Wednesday, June 19, 2019 10:19:59 AM

IGNORING FACTS AND CONTEXT IN RXMD FILINGS

WHEN INTERPRETED HORRIBLY INACCURATELY THE INFORMATION FROM FILINGS CAN BE REFERRED TO AS "FALSE INFORMATION"

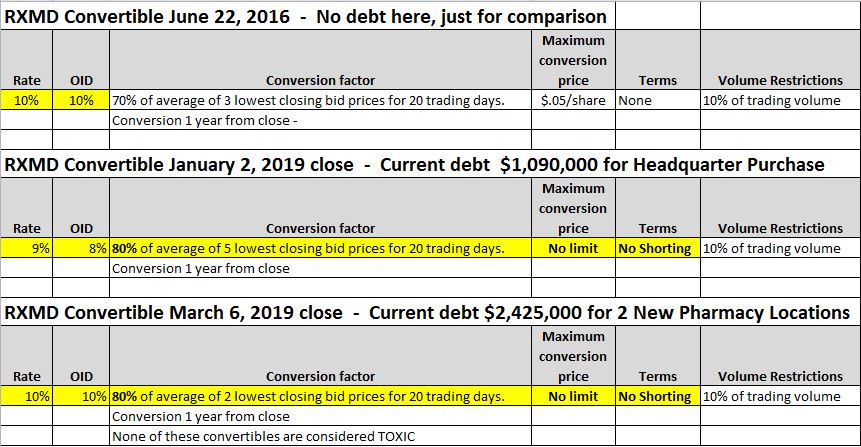

The shares to be held in reserve are at least 3 times the amount that would potentially be issued if amounts were fully converted and that's at current day's prices. Also, that's for the entire $6,000,000 in funding, presently the funding amounts to $3,515,000 for the new acquisition and new company headquarters.

PROOF:

ADDITIONAL FACTS:

What did take place was a major increase in company assets and revenues. The acquisition deals that this funding completed doubles both. Over $8 million in assets and $40 million in revenues

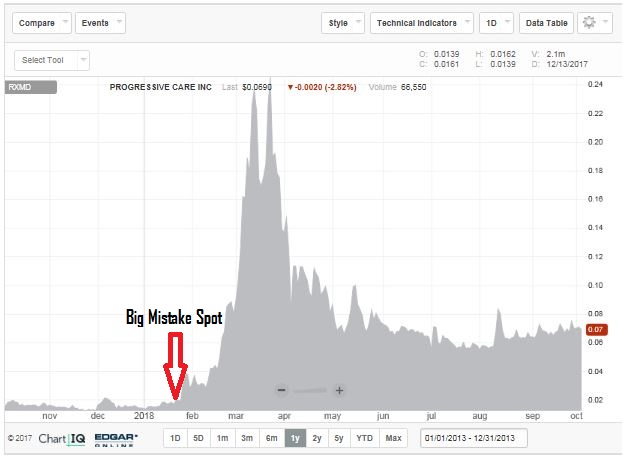

HERE's REALITY, coming from someone who bought shares at $.019. Wise choice, but bad for whoever the seller was.

Yes, it is likely shares will be converted starting January 2, 2020 to pay for the two new location acquisitions that added another $18 million in revenue and the new company headquarters that will remedy a $230k a year lease expense.

Well prior to that, come this May, we will experience a doubling of revenues, doubling of scripts and then SEC Registration soon after that. I think shareholders have done the DD and know all to well what is in store for RXMD, and it's called share price increases and eventual NASDAQ listing.

Background

Why did we take funding? For Acquisitions!!

Nearly everyone has to take out loans for acquisitions, it's the assets you get that matter. That's why some fail to mention the huge assets that are obtained that outweigh the funding and are substantial to ProgressiveCare's continued success.

Here is an example calculation that can occur that I have provided a million times. Remember this conversion can't take place until 1 year after the 2019 agreement dates below, and they can only obtain a small portion of shares and then sell 10% of weekly share volume max at a time, its a brilliant leak-out clause. Also, the company can pay back in cash at anytime as well instead of issuing shares. Hope this makes sense.

Calculation

We all know reservation of shares is not an indication in any way to the number of shares that will be issued. It is at least 3 times the expected amount of shares to be issued When conversion time comes around, the share price could be in the $.50 or better range, that conversion factor for the present outstanding funding amounts ($3.515 million as noted below) calculates to approximately 7 million shares.

Let's say it is $.25, that's 14.1 million shares.

Let's say it is $.10, that's 35.2 million shares.

Let's say it is $.07, that's 50.2 million shares.

What if the convertible ends up being $6,000,000 total to fund the two purchases. This is the amount that could be borrowed on the 2 agreements.

Let's say it is $.50, that's 12 million shares.

Let's say it is $.25, that's 24 million shares.

Let's say it is $.10, that's 60 million shares.

Let's say it is $.07, that's 85.7 million shares.

So as you can see, the current A/S count very well could be enough to cover any potential conversions with the exception of a few unlikely scenarios. This is if the company even chooses to convert to shares instead of paying a portion of the funding back with cash.

IMPROVED FUNDING AGREEMENTS FOR ACQUISITIONS and NEW HEADQUARTERS

DOOM AND GLOOM AVOIDED AGAIN, unless you sell low. LOL

WHEN INTERPRETED HORRIBLY INACCURATELY THE INFORMATION FROM FILINGS CAN BE REFERRED TO AS "FALSE INFORMATION"

The shares to be held in reserve are at least 3 times the amount that would potentially be issued if amounts were fully converted and that's at current day's prices. Also, that's for the entire $6,000,000 in funding, presently the funding amounts to $3,515,000 for the new acquisition and new company headquarters.

PROOF:

ADDITIONAL FACTS:

What did take place was a major increase in company assets and revenues. The acquisition deals that this funding completed doubles both. Over $8 million in assets and $40 million in revenues

HERE's REALITY, coming from someone who bought shares at $.019. Wise choice, but bad for whoever the seller was.

Yes, it is likely shares will be converted starting January 2, 2020 to pay for the two new location acquisitions that added another $18 million in revenue and the new company headquarters that will remedy a $230k a year lease expense.

Well prior to that, come this May, we will experience a doubling of revenues, doubling of scripts and then SEC Registration soon after that. I think shareholders have done the DD and know all to well what is in store for RXMD, and it's called share price increases and eventual NASDAQ listing.

Background

Why did we take funding? For Acquisitions!!

Nearly everyone has to take out loans for acquisitions, it's the assets you get that matter. That's why some fail to mention the huge assets that are obtained that outweigh the funding and are substantial to ProgressiveCare's continued success.

Here is an example calculation that can occur that I have provided a million times. Remember this conversion can't take place until 1 year after the 2019 agreement dates below, and they can only obtain a small portion of shares and then sell 10% of weekly share volume max at a time, its a brilliant leak-out clause. Also, the company can pay back in cash at anytime as well instead of issuing shares. Hope this makes sense.

Calculation

We all know reservation of shares is not an indication in any way to the number of shares that will be issued. It is at least 3 times the expected amount of shares to be issued When conversion time comes around, the share price could be in the $.50 or better range, that conversion factor for the present outstanding funding amounts ($3.515 million as noted below) calculates to approximately 7 million shares.

Let's say it is $.25, that's 14.1 million shares.

Let's say it is $.10, that's 35.2 million shares.

Let's say it is $.07, that's 50.2 million shares.

What if the convertible ends up being $6,000,000 total to fund the two purchases. This is the amount that could be borrowed on the 2 agreements.

Let's say it is $.50, that's 12 million shares.

Let's say it is $.25, that's 24 million shares.

Let's say it is $.10, that's 60 million shares.

Let's say it is $.07, that's 85.7 million shares.

So as you can see, the current A/S count very well could be enough to cover any potential conversions with the exception of a few unlikely scenarios. This is if the company even chooses to convert to shares instead of paying a portion of the funding back with cash.

IMPROVED FUNDING AGREEMENTS FOR ACQUISITIONS and NEW HEADQUARTERS

DOOM AND GLOOM AVOIDED AGAIN, unless you sell low. LOL

"To Give Anything Less Than Your Best, Is To Sacrifice the Gift." - Steve Prefontaine

Discover What Traders Are Watching

Explore small cap ideas before they hit the headlines.