News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

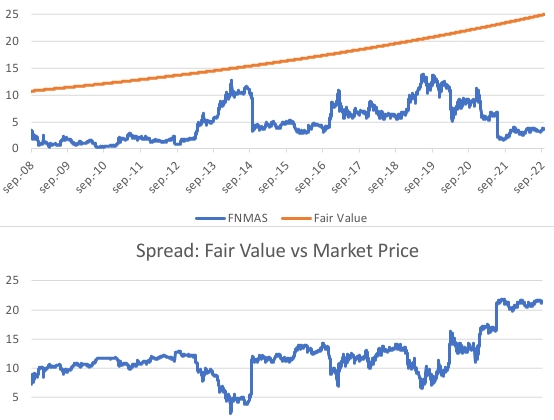

To be precise, FNMAS' Fair Vaule $10.8 in 2008.

$9.8 now for a second Conservatorship that would start today, assuming that it'd be necessary 16 years to build capital with the Restriction on Capital Distribution and resume the dividend payments (Table 8), when the fair value fetches the stock par value.

Say no to do-overs and the "back to the future" promoted by the Investment banks and the hedge funds that own the FHFA.

"Less than $10 — these are cheap."

"JPS anti dilution provisions"? You are a fraud, Bradfraud.

JPS are wiped out today with the current Balance Sheet, because their Net Worth is $118.4 billion, but there is $312.5 billion SPS outstanding, including the ones absent from the Balance Sheets.

And things don't get better every quarter because FnF are building SPS in their Net Worth, not regulatory capital, due to the offset when the SPS LP is increased for free in the same amount as the Net Worth increase in the quarter (Their $118.4 billion Net Worth is exactly the $118.4 billion SPS

(*) that are missing on the Balance Sheet. Financial Statement fraud)

(*) Fannie Mae has $1.1 billion more SPS increased for free than Net Worth, due to a prior accounting adjustment.

So, the JPS are worthless unless you join the Separate Account in accordance with the law, that gives you the full par value for your stock, but you don't care because you are here on a mission.

You just can't stop lying, can you.

in my view fnma has no intrinsic value because the spspa and fnmas is worth 25 when the companies are restructured.

It's never too late for Pagliara to learn Finance: financial concepts of Capital distribution and dividend.

— Conservatives against Trump (@CarlosVignote) November 11, 2023

The FHFA-C's Incidental Power allows it to mislead/mess around(Separate Acct)respecting the financial rehabilitation(Justice Alito/judge Willett)#Fanniegate@TheJusticeDept https://t.co/IOD74Hmn1A pic.twitter.com/T6WmNURtjd

Our negotiator stresses the stark difference between DeMarco and Sandra Thompson, as a new line of attack to the Fanniegate scandal.

The approach is to highlight the intent with their actions.

DeMarco, with the strict compliance with the law, although you may think that he succumbed to the CRT, barred in the Charter's credit enhancement clause, it's assumed that it's another way to hold their capital in escrow at the Treasury Department, because this "fee or charge" is also barred in the Charter's Fee Limitation. Thus, complying with the conservator's Rehab power, and the concealment is another way to misrepresent their financial condition.

On the other hand, the Goldman Sachs alumni Sandra Thompson, who even the timing of her arrival to the FHFA was ill intent and failed, attempting to distance herself from the NWS dividend (she didn't know that the dividend is paid at the end of the next quarter), to later use it as a legal defense strategy in court: "DeMarco is to blame", in one of the lawsuits brought by her Hedge Funds guard that adores her: at the FDIC, she spearheaded the multiple Public-Private Partnerships with Wall Street in the 1989 RTC scheme using the FHLBanks, that saddled the taxpayer with an estimated $48.8 billion loss. DeMarco was the auditor at GAO.

Their intent says it all:

DeMarco is helping out to some extent, playing both ways: a separate account plan that upholds the law and misleading about it.

Sandra Thompson is ready for the coup the grâce.

DEMARCO'S INTENT: LAW

— Conservatives against Trump (@CarlosVignote) November 10, 2023

Opposed to short-sales Trump approved(NPL,RPL w/ debt forgiveness string)

ST'S BLAME DEMARCO ILL INTENT

Arriving in 3/2013. 1st NWS div March 30.Oops!

Compelled DeMarco to appear in court w/ atty.

Removed herself as Defendant.

Jury:"2011 MBS data"#Fanniegate https://t.co/ewQOcagWFf pic.twitter.com/v2gfP675y7

A downgrade of outlook in the U.S. debt rating bodes well for the scenario of Charter revoked, as it's what intertwines the Treasury yields with the cost of funding in FnF: the so called UST backup of FnF at rates similar to Treasuries "as of the end of the month preceding the purchase" (Subsection (c))

Having FnF well capitalized Basel framework and with a guarantee fee that reflects its risk, allows them to be detached of the Treasury department, as the soundness is always what drives the cost of funding and the Charter's UST backup is only suitable upon lack thereof.

Thank goodness the conservator had the clear mandate to put FnF in a sound and solvent condition. 15 years in the making.

Exactly. Only the nutty allies Bradford, Rum commodore and the pro se plaintiff Joshua Angel have conversations with oneself in this board.

Bradford: LuLeVan, Bradford86 and Make it or break it.

Rum: navycmdr, Patswil and Stockprofitter.

Plaintiff Joshua Angel with more than 20 different alliases: EternalPatience, stvupdate, Rodney, Barron, HappyAlways, etc.

This plaintiff attacks our negotiator on #Fanniegate regularly because he thinks he is negotiating with his shitty lawsuits. First in the Lamberth court, then surprisingly allowed to try again in the CFC with judge Sweeney that now keeps it artificially active, so he stages a negotiation.

He is envious of our negotiator Carlos that submits thoughful financial analyses through Twitter, in this one-way negotiation.

They can't understand that it isn't the same to talk to yourself than referring to oneself in third person, recommended when writing academic reports or, in the case of our negotiator, in-depth financial analyses.

Only a crackpot uploads a meme ridiculing himself as profile picture.

The joke's on you.

Not so fast. These are the stocks' fair values in Q3 in comparison with Q2, under a Privatized Housing Finance System we've been heading to since 2011 and in a Taking/resale scenario:

By the way, show some respect to our negotiator Carlos on #Fanniegate:

i'm going to fire his a@$

TAKING +RESALE +JPS REDEEMED:$349B PROFIT

— Conservatives against Trump (@CarlosVignote) November 3, 2023

+$14B extra Corp. Tax(Deferred Income)$FNMA/ $FMCC

Price;PER;BV;Mkt Cap

-Existing shareholder

$112/$164;6/7;1/1;$130B/$106B

-UST

$288/$388;15/16;2.6/2.4;$333B/$252B

-Buyer(Amortization of DI)

$273/$335;14/14;2.4/2;$317B/$218B#Fanniegate https://t.co/tbtoa5ax4v pic.twitter.com/dcp0KhYtu4

Why do you make up our negotiator's name?

His name is Alfred E. Neumann

Who is our negotiator Carlos? I post his Twitter link every time I mention him.

Anyone can be negotiator. You just have to post thoughtful financial analyses and send it to the DOJ and the Congress.

Guess what. No one else does it.

No wonder why he self-imposed negotiator. You didn't figure it out and you had to ask

Who is OUR NEGOTIATOR????

Fanniegate meme.

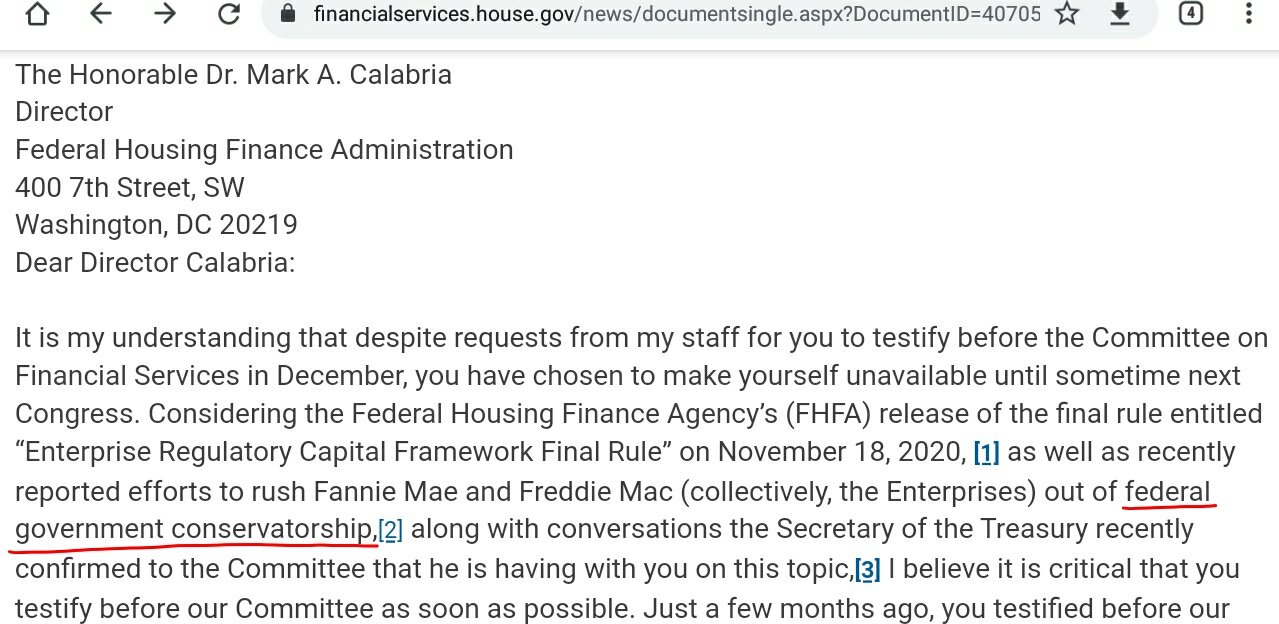

BOMBSHELL! Our negotiator clamps down on the gang that aims to pass a Conservatorship off as Nationalization.

Just calling it "Federal government conservatorship", so they act pretending that the guarantee fee that FnF charge, or the money sent to UST through CRT expenses (because these people might still be thinking that the purchase of SPS is a credit loss of the taxpayer, instead of obligations of FnF, as stated by representative Hensarling in early conservatorship. That's why the "CRT, to protect the taxpayer" of the Goldman Sachs alumni, Sandra Thompson. Illegal in the Charter's Credit Enhancement clause, by the way), is related to the bill HR1859 submitted to Congress on May 12, 2011, when this bill wasn't enacted into law, and thus, it died, as it contemplated a "Catastrophic Federal Guarantee on Federal Housing Finance Agency securities".

So, they sneak the word "Federal" in a conservatorship and see if it sticks.

Also the attempt by a NYT reporter stating in a talk-show: "Their name starts with Federal, no?", commented yesterday about this issue.

A conservatorship preserves their status as private shareholder-owned enterprises, so these attempts are futile.

Let alone, Sheila Bair that showed up as BOD chair in Fannie Mae pretending that FnF are included in the failed Resolution Trust Corporation (RTC), a 1989 scheme of Public-Private Partnerships with Wall Street, where the UST likely lost the $48.8 billion it invested in, with GAO (DeMarco) as the auditor, at the same time Sandra Thompson arrived to the FDIC as well ($30 billion through RefCorp obligations issued by Funding Corporation owned by the FHLBanks and $18.8 billion invested directly in RTC by law), because RTC was managed by the FDIC where Sheila Bair was president not so long ago. And, by the way, Sheila Bair took part of the conclave that made the decision of Conservatorship in FnF, according to a famous WSJ article published at the time ("top banking official"), which leads us to rule that her presence as FNMA BOD chair later on, is another aspect that puts the entire conservatorship into question (besides manufactured losses in FnF to justify the conservatorship with (G) LOSSES, etc.) and reinforces the view that these officials were desparate enough, amid taxpayer's losses, to carry out a Separate Account with FnF, similar to the 1989 Separate Account in the FHLBs, to achieve a different outcome that would save them in all their deeds since 1989 (Famous 2011 FHFA press release: "The FHLBanks fulfilled their obligation to pay interests", leaving the principal of the RefCorp obligation mentioned before, unpaid. So, it wanted to pass the RefCorp obligation off as an obligation to pay interests, knowing that it was Funding Corp the one that only had to pay interests, but its Equity holders (FHLBanks) had to pay down both interests and, with the excess, pay the principal of the RefCorp obligation at maturity through a Separate Account ("credit due to FHLBanks") with monies invested in zero coupon Treasury notes, so that the sum matches the principal of RefCorp at maturity. Playing with word "obligation" (a bond and also a requirement) to deceive the taxpayer, while attempting the seizure of FnF to make up for the losses prompted by mismanagement and lack of professionalism)

This was posted at the time on a blog tracking the Fanniegate scandal, just after the bill was submitted:

Likewise, they think that the Resecuritization fee worth 9.375 bps unveiled by Freddie Mac in 2022, commonly known as Catastrophic-Loss Reinsurance fee, is a kind of "Catastrophic Federal Guarantee on Federal Housing Finance Agency securities".

I knew that sooner or later the combo Pagliara-Guido would be exposed.

Pagliara:"Involved in every aspect(of #Fanniegate)at the highest levels"

— Conservatives against Trump (@CarlosVignote) November 8, 2023

His footman Guido tweets:"Govt consvtrshp".

Then "Federal consvtrshp" when Pagliara called him to post @MaxineWaters' slogan.

"I told you Federal govt consvtrshp,moron!"

MW,go-to person of chamber investors. https://t.co/WVwIAyipvx pic.twitter.com/iimCtwuuqK

FHFA can't submit the proposed order of final judgment on November 14th at the request of judge Lamberth, because it involves the payment of a claim considered a capital distribution by the very FHFA in its July 20, 2011 Final Rule, when it amended its definition to add it up in #3.

It would be considered that it's formally proposing the commission of a felony, which couldn't have been said before, regardless that there is no final court order yet.

This intent to commit a felony makes this illegal act worse, when we assess the grade of culpability of this Federal Agency.

Restricted in the FHEFSSA's Restriction on Capital Distributions when FnF are undercapitalized (U.S. Code §4614(e)), just like:

#1. Any dividend and today's SPS LP increased for free as compensation to UST in the absence of dividends.

#2. Stock buybacks.

The Separate Account plan comes to the surface, because those payments mentioned in #1, existed, and we are using the exceptions to the restriction, to legalize them. Besides, there was no money for distribution as dividend all along.

It was explained here.

The fact that FHFA's DeMarco enacted in this Final Rule the 2nd phase of the plan (Recap outside their balance sheets. CFR 1237.12) with an effective date exactly on the Time Limitation as Acting Director, proves the intent to make sure that every subsequent action is legal (NWS dividend and today's gifted SPS), beginning with upholding his power of Rehab, whether he wanted or not.

If they thought that, as U.S. official, they can steal money from private corporations and get away with it, because later on, the Congress will approve something else, they failed, because everything is adjusted and the outcome is that, with the "take any action" in a law, they chose lying and mess around in the administration of a simple Conservatorship, with the collaboration of reckless attorneys in the coverup in court of everything else.

Besides lack of professionalism, I don't see any scenario where the FHFA can survive. It's owned by the Investment Banks and hedge funds.

To be precise, Maxine Waters: "Federal government conservatorship".

Just what Guido stated in his two tweets. First, government conservatorship. Then, federal conservatorship.

It seems that he didn't get it at first and was ordered to post a second tweet.

Are credit agencies and creditors aware that the federal debt actually exceeds $40 trillion? Shouldn't the creditors be aware that actual federal debt should include $7.5 trillion Fannie Mae and Freddie Mac debt while they remain in federal conservatorship?

— Guido da Costa Pereira (@GuidoPerei) November 8, 2023

@MoodysAnalytics

Guido's "Federal conservatorship" was only mentioned by Maxine_Waters before. Coincidence? Everyone else just says "conservatorship" or "FHFA conservatorship".

Thinking that it would change the fact that a conservatorship preserves their status as private shareholder owned-enterprises that I mentioned before.

Yes, the FHFA director appointed the FHFA conservator of FnF, as set forth in the law.

Our rights and powers are transferred to the conservator to help it carry out its functions, otherwise two-thirds shareholder vote would still be necessary as always and we would have opted out of every single measure, for the sake of just saying "No". And so do the management's and BOD's, that have continued performing their functions. It's when Fiduciary Duties (plural form) emerge, as occurs always that someone is acting on behalf of other. It's not acting in our best interests like a Trustee, but there are more fiduciary duties, something that judge Sweeney skipped: Duty of care (broken), confidentiality (broken in the Lamberth court), loyalty (broken), good faith (broken), prudence (broken) and disclosure (broken)

A conservatorship regulated by law, over congressionally-chartered private corporations and their soundness and solvency is also overseen by law.

In FnF, everything is decided, controlled and required by law. This is why the Fanniegate scandal is laughable, based on the coverup of statutory provisions in court and basic financial concepts like "dividends, a distribution of earnings", impossible with Accumulated Deficit Retained Earnings accounts, with the help of laymen shouting out loud on social media and rookie attorneys financial illiterates, hired by hedge fund managers.

This reminds me a well-known NYT reporter stressing: "Their name starts with Federal, no?", as if it changed anything about their legal status.

1968 law. Privatization of Fannie Mae:

It seems that your boss Tim Pagliara has frequent conversations with Maxine Waters. A chamber investor.

The same stance ("Thanks for sharing") as the other plotters Gary Hindes and Timothy Howard, that leads to a swap JPS for Cs, Warrant exercised and stock offerings.

This is why the payment of Punitive damages by the plotters that have decimated the share price with their stance written in formal documents (Ackman's letters with "re-privatization" and "FnF continue to build capital through retained earnings", etc), is of supreme importance (deterrence)

Conservatorship preserves their status as private shareholder-owned enterprises, so your statement is wrong, contending that their $7.5 trillion debt is federal debt in Conservatorship.

Now, what do you do? Are you going to leave the board or what?!

Guido is a layman hired by Pagliara to promote his book "Govt theft story" for stock price manipulation, the JPS holders get a better deal than otherwise would be and seeking the endgame of stock offerings for his colleague hedge funds (Warrant and SPOs)

Guido also has the task of tarnishing the image of the shareholders, bothering the lawmakers and others with his tweets crying out loud: "We've been robbed!", besides insulting the savvy investors betting on a Separate Account plan according to the law.

Another one on a mission: AI-generated image.

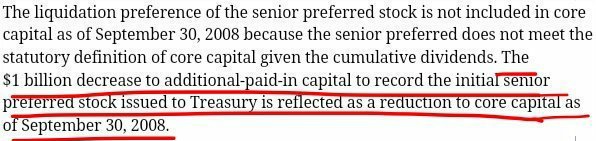

Table: Net Worth Activity in Freddie Mac, adjusted for the SPS increased for free that are missing on the balance sheets (Financial Statement fraud)

Here is why:

It shows how the offset attached that happens always when a company issues a security for free (without receiving the corresponding cash): stock dividends, Employee Stock Ownership Plan (ESOP), or the very FnF when they issued $1 billion SPS for free on day one of conservatorship, reducing APIC account (Core Capital), now exhausted, this is whey it's debited from Retained Earnings (SEC rules)

There is nothing "for free". It always comes out from someone's pockets. In this case, from the shareholders' pockets.

It also shows the objective: peddle the lie of "FnF continue to build capital" or "Retained Earnings, happy emoji, smile emoji" by the plotters. The reality is that FnF are building SPS, not regulatory capital, which remains stuck at $-194 billion Core Capital, FnF combined, every quarter ($402 billion capital shortfall over Minimum Leverage Capital requirement)

So, the full $44,661 million Net Worth in Freddie Mac as of September 30, 2023, belongs to the UST, as they are the $44,661 million gifted SPS currently absent from the balance sheet. Besides there is $117,308 million SPS outstanding in total.

The key: it shows how the Common Equity is held in escrow. Gifted SPS are a capital distribution restricted. Then, we consider it a joke and the Common Equity is held in escrow to comply with the exception to the Restriction on Capital Distributions (Recap) and also with the FHFA-C's Rehab power.

Another objective of this concealment is that people would begin to wonder if it occurred the same with the dividend payments to UST, as it's another capital distribution restricted, and there is the exception in the law: reduction of SPS and, later on, the Recapitalization in the CFR. It would have put an end to the Separate Account plan. This is the broad population, as the savvy investors spotted the Separate Account plan from the onset.

Finally, I post the two tweets from Calabria mentioned in my prior post.

He doesn't like the Charter's UST backup of FnF that he calls "government guarantees" and he proposed to revoke the Charter. Good. A Taking will do it or, simply, Charter revoked, as FnF are private shareholder-owned enterprises.

@schulte_stef you provide a gov't guarantee, then shareholders have strong incentive to capture it's value, need to minimize guarantees

— Mark Calabria (@MarkCalabria) February 8, 2016

@DoNotLose my own view is that shareholders can have the assets/liabilities, take 'em, but charters should go away, those are "public"

— Mark Calabria (@MarkCalabria) January 17, 2015

*** Calabria advocated a Taking at Book Value ***

The Book Value of a common stock is called Common Equity.

The Book Value of a JPS is called par value.

Navycmdr claims with the alias "Patswil":

The government is prohibited from making a profit off of stock transactions

TAKING +RESALE +JPS REDEEMED:$349B PROFIT

— Conservatives against Trump (@CarlosVignote) November 3, 2023

+$14B extra Corp. Tax(Deferred Income)$FNMA/ $FMCC

Price;PER;BV;Mkt Cap

-Existing shareholder

$112/$164;6/7;1/1;$130B/$106B

-UST

$288/$388;15/16;2.6/2.4;$333B/$252B

-Buyer(Amortization of DI)

$273/$335;14/14;2.4/2;$317B/$218B#Fanniegate https://t.co/tbtoa5ax4v pic.twitter.com/dcp0KhYtu4

The plaintiff Joshua Angel spinning the Separate Account, in order to not name it by its name and conceal the merits from our negotiator on the Fanniegate hashtag.

You always denied its existence but now you promote it somehow with the objective to deceive in key elements:

1st. It's laughable coming from you that went to the Lamberth Court to claim that FnF should have stored the dividend on your JPS, unaware that the dividend is a capital distribution and now you are talking about a Restriction on Capital Distributions. You still don't get that it's a dividend what is RESTRICTED when FnF are undercapitalized (also the SPS increased for free nowadays) and also unavailable Earnings for distribution as dividend, out of an Accumulated Deficit Retained Earnings account.

Dividends aren't interest payments. So, there is no such thing as "mandatory dividends" as the Wall Street law firm representing the FHFA claimed in court.

So, you want a resolution today (back-end resolution) with the money sent to UST, when it's a front-end resolution at the same time the funds were sent to UST, because it was not an actual dividend payment but a capital distribution under the guise of dividend, that we apply towards the exceptions to its restriction.

2nd. It's set forth in the FHEFSSA that you conceal, not in HERA. Because we can read how HERA inserted it in the FHEFSSA, the law in force along with the Charter Act.

3rd. The repayment of SPS isn't a "refinancing option". It's been explained that the EXCEPTION A that requires to raise cash in the same amount as the amount of SPS repayment, is achieved with the increase in the Common Equity in FnF, as the double-entry accounting means a posting of Cash/Total Comprehensive Income (Retained Earnings + OCI) in the Balance Sheet. This is what is contemplated in the Separate Account plan when FnF sent to UST the Net Worth increase. This is seen in the image of Freddie Mac below. So, it satisfies the intention of the lawmakers of raising cash in the same amount.

4th. You point out that the FHFA didn't activate this option of SPS repayment, because it hasn't been made public, when that's what the Separate Account is about: the FHFA-C's Incidental Power allows it to mislead about it, that is, to do it secretly (Take any action authorized by this section, in the best interests of FnF and the FHFA)

Remember that we are here to legalize every action, so we are forcing them to be legal without second-guessing and whether they want it or not. So, don't come out with what should have happened but with what has happened.

5th. Why on earth you are claiming that the controversial Bryndon Fisher has contemplated the repayment of SPS, when he advocates the payment of a 10% dividend and his claims are never backed up by statutory provisions, like this one U.S. Code §4614(e) and the one that supplemented it "...and shall not replace or affect the Restriction of Capital Distributions by statute") through regulation CFR 1237.12. He proposes a cattle market-style resolution counting on one's fingers: "You owe me X, I owe you Y. I add 2 goats and a cow and we are good!"

You have been explained all of the above a thousand times, but you don't care because you are here on a mission, like posting flawed analyses with your more than 20 different aliases, to make our heads spin and aming to tarnish other valid analyses.

Our negotiator adds dramatism once we enter unchartered territory.

Under the Separate Account plan, FnF weren't released upon Undercapitalized enterprises (mandatory release in the FHEFSSA struck by HERA: Core Capital > Minimum Leverage Capital requirement), nor when they met the threshold to resume the dividend payments (Table 8: Payout ratio. >25% of Prescribed Capital Buffer), for the sake of waiting for the JPS's fair value to fetch its par value, but FnF have continued to build capital thanks to the FHFA's Incidental Power (best interests of FnF and the FHFA) and now we are using as benchmark the threshold established by Calabria/Mnuchin in the January 2021 PA amendment, contending that there is no release until the CET1 > 3% of Total Assets.

If the February 16, 2021 ERCF requires Tier 1 Capital > 2.5% of Adjusted Total Assets, clearly that benchmark was overblown (Tier 1 Capital = CET1 + AT1 Capital -JPS-), for the only reason to encourage a swap JPS for Cs, and the assault on the ownership. It's ruled out.

This is why we must promote a more reasonable CET1 > 2.5% of Adjusted Total Assets as a new benchmark for the release, that would enable the redemption of JPS, which is suitable for the 2011 3-option Privatized Housing Finance System revamp (Basel framework) in the case that the Congress wanted that bigger players acquire FnF, and FnF would still meet Tier 1 Capital > 2.5% of Adjusted Total Assets in the ERCF.

We still don't know which of the 3 options has been chosen by the Congress for the Privatized Housing Finance Sytem revamp, chosen, in turn, by the UST as "recommendations on ending the conservatorships, no later than January 31, 2011", at the request of the Dodd-Frank law (the same law that imposed the annual Stress Tests)

Fannie Mae was lagging and it surpassed this threshold last week. So, now we are in unchartered territory, as there are no more reasonable thresholds to meet beyond this point that justify the lengthly conservatorship.

The dramatism is necessary to help our friends JPS holders suffering with a non-cumulative dividend stock. Although there are no victims as everything is legal with the FHFA-C's Incidental Power, their role of helping in the recapitalization of enterprises (Core Capital), authorized in their contract, can't be used and abused beyond what is strictly necessary. This is why the financial companies are managed by people with experience in Finance, not by attorneys.

Did I say unchartered territory? This is it!

MORE TWEETS BELOW. SCROLL DOWN.

Q3:TRACKING THE NUMBERS AT A CRITICAL JUNCTURE

— Conservatives against Trump (@CarlosVignote) November 5, 2023

▪️MISSED DIVIDEND(Table 8:Payout ratio)

Freddie Mac Equity holders:8 qtrs.

Fannie's,4 qtrs.

▪️RELEASE FROM CONSERVATORSHIP (CET1>2.5% of A. Total Assets, instead of Mnuchin's 3%)

FMCC:2 qtrs,3 days in overtime

FNMA:4 days.#Fanniegate https://t.co/lvoYVrqZOR

BV ($B) FMCC/FNMA:106/130

— Conservatives against Trump (@CarlosVignote) November 5, 2023

-1.2/19.5 Beginning bce 6/2008

+80/94 Acc Total Comprehensive Income, adjusted for these Accounting Change charges:

4/2009: 5/3

1/2010: -11.7/3.3

1/2020: -0.24/-1.1

+9.3/9 CRT,net(RE)

+18.7/6.8 PLMBS settlement:73%/27% based on AOCI in 6/2008.#Fanniegate https://t.co/EmZTYgahAE

NO INSTANT RECAP

— Conservatives against Trump (@CarlosVignote) November 6, 2023

"Return the stolen $" or "SPS repaid" by Howard(Berko's legal team)meaning "forgiven"(at the SCOTUS he said:"SPS,non-repayable securities")

Cumulative Recap through CET1>2.5% TA,so JPS are redeemed.

Plaintiffs liable for $4.8B in damages,feel the heat.#Fanniegate https://t.co/8RJbZCnVEK

Neither Howard refers to repayment but forgiveness, nor the dividends were actual dividends but assessments in the form of capital distributions under the guise of dividends (restricted and unavailable Earnings for distribution as dividends, out of an Accumulated Deficit Retained Earnings account) that we apply towards these exceptions to the Restriction on Capital Distributions in the law/CFR (Separate Account plan):

-Reduce the SPS. FHEFSSA (U.S. Code §4614(e))

-Recapitalization. CFR 1237.12.

Playing the fool is not an option.

No one in his right mind links W.Buffett with Fannie Mae.

Then, there is you, pro se plaintiff with your more of 20 different aliases, that can't stop lying and always pointing out the opposite of the reality.

Warren Buffett is known for having held an 8.5% stake in Freddie Mac that sold in 2000 after 15 years.

.png)

You post a link that looks like the reporter simply thinks that FnF are a single company.

And the day before, you posted another lie, stating that W.Buffett attempted to buy Fannie Mae "20 years ago when it was in trouble", which I assume it refers to the 2008 crisis. A lie because he wanted to buy its tax credits, not the stocks, jointly with his partner Goldman Sachs (Posted here)

Warren Buffett is always associated with Freddie Mac, and you just want to transmit the opposite idea. Why?

The elderly pro se plaintiff Joshua Angel talking again about being added to a "hate list" that I have created and that I hate people, when I'm just calling out all the conspirators that want to rip off the shareholders under the orders of the investment banks and hedge funds. It's not the first time that you mention it. It seems that you are very interested in being included in a list, so you can play the victim and attack me with that, instead of talking about financial matters.

Tell us how you are going to pay punitive damages to the Equity holders ($4.8 billion, the second round out of three, against the litigants and others with the Govt theft story in formal documents)

You can't put FnF in the same bag with other bailouts.

FnF are not ordinary businesses.

They have a UST backup embedded in their congressional Charter, in exchange for their risky Public Mission.

Now it's when you repeat again that FnF have to buy back the Warrant, like the banks, right?

All day with the Government theft story: "We've been robbed", for stock price manipulation.

Your boss Pagliara is very proud of you.

When Howard says "SPS repaid", he means "forgiven", because the SPS are obligations issued by FnF (debenture) and if it's cancelled, it's been forgiven. Because he doesn't mention how they were repaid, like I do with the assessments (capital) sent to UST quarterly, in the Separate Account plan backed up by statutory provisions. Now, we want that capital back, because it's held in escrow. The conservator's Incidental Power (take any action authorized by this section -Rehab-) allows it to hold the Common Equity in escrow, both through phony dividend payments to UST and the offset when the SPS LP is increased for free and for no reason, as of September 2019, and a one-time $3 billion on December 2017. So, there is no need to cancel the SPS if there are none in the Separate Account. Other theme is that in the current Balance Sheets, the gifted SPS are missing. Financial Statement fraud to avoid the "walk of shame" once the FHFA is compelled to unwind its plan that would show $-194 billion Core Capital today, and the same amount every quarter.

1st. Howard's stance is struck down right away. So, the UST took all their capital generated away, directly ($301 billion cash) and indirectly, through the gifted SPS ($121 billion) and, 15 years later there is a negotiation and it would claim that the debt has been satisfied. This isn't serious and can't be a bailout mechanism. Two guys seated at a table with a pencil and without any financial knowledge, talking about billions in FnF and counting on one's fingers. Maybe if FnF throw in a dozen of goats and a cow it's considered done faster.

2nd. Neither FnF are Zambia that need to have their debt forgiven, nor the UST will ever forgive a debt it's owed, just because Howard says so.

3rd. If the SPS are cancelled (forgiven), FnF would post a profit (core capital) but they would have to pay taxes on that profit. So, the capital wouldn't increase 1:1 as he claims.

4th. Funny that Howard says "SPS deemed to have been repaid", because he went to the Supreme Court as Court Amicus, to claim a dozen times that the SPS are "non-repayable securities" and conceal that the FHEFSSA allows the repayment of SPS as exception to the Restriction on Capital Distributions, which is what has happened. An Amicus brief that is the reason why he has to pay us Punitive damages (formal document)

He reminds me you, Glen Bradford, now cheering up when the common stock price rises one day. It seems that you think that we will forget all you've done in the past, with all your toxic SA articles bashing the common stocks and peddling the government theft story, accused of stock price manipulation.

Lie. Warren Buffett didn't try to buy FNMA but its tax credits.

Warren Buffett's Berkshire Hathaway Inc. has joined Goldman Sachs Group Inc. in the investment bank's bid to buy $3 billion in tax credits from government-owned mortgage giant Fannie Mae, according to people familiar with the matter.

He said he probably cost Berkshire Hathaway at least $5 billion by not buying Federal National Mortgage Association (also known as Fannie Mae) (FNMA, Financial) 20 years ago when it was in trouble.

Howard only knows stealing from private shareholder-owned enterprises, as proven in the 300-page OFHEO report when he was ousted from Fannie Mae in 2006 for Accounting fraud.

He talks about capital needs when there is still $7.4 billion Treasury Stock in the balance sheet reducing Equity and Core Capital in Fannie Mae. They are the stock buybacks to boost his EPS target bonus back then, hand-in-hand with the Accounting fraud he was accused of.

Surprisingly, in 2012 he was acquitted of civil charges by a DC judge (coincidence?) because there was no evidence that he had the intention to commit fraud. Huh?

I see 27 million reasons in this table:

I'm wondering whether his current blog about the Conservatorships was part of this kind of settlement with the DOJ, with the objective to rip off the shareholders and enrich the Treasury.

Besides, he should always disclose that he's a member of Berkowitz's legal team.

By the way, the Request for Input on pricing, was not about the Capital Rule and the Basel framework. It was about the recent LLPA changes.

$191 billion were the draws from Treasury (1:1 SPS)

The SPS can't be cancelled. They were repaid.

Our negotiator is opposed to a resolution today by two guys seated at a table, because the current Balance Sheets have nothing to do with the reality, instead of as a result of an ongoing Conservatorship that began in 2008 and in accordance with the law, that is, unwinding the Separate Account plan.

The key, in compliance with the FHFA-C's Rehab power: Put FnF in a sound and solvent condition. A statutory provision covered up in court by the plaintiffs, along with all others mentioned next.

You are negotiating with the government here, because the SPS can't be cancelled without a statutory provision backing it up and the Warrant can't be exercised. You are paid by the hedge funds, Glen Bradford, disregarding the laws and regulations, besides basic financial concepts:

I would be very happy if it was due to a release where the SPS were cancelled and only the warrants were exercised.

the FHLBanks have fulfilled their obligation to pay interests

Summary of a Taking + Resale scenario.

First of all, the JPS are redeemed at their par value after FnF surpassed the threshold CET1 > 2.5% of Adjusted Total Assets in the third quarter (Separate Account plan), which means that they'd meet Tier 1 Capital > 2.5% of the ERCF and the AT1 Capital (JPS) is no longer necessary.

Then, the common stocks are bought out at the BVPS (Price to BV ratio=1)

If there isn't a Taking, the existing shareholder takes the place of the Treasury Department in the table.

The prospective buyers acquire FnF at an effective PER 14x under a Privatized Housing Finance System revamp scenario (no TCCA fees/CRT expenses), although an increased price offered to Treasury reflects the value of the Deferred Income, net. Once the DI is amortized into Earnings in one fell swoop (Accounting Standard change of the upfront g-fee is necessary), it's a gift, so they can recover the increased price paid through a dividend, or it stays in the business.

Twitter thread: Prices and stock valuation in Q3.

Below, the same in Q2.

TAKING +RESALE +JPS REDEEMED:$349B PROFIT

— Conservatives against Trump (@CarlosVignote) November 3, 2023

+$14B extra Corp. Tax(Deferred Income)$FNMA/ $FMCC

Price;PER;BV;Mkt Cap

-Existing shareholder

$112/$164;6/7;1/1;$130B/$106B

-UST

$288/$388;15/16;2.6/2.4;$333B/$252B

-Buyer(Amortization of DI)

$273/$335;14/14;2.4/2;$317B/$218B#Fanniegate https://t.co/tbtoa5ax4v pic.twitter.com/dcp0KhYtu4

And quit posting statements:

"at least according to Mnuchin - SPS and JPS will be converted to commons together, in one go."

The BVPS of $FMCC rises to $164 from $159 under the Separate Account plan.

Common Equity = $106 billion.

The key: CET1=2.7% of Adjusted Total Assets, which means that the JPS can be redeemed and it would comply with Tier 1 Capital > 2.5% of Adjusted Total Assets in the ERCF.

After the JPS redemption, it'd have 67% of the Prescribed Capital Buffer, but it rises to 380% in the case of amortization into earnings of the Deferred Income in one fell swoop (Accounting Standard change necessary), because it holds a disproportionate amount.

🚨PER 14 times in Freddie Mac adjusted for the amount of damage award = $335, versus $312 in Q2, under a Privatized Housing Finance System revamp (no TCCA fees/CRT expenses, no Warrant and fully reserved against expected losses, that is, adjusted for Provision/Benefit for Loan Losses), proving that FnF have reported blowout numbers in Q3.

By the way, yesterday I didn't adjust the PER 14x of Fannie Mae, for the amount of damage award, here. It's $273 in Q3, versus $245 in Q2.

A cramdown doesn't take place after a cramdown.

A cramdown, which is like a bankruptcy, takes place with the picture of their Balance Sheets today. That is, with $311.8 billion SPS outstanding, including the ones that are missing.

And today's Net Worth is just $118 billion. The JPS are wiped out in a cramdown scenario.

You think that the JPS aren't affected by their awful financial condition shown today. All day with Happy emoji, Smile emoji, "Equity cash" by your buddy navycmdr, etc.

It's like holding JPS from different companies. Surreal.

"The JPS are mispriced (way too cheap),"

Bullet points: The BVPS rises to $112.

Figures adjusted for the Separate Account plan.

Common Equity= $129B.

The key: CET1 = 2.6% of Adjusted Total Assets (Leverage ratio). Remember that it was snubbed the threshold for the release from conservatorship of CET1 > 3% of Total Assets, established by Mnuchin/Calabria in the January 2021 PA amendment, 12 days before Sec.Yellen was sworn in and nocturnality.

But, watching that the ERCF requires Tier 1 Capital > 2.5% of Adjusted Total Assets, the threshold for release is considered ostensibly overblown, designed to encourage a swap JPS for Cs, and it was lowered to CET1 > 2.5% of Adjusted Total Assets, which means that once it's met, FnF can redeem the JPS, as they would be in compliance with the ERCF.

Tier 1 Capital = CET1 + AT1 (JPS)

Therefore, with CET1 = 2.6%, the JPS can be redeemed for cash and Fannie Mae would meet Tier 1 Capital > 2.5%.

The Common Equity is required for a Taking but, in a takeover, the fair value is a PER 14 times, plus the Deferred Income, net, if the Accounting Standard of the upfront g-fee is changed (a Delivery fee, instead of g-fee), as it would enable its amortization into earnings in one fell swoop.

PER 14 times = $255, reflecting the blowout numbers posted yesterday.

Other theme is that it may need further adjustments, as it's been captured a very good quarter that isn't representative of coming quarters, control premium?, forward PER?, etc.

$491mll expenses in phony damages, incl.,granted by J.Lamberth(Back divs, he told us👇),that will be recovered.

— Conservatives against Trump (@CarlosVignote) November 1, 2023

PER 14x =$255 (+DI,net,if that's the case), calculated (JPS redeemed):

Annualized adjusted Q3 EPS

No TCCA fees/CRT expenses

No provision for loan losses(Fully reserved) pic.twitter.com/FIEjTtYTwZ

The JPS aren't part of the Net Worth amount, which is what Louie_Louie was referring to here:

Show us current accounting that proves 33B is part of the current capital quoted (the 110B retained)

stockholders’ equity

No. This payment of Securities Litigation judgment CANNOT be paid.

It's a capital distribution per FHFA rulemaking and therefore, restricted in the Restriction on Capital Distributions of the FHEFSSA, when FnF are undercapitalized.

Explained here.

It's evidence of a sham trial and litigation rigged by the parties, the DOJ included, because it would unveil the Separate Account plan, as the dividend payments and today's SPS LP increased for free every quarter are also capital distributions restricted, and the FHFA has been using the exceptions instead: reduce the SPS and Recapitalization outside their balance sheets, under the guise of dividends.

The FHFA and the hedge funds are obsessed with becoming a corrupt organization. But we will make all their actions lawful, whether they want it or not.

This shows that Wise Man was wrong to claim that the Lamberth damages cannot and will not be paid.

Our negotiator refuses to comment about the Earnings report and calls on the S.E.C. to compel the company to restate it, after it's been spotted a charge equal to "$491 million of expense attributable to a jury verdict and an award of prejudgment interest".

Zero consideration to:

1- The absence of judgment which is when the verdict takes effect,

2- The Restriction on Capital Distributions in the FHEFSSA, as the FHFA determined in the July 20, 2011 Final Rule, that the payment of Securities Litigation judgments is a capital distribution and thus, restricted (just like dividends and today's gifted SPS)

3- Let alone that the plaintiffs haven't submitted yet to court the amount of interests requested, expected on November 7th.

It will backfire: evidence that everything is rigged by the parties.

https://twitter.com/CarlosVignote/status/1719349945436651628

⚠️Attention to the figures adjusted for the Separate Account plan.

The only plan that legalizes every action.

1st. A cash refund of the amount due (Latest: $77.2 billion): SPS overpayment + CRT expenses, net + PLMBS lawsuit settlement (27% of total, based on its AOCI as of June 30, 2008, in comparison to Freddie Mac. The unrealized losses prompted by these PLMBS sold with fraudulent information and the mispricing in general)

2nd. The funds sent to UST were assessments under the guise of dividend payments, applied towards the reduction of SPS and Recapitalization outside their balance sheets, because they are the exceptions to the restriction of these capital distributions, besides no dividend was ever possible with Accumulated Deficit Retained Earnings account (adjusted $-216B FnF together, June 2023). Therefore, this Common Equity sent to UST (Total Comprehensive Income) is considered to have been held in escrow all along, and it needs to be recorded now as such on the Balance Sheet, with a posting on the Retained Earnings account.

We also take the opportunity to retire the Treasury Stock (stock buybacks to boost Howard's EPS target bonus) that currently is reducing the Net Worth and regulatory capital, which would reduce the Retained Earnings account.

The PLMBS lawsuit settlement, plus the refund of the CRT expenses, net, boost the Retained Earnings account.

Latest posting: $124.5 billion.

🚨Focus on the new threshold for the release from conservatorship of CET1 > 2.5% of Adjusted Total Assets, instead of Mnuchin/Calabria's CET1 > 3% of Total Assets in the January 2021 amendment of the PA. It translates into an authorization to redeem the JPS, as the ERCF requires a TIER 1 Capital > 2.5%. So, if you meet CET1 > 2.5%, you meet TIER 1 Capital > 2.5% and the JPS (AT1 Capital ) are no longer necessary.

TIER 1 Capital = CET1 + AT1

It's estimated that, under the Separate Account plan, Fannie Mae was just $1 billion short of this threshold, as of June 30, 2023.

The Common Equity is used to calculate the BVPS required in the case of Taking by the UST.

Otherwise we would be talking about PER 14 times, plus the value of the Deferred Income, net, in the case of Accounting standard change, because currently this income already collected is in limbo (recorded as Debt), instead of Net Worth.

Beware of the internet trolls with happy, smile emojis to provoke us, like "Hi Rum!" commodore stating that FnF are retaining earnings without adjusting the figures, because that's not the reality concealed with Financial Statement fraud in FnF (gifted SPS absent from the balance sheets)

Or Bradford, stating that the $301 billion sent to UST is gone. That doesn't rehabilitate FnF (prerequisites from Justice Alito and judge Willett), but the opposite. Today FnF are in the worst financial condition ever.

Anyone can purchase those loans. That's why the g-fee was increased, so FnF compete with the fully private sector on a level playing field.

This was explained in 2011 as part of the "recommendations on ending the Conservatorships". A report to Congress.

You should read more and write less.

Who do you think will buy the "affordable housing" loans once the lender has made the sale to the residential customer - and then Who is large enough to package the MBS if this is a Govt sponsored program ?

I've laid out what the Warrant was meant to do, according to what is written in the prospectus. Related to a Housing Finance System revamp through the assault on the ownership of FnF by Wall Street and the Community Banks, paying nothing.

Just read it and don't ask why.

Why would the government give up on up to $100 billion?