 AM

Epazz plans to spin off Galaxy Batteries Inc. • EPAZ • May 8, 2024 7:05 AM