Thursday, November 02, 2023 2:40:06 AM

"The JPS are mispriced (way too cheap),"

Only if the business goes on, they are undervalued today in the scenario of Govt theft story of the conspirators.

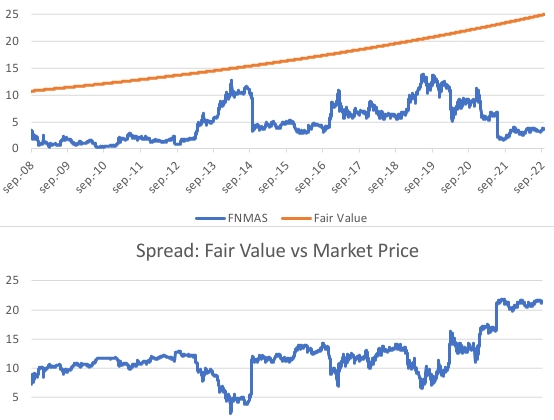

For instance, the $25 par value JPS series of Fannie Mae FNMAS is trading at 9% of par value ($2.16), when its fair value today is 39% of par value ($10), discounting 16 years to resume the dividend payments (Table 8: Payout ratio. >25% of Prescribed Capital Buffer) with the current adjusted capital metrics posted in their ERCF tables, which is when the fair value fetches the par value. So, like any zero coupon fixed-income security, they are trading at a discount to par value. I've considered a 6% discount rate.

But, this fair value will always be 39% of par value, because with the SPS increased for free every quarter, there will always be 16 years left to meet the capital requirements or this threshold of dividend resumption (Groundhog day every quarterly report), as these gifted SPS carry an offset that reduces the Retained Earnings just built (concealed with Financial Statement fraud in FnF: the gifted SPS and their offset are missing on the balance sheets)

So, FNMAS will always trade undervalued.

BACK TO THE FUTURE

Your gang wants to take us back to 2008, when the Fair Value of FNMAS was also $10, as we see in the image that represents the Separate Account plan according to the law that states that Fannie Mae has been repaying the SPS and recapitalizing through today, the threshold for resumption of dividend payments was met with the 3Q2022 earnings report.

It coincides with the image of a normal Conservatorship in cogressionally-chartered private corporations, because it brings to the surface the separate account.

That is, the gang wants now a Receivership, because that's the option that they would have wanted in 2008, instead of Conservatorship.

Sorry, but we are 15 years into a Conservatorship, you can't undo what's already been done and the time for release has come.

Even FnF can redeem the JPS and remain Adequately Capitalized with a CET1 > 2.5% of Adjusted Total Assets as of September 2023, under the Separate Account plan.

So, you are throwing stones at your own roof in an attempt to rip off the shareholders and for stock price manipulation, following orders from renowned hedge fund managers, Glen Bradford "the hippie".

You have caused us harm (spread Fair Value vs Market Price, seen in the image) and, because you have written SA articles (formal document) with the Govt theft story, now you have to pay us punitive damages.

Glidelogic Corp. Becomes TikTok Shop Partner, Opening a New Chapter in E-commerce Services • GDLG • Jul 5, 2024 7:09 AM

Freedom Holdings Corporate Update; Announces Management Has Signed Letter of Intent • FHLD • Jul 3, 2024 9:00 AM

EWRC's 21 Moves Gaming Studios Moves to SONY Pictures Studios and Green Lights Development of a Third Upcoming Game • EWRC • Jul 2, 2024 8:00 AM

BNCM and DELEX Healthcare Group Announce Strategic Merger to Drive Expansion and Growth • BNCM • Jul 2, 2024 7:19 AM

NUBURU Announces Upcoming TV Interview Featuring CEO Brian Knaley on Fox Business, Bloomberg TV, and Newsmax TV as Sponsored Programming • BURU • Jul 1, 2024 1:57 PM

Mass Megawatts Announces $220,500 Debt Cancellation Agreement to Improve Financing and Sales of a New Product to be Announced on July 11 • MMMW • Jun 28, 2024 7:30 AM