Donald Trump has given Paul Krugman a ‘Fake News Award’ – but did the economist really get it so wrong?

"The Myth of the ‘Trump Miracle’"

Krugman’s prediction was just that: a prediction. If it was reported, then it should have been reported with the usual caveats attached to all economic forecasts, predictions and received bits of wisdom

Sean O'Grady @_seanogrady Thursday 18 January 2018 14:21 GMT

Krugman predicted that the stock market would crash on a Trump victory Getty

I have no doubt, for example, that the top Fake News “Oscar” – maybe we should call it a Trumpscar? – that went to the distinguished economist Paul Krugman was a “fake” award. Krugman, it is perfectly true, predicted that the stock market would crash on a Trump victory. In fact it is up about 30 per cent in the year since Trump took over, one of its better performances in history. Still, Krugman’s prediction was just that: a prediction. If it was reported, then it should have been reported with the usual caveats attached to all economic forecasts, predictions and received bits of wisdom. Of these, by the way, my favourite is the wisecrack that “economists have predicted 10 out of the last three recessions”, or variations thereof. The deflationary effect of that on any professional economist’s ego is usually entertaining to behold.

Krugman himself, professor, Nobel prize winner and brilliant mind, took to Twitter, appropriately, to make light of it and indulge in a little satire of his own; “I get a ‘fake news award’ for a bad market call, retracted 3 days later, from 2000-lie man, who still won’t admit he lost the popular vote. Sad!”

[VIDEO] - Donald Trump has announced the winners of his ‘Fake News’ awards

It is worth mentioning a couple of other economicsy things. First, the US stock market and Donald Trump are not what an economist would term “independent variables”. By which I mean the fact is that President Trump’s words, policies and actions can actually move the stock market – and indeed they have. The Trump tax reforms basically mean a bonanza for corporate America as profits previously parked offshore anywhere from the Cayman Islands to Switzerland for fear of the US Internal Revenue Service can now be “repatriated”. Only this week, Apple for example announced the cashing out of $250bn (£180bn) from its overseas tax havens.

When such funds do get back to America a fair slice will be paid out to shareholders in those big companies, maybe via some juicy special dividends, and the anticipation of that that makes those shares more attractive and pushes their price higher. Plus Trump has a more pro-business approach generally than his predecessor.

Second, Trump’s decision to let rip on oil exploration and ditch all the green stuff has been excellent news for shares in energy firms.

Third, we have the expansionary effect of the (even) bigger budget deficits the US will probably run under the Trump administration which – in true Keynesian style, as Professor Krugman would well understand – will boost economic growth and thus corporate revenues and profitability.

Last, no one should rely on stock market indices as evidence of very much at all. For the stock market will, sooner or later, “correct” itself (that is a safer prediction than most, by the way, as it always does). That doesn’t mean capitalism is finished or that the US economy is suddenly busted. It does mean that those who use the Dow Jones, the Nasdaq or any other index as their sole guide to the health or otherwise of the US economy – as Donald Trump so often does now – are rather foolish, because it is a rather capricious beast and you can end up looking very silly if it moves in the “wrong” direction. In that respect, if no other, the stable genius Professor Krugman and the fake stable genius President Trump have one genuine mistake in common.

Why Trump Is Probably to Blame for the Weak Dollar

"The Myth of the ‘Trump Miracle’"

According to the Mercury and Mars hypothesis of currency choice, "America First" hurts the American currency.

by Leonid Bershidsky

January 6, 2018, 2:32 AM GMT+11

Worth less these days. Photographer: Sanjit Das/Bloomberg

President Donald Trump keeps bragging about the stock index gains since his election. He did so ..

Dow goes from 18,589 on November 9, 2016, to 25,075 today, for a new all-time Record. Jumped 1000 points in last 5 weeks, Record fastest 1000 point move in history. This is all about the Make America Great Again agenda! Jobs, Jobs, Jobs. Six trillion dollars in value created!

.. again on Friday, claiming he'd helped create "six trillion dollars in value." Be that as it may, it's also likely that Trump is at least partially responsible for the dollar's weak performance in 2017, which, from an international perspective, wiped out much of that "value."

Last year, the U.S. dollar lost 10 percent against the euro and 5.5 percent against the renminbi. It was the second worst performer among major currencies after the New Zealand dollar, and its drop was the steepest in more than a decade despite three interest rate hikes and the passage of Trump's tax reform, which could logically be expected to drive the dollar's value upward. This happened for a complex set of reasons which may include the dollar's popularity as a funding tool .. https://www.bloomberg.com/news/articles/2018-01-05/global-credit-merry-go-round-may-solve-weak-dollar-conundrum .. for foreign companies and governments, but Trumps's effect on his country's global standing must be a key driver of the dollar's decline.

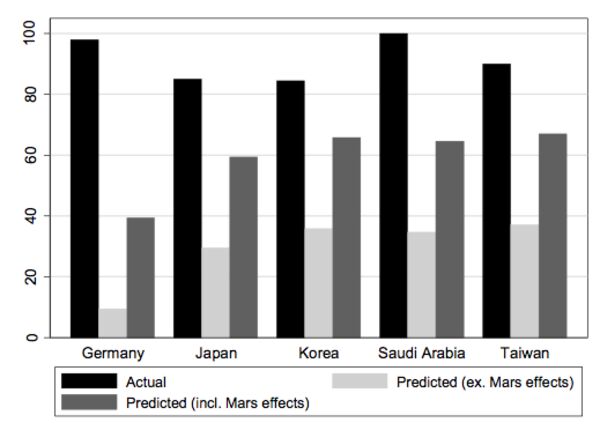

In a 2017 paper .. https://www.nber.org/papers/w24145 , Barry Eichengreen of the University of California, Berkeley, and Arnaud Mehl and Livia Chitu of the European Central Bank developed a "Mercury and Mars" hypothesis about the value of reserve currencies. They wrote that there are two sides to a currency's appeal. The Mercury side is economic: It's all about safety, liquidity, network effects and economic connections. The Mars side is geopolitical: It reflects the issuing country's strategic, diplomatic and military power.

The researchers attempted to quantify this duality by looking at the composition of nations' currency reserves. They found that as long ago as between 1890 and 1913, countries were more likely to hold reserves in the currencies of their defense pact partners, even when purely economic choice would have dictated otherwise. The same is still true, with a nuclear-era twist. Nations such as Japan and South Korea, dependent on the U.S. for security, hold a greater share of reserves in dollars than France, Russia or China, which possess their own nuclear deterrent. Eichengreen, Mehl and Chitu developed a model to predict the composition of countries' foreign reserves with and without the "Mars effect" and found that for America's security dependents, the actual share of dollar holdings (shown on the chart below) was always higher than the model's highest predictions:

Eichengreen and collaborators argued that the dollar's "security premium" accounts for a significant part of its attractiveness as a reserve currency. Losing it would mean a 30 percentage point reduction in the share of U.S. currency in nations' reserves. Isolationist "America First" policies would certainly seem to undermine the "security premium." Einchengreen, Mehl and Chitu wrote:

---- The dollar’s dominance as an international unit is buttressed by the country’s role as a global power guaranteeing the security of allied nations. If that role were seen as less sure and that security guarantee as less ironclad, because the U.S. was disengaging from global geopolitics in favor of more stand-alone, inward-looking policies, the security premium enjoyed by the U.S. dollar could diminish. Our estimates suggest, in this scenario, that $750 billion worth of official U.S. dollar-denominated assets – equivalent to 5 percent of US marketable public debt – would be liquidated and invested into other currencies such as the yen, the euro or the renminbi. ----

All year, the Trump administration has blown hot and cold on its commitment to alliances, to the point that any assurances it makes today can't be taken at face value. Trump's quick temper and his willingness to play the "whose nuclear button is bigger" game haven't helped bolster the U.S. reputation as a security guarantor. The constant leaks pointing to Trump's incompetence, such as the new Michael Wolff book, appropriately titled "Fire and Fury," also detract from the dollar's reputation as a safe asset.

No wonder its share of global foreign exchange reserves, as reported .. http://data.imf.org/?sk=E6A5F467-C14B-4AA8-9F6D-5A09EC4E62A4 .. to the International Monetary Fund, stood by the end of the third quarter of 2017 at the lowest level since the middle of 2014. It declined throughout the first three quarters of last year.

That share still stands at 63.5 percent, dwarfing other reserve currencies. Central banks hold $6.13 trillion. It would take many years or even more drastic shake-ups to destroy both the "Mercury" and the "Mars" advantages of the U.S. juggernaut. But the slight shift in favor of other currencies reflects a perception that making bigger bets on the U.S. might be unsafe. That's likely one of the motives behind other reserve currencies' exchange rate gains relative to the dollar.

Trump, of course, has spoken out in favor of a weak dollar because it helps trade competitiveness. But the U.S. currency is not weakening because of any consistent policy. On the contrary, it's Trump's loose cannon behavior that's undermining it. An unhinged Mars is beating up Mercury in a fit of fire and fury.

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

To contact the author of this story: Leonid Bershidsky at lbershidsky@bloomberg.net

To contact the editor responsible for this story: Therese Raphael at traphael4@bloomberg.net

Trump also, of course, speaks in favor of a stronger dollar.

Dollar rallies off a 3-year low in sudden reversal after Trump says it will get 'stronger and stronger'

* The dollar erased its losses and went positive after President Trump said Treasury Secretary Steven Mnuchin's remarks about a weak dollar being good for the economy were taken out of context.

* Mnuchin kicked off a two-day 2 percent decline in the dollar index when he made the remarks at the World Economic Forum in Davos, Switzerland Wednesday.

* By Thursday, Mnuchin tried to backtrack the comment by saying his comments were no different than in the past, but the market read it as a change in the long term U.S. policy to back a strong dollar.

It’s a sure thing that Donald Trump will spend much of his State of the Union boasting about the economy. So this seems like a good time for a refresher on some basic macroeconomics – and the reasons why the expansion of 2017, which continued the long expansion that began in 2010, is in no sense a justification for wildly optimistic growth projections looking forward.

As a reminder, the Trump Treasury department claims that tax cuts will pay for themselves because the economy will grow at almost 3 percent .. https://www.nytimes.com/2017/12/11/us/politics/treasury-tax.html .. a year for the next decade. This growth projection didn’t come from any model; it was just pulled out of … well, you fill in the rest. But every time there’s a good quarter of growth, the usual suspects take time off from talking about deep state conspiracies to claim that the forecast is coming true. Why is this nonsense?

First, you need to know that quarter-to-quarter and even year-to-year growth rates are very variable. The economy grew at a 5 percent annual rate during much of the Carter administration (how many people know that?); it grew around 4 percent during the second Clinton administration:

What’s behind these growth fluctuations? The business cycle. Potential output – the economy’s productive capacity – grows fairly smoothly. But recessions leave some of that capacity idle, and the economy can temporarily grow fast as that capacity is put back to use. The unemployment rate is an imperfect measure of idle capacity; still, there’s a strong relationship – Okun’s Law – between changes in the unemployment rate – capacity going into or out of use – and short-run economic growth.

The thing is, however, that we’re currently close to full employment. The unemployment rate is historically low. Other indicators, like the rate at which workers are quitting jobs (a sign of how confident they are of finding new jobs) also point to a more or less full employment economy. Wage growth and inflation are still subdued, but it’s still unlikely that unemployment can fall a lot from here. This means that growth over the next decade will have to come from rising capacity, meaning growth in potential output.

So is there any sign that potential output growth is anywhere near 3 percent, or in fact that it has accelerated? No. Here’s Okun’s Law for the past decade:

The relationship isn’t perfect, because this is economics, but it’s pretty strong. It suggests a potential growth rate – growth consistent with constant unemployment – of maybe 1.5 percent. And 2017 isn’t an outlier.

Why is potential growth so low? Unfavorable demographics are one big culprit: the baby-boomers are getting old (you kids get off my lawn), so the working-age population is barely growing. Oh, and cracking down on immigration is, you know, not likely to help on that front.

Productivity growth is also lackluster, despite all the hype about robots and all that.

So if you think about it, 2017 offers no evidence to support big talk about future growth. On the contrary, the fact that unemployment declined despite not-so-fast growth is a sign that growth will be a lot slower going forward, now that we don’t have a lot of unemployed Americans to put back to work.

If you weren't thinking of the "immigration" point Krugman slipped in before you read it then you may be only thunking as Trump does on so many policy questions.

A massive change in perceptions masks continuity with the Obama years.

By Matthew Yglesias@mattyglesiasmatt@vox.com Jan 30, 2018, 9:00am EST

[...]

More broadly, whether you want to characterize current economic trends as fantastic or terrible (I prefer, “They’re okay”), they simply aren’t very different from the trends we saw under Obama. In the fourth quarter of 2017, the economy grew 2.5 percent relative to where it had been a year ago. That’s better than what we saw in 2016 or 2015 but worse than what we got in 2014 and 2013. It’s also considerably lower than the 3 percent average annual growth he promised in his official budget submission, which in turn was lower than the 4 percent average annual growth he touted on the campaign trail. It’s also slightly worse than Canada or Mexico did last year.

Perhaps the clearest indication that we’re looking at a continuity recovery is a glance at annual job growth, which was decent under Trump but reflected an ongoing slowdown rather than an acceleration.

That’s not Trump’s fault.

Job growth slowed in 2017 for the same reason it slowed in 2016 — the closer we get to a full-employment economy, the fewer unemployed workers there are out there to easily rehire. But if Trump had actually delivered some kind of game-changing supply-side transformation of the American economy, he wouldn’t be stuck with that slowdown. He’s presiding over the same “steady as she goes” demand-side recovery that Obama had for his second term, and that should really be no surprise, since the Federal Reserve has remained in the same hands.

[...]

The United States is the only high-income country to have millions of citizens who lack health insurance, has a relative child poverty rate that’s off the charts by the standards of other developed countries, has no guaranteed paid parental leave or paid vacation, and remains one of the world’s highest per capita emitters of greenhouse gases even as the world hurtles toward an environmental crisis. Under those circumstances, efforts to pitch the notion that “America is already great” end up falling flat not just — or even especially — with skeptical swing voters but with Democrats’ own base that yearns for transformative change to aspects of the American welfare state and of American political economy.

Market Data

Market Data  Markets

Markets

/cdn.vox-cdn.com/uploads/chorus_asset/file/10115701/Screen_Shot_2018_01_29_at_11.01.29_AM.png)

/cdn.vox-cdn.com/uploads/chorus_asset/file/10115737/Screen_Shot_2018_01_29_at_11.08.29_AM.png)