News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Chance To See

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

This quote from Lord Steinberg has always been intriguing, and I’ve never really known what he meant. It's not evidence, but if Bally’s knows what he meant – and agrees – maybe they could be buying the company.

From the September 3, 2008 PR announcing his election as Chairman of the Board:

"This is a pivotal day for Electronic Game Card," commented Lord Steinberg. "This Company's core technology is quite novel and very much the precise next generation product for which the gaming industry has been searching.”

http://www.electronicgamecard.com/Investors/PressCenter/2008Releases/PressRelease080903.aspx

Thanks for the heads-up. Link.

Here's the CNBC Nolan video link.

http://www.cnbc.com/id/15840232?video=1431392905&play=1

Q409 Net Billings, Revenue, EBITDAS, Earnings

FWIW, here are screen prints of my template for Q4 for Net Billings, Revenue, EBITDAS, Earnings, Cash, and a table for estimating Deferred Revenue. The yellow cells are the inputs; the rest are calculations. I included SED TDM bundling revenues for 40,000 automotive seats. Even without that, this template shows positive earnings for Q4. We’ll see.

NET BILLINGS

REVENUE, EBITDAS, EARNINGS

DEFERRED REVENUE TABLE

CASH

gophilipgo, you are correct that it was quite unseemly for HDVY to refer to the Biomed report in positive terms (“an independent, positive report”) when it is as much a piece of crap as the Adam Feuerstein hatchet job.

I agree that it is disappointing that HDVY responded as they did, which sounded hysterical and defensive to me. But I disagree with the idea that they should not have responded at all. They are a small company and thestreet.com has a wide audience. If HDVY had not let their anger get the better of them, this would have been an excellent opportunity to clearly present their work and information about diagnostic tests (including the PSA mess) while calmly refuting the inaccuracies in Feuerstein’s article.

With skillful writing and care they might have gotten thesteet.com (and others) to see the enormous potential for a company with proven pattern-recognition technology which has already discovered a number of potentially life-saving biomarkers.

Manufacturers. This is from Kevin’s opening remarks in the Q2 2009 transcript.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=40450448

Number Three, in beefing up our infrastructure and moving forward: enhanced manufacturing. This is a critical point as we discuss our infrastructure. As we attract new enterprise-level relationships, capacity and price have become even more critical. Over the past three months we have established relationships with three additional outsourced manufacturing partners, which have permitted us to materially lower our product cost and potentially triple our capacity to provide greater flexibility to accommodate both large-scale runs and short-term turn-around projects. One group is who we have worked closely with in the past. Another group was introduced to EGC by our partner, Sovereign Game Card. And the third group is vertically integrated with our own marketing services and channels and distribution. These relationships have given our firm the opportunity to expand our addressable market even further given the substantially lower cost of production.

On average, we can now produce a base-model EGC game card at 25% to 35% less expensive than in the past on relatively low production runs. With larger orders and potentially with less security features we will likely see even further reductions in cost. This development is highly material for the lottery market as well as certain mass consumer promotional opportunities.

With these meaningful structural moves in place, let me recap. New CFO, new headquarter office in Southern California with slight increase in staffing, new website, new brand, new partnerships, new lower pricing on EGC game cards, and expanded manufacturing capacity. We are fully prepared to handle our expected growth.

I’ve been told consistently by E*trade reps that on the OTC market what you see are not necessarily firm bids and offers - they can be merely an indication of approximately what the bid or offer may be. In other words, the MMs are not obligated to fill orders at the prices they put up as they are on the exchanges.

I've never looked into this to find out if this is correct.

“Events and decisions”

Like everyone else on the board, I’m putting 2 and 2 together and trying to get 4.

We have the following:

1. Scheduling a conference call.

2. Then cancelling it.

3. Plus Kevin’s comments elicited by pegasus1 in post #10010: “It was very unfortunate for the shareholders and EGC management both that we had to postpone our previously scheduled conference call set for today. We were hopeful that certain events and decisions would have been completed before today.”

I woke up on Sunday with my mind telling me that there really must be something important going on – whether positive or negative, whether a buyout or something else – because otherwise these actions make no sense.

Why would they have scheduled a conference call in the first place when all we really needed was a PR addressing a few issues? Then cancelling it while investors are beside themselves with frustration, and then this comment about waiting on some events and decisions.

Initially I thought Kevin’s comment was referring to the CFO and Board members, but it doesn’t make sense to cancel such an eagerly-awaited call for those things. I suppose it could be a decision relating to Poken, but why put investors through the mill over that? They would only need to say, “We’re working on the best arrangements” and go on to other subjects. Similar for ChinaLot.

So it seems (to me) that there is nothing that we know anything about that would explain the actions we’ve seen.

kardon, thanks for your contribution, but

do you really think it’s likely that EGMI would choose to give up 60% of every Poken sold in the U.S? I’m guessing, but I would think that the most logical explanation is that Poken was displeased with the progress so far. I always wondered why they would put their fate in North America in the hands of a tiny company with no experience selling direct to the consumer. I’ve assumed that Kevin charmed them.

I hope and assume that the companies will continue to work together, just without the exclusivity.

This was Kevin in the Q3 cc:

"This interesting opportunity for our company which we anticipate over time will have activity in all three of our business verticals.”

“The Poken opportunity is also another enormous opportunity. It’s a proprietary, an incredible technology of social engagement. As we all know, the social online media space is enormous and massive with a value per user as well as having a retail product to generate revenue from, so it’s a unique business model. So we’ll be divulging all that information to the market in upcoming announcements.”

“We continue on the sports front. The major sports properties with the relationship we have with BD&A. BD&A is a master licensee of the majority of sports properties and we’re looking at a couple that continue with the promotional cards for Electronic Game Card and also now with the new Poken product because the Poken product leads the consumer in that sports fan initiative online. And you can only imagine the possibilities that stem from having that product leading the consumer online, online engagement, online interaction, and the measurability of that product. And so the discussions have been helping the other products grow in further opportunities within the sports properties. And so there’ll be some forthcoming information, you know, released in greater detail.”

+++++++++++++

Incidentally, the initial announced agreement with China LotSynergy was also an MOU.

June 17, 2009 8K

http://www.sec.gov/Archives/edgar/data/1083036/000114420409032997/v152634_8k.htm

"Electronic Game Card, Inc. (OTCBB: EGMI) (“EGC”), announced today that it has completed a confidential Memorandum of Understanding (“MOU”) with China LotSynergy (“CLS”) to partner together to deliver EGMI lottery products to the Chinese market"

Mike, could you cut and paste the section you're referring to?

Thanks very much.

Spoke to IR this afternoon.

Yvonne was out, but Joe Zappulla spoke with me. I didn’t ask many detailed questions, as covering EGMI isn’t his job, but some interesting points:

BOARD MEETING. This has not happened yet, which would explain the company’s silence on the CFO and new Board members. Lee was traveling when they expected to meet earlier, and they should be meeting shortly. (Wmthecommoner, post #9524, says it should happen Thursday.) This was one of the most important points, as I had thought the Board meeting had taken place a couple of weeks ago, and I think most of us expected some news after that. They have several good CFO candidates and several potential Board members who are interested in joining the company.

NOLS. It sounds like there’s a good chance that the NOLs will reappear. Apparently the problem had to do with tax preparation overseas (where, as we know, most of the revenue has been) and once the proper filings are made the NOLs should reappear. They are fairly confident about this. I believe another poster mentioned that Yvonne has said that they took the worst case scenario in the 10Q, which Mr. Zappulla repeated today.

STOCK PRICE/RUMORS. He said that there have been some negative rumors floating around concerning revenues and that the company has said those rumors are not true.

CHINA. They had good meetings, Lee one week, Eugene C. the next. There are still some manufacturing license regulatory things that are being worked on, which should be relatively easy since the cards are made in China. They may not have yet finalized the three provinces for initial testing. I don’t have it in my notes, but I think he said Eugene was very positive on his return and strong in his belief in the potential here.

SPORTS. I mentioned sports and Mr. Zappulla said that Kevin has great sports contacts. He mentioned something I didn’t quite catch about NFL executives “coming over” plus MLB and NBA contacts

AccipiterQ, re your question.

From my post: “I asked if Quest will use the same data that Abbott develops. He said that to some extent the findings from Abbott will be of benefit to both parties (Abbott and Quest) but they are going down independent tracks.”

I don’t think there would be a definitive answer to your question without asking Mr. Tobin.

BUT HERE IS A GUESS WITH THE CAVEAT THAT I HAVE NO EXPERIENCE IN THIS: Phase 1 was to develop the assay. Phase 2 consists of the initial tests of the assay on real people and real specimens (not spiked). We know from the February filing (see Tryn2makamil’s post #2571) that the Phase 1 and 2 work was set up by HDVY before the Abbott and Quest agreements and that Abbott agreed to pay $100,000 for that work, but may not pay for all of it. Perhaps if/when Phase 2 is successful, Quest will pay for the part of the Phase 1 and 2 work that Abbott does not pay for.

February filing: “Abbott and HDC agree to have the experimental testing of Phase 1 and 2 performed at *, with *, as the principal investigator. HDC already has a experimental testing agreement in place with * that will cover the performance of Phase 1 and 2. HDC warrants that it has the right under the agreement with * to transfer the data resulting from Phase 1 and 2 testing to Abbott and that Abbott has the royalty-free right to use the data in any regulatory submission. Abbott shall be responsible for payment to HDC of *’s actual costs for performance of the Phase 1 and 2 experimental testing, up to a maximum of One-Hundred-Thousand Dollars ($100,000.00). HDC shall be responsible for payment to * of all costs in excess of the One-Hundred-Thousand Dollars ($100,000.00). Abbott shall make the payments to HDC within thirty (30) days of receipt of invoice from HDC, and HDC shall make the payment to * for any excess costs within thirty (30) days of receipt of notice from Abbott."

So after the assay is developed (Phase 1 - done) and tested and proven on real specimens (Phase 2), then perhaps each company carries on independently from there? It sounds like Abbott is definitely doing Phases 3 and 4 on its own.

I had a nice talk with Scott Tobin today about the prostate urine test. He was very generous with his time.

ABBOTT

I specifically asked if I was correct in my assessment that Abbott had not yet accepted the results of Phases 1 and 2 (carried out by a third party). He said that Phase 1 results have been accepted, but Abbott is still working on assimilating the results of Phase 2 and they are currently awaiting some further testing.

As we know, when both Phases 1 and 2 are accepted by Abbott the next $250,000 from Abbott will be received. And then Abbott would commence Phases 3 and 4. (See my posts #2582 and #2631.)

I asked if there was a “roadblock” but he said that although it has certainly taken longer than they expected or hoped for initially, it is still looking “very optimistic” and the evaluation process continues to advance.

QUEST

I asked if Quest will use the same data that Abbott develops. He said that to some extent the findings from Abbott will be of benefit to both parties (Abbott and Quest) but they are going down independent tracks. I meant to clearly establish if Quest could develop results earlier than Abbott (aside from not needing FDA approval for a lab-developed test) but I lost my train of thought on that.

CLINICAL LABORATORY IMPROVEMENT AMENDMENTS

While we were discussing Quest, Mr. Tobin said that about a year and a half ago there was a modification in how CLIA regulations are interpreted. I gather these are regulations (administered at the state level?) that apply to the development of lab-developed tests. Because of that change in interpretation, labs are required to take a role earlier in the development process of tests such as ours.

“Take a role earlier” essentially means “contribute money to the process earlier” so that the lab can establish rights to the test. Because they need to pay for certain things to establish rights, a company such as Quest will want to pay a company such as HDVY earlier in the development process than in the past. Although Mr. Tobin was NOT saying that money will be coming soon from Quest, he was saying that it can be expected sooner in the development process than in the past (and should be received prior to final development of the test). He said we should “stay tuned” re receipt of money from Quest.

OTHER LABS

He also mentioned that HDVY is continuing to identify other labs that are interested in the tests and that some of these labs are “looking at the process.”

IN SUMMARY

I have to evaluate things in light of the fact that I am investing retirement money, and for me there is both positive and negative. The negative is that this is going to take a while. Of course, I already knew that because I knew we have not yet received the $250,000 from Abbott for Phases 1 and 2. The positives are that HDVY should see some money from Quest earlier than expected in the process and that testing by Abbott is continuing to advance.

A Good Laugh

AB, you have a point. But for me, as long as they confirmed the investment and the Board seat, I’m okay with the lack of financial detail in this PR since its purpose is to trumpet the fact that they are launching their campaign at the Sundance festival, which I think is a pretty interesting choice.

My objection to the PR is that it is so outrageously sloppy: full of jargon (which you allude to), incorrect punctuation, incorrect capitalization, incorrect names, and incoherent sentences.

One good thing about it, though, is that I laugh out loud every time I read “Main Street Carpet Lounge.” Carpet Lounge?? Even as I type this, it’s making me laugh. They got the name right later in the PR: it’s the Main Event Red Carpet Lounge. It happens to be on Main Street, which I guess confused the person who wrote the PR.

Source of PR quote from Galina Sobolev

This blog seems to be the source for the Galina Sobolev quote in the PR.

http://galinasobolev.blogspot.com/

Hello to all my dear readers,

I hope you are having an amazing week so far! I've been up to my ears in the Single design studio, spending day and night sketching new designs, working with patterns and textiles, and just letting my inspiration flow. Fall is going to be a fantastic collection!

In addition to the runway looks that the hottest, most in-demand models strut down the various catwalks of the world's fashion capitals, there are other fashion trends besides simple the clothes that have caught my eye recently. One of these trends is the fusion of technology and fashion, which I absolutely love!

A hot new technology called Poken is leading the pack when it comes to this trend... they make staying connected oh-so-chic! I pride myself in staying ahead of the game when it comes to what's next in the fashion industry, and must admit, Poken is DEFINITELY going to be the next big thing. Think of it as a stylish way to sync all of the ways that you communicate. It's an adorable keychain-like device that when touched against someone else's Poken device, instantly exchanges tons of information, from email to phone numbers to your Twitter and Facebook info and picture. Soo cool!

My friends at ShopPoken.com came to me for advice on ways that impeccably dressed women can incorporate their device into their look, and I suggested that it can be worn as a fashionable-meets-funky necklace! I love lending my advice to other creative types, and now have found that I can barely put my Poken down. They loved my idea so much they created a Special Edition necklace for the Sundance Film Festival 2010 to be given to celebrities at the Fred Segal Fun event and also at Bravo TV's Main Event Red Carpet Lounge. It will even be available for sale to the public as a limited edition available on www.shoppoken.com! This is definitely the fashion accessory of the future.

My approach in life has been to be a leader and a trendsetter. I love that Poken has this cutting edge technnology that doubles as a trendy fashion accessory. It is the modern approach to functional fashion. I have profiles on Facebook, YouTube, Twitter, A Small World and many more and have always believed in the power of networking and social media. This is going to be a huge breakthrough. As they say on Bravo, watch what happens!

Xo,

Galina

Check out some pictures of me with my Poken necklace below. So much fun.

DIH, Thanks very much! eom

Abbott, Quest, Timelines, Licenses

So there were no direct responses to my post #2582 on December 15th regarding Abbott.

Yes I’m new to the stock, and sometimes newbies go over the same ground that has been covered a million times, but in my post I gave evidence which indicates that so far Abbott has not accepted the results of Phases 1 and 2, which were apparently completed by August by the third party doing that work.

If this is correct, it is interesting for three reasons.

1. We know what to look for next. HDVY should be receiving the $250,000 milestone payment due when those results are accepted. That should come far before the 510(k) draft.

2. There is a legitimate question about what is taking so long for Abbott to accept these results. Maybe 4+ months is really not so long for something like this, and maybe this question could be easily answered by the company. Last Friday I phoned the number for Scott Tobin in the latest PR. Dr. Madyastha answered the phone and he directed me to Mr. Tobin and was kind enough to give me the correct number, but Mr.Tobin was not there. I didn’t leave a voicemail and haven’t yet tried again.

3. Will Quest be able to develop its test more quickly?

+++++++++++++++

There were no direct responses to my post, but I think a couple of subsequent posts were indirect responses.

MONEY DUE FROM ABBOTT

AccipiterQ wrote (#2588), “…at this juncture how much more are we potentially owed by Abbott? 200K? That's a blip basically; big money's in Quest's results.”

This is what is due from Abbott in development milestone payments alone:

$ 250,000 upon acceptance of Phases 1 and 2 results

$ 250,000 upon successful completion of Phases 3 and 4

$ 500,000 upon filing of 510(k) or PMA

$ 500,000 upon approval of either of these

Then royalty and sales milestone payments.

+++++++++++++++

ABBOTT VS. QUEST

Degreed wrote (#2583), “Just to bring everyone back on focus we are waiting for Quest not Abbott Labs….”

I assume that Abbott does not have testing laboratories such as Quest and Lab Corp, but as I understand it, this is what is licensed:

QUEST has the right to develop and use a “Laboratory Developed Test” for urine for its own use.

ABBOTT has the right to develop and use a “Laboratory Developed Test” for urine and also for biopsied tissue, and it will develop “test kits” for these tests for sale to all the other labs in the world.

Can someone let me know why Quest is considered so much more important than Abbott? Do the tests Abbott can sell require FDA approval before they can sell them in the U.S.? Is my understanding of the licenses incorrect?

(INITIAL FEES. One interesting note which may have been discussed already (but I could not find it posted on the board) – and which may mean nothing or may mean something – is that it appears that Abbott paid $100,000 up front while Quest paid only $50,000. 10Q, Note B, Revenue Recognition: “The Company received $150,000 in cash in February 2009 in connection with two licensing agreements completed in the first quarter of 2009. Deferred revenue of $150,000 was recorded and will be recognized as income over the 15 year remaining term of the underlying patents.”)

Do you remember the area code?

If it was 845 it was probably her.

Also, cell phones in NYC area can have different area codes.

Here’s what I’ve pieced together.

I’m no expert, but this is what it looks like to me at this point based on the February filing in Tryn’s post #2571 and the recent 10Q’s. Any comments/corrections are welcome.

1. HDC received the initial $100,000 in February.

10Q: “In February 2009, Abbott paid to us a one-time initial signing fee of $100,000.”

2. Phase 1 and 2 testing was done by a third party.

February filing: “Abbott and HDC agree to have the experimental testing of Phase 1 and 2 performed at *, with *, as the principal investigator. HDC already has a experimental testing agreement in place with * that will cover the performance of Phase 1 and 2. HDC warrants that it has the right under the agreement with * to transfer the data resulting from Phase 1 and 2 testing to Abbott and that Abbott has the royalty-free right to use the data in any regulatory submission. Abbott shall be responsible for payment to HDC of *’s actual costs for performance of the Phase 1 and 2 experimental testing, up to a maximum of One-Hundred-Thousand Dollars ($100,000.00). HDC shall be responsible for payment to * of all costs in excess of the One-Hundred-Thousand Dollars ($100,000.00). Abbott shall make the payments to HDC within thirty (30) days of receipt of invoice from HDC, and HDC shall make the payment to * for any excess costs within thirty (30) days of receipt of notice from Abbott."

3. HDC received $100,000 in August. This appears to be what was due from Abbott for HDC to pay the company identified as * in the February agreement, the company doing the Phase I and 2 testing. This probably means that the Phase 1 and 2 testing was completed in mid-summer.

10Q: “On August 7, 2009, Abbott reimbursed us $100,000 in development costs as required by the license agreement.”

This is reasonably within the timeline of 1-1/2 months for Phase 1 and 2 months for Phase 2.

WE APPEAR TO BE HERE

4. So it appears that since August Abbott has been evaluating the Phase 1 and 2 results. (Tryn, maybe your timeline needed to include extra time for evaluation.)

February filing: “The successful completion of Phase I will be the demonstration of “Feasibility” for the assay, and will be determined by Abbott in its sole discretion.” “The successful completion of Phase 2 will be determined by Abbott in its sole discretion…”

5. When Abbott is satisfied they will pay $250,000 to HDC.

10Q: “In addition, with respect to the products subject to the license (the “Products”), Abbott will pay milestone payments to us upon achievement of the following events: $250,000 upon completion of Phases 1 and 2 as described in the FDA Submission Plan;

6. Then Abbott and another third party will design and carry out Phase 3 and 4.

February filing: “Phase 3 and 4 studies (below) will be initiated only upon the review and acceptance of Phase 1 & 2 as meeting the Result Completion Standards. “

February filing: “Abbott at its sole discretion shall select the institution to perform the Phase 3 and 4 testing. Abbott shall be responsible for negotiating and signing the test performance agreement with the institution selected. Abbott shall be responsible for the costs of the selected institution for the performance of Phase 3 and 4.”

7. When Abbott is satisfied about Phases 3 and 4, they will pay another $250,000 to HDC.

10Q: “In addition, with respect to the products subject to the license (the “Products”), Abbott will pay milestone payments to us upon achievement of the following events: ….; $250,000 upon completion of Phases 3 and 4 as described in the FDA Submission Plan;”

8. Then the 510(k) procedures will commence

Re 510(k) Timeline

According to the latest 10Q (for Q3, submitted in mid-November):

“In February 2009, Abbott paid to us a one-time initial signing fee of $100,000. On August 7, 2009, Abbott reimbursed us $100,000 in development costs as required by the license agreement. In addition, with respect to the products subject to the license (the “Products”), Abbott will pay milestone payments to us upon achievement of the following events: $250,000 upon completion of Phases 1 and 2 as described in the FDA Submission Plan; $250,000 upon completion of Phases 3 and 4 as described in the FDA Submission Plan; $500,000 upon submission of either a 510(k) or Pre Market Approval (“PMA”) submission to the FDA; and $500,000 upon the receipt of a written notification by the FDA of the approval of the applicable 510(k) or PMA submission.”

I don't see any indication that we’ve received the $250,000 for the completion of Phases 1 and 2 (let alone Phases 3 and 4) so I wonder why we are expecting the 510(k) anytime soon. Am I missing something?

Does this imply that Bally will be helping to sell our cards?

Why else would Kevin mention their sales team.

"This strategic licensing agreement between EGC and Bally expands our game library well beyond the immediate goal we set earlier this year. Not only does Bally have an extensive game library of some of the most valued games in the world, but it also has one of the largest dedicated R&D and Sales teams in the industry, worldwide, that continue to develop and market the next exciting games for players to enjoy," added Kevin Donovan, Interim Joint Chairman and Chief Executive Officer of EGC.

Without their sales help, it would still be excellent, but I would be less enthusiastic about something else for which we have to do all the selling.

"Simon reportedly mulls General Growth bid"

Nov. 18, 2009, 10:39 a.m. EST

By John Spence

BOSTON (MarketWatch) -- Simon Property Group Inc. (SPG 74.44, +2.26, +3.13%) has hired investment adviser Lazard Ltd. and law firm Wachtell, Lipton, Rosen & Katz to explore a potential bid for all or part of General Growth Properties Inc. /quotes/comstock/11i!ggwpq (GGWPQ 5.50, +1.23, +28.81%) , which filed for bankruptcy in April, The Wall Street Journal reported Wednesday. Real estate investment trust Simon's interest in General Growth could lead to a takeover struggle as General Growth prepares a plan to restructure and exit from bankruptcy, the newspaper reported. Mall operator General Growth sought bankruptcy protection after it was unable to refinance a crushing debt load in the credit crisis. Pink-sheet-listed shares of General Growth surged 40% in morning trade Wednesday, while Simon shares were up nearly 2%.

http://www.marketwatch.com/story/simon-reportedly-mulls-general-growth-bid-2009-11-18-1039570?siteid=yhoof2

EGMI Q3 2009 CC Transcript

Still nothing on Seekingalpha.

EGMI Q3 2009 CC

Kevin Donovan, CEO, Co-Chairman

Lee Cole, Board member, previous Interim CEO

Yvonne Zappulla, IR Representative

YVONNE ZAPPULLA

[Introductory remarks]

On December 10th at 11:00 am east coast time, Electronic Game Card will be holding its annual shareholder meeting in our offices at Grannus Financial, 1120 Avenue of the Americas in Manhattan. All are welcome. Please e-mail either myself or John _____ to let us know if you will be attending. Kevin.

KEVIN DONOVAN

Great. Well, thank you very much Yvonne, and thank you all for joining us this morning.

During this past year, the late honorable Lord Leonard Steinberg assembled a small but hardworking, effective team at Electronic Game Card, all with skills beyond what is normally expected of a company of this size. We work very well together and share a common goal of building this company into a significant entity. Under Lord Steinberg’s stewardship we transitioned from a one-product company, turnaround story, to a company with multiple product lines selling into multiple distributors globally. We grieve and are deeply saddened by Lord Steinberg’s untimely and sudden passing last week. We lost a dear friend, family member, mentor, chairman, and leader of the Jewish community and cricket club in Manchester, England. Today we are even more resolute in continuing Lord Steinberg’s legacy and building this company into one in which he would be so very proud.

During third quarter 2009, Electronic Game Card generated record revenues of $4.2 million, slightly ahead of analysts’ expectations and a meaningful step up from prior quarters’ revenue. Revenue growth during the quarter was predominantly driven by repeat business as well as further penetration of the Electronic Game Card into the promotions market, additional licensing, and trial orders of new product lines. The company’s current contracted backlog is expected to generate our business for the remainder of the year, further validating our confidence in revenue guidance of $16 million for 2009.

Electronic Game Card’s operating income grew 42% year-over-year and grew by 38% over the prior second quarter. We generated $2.9 million or $.04 per diluted share in comprehensive net income applicable to common stockholders, marking our 11th consecutive profitable quarter. As of September 30, 2009, Electronic Game Card had approximately 68.1 million shares of common stock outstanding with a weighted fully-diluted share count totaling 72.2 million.

The gross profit generated for the three months ended September 30, 2009 was at the record level of $3.3 million, generating a 78% gross margin. Growing and maximizing gross profit dollars is our top focus. Please note that as future events unfold throughout the year and 2010, some of our current contracted opportunities may greatly accelerate our revenues at margin percentage levels that, while still strong, could be less than the 70+ margins we have enjoyed on less robust revenues and volumes. Conversely, there are a number of potential license royalty relationships with well-established household brand names that naturally generate little cost against revenues. As these new business relationships become public we will update you with proper guidance.

Operating expenses during the third quarter 2009 totaled $798,000, or approximately 19% of revenue, and represents an increase of approximately $274,000 over the third quarter 2008 and an increase of $159,000 over the previous 2009 quarter. This increase was attrivut3d predominantly to higher costs resulting from the strengthened management team and a heightened marketing effort. Going forward we anticipate three strategic personnel additions to our sales and project management teams as we increase our activity in North America, the Pacific Rim, and continental Europe.

For the nine months ended September 30, 2009, Electronic Game Card revenues increased 31% to $10.2 million over the prior year nine-month period. Net income totaled $6.6 million or $.10 per diluted share compared to a net income of $4.3 million or $.07 per diluted share during the prior year’s first nine-month period.

Cash and equivalents on September 30, 2009 totaled $12.7 million, an increase of approximately $4.5 million from year-end December 31, 2008, and an increase of over $1.4 million from the period ended June 30, 2009. Consistent with the prior second quarter, the company’s current ratio remained flat at 17:1 and EGC’s 6% convertible redeemable preferred debt instrument, which converts at $1.01, was reduced to $2.8 million from the prior second quarter 2009 of $3.3.

Importantly, Stockholders Equity continued to rise, to $23.2 million, an increase of $4.7 million from the prior second quarter.

Thus far, the balance of the year is shaping up to deliver an acceleration in revenues and earnings to put us on target of hitting our guidance of $16 million in revenues and $.14 earnings per share.

And looking forward into 2010 we have a number of initiatives already announced, and others soon to be announced, that will create significant momentum to add to our 2009 base. Before reviewing our business lines and future initiatives, it is important to discuss our base of operations and infrastructure that will enable us to smoothly ramp up our revenue levels.

First, replacements to the Board and executive ranks. As a result of the death of our Executive Chairman, The Lord Leonard Steinberg, the Board of Electronic Game Card has elected to replace our loss in the interim with Eugene Christiansen and myself as joint Chairmen of the company. Eugene was nominated by Lord Steinberg and elected to the Board of Electronic Game Card in September 2008. Mr. Christiansen has been active as an executive consultant to the commercial gambling and entertainment industries since 1976 through New York-based Christiansen Capital Advisors. Mr. Christiansen has conducted studies of the economics, taxation, financial structure, and regulation of casino gaming, pari-mutual wagering, and lotteries, and has counseled Manhattan and Washington, D.C. law firms in legal proceedings regarding in legal proceedings regarding gaming issues and has also authored numerous articles dealing with all aspects of the gaming industry. I look forward to working even more closely with Eugene in the coming months.

We plan additional changes to the Board within the next 30 days with the goal to establish an independent Board. We are already in advanced discussions with several prospective candidates. Our plan is to replace three to four new members. Our criteria in our selection process is based upon adding exponential value through potential new business revenue from their relationship network and seasoned public market, legal and finance experience.

I would like to take a moment to discuss the announcement from last week of Tom Schiff’s stepping down as CFO. This move in his name function, given Tom’s personal situation and frankly the company’s oversight is not sending in the D&O insurance payment – until such time as all paperwork was properly filed and coverage resumed, Tom will be operating as a consultant, albeit closely attending to our books and financial details very similar to his prior responsibilities prior to this unfortunate oversight. We hope Tom will join our executive ranks once again in the near future.

Over the next six months our additional staffing plans are modest. We may add two or three admin and mid-level individuals as project, sales, marketing, and operations managers specific to new growth areas and management of evergreen accounts.

We are also pleased to announce that we have hired a top design, branding, marketing, and media relations firm based here in New York City, Perillo & Co., which will be helping us to increase our company profile and launch our new CirQ brand, website, iPhone applications, and overall new business development marketing initiatives. Joe Perillo, co-founder of Perillo & Company’s experience is vast in public and private enterprises including his previous tenure as the first ever chief marketing officer for the City of New York appointed by Mayor Bloomberg. He is also Vice President of Marketing for the New York Yankees and held several key global brand accounts including the History Channel. I’ve been privileged to work with Perillo & Co. in the past, achieving fantastic results, and expect to do the same with the launch of our new brand, CirQ.

Secondarily, branding of our company. As you all know, my roots are based in branding and marketing from the Salt Lake 2002 Winter Olympic Games to the NASCAR Speed Parks. As we’ve discussed in the past, our name is too limiting to properly carry this company forward and our vision into the future. Therefore, over the next couple of months we will rebrand the company to CirQ, and with that launching our new brand and website before year-end at cirp.com. The new CirQ brand, inspiring technology, will provide the company with a broader scope of recognition for our expanded suite of technology platforms and easier adaptability to the new business applications, market opportunities, and B2B partnerships. Perillo & Co. have been working behind the scenes over the past couple of months. We are very excited to unveil a highly impressive, next gen look and image within the next 60 days.

With these final organizational milestones in place, here’s what I see as the opportunities in each of our three business segments.

First, promotions. Here historically lie the bulk of our revenues, and I’m happy to report that we continue to see impressive growth opportunities in this business segment. In progressing our relationships further with BD&A, the third largest promotions agency in the U.S., and their partnerships with high-profile entertainment brands and professional sports marketing and properties, with our integrated vertical marketing approach. Also, as we further develop our relationship with Havi Global Logistics and their family of companies worldwide.

Second is in gaming. This quarter we recognized revenues from our two license deals with Sovereign Game Card, our native American casinos-focused licensed distribution partner, and Scientific Games. Sovereign has been working diligently on several key initiatives in turnkey promotional orders within tribes in Southwest, Northwest, and Midwest regions of the U.S.

Another important recent development is our announced agreement to form a strategic partnership with China Lot Synergy, which is responsible for the welfare lottery in China. This is only one of two legal lotteries in the People’s Republic of China and, as we know, effective this past July 1, the massive illegal lotteries in China have been outlawed, thereby creating an excellent opportunity to capture business for the legal lotteries in China. The Chinese welfare lottery market currently sells approximately 9 billion scratch tickets annually. During my recent visit with Lee Cole to China Lot Synergy at their office in Beijing we met with their Chairman, CEO, COO, and several other senior level executives in marketing, operations, and logistics. They are a first-class, high-knowledgeable, and well-run organization. I plan to be in China again in the next three weeks with Lee Cole to kick off our relationship as we establish our joint company and launch strategy plans into the first three provinces in China. We plan to launch the trial of our Electronic Game Cards in three provinces during the first half of 2010, and hope to expand nationally during the second half of the year upon successful conclusion of those trials.

In addition, we have been working on sectors such as national and state lotteries outside the United States and casino gaming projects in Las Vegas, Australian, and Asian markets where Miss Anna Houssels, our Executive Vice President of Sales and Director, has long-established, successful relationships.

And finally, a quick update on EGC products into betting shop opportunities in Eastern Europe. As you might recall, the Lord Leonard Steinberg had introduced the company to the Stanley Leisure betting shops in Eastern Europe, namely Romania, Croatia, and Poland. We continue to advance in regulations, and there are several other tax reductions into those particular markets which are accelerating the opportunities for new growth in Europe.

Number three, our vertical market of education. This is a $2.2 billion global market and growing. To our knowledge, there are no interactive learning systems products that are as affordable, from $8 to $12 retail price points. We are confident we have a category buster as an on-the-go, edutainment-style game card product by early responses from our European B2B network reaction and here at home in the United States. Currently there are several gold standard brands in education, publishing, and media in review of this new product offering. We expect the first cards to be shipped in the UK in first quarter 2010.

And finally, an update on our most recent platform and agreement to form a joint venture with Poken Holding. This interesting opportunity for our company which we anticipate over time will have activity in all three of our business verticals. I spent several days at Poken headquarters in Switzerland. There is incredible synergy between our two companies and our two management teams have great chemistry together. We have before us what we suspect will be an immediate development, sales, and distribution opportunity in North America, which we hope to share with all of you in the near future. We also believe that there are opportunities to expand our relationship, which we are currently investigating. So please stay tuned. This relationship could fodder some exciting developments into the close of this current year.

Now in closing. The management, Board, and consultants of Electronic Game Card would like to express our heartfelt condolences to the Steinberg family and the Lord Leonard Steinberg, a great man who was generous with his time and gave this company a great foundation from which to grow. It is all our intention to build this company into the success that Leonard so envisioned.

With that, I will now open this call up for questions.

19:00

Q&A

TODD EILERS – ROTH CAPITAL PARTNERS

Q. Morning, everyone. Kevin, I was wondering if you could maybe break down your revenue a little bit under – you know maybe give how much was promotions, how much was gaming and lottery and how much was under the educational segment. And then also maybe if you could give the unit breakdown for those segments as well.

LC. You want me to do that, Kevin?

KD. Yes, Lee, please feel free. Thank you.

LC. Hi, Todd. Basically, I mean we’re reclassifying the segments with new products, but I mean, and we’re sort of throwing[?] more in the promotional segment, so I would say putting promotion and toys together, really it’s probably about 80% promotion and toys and 20% gaming and lottery. And really the growth in sales this quarter was mainly due to a pick-up in licenses that we’ve got and additional licenses.

Q. OK. And Lee can you also give, I know in the past you’ve given how much your total royalty and recurring revenue was in the quarter. Can you give that again?

LC. I haven’t got the exact figure. It’s approximately $2 million.

Q. OK. And then, did you guys ship any of the iQuiz cards or the Thomas ePlay cards in the international markets in the quarter?

LC. No, Thomas is going out Q1 and the iQuiz cards are going out in this quarter.

Q. And will that - will the iQuiz, will that be just international markets or will that also be domestic?

LC. What domestic U.S.? It will be domestic U.S. next year. It’s just - the ones that are going out this quarter are just UK.

20:30

Q. OK. And then can you maybe also give an update on I guess the distribution relationship with FMM. Are they - will they just be distributing the iQuiz Card and the Thomas ePlay cards or will they also be distributing other products for you guys? And I’m assuming, it sounds like we should expect a first quarter, second quarter next year rollout domestically.

KD. Lee, do you want me to take that?

LC. Yeah, thanks Kevin.

KD. Great. Todd, you know we have a great relationship with this 52 year-old company who’s very well-respected in retail marketing and placements. And we enjoy a great relationship with them. The core products will be distributed in the second half of 2010 in the U.S. based on the six major categories of retailers that they service on a daily basis. We’re looking to add to that. As you know we have a deal with SSD Company Limited out of Japan, and the smart stick pen scanner and the barcode scanning system, and so we’re looking at placement there. With Poken for North America we’ve been approached by several other new retailers in the past 30 days and we’re looking at including the Poken products also into those retail channels and distribution from a very strategic standpoint. And FMM is well-suited with us to handle that.

Q. OK. Perfect. And then I guess a follow up question on the China Lot opportunity. You kind of highlighted the expected trial there coming up. Can you maybe in general kind of give us a sense of what will determine a successful trial for you guys. Is there – can you maybe talk in general about that? And then also what do you see as the biggest risk to that opportunity for you guys?

KD. Well, if I may, and then Lee, please jump in. Todd, I think it’s why we’re going to China, based on our discussions – when you get in the room in the early part of December, we’re working through the criteria. And also making the decision on which of the three out of the first 13 provinces that we’re going to launch in, and the number of cards. So all those decisions are forthcoming. We have an annual shareholders meeting back here in New York by which we’ll be able to share additional information after our meetings in China.

LC. Yeah, and just on risks, I mean the China Lot Synergy relationship isn’t in any of our forecasts.

Q. OK. And then one last question. Lee, can you – I think I forgot to ask this. But can you give the total number of game cards sold in the quarter?

LC. Yeah, it was approximately 1.7 million. It wasn’t up that much because we had a lot more licensing revenue, which also explains the increase in margin.

Q. OK. All right. Thanks. Thanks, guys. Congrats on a great quarter.

KD. Thanks, Todd.

RICHARD FETYKO - MERRIMAN

Q. Good morning, guys. Congrats on the results. Lee, could you explain a little more about the sequential increase in the revenues. You mentioned more licensing. What type of licensing? From promotional type of clients and what type of clients are they? And then looking into fourth quarter, your 16 million revenue guidance implies a $1.5 million sequential increase in revenue in the fourth quarter, which is phenomenal, it’s great, just curious what will drive that. If you have a couple of things that you expect on a sequential basis to contribute to that increase.

24:20

LC. Sure. Yeah, the increase in licensing is one special bespoke license where we’re developing a new product. And the other is just another promotional distributor in a different territory. With regard to the increase in revenues, that is all from Quiz Cards and that’s all to do with – that all comes from Quiz Card shipments basically. You know we were expecting them to ship back end of Q3 but you know just due to technical matters you know they’re actually finally shipping this month.

Q. Gotcha. And on that Quiz Card shipment, is there a certain level of commitment that you have for the next few months?

LC. Yeah, if you look at Q1 of next year you’re not going to see much increase because it’s just, you know, Q1’s fairly steady with Q4 because – where you’ll see the increase next year is Q2 onwards when U.S. – when we expect U.S. revenues to start kicking in.

Q. From the same Quiz Cards and then on top of that I guess the Thomas, the Engine cards?

LC. Yeah. All the different initiatives that we’re working on there. That’s right, isn’t it, Kevin?

KD. That’s correct.

25:50

Q. OK, great. And Kevin, on the promotions side, you’ve been having a lot of conversations with BD&A. I don’t know to the extent you can give us a little more color on how that’s progressing, what type of cards or content ____ they’re interested in using the platform for?

KD. Sure thanks, Richard. So BD&A, based in Seattle, Washington. You can go on their website, bdainc.com, to find out more about the company. They have their entertainment division down in Irvine, CA. We’ve been working closely with them. Third-largest agent’s promotions agency in the country. They have a line-up of entertainment accounts which also includes Freemantle, and Freemantle has brands like American Idol, The Price is Right, Family Feud, and some of the top game shows on television. And so we’re working very closely with them and their licensor partners, both the promotions side of integrating the IP into our technology platforms, primarily the iQuiz Digital Squirt, and then also the iQuiz smaller version of the card without the sound. And into the promotions side with their clients that are sponsors of the shows. And then also from the retail side of bridging it back over with the FMM-The Moscoe Group into the other channels of distribution. We really have a great relationship with them. We’re working through orders and will be forthcoming announcements regarding greater details on that relationship.

Q. Great. And then lastly perhaps Lee has an update on the investments on your balance sheet and some of the private companies with regards to monetizing some of those. Any update there, Lee?

LC. Yeah, I mean as we’ve said previously we’re looking to monetize the whole investment sector by the middle of next year, and we’ve got – we’re in active negotiations on a very large portion of that at the moment. And then the other real sector of the investments is PrizeMobile, where their business is progressing nicely. They’re in a very interesting space which we think could be synergistic with us in some respects. And they’re hopeful to get their mobile platform – they’ve got some good news with a couple of large carriers in Europe, hopes going to emerge soon. So basically, bottom line is we feel very confident of getting out of all of our investments by the middle of next year and hopefully at a profit but definitely not at a loss.

Q. Gotcha. All right, thanks guys.

STEVE MAIDEN – MAIDEN CAPITAL

Q. Hi, guys. Great Quarter. Couple of questions for you. One was, trying to understand as you ran through the growth going forward what your operational expenses are going to look like going forward. Are you going to have to hire a bunch of headcounts. Trying to get an idea of your ability to drop profits to the bottom line.

KD. Sure. I’d like to start on that. Steve, it’s not a bunch of people. First of all we’ve identified two to three key areas for types of[?] consultants with performance criteria, specific projects. We will not have all the other employee benefits that are typically associated so we hold a lean operation and will continue to do so, watching the bottom line. And these are additive based on an increase in volume and revenue that we are projecting into 2010.

Q. Gotcha. I think – can you talk just generally a bit about the – both the China economics and the Poken economics to some degree. You talked you know about 9 billion scratch cards being sold annually in China. I saw a Roth report that said only 4 million sales – 4 million cards sold from Electronic Game Card would add about $.01 in earnings. I don’t know if you can bless that or if you can talk through the economics of that but that seems like just a massive opportunity. And then sort of a similar question on Poken. I don’t know if you’re willing or able to talk about that, but Poken’s getting a lot of buzz and I just want to understand what it could mean to the company.

KD. Well, I really – I don’t

LC. Do you want me to….

KD. I don’t want to disclose either one of those at this point, and it’s not for withholding information. It’s clearly – as we’re defining the economics and I’d rather reserve our comments to properly address the marketplace as it pertains to China Lot Synergy and the China welfare. We are reviewing it, we are getting to the final numbers, and especially as it comes out of the criteria for these three provinces. So I’d like to reserve judgment on that and communication further.

The Poken opportunity is also another enormous opportunity. It’s a proprietary, an incredible technology of social engagement. As we all know, the social online media space is enormous and massive with a value per user as well as having a retail product to generate revenue from, so it’s a unique business model. So we’ll be divulging all that information to the market in upcoming announcements.

LC. And again, it’s not in our forecast.

Q. Yeah, that was going to be my next question. Just kind of asked last quarter, comfort with the forecast that’s out there. It’s $.20, basically a doubling of revenue to something like $27 million, I think, in 2010. So $.14 earnings per share going to $.20. I think you said last year none of China is in there. Certainly I assume Poken’s not in there So any comments you can make on the comfort of hitting those numbers or exceeding them.

LC. I mean, they’re analyst estimates. And, you know, we – if with our current pipeline and if with the initiatives we’ve got out there on our current products kick in as we expect they will, then we don’t see anything too contradictory in those revenues, but we haven’t actually given an estimate. Put it this way, we certainly see our earnings bright.

KD. Yeah. Well said. And I think, Steven, you can look at it and say, what were the products that we were able to deliver on in 2009 vs. the products we’ll be able to put into the market and promotions and retail and other strategic opportunities for revenue in 2010 are vastly different. It’s rounding off the suite of technology with greater opportunities regardless of who that B2B or consumer client is.

LC. Yeah, what Kevin’s done and what the company’s done is expand the distribution base and have expanded the product base and continued to expand his product base so we’ve probably got – probably have three times the product base going into two times the distribution base next year.

Q. Yeah. It would be hard not to grow materially with that. And the China opportunity seems enormous. Well, that’s great. And I guess one more just housekeeping. I think I noticed your Paid-in Capital growing. I don’t know if there’s any color you can give on that.

LC. I think it’s mainly where the stock price has gone up and people have been converting options and warrants from old financings and converting Preferred shares.

Q. OK, OK. Continued success, guys. Thank you.

LC. Thanks, Steve.

KD. Thanks very much, Steve.

JOE MAXIM[?] – DOUGHERTY & COMPANY.

Q. Hi. Thank you. Kevin, just wondering if you have working models of your prototypes you know for the larger Quiz Cards and education cards yet?

LC. Yes.

KD. Hi, Joe. How are you?

Q. I’m doing well, thank you.

KD. Good. good. Thanks for joining the call today. We do. Lee, do you want to expand on that further?

LC. Yeah, we’ve got working prototypes for the first generation of the Quiz Cards and the Edu Cards. And the ones I think you’re referring to is the one of the specific brands where, which is part of our shipment strategy for next year, where we’re actually putting sound on the cards as well. Again, we’re – tthey’ll – we’ll have them before the year-end as well. So we’re already set quite nicely for next year, Q1, Q2 shipping now that we’ve finally got the prototypes done.

35.30

Q. You have working models but you need to add sound to them yet.

LC. Correct [?]

Q. What’s the feedback then from your potential customers. Has everyone seen these? And obviously I’m assuming they like them that’s why you’re excited about next year, but I just wanted to get your comments.

LC. Yes.

KD. Joe, when you look at it from our PowerPoint presentations posted online from the various conferences we’ve had at Roth Capital China in Miami and also this past week in New York here at the Merriman conference, the two core new products are in ePlay, and the ePlay is that educational learning platform with Thomas & Friends. And that does have audio embedded in for the play with numbers and also the character association products, And so that’s a defining line.

The second is with the iQuiz Cards. Now, there’s two different types of iQuiz cards. There’s the one with the sound, right around an $8.99 MSRP in the States, and then a smaller version that does not have sound which is similar to our size and dimension of our Electronic Game Cards, but a little bit thicker than a credit card. And that particular platform does not have sound and is priced between $3.99 and $4.99 MSRP and has a variety of genre associated, popular culture and interests.

Q. OK. that’s helpful. On the World Expo potential in China, where do you see yourselves standing? Do you think there’s still an opportunity or are you a little – or based on your initial move into the country, will you be able to still, you know.

KD. Let’s look at it in terms of where we’re going in terms of beginning of December with them. So we’re working through the details for the next year. Although the Shanghai World Expo starts in May, it does run all the way through the end of October, and one of the key initiatives we have together is to hit tourism, and that will be one of the featured highlight areas of tourism in the country of China during 2010. So the final decisions have not been made yet. There have been discussions with China Lot Synergy and the local government and legal officials there in Shanghai, so we’ll be able to disclose whether we’re part of that or not forthcoming, we hope, in December.

Q. OK., Lastly, just a quick update on the CFO situation. Are you looking for a new CFO currently or what is your plan?

KD. At the present time we are working very closely with Tom Schiff, who’s a great person, very talented, and well-skilled, and seasoned experience at the CFO position with public companies. And so we are in the process of working through a little bit of time here, and the ability to see if we can bring Tom back in. In the event that Tom does not come back in, we will have another CFO added to our Board.

Q. All right. Thank you very much.

KD. Thank you, Joe.

JACK CUMMINS

Q. Great job. When are you guys going to move to NASDAQ?

KD. Thank you, Jack. We’re doing everything we can on a daily basis to organically grow this company and the stock and our sales efforts. So, you know, that’s our core goal. And so we hope to get there sooner than later. Lee?

LC/Q ________

KD. Thank you very much, Jack.

ANDREW COWAN – TRICADIA

Q. Hi, guys. Great quarter. Really nice execution across the board. Quick question. I know that Lord Steinberg had been working with getting the cards into his betting parlors of Eastern Europe. I’m just wondering with his unfortunately untimely passing, where that stands and if there were any other lottery opportunities going on in Europe that I thought I had heard that he had been working on or the company had been working on previously in addition to the lottery opportunity in China.

LC. Yes, I mean with the betting parlors we’ve actually got samples going out I think next month into a variety of stores in a test market. And with the lotteries, we’re currently talking to two other lotteries in Europe, which we don’t – which we’re not at the stage to disclose yet.

Q. OK. That’s all I had. Great quarter.

KD. Thank you very much, Andrew.

RICHARD FETYKO – MERRIMAN

Q. Hey guys. My question is just to follow up on the betting parlors. What type of cards are we talking about? Promotional cards or some other, you know, concept?

LC. Actually, some other concepts where they’d be betting. I haven’t actually been dealing with it. The guy who’s been dealing with it actually isn’t with us today because his wife’s just had a baby. So yeah, but they’re going out. I will get you some samples of the mock-ups, Richard.

Q. That’s fantastic. And on the D&O insurance. Just curious, what is the timing of having the D&O insurance? I assume you’re looking to have that.

KD. We do have the D&O insurance in place now.

Q. OK.

KD. It was an oversight by the management, not by Tom Schiff. And so what – we do have that in place nowl and so we’re just working through the process of the item of getting Tom back on board.

Q. Got it. All right. Thanks.

KD. Thank you very much, Richard.

MICHAEL WEISS – JOSLYNDA CAPITAL

Q. Hi, guys. Very good quarter. Can you speak a little bit – I haven’t heard you speak about your sports initiatives lately. How’s that going? Or are you de-emphasizing that at all?

KD. No. Not at all. Hi, Michael. How are you?

Q. Hey, Kevin. How are you?

KD. Good, thanks. We continue on the sports front. The major sports properties with the relationship we have with BD&A. BD&A is a master licensee of the majority of sports properties and we’re looking at a couple that continue with the promotional cards for Electronic Game Card and also now with the new Poken product because the Poken product leads the consumer in that sports fan initiative online. And you can only imagine the possibilities that stem from having that product leading the consumer online, online engagement, online interaction, and the measurability of that product. And so the discussions have been helping the other products grow in further opportunities within the sports properties. And so there’ll be some forthcoming information, you know, released in greater detail.

Q. Thank you very much.

KD. Thank you, Michael.

DAVID WATSON

Q. Yeah, hi. I’m just curious, you know you guys are building a pretty large cash position. What do you plan on doing with that?

47:45

LC. Well, I mean as the company grows, it’s going to need to take in more inventory and there’s potential acquisitions that can grow our EPS. That’s actually what the near term is, wouldn’t you say, Kevin?

KD. Yes. Absolutely. Those are the two – or usage for the capital.

Q. Can you describe sort of what your criteria – when you’re going to do an acquisition what your criteria might be?

KD. Well, we look at an acquisition and the first thing is always having a controlling interest of an acquisition, And it has to be complementary in technology to reach a larger growth market, and so that’s core and fundamental. And so we work through the business model with our strategic consultants to assess and evaluate, and if that technology fits within a formula that we have based on low cost, high margin, high volume, customizable to the B2B market, then there could be some great fits. So based on that – we also look at doing joint ventures. We also, as our track record has showed, we’re not afraid to license in for exclusive rights and distribution. So we just have to continue along the evaluation of those three routes of acquisition, joint venture, or licensing in.

Q. And so you guys haven’t given guidance for 2010 but sort of your base business, which is the promotions market as well as some of the licenses you get from Sci Games and the tribal gaming. That core business, assuming you didn’t get any new business from a lot of the new stuff that you guys have talked about, how much growth would you expect in that base business next year?

LC. Well, even if you only add 10% or 15% growth on that base business, that would be $.16 on its own. But we’re expecting more growth with all the new products.

Q. OK. So the base business, you feel like 10 to 15% growth is achievable, so next year just on the base business you’d assume $.16 EPS.

LC. Yes. And with all the new products and all the new initiatives that’s where we see the real growth. _____ all products have life cycles.

Q. OK. Thanks.

KD. Thanks, David.

{Operator comments]

KD. Well thank you very much, everyone, for your great questions, Yvonne Zappulla, our Board. And I would like to personally thank all of you for your interest and support of our company. We are in an enviable position. We have a company that has a solid financial base to address a multi-billion dollar market opportunity with several proprietary product platforms that generate high margins with little competition. To this we have added an infrastructure of high level outstanding executives, high level joint venture partners and distributors, as well as top-quality, low-cost manufacturers with ample capacity to meet the extraordinary growth we intend to deliver.

Our annual shareholder meeting is now scheduled for Thursday, December 10th at 11:00 am Eastern Standard Time at the Grannus Financial offices in Manhattan, New York. Please contact Yvonne Zappulla if you plan to attend.

And that is it. I’d like to thank all my colleagues here in the U.S. and the London office. And I want to personally thank each and every one of you from the company. Have a happy holiday season. And we have many things to be thankful for.

New Wave, Q2 comments re TPM customer

My computer is not yet able to access the call, so I don’t know exactly what SKS just said, but for comparison, this is what he said in the Q2 cc about minute 15:

“We’ve also seen the in the course of the last couple of months now some of the first really large transactions associated with Trusted Platform Module management. We have a large multi-national that’s just started a 1,000-seat pilot. They’re turning on technology for securing their Virtual Private Network, for securing their wireless infrastructure. And they really have a tremendous potential for us. They represent somewhere between a 50 and 70,000 seat opportunity in front of us if the pilot goes well. So we’ll see how ultimately their adoption curve is. They’re going to get used to this technology and understand how that it can impact their daily security needs.”

I’m not sure how a 50 to 70,000 seat company turns into a 100,000 seat company. But isn’t it better anyway if it’s two large pilots rather than one?

GWMAN, good information. Thanks.

Did this info come from a previous post?

GWMAN, thanks for responding

I'm sorry to hear that the product was barely available on September 15, as Lee stated it would start shipping in Q3 (in the Q2 CC). See below.

It's hard to believe that promotions would suddenly jump up 30% sequentially after showing slow and gradual growth - especially since no one mentioned such an expectation in the Q2 CC.

Well, per the Roth conference Q3 revs were about $4.1 million, guidance given after quarter end. I guess we'll have to wait to find out where it came from unless casino has more details.

+++++++++++++++++++++

Transcript, around minute 31

Q. My question. I have two questions. The first one: it looks like you’re currently on a $12 million revenue rate. And also it looks like you’re basically on a $.03 per quarter rate. And I was wondering, with the second half of the year now upon us and expectations for 17 to 18 million in revenue and $.14 in earnings, where is that extra bump in revenue and earnings going to come from?

LC. Coming from a new product which we’re shipping third quarter, [which is?] Quiz Card.

Transcript Post

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=40450448

casino, you say

“The increased revenues are attributed to increased distribution partners mostly in Europe.”

“Further sequential revenue/net income gains are expected in Q4 2009 as the iQuiz card rollout commences.”

1. Are you saying that the Quiz Cards did not ship in Q3?

2. And you’re expecting an additional $1 million in revenues qtr over qtr from the promotion business alone?

3. This in spite of Lee’s statement in the cc in response to your excellent question that the ramp needed in Q3 and Q4 to meet guidance would come from the Quiz Cards?

TIA for any clarification.

Twitter feed from i-stage re ZAGGbox

http://twitter.com/CEAfeed

Judges getting down to it. @jeffpulver to @zagginc: is this good for stealing content?

20 minutes ago from Twitterrific

Well, you know they’ve been saying $16 to $17 million revenue for 2009. I have felt there wasn’t enough information on how they were going to jump from about $6 million in 1H09 to $10 million or more in 2H09. So it sounds like they’ve got $4.1 million in the bag for Q3. Now they just have to come through in Q4 for a couple of million more.

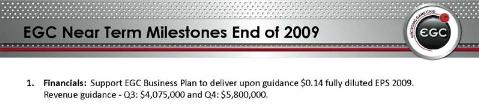

For the Short-term View

2H09 Revenue Guidance

Q3: 4,075,000

Q4: 5,800,000

My impression was that posters were saying IGT was somehow going to be funding this. Whether EGMI is providing cards or money, it will pay its share, I still have to assume.

Concerning the statement from the PR you quoted, “Under the terms of the Strategic Partnership, EGC will provide the China LotSynergy Electronic Lottery GameCards for initial sales and marketing efforts.” Earlier the PR says, “The companies will conduct initial trials during the next few months in China to ensure optimum offering for the market.”

Do “initial sales and marketing efforts” equal “initial trials”? I don’t know. Maybe the point of the statement you quoted is that EGMI will be providing the cards in the initial stages of the actual roll-out of the product and then later CLS or the JV will do the manufacturing. I don’t know.

But maybe it’s not even worth speculating who pays, because possibly the trials won’t cost very much. Or possibly the major cost of a trial will be the cards themselves. Who knows?

Anyway, I’m glad I brought it up. Your responses have given me a little more clarity on the possibilities although I still don't have much clarity on the facts.

++++++++++++++++++

As for, “In addition to the Lottery GameCards, EGC and CLS will also cooperate in markets involving royalty credit and gift projects.” I assume they left out commas and it should be “royalty, credit, and gift projects.” It may mean there will be other programs that will be based on a royalty or license-type arrangement. Also other uses of the cards entirely such as gift cards like we have here for shopping but with some added functionality which allows people to win something. Could also mean promotions, as you suggest. Or….

GWMAN, thanks for the response.

Below is a report of a substantial investment by IGT into CLS in 2007 and a statement from EGMI’s last CC mentioning IGT.

But I don’t (yet) see any reason to think that EGMI would not be funding its share of developing a program with CLS.

++++++++++++++++++

May. 03, 2007 “International Game Technology, the Reno-based slot giant, on Wednesday announced an alliance with China LotSynergy Holdings Ltd. that will let it gain a foothold in the China lottery market. In a statement, IGT said it will invest $103 million in China Lot Synergy through shares and a convertible note. IGT said it expects the deal to close by the end of the month. An IGT representative did not return a call for comment Wednesday afternoon.”

From the last EGMI CC: “This partnership will provide EGC with new strategic relationships with GTECH and IGT for alignment synergies of new lottery opportunities within additional territories within the region and other parts of the world.”

Back to China and IGT for a moment

Why does the IGT and CLS investment into their JV have anything to do with EGMI’s joint venture with CLS (other than to indicate CLS is putting money and energy into moving forward on a number of fronts to build the lottery business)?

There were four or five posts concerning the EGMI JV with statements like “the majority of the capital is being funded by others” and “there's little to no costs associated with it” apparently believing IGT would be funding the trial programs for EGMI’s cards. I don’t see any indication that any of the IGT money will be going to the EGMI program.

If someone reads it differently, or has other info, I’d appreciate your posting it.

From post #6442

The board of directors (the “Directors’) of China LotSynergy Holdings Limited (the “Company”, together with its subsidiaries, the “Group”) would like to update the shareholders of the Company on the latest development of the Group’s businesses.

The Board is pleased to announce that, on 12 October 2009, the Group and International Game Technology (“IGT”), the Group’s strategic partner, made a further capital injection in the amount of US$9,860,000 into their joint venture in China – IGT-Synergy Technology (Beijing) Co., Ltd. (the “Capital Injection”). The injected capital will be used to develop the lottery business in China.

You gotta love this.

"If we could afford to replace all our poles tomorrow with the RStandard pole, we would do it...."

Composite Poles Stand Up to Texas Tornado

Oct 13, 2009 07:10:00 (ET)

CALGARY, Oct 13, 2009 /PRNewswire-FirstCall via COMTEX/ --

RStandard(R) Poles Continue to Perform Where Other Poles Failed

Resin Systems Inc. ("RS") (RS - TSX), a technology innovator and manufacturer of advanced composite products for infrastructure markets, announces its RStandard(R) poles have withstood an important field test in Lajitas, Texas - a direct hit by a tornado. In spite of high winds and swirling debris, the RStandard poles demonstrated their worth and capability in hardening the Rio Grande Electric Cooperative, Inc. ("RGEC") grid. RGEC maintains over 9,400 miles of distribution line and 143 miles of transmission line in west Texas and southern New Mexico comprising an area over 27,000 square miles.

Dan Laws, general manager and chief executive officer for RGEC, stated, "A tornado touched down in Lajitas on October 7th. Several homes in the area had roofs ripped completely off. We had padmounted transformers and junction boxes swept completely off their pads! We lost eight 40 ft. Class 3 wooden poles on our brand new Study Butte-Lajitas 34.5kV 3O line. These were snapped off like toothpicks two feet above the ground. RGEC Operations reported that the RStandard composite poles that we installed in this area 'did not budge at all.' "

Even before the tornado struck, RGEC was already considering the purchase of additional RStandard poles for several projects because of their favorable previous experience installing RStandard poles. Obviously, the RGEC is now even more impressed with RStandard composite pole technology.

"If we could afford to replace all our poles tomorrow with the RStandard pole, we would do it given the increased strength, durability and reliability that we believe these poles would provide." stated Larry T. Powell, director of engineering for RGEC.

Paul Giannelia, president and chief executive officer of RS, stated, "The fact that our poles withstood this tornado proves our RStandard poles are the most reliable and robust pole technology on the market. Combining the strength of our poles with our industry-leading lifetime guarantee and 41-year warranty gives utilities like RGEC confidence they are providing a higher level of reliable electric service to their customers."

About Rio Grande Electric Cooperative, Inc.

Rio Grande Electric Cooperative, Inc., headquartered in Brackettville, TX, is a member-owned, non-profit electric cooperative, serving rural residents in eighteen counties in Texas, and two counties in New Mexico. With offices in Brackettville, Carrizo Springs, El Paso, Fort Stockton, Dell City, and Marfa, RGEC employs over 130 rural residents. RGEC has a strong history of community service and promotion of sustainable rural development throughout its 27,000 square mile service territory. RGEC also maintains the electrical distribution system for Ft. Bliss, El Paso, TX, the nation's largest Army Air Artillery Base. In addition, RGEC was just awarded the privatization contract for the electric distribution infrastructure at Laughlin Air Force Base in Del Rio, Texas. For more information on Rio Grande Electric Cooperative, call 1-800-749-1509, or visit the web site at www.riogrande.coop .

About RS

RS is a technology innovator that develops advanced composite material products for infrastructure markets. The composite products manufactured using the Company's proprietary resins and processes are typically lighter, more durable and longer-lasting than competing products made from the traditional building blocks of wood, steel or concrete. RS's flagship product is its award-winning RStandard(R) composite pole. The pole is used as transmission and distribution poles to carry electric grids and as communication structures for various uses including wireless networks and microwave communications systems.

For the latest on RS's developments, go to the company's website at www.grouprsi.com .