No reasonable person blames MW and SG for securing a bright future for us while under a Gag Order from their successful mediation. Of course they can't reveal everything. I'm a big picture guy and have always read between the lines thru this BK BS.

I disagree. According to filings and court actions.

JPM does not hold these WMB mortgages they service them for the FDIC-R.

See the court filings.

JPM’s Motion for Summary Judgment in a case filed against it and the FDIC by Deutsche Bank in the District of Columbia Federal Court, where JPM admits that it was NOT the “successor in interest” to WaMu

Also, the Receiver must resolve a number of indemnity claims made by JPMC. JPMC has submitted over 35 notices of potential indemnity claims. (Notices can be found at JPMorgan Chase Notices relating to Washington Mutual Whole Bank P&A in the Freedom of Information Act (FOIA) Service Center Reading Room). Some of these claims for indemnification will be resolved through the implementation of the settlement, but many will not. In addition, JPMC has until September 2014 to provide the Receiver with notice of additional potential indemnity claims. Should the Receiver be found liable on any of JPMC's indemnity claims, under the P&A, those claims will be satisfied as administrative expenses and thus before the claims of general unsecured creditors. Current information indicates that the Receiver is unlikely to have sufficient funds to distribute to holders of receivership certificates issued to junior note holders or equity holders of WAMU.

Sept 2014 JPM must file all claims by this date. Per the FDIC website.

Both JPMC and the FDIC have acknowledged that the Repurchase Obligations are ongoing; indeed, they contend (incorrectly) that the Repurchase Obligation depends upon how the breach of Representation or Warranty impacted the mortgage loan after securitization.

See page 39

Indeed, other Courts have read Section 2.5 and Section 2.1 of the PAA together to “allocate [WaMu’s] lender liability to the FDIC and . . . transfer [WaMu’s] servicing liability to[JPMC].” Johnson v. Wash. Mut. , No. 1:09-CV-929, 2010 WL 682456, at *4 (E.D. Cal. Feb. 24,2010) (quoting In re Pena,409 B.R. at 861); see also Hayes-Broman v. J.P. Morgan Chase Bank,724 F. Supp. 2d 1003, 1015 (D. Minn. 2010) (adopting the reasoning of Johnson and Pena);Punzalan v. FDIC, 633 F. Supp. 2d 406, 409-10 (W.D. Tex. 2009) (“Chase Bank purchased Washington Mutual on the condition that FDIC remain responsible for any ‘Borrower Claims’ . .. in connection with Washington Mutual’s lending or loan purchase activities. In exchange . . .Chase Bank promised to assume responsibility for all other liabilities, specifically including all mortgage servicing rights and obligations of [Washington Mutual].”) (internal quotations omitted).

Case 1:09-cv-01656-RMC Document 56 Filed 01/14/11 Page 39 of 54

See page 40

To the extent there is any ambiguity, the recently filed Examiner’s Report in the Washington Mutual, Inc. bankruptcy proceedings supports the FDIC’s argument that the parties intended to transfer the liabilities.

See page 52

Neither the FDIC nor JPMC dispute that the Governing Documents, which provide for the sale of an interest in a mortgage loan in the secondary market as well as the repurchase of a loan, constitute qualified financial contracts pursuant to 12 U.S.C. § 1821(e)(8)(D)(i).

35

AC ¶¶26, 29, 31-34. 12 U.S.C. § 1821(e)(8)(D)(i). FIRREA provides that “n making any transfer of assets or liabilities of a depository institution in default which includes any qualified financial contract, the conservator or receiver for such depository institution

shall . . . [transfer]

all

qualified financial contracts between any person . . . and the depository institution in default . . .

or transfer none

of the qualified financial contracts.” See 12 U.S.C. § 1821(e)(9) (emphasis added). Having assumed, and not repudiated, all of WaMu’s rights under the Governing Documents in order to sell them to JPMC, the FDIC now must cause WaMu’s obligations under those same Governing Documents to be performed or pay damages in lieu thereof. See Sharpe,126 F.3d at 1155-57; Deutsche Bank, No. 09-3852, at 11-14

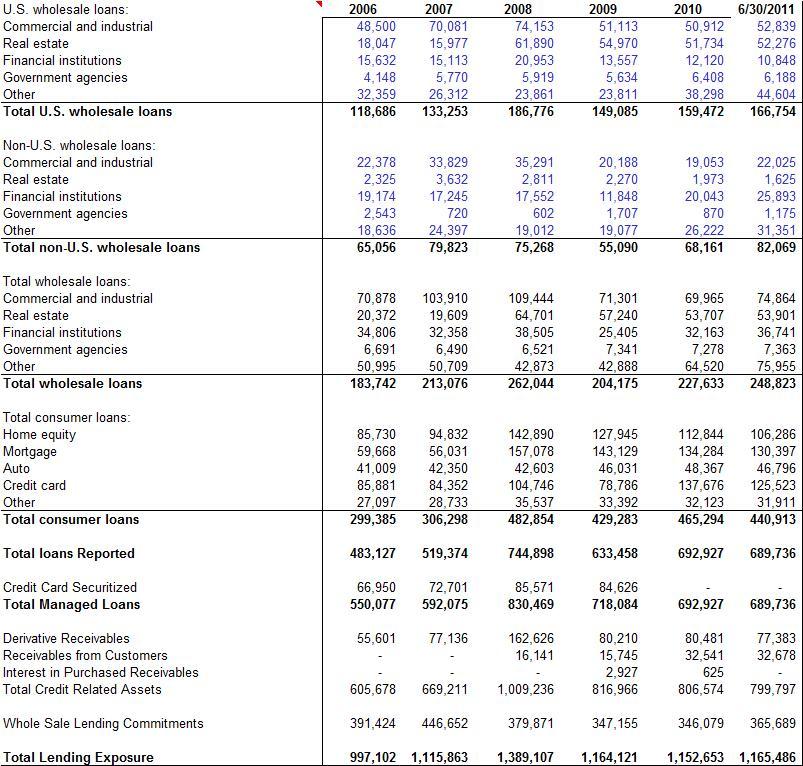

You're talking about a net increase of $225,823M in loan value from 2007 to 2008.

The increase you come up with is INCLUDING WHOLESALE LOANS. As we all know those are NOT considered PORTFOLIO LOANS!

Look at this one, one more time:

If we look at consumer loans (after all that's where we are talking about, loans in PORTFOLIO and NOT the WHOLESALE loans) the net resulting difference is only:

482B minus 306B=176B

Look further and you'll see 20B of this difference is explained by an increase of 20B in credit card loans (which mostly comes from WaMu).

176B minus 20B= 156B difference

Of which 81B is coming from WaMu (in the form of the so called PCI loans, see below)

81B is the combined total of PCI loans in 2009 (vs. 69B in 2011).

As I explained in my previous post these PCI loans, which are pooled together and accounted for on a separate basis, are coming from WaMu through FDIC receivership.

81B in 2009 reported by JPM vs. 244B in 2007 reported by WaMu.

Let that sink in for a moment...

You're telling me 244B in assets from 2007 is devalued to a mere 81B in 2009?

I'm not gonna believe that.

What I do believe, purely by breaking down the numbers from the PCI loan breakdown, JPM took over half of the home equity loans, and almost all prime and subprime mortgages from Wamu. But no mention whatsoever about the home loans!!!

110 billion just went poof on the books.... Some shady accounting here.....

JPM doesn't have them on the books (PCI loans don't exceed 81B).

FDIC doesn't either.

WMI LT doesn't either.

OK those were the COLD HARD FACTS...

Now for some fun:

Someone is holding back assets!!

Can you say SMOKING GUN?

"It's all over"

"He could have gotten more" (about Susman)

Susman and EC got air of this, and confronted Walrath AND Rosie with these assets that were held back. All this on a beautiful day in 2011, in Walrath chambers, with only those three people present.

IMO Susman did them a huge favor for the sake of their professional careers, by discussing it in chambers and not on the record! Think and ponder about that one for a bit....

That's why their faces, according to eye witness records, saw a little bit scared and white. Can't blame them right?

Which made EC's seats on the mediation table very comfy.

Hedgies had the opportunity to walk away from murder, while caught in the act to sell the body for organs, but had to return their stolen house and 2/3 of the money on their bank account.

Sounds like a good deal. Hedgies don't go to jail, got a bit for their PIERS, and escrows make BIG FAT MONEY.

That's why PIERS were deemed popular just before reorganization.

That's also why buying of commons and preferred went on in big volumes even after the voting deadline with the ultimate risk to end up with shares you cannot sell (and haven't been sold!!)

That's why escrows are IMHO...

...BWTFDIK....

where the big money sits!

Case closed.

PS. I can post only once daily, so gotta make em count I guess ;)

but I do not understand why any so called legacy mortgages would not be offset by deposit liabilities --- unless this is some MASIVE retained earnings no one used to salvage the bank

Modern Lending for BIGGY Banks

WaMu takes in 250B in deposits WaMu issues 240B in mortgages (loans secured by mortgage) (some amount less then the 250 for reserves - no math done)

WamU for years until PLMBS paper - to make new loans sells the obligations to itfor principal and interst to F or F and gets cash back. At that point it does not not own the mortgages any more

This is done over and over

At any given time WaMu holds either a ton of cash From F or F or a ton of mortgages

Wamu also holds a small capital reserve

Capital Reserve plus cash if just sold mortgages assuming its bulk)plus some profit in small percent = deposit obligation to the people who bank at WaMu

If not recent swap with F and F then WaMu holds mortgages with value = to deposits

If WaMu went PLMBS then again it sold the mortages to investors for cash = some profit some reserve and deposit obligations and does not own mortgages

Over time a profitable bank can own mortgages or cash from profit in retained earnings. But even the FDIC on its worst day would not close Wamu if it had good reserves with good Morgages or cash

Market Data

Market Data  Markets

Markets