Sunday, November 12, 2023 11:12:16 AM

"Less than $10 — these are cheap."

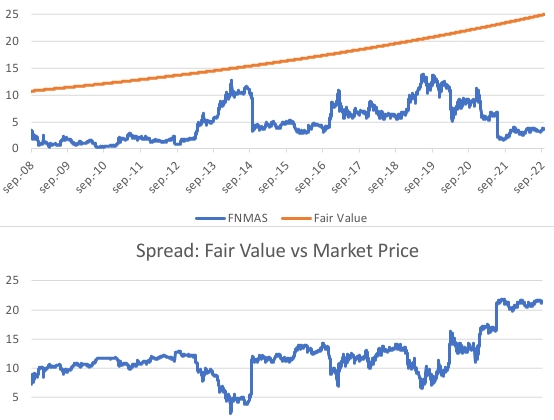

Your insinuation that $10 is the true fair value of FNMAS today, just because I said so a few days ago, here, is repulsive, because it assumes that the current Balance Sheet is for real and the Conservatorship starts all over again from scratch today, as it's a fair value that discounts the 16 years left to resume the dividend payments at a 6% discount rate, under the Table 8: Payout ratio, and the Restriction on Capital Distributions in the law (U.S. Code §4614(e)), the two key elements covered up by the plaintiffs and company all along.

A do-over of the Separate Account plan, but now, made public. So, the same chart, as a Separate Account plan is an actual Conservatorship concealed with tricks taken from the law and others added up through regulation, like the CFR1237.12 in 2011, aiming to misrepresent their financial condition.

Sorry, but we are not in 2008 again when FNMAS had a fair value of $10 as well, but 15 years into a Conservatorship under a Separate Account plan and the fair value of FNMAS fetched its par value with the 3Q2022 Earnings report, one year ago exactly. Now, both FnF are continuing to build capital buffers beyond the 25% of Prescribed Capital Buffer that marks the resumption of dividend payments, when FNMAS fetched its par value mentioned before (Table 8. Capital Rule), authorized under the FHFA-C's Incidental Power.

It turns out that its CET1 was 2.6% of Adjusted Total Assets as of end of Q3 and, because the ERCF requirement is Tier 1 Capital > 2.5% of Adjusted Total Assets, Fannie Mae can redeem the JPS and it would still meet the Tier 1 Capital mentioned.

Tier 1 Capital = CET1 + AT1 (JPS)

Glidelogic Corp. Becomes TikTok Shop Partner, Opening a New Chapter in E-commerce Services • GDLG • Jul 5, 2024 7:09 AM

Freedom Holdings Corporate Update; Announces Management Has Signed Letter of Intent • FHLD • Jul 3, 2024 9:00 AM

EWRC's 21 Moves Gaming Studios Moves to SONY Pictures Studios and Green Lights Development of a Third Upcoming Game • EWRC • Jul 2, 2024 8:00 AM

BNCM and DELEX Healthcare Group Announce Strategic Merger to Drive Expansion and Growth • BNCM • Jul 2, 2024 7:19 AM

NUBURU Announces Upcoming TV Interview Featuring CEO Brian Knaley on Fox Business, Bloomberg TV, and Newsmax TV as Sponsored Programming • BURU • Jul 1, 2024 1:57 PM

Mass Megawatts Announces $220,500 Debt Cancellation Agreement to Improve Financing and Sales of a New Product to be Announced on July 11 • MMMW • Jun 28, 2024 7:30 AM