News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

iwfal

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

A weakness in your analysis is that Daxxify is the ONLY there longer lasting toxin on the market and there isn't any timeline out there yet for when, or even if, another will get FDA approval.

If Daxxify isn’t better than Botox, then there is no investment case here.

Daxxify is better product and it lasts longer so I think it makes sense for injectors to charge more.

I think it’s clear that the price cut didn’t get to the consumers as quick as some of us hope.

Specifically, DAXXIFY volume sold in Q4 increased 22% on a quarter-over-quarter basis

CARA

The management of this company is a good example of why you cannot invest in a company just because they have a reasonably good drug (the IV version of the drug is actually approved for pruritis (in T2D), and several of the ph2s of the oral version in other indications have stat sig in primary endpoint). They have an extensive history of poor decisions.

The best ph2 was in Notalgia Paresthetica - hit strong stat sig in primary endpoint of itch reductions, altho secondaries, like sleep disturbance, were mininal efficacy, albeit likely for other reasons. Note that this was at a higher dose than in Atopic Dermatitis.

In the Atopic Dermatitis they did not hit stat sig at any dose and carried forward an intermediate dose, even though a higher dose got a substantially better result and side effects are not huge (constipation, excess urination in Notalgia Parathetica, which used higher dose).

They were pretty clear that their goal was biggest possible indication - hence ignoring the indication with much stronger ph2 results. (At least one of the conf calls was pretty interesting because the analysts were clearly probing with the message 'what in the world are you doing?')

I'll have to now re-assess for any on-going trials (they should have a ph3 on-going in non-dialysis dependent CKD - and their ph2 was partial success (met endpoint, but not for responder version FDA would want in ph3), since I've been ignoring it until the bad trials run their course.

BTW - amusingly they are the only biotech I've seen put out a PR on ESG Report.

re:CAR-T lymphoma risk

I also fault his launch strategy for not being more methodical in addressing the frontalis injection pattern and they should have had a plan in place where KOLs that got access to Daxi in Sept 2022 should have performed various frontalis injection patterns with varying dilutions, and varying unit ratios to Botox (1 to 1, 1.5 to 1, 2 to 1, etc). 100 patients injected objectively by 10 KOLs and followed out 3 to 5 months would have given new injectors a 3 month lead on this learning curve.

they should have had a plan in place where KOLs that got access to Daxi in Sept 2022 should have performed various frontalis injection patterns with varying dilutions, and varying unit ratios to Botox (1 to 1, 1.5 to 1, 2 to 1, etc). 100 patients injected objectively by 10 KOLs and followed out 3 to 5 months would have given new injectors a 3 month lead on this learning curve.

re Diagnostics: That's enlightening and surprising given the heft of the corporate lobby. One would think that this is an easily addressable issue.

No. First you have to have SOME kind of evidence that it works........lol

That’s circular reasoning, no? You have to run the trial to find out if it works.

How many patients? (Was the Jeuveau Extra Strength trial)

The real reason EOLS isn’t seeking FDA approval is that they know the double-dose data can’t stand up to FDA scrutiny. This is also why the double-dose data have not been published.

It’s not scientifically plausible to double the amount of active toxin administered to a patient without generating a concomitant increase in the rate of ptosis, regardless of the amount of diluent used.

Analysts have often asked EOLS what kind of commercial uptake EOLS expects from double-dose Jeuveau, and the answer has always been wobbly, as in “we don’t plan to track that, and we expect most of our customers will continue to use the regular dosing.

This chart is deceptive and intentionally misleading.

I have no doubt that Daxi would shine in the therapeutic section by a wide margin.

But what are they doing about it? They have their first approval and it'll take 10months to roll it out. What?

EOLS can't market any duration data, and cost would be prohibitive IMO anyway.

My hunch is that in a more rigorous larger trial you may get some safety issues popping up but who knows

I still think RVNC has a product edge for aesthetics and an untapped therapeutic market

ABBV EOLS RVNC all down today. Sector rotation???

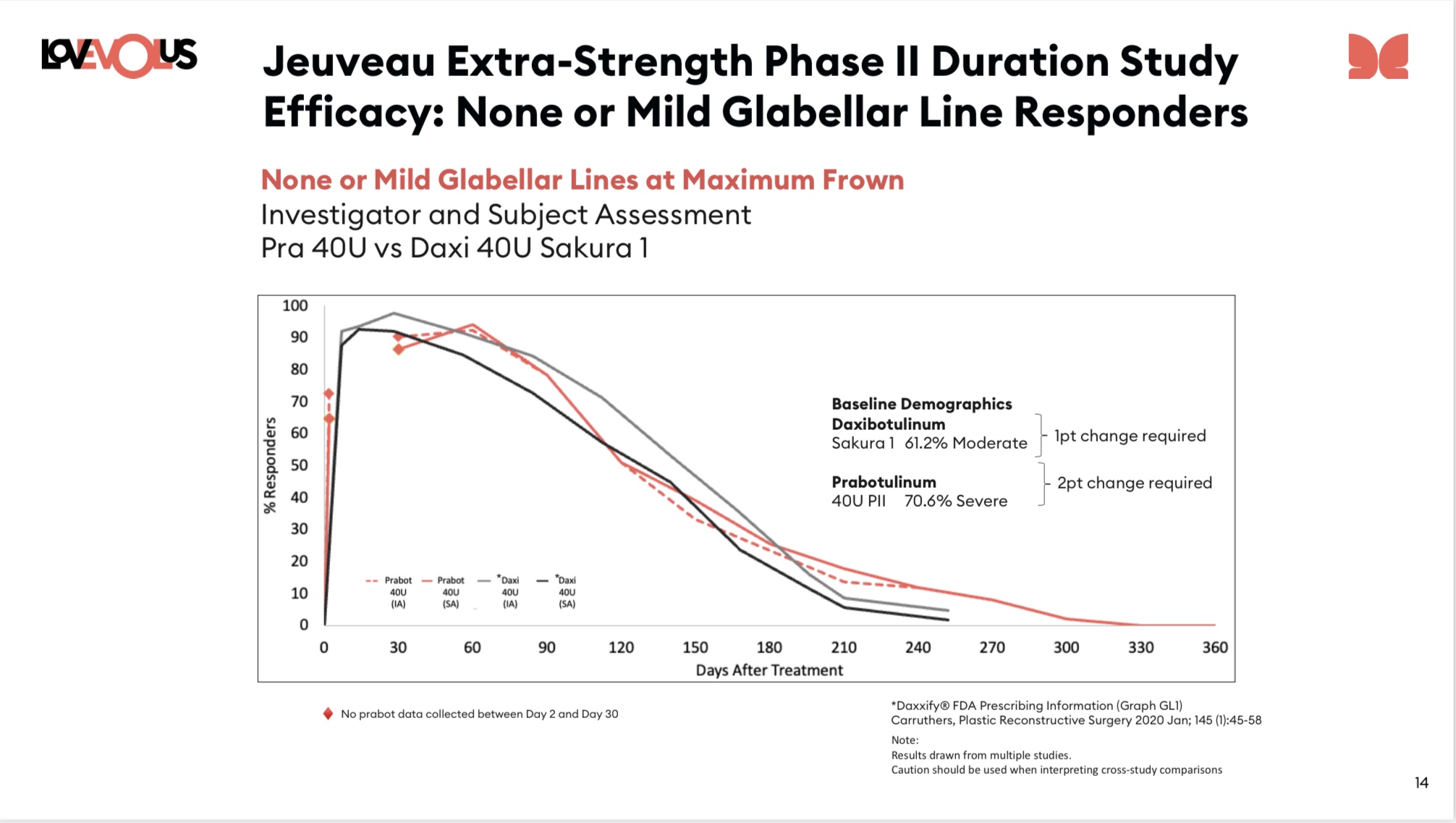

RVNC - suggest any story about the recent collapse of RVNC probably needs to have the below, mostly apples-apples, comparison of aesthetics duration in the story. It used to be that RVNC had a technical moat on duration in aesthetics. Other BONTs tried to increase dose to get the same duration, but failed in one of several ways: too big a dose (a $ problem or feel problem or …) or AE increased too much. But Jeuveau may have overcome that, and cast (post hoc) the data into the same data/metric frames used by Revance in order to get Apples to Apples. Or at least close to it - full Apple to Apple is never possible wo head to head trial. Note the frame below, as EOLS described in their chart package, is of an endpoint the FDA prefers. And the Daxi curves come from the FDA review package.

My further comments:

A) obviously RVNC still has by far the best data and label on Cervical Dystonia. Both are important somewhat separately important (eg there is no reason, in principle, that the shorter duration BONTs couldn’t redose, as the Daxi label allows, as the efficacy wears off). But not at all clear RVNC has the management wherewithal to extend this into other, off label, indications. At least not remotely quickly. See next point.

B) I still tend to suspect that Daxi is the best drug (see CD data, which really is astoundingly better), but it turns out that lots of other parameters can change efficacy, duration, side effects. Eg EOLS clearly thought hard about what dilution to use in their Extra Strength trial (they used much less). It’s a moderately big parameter space - big enough you probably need to be good at sorting through messy real world experience to optimize. Something EOLS seems like they can do? But RVNC cannot? And even we’re they good at it… it’ll take substantial time.

Jeuveau Extra-Strength results - further comments:

One of the meaningful differences in the Extra Strength trial was less than half the normal number of men (about 14% in ph3, about 6% here). Given that they were testing fixed doses... this would mean longer duration. Not likely to be huge effect given a difference of only 8%, but not minor either. (Comment: I'd wager this was intentional since it is out of family for the ph3's in Glabellar, which are normally at least 10% and typically 12 to 20%.)

Comment: assuming an undiscounted price per 100 unit vial of ~$600, Daxi is significantly cheaper for the same duration.

Jeuveau Extra-Strength - now they've moved to identical analysis

Previously it's been noted that Jeuveau (and others) have been misleadingly looking at a return to baseline from only patients who were, first, responders - although they, and others, are generally somewhat opaque about this and it has to be surmised by the fact that the KM curve starts at 100.

HOWEVER these latest sets of charts from EOLS compare using the Sakura endpt definitions - with a graph ⬇️ that looks like apples to apples and shows rough equivalence for duration. Additionally, note that on the chart they correctly note that Daxi used substantially more "Moderate" patients. Obviously that means the graphs are not entirely comparable, which is fair... However they're also implicitly asserting that this makes Daxi look longer than it really is... and this implication seems suspect. My guess (very tentative) is that getting a moderate baseline patient up to None or Mild is probably faster than a severe baseline patient, but also faster to degrade - both of which are seen in the chart.

Caveat: it's always possible I missed something important, but if so... that's par for the course when trying to catch gaming of stats.

Fastest weight loss is not always the best.

However, my problem with EOLS is that they're promoting intentionally deceitful clinical data to make it appear that double-dose Jeuveau is comparable to Daxxify

what am I missing guys? Please walk me through the graphs they presented at ASDS

Results demonstrated 26 weeks, or 6 months duration across the multiple metrics presented, including the time it took for patients to return to their baseline GLS score after their treatment, the duration of effect for a patient with at least a one-point GLS improvement, and the time it took a patient to return to their baseline using the Global Aesthetic Improvement Scale.

Some KOL's (Dr Jean Carruthers, Dr. Sue Ellen Cox among others) have been promoting/studying the idea that using less diluent with the same amount of Toxin increases duration.

That makes me laugh. You want people who have no data from which to base their guesses, uh estimates of sales and then you will judge them based on what they guess. Come on, be serious.

Disappointed that not a single person on this board has made a prediction on Daxi revs for Q3. If you don't have any idea of Daxi sales for Q3, then how do you know what kind of sales would be a beat in your mind and give you conviction to buy more or what sales would be a miss and cause you to not buy more or even sell?

Revenue Recognition for contracts signed in Sept?

Anyone given any thought to how much of the increased interest in Daxxi after the Sept 1st pricing change… actually turns into recognized revenue for Q3? I’d assume it’s a fairly small fraction that shows up in Q3 formal numbers - just because it takes time to manufacture and ship.

US cosmetic: $388M (-8% QoQ*, +5% YoY)

Lastly, why would aesthetic physicians go on social media to post that the product “doesn’t” work as per the study results? So many physicians that we dealt with in my days had ulterior motives.

Are you saying the effect is weak because it lasts a week shorter. :)

More comments from Instagram sweep:

A) zero mentions of providers being concerned with impacts to them from less frequent visits - although 1 provider noted patients are showing up with much less movement and she ascribes it to them having regularly scheduled visits based upon old wearoff rates.

B) why would multiple providers note movement returns at roughly same time as w older BONTs but return to baseline is extended? My guess at some big factors is: 1) non optimum injection pattern for a drug that diffuses less than traditional BONT, so areas outside of pattern wear off too soon, but full fade doesn’t happen until much later, 2) some amount of lesser fidelity for shorter periods. 15% of 8 weeks is a week, of 18 weeks is 2.5 weeks.

Instagram Reviewer data sweep, and comments on:

I must admit, I don't understand the differing results among reputable board certified dermatologists.

Outside of getting a CRL upon PDUFA - I haven't seen this aggressive sell off in a while.

we are lowering our market share assumptions for the drug in the aesthetic setting to 10% from 15% (in 2030),

You're acting like models shouldn't be used because they could end up being wrong because one didn't accurately predict a large potential disruptive change to a given industry over a short-time frame.

When you've got people out there saying Daxi doesn't perform as well as advertised then it's an uphill battle to refute those claims. The biggest selling point was the longer duration & now CosmeticMD is saying sales personnel have been instructed to downplay the longer term efficacy.

Per conversations, Revance is now providing quantity discount contracts to large buyers.

Q: assuming Daxxy does make big headway in large volume accounts it will, by definition, be disrupting the package deals for fillers and BoNT. What happens to the now uncoupled filler orders? What opportunity even without Revance providing similar package deals?

RVNCs failure to dumb this down so injectors, investors, patients etc. could understand and accept these delayed rollout facts may be their biggest failure.