News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

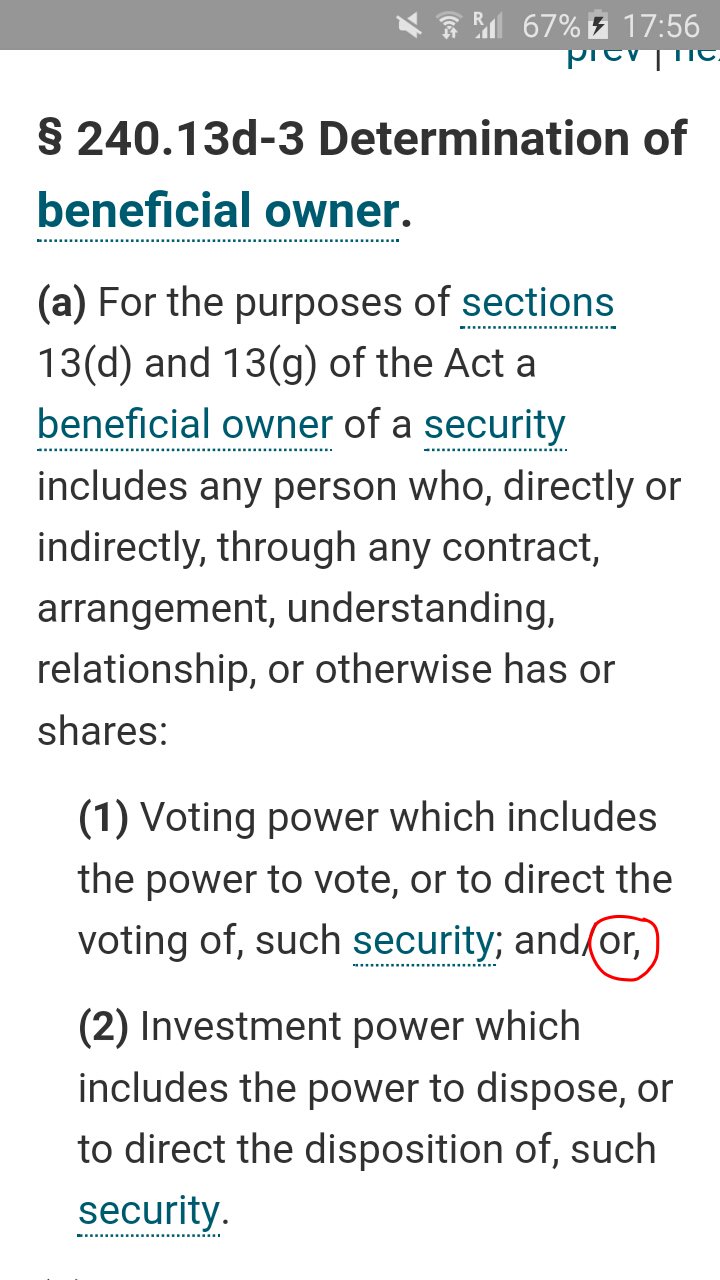

No. The SEC requires reporting 5% beneficial ownership, either with Voting power or the power to dispose of such security.

Never use Investopedia as source of information.

Pershing indicated that because it believes our common stock is not a voting security, it had determined not to file future reports on Schedule 13D. We do not know Pershing's current beneficial ownership of our common stock.

Only the penalty for Punitive damages,is worth $1.94 per common stock, as they match the amount for a $50 par value JPS. And it's been requested 3 rounds:

-Settlement of the 7 Securities Law violations.

-Deferred Income accounting if it's changed.

-Against the plotters writing in formal documents: Books, articles, court briefs, financial analyses, GSE slides, letters, etc.

With some caveats, because the commons waive the 2 claims against the DOJ in a Takeover or "as is" scenarios, not in a Takings at BVPS.

A $50 par value JPS is the closest fair value in a security issued by FnF, that can be better assessed the dollar amount with criterion, as its fair value all along is straight forward: 6% discount rate to par value, fetched upon dividend resumption (Therefore, the Common Equity has to be built first).

A 0.5% rate (equal to the spread earned by the UST with the SPS) on the true damage: spread market price versus fair value. The average is half a JPS exactly.

Therefore, a 0.25% IRR on a JPS par value, during 15 years.

By "legal hearings",he means frivolous lawsuits/abuse of court process.

Bradford keeps looping between the enumerated restrictions on capital distributions in the law: dividends and SPS LP increased for free when the dividend came to an end.

Also, he pitches a 10% rate, notwithstanding the rate similar to Treasuries in the authority of UST to finance their operations as a last resort, in exchange for their Public Mission, as part of the Charter dynamics (section Statutory Purposes).

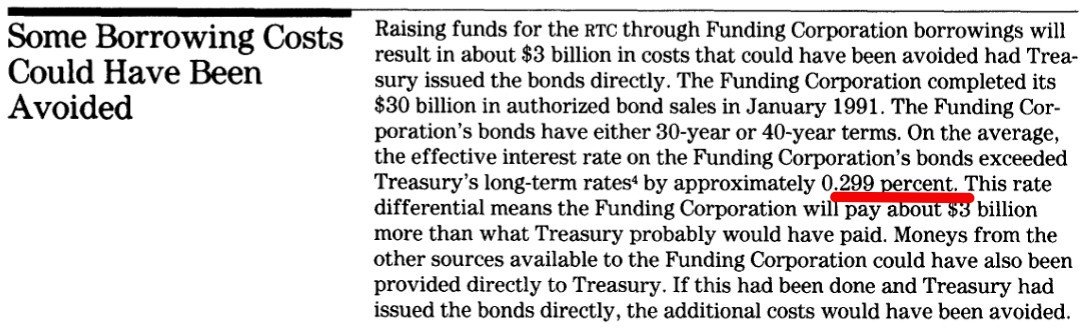

The rate was assessed at a weighted-average 1.8% cumulative dividend rate "taking into consideration the Treasury yields as of the last day of the month preceding the purchase" and the quarterly repayments, and with a 0.5% spread over Treasuries (0.299% spread in the 1989 bailout of the FHLBanks by Congress. GAO report)

The cumulative dividend that FnF owe to the Treasury Department, is netted out with the interests on the $152B that the Treasury owes to FnF.

Aren't tired of promoting your group's frivolous lawsuits?

If the slogan: "Capital Reserve is what meets the Capital requirements" began with Calabria and Mnuchin in the January 14th, 2021 6th PA amendment: "Capital Reserve End Date", one month before the Capital Rule (ERCF) came into effect on February 16th, 2021 (anyway, the capital shortfall over Min Capital requirement has been posted every quarter since day one, with the old 0.45% of MBS Trusts, because it's statutory), the other slogan: "Net Worth is what meets the Capital requirements", for instance, the former FMCC CEO, Layton, in an article last week, was initiated by Sandra Thompson, pointing out in the FHFA 2021 Report to Congress published in mid 2022, that the Net Worth or Equity is the Capital Reserve.

Capital Reserve is the amount of Net Worth above the Capital Stock. An invalid capital metric in the FHEFSSA.

Nowadays both amounts coincide ($125B) thanks to the Financial Statement fraud in FnF (SPS LP increased for free and its offset, are absent from the Balance Sheet).

It doesn't mean that the Net Worth or Equity is a capital reserve.

Without this fraud, the $125B worth of Net Worth is comprised of SPS and the Capital Reserve is, thus, $0.

We can also read the slogan nowadays peddled by Ackman and his clerk, Bradford: "FnF continue to build capital through Retained Earnings".

The column Capital Shortfall was removed from the ERCF table and the Critical Capital level is missing, commented yesterday. Both bother for their slogans that end up with "FnF have been rehabilitated" and "Why are they still in Conservatorship?".

Notice that the Goldman Sachs alumni Sandra Thompson arrived at the FHFA in March 2013 as Deputy Director in charge of Capital Adequacy matters, financial analysis, ...

The overnight payment of Punitive Damages serves as a settlement of the 7 Securities Law violations during conservatorship.

The corrupt litigants and the celebrities writing in formal documents share one of them: stock price manipulation.

It's been assessed 3 rounds with caveats.

Others might surrender their stocks, even without a direct participation in the con job. They are all acting in concert.

It's pointless to play the game "Which cup is the ball in?".

Berko sold out

Ackman who knows

There is no such thing as "prep work", neither for an extended Conservatorship nor for the release, which is also what the 3R scam is about: Recap; Release; Relist, thinking of starting the rehabilitation of FnF 15 years into Conservatorship.

The FHFA was appointed conservator by the FHFA Director in 2008.

There is no ON/OFF button to choose when FnF will start the rehabilitation.

It turned out to be a typical Transition Period to build capital and meet the new thresholds, Basel framework for capital standards, chosen in 2011 for the release at the request of the Dodd-Frank law.

The prior MANDATORY release Undercap was Core Capital or Tier 1 Capital greater than 0.45% of the MBS Trusts. Now, it's 2.5%.

Regulatory Risk.

HERA removed it, this is why now we are in overtime: CET1 >2.5 % of Adjusted Total Assets (Leverage ratio)

Suitable to redeem the JPS, that is, "wind down the affairs of (FnF) with the unwanted members" (wording in a 2016 Final Rule for the expulsion of the hedge funds that used captive insurers to gain access to the FHLBanks' low cost funding).

Conservator Risk: "Best interests of the FHFA" (Incidental Power)

FHFA now wants to make up for the losses of dividend suspension for this overtime with the Lamberth rebate, even beyond the threshold 25% of the Prescribed Capital Buffer for the resumption of dividend payments (Capital Rule, Table 8: Payout ratio). So, a little bit more than Undercapitalized (The Adequately Capitalized threshold uses the Risk-Based Capital requirement. This is why it's lower. "Inverted" threshold. Howard & Co complain about this requirement, when the binding one is the other)

The column "Capital Shortfall" removed from their ERCF tables.

More evidence that FnF are being conned with the "rehabilitation of FnF", based on the FHEFSSA-invalid capital metric "Capital Reserve", badly assessed (adjusted CR =$0), so they can spread the slogan: "Why are FnF still in Conservatorship?".

"Rehab FnF" was the prerequisite laid out by the Supreme Court to authorize the Separate Account plan "in the best interests of FHFA".

The last time we saw it, was with the data as of June 30, 2023.

.JPG)

Not that it matters, because it's the result of subtracting the "available capital" from the "capital requirement". So, DIY.

It's a problem of attitude.

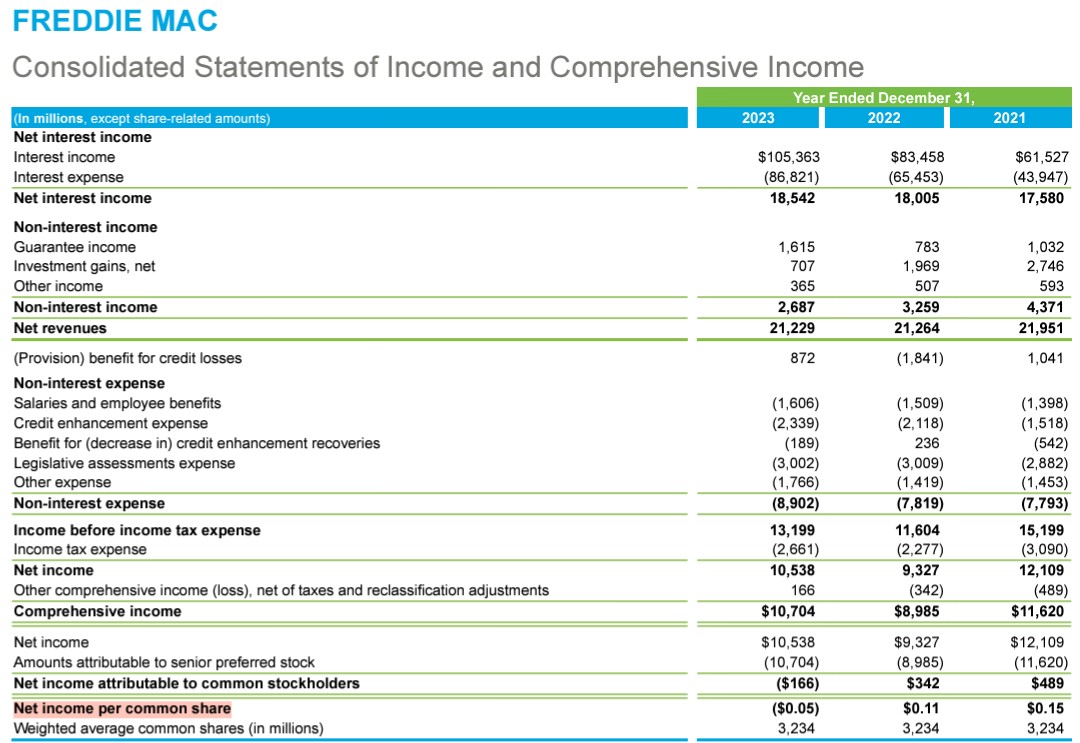

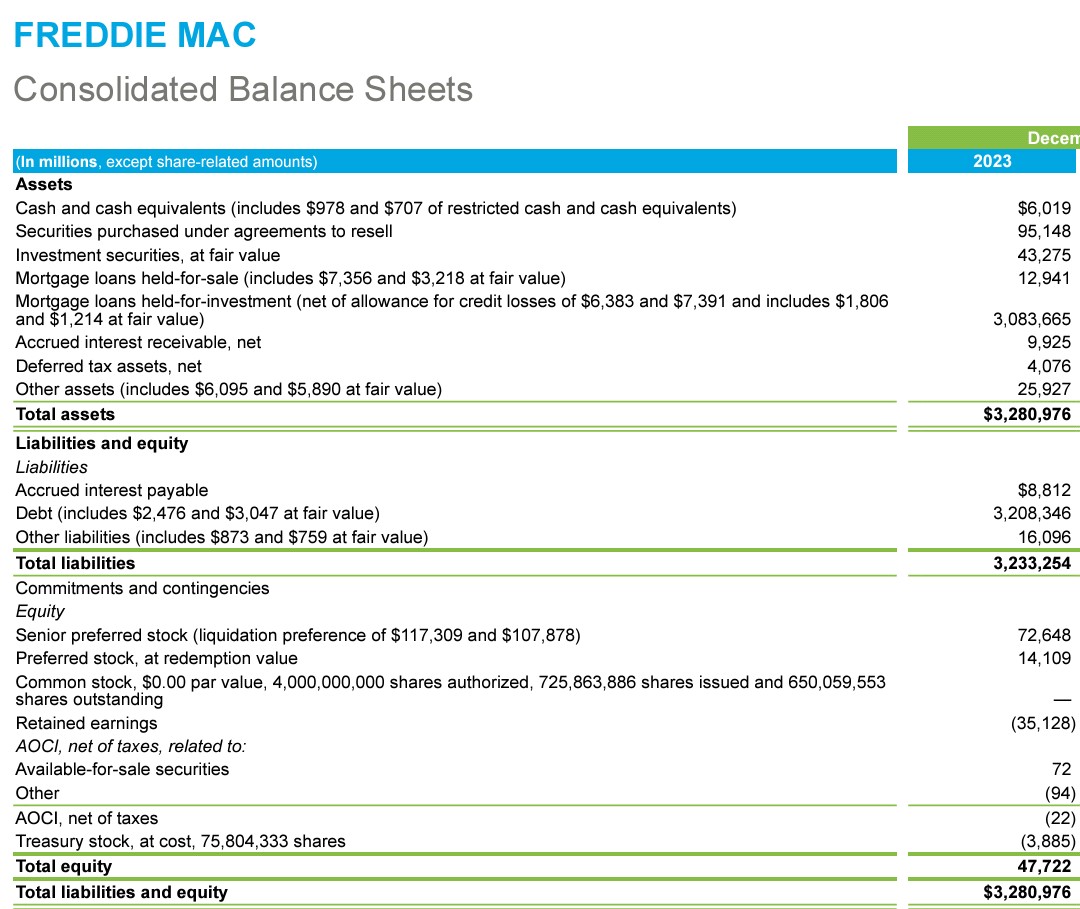

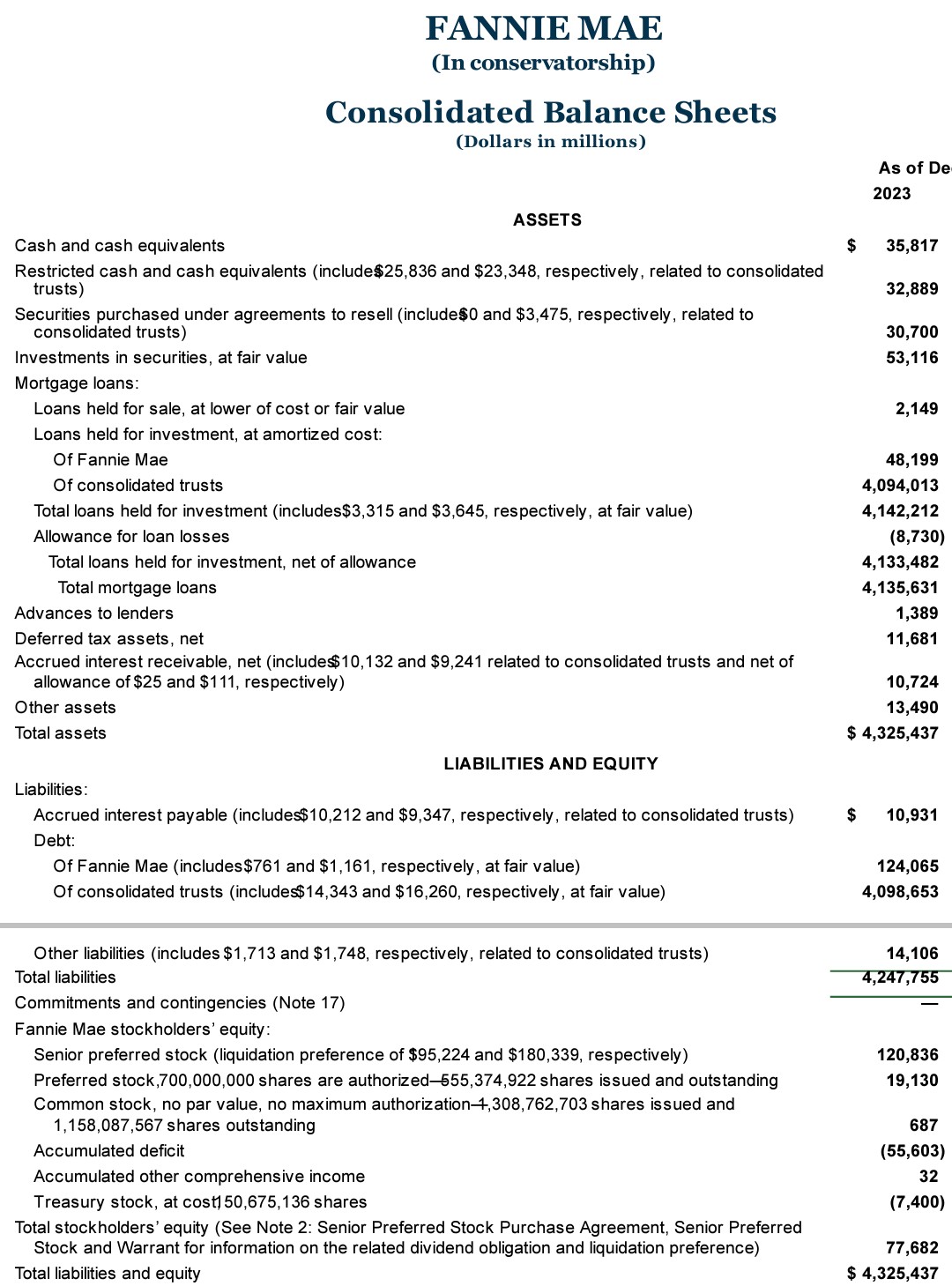

No one can claim that FnF have been rehabilitated (Fannie Mae CEO) with such enormous capital shortfalls in the most important table of all. The amount posted, later needs to be adjusted for the offset (reduction of Retained Earnings -Core Capital-) attached to the SPS LP increased for free, both absent from the balance sheets to evade it, where the data is taken from ($-78B in Fannie Mae and $-48B in Freddie Mac as of December 31, 2023).

The outcome is a whopping $402B core capital shortfall over Leverage capital requirement together (Undercapitalized threshold. Prior Capital Classification for MANDATORY release.)

The adjusted Core Capital remains stuck at $-194B every quarter, and FnF only build SPS in their Net Worth, more debentures with the taxpayer.

So much for "rehab".

This reminds me that the Critical Capital level is also missing in the ERCF tables (0.25% of the MBS trusts + 1.25% of the Retained Portfolio).

They are 3, not 2 capital requirements.

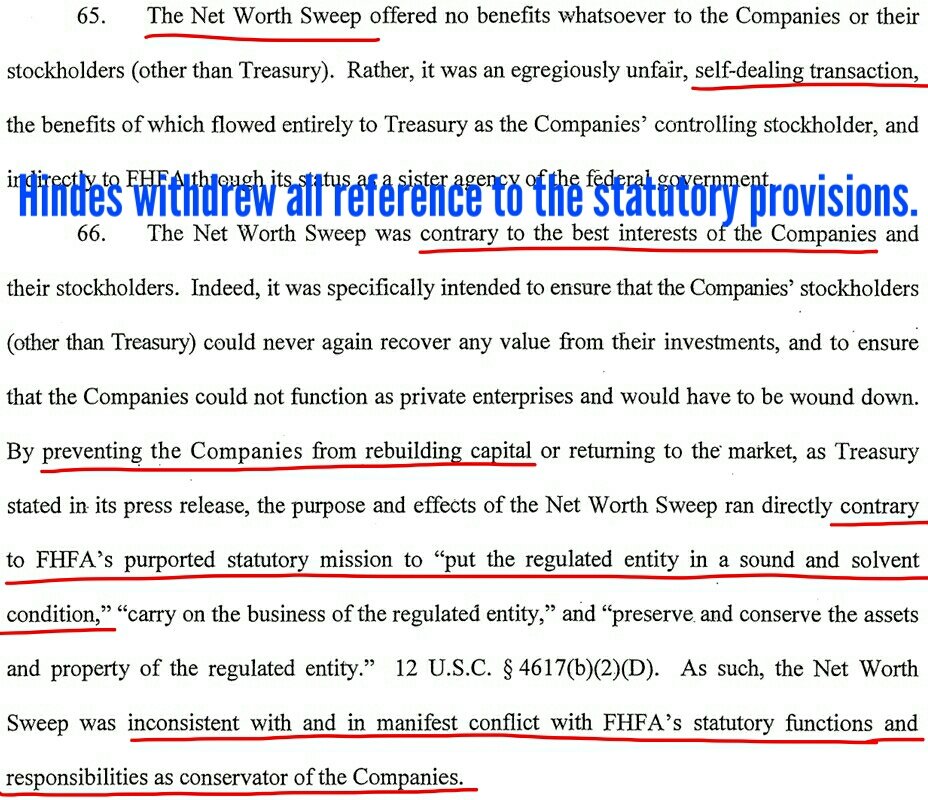

HERA amended the FHEFSSA to authorize the FHFA change the percentages in the Minimum Leverage Capital requirement, add new capital metrics (CET1 and Tier 1 Capital) and reserves (Prescribed Capital Buffer), and come out with a new formulaic for the Risk-Based Capital requirement (without the required 18-month implementation provision, by the way), but nothing about the Critical Capital level that remains as is.

Because all of them emanate from an express grant of authority in the FHEFSSA (a law enacted exclusively to oversee the soundness of FnF. Capital adequacy matters), it's why the ERCF is also statutory, regardless that it's laid out by regulation. FHFA has very limited powers.

The same reason: not meeting a capital level consider "Critical" bothers for their slogan "FnF have been rehabilitated" and "release".

12 U.S. Code §4614(a)(4)

An enterprise shall be classified as critically undercapitalized if—

(ii) does not maintain an amount of core capital that is equal to or exceeds the critical capital level for the enterprise;

Since entering conservatorship in 2008, the Enterprises have remained undercapitalized,

IN GENERAL. No capital distribution if, after making the distribution, the regulated entity would be undercapitalized.

Quit posting Plans of Share Appreciation.

The same two plotters with multiple aliases, keep on throwing numbers at the wall and pointing out that it's over a period of time.

The way a Separate Account is unwound, is fixing the stocks' fair value upon listing on the NYSE again, when the CUSIP symbol changes and they need to have a Reference Price on day one, regardless of the prior closing price. The same occurred when we were listed on the OTC market.

An "overnite" fix.

This fair value used as Reference Price must, at least, reflect the prospects of a Housing Finance System revamp we've been bound for and chosen for the release in 2011 (no TCCA fees) and the key: no dilution in the common stocks and JPS redeemed, both thanks to CET1 > 2.5% of the Adjusted Total Assets. Obviously, no CRT operations which are Charter-barred nowadays and the reason why it's been requested a refund of the CRT expenses, net.

So, everything that is known in the past. The reason why it's been suggested that FMCC should trade at PER 12 times, whereas 10x in FNMA, based on volume growth. Let alone that it was Fannie Mae the one that dragged Freddie Mac into conservatorship and now it's the laggard to meet the capital requirements.

For instance, it's been estimated that the dividend resumption, equal to par value JPS valuation, was fetched with the 3Q2022 results of Fannie Mae, one year earlier in Freddie Mac.

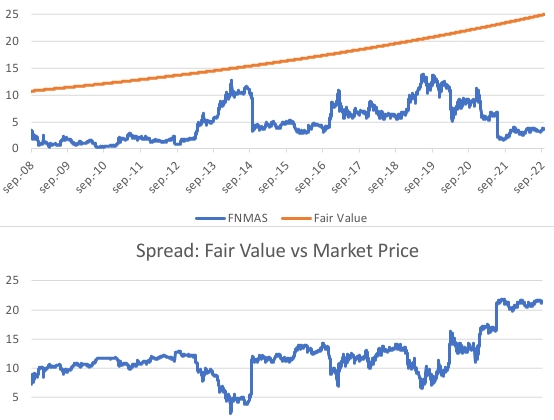

$FNMAS chart, the most liquid series of JPS:

A fair value or Reference Price can't discount other matters, like a forward EPS, the case of FHA's MMIF ceasing to exist, a future spin-off of CSS, etc.

That would be the market the one that puts the exact fair value with all the available information at the time and on the first day of trading on the NYSE.

And an "overnite" payment of Punitive Damages depending on the ultimate scenario, because the common shareholders waive their claim in a Takeover or "as is" scenarios, not in a Takings at the stocks' fair value of Common Equity per stock (BVPS) as of December 31, 2023.

The plotter Bill Ackman has already received a "capital requirement". And yes, "capital" means "cash" in this case. Not Equity, not regulatory capital, not Capital Reserve. Jesus!

The E in EPS=$0 is the same E in Retained Earnings that @BillAckman claims is being retained by FnF.

— Conservatives against Trump (@CarlosVignote) February 27, 2024

The same E to assess the Common Equity.

$0

He is liable for the payment of Punitive Damages for stock price manipulation, peddling the Govt theft story.#Fanniegate @TheJusticeDept https://t.co/AM7YZELbb0 pic.twitter.com/gUofottuZZ

Common Equity (CE) is comprised of:

-Common stock par value, less Treasury Stock (stock buybacks)

-Additional Paid-In Capital account

-Retained Earnings account

-Accumulated Other Comprehensive Income (AOCI)

It's not just the "common" as you pointed out. Hello?

Data taken from the Balance Sheets (picture of a company at a determined date).

For regulatory purposes (capital requirements to measure the soundness), there are other metrics:

CET1 = CE + regulatory adjustments (certain limits to improve the quality)

The FHFA provides the definiton by regulation: 12 CFR 1240.20(b)

Additional Tier 1 Capital (AT1) = JPS

Tier 1 Capital = CET1 + AT1

This is why, with CET1 > 2.5% of the Adjusted Total Assets (Separate Account plan "in the best interests of the FHFA"), FnF can redeem the JPS and still meet the ERCF with Tier 1 Capital >2.5% of ATA (Leverage ratio, previously known as statutory Minimum Capital requirement with 0.45% of the MBS Trusts. The ERCF is still statutory -FHEFSSA- regardless)

Statutory Critical Capital Level missing (they are 3, not 2). Not meeting a level called "Critical" bothers for the slogan "FnF have been rehabilitated" (Fannie Mae CEO, Pagliara, etc.)

This is what the Supreme Court referred to as "not in the interests of FnF", when it pitched the Separate Account plan ("Rehabilitate FnF" in a way that it's beneficial to the FHFA, meaning what it's written: "in the best interests of the FHFA"): Awful ERCF tables that need to be adjusted for the offset (reduction of core capital) with the SPS LP increased for free since December 2017 (Trump-Watt combo): $-78B in Fannie Mae and $-48B in Freddie Mac)

The Capital Reserve worth $125B, is an invalid capital metric (only used by the Federal Reserve -Capital Surplus-) and wrongly assessed. Adjusted Capital Reserve =$0.

A whopping adjusted $402B core capital shortfall over Leverage capital requirement together.

FNMA's 0.65 Conversion Ratio to FMCC.

You would get 13 FMCC for every 20 FNMA you hold.

Based on the assumptions pointed out in the 2 tweets.

Also that both are fully reserved against expected losses (ALLL)

A Conversion ratio consistent with their different Deferred Income as of end of 2023:

Freddie Mac: $42B

Fannie Mae: $19B

Although, some people would say that it should be adjusted more.

Therefore, the FNMA holders should be very happy with this ratio.

FAIR VALUE/CONVERSION RATIO WITH PER FINE-TUNED

— Conservatives against Trump (@CarlosVignote) February 27, 2024

FNMA PER 10x =$173

FMCC PER 12x =$266

Stock price driver also the adjusted EPS (annualized 4Q):

$17.3

$22.1

If FnF were combined:$FNMA's 0.78 Conversion Ratio to $FMCC based on EPS.

0.65 adding the different PE multiple.#Fanniegate https://t.co/2r8TQ0JnOJ

FNMA posts 80% of the adjusted EPS in FMCC.

Also Freddie Mac always grows faster. For instance, the latest figure: annualized 2.5% volume growth qoq in Q4, versus 0% in Fannie Mae.

Top line growth plus margin improvements, drive the PE multiple.

Therefore, Freddie Mac deserves a higher PE multiple and it posts higher EPS. Multiply both to assess the target price and you'll see why $FMCC should trade always at a price at least 50% higher than $FNMA.

You don't even know that BoA doesn't sell mortgages to Fannie Mae.

You don't talk about the non-bank lenders that sell mortgages to Freddie Mac.

You attempt to justify the current share price and the fact that someone is accumulating the stock with greater upside, needing a lower price to get more stocks, in an attempt to offset the difficulties in accumulating stocks in a company with a light trading volume.

Do you happen to know Ackman's clerk, Glen Bradford?

Are you going to write a SA article with that muddy story of visiting construction sites in winter?

Bill Ackman is defending the indefensible.

No matter how many PR campaigns he is always involved in, when he carries out conspiracies, like commissioning the KBW report released at the same time he published the GSE slide yesterday.

The E in EPS=$0

Income Statement.

, is the same E in Retained Earnings that Ackman claims is being retained by FnF.

Balance Sheet. Changes in Equity.

The same E to assess the Common Equity and CET1 for the ERCF.

Always $0. FnF are NOT building regulatory capital.

There are no excuses based on the Financial Statement fraud in FnF that don't post the SPS LP increased for free and its offset (reduction of Retained Earnings -Core Capital- that happens always when someone issues/increases stocks for free, like the initial $1B SPS issued for free in FnF. Someone has to pay for it) on the Balance Sheets.

Anyone could see, first, the SPS LP increased for free is a capital distribution restricted (#1 in the statutory definition of capital distribution). Secondly, that FnF are posting $0 EPS. Thirdly, that it's a breach of the FHFA-C's Rehab power: "put FnF in a sound condition". Soundness measured with capital levels in a financial company.

Then, there is no wonderland as claimed by the attorney for Berkowitz, David Thompson in the Collins, Rop and Bhatti cases, seeking "constitutional damages", where the UST gets rich with SPS LP increased for free and, at the same time, FnF are being recapitalized.

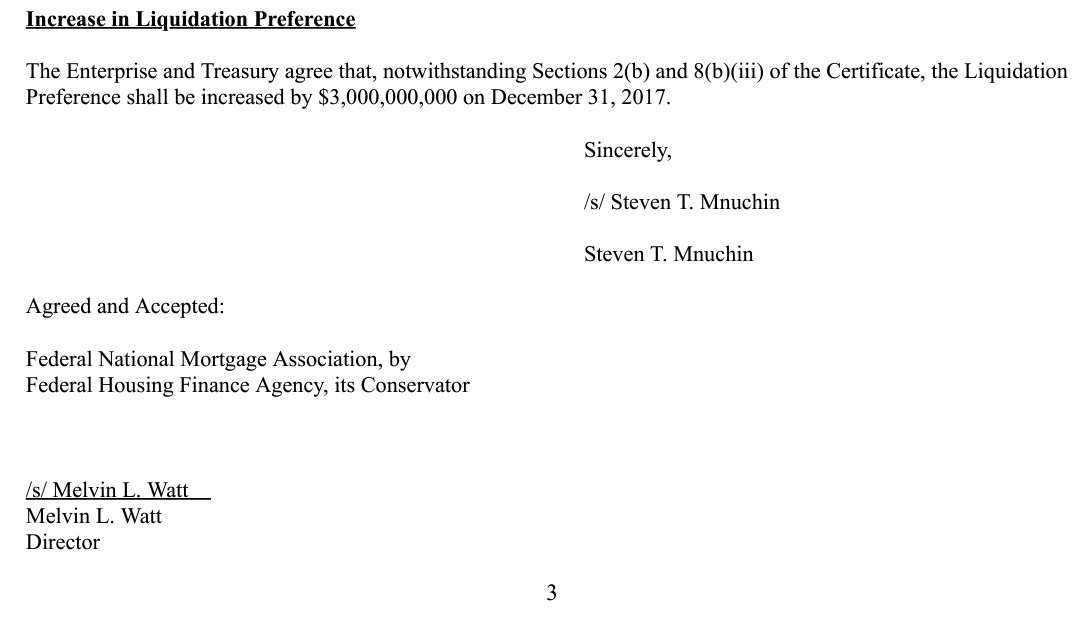

The same Common Equity Sweep as before. Now a 3rd phase that Trump started out with the template laid out by Watt-Mnuchin in the December 2017 PA amendment ($3B SPS LP increased for free and its offset, absent from the balance sheet for the first time, when the Applicable Capital Reserve was raised to $3B. Who told them that they can put limits, Federal Reserve-style? All part of the Separate Account plan. A plan of deception.)

Otherwise I don't know why JPS, GS, etc, don't do the same each quarter.

BOTTOM LINE

Necessarily the capital distributions are applied towards the exceptions in the law/CFR in order to legalize them.

That is, the Common Equity is held in escrow and the SPS are long gone.

Ackman conceals it to transmit a sense of normalcy, instead of being in the 3rd phase of the Separate Account plan (SPS LP increased for free, a joke "in the best interests of the FHFA". Zing!)

ACKMAN'S🆕GSE SLIDE,WRONG

— Conservatives against Trump (@CarlosVignote) February 26, 2024

▪️"FnF continue to build capital through RE",based on Financial Stmnt fraud(SPS/offset absent from B-Sheet)

👀 $0 EPS

▪️Unaware the #SCOTUS called for Rehab:Capital(not profitability)+↓SPS,as of day 1,"in the interests of FHFA"(Separate Acct)#Fanniegate https://t.co/dNNN7V9n6b

We don't need more laymen. With sophisticated investors playing the fool, is enough.

Profitability isn't a measure for the soundness in a financial company.

It's the capital metrics in comparison to capital requirements.

Like the 6th Circuit Court of Appeals in the Robinson case (almighty attorney for Berkowitz, David Thompson), about "put FnF (restore) in a sound condition", it claimed that it was achieved with "the return to profitability, even if a large portion of that profit was sent to Treasury's coffers'".

And about the "put FnF (restore) in a solvent condition", which is the ability of a company to pay its obligations, including the SPS, it claimed that it was achieved with the funding commitment, when it's supposed that rehabilitation is when a company is in solvent condition on its own.

The remark: "The companies likely should not return to business as usual", says it all. No one asked the judge about his opinion.

Both restoration plans were achieved through the exceptions to the statutory Restriction on Capital Distributions: reduce the SPS and Recapitalization.

It's not that they don't know what a capital distribution is, because there is a statutory definition.

To become FHFA Dtr, it's required by law a deep understanding of housing finance and the financial markets in general. Which reminds me of Judge Lamberth asserting that the plaintiffs were denied dividends that otherwise were certain to receive.

Everbody wants dividends.

Let alone the jurors that are only required to have driver license.

Pagliara and David Fiderer playing the fool:

More of a threshold, or evergreen, question: If Fannie and Freddie have been so profitable for over a decade, why are they in conservatorship?

— David Fiderer (@Ny1david) February 24, 2024

BERKO UNAWARE OF CONSERVATORSHIP

— Conservatives against Trump (@CarlosVignote) February 26, 2024

Let alone that the Undercap threshold for FHEFSSA (prior)MANDATORY release ↑from 0.45% to 2.5% of MBS.

"Highly regulated industries" is precisely why FHFA has limited powers:

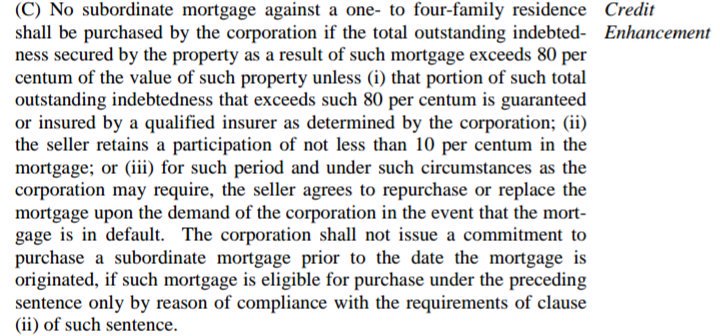

-Charter-barred CRT

-Capital distribution,restricted

-Rehab.#Fanniegate https://t.co/e4vGGllQlQ

Accounting Standard for the Upfront g-fee "Deferred Income", beyond shenanigans.

Two different issues:

1- Effective January 1st, 2010: "Changes in Accounting Standards Related to Accounting for Transfers of Financial Assets and Consolidation of VIEs". Their mortgage loans and the debt from their securitization trusts are now subject to consolidation on the balance sheets.

It prompted charges in Equity (Both in the Retained Earnings accounts and in the AOCI line item)

I find it extraordinary that in Freddie Mac, it resulted in a charge of $-11.7B, but a windfall of $3B in Fannie Mae.

It kick-started the Deferred Income accounting of the Upfront g-fee, which is the same as the Guaranty Obligation previously reported for their VIEs, that is, Debt.

The management of Freddie Mac might have siphoned off income to Deferred Income over a series of years. Numerous quarters a few years ago, during the refinancing boon when the Deferred Income is amortized, Freddie Mac increased it, whereas the opposite in Fannie Mae.

It could explain the disproportionate amount of Deferred Income in the smaller Freddie Mac, in comparison to Fannie Mae ($42B vs $19B) that can't be explained just because Freddie Mac has grown faster.

2- Deferred Income is valuable income already collected (upfront g-fee or LLPAs) necessary to meet capital requirements, recorded as Debt instead.

Because this part is lawful, we don't have a legal claim, primarily because the income is still there, but, if the Accounting Standard is changed in order to amortize all the Deferred Income into earnings in one fell swoop (just by changing the name Upfront g-fee for Delivery fee), and there is a Takings or takeover before, we are entitled to a compensation for damages, because FnF have been prevented from recording this capital during the Transition Period to build capital, that would have fast-tracked the release from conservatorship and the resumption of dividend payments.

Deferred Income is one of the 3 rounds of Punitive Damages. Although the common shareholders waive this claim in the case of release "as is".

There have been 3 Accounting Standard changes during Conservatorship, that have resulted in a charge on the Common Equity or Book Value.

PS: the tweet cited shows the charges for Accounting Standard changes. The BVPS is an old figure.

JAN 1,2010:GUARANTY OBLIGATION SWITCHED FOR DEFERRED INCOME

— Conservatives against Trump (@CarlosVignote) February 26, 2024

The same?

Change in Accounting Standard Related to Accounting for Transfers of Financial Assets and Consolidation of VIE→Equity charges:FMCC/FNMA $-11.7B/$3.3B

Did FMCC siphon income to Deferred Income(Debt)?#Fanniegate https://t.co/EmZTYgahAE pic.twitter.com/CVjhyMmKbd

Glen Bradford at it again.

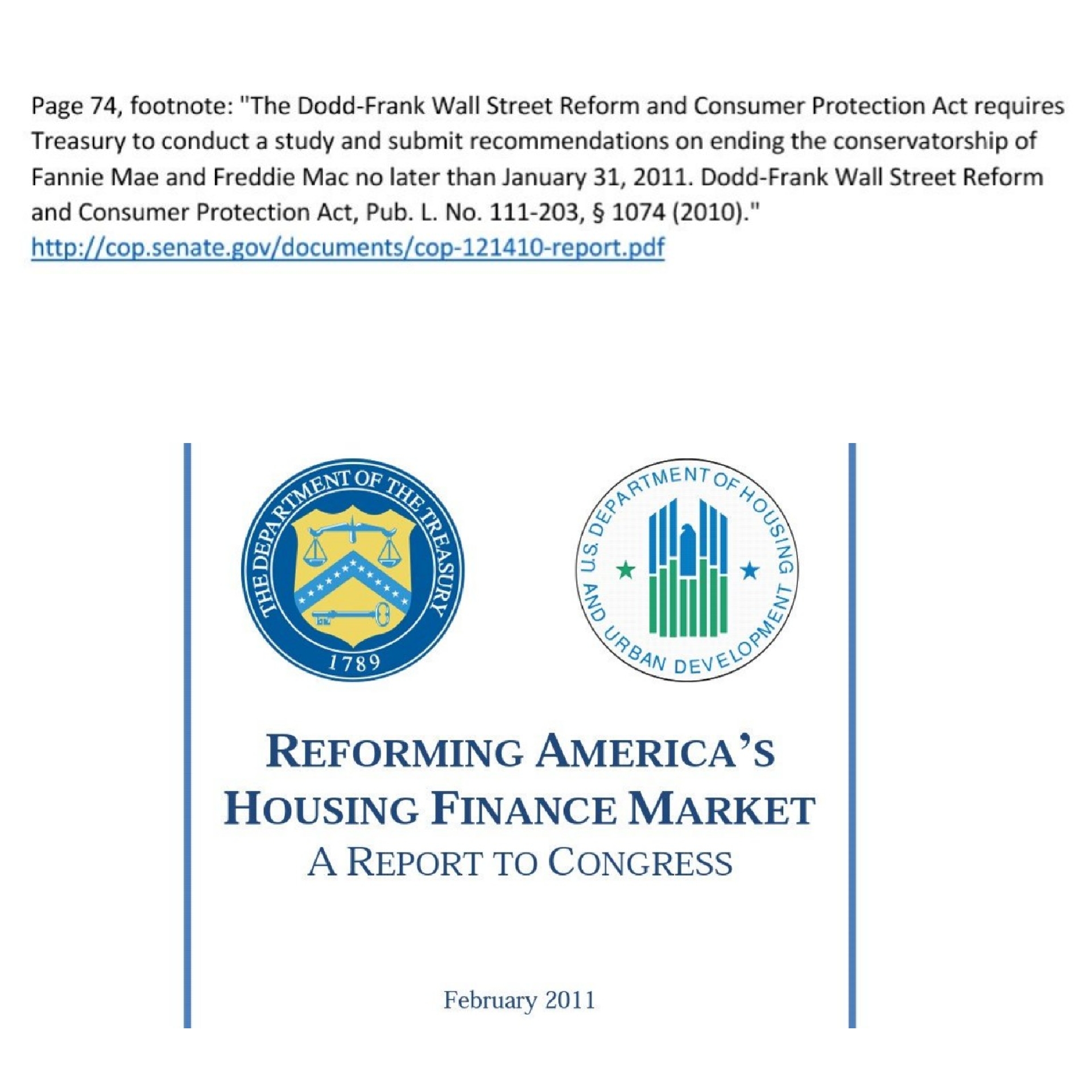

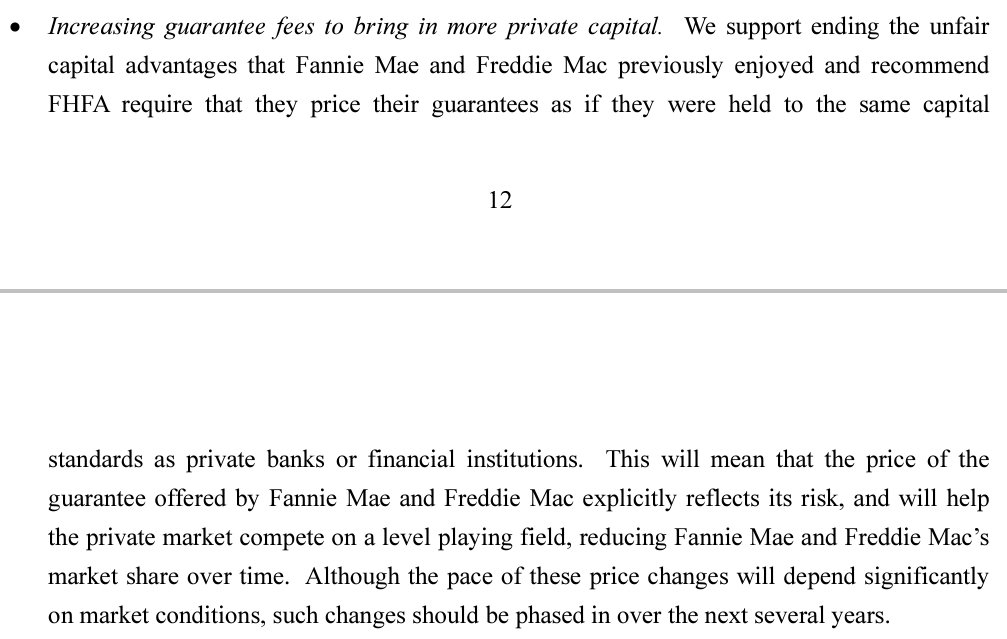

-He conceals the 2011 Report to Congress at the request of the Dodd-Frank law, with "recommendations on ending the conservatorships": Privatized Housing Finance System. A 3-option plan.

Increasing the guarantee fees, so FnF can be subject to higher capital standards like the banks (for the same risk exposure), which, in this world is called "Basel framework for capital requirements", was a recommendation by the UST in that report.

It was all about eliminating their Charter- and FHEFSSA (capital adequacy matters)- privileges, beginning with winding down their PLMBS portfolio funded with low cost bonds thanks, precisely, to the most precious privilege of all: a UST backup of their operations (both Equity and Debt) as a last resort and at rates similar to Treasuries, in exchange for their Public Mission (section Purposes).

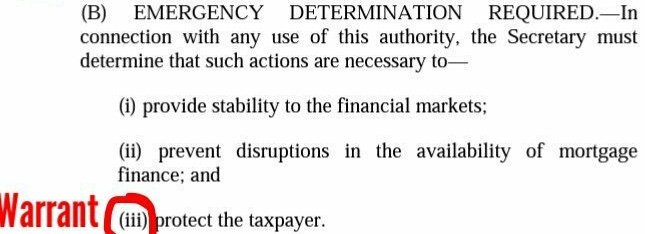

Subsection (c):

"To yield a return at a rate determined by the Secretary of the Treasury, taking into consideration the current average rate on outstanding marketable obligations of the United States as of the last day of the month preceding the making of such purchase."

COMMON EQUITY SWEEP GOES ON

— Conservatives against Trump (@CarlosVignote) February 26, 2024

Income Stmnt: $0 EPS

Operations absent from the Bce Sheet: gifted SPS LP/its offset.

Capital distribution #1(FHEFSSA definition), restricted. It's applied toward exception: Recap.

The same w/ the 10%/NWS divs(↓SPS/Recap)

Who hired this guy?#Fanniegate https://t.co/4QoT6Smbmb pic.twitter.com/h6X30C0awK

3R was an invention by Pagliara for his buddies hedge fund managers lying in wait: Recap, Release and Relist.

Do you really think that Freddie Mac needs a recapitalization with all the Core Capital generated during conservatorship?

I told you that the JPS holders rather see their dividend suspended kept by the government, instead of being kept by FnF for their recapitialization as usual. Hence the frivolous lawsuits and their shills on social media.

It's 3U: Unwind (Separate Account), Uplist (NYSE) and Unleash (Target price potential: CSS spin-off, Housing Finance System revamp, etc.)

I think no 3R in Biden administration??

NYSE? $10? When I say $0 EPS posted every quarter due to the SPS LP increases for free, what do you understand?

Do you know something about stock valuation?

Also that it's a capital distribution, restricted (U.S. Code §4614(e), plus the CFR 1237.12 that supplemented it and did not replace or affect it, so the UST can't steal money from FnF arguing that it's in the pubic interest -exception 4-, because the statutory restriction is for the recapitalization. The public interest is to have a FnF adequately capitalized)

We visually can see how it works, as necessarily the offset with the reduction of Retained Earnings is meant to hold it in escrow, as it's the required CET1 for the recapitalization that upholds the Restriction on Capital Distribution.

This operation is missing in the balance sheets, when FnF don't post the SPS LP increased for free since the December 2017 PA amendment by the Mnuchin (Trump)-Mel Watt combo. This template was later on used for the case when the dividend payments to UST came to an end: Sept 2019 and the Jan 2021, by Mnuchin (Trump)-Calabria, currently in place.

The reason why they carried out this Financial Statement fraud, is because people would start thinking that the same occurred with the prior capital distribution restricted: the 10% and the NWS dividends. It was applied towards the exceptions in order to legalize them: reduce the SPS and Recap.

Separate Account phases 1 (10% dividend), 2 (NWS dividend) and 3 (SPS LP increased for free) translate into Common Equity held in escrow, as the reduction of SPS was also a recapitalization, because FnF sent Common Equity to Treasury (Dividend, a distribution of Earnings -Core Capital-. A "Changes in Equity" operation), in the form of capital distribution, not simple cash.

The next chart shows all the Net Worth generated by Freddie Mac during conservatorship. It's why the Separate Account is unwound with a posting in the Retained Earnings account that, in the case of Freddie Mac is $110B, versus the $-35B currently in its Balance Sheet.

All the Comprehensive Income generated (Retained Earnings + OCI) must show up. Notice that the ending balance also includes a tiny amount of AOCI $-22 million as seen on the Balance Sheet as of end of 2023.

Also, it's been considered that the Treasury Stock -stock buybacks- worth $3.9B, is retired.

Once everything is unwound, it's assessed a fair value for each share class and it's the reference price when they are placed on the NYSE.

The price discounts all available information at the time:

Have the JPS been redeemed or repurchased?

Will the FHA's MMIF cease to exist?

Etc.

Once they start trading, the PER valuation will use the estimated 2025 EPS. This is why in a takeover or on day one of NYSE placement, there is still a buying opportunity because I'm using for the reference price (Fair Value) the annualized adjusted 4Q2023 EPS, the most recent official EPS, and a 14x PE multiple that might be reduced to 12 times in Freddie Mac and 10 times in Fannie Mae, after watching the sluggish Q4 volume growth qoq (annualized 2.5% and 0%, respectively).

Then, the PER multiple could soon be back up at 14x taking into consideration the expectations in a the new Housing Finance System revamp, and the acquirers or investors will begin to realize that the stocks would be trading at an estimated 2025 PER of 10x and 8x, resp.. Prospects of a spin-off of CSS from FnF, etc.

Therefore, plenty of upside even after being placed on the NYSE, or a good price for the acquires if they are taken private.

It's time to let the stocks trade at their fair value and snub all the conspirators stuck to the Fanniegate scandal.

Once the publicly notify ( submit application ) that they have applied to trade on NYSE we will see the SP jump to at least $10. Do you think?

Only one person says "NWS" instead of "NWS dividend".

BUSTED.

I never said that you are Bill Ackman, Gary Hindes or the pro se plaintiff Joshua Angel.

You always put words in other's mouth that they didn't say. Typical Bradford.

It seems that you stopped after reading the first sentence. Atta boy!

There you go! The same GSE slides/staged emails always posted by the combo Bradford/Ron "Rum", with their multiple aliases.

The 2011 Privatized Housing Finance System revamp chosen for the release, recommending an increase in the guarantee fees to reflect their risk, so they can be subject to the same capital standards as the fully private sector (Charter revoked), that is, Basel framework for capital requirements, a Report to Congress required in the Dodd-Frank law, and, at the same time, the categorical stance by the former Treasury secretary Geithner: "Don't listen to banks", at a time just after the HR 1859 was introduced in Congress (May 12, 2011) three days after China VP Qishan said to Geithner on national TV (Charlie Rose interview) with a petrified face: "Housing hasn't been addressed yet", aiming the assault on FnF for free, as explicitly stated in the ICBA plan of 2011, two months before:

kick-started the con operation in the U.S. courts pretending that a Conservatorship for the financial rehabilitation is, instead, a Nationalization, led by Berkowitz and his attorney David Thompson, Bill Ackman-Fried who is, allegedly, our market maker with a large short position in FnF at the same time, etc, their social media crew and, finally, the WH advisors sending each other emails stating that they are gonna steal everything from FnF, as part of the same plan to conceal the ongoing Separate Account plan in accordance with the law, rules and basic Finance (3rd phase: SPS LP increased for free, a capital distribution restricted is applied towards the exception: Recap, as per the CFR 1237.12. That is, the Common Equity is held in escrow through the offset attached to gifted stocks. Concealed with Financial Statement fraud: SPS LP absent from the balance sheets).

The goal is always the same: to cover up or twist the statutory provisions. For instance, the Treasury using the Charter Act of FnF for its 2009 MBS purchases program to purchase MBSs from Blackrock & Co in the secondary market, when it's about purchases of MBS from FnF in the TBA market, that is, a UST backup of FnF to finance their operations as a last resort (the operations are financed both with debt and Equity) and in exchange for their Public Mission that no other company has (not even the FHLBs, as this Public Mission "Purposes" is unrelated to the "Housing Goals" inserted by HERA, goals that always lag the market, pointed out by the very FHFA), commented yesterday.

I wouldn't be surprised if the Treasury Department now wants to pardon the debt outstanding that FnF owe to it, as part of the twisted Charter dynamics, Argentina/IMF-style, which is the same stance that someone that has just come from other planet would say, because these officials wouldn't tell the extraterrestrials what has happened before. For instance, the extraterrestrials wouldn't know that the ERCF tables exist, which is the case of many people from this planet nowadays, who don't even have any excuse for not knowing that the statutory Critical Capital level is missing in the ERCF.

It's not that we have to repeat the same things over and over again, the thing is that we have to start explaining them since 1992, so they can see that the Critical Level level is missing, that there was a MANDATORY release Undercapitalized in the prior law, currently a Core Capital or a Tier 1 Capital

> 2.5% of the MBS Trusts with the new Capital Rule, when before it was just 0.45% (Regulatory Risk concealed by the holders of non-cumulative dividend JPS, as their dividend is suspended for the Recapitalization of FnF), that a conservatorship has nothing to do with the Federal Government, etc..

The Charter dynamics can't be subject to random officials in the Administration (Blackrock, Citigroup, GS, ...) stating that the Treasury has to be appropriately compensated, against the Charter dynamics, and even dare to approve CRT operations barred in the Charter's Credit Enhancement clause, promoted with the pomp of CRT symposiums, just after their PLMBS were sold off, which were barred as well in the same clause, and also numerous DOJ and SEC attorneys that also have come and gone from Wall Street law firms during the Conservatorships (Mooppan, "Jody" Hunt, Daniel Kahn "Deputy Assistant AG criminal division", the solicitor general Noel Francisco who let Mooppan take his post before the SCOTUS, SEC's Clayton, etc) but a continuation of the plan that started out with the mandate to Treasury of recommendations on ending the conservatorship in the Dodd-Frank law.

Let alone letting the battered holders of JPS to opine. A made-up fixed-income security created exclusively for capital adequacy matters (Core Capital) and the reason why they get a higher dividend rate than the interest rate on similar obligations by the same issuer. Obviously, they rather see their dividend suspended kept by the Treasury, instead of kept by FnF, so they can call for an Equity restructuring for a swap JPS for Cs that would make up for their losses.

What it looks like, is a series of officials that leave their post without telling their replacement anything about the Separate Account, and the new official, when he finds out about it after reading the Fanniegate hashtag on Twitter or this message board, is replaced with an offer of a top job that he couldn't refuse.

This explanation of the Conservatorship of FnF and the rehabilitation, in accordance to the law, rules and finance, is a blow to the FHFA and the Treasury Department:

HOUSING FIN SYS REVAMP TO PERFECTION

— Conservatives against Trump (@CarlosVignote) February 23, 2024

Chosen in 2011 for the release🆚prior MANDATORY Undercap (Tier1 C.>2.5% of ATA) struck by HERA.

Laggard $FNMA: CET1 >2.5% in Q3, for JPS redemption(AT1),so T1>2.5%, but 22% of C.Buffer<25% for div resumption.

Hence Q4:40%$FMCC=102%#Fanniegate pic.twitter.com/cIyfWf16EV

A haircut or a cut to perfection?

The overtime was first thought for the acquisition of FnF by bigger players, though Congress might disagree.

— Conservatives against Trump (@CarlosVignote) February 23, 2024

The redemption of JPS is now a corporate decision regardless.

The last additional quarter could indicate that the Accounting Standard for the Deferred Income won't change.

Whoa! Fisher's innovative stance was the Tyler SCOTUS ruling, contending that the government can't take more of what it's owed.

It turns out that, in the Charter Act, it's called dividend rate for the SPS the Treasury was authorized to purchase (not even one security purchased, in an attempt to twist the Law. A telltale sign).

Subsection (c):

"To yield a return at a rate determined by the Secretary of the Treasury, taking into consideration the current average rate on outstanding marketable obligations of the United States as of the last of the last day of the month preceding the making of such purchase."

Berkowitz and Co seek a Nationalization during Conservatorship, that is, give the companies away to the government with the blessing of the courts, expecting some secured deals from the Administration or Congress later on.

They are known as Chamber investors.

Google_Drive format. No evidence of doc submitted to court.

NWS dividend authorized under one prerequisite: Separate Account plan.

Through the FHFA-C's Incidental Power "best interests of the Agency".

So, it wasn't an actual dividend payment but assessments sent to UST, in the form of capital distributions, under the guise of dividend payments (Restricted and unavailable Earnings for distribution, out of an Accumulated Deficit Retained Earnings accounts)

The dividend was impeccably suspended for the recapitalization of FnF.

Two sides of the same coin: the financial rehabilitation.

I don't see that it was electronically filed. Notice that it's a Google Drive file taken from Bryndon Fisher's personal cloud storage, posted on this board by Pagliara's clerk, Guido.

Anyway, Fisher can't understand that a Taking isn't authorized in a Conservatorship, much less using an Incidental Power, as explicitly stated by judge Willett in the 5th circuit court of appeals, with "any action within the enumerated powers", referring to the Rehab power (put FnF in a sound and solvent condition, that, in a financial institution, it's measured with capital levels and the ability to pay the debt outstanding, including the SPS, respectively) and confirmed by Justice Alito when he started out his interpretation of the same provision with "Rehabilitate FnF", adding the wording that authorizes a Separate Account in the process, not in the interests of FnF as seen in their ERCF tables, but "beneficial to the Agency". He meant what is written, which is "in the best interests of the Agency" related to activities, because there is no possibility to think of "monetary benefit" and he was just paving the way for the hedge funds/investment banks and their attorney-mercenaries with their Government theft story for stock price manipulation. A mistake, because now they will have to pay Punitive damages.

The idea that FnF are now rehabilitated is laughable. Just watch their balance sheets with an adjusted Accumulated Retained Earnings accounts of $-216B together, an account that absorbs future losses and where the dividends are distributed from. This is why the plaintiffs submit their own fabricated GSE sides.

Besides, FnF would be declared Critically Undercapitalized today (adjusted $-194B Core Capital), had the FHFA posted their statutory (FHEFSSA) Critical Capital level in their ERCF, which is another element in the plan of deception by this rogue Federal Agency "in its best interests". At some point, it'll be posted for sure.

With the Separate Account plan in accordance with the law, CET1 > 2.5% of the Adjusted Total Assets. That's rehabilitation. Although a conservatorship isn't meant to build full capital requirements, the fact that the release was linked to a Privatized Housing Finance System revamp in 2011, is why it's been stretched to the max, as bigger players in Housing Finance might acquire FnF and as part of a "membership cleansing", FHLBanks-style in 2016.

We are still waiting for Congress to choose one of the 3 options laid out by the Treasury in 2011. That's the "work with Congress" (come clean about the Separate Account, Charter-barred CRT expenses, PLMBS settlement,...) by all the prior FHFA directors and UST secretaries, as opposed to "I defer to Congress" by Sandra Thompson, signaling that she refuses to unveil the Separate Account and rather rely on the attorney-mercenaries and their social media crew.

Bryndon Fisher can't understand that his Derivative Takings claim (on behalf of FnF), is the same as a Direct claim in the common stocks, as they represent a legal claim on the entire Earnings of FnF, after the payment of dividends to Preferred Stocks (all of the remainder is "Net Income attributable to the common shareholders" in the Income Statements), unlike the latter, fixed-income securities, that only have a contractual claim with FnF (dividend impeccably suspended). A common stock isn't an unbacked token.

A Direct claim was already denied and his Derivative claim too, by the very Supreme Court when it denied a petition for writ of certiorari submitted recently by one of the Fairholme Plaintiffs, Andrew T. Barrett:

Let alone that he already submitted an interlocutory appeal (interim appeal), as part of the related cases led by Fairholme in the CFC, which annoyed him because he always seeks to be in the limelight as we are witnessing nowadays. That's why, after his insistence, judge Sweeney allowed him to file an interlocutory appeal with his Derivative claim. Numerous appeals to the Supreme Court were filed afterwards.

Therefore, Fisher now wants to file a third appeal over the same issues already dealt with, selling the idea that his stance is unique, a "groundbreaking case study" that no one has brought up before. "I know math" he has said in this message board when he proposed 15 years on, a cattle market-style negotiation with the Treasury, not backed up by any statutory provision, so he can sneak the 10% dividend that has been restricted all along, instead of being all part of the same plan since day one, and where the cumulative dividend rate will "take into consideration the Treasury yields as of the end of the month preceding the purchase", as per the original UST backup of their operations since the Charter's inception.

The fact that it was enabled regulation on July 20, 2011, for the continuation of this plan and on the Time Limitation of the Acting Dtr DeMarco, proves that they were really thinking of this plan, as it contemplates the case for when the SPS were fully repaid, with the CFR 1237.12: "Deplete capital is authorized to build capital", which is a Separate Account wording right there.

Also, Bryndon Fisher can't understand that capital distributions are restricted (dividends, SPS LP increased for free and the Lamberth rebate). A provision covered up by all the litigants acting in concert, as it's the key to understand the Separate Account plan through the exceptions and with the CFR 1237.12 that supplemented it (July 20, 2011).

Finally, the DOJ attorneys might have sounded the alarm after reading this comment from Fisher, proposing a settlement out of court and only with the attorneys in the Collins case, just before the Oral Arguments at the Supreme Court.

It has all to do with the Privatized Housing Finance System revamp, chosen for the release in 2011 at the request of the Dodd-Frank law, and the fact that the FHFA already carried out a "membership cleansing" with the FHLBanks in a 2016 Final Rule: "Wind down their affairs with the captive insurers."

This is achieved once FnF fetch a CET1 > 2.5% of the Adjusted Total Assets, so the JPS can be redeemed, complying with Tier 1 >2.5% of ATA afterwards (ERCF).

The laggard Fannie Mae achieved this threshold with the 3Q 2023 results, under the Separate Account plan. But then, the threshold for the resumption of the dividend payments (25% of the Prescribed Capital Buffer.Table 8: Payout ratio) wasn't met yet (22%. Whereas Freddie Mac, 69%).

With the recent 4Q 2023 Earnings reports, 40% (Freddie Mac, 102%). Leverage ratio.

Never underestimate the Incidental Power: "Zing!".

Although the Congress might not want that FnF be acquired by other players, even with the profitable scenario of doing it through a Taking at BV by the UST as an interim phase, and FnF would be released as is.

Too late. The redemption of the JPS is now a corporate decision regardless.

That's the reason of the 15 years and 5 months.

The Plan of Allocation of penalties on plotters peddling the government theft story in formal documents, is more interesting.

For instance, there are at least 3 plaintiffs that write in this message board to mislead and harass the shareholders, that could be fined twice as much. Haven't you noticed it?

Others might have to surrender their stocks, even without a direct participation if proven that they acted in concert with a known plotter.

Another example. Trump fabricated evidence with the famous Trump letter, when the SCOTUS didn't ask for his opinion about what he would have done in the past, but whether he had made a public statement showing displeasure with the FHFA Director's actions at the time that he was in office.

There's been only one, just one month after Calabria was sworn in:

We are doing well with them...

lawyer fees aka pro bono cases range from 15% to 25% so that $612 million going to get a BIG haircut !!

Patswill: "Do you think we break through $1.30 today?"

Response:

Augie Boukalis: "I think we break through 1.30 today 🌵🛹🇺🇸"

Who hired this guy?

Mounting evidence that rogue officials attempt to turn FnF into the Fed, passing the SPSPA off as "the Law", as stated by representative Davidson in a congressional hearing (watch the tweet below), mimicking the statutory limits in the "Capital Reserve" that the Fed calls "Capital Surplus", the rest swept to Treasury (remittances to Treasury).

FnF don't have such statutory limits.

Actually, it's the opposite with a Fee Limitation of the United States.

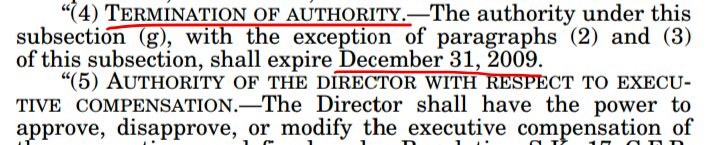

It wasn't changed "as of the passage of HERA" (DOJ attorneys), primarily because the 2nd UST backup of FnF with an infinite rate on SPS, inserted by HERA in the Charter Act, was a TEMPORARY authority with a deadline on December 31, 2009.

Let's not forget the multiple attempts by Mnuchin to portray FnF as "liquidity providers" for the banks, when that's the FHLBanks and the Federal Reserve.

FnF carry out a Public Mission, but related to the Guaranty Mortgage Securitization business, with secondary market operations.

So, a business activity that can be perfectly carried out by fully private companies (Charter, revoked)

A Charter Act with a UST backup of their operations as a last resort (Section: statutory purposes), now pointless with FnF subject to the Basel framework for capital requirement, 15 years into a conservatorship.

MISTAKE OF PA "THE LAW" WASN'T MADE BY CHANCE

— Conservatives against Trump (@CarlosVignote) February 20, 2024

Capital Reserve(FHEFSSA-invalid) mimics the Fed's Capital Surplus,w/ statutory limit changed from time to time by law:$7.5B→$6.825B,May 2018.

PA changed the Applicable CR too,but as part of a Separate Acct.#Fanniegate @TheJusticeDept https://t.co/vZClCSXivH

⚠️TOS VIOLATION⚠️Don't post the same article that was debunked when you posted it the first time.

An article commissioned by the plotters to peddle the same lies.

FnF don't pay interests on SPS, but dividends (a capital distribution restricted, like the gifted SPS. The exceptions kicked off: for this case, U.S. Code 4614(e): it's applied towards the reduction of SPS.

And the capital requirements are met with the regulatory and statutory capital metrics Core Capital, Total Capital, CET1 and Tier 1 Capital in any financial institution in the world, not with the Net Worth and not with the invalid in the FHEFSSA "Capital Reserve", that is only used for the balance sheet of the Federal Reserve and called "Capital Surplus", with a statutory limit of $6.825B (a reduction from $7.5B was enacted by law on May 24, 2018: The Economic Growth, Regulatory Relief, and Consumer Protection Act. Its limit is changed from time to time).

FnF don't have these statutory limits in the Charter Act and the SPSPA isn't a law. This is why the FHFA and the UST cannot establish limits in the "Applicable Capital Reserve" with fact sheets or agreements, that the plotters call "contracts". Evidence that it was all part of the Separate Account plan.

By the way, adjusted Capital Reserve= $0 (adjusted for the offset attached to the $125B SPS LP increased for free). So, an invalid capital metric and badly assessed. Nice going!

That's a lie. FnF are NOT rebuilding capital,but SPS.

This SPS LP increased for free in the same amount as the Net Worth increase, is absent from their Balance Sheets (Financial Statement fraud).

A capital distribution restricted. Then, necessarily the Common Equity is held in escrow pursuant to the 12 CFR 1237.12, that, at some point, it'll be unwound. That's recapitalization (CET1).

The evidence is on everyone's desk this time:$4.8B x3.

EXHIBIT A: Dividends are a Change in Equity.

The Income Statements reflect the result of operations during a period. The bottom line is Net Income. A different financial statement is the Balance Sheet, a picture of a company at a determined date.

There are two exceptions when changes in Equity must be reflected on the Income Statements, but separately from the operations during the period ("outside").

Under accounting rules, the companies are compelled to put more data in the Income Statements, so the shareholders have a better picture of what has happened with their companies during the period, that otherwise would go unnoticed and give a false impression about the financial health of their companies.

This is why FnF don't post only the Net Income that would make the companies be subject to the current con operation by renowned hedge fund managers that make a Guirdo write:

They have consistently earned over $10 per share the last 11 years

Bradford caught peddling the same lie as Ackman yet again, in his latest SA article.

Bill Ackman: "FnF continue to build capital through Retained Earnings" (Source), based on the Financial Statement fraud in FnF that don't post on the Balance Sheets the SPS LP increased for free and its corresponding offset with reduction of Retained Earnings account (Organized group).

With the adjustment, FnF are building SPS in their Net Worth, not regulatory capital, and it exposes that, necessarily, the Common Equity is held in escrow, and the same occurred with the dividend payments to Treasury since day one, as both are capital distributions restricted, when the exceptions kicked off to legalize these payments: reduction of SPS and recapitalization (both in a Separate Account)

The lie of a new paradigm since the September 2019 SPSPA amendment, for which the attorney David Thompson even seeks "constitutional damages" in court with the Bhatti and Collins cases, contending that FnF are being recapitalized since then and the "for cause" removal restriction prevented it from happening sooner, when, first of all, it was initiated by Mel Watt and Mnuchin with a one-time $3B SPS LP increased for free on December 2017 (4th SPSPA amendment).

Always the same lie peddled by the "Canasta game" group, that later wants to meet the capital requirements with the capital metric Capital Reserve (invalid in the FHEFSSA. Adjusted Capital Reserve = $0), pursuant to Mnuchin-Calabria's "Capital Reserve end Date" in the January 14, 2021 SPSPA amendment, that has ended up with the former FMCC CEO, Layton (currently a blogger in the Harvard School of Cheating), asserting that it's the Net Worth the one that has to meet the capital requirements (he changed to layman terms, so the average Guido can understand the debate)

Freddie could be considered recapitalized when their net worth hits $150 billion

the mortgage giants long ago repaid the $191 billion taxpayer bailout, plus interest.

My group is considering lawsuits against FHFA.

BRADFORD'S SA, SPONSORED BY @BillAckman

— Conservatives against Trump (@CarlosVignote) February 17, 2024

🆕paradigm:"FnF remain in Conservtrshp since 2019",brain cracking, despite

-NW increase=SPS increased for free

-1st,Watt-Mnuchin's $3B in Dec 2017

-SPS & offset(↓Retained Earnings)absent from the Bce Sheets

-$0 EPS as a result👇#Fanniegate https://t.co/4xuRHwTUKT pic.twitter.com/DgK4lPN1f3

Are you aware that FnF post $-68B Core Capital?

That's the official figure posted in their ERCF tables (image below), as seen in their Earnings reports.

The Core Capital drops to $-194B with the adjustment mentioned before (Reduction of $125.4 in the Retained Earnings account) when someone issues/increases stocks for free. For instance, FnF with the initial $1B SPS issued for free, debited from the Additional Paid-In Capital account (Core Capital as well), an account now exhausted:

A whopping $402B capital shortfall over $208B minimum Leverage Capital requirement.

Again, you must be talking about different companies:

they'll have plenty of reserves to soon redeem the preferred at par.

Are you aware that their Retained Earnings accounts stand at an Accumulated Deficit $-91B together (Balance Sheets)?

Then, adjusted for the offset (reduction of Retained Earnings) attached to the $125.4B SPS LP increased for free since December 2017, both operations absent from the Balance Sheets (Financial Statement fraud), so Bill Ackman and his subordinate, Glen Bradford, can peddle the lie of: "FnF continue to build capital through Retained Earnings", it stands at $-216B.

An account that has to absorb future losses and where the dividends are distributed from.

You must be talking about different companies.

Even if they pay just $5 dividend per common share

Are you aware that FnF post $0 EPS every year?

They have consistently earned over $10 per share the last 11 years.

The CRT operations are NOT among the enumerated ones authorized in the Charter Act.

PLMBSs, barred as well, by the way.

Unlike the recent Commingled securities, 100% guaranteed against default (number 3). The way to go.

The DOJ, vicariously responsible, which means that it'll have to make this claim whole. No one cares how it will do it.

Likely, a backdoor fee syphoned off to Treasury, following Mnuchin's slogan "the taxpayer be appropriately compensated", which is fine, but it's NOT authorized in this Charter that only authorizes a rate similar to Treasuries on any redeemable obligations, including the SPS.

Or likely, a backdoor Housing Finance System revamp imposed by Michael Bloomberg, which is even worse.

Again, no one cares. It's capital necessary to absorb future losses.

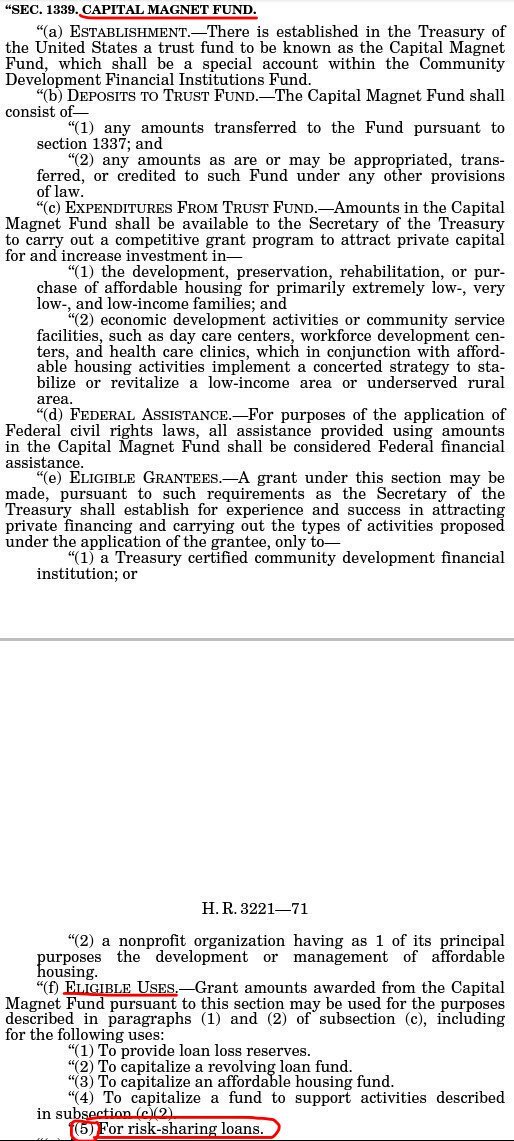

The law only authorizes the UST to do CRTs with its own money, not FnF's, with its portion of the 4.2 bps, sent to the Capital Magnet Fund.

The FHFA has no authority to circumvent the law. No "best interests" can override a statutory restriction.

This has been explained a thousand times.