News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Wise Man

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

The common stock par value was reclassified in the third quarter of 2008 earnings reports, to Additional Paid-In Capital account.

Then, it was reduced (which is a reduction of Core Capital and thus, a breach of the FHFA-C's Rehab power) with the following amounts:

- The $1B worth of SPS issued for free on day one. Like any other stock issued or increased for free (today's SPS LP increased for free, absent from the balance sheet to evade this operation. Financial Statement fraud), there is an offset that reduces the Core Capital.

Hank Paulson needed this gift on day one, not only to reduce the Core Capital and justify the conservatorship under the discretionary authority of FHFA with "(G) LOSSES: likely to incur (fabricated) losses that deplete all of its capital", but also to begin with another Securities Law violation with the SPS LP increases, instead of issuances and purchases, in order to skip the deadline in the temporary authority of Treasury to purchase securities/obligations of FnF, of December 31, 2009, with a high yield, necessary for the Separate Account plan (later the original rate similar to Treasuries is the one that prevails: assessed at a weighted-average 1.8% cumulative dividend rate on SPS, applying a 0.5% spread over Treasuries)

- The value of the Warrant ($2,304 million in Freddie Mac) to purchase 79.9% of common stock for $0.00001 per stock (A collateral of the SPS, to (iii) protect the taxpayer). Again, like any security issued for free, it carries an offset.

We see also one of the 7 securities law violations, because the value of the Warrant was also credited to the Additional Paid-In Capital account, when it should only be debited from that account.

HOW TO UNWIND IT

There is no need to put the value of the common stock par value back in its place once the Separate Account is unwound, because most of the companies operate with no par value common stock.

Not even back to Additional Paid-In Capital account, because the value that was eliminated, will be recovered once it's reflected on the Retained Earnings account that belongs to them.

All of them are part of the Common Equity.

It seems that Howard feels comfy with Brainard playing along.

Common stock par value and Common Equity are different things.

The Common Equity belongs exclusively to the common shareholders, also known as the Book Value of a common stock.

Hence, we calculate a Book Value Per Stock (BVPS).

It seems that you have never read that Book (Balance Sheet), because I already explained it to you here.

Even I calculated $JPM's Price to BV ratio for you: 1.8 times, knowing that you would never make it on your own.

FnF operate business as usual during Conservatorship.

A UST backup came to substitute their light capital requirements as a result of a subsided guarantee-fee.

Everything changed with the UST's 3-option Privatized Housing Finance System revamp in 2011, as "recommendations on ending the Conservatorship", at the request of the Dodd-Frank law.

Now, the UST backup is pointless and their Public Mission outdated.

Charter-revoked wording in the very 2011 Report to Congress.

FnF don't compete with the banks. FnF help them to off-load mortgages from their balance sheets, so they can continue to lend out.

FnF compete with others that have a securitization platform, like Blackrock.

The commingled securities were created to fuel competition, for those that lack a Securitization Platform and also in the sale of their products if the market requires Reinsurance by FnF.

This is why Blackrock is involved in the Fanniegate scandal, with the CRT (Craig Phillips) and sending people to the White House, like Brian Deese, to conceal the Separate Account plan. Just what you are doing, Bradford.

Notice that CSS could operate globally once it's IPOed, and Blackrock has huge business with the ECB's fraudulent activities across the board, and with other countries/governments.

Trump is the cheater (mastermind of the phase 3 in the Separate Account plan: SPS LP increased for free holds the Common Equity in escrow. It began with Watt-Mnuchin).

The shareholders' worst-case scenario (99.99% dilution).

Trump did write in his Nov. 21 letter that he plans to release the twins so that hard-working Americans will no longer be cheated out of their retirement savings.

It was an expense in Q3 of 2023 under accounting rules.

But, as capital distribution (an expense unrelated to the normal operations and, considered so by regulation), it's a restricted payment.

Restricted for a reason as pointed out before: build capital.

Yeah, we know. "Zing!" (FHFA-C's Incidental Power)

The Book Value is also adjusted for the Lamberth rebate.

+$0 billion in Fannie Mae ($491 million gross. A deductible expense. It has been added up the net amount. That is, turned into Retained Earnings account) and +$0 billion in Freddie Mac (313 million gross).

BV($B)FMCC/FNMA:110/134

— Conservatives against Trump (@CarlosVignote) March 11, 2024

-1.2/19.5 Beginning bce 6/2008

+83/98 Acc.Comprehensive Income,adjusted for 3 Accounting Change charges:

4/2009:5/3

1/2010:-11.7/3.3

1/2020:-0.24/-1.1

+10/9 CRT,net(RE)

+19/7 PLMBS settlement:73%/27% based on AOCI in 6/2008

+0/0 Lamberth rebate.#Fanniegate https://t.co/EmZTYgahAE

except to the extent the director determines is in the interests of the conservatorship.

"KEEP TALKING" was a response to Mark Calabria.

The CONGRESSIONAL FINDINGS mentioned, is the point (5). Laughable.

KEEP TALKING

— Conservatives against Trump (@CarlosVignote) March 14, 2024

Established as an independent agency of the Federal Govt.

Limited powers under the Charter Act/FHEFSSA.

Section CONGRESSIONAL FINDINGS:@FHFA,sufficient autonomy from FnF (15-yr Conservatorship)and Special Interest Groups(@Moelis,@urbaninstitute,JPS hldrs)#Fanniegate https://t.co/m0aKlThEU2 pic.twitter.com/etI2UAOHk0

The Charter Act dynamics at a glance.

They can only say "sponsored",which doesn't allow them to mess with their mortgages and activities.

— Conservatives against Trump (@CarlosVignote) March 14, 2024

The backup relates to a UST backup of the enterprises to finance their operations as a last resort👇at rates ~to Treasuries, in exchange for their Public Mission(nowadays outdated) pic.twitter.com/E9T9vLm75s

I've realized that FnF also include the Prescribed Capital Buffer to calculate the Capital Shortfall, as seen in the figure that was posted for the last time with the ERCF of June 30, 2023.

They haven't read the explanation from the FHFA in the Capital Rule, of being a cushion above the capital requirement. It isn't a capital requirement. There is no "Total Capital requirement", but a minimum capital requirement. The other portion is a cushion.

As always, there are people playing with the words, because there is a capital metric called Total Capital = Core Capital + ALLL.

Also, there is a Minimum Capital Level, now called Leverage ratio, that Howard wants to pass it off as the minimum capital requirement for the Risk-Based capital requirements, so, all of a sudden, the Minimum Capital Level disappears. This is because he focuses on the Risk-Based, to peddle the bank-like rhetoric and bash the Capital Rule, when the binding capital requirement is the Leverage ratio, because it's higher.

What it looks like, is a regulator pretending to manage the enterprises it regulates, taking the place of the management.

For instance, in an amendment of the Prescribed Capital Buffers one year later, the FHFA confirms that it's just a gauge to control the capital distributions of the enterprises, like dividend payments, when the company operates business as usual.

That's not the role of a regulator. It must establish a minimum capital requirement and be ready to require Prompt Corrective Actions upon breakout (not a 3-notch jump in the Capital Classifications or a Mnuchin-style OFF MARKET deal at a time they are Adequately Capitalized. If any, it's upon Significantly Undercapitalized, but a Rights Issue first).

Another reason of the existence of capital buffers, is stated in the Captial Rule:

To mitigate the inherent risks and limitations of any methology for calibrating granular credit risk capital requirements.

The Warrant has been explained a thousand times before.

- The objective was the assault on the ownership by Wall Street and the Community Banks.

- Issued for free to skip the prerequisite in the authority of UST in purchases of securities, of collateral for this security.

-Etc.

Contract, void.

Security, cancelled.

For instance, here.

De facto Charter-revoked wording in the White House Budget proposal.

.@WhiteHouse BUDGET WAIVES THE CHARTER ACT WORDING

— Conservatives against Trump (@CarlosVignote) March 12, 2024

"Housing finance policy that increases the supply of housing that is affordable for low- and moderate-income households"

1946 national goal re housing supply.

FnF no longer mandated to buy loans at a subsidized g-fee.#Fanniegate pic.twitter.com/fKi5kI1jL0

"Bloomberg Intelligence or lack thereof" forms part of a long list of market participants that include the Prescribed Capital Buffer to assess the capital shortfall, when that portion isn't a capital requirement. Like BOA.

A capital buffer is a cushion to prevent a company from breaking out the capital requirement that would trigger Prompt Corrective Actions (Does Restriction on Capital Distributions like dividend payments, gifted SPS and the Lamberth rebate ring a bell?)

A capital buffer isn't a capital requirement for the Capital Classifications, and it's only valuable to determine the Payout ratio, in the case of FnF (Table 8: the dividend is suspended if the capital buffer < 25% of the Prescribed Capital Buffer). So, now the dividend payment is more stringent.

This is the treatment of the management like Kindergarden. The Capital Buffers should be eliminated, making sure that the Prompt Corrective Actions are activated when a company becomes undercapitalized, not the 3-notch jumps in the Capital Classifications we are used to, or an OFF MARKET deal like Mnuchin with $NYCB pretending that it was undercapitalized, when its capital ratios were pristine as of end of december 2023 and thus, there was no need to raise capital. Let alone that it must be done solely through a Rights Issue to avoid these conspiracies by the same people over and over again that want to impose their own rules. That is, any common stock must have Preferential Subscription Rights because that's inherent to a common stock.

This is why Blooomberg wrongly claims that the capital shortfall over Risk-Weighted Assets of $161B in Freddie Mac and $243B in Fannie Mae, measured with the "Adjusted Total Capital".

The official numbers of capital shortfall posted in their ERCF tables as of December 31, 2023, are $110B in Freddie Mac and $164B in Fannie Mae, had they posted the column "Capital Shortfall" because they no longer post it for the fraud of peddling the idea that the capital requirements are met with the Capital Reserve or with the Net Worth. Below, it's posted the ERCF table as of June 30, 2023, to see this column for the last time.

They also ignore that the official numbers have to be adjusted for the offset (reduction of Retained Earnings. Core Capital) attached to the $125B SPS LP increased for free in FnF together by Mnuchin/Trump - Calabria, but first a one-time $3B SPS LP for free with Mnuchin/Trump - Watt on December 2017.

Therefore, the capital shortfall is worse than the one officially posted.

June 30, 2023:

.JPG)

At least, Bloomberg Intelligence or lack thereof, has exposed the scammers that are using the FHEFSSA-invalid capital metric "Capital Reserve" that is only used by the Federal Reserve (Capital Surplus), and also the fact that the conservatorship isn't in compliance with the Supreme Court's prerequisite of "rehabilitation of FnF" with such awful ERCF tables that correspond to Justice Alito's out-of-the-box remark: "in a way not in the interest of FnF" on paper, to legalize the Separate Account plan, aiming the add-on "and the public it serves" for the utilization of FnF for public policy ($15B owed to FnF for the MHA program will have to be condoned; Sale of loans to women- and minority- owned businesses, LGTB associations, etc).

Good! But, at some point, the Separate Account plan will have to be unwound to see the financial rehabilitaion of FnF for real (on their Balance Sheets).

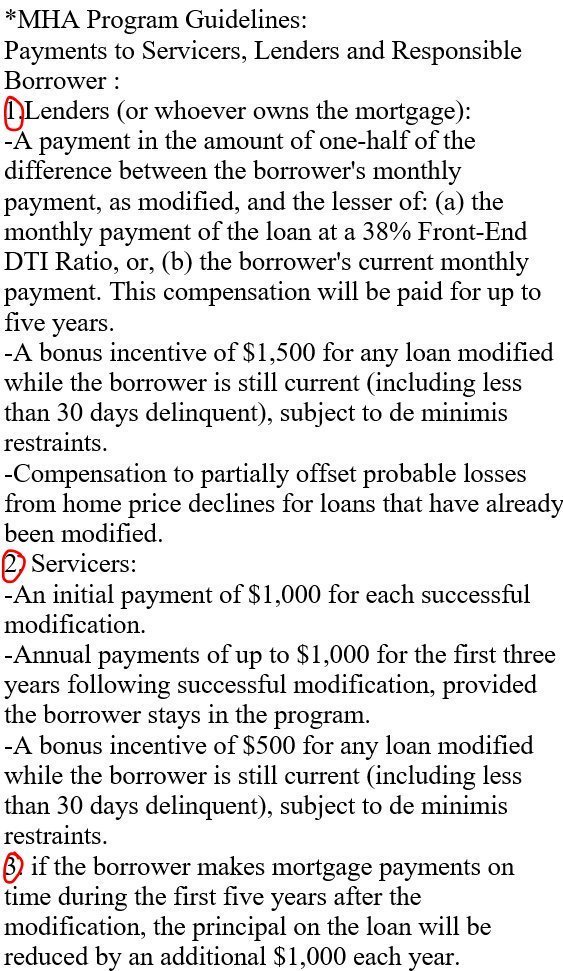

As a reminder, these are the guidelines in the Making Home Affordable program. FnF advanced payments to servicers (banks) and borrowers, later Obama forgot to pay the bill.

Big bank bonuses in the banks those years.

FnF have their own programs and foreclosure prevention actions.

Besides, in cash-out refinancings the only harmed parties are FnF.

22% of new acquisitions were cash-out refinancings during the latest boon in refinancings.

Therefore, we aren't talking just about a $200,000 worth of refinancing or so. The borrower can end the day taking home up to 80% of the value of the property in cash (80% LTV limit in the credit risk, under the Credit Enhancement clause of the Charter Act. Because there is no longer PMI, the loan is capped at 80%.)

FnF are a harmed party because the lender is using the collateral owned by FnF (the property) to back up this second-lien loan. So, it's doing business with an asset owned by FnF. More evidence of collateral scrapped pointed out in my prior comment. Collateral-sharing in this case, which is the same.

The thing is that the Charter Act allows FnF to do second-lien loans: "To lend on the security of a mortgage".

Even Freddie Mac stated:

We are not entitled to receive notification when a borrower obtains second-lien financing.

The flat fee is discarded if they are on the hook for the mortgage loan dollar amount, in the case of fraud.

FnF aren't in the business of Title Insurance. It could be deemed a credit enhancement operation barred in the Credit Enhancement clause of the Charter Act, like the CRT operations and, by the way, the prior PLMBS.

It should be a flat fee because the service provided relates to a deed, not the mortgage loan dollar amount. And, if it's a high cost, is an issue for the Judiciary Committees in the House and the Senate.

In refinancings, it drops to 0.4%, I've found out. Yet, a notary is still necessary because it's a new mortgage loan. A new deed.

The letters of opinion by attorneys are worthless and subject to conspiracies.

Can you imagine the Fanniegate attorneys accused of abuse of court process in their frivolous lawsuits aiming to rip off the shareholders, Brydon Fisher, David Thompson, Hamish Hume, etc., signing an attorney-opinion letter?

There is a reason why a notary exists.

The U.S. is slashing everything that adds up to protection, like a collateral in:

-Unbacked crypto scam,

-Money printing without Forex reserves to back it up.

-Sale of NPL or RPL without taking possession or considering the REO-collateral (RPL bundled into UMBS again)

-Let alone backing up the European allies in fraud, with their fraudulent ECB Payment Systems Target 2 and TIPS, where no one pays its bills. A scheme attached to their EURO cryptocurrency called "Book Money" with an exchange rate 1:1 with the Euro (Postings in the banks' accounts at the ECB, converted into euros only when it exits the ECB balance sheet) that, because it isn't legal tender, it isn't recorded in the statistics of Money in Circulation (M2) (Financial Statement fraud? Sounds familiar?)

Or, in this case, the figure of a notary.

Evidence that Howard attempts to discredit Secretary Yellen, in favor of the NEC Director, Lael Brainard.

Besides Bradford's remark: "Yellen is clueless on housing". Source in a post promoting next Tuesday's event at the Urban Institute headquarters with Lael Brainard.

Timothy Howard in one of his latest comments in his personal blog, we can read how he tries to discredit secretary Yellen, when she said "not knowledgeable" when asked in a congressional hearing about the possibility of monetazing the Warrant. She simply wanted to stress immediately after, that she has "staff that spends great amount of time thinking about it".

We can see how Howard aims to favor the hedge funds' choice, Lael Brainard, when he, at the same time he attempts to discredit sec. Yellen, emphasized that he wants "the initiative to come from outside the FHFA and the Treasury, someone at the NEC, CEA or potentially the Office of the President"

This is why the hedge funds' social media crew repeats that POTUS is the one to release FnF from conservatorship, when it's an issue solely for the conservator, working with Congress as it was chosen by the UST in 2011, a Privatized Housing Finance System revamp for the release (which means Basel framework for capital requirements), at the request of the Dodd-Frank law, and there are many scenarios to ponder.

JOoaoky, one of the 20+ aliases from a renowned plaintiff yesterday:

Even if Trump were to release FnF... it would be at least 12-18 months into his presidency.

Have to settle in and get all the people into place.

Has the White House turned into a think tank?

The White House NEC Director, Lael Brainard will attend an event at the Urban Institute headquarters next Tuesday, to promote this think tank.

It turns out that Biden's proposal at the SOTU speech, contending that FnF self-insure the Title Insurance, was written by UI three months earlier:https://www.urban.org/urban-wire/rethinking-title-insurance-could-dramatically-lower-costs-homebuyers

Has the White House ever met with the Judiciary Committees in the Senate and the House, or with the Democrats in Congress to pull ideas together, instead of meeting with these lobbyists, whose interests aren't aligned perfectly with the broad interests of the American economy?

This is why Bradford and Timothy Howard are harassing UST secretary Yellen, in favor of Lael Brainard.

"Yellen is clueless on housing" from Bradford.

Timothy Howard in one of his latest comments in his personal blog. We can read how he tries to discredit secretary Yellen, when she said "not knowledgeable" when asked about the possibility of monetazing the Warrant. She simply wanted to stress immediately after, that "she has staff that spends great amount of time thinking about it", and aiming to favor the hedge funds' choice, Lael Brainard, when he emphasized that he wants "the initiative to come from outside the FHFA and the Treasury, someone at the NEC, CEA or potentially the Office of the President"

This is why the hedge funds' social media crew repeats that POTUS is the one to release FnF from conservatorship, by the way, when it's an issue solely of the conservator, working with Congress as it was chosen by the UST in 2011, a Privatized Housing Finance System revamp for the release, at the request of the Dodd-Frank law, and there are many scenarios to ponder.

Urban Institute is a Special Interest Group doing political lobbying in broad daylight, with all the Investment Banks and hedge funds backing it up.

They know the trick in CARES Act of "Federally-backed mortgages", making sure that they don't change the reality of mortgages 100% guaranteed by FnF themselves and not by the United States, as expressly written in the Charter Act.

This is why the say "backing", but it refers to FnF having a UST backup as a last resort in their congressional charter that later they conceal, in exchange for a Public Mission regarding secondary market operations, not to waive protections like the Representations and Warranties obligations by the sellers of mortgages to FnF, self-insure the Title Insurance or to come up with a Title Opinion letter signed by attorneys, instead of a formal deed signed by a notary. 3 ideas pointed out in the UI's piece.

- The Charter Act doesn't authorize FnF to self-insure the Title Insurance.

- The FHEFSSA of 1992 "CONGRESSIONAL FINDINGS" section, requires FHFA to have sufficient autonomy from these Special Interest Groups (let alone the "Meeting with Moelis and Company LLC"

- HERA makes clear that the FHFA (as successor of OFHEO) is established as an independent agency of the Federal Government. It hasn't changed with the SCOTUS opinion.

Bradford-LuLeVan now claims the hedge funds dump shitbags of JPS on clients.

That reminds me the former Blackrock and Morgan Stanley executive, Craig Phillips, in this Rolling Stone piece, denouncing that he dumped "shitbag CDOs on clients".

https://www.rollingstone.com/politics/politics-news/man-trump-named-to-fix-mortgage-markets-figured-in-infamous-financial-crisis-episode-109861/

Craig S. Phillips, then president of the Asset Backed Securities division at Morgan Stanley, was the man Donald Trump put in charge of reviewing Wall Street rules and GSE affairs, as counselor to the Treasury Department.

He attended the 2nd CRT Symposium, when the CRT are barred in the Charter Act, the reason why we are requesting a refund of the CRT expenses, net.

In early 2007, a group of Morgan Stanley bankers bundled a group of subprime mortgage instruments into a package they hoped to sell to investors.

Phillips headed a division that sold billions of dollars of mortgage-backed investments to Fannie and Freddie. Many of those investments were as bad....

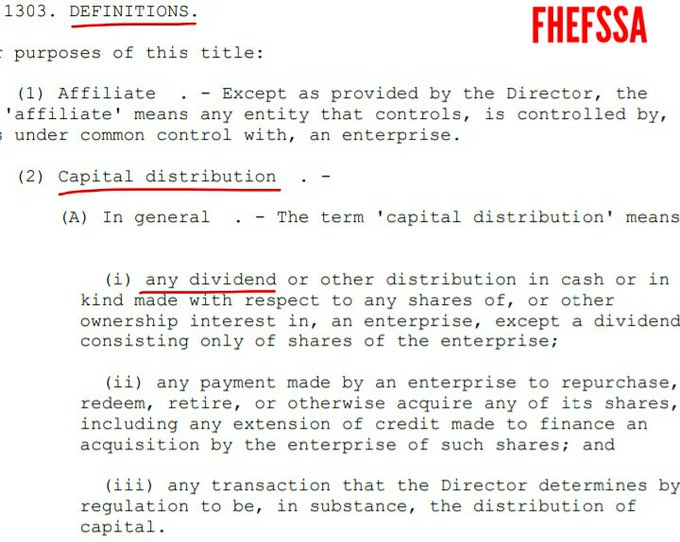

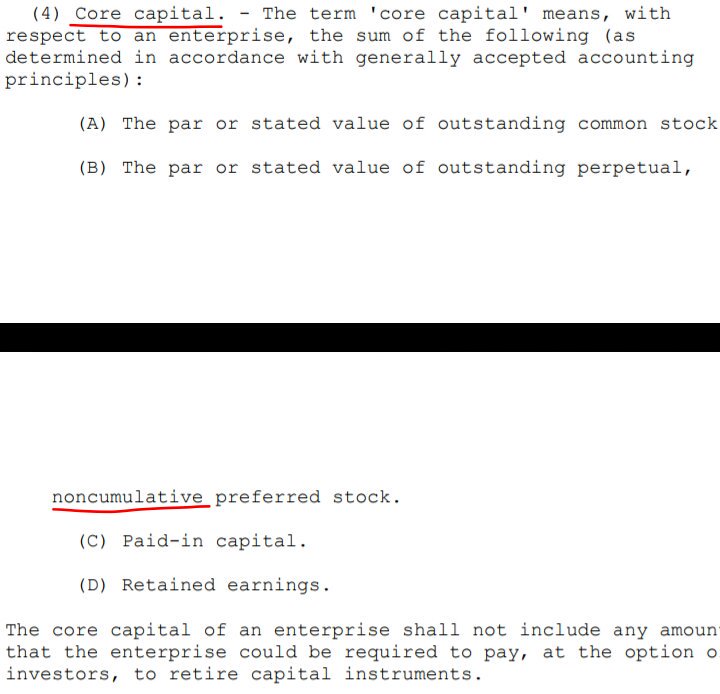

There is no definition of Core Capital in HERA, but in the FHEFSSA of 1992. A law enacted exclusively for Capital adequacy matters.

The definition of core capital in HERA.

TAKING+RESALE +JPS REDEEMED:$178B PROFIT

— Conservatives against Trump (@CarlosVignote) March 5, 2024

+$13B extra Corp Tax(Deferred Income)$FNMA/ $FMCC

Price;PER;BV;Mkt Cap

-Existing shareholder

$116/$170;7/8;1/1;$134B/$110B

-UST

$186/$317;11/14;1.6/1.9;$216B/$206B

-Buyer(Amortization of DI)

$173/$266;10/12;1.5/1.6;$201B/$173B#Fanniegate https://t.co/mqKqepObPX

The hedge funds are nervous, posting the Trump letter like mad.

I'm wondering if they think they can fool even one person.

Free title insurance fees? That's basically a Notary fee.

Thus, they aren't charged by FnF.

Take into account that the Title Insurance fee drops markedly in refinancings (0.4%), but it's still necessary, because the old mortgage disappears and you have to take out a new mortgage loan. A notary is necessary again for the new deed.

They aren't junk fees and a notary can't work for free. If they are high, then it's an issue for the Judiciary Committee in the Congress.

Who did come out with this idea? Someone read "fee" and that's it! Let me guess. Urban Institute's Parrott, a think tank selling ideas to the White House.

Anyway, the FHFA is an independent agency of the Federal Government.

MORE EVIDENCE of a Separate Account with FnF, FHLBanks-style.

When the word "separate" becomes an obsession.

Below, there is a statement from the FHFA explaining the announcement on August 5, 2011, when it solemnly declared that the FHLBanks "fulfilled their obligation to pay interests" (That was Funding Corp, not their Equity holders, the FHLBanks. So, the principal of the obligation RefCorp remains outstanding). Source.

Unaware that their Separate Account was for the reduction of the principal of the obligation RefCorp, not for the payment of interests. Source.

In that press release, the FHFA also unveiled a plan to build capital through Retained Earnings. Notice that it's dated just two weeKs after the effective date of the Final Rule that paved the way for the continuation of the recapitalization of FnF also in a Separate Account, once the SPS were fully repaid (phases 1 and 2, with the statute), enacting the July 20, 2011 CFR 1237.12. The difference is that, with FnF, the follow-on Recap plan was kept secret (no press release. You have to find it out yourself in the Final Rule)

This is how the FHFA explained the Recap plan of the FHLBanks, even making up the concept of "separate Retained Earnings account" within a Balance Sheet, when that's impossible. Everything is posted together and a separate Retained Earnings account doesn't exist, regardless that now, I bet that JPM has formed a task force to claim otherwise.

All forms part of the same Retained Earnings account and you can't even say that it's restricted, so that the shareholders don't take that money away through a special dividend. This isn't serious and the shareholders and the managements aren't in kindergarten.

As long as it shows up on the Balance Sheet, you can call it whatever you want "layman's terms".

The problem is in FnF, when "separate" means that it's outside the balance sheet, like the SPS LP increased for free and its offset absent from the balance sheet. That's financial statement fraud and stock price manipulation.

At some point, it'll have to be unwound, in order to comply with the statutory provisions: restriction on capital distributions, Rehab power, etc. and it'd be a case of Separate Account plan "in the best interests of the FHFA".

It shows an obsession. A global pandemic: the Bundesbank's External Position with the other european central banks, to hide the Claims/Liabilities in their flawed Payment Systems Target 2 (between central banks) and TIPS for the Local governments (TIPS known also as debt hidden in the drawers)

No one can say that the SPS were repaid as if by magic, because that's asking for the debt be condoned, Argentina-style.

You have to back it up with a statutory provision.

The SPS are the taxpayer's assistance to finance their operations as a last resort, as contemplated in the Charter Act dynamics, that must be repaid fast.

FnF are not ordinary businesses.

They were repaid through the exceptions to the Restriction on Capital Distributions and the fact that no Earnings were available for distribution as dividend, out of an Accumulated Deficit Retained Earnings account.

Therefore, FnF sent, in reality, assessments to the Treasury, 1989 FHLBanks-style (statutory provision entitled SEPARATE ACCOUNT FOR THE REPAYMENT OF PRINCIPAL OF THE OBLIGATION) in the form of capital distributions and under the guise of dividend payments (NWS dividend, the fastest speed to that end, as the 10% dividend prompted the "death spiral": in many quarters, the dividend was the reason of the capital deficiency (negative Net Worth) and subsequent draws from the Treasury 1:1 SPS LP increase, draining the Funding commitment. The NWS dividend solved this issue. Similar to the FHLBanks bailout, when they didn't have to send the assessment to a Separate Account, when they posted losses.)

The FHFA-C's Incidental Power allows it to mislead the world "in the best interests of the FHFA", if the endgame is the financial rehabilitation of FnF, as literally stated by Justice Alito ("Rehabilitate FnF....") and judge Willett ("Any action within the enumerated powers": Rehab power).

Judge Sweeney (CFC chief judge at the time) was more rogue in a prior ruling. This is why the 5th Cir. and the Supreme Court came to debunk her flawed ruling, after watching that she was being called "The Tipp-Ex Queen" on social media, because she simply erased the "authorized by this section" in "take any action authorized by this section".

We cannot lose track of the statutory provisions, like the U.S. Code §4614(e), FHFA-C's Rehab power, Charter's Purposes/dynamics,.... and regulations: CFR 1237.12 that "supplements and shall not replace or affect the one by statute" in a 2011 Final Rule "for the transparency of Conservatorship" (Tweet below).

Let alone the mandate to UST to come out with "recommendations on ending the conservatorship" and its Report to Congress as a result.

Likewise, we cannot lose track of each amendment of the Purchase Agreement: it's very important when, what and why was done, playing with the "Applicable Capital Reserve" that continues through today.

For instance, this is my post yesterday, explaining that Mnuchin and Trump are the masterminds of the 3rd phase of the Separate Account (SPS LP increased for free. Also that these gifted SPS LP and its offset are missing on the Balance Sheets) and the scam of capital requirements met with Capital Reserve, adding an additional evidence in the next post: Mnuchin Treasury recommended Congress to repeal the FHEFSSA definitions regarding Capital adequacy.

Also it explains the 3rd, 4th, 5th and 6th PA amendments.

We cannot allow Fanniegate to come down to "layman's terms" for a cattle market-style negotiation, also known as chess game (Gimme that I give you that. You do that, I do that. Dothat, dothat. Dothatdothat,...), which is what the footman Guido and Bryndon Fisher are up to, under the orders of their boss, Pagliara, making the legal defense for the corrupt litigants that have deliberately waived the financial concepts behind (Felonies of Making False Statements and stock price manipulation), even it's been done shamelessly, with Gary Hindes removing the breach of FHFA-C's "statutory mission" (Rehab) in an amended complaint (PROOF), when he realized that the 10% dividend that he defended was the same breach and was told to amend it and that the Supreme Court was activated to play with the Incidental Power instead: "Beneficial to the FHFA", instead of what is written "best interests of the FHFA", to play the hedge funds' game of a Govt theft story (monetary benefit) and their paid shills: Guido in his daily tweets harassing the lawmakers when he replies to them with: "WE'VE BEEN ROBBED! Weeee!".

That's the taxpayer's assistance you are talking about. Fair value=all of it.

— Conservatives against Trump (@CarlosVignote) March 8, 2024

SPS 1:1 draws from UST, fully repaid as of end of 2013/2014 (FMCC/FNMA). Phases 1/2 (10%/NWS divs) using the exception to the Restr.on C.Distr.

The rest(gifted SPS),a joke. Phase 3:For Recap.#Fanniegate https://t.co/xPb2F1LyBe pic.twitter.com/tPEcH77RmG

Besides, the $NYCB "rescue deal" has Pagliara's stamp on it.

It contemplates the issuance of Warrants to the existing shareholder, which is similar to a Rights Issue, as both give the right to purchase common shares at a determined price. The difference is that a Rights Issue allows the shareholders to maintain the current percentage of ownership and, secondly, the issuable shares have Voting Right, whereas the Mnuchin's plan for $NYCB are non-voting common shares that will trade at a different price (Class B shares).

Also, it's a 7-year warrant, whereas in a Rights Issue, the company raises Capital in a matter of weeks (each common stock has one right to buy X shares. These rights would trade on the Stock Market for a few weeks. If you don't want to participate in the Rights Issue, you sell your Preferential Subscription Rights on the market or the company sells it for you on the last day).

They can argue that their Beneficial Ownership won't change much with the Warrant, because under SEC rules, it doesn't matter the Voting Right for the Beneficial Ownership of FnF, as I commented on Saturday. It doesn't mean that you have to strip it out.

Tim Pagliara set up a phony Association of Shareholders "Investors Unite" to trick them into a similar plan in Fanniegate, proposing to throw in some Warrants to the shareholders.

Do you still think that the consortium of investors led by Mnuchin isn't the same "group" lying in wait for the assault on the ownership of FnF?

Last evidence: The Mnuchin Treasury recommended Congress to repeal the statutory definitions of capital adequacy matters, where is set forth, for instance, that the Minimum Leverage Capital requirement is met with Core Capital or Tier 1 Capital, not with "Capital Reserve".

The FHFA removed the column Capital Shortfall to the same end (an adjusted $402B Core Capital shortfall over Minimum Leverage Capital requirement together)

They rather write their own rules.

2019 UST Housing Reform plan:

It's obvious that the consortium of investors led by Mnuchin wanted to invest in FnF,

Mnuchin would never invest in Fannie and Freddie

the GSEs, with their "socialist business model,"

OFF-TOPIC. They have accumulated a CET1 of 2.7% and 2.8% of Adjusted Total Assets as of December 31, 2023 (Fannie Mae and Freddie Mac, respectively), with a Separate Account plan.

This is the Common Equity generated during Conservatorship.

Below, it's the accumulated figure, with a beginning balance on June 30, 2008. Freddie Mac as well. Here, the 3 charges for changes in Accounting Standards don't show up, in order to not distort the beautiful chart.

Quit repeating that Berkowitz no longer holds JPSs.

It isn't necessary for the payment of Punitive Damages for filing frivolous lawsuits and for stock price manipulation with the Government theft story.

Secondly, you are making the whole thing up. The record date is when the judgment becomes unappealable, according to the court briefs.

Heard delay in judge signing is that Berkowitz lawyers are arguing Bruce should get paid damages even though he no longer holds shares.

You aren't doing any favor to Trump posting his letter.

The Supreme Court didn't opine that a new statement from Trump, is what it's needed to prove constitutional damages.

It's obvious that it was related to a statement when he was in office.

This is fabricated evidence since it was used by Berkowitz's attorney in Court, both in the Collins case and, recently, in the Bhatti case.

Besides stock price manipulation, since he proposes actions not authorized in the law and CFR, for the assault on the ownership of FnF, as it would dilute the common shareholders 99.99% in their companies, and, secondly, against the Supreme Court's prerequisite of the rehabilitation of FnF since day one, synchronized with the prior ruling by judge Willett (take any action "within the enumerated powers": put FnF in a sound and solvent condition, which is what is called financial rehabilitation).

Let alone judge Sweeney omitting the "authorized by this section" in question, in her interpretation of the same sentence of the Incidental Power. So, she just read "take any action ...................... (this part intentionally left blank), in the best interests of FHFA". How is this even possible?

Let's not forget that it's an Incidental Power. It couldn't have been created to override the main power, but the opposite. Its purpose is to help fulfill the main power by definition.

Take their capital away is NOT authorized. Necessary for their financial rehabilitation (Retained Earnings account. Core Capital). Today, adjusted $-216B Accumulated Deficit Retained Earnings accounts together, the only account that absorbs future (unexpected) losses (not the Capital Stocks that just offset a negative RE account, so that the Net Worth remains positive) and where the dividends are distributed from (at least you need to have a positive balance on the Balance Sheet, as a picture of a company on a determined date, to distribute it out. It's not a simple charge like happens with a loss in the period).

The only gauge of the financial condition in a financial company: Does Capital ratio ring a bell?

Notice that the tweet posted below comes from the guy that said: "The Supreme Court said FHFA can do whatever the hell it wants" (Source)

So, all made up.

The same stance by his mentor, Bill Ackman, implying that the Supreme Court said FHFA has absolute discretion (Source)

This is the bread and butter during Conservatorship: coverups, twists and outright lies.

$FNMA #FANNIEGATE --- the supreme court opined that if trump wrote a letter like this that it would be sufficient to show that the statutory provision caused harm. God Bless Trump pic.twitter.com/RQqty13WFv

— Fanniegate Hero (@DoNotLose) November 30, 2021

Hamish_Hume & Co are liable for filing frivolous lawsuits.

Only the conservator can release FnF, working with Congress.

This is because the Treasury Department chose in 2011 a 3-option Housing Finance System revamp as "recommendations on ending the Conservatorship", at the request of the Dodd-Frank law.

Otherwise the Congress isn't necessary either.

The important thing is to don't lose track of the numbers.

"Recap and release" starting now, is Pagliara's scam peddled on this board by his clerks.

It's like, all of a sudden, the 15 years into conservatorship don't exist and all comes down to the outsidiers President Biden or Trump.

If Trump dominates today...

If biden recaps and releases...

Watching the time sequence of Capital Available versus the different thresholds possible for the release from Conservatorship,here, we can come to the conclusion that Bruce Berkowitz was following closer the Separate Account plan and their capital levels, and he withdrew the motion to compel compliance with judge Lamberth's subpoena to Treasury to produce the "hidden documents" that would have uncovered it, in August 2021, when he was told, not only that with the new capital metric added up in the Capital Rule, Tier 1 Capital, the Undercapitalized threshold for the release (2.5% of Adjusted Total Assets) wouldn't be achieved until one quarter later, the 4Q2021 in Fannie Mae, but also that, under the Table 8: Payout ratio, the dividend payments wouldn't be resumed and that's the driver of his holding in Preferred Stocks (it's when their fair value fetches the par value), so the FHFA was thinking of continuing the Separate Account plan and the con operation in court, to the maximum extent possible (point 5 in the time sequence) achieved a few days ago with the laggard Fannie Mae, for a membership cleansing (JPS redeemed) before a Housing Finance System revamp.

Basically that, to the prior Regulatory Risk, he now will have to add Conservator Risk.

It's when Berkowitz went mad and decided to go all in with the Government theft story: A trial for an "Implied in fact contract claim", a Takings case in the Supreme Court through one of the co-plaintiffs, Andrew T. Barrett (petition of writ of certiorary, denied) and turned into Youtuber last week with a video insisting on a despotic Federal Agency to make his Takings case in court.

Let alone a Takings with the attorney-mercenary Bryndon Fisher selling smoke with a "Derivative Takings" claim (on behalf of FnF), already filed by Barrett and secondly, for a common shareholder, a Derivative claim turns into a Direct claim, because all the Net Income posted by FnF is attributable to the common shareholders (all of it, regadless that it's kept by FnF as Retained Earnings later, instead of distributed as dividend), after the dividends to the preferred stocks (contract claim or Direct claim), posting a Google Drive file instead of a document electronically filed in court.

Berkowitz can't have the perception that he can abuse the court process to satisfy his investment cases, and then, get away with it.

This is why all the plotters are liable for the payment of Punitive Damages to the Equity holders.

The "hidden documents" don't exempt the litigants from crippling liabilities, along with the rest of plotters that write formal documents, for the coverup of the key statutory provisions, financial concepts (dividends, a distribution of earnings. Unavailable funds with Accumulated Deficit Retained Earnings accounts) and even the Charter dynamics: a UST backup of FnF to finance their operations as a last resort. Evidently, in exchange for their Public Mission (Everything in the same section: statutory purposes).

Obama has 11,000 Fnma hidden documents

Will we ever see them?

Bradford - how do you feel now that number 1 shareholder Bruce Berkowitz has sold all his shares?

Will we ever see them?

Politico's Katy O'Donnell gets her due response on the Fanniegate hashtag.

The tweet cited is from 2018. This is why her pro-Trump piece yesterday, was another piece commissioned by the plotters to assault the ownership of the enterprises through stock offerings, etc.

That's NOT what a Conservatorship is about.

.@politico's @KatyODonnell_ COMMISSIONED ONCE AGAIN FOR A CON JOB IN #FANNIEGATE

— Conservatives against Trump (@CarlosVignote) March 5, 2024

Now she calls the release from Conservatorship "privatization":"the Govt-controlled Cos could once again become private businesses"

Conservatrshp preserves their status: private shareholder-owned Cos https://t.co/lzoXwRlREl pic.twitter.com/UXA9KrCohf

The settlement of the PLMBS lawsuit is non-taxable income to begin with: Damages awarded for loss of an income-producing asset, not loss of income.

IF YOU ARE SURE THAT THIS HAS NOT BEEN RECORDED AS INCOME

This confirms the Separate Account Plan.

Don't say "raise money" when someone taps the capital markets for funds, because that money could be raised in the debt markets.

You still don't understand the double-entry accounting in a Balance Sheet.

FnF need Equity, not cash. They have tonnes of cash.

This is why, when FnF sent cash dividends to UST, they sent capital (Equity) because a dividend is a distribution of Earnings (Equity.Core Capital). Therefore, the plaintiffs can't ask for a simple cash refund of the SPS overpayment.

If you want to harass the shareholders, we require that, at least, you do it properly, otherwise let other take your place, like Bradford-LuLeVan or the plaintiff Joshua Angel in this board with 20+ aliases.

If they do not need to raise money they will remain on OTC until Conservatorship is complete.

$Overnite 3-month $Share $Appreciation $Plan $FLAGGED $Signed $Order

FOR IMMEDIATE RELEASE

Navy Hedge Fund promoting the hedge fund manager Alec Mazo's tweets once again, for the slogan that I denounced just one day before: "Net Worth is what meets the capital requirements".

These two members of The Group repeat the same gig staged on February 14, 2023:

https://investorshub.advfn.com/boards/read_msg.aspx?message_id=171209916

Alec Mazo must have been warned, this is why now he refers to the amount "on the balance sheets" without specifying which concept is he talking about.

Two approaches, because there is The Bill Ackman Way that calls "Capital Reserve" the amount that has to meet the capital requirement, pursuant to Calabria-Mnuchin: "Capital Reserve End Date".

Alec Mazo has chosen The Sandra Thompson Way, like the former FMCC CEO, Layton: "Net Worth is what meets the capital requirements".

This is why the Capital Shortfall column was removed from the ERCF tables, so that The Group flourishes.

Besides in the ERCF tables, the capital metrics that meet the capital requirements are found in the FHEFSSA definitions of each Capital Classification:

-Adequately Capitalized: Total Capital greater than the Risk-Based Capital requirement.

Total Capital = Core Capital + ALLL (statutory definition. FHFA has added some limits through regulation)

-Undercapitalized: Core Capital greater than the Minimum Leverage Capital requirement. Tier 1 Capital was included in the Capital rule, similar to C.C. (CET1 has regulatory adjustments and it includes AOCI)

-Significantly Undercapitalized: C.C. > Critical Capital level.

-Critically Undercapitalized: C.C. < Critical Capital level.

The Mnuchin Treasury recommended Congress to repeal the statutory definitons regarding capital, so The Group makes up its own rules, as we are witnessing.

The settlement worth $25.5B of the PLMBS lawsuit against 18 financial institutions (a $200B+ PLMBS portfolio sold to FnF with fraudulent information), brought by the conservator on behalf of FnF, has NOT been recorded as income.

It's held in escrow and thus, another evidence of a Separate Account plan.

The FHFA owes it to FnF, less $500 million in attorney fees.

Please, stick to promoting your boss' book with your crazy tweets: "WE'VE BEEN ROBBED! Weeee!".

You are always misleading the retail investor, with:

-Flawed definition of Common Equity: "the common".

Notice that this settlement and the refund of CRT expenses, net, are added up to assess the Common Equity as of December 31, 2023.

-Don't challenge the Warrant until it's exercised. Precisely, it'd be when the ongoing damage since day one (EPS posted on a diluted basis. SEC rule) can't be unwound. The reason why the stocks trade at rock bottom prices, besides the fact that FnF are posting $0 EPS every quarter with the ongoing Common Equity Sweep. He conceals the fact that his boss, Pagliara, and the rest of The Group, are using the Warrant to negotiate with the Treasury a better deal for the JPS.

-Pitch the idea of repurchasing the Warrant.

-Rasing concerns about the economic sense of the CRTs, like Timothy Howard, when those operations are challenged simply stating that they are barred in the Charter Act, Credit Enhancement clause. $19B owed to FnF in CRT expenses, net (turned into Retained Earnings to protect FnF against future unexpected losses = Capital ratio).

-Now, in a response to Navy Hedge Fund (coordination), about the PLMBS lawsuit settlement:

That was booked as income and then swept to the Treasury.

The exercise shares issuable with the Warrant don't compute as shares outstanding to calculate your Beneficial Ownership in FnF, unless you are the holder of the Warrant.

It's explained in the continuation of the screenshot of the SEC rule that I posted yesterday.

Please, don't try to explain financial matters when you haven't checked out the source beforehand.

Just write the disclaimer "Pagliara's clerk", so we know that you are here to mislead the retail investor.