Friday, January 16, 2026 9:09:48 AM

Netflix And Its Real Value

Jan. 16, 2026 4:12 AM ETNetflix, Inc. (NFLX) StockNFLX:CA

https://seekingalpha.com/article/4860420-netflix-real-value

Grant Gigliotti

Investing Group Leader

Summary

Netflix demonstrates strong fundamentals, with robust global scale, high ROE, and consistent margin expansion despite recent acquisition-related uncertainty.

Recent merger speculation with Warner Bros. Discovery (WBD) has pressured NFLX’s share price, but core operations remain resilient and cash flow positive.

NFLX trades below its historical PE range and intrinsic value estimates, suggesting the stock is currently undervalued relative to long-term growth prospects.

This article focuses on the fundamentals, the real value versus the current share price, and if NFLX is currently worth investing in.

Netflix, Inc. (NFLX) is a broadly known worldwide entertainment corporation and the most well-known subscription-based streaming platform, which incorporates a diverse variety of original and licensed movies, documentaries, and live shows. Netflix has been at the center of the reinvention of media consumerism. With its operational location in over 190 countries, it is considered among the largest streaming services globally and has a powerful competitive edge in its size, its distribution potential, its originality, and its data-driven personalization power.

Investors are concerned with more than subscriber growth and margins at Netflix. The recent events related to a potential merger with Warner Bros. Discovery (WBD) have increased the uncertainty regarding Netflix’s strategic forecast, spawning legal issues, shareholder doubts, and valuation discussions. Although the management has focused on trusting the transaction and the long-term advantages of this decision, issues related to regulatory approval, integration risk, and competitive reactions still hover over the sentiment.

In a filing with the SEC, Netflix executives Greg Peters and Ted Sarandos said that the transaction with Warner Bros. Discovery (WBD) would be beneficial to consumers by providing more content and contributing to long-term growth. After this proposal, Paramount also came up with a competing offer and mounting pressure on Warner Bros. Discovery shareholders to change their mind about the Netflix deal. The constant speculation about the deal has taken a toll on investor trust and is part of a recent fall in the share price of Netflix.

However, the key business of Netflix is not weak. The company has also shown that it is capable of scaling content investments in a manner that is efficient, growing margins, and increasing cash flows. Its development of an ad-supported tier as well as its entrance into live events is transforming Netflix into not only a discretionary streaming service but a more sustainable entertainment platform with recurring engagement and enhanced monetization prospects.

Snapshot of the Company

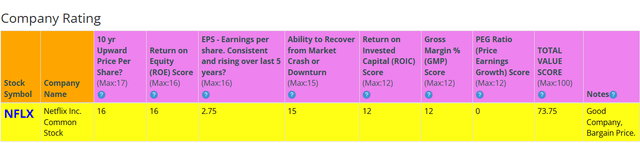

Netflix (NFLX) has a company rating score of 73.75 out of 100. It appears to have above-average fundamentals.

(Source: BTMA Stock Analyzer)

Fundamentals

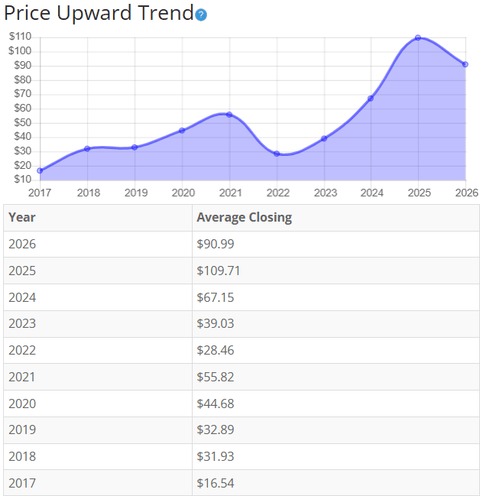

In the chart below, we can see that the price per share has been mostly consistent at increasing over the last 10 years, with only one year when the share price declined greatly in 2022. Now, due to the uncertainty regarding the probable acquisition, we can see there has also been a significant drop in stock in the past year. Overall, the share price average has grown by about 450.14% over the past 10 years, or a Compound Annual Growth Rate of 20.86%. This is an excellent return.

(Source: BTMA Stock Analyzer – Price Per Share History)

Earnings

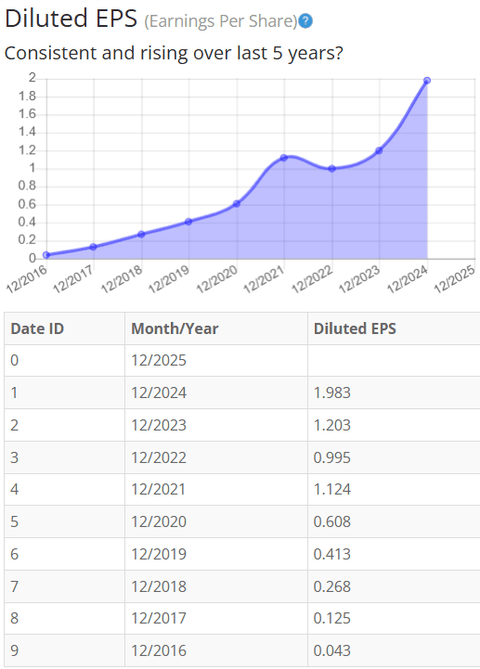

The earnings of Netflix have been increasing steadily in the last couple of years; the long-term upward trend in diluted earnings per share is evident. Although there have been some small ups and downs, the growth in earnings has generally been high given Netflix’s focus on growth.

Netflix’s profitability has been fueled by the increase in its subscriber base, global expansion, and monetization. The COVID-19 pandemic came at a time when Netflix was enjoying the benefits of an increased level of at-home entertainment consumption, leading to faster subscriber growth and uptake. In more recent times, the growth in earnings has been aided by pricing moves, enhanced cost control in relation to content expenditure, and the publication of an ad-supported level of subscription. Nevertheless, as the streaming market grows, Netflix will have less and less uninterrupted customer traffic and may experience pressure due to the possible increased content expenditure.

(Source: BTMA Stock Analyzer – EPS History)

Return on Equity

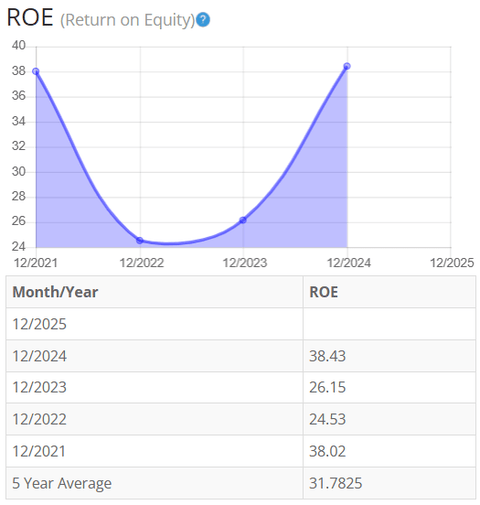

The return on equity decreased significantly in 2022, but there has been a noticeable increase in recent years. For return on equity (ROE), I look for a 5-year average of 16% or more. NFLX has an average of 31.78%, so it easily meets my requirements.

(Source: BTMA Stock Analyzer – ROE History)

Let’s compare the ROE of this company to its industry. The average ROE of 99 Entertainment companies is 6.09%.

Therefore, NFLX’s 5-year average of 31.78% is well above average, and so is its current ROE of 38.43.

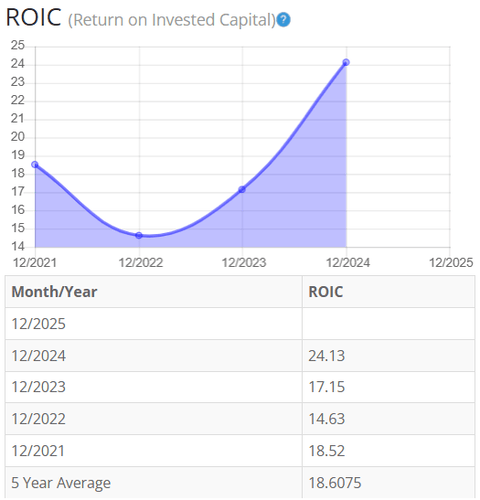

Return on Invested Capital

The return on invested capital fell in 2022 but has been consistently increasing ever since. The 5-year average ROIC is above expectations at around 18.61%. For return on invested capital (ROIC), I also look for a 5-year average of 16% or more. So, NFLX passes this test as well.

(Source: BTMA Stock Analyzer – Return on Invested Capital History)

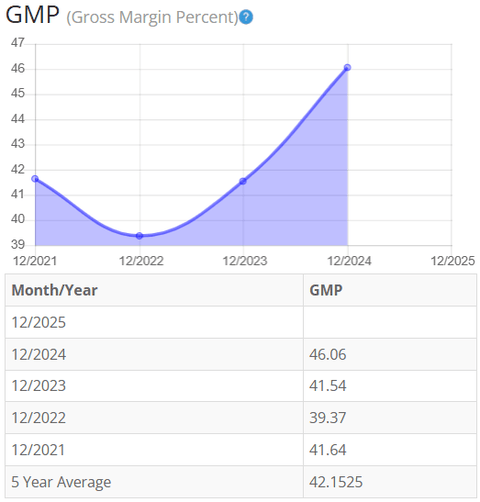

Gross Margin Percent

The gross margin percent (GMP) decreased in 2022 but has been on a steady increase since then. Five-year GMP is good at around 42.15%. I typically look for companies with gross margin percent consistently above 30%. So, NFLX has proven that it has the ability to maintain acceptable margins over a long period.

(Source: BTMA Stock Analyzer – Gross Margin Percent History)

Financial Stability

Looking at the fundamentals relating to NFLX’s balance sheet, the debt-to-equity ratio is less than 1. It is marked at 0.56, indicating that the company has nearly double the equity compared to its debt. It shows that Netflix is in a good financial position and has enough equity to pay off its debt.

Moreover, the current ratio of 1.33 is also reliable. It reflects that the company can use its current assets to pay its short-term liabilities. Ideally, a current ratio greater than 1 is satisfactory, and NFLX exceeds this amount.

Netflix operates with high capital and content investment requirements, which are characteristic of a large entertainment and streaming company. Over the past years, Netflix has been enhancing its financial standing by increasing its free cash flow as well as reducing the rate of content expenditure increase. This means that the company has had more capacity to finance its operations.

Netflix does not pay a regular dividend.

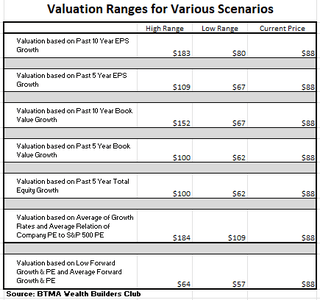

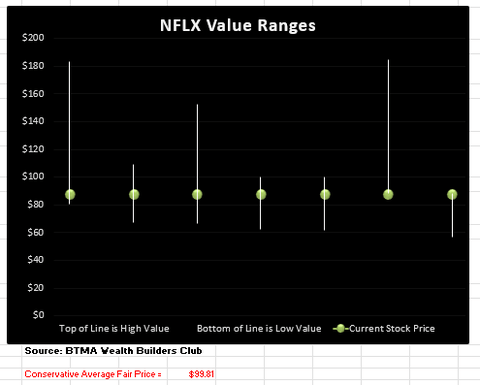

Value vs. Price

Netflix has a price-earnings ratio of 36.99.

The 10-year and 5-year average PE ratios of NFLX have typically been 103.04 and 42.6, respectively. This indicates that NFLX could be currently trading at a low price when compared to its average historical PE Ratio range.

(Source: BTMA Stock Analyzer – Stock Value)

The Estimated Value of the Stock is $108.12, versus the current stock price of $88. This indicates that NFLX is currently selling at a bargain price.

(Source: BTMA Wealth Builders Club)

This analysis shows an average valuation of around $100 per share versus its current price of about $88; this would indicate that Netflix is undervalued.

Summarizing the Fundamentals

As the facts indicate, Netflix seems to be financially sound in the long-term perspective, with the support of increased cash flow generation and a more restrained attitude towards expenditure. Netflix has shown that it has a great capacity to finance its operations internally and manage its long-term liabilities.

The company also has a good earnings history and has an upward trend in the long-term diluted earnings per share. In addition, Netflix has been able to scale its streaming business across the globe.

Other fundamentals are in good standing. The return on equity, the return on invested capital, and the gross margins are all higher than industry averages. Although certain metrics have dropped around 2022, they have since been on the rise, which indicates better efficiency and profitability as the company was able to realign its cost base to further monetize the business.

The other factor that Netflix should consider is the changing landscape of the streaming industry. With a maturing market, Netflix is becoming more competitive with consumer attention and costs over content. Nevertheless, efforts like the ad-based subscription plan and the development of live shows are meant to enhance interaction, reduce churn, and increase monetization in the long term.

Multiple forms of valuation analysis indicate that NFLX is currently selling at a discount price.

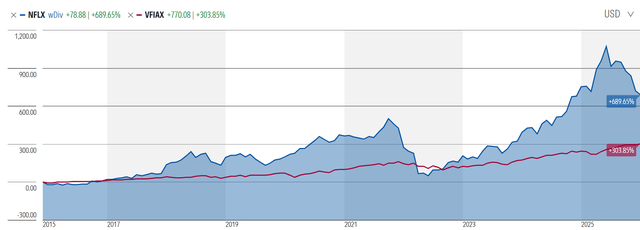

NFLX vs. The S&P 500

From the chart below, we can see that NFLX has mostly outperformed the general market. NFLX is clearly a high-growth stock that continues to be in a growing industry (entertainment). After the surge from COVID, we can see a clear drop during 2022, but it recovered quickly. After being at the highest point in the past decade, NFLX’s price has dropped. But it has still greatly outperformed the general market. If the stock continues to drop, it could provide a great opportunity to invest at an even better bargain price.

Morningstar

Forward-Looking Conclusion

Over the next five years, the analysts that follow this company are expecting it to grow earnings at an average annual rate of 23.83%.

In addition, the average one-year price target for this stock is at $124.53, which is about a 37.8% increase in a year.

Here is an alternative scenario based on NFLX’s past earnings growth. During the past 10- and 5-year periods, the average EPS growth rate was about 52% and 26%, respectively.

But when considering cash flow growth over the past 5 years, the average growth rate was 28%.

Does NFLX Pass My Checklist?

Company Rating 70+ out of 100? YES (73.75)

Share Price Compound Annual Growth Rate > 12%? YES (20.86%)

Earnings history mostly increasing? YES

ROE (5-year average 16% or greater)? YES (31.78%)

ROIC (5-year average 16% or greater)? YES (18.61%)

Gross Margin % (5-year average > 30%)? YES (42.15%)

Debt-to-Equity (less than 1)? YES

Current Ratio (greater than 1)? YES

Outperformed the S&P 500 during most of the past 10 years? YES

Do I think this company will continue to successfully sell their same main product/service for the next 10 years? LIKELY BUT NOT CERTAIN IN THIS EVER-CHANGING STREAMING INDUSTRY

NFLX scored 9.5/10 or 95%. Therefore, NFLX is definitely worth considering as a potential investment!

Is NFLX Currently Selling at a Bargain Price?

Price Earnings less than NFLX’s average historical PE range of 42-103? YES (36.99)

Estimated Value greater than Current Stock Price? YES (Value $108.12 > $88 Stock Price)

Detailed Valuation greater than Current Stock Price? YES (Value $100 > $88 Stock Price)

I would consider adding NFLX to my watch list of stocks and potentially consider investing in it because it did tick all of the boxes in my checklist. Netflix seems to be able to cover its long-term liabilities as it can finance its operations in the short term without interruptions to its business operations, as indicated in the balance sheet.

I would like to see how the anticipated acquisition impacts the fundamentals of the company before I invest. Since changes in this streaming technology industry can cause great price swings, it is imperative to add a margin of safety. Therefore, I will wait for the acquisition news and fundamentals to settle and look for a potential drop in share price to invest.

Grant Gigliotti is the founder of Beat The Market Analyzer, a leading value investing stock software and has been an active investor for 20+ years. He focuses on the value investing strategies of Warren Buffett to find good companies at bargain prices. He aims to show you how he buys good companies with strong fundamentals at large discounts from their intrinsic value.

Jan. 16, 2026 4:12 AM ETNetflix, Inc. (NFLX) StockNFLX:CA

https://seekingalpha.com/article/4860420-netflix-real-value

Grant Gigliotti

Investing Group Leader

Summary

Netflix demonstrates strong fundamentals, with robust global scale, high ROE, and consistent margin expansion despite recent acquisition-related uncertainty.

Recent merger speculation with Warner Bros. Discovery (WBD) has pressured NFLX’s share price, but core operations remain resilient and cash flow positive.

NFLX trades below its historical PE range and intrinsic value estimates, suggesting the stock is currently undervalued relative to long-term growth prospects.

This article focuses on the fundamentals, the real value versus the current share price, and if NFLX is currently worth investing in.

Netflix, Inc. (NFLX) is a broadly known worldwide entertainment corporation and the most well-known subscription-based streaming platform, which incorporates a diverse variety of original and licensed movies, documentaries, and live shows. Netflix has been at the center of the reinvention of media consumerism. With its operational location in over 190 countries, it is considered among the largest streaming services globally and has a powerful competitive edge in its size, its distribution potential, its originality, and its data-driven personalization power.

Investors are concerned with more than subscriber growth and margins at Netflix. The recent events related to a potential merger with Warner Bros. Discovery (WBD) have increased the uncertainty regarding Netflix’s strategic forecast, spawning legal issues, shareholder doubts, and valuation discussions. Although the management has focused on trusting the transaction and the long-term advantages of this decision, issues related to regulatory approval, integration risk, and competitive reactions still hover over the sentiment.

In a filing with the SEC, Netflix executives Greg Peters and Ted Sarandos said that the transaction with Warner Bros. Discovery (WBD) would be beneficial to consumers by providing more content and contributing to long-term growth. After this proposal, Paramount also came up with a competing offer and mounting pressure on Warner Bros. Discovery shareholders to change their mind about the Netflix deal. The constant speculation about the deal has taken a toll on investor trust and is part of a recent fall in the share price of Netflix.

However, the key business of Netflix is not weak. The company has also shown that it is capable of scaling content investments in a manner that is efficient, growing margins, and increasing cash flows. Its development of an ad-supported tier as well as its entrance into live events is transforming Netflix into not only a discretionary streaming service but a more sustainable entertainment platform with recurring engagement and enhanced monetization prospects.

Snapshot of the Company

Netflix (NFLX) has a company rating score of 73.75 out of 100. It appears to have above-average fundamentals.

(Source: BTMA Stock Analyzer)

Fundamentals

In the chart below, we can see that the price per share has been mostly consistent at increasing over the last 10 years, with only one year when the share price declined greatly in 2022. Now, due to the uncertainty regarding the probable acquisition, we can see there has also been a significant drop in stock in the past year. Overall, the share price average has grown by about 450.14% over the past 10 years, or a Compound Annual Growth Rate of 20.86%. This is an excellent return.

(Source: BTMA Stock Analyzer – Price Per Share History)

Earnings

The earnings of Netflix have been increasing steadily in the last couple of years; the long-term upward trend in diluted earnings per share is evident. Although there have been some small ups and downs, the growth in earnings has generally been high given Netflix’s focus on growth.

Netflix’s profitability has been fueled by the increase in its subscriber base, global expansion, and monetization. The COVID-19 pandemic came at a time when Netflix was enjoying the benefits of an increased level of at-home entertainment consumption, leading to faster subscriber growth and uptake. In more recent times, the growth in earnings has been aided by pricing moves, enhanced cost control in relation to content expenditure, and the publication of an ad-supported level of subscription. Nevertheless, as the streaming market grows, Netflix will have less and less uninterrupted customer traffic and may experience pressure due to the possible increased content expenditure.

(Source: BTMA Stock Analyzer – EPS History)

Return on Equity

The return on equity decreased significantly in 2022, but there has been a noticeable increase in recent years. For return on equity (ROE), I look for a 5-year average of 16% or more. NFLX has an average of 31.78%, so it easily meets my requirements.

(Source: BTMA Stock Analyzer – ROE History)

Let’s compare the ROE of this company to its industry. The average ROE of 99 Entertainment companies is 6.09%.

Therefore, NFLX’s 5-year average of 31.78% is well above average, and so is its current ROE of 38.43.

Return on Invested Capital

The return on invested capital fell in 2022 but has been consistently increasing ever since. The 5-year average ROIC is above expectations at around 18.61%. For return on invested capital (ROIC), I also look for a 5-year average of 16% or more. So, NFLX passes this test as well.

(Source: BTMA Stock Analyzer – Return on Invested Capital History)

Gross Margin Percent

The gross margin percent (GMP) decreased in 2022 but has been on a steady increase since then. Five-year GMP is good at around 42.15%. I typically look for companies with gross margin percent consistently above 30%. So, NFLX has proven that it has the ability to maintain acceptable margins over a long period.

(Source: BTMA Stock Analyzer – Gross Margin Percent History)

Financial Stability

Looking at the fundamentals relating to NFLX’s balance sheet, the debt-to-equity ratio is less than 1. It is marked at 0.56, indicating that the company has nearly double the equity compared to its debt. It shows that Netflix is in a good financial position and has enough equity to pay off its debt.

Moreover, the current ratio of 1.33 is also reliable. It reflects that the company can use its current assets to pay its short-term liabilities. Ideally, a current ratio greater than 1 is satisfactory, and NFLX exceeds this amount.

Netflix operates with high capital and content investment requirements, which are characteristic of a large entertainment and streaming company. Over the past years, Netflix has been enhancing its financial standing by increasing its free cash flow as well as reducing the rate of content expenditure increase. This means that the company has had more capacity to finance its operations.

Netflix does not pay a regular dividend.

Value vs. Price

Netflix has a price-earnings ratio of 36.99.

The 10-year and 5-year average PE ratios of NFLX have typically been 103.04 and 42.6, respectively. This indicates that NFLX could be currently trading at a low price when compared to its average historical PE Ratio range.

(Source: BTMA Stock Analyzer – Stock Value)

The Estimated Value of the Stock is $108.12, versus the current stock price of $88. This indicates that NFLX is currently selling at a bargain price.

(Source: BTMA Wealth Builders Club)

This analysis shows an average valuation of around $100 per share versus its current price of about $88; this would indicate that Netflix is undervalued.

Summarizing the Fundamentals

As the facts indicate, Netflix seems to be financially sound in the long-term perspective, with the support of increased cash flow generation and a more restrained attitude towards expenditure. Netflix has shown that it has a great capacity to finance its operations internally and manage its long-term liabilities.

The company also has a good earnings history and has an upward trend in the long-term diluted earnings per share. In addition, Netflix has been able to scale its streaming business across the globe.

Other fundamentals are in good standing. The return on equity, the return on invested capital, and the gross margins are all higher than industry averages. Although certain metrics have dropped around 2022, they have since been on the rise, which indicates better efficiency and profitability as the company was able to realign its cost base to further monetize the business.

The other factor that Netflix should consider is the changing landscape of the streaming industry. With a maturing market, Netflix is becoming more competitive with consumer attention and costs over content. Nevertheless, efforts like the ad-based subscription plan and the development of live shows are meant to enhance interaction, reduce churn, and increase monetization in the long term.

Multiple forms of valuation analysis indicate that NFLX is currently selling at a discount price.

NFLX vs. The S&P 500

From the chart below, we can see that NFLX has mostly outperformed the general market. NFLX is clearly a high-growth stock that continues to be in a growing industry (entertainment). After the surge from COVID, we can see a clear drop during 2022, but it recovered quickly. After being at the highest point in the past decade, NFLX’s price has dropped. But it has still greatly outperformed the general market. If the stock continues to drop, it could provide a great opportunity to invest at an even better bargain price.

Morningstar

Forward-Looking Conclusion

Over the next five years, the analysts that follow this company are expecting it to grow earnings at an average annual rate of 23.83%.

In addition, the average one-year price target for this stock is at $124.53, which is about a 37.8% increase in a year.

Here is an alternative scenario based on NFLX’s past earnings growth. During the past 10- and 5-year periods, the average EPS growth rate was about 52% and 26%, respectively.

But when considering cash flow growth over the past 5 years, the average growth rate was 28%.

Does NFLX Pass My Checklist?

Company Rating 70+ out of 100? YES (73.75)

Share Price Compound Annual Growth Rate > 12%? YES (20.86%)

Earnings history mostly increasing? YES

ROE (5-year average 16% or greater)? YES (31.78%)

ROIC (5-year average 16% or greater)? YES (18.61%)

Gross Margin % (5-year average > 30%)? YES (42.15%)

Debt-to-Equity (less than 1)? YES

Current Ratio (greater than 1)? YES

Outperformed the S&P 500 during most of the past 10 years? YES

Do I think this company will continue to successfully sell their same main product/service for the next 10 years? LIKELY BUT NOT CERTAIN IN THIS EVER-CHANGING STREAMING INDUSTRY

NFLX scored 9.5/10 or 95%. Therefore, NFLX is definitely worth considering as a potential investment!

Is NFLX Currently Selling at a Bargain Price?

Price Earnings less than NFLX’s average historical PE range of 42-103? YES (36.99)

Estimated Value greater than Current Stock Price? YES (Value $108.12 > $88 Stock Price)

Detailed Valuation greater than Current Stock Price? YES (Value $100 > $88 Stock Price)

I would consider adding NFLX to my watch list of stocks and potentially consider investing in it because it did tick all of the boxes in my checklist. Netflix seems to be able to cover its long-term liabilities as it can finance its operations in the short term without interruptions to its business operations, as indicated in the balance sheet.

I would like to see how the anticipated acquisition impacts the fundamentals of the company before I invest. Since changes in this streaming technology industry can cause great price swings, it is imperative to add a margin of safety. Therefore, I will wait for the acquisition news and fundamentals to settle and look for a potential drop in share price to invest.

Grant Gigliotti is the founder of Beat The Market Analyzer, a leading value investing stock software and has been an active investor for 20+ years. He focuses on the value investing strategies of Warren Buffett to find good companies at bargain prices. He aims to show you how he buys good companies with strong fundamentals at large discounts from their intrinsic value.

"Then there was a woman, a lion of a woman."

Discover What Traders Are Watching

Explore small cap ideas before they hit the headlines.