News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Dragon Lady

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

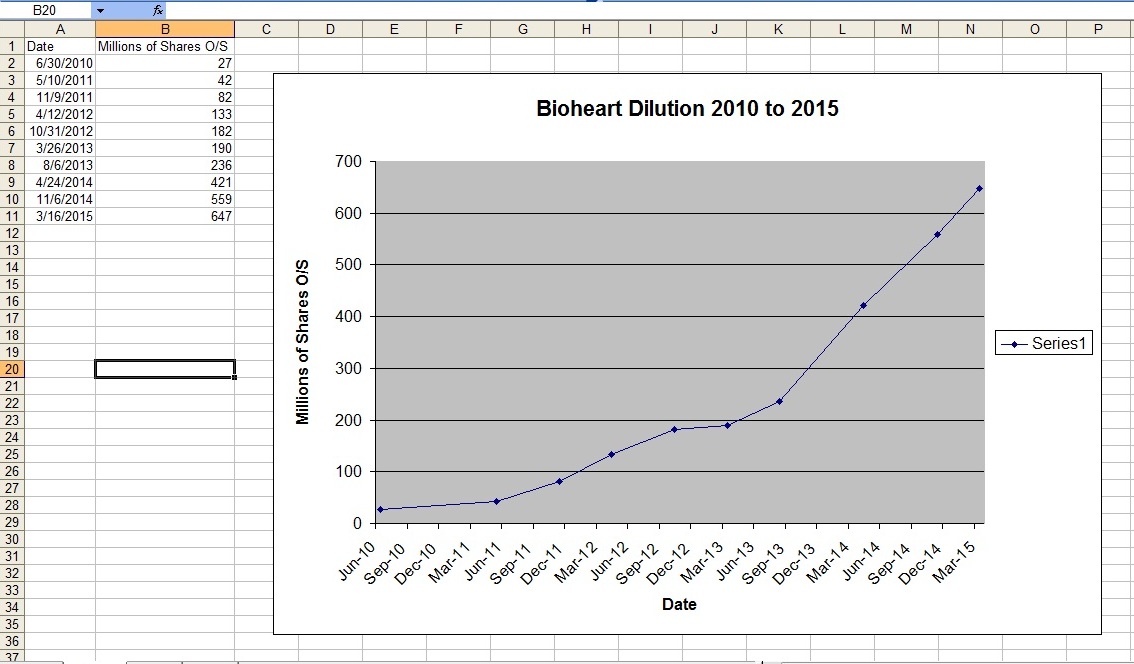

What does MASSIVE DILUTION "look" like?

I'm more a "visual" chart/graph kinda person. I know there's been a lot of dilution on this one from reading their SEC filed 10-Q and 10-K statements. But I wanted to "see" how rapidly or not it's been accelerating and occurring. So I took about 10 minutes and went through the 10-Q/10-K filing links on BHRT's web page- and picked enough files to give me enough data points to get a relatively "smooth" plot.

I just took the O/S share count which is typically PAGE 1 of any 10-Q or 10-K filing (will say something like, "As of date such n such the number of outstanding shares of the registrants common stock was X millions of shares", something like that, always on PAGE 1 or 2 of the SEC filing).

So I just went back to mid 2010 when Tomas took over as CEO and found the O/S share count was then about 27 MILLION shares. As of this just filed 10-K covering to the end of yr 2014, it's now like 647 MILLION shares O/S (668 million shares fully diluted) and climbing rapidly. Here's what it looks like- DILUTION and lots of it. The graph is the date/months/yr on the "X" axis, versus MILLIONS of shares of dilution on the "Y" axis. One can see it's accelerating, going more vertical- not slowing down as some have indicated or implied.

So I just tossed the O/S share numbers and dates real quick into an Excel spread sheet to get a "visual" graph of O/S share dilution and that graph above is what it looks like. IMO it explains a lot of what's happening to the falling share price.

It's one thing to go from say 30 MILLION to 60 MILLION shares in one yr in the past- as that's only 30 million shares the market needed to "soak up". But as the pace picks up and ever accelerates- you now have a past 1 yr where the market now needs to "soak up" 300 MILLION or more shares. It's gonna get harder and harder IMO to "vacuum up" the shear volume of shares hitting the sell-side of the market as the "dilution curve" goes more and more towards vertical as the graph shows.

For an example of what's been happening dilution wise- look at the dates and share count. It took the company from inception/IPO date to about March of 2012 to reach 100 MILLION shares O/S. It then only takes from March of 2012 to about April/May or so of 2013 to double to 200 MILLION shares O/S. It then takes from May of 2013 to only May/June of 2014 to DOUBLE AGAIN to about 400 MILLION shares O/S. And then from May 2014 to now March of 2015 to hit over 640 MILLION shares. Pretty staggering to consider IMO.

And remember, all along the way- the BOD (Board Of Directors) has continually been upping/increasing the A/S (available shares) so they can keep this dilution thing going. The last A/S increase by the BOD increased the available shares now to 2 BILLION available, as they know, they plan to dilute to "no end" essentially IMO. Why else pick a staggering number like 2 BILLION when there was already 950 MILLION shares available when the BOD filed that share-increase authorization SEC filing back in only May of 2014 w/ a SEC Form Schedule 14A filing?

From their IPO in 2008 to mid 2010 when Tomas took over as CEO, BHRT had only reached about 30 million shares outstanding. From mid 2010 to today, about 5 yrs later, the shares O/S have gone up by a factor of more than 23X, just a staggering increase, and still climbing rapidly due to continual use of dilutive financing deals- the most recent deal inked in Feb of 2015 with "Vis Vires" group and also the Magna "credit line" now being tapped, more than likely continually, on-going, for what will be 22 or so more months (if BHRT continues to be in business as a "going concern" for 22 more months, see their latest filed 10-K "going concern warnings" from their auditing firm, PAGES 27, 44, 56, F-2 and F-12.)

Again, just my .009 cents worth. Just some data to look at.

.008 day's low, There it goes- probably new all times lows on the way soon IMO.

Look at all the volume this AM as both the Bid/Ask are dropped hard by these MM's. Ask even went sub .009 It seems like Friday lows are becoming a "new normal" now too? I'd have to check a daily chart- but it seems these MM's have a knack for liking to bury it on Fridays in particular.

.007 is now the 52 week low made in early 2015 and it's trading presently just a shade off of that. And .0063, which it touched for a brief moment Dec 2013 is the all, all time low. I think at some point here before too long- it's gonna break that .0063 all time low IMO.

Another round of "PR's" and whatnot- and nothing, it just sells off (though the PR's to me contain pretty much nothing of substance- as they lack any clue as to how BHRT will move ahead financially, ending 2014 w/ $36K cash-on-hand and no trials being conducted and their R&D spending cut by over $500K in 2014 to almost nothing, but grand sounding PR about how they're gonna "spend" on this and that, and not even on their core trials or business? Actually, I find it hard to even figure out what their actual "business" they're in really is anymore IMO. Makes zero sense to me personally, none.)

There is absolutely no buying interest/buying pressure I can see and now a near endless supply of dilution shares- hitting now in real time and 10's of millions more coming all through the summer and all the way to Oct 2015 when one read the due dates on all the toxic notes that can (and will IMO) be getting converted to very, very cheap free-trading shares. Plus the Manga "credit line" per the 10-K is being "tapped", most likely continually now, so all those dilution shares will also be flowing onto the sell side of the market, 10's of millions of them.

So they're also being financed too now (living off of, for all intents and purposes) using two deals from the firm "Magna LLC" of notorious "fame" on the street. Yet they just did Qty-3 more "toxic" convertible note financing deals w/ other lending firms too, as recently as Feb 2015 per their just filed 10-K report, see PAGE F-34, even adding a new firm I've never seen them use prior, named "Vis Vires Group" (plus another deal with KBM and one with Fourth Man again), "Vis Vires" another convertible debt lender/hedge firm of some sort. BHRT did a convertible, aka "toxic" note with this Vis Vires in Feb 2015 for a grand total of $38K, at a 45% share discount- that's how desperate they are for cash IMO. $38K lousy bucks of cash at horrible, highly dilutive terms.

Here's what Bloomberg finance, one of the most respected financial journals and TV channels in the world had to say about "Magna LLC" (who BHRT just made use of twice, for financing deals recently end 2014/early 2015 and ongoing now via an open "credit line")- it ain't a pretty picture IMO.

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Looks like tough sledding ahead here IMO for these common shares. It appears to me to be "ratcheting" down in stair-steps. Lower highs and lower lows continuously as the "trend" now- blips up along the way, but makes a continual, un-broken "stair-step" down, an unbroken down-trend of now 10 plus months is what I'm seeing as these convertible debt firms "convert" and then sell, then convert again, at ever lower prices for ever higher amounts of shares, that they then sell and dump onto the sell-side of the market. I don't see how any "PR" is going to overcome that? Just don't see it at this point IMO.

BMAK just slid down the Ask to .0092 w/ what? You got it, a 10K share block as always. They keep bringing that Ask lower and lower in increments- by the week or so. Let it breathe a bit, then back on it with the 10K share block, setting the "cap" when, and as needed, by whoever they're buying or selling for (Magna or Asher IMO).

http://www.otcmarkets.com/stock/BHRT/quote

My .008 cents worth

What? Death and taxes? The other poster said based on "insider info" that HE KNOWS, FOR CERTAIN it's going to be a "successful venture" and "sooner than later".

That's the exact words stated. The words, "I KNOW FOR A FACT". FACT doesn't mean "maybe" it means with 100% certainty.

Quote below:

"I know for a fact - which unfortunately cannot be disclosed - that this project is "very real" and "very near and dear" to Mr Tomas. This will be a successful venture sooner rather than later!

For the sake of anyone who would question my integrity and knowledge of inside info and the legality of such, that is not the reason for my non disclosure. It is purely for professional and ethical obligations.

IMO... This is fabulous news!!!"

Says FACT it "will be a success", not "maybe"?? And that claim is that it's based on insider info per the statement.

But that's in 100% contract to the actual PR "disclaimer"?

http://finance.yahoo.com/news/bioheart-ascyrus-medical-execute-investment-133000431.html

"Forward-Looking Statements: Except for historical matters contained herein, statements made in this press release are forward-looking statements. Without limiting the generality of the foregoing, words such as "may", "will", "to", "plan", "expect", "believe", "anticipate", "intend", "could", "would", "estimate", or "continue", or the negative other variations thereof or comparable terminology are intended to identify forward-looking statements.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Also, forward-looking statements represent our management's beliefs and assumptions only as of the date hereof. Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

The Company is subject to the risks and uncertainties described in its filings with the Securities and Exchange Commission, including the section entitled "Risk Factors" in its Annual Report on Form 10-K for the year ended December 31, 2014, and its Quarterly Reports on Form 10-Q."

TOTAL BS IMO, quote, "I know for a fact - which unfortunately cannot be disclosed - that this project is "very real" and "very near and dear" to Mr Tomas. This will be a successful venture sooner rather than later!

For the sake of anyone who would question my integrity and knowledge of inside info and the legality of such, that is not the reason for my non disclosure. It is purely for professional and ethical obligations.

IMO... This is fabulous news!!!"

Total, utter nonsense IMO.

Here is the PR disclaimer that says the company itself doesn't even know if this is going to be a "successful venture" or not. Right now, according to the PR itself- it's not even an actual "venture" between two companies but merely some "agreement" and has "milestones" that must be met by June of 2015, or apparently the whole thing is for not, etc

http://finance.yahoo.com/news/bioheart-ascyrus-medical-execute-investment-133000431.html

Quote from the PR:

"Forward-Looking Statements: Except for historical matters contained herein, statements made in this press release are forward-looking statements. Without limiting the generality of the foregoing, words such as "may", "will", "to", "plan", "expect", "believe", "anticipate", "intend", "could", "would", "estimate", or "continue", or the negative other variations thereof or comparable terminology are intended to identify forward-looking statements.

Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Also, forward-looking statements represent our management's beliefs and assumptions only as of the date hereof. Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in these forward-looking statements, even if new information becomes available in the future.

The Company is subject to the risks and uncertainties described in its filings with the Securities and Exchange Commission, including the section entitled "Risk Factors" in its Annual Report on Form 10-K for the year ended December 31, 2014, and its Quarterly Reports on Form 10-Q."

Bioheart itself is saying they don't know with any certainty whatsoever and will not "guarantee" it's going to be a "successful venture", let alone "SOONER THAN LATER", etc

LOL, quote, "The market is not reflecting the real PPS of BHRT at this time. In my opinion we should be at .20 minimum IMO"

OK? So this is a "fake" free market share price and not the "real" imaginary, make up a wish price of .20 "minimum"??

How does that work exactly? A FREE MARKET where shares are bought and sold based on supply and demand is FAIRLY PRICING a stock right now at about .009, aka 9/10ths of ONE CENT. Buyers and sellers are trading actively in real time paying .009 or so, but that's the "fake" price and it should really be like 20X more at .20 "minimum"?? Wow !!

So the stock is supposedly imaginary worth over 20X's the current MARKET price of .009 but no one apparently knows it, and it's really supposed to be at a "minimum" of .20?? Based on what criteria?

IF it's "worth" .20, one can always put in LIMIT BUY ORDERS for millions of shares of $millions of dollars worth at .20 and the MM's as far as I know will fill those orders probably. Not sure- they may have to fill them "at market" which is .009 or so right now?

Else, someone could call the company itself and offer $MILLIONS of investment money and say they want to buy shares at .20 "minimum" and I'm sure that can be arranged. AS opposed to say Magna or Asher or similar who are getting their shares for as low as .005 each based on the convertible debt "conversion formulas" build into those the toxic debt deals.

I'm sure someone will take the money at .20 a share since that's the "real" price and all. I mean why pay the FREE MARKET .009 per share of today when one could pay the apparently "real price" of .20 or more??

LOL, quote, ""The Ascyrus Medical Hybrid Graft, when approved for commercialization, will save thousands of lives," said Dr. Ali P. Shahriari, CEO, Ascyrus Medical, LLC. "We believe the AMHG is superior technology in its medical utility, ease of use and risk reduction. Inventing the AMHG is a single step in commercializing this novel and important medical technology. Our developing partnership with Mike Tomas and the Bioheart team will enable Ascyrus Medical to expeditiously advance the AMHG through its clinical evaluation, regulatory approval and market penetration. The Bioheart / Ascyrus Medical partnership will save lives." "

OK, LOL, "sounds great"???

When approved? And when might that be- like in HOW MANY YEARS FROM NOW and how many $10's of millions of dollars later?

And "we believe" it's "superior technology" but know one even knows what "it" is exactly or what makes it "superior" supposedly etc?

OK. Sounds like "PR" to me. Classic. It doesn't even list where this "new company" (a just formed LLC) is even located or if it has one dime of investment money already lined up, etc.

It's so vague- what can possibly be even known about this "thing" - at this point? NOTHING, that's what IMO.

It needs "clinical evaluation and regulatory approval"?? YEARS then, if ever approved. Big whoop. What's BHRT going to use to "invest" in this unapproved device then? They, BHRT, can't even fund their own clinical trials for "LACK OF FUNDS" per their own, just released 10-K filing. But now are supposedly going to "invest" in some just formed, one person LLC and get a medical device funded all the way to regulatory approval, LOL? Really?

Is this coming from the BHRT imaginary "share buy-back money" that they don't have too, LOL ?(see just filed 10-K, finished 2014 with $36K TOTAL CASH to their name and did convertible debt financing as recent as Feb 2015, so they're gonna "buy back" share with their own dilution financing deals, LOL? Really?) Or, is this "agreement" going to be paid for with the just the sell shares at .0085 cents dilution fund- or via the latest convertible debt deal they did in Feb 2015 for like $25K or whatever it was with some new toxic lender named Vis Vires Group?

This is past out in "pipe dream" land IMO. Just another BHRT ole "PR" about some vague "agreement"- I've got a list of these from the past all bookmarked and archived. "South Africa" for example wasn't even mentioned in the just filed 10-K, but was per "PR" supposedly a "new partnership" and all. Getting a brand new "medical heart device" through the initial clinical phases and then through "regulatory approvals" when BHRT isn't even funding their own trials for "LACK OF FUNDS" and in 2014 just cut their own R&D spending to near zero, CUTTING their own R&D by over $500K. But now they're gonna supposedly (maybe, might, perhaps) "invest" (no money amount listed in the PR OF COURSE, what a surprise) supposedly "invest" in some just formed LLC of a "doctor" who's location and details of this "device" are not even clearly listed or spelled out in the ole "PR"?? Really?

I don't even expect to ever hear about this Dr whoever again in any BHRT SEC filings and the "maybe" agreement that's not for sure until June 2015 or whatever- for a LLC "company" that's not even listed as having an address or location. Just a vague "PR" that doesn't say much of anything concrete IMO. So vague that one can't even understand what's actually involved in it from a business "deal" standpoint that I can figure out- just a typical BHRT "PR" to me. (The "South Africa" ole "agreement" and "great sounding PR" blasts all about "it" being the most similar non-event to me, in my recent memory. Search the just filed 10-K and try and find the "South Africa partnership" and see how much money BHRT is making off of that one now, LOL)

My .0085 cents worth.

LOL, another "PR" about some vague "agreement" being "entered into"???

http://finance.yahoo.com/news/bioheart-ascyrus-medical-execute-investment-133000431.html

That's about as vague a one I think I've ever read put out by them. Some doctor's name, and an "agreement" (hand shake, piece of paper back of napkin, etc? Remember the South Africa deal- the one later in the SEC filing that really had no legal contract or documents signed so it kinda like really never happened like the PR said (see PAGE 23 last filed 10-Q, and not even a mention of "South Africa" in just filed 10-K) - but "it" was an "agreement" had a "grand opening" and "treated patients" in the "PR" releases, only to be said later in the 10-Q, oops, we sorta never actually had any legal construct, no legal partnership so it sorta isn't really anything anymore. That was a real good one IMO, classic.

I don't even think the "PR" thingy even says where this supposed new LLC of Dr whoever is even located? I read it several times- and I don't even find a general location like what State, City other country, whatever?

Well, this one, this "PR"- even more vague IMO than even one like the ole "South Africa" or others in the oldies, classic files, IMO. They have an "agreement" according to the PR, but not really as "certain milestones" (NOT LISTED or spelled out of course) - ole "certain milestones" must be met by 6 months or something like that. So BHRT has until June 30th, 2015 to meet the un-listed "mystery milestones" and then what? What happens then? BHRT will take a "consolidating ownership stake" in this one doctor's company Ascyrus Medical, LLC which was just "organized" in Jan 2015, like 2 months ago, LOL? What exactly is a "consolidated" ownership stake versus just an "ownership stake"???? Never heard of such a thing or don't even know if that's a actual business term? Guess it sounds more "exciting" or something to say "consolidated"?

Of course, in TYPICAL, IMO, ole BHRT "PR" fashion- no mention of MONEY, or how much this "consolidated ownership stake" thingy would be, as in actual dollars, or what this new LLC of doctor so and so is supposedly even worth, or why it would be worth anything, etc?

I mean- an LLC is formed a few months ago and someone "might, maybe, could possible, perhaps" buy a unnamed part of it - but no one knows for how much, but they have until June of 2015 to do "it", execute this unknown "agreement" they have? Makes zero sense to me as always.

Then they either do, or do not have an "agreement" I guess with some single names "doctor" in some place- which it's not even clear what he does or why BHRT would have an "agreement" with him and some "company" this one doctor has that apparently has no product or sales or anything else?

That's a "PR CLASSIC" IMO if there ever was one. I guess it was time for a PR about something? I can't even remember how many Bioheart "agreements" there have been in past "PR's" put out - that were never heard about again and/or never amounted to anything for this company. I have all of um bookmarked and all, it's a long list of those ole vague, but "PR" worthy "agreements" of old.

Just a vague, nothing much "PR" IMO. I'd expect personally to probably never hear a thing about it again in the future.

My .0087 cents worth, NO OPENING TRADE, ZERO VOLUME again on open day's worth

Here is a great paragraph from the PR IMO- it uses the words "short term" and then hope to have a "long and prosperous relationship" in the same few lines- too funny IMO. Which is it? A short term investment or a long and prosperous one? Makes ZERO sense again to me, IMO? Very confusing the way it's written.

Quote:

"This investment agreement will enable Bioheart to share, if successful, in a significant and relatively short-term business opportunity. We greatly appreciate Dr. Shahriari's trust in our abilities and we look forward to a long and prosperous relationship with Dr. Shahriari and Ascyrus Medical." ???

What? LOL, is it a "short term" deal or a "long and prosperous" one? I sure don't get it? About as confusing a couple of lines as I've ever read? Again, I don't find a single line that even says where this doctor whoever is located and/or where this "Ascyrus Medical LLC" is even formed or located- in what state or wherever? One can't even look up the LLC since there's not even a location given? So its an "agreement" with what looks to be a single doctor and a newly formed LLC (forming an LLC literally takes about 20 minutes worth or less of paperwork to fill out and a small filing fee in almost every state I'm familiar with)

And this "thing" this one doctor has in a newly formed LLC is apparently going to need to go through "regulatory approval" via the PR- but is a "short term" thing? What? And what part of the $36K cash that BHRT ended 2014 with are they going to sink into some "medical device" that is at step ONE apparently of entering the FDA approval process- which would mean years to a commercial product if ever, most likely?

Quote:

" Our developing partnership with Mike Tomas and the Bioheart team will enable Ascyrus Medical to expeditiously advance the AMHG through its clinical evaluation, regulatory approval and market penetration. The Bioheart / Ascyrus Medical partnership will save lives"

Well, all except that the PR says they don't actually have a "partnership" yet, it says they have an "agreement" that's a "maybe" dependent on certain "financial milestones being met" (unnamed, not spelled out of course) and not even a "deal" until June of 2015, if ever- and of course no financial info is given (how much "investment", what ownership stake, etc, blah, blah, blah VAGUE as usual IMO)

LOL, quote, "Something is not right, why is this still under .01 with all the good news?"

Well, something's not right, that much is for sure IMO.

When a company (one that is THREE people total now per the 10-K just issued) dilutes out about 300 MILLION shares in the past 1 yr to live off of- it's gotta have some effect (negative IMO) eventually to the common shares.

Just filed 10-K PAGE F-10:

". Fully diluted shares outstanding were 668,063,786 and 344,241,761 for the years ended December 31, 2014 and 2013, respectively."

When a company with a stock price in the pennies, now SUB ONE CENT pours out 668,063,786 - 344,241,761 = 323,822,025 shares of PURE DILUTION in a one yr period (323 MILLION SHARES) - well, IMO at some point the ole "chickens gotta start to come home to roost". I think this is that point now.

Also, that massive, massive dilution is continuing on- unabated due to the continual use of toxic, convertible debt (floorless) financing deals for their survival cash- to pay their salaries, legal and other enormously increased "general and admin" expenses per their own just filed 10-K (general and admin expenses more than DOUBLED in 2014 from 2013, see PAGE F-4, just filed 10-K)

Also, when a company lives off of "toxic" convertible debt financing (and NO, "toxic" is not a "derogatory" or otherwise negative term as a poster yesterday tried to imply, the SEC, United States Securities And Exchange Commission uses that exact term on their website to describe this type of financing, as well as, the terms "death spiral" or "ratchet" etc. "toxic" debt financing is a well recognized, industry used term for this type of penny lending, floorless convertible debt, Bloomberg just used the same terms in a piece they wrote about Magna)- when a firm makes use of an essentially endless, on-going, continual flow of convertible debt deals to finance their operations- thus creating a never ending stream of 10's of MILLIONS of shares of stock dilution, LOW PRICED shares that will hit and be dumped to the sell side of the market- the share price per all standard research is usually going to get hit hard sooner or later (just read BHRT's own extensive warnings regarding their use of MAGNA financing in their latest filed 10-K, PAGES 36/37)

Just filed 10-K, PAGE 36:

"The sale or issuance of our common stock to Magna Equities II, LLC at a discount may cause substantial dilution and the resale of the shares of common stock by Magna Equities II, LLC into the public market, or the perception that such sales may occur, could cause the price of our common stock to fall."

Add to that- a continual list of convertible debt financing deals including Asher multiple times, Daniel James multiple times, Fourth Man multiple times, KBM Worldwide multiple times, and now a brand new 2015 toxic lender called Vis Vires Group, used just about one month ago, in Feb of 2015, their, BHRT's latest additional to their long, long list of toxic lenders they use for survival cash and to keep whatever it is exactly they do- going.

Including paying ever larger base salaries to TWO people and "cash" bonuses to TWO people of a now THREE total person company. Just TWO people of a now THREE total "employee" company- now have annual compensation packages totaling about $2.7 MILLION dollars annually. (see latest filed 10-K, compensation table, PAGE 65)

Just as ONE example of how much toxic debt is "hanging out there" to be converted - much of it coming due now, or in the next 6 months or less, just look at PAGE F-17 of the just filed 10-K, the 2014 ASHER NOTES:

"During the year ended December 31, 2014, the Company entered into a Securities Purchase Agreements with Asher Enterprises, Inc. (“Asher”) or affiliates, for the sale of 8% convertible notes in aggregate principal amount of $334,000 (the “Asher Notes”).

The Asher Notes bear interest at the rate of 8% per annum. As of December 31, 2014, all interest and principal must be repaid nine months from the issuance date, with the last note being due August 12, 2015. The Notes are convertible into common stock, at Asher’s option, at a 45% discount to the average of the three lowest closing bid prices of the common stock during the 10 trading day period prior to conversion. The Company has identified the embedded derivatives related to the Asher Notes.

These embedded derivatives included certain conversion features and reset provision. The accounting treatment of derivative financial instruments requires that the Company record fair value of the derivatives as of the inception date of Asher Notes and to fair value as of each subsequent reporting date, which at December 31, 2014 was $149,770. At the inception of the Asher Notes, the Company determined the aggregate fair value of $566,294 of the embedded derivatives.

For the year ended December 31, 2014, the Company amortized $248,153 of debt discount to current period operations as interest expense.

The remaining principle balance as of December 31, 2014 was $151,000."

So Asher has been doing some converting of a total of $334K worth of "toxic" style convertible debt notes all done in 2014. But still has a $151K balance due- and that all is due by August 12, 2015 about 5 months from now. At these current price- how much more dilution would that add?

Well, Asher gets a 45% discount on their shares when they convert.

So .009 X .45 = .004. .009- .004 = .005 Asher gets their shares for if they convert right now. So how much dilution would that $151K Asher balance create if converted now at .005 per share?

$151K / .005 = 30 MILLION more dilution shares that is highly likely going to get paid to Asher alone, to settle notes that were already done months, and months ago and from which the money/cash was long ago spent.

THAT is what DILUTION DOES TO A STOCK and especially toxic dept financing type dilution. Asher will have 30 MILLION more shares at .005 cents each to dump onto the sell-side of the market. I don't see how there would possibly be enough retail buy interest generated to soak up all that cheap priced share selling that's most certainly coming. And that's just Asher. Not Magna, Daniel James, Fourth Man, KBM and now Vis Vires too- ALL of which will similarly be receiving shares to sell in the 10's of MILLIONS. It's DILUTION, a common share price crusher IMO.

Remember too- by the very way these "toxic" convertible debt financing deals are constructed- the LOWER THE SHARE PRICE GOES, a firm like Asher just gets more shares to convert. The price going lower makes no difference to them- they can actually profit even more typically the lower the share price goes.

What exactly was the "good news" part? I may have missed all that perhaps? I read the 10-K cover to cover yesterday and last night- I didn't really find the "good news" part I guess? There is none IMO?

But that just me I guess?

My .0085 cents worth

Excellent financial journalism piece by one of the most respected financial papers in the world, Bloomberg. It explains toxic type "penny financing" via explaining how Magna does what they do- but all the other firms operate on very similar business models (Asher, KBM, Daniel James, Fourth Man, etc)

Fascinating reading- very enlightening IMO as to why the BHRT share price is likely where it is today. DILUTION has consequences IMO, and BHRT lives off of dilution for all intents and purposes IMO.

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

LOL, "5. A 20% reduction in the Company's working capital deficit."

Well, add this little FACT from the 10-K and it's pretty easy to reduce that ole "working capital deficit" IMO.

Just filed 10-K, PAGE 55:

"Research and Development

Research and development expenses were $66,420 in 2014, a decrease of $560,563 from research and development expenses of $626,983 in 2013. The decrease was primarily attributable to a decrease in the amount of available funds.

The timing and amount of our planned research and development expenditures is dependent on our ability to obtain additional financing."

I used "word search" on that 10-K filing and I think the term "research and development", the term, exact phrase, appears at least 50 times or more before one gets to PAGE 55 WHERE THE ole "research and development" spending by the company is cut/hacked DOWN, REDUCED by over HALF A $MILLION large. $560,563 CUT from R&D makes the ole reduce that "working capital deficit" just a tad easier usually.

Only problem is, IMO, is that in the 54 pages of the 10-K that precedes that $560K CUT to R&D spending- they, BHRT, sure spent a whole lot of lines and time explaining how they're supposedly a "stem cell RESEARCH AND DEVELOPMENT" company of some sort and how RESEARCH AND DEVELOPMENT and the creation and maintaining supposedly of pesky stuff like PATENTS and NEW PRODUCT AND THERAPY development (aka R&D SPENDING) is just the ole life-blood and key to their supposed future and all.

Me, it's very confusing to me. To use the term "research and development" just so gosh darn many times in one part of that 10-K filing, and then to get to PAGE 55 and see they CUT THAT R&D SPENDING by over $550K to just about nothing per month being spent now?

I just can't personally "figure out" exactly how that would all quite "work" and all? But hey, that's just ole me I guess?

But yeah- knocking over $550K out of the ole R&D budget and CUTTING EMPLOYEES (see 10-Q from 3rd qtr compared to this just filed 10-K, PAGE F-11, THREE full time employees left total, at company now)- that always as far as I'm aware sure helps the ole "cut the working capital deficit" part a tad. Put that $500K plus CUT back to the R&D budget and then see what the old "working capital deficit" turns out to be.

My .0091 cents worth

Opening trade today of 600 shares at .0091. That's 600 X .0091 = $5.64 worth.

FIVE BUCKS and change for the opening trade and now almost ONE HOUR into the trading day, LOL?

Guess those buyers are just barreling in here after that incredible 10-K and the ole rosey "PR" the next day and all this other "good news" and the $BILLIONS it's all worth according to statements posted right here. Amazing IMO. Incredible to see that $5.64 worth of shares being bought up so rapidly on the Ask- that's a sure sign IMO of $BILLIONS fa sure.

LOL quote just stated by another post, "Frivolous, that's why they have low cash at hand because it is being protected, in my opinion. Why was NS created, to protect the company's interests, in my opinion. There so many layers I don't think they'll get a dime, in my opinion."

What? How's that?

So a PUBLIC TRADED COMPANY just filed it's annual report with the United State Security and Exchange Commission, thee SEC, thee securities regulatory body in the U.S., a very powerful agency, powerful enough to prosecute company officer's of businesses, shut down companies completely, halt the trading of any public stock it wants for any number of 100's of reasons etc.

And Bioheart per a stock msg board "theory" is supposedly HIDING CASH and using "layers" of secrecy and "protection" to secretly HIDE CASH that's supposedly really there- but not DULY REPORTED in the 10-K SEC report they just filed?

What? They have "low cash" because it's somehow imaginary "being protected" using "layers" in what's a PUBLIC TRADED, aka SUPPOSED TO BE 100% TRANSPARENT AND OPEN public traded firm that has public shareholders? Really?

I'd love to read more on EXACTLY how this "cash hiding" is being done supposedly. This is fascinating IMO. A public traded company is using secretive, non transparent to the public and SEC supposed "layers" and is HIDING or "protecting" CASH that they imaginary "have" but did not report on their balance sheet they just filed to the SEC??

Wow !! That would be amazing IMO. Stunning? I'd guess lots of biz folks on Wall Street and even the SEC and FINRA and just all kinds of folks would be interested to see how this "hide the cash" that's really there thingy-ma-jig system and methodology actually works and is supposedly being done right now at a public traded firm per the ole msg board "theory".

Fascinating IMO.

No opening trade? Back to flat-lining mode again?

Interesting? So after all the "big news" and great sounding "PR" yesterday and whatnot, that fantastic 10-K in which they finished the yr with only $36K cash on-hand (must be hidden cash somewhere according to latest posted "theories") given all that and it's now back to where it doesn't even post an opening trade with the Ask at only .0091?

0.009 / 0.0091 (111100 x 200000)

http://www.otcmarkets.com/stock/BHRT/quote

Where's all those buyers rushing in cause it's going to be worth a $BILLION or more and all? They don't want to buy it at SUB ONE CENT and get "rich" and all? They're all waiting I guess cause of twitter and imaginary "hidden cash" and Youtube and all that "stuff" explained earlier, LOL?

Very confusing IMO? I don't get it?

Wow, "filed a motion"??

AND WAS IT GRANTED? Where was anything "declared a sham"?? Just cause a defendant attorney files a motion doesn't mean anything has been "declare" by the court and the judge? Motions gets filed and dismissed and tossed all day long in cases- filing motions doesn't mean a thing unless the judge "grants" them and agrees with them. Where was this "sham" motion shown as being "granted" by the presiding judge?

Case still looks pretty "live" and on-going IMO?

That motion, the ole "sham" motion by the defendant attorney (what a surprise?) was filed what, back in Jan. I believe? And the ole defendant attorney of course puts out the old, "It's all a sham" PR like they always do? It's past Mid March 2015 now, almost April. Why's the "sham" case still going on then?

https://www.clerk-17th-flcourts.org/Clerkwebsite/BCCOC2/OdysseyPA/CaseSummary.aspx?CaseID=7862332&hidSearchType=party_case&DisplayCitation=no&CaseNumber=CACE14021256&SearchType=

Upper right hand corner- case number, judge's name assigned, and PENDING- which in court-speak means the case is 100% still live and "open" and "on-going".

There was nothing "declared a sham" by that court that I'm aware of?

LOL, quote, "And this latest suit was declared a sham and a motion was filed with the court."

What? Who "declared" what a "sham"??? By what legal entity, court or presiding judge or whatever? When was this imaginary "declaration" made?

Has the JUDGE IN THE CASE been alerted to this "sham" myth yet? Cause he's shown as STILL ASSIGNED and presiding over the 100% REAL, NON SHAM lawsuit in a 100% real Florida Court in Broward County?? He's had the case for going on close to FIVE MONTHS now- so he, the judge, is working on a "sham" all this time and doesn't know it?

A creditor to Bioheart is seeking over $2 MILLION in alleged prior owed, non repaid DEBT (DEBT by the way that's on the recent, just filed 10-K, right where the ole lawsuit says it should be, PAGE F-3, "SUBORDINATED DEBT, RELATED PARTY" for principal of $1.5 MILLION, exactly as spelled out in the original lawsuit filing by the plaintiff attorney)

https://www.clerk-17th-flcourts.org/Clerkwebsite/BCCOC2/OdysseyPA/CaseSummary.aspx?CaseID=7862332&hidSearchType=party_case&DisplayCitation=no&CaseNumber=CACE14021256&SearchType=

http://lawsuitpressrelease.com/investors-sue-bioheart-inc-millions-unpaid-debt

http://lawsuitpressrelease.com/wp-content/uploads/2014/12/Leonhardt-v.-Bioheart.pdf

Looks pretty real, aka "non sham" to me? Guess that judge tossed the ole "sham motion" maybe? Like that never happens in cases every single day?

And here's the 2nd large Bioheart lawsuit involving a sitting company Sr. Officer and member of this BOD. Is this one an imaginary "sham" too?

https://www.clerk-17th-flcourts.org/Clerkwebsite/BCCOC2/OdysseyPA/CaseSummary.aspx?CaseID=7155410&hidSearchType=party_case&DisplayCitation=no&CaseNumber=CACE13024037&SearchType=

All looking pretty real, ole "non sham" to me- they've been in that court system for a long time- for the presiding judges to not know about this "sham" myth IMO?

LOL, quote, "You would think that with all this negative talk about toxic financing, some would be happier that the company is trying to move away from it."

What? Move away from it? How's that?

They just did probably a record amount of it (toxic financing, would need to check the past 5 yrs or so of 10-K filings to see if it's a record- but it's as much as ever, if not more than past yrs) in 2014- and they just did qty-3 more, toxic, classic convertible debt deals in just 2015 already (floorless, high interest rate, 45% to 47% share discount, toxic/floorless floating conversion formula, etc) and it's only MID MARCH (KBM again, Fourth Man again and now Vis Vires in just 2015 Jan/Feb), the most recent deal being done in Feb 2015, even adding a new toxic lender to their long list, the "Vis Vires Group"

AND in addition to those qty-3 classic "toxic" style convertible notes- they, BHRT are now already actively tapping the Magna "credit line" facility- purely dilutive and "toxic" via its share discounting provisions and numerous other formulas built into it. BHRT has already given Magna a minimum of about 12 million shares in just "fees" and at least about 20 million shares for an initial "draw" on the credit line- for a total of about 32 MILLION pure, free trading dilution shares to Magna just right there. And that's not even counting if/when the $205K/$307K Magna classic style, "toxic" note begins to get fully diluted- another round of massive dilution will go to Magna from that also.

So what proof is there in any way that they, BHRT are "moving away" from use of toxic, convertible debt, dilution based funding? I don't see a single indication that that is remotely true? AND BHRT has cut their R&D spending to practically nothing (over $550K cut in just 2014 alone)- so what would happen if they even remotely tried to fund an actual FDA type legit, large scale clinical trial? PAID FOR WITH WHAT? I don't even see a trial as a remote possibility at this point IMO- they just ended the yr with $36K total cash on-hand and are already back at the till of qty-3 toxic dilution lenders for amounts like $25K and $38K etc? WHAT would possibly fund some large trial(s) costing minimum $10's of millions to even get close to getting a clinical trial off the ground? Total pipe dream IMO. Not happening that I can see.

They recently signed on to Magna- one of the most notorious penny lenders of last resort, a "toxic death spiral" finance house of high notoriety on the "Street" according to a recent Bloomberg Finance investigative journalism piece- and they, BHRT, in the SEC filings for the Magna deal said they intend to, and need to tap all $3 MILLION of it to advance their "business plans" forward and even that won't be enough (those exact words quoted below direct from the 10-K) - read the original share filing prospectus.

Here is the Bloomberg article and TV interview about Magna-

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Here is BHRT's own Sr Mgt words from the just filed 10-K, describing all the risks, highly likely dilution and all the rest of it - via their making use of Magna. It's all in the 10-K just filed.

PAGE 35/36 (it basically spells out the risks of the "death spiral" and "toxic" financing scenarios playing out same as the Bloomberg piece and the same as described on the SEC site itself- under "convertible debt")

From BHRT's just filed 10-K PAGE 35/36:

"Risks Related to the Transactions with Magna Equities II, LLC

Funding from our Purchase Agreement with Magna Equities II, LLC may be limited or insufficient to fund our operations or to implement our strategy.

Under our Purchase Agreement with Magna Equities II, LLC, and following December 22, 2014, the date of effectiveness of the registration statement of the shares underlying the Purchase Agreement , and subject to other conditions, we may direct Magna Equities II, LLC to purchase up to $3,000,000 of our shares of common stock over a 24-month period. Although the Purchase Agreement provides that we may sell up to $3,000,000 of our common stock to Magna Equities II, LLC, only 143,812,591 shares of our common stock were offered under the prospectus of the Registration Statement and disclosed in the Purchase Agreement, which represents (i) 31,000,000 shares of common stock that may be issued to Magna Equities II, LLC upon conversion of the Convertible Note, (ii) 12,000,000 shares of common stock that we issued to Magna Equities II, LLC as Initial Commitment Shares on October 27, 2014, (iii) a maximum of 15,890,872 shares of common stock that we may be required to issue to Magna Equities II, LLC as Additional Commitment Shares and (iv) 87,812,591 shares of common stock that we may issue to Magna Equities II, LLC as Shares pursuant to draw downs under the Purchase Agreement.

At an assumed purchase price of $0.01460 (equal to 93% of the closing price of our common stock of $0.01570 on November 10, 2014), and assuming the sale by us to Magna Equities II, LLC of all of the 87,812,591 Shares, or approximately 15.7% of our issued and outstanding common stock, including the issuance of such shares, being registered hereunder pursuant to draw downs under the Purchase Agreement, we would receive only approximately $1,282,064 in gross proceeds. Furthermore, we may receive substantially less than $1,282,064 in gross proceeds from the financing due to our share price, discount to market and other factors relating to our common stock. If we elect to issue and sell more than the 87,812,591 Shares offered to Magna Equities II, LLC, which we have the right, but not the obligation, to do, we must first register for resale under the Securities Act any such additional Shares, which could cause additional substantial dilution to our stockholders. Based on the above assumptions, we would be required to register an additional approximately 117,666,849 shares of our common stock to obtain the balance of $1,717,936 of the Total Commitment that would be available to us under the Purchase Agreement. We currently have authorized and available for issuance 2,000,000,000 shares of our common stock pursuant to our charter. Depending on the price at which Shares are ultimately sold, we may have to increase the number of our authorized shares in order to issue Shares to Magna Equities II, LLC.

There can be no assurance that we will be able to receive all or any of the Total Commitment from Magna Equities II, LLC because the Purchase Agreement contains certain limitations, restrictions, requirements, conditions and other provisions that could limit our ability to cause Magna Equities II, LLC to buy common stock from us. For instance, we are prohibited from issuing a Draw Down Notice if the amount requested in such Draw Down Notice exceeds the Maximum Draw Down Amount, or the sale of Shares pursuant to the Draw Down Notice would cause us to sell or Magna Equities II, LLC to purchase an aggregate number of shares of the Company’s common stock which would result in beneficial ownership by Magna Equities II, LLC of more than 9.99% of our common stock (as calculated pursuant to Section 13(d) of the Exchange Act and the rules and regulations thereunder). Moreover, there are limitations with respect to the frequency with which we may provide Draw Down Notices to Magna Equities II, LLC under the Purchase Agreement. Also, as discussed above, there must be an effective registration statement covering the resale of any Shares to be issued pursuant to any draw down under the Purchase Agreement,. These registration statements may be subject to review and comment by the staff of the Commission, and will require the consent of our independent registered public accounting firm. Therefore, the timing of effectiveness of these registration statements cannot be assured.

The extent to which we rely on Magna Equities II, LLC as a source of funding will depend on a number of factors, including the amount of working capital needed, the prevailing market price of our common stock and the extent to which we are able to secure working capital from other sources. If obtaining sufficient funding from Magna Equities II, LLC were to prove unavailable or prohibitively dilutive, we would need to secure another source of funding. Even if we sell all $3,000,000 of common stock under the Purchase Agreement with Magna Equities II,

35

LLC, we will still need additional capital to fully implement our current business, operating plans and development plans.

The sale or issuance of our common stock to Magna Equities II, LLC at a discount may cause substantial dilution and the resale of the shares of common stock by Magna Equities II, LLC into the public market, or the perception that such sales may occur, could cause the price of our common stock to fall.

Under the Purchase Agreement with Magna Equities II, LLC, and following December 22, 2014, the date of effectiveness of the registration statement of the shares underlying the Purchase Agreement, and subject to other conditions, we may direct Magna Equities II, LLC to purchase up to $3,000,000 of our shares of common stock over a 24-month period. We are registering an aggregate of 143,812,591 (including 12,000,000 shares already issued) shares of common stock in the registration statement of which this prospectus is a part pursuant to the Registration Rights Agreement, representing shares which have been and may be issuable to Magna Equities II, LLC under the Purchase Agreement and shares underlying the Convertible Note we issued to Magna Equities II, LLC. Notwithstanding Magna Equities II, LLC’s beneficial ownership limitation set forth in the Purchase Agreement and the Convertible Note, if all of the 143,812,591 shares offered under that prospectus were issued and outstanding as of the effective date of the registration statement, such shares would represent approximately 20.7% of the total number of shares of our common stock outstanding and 20.9% of the total number of outstanding shares of our common stock held by non-affiliates, in each case as of November 20, 2014. The number of shares ultimately offered for sale by Magna Equities II, LLC under that prospectus is dependent upon a number of factors, including the extent to which Magna Equities II, LLC converts the Convertible Note into shares of our common stock and the number of Shares we ultimately issue and sell to Magna Equities II, LLC under the Purchase Agreement. Because the actual purchase price for the Shares that we may sell to Magna Equities II, LLC will fluctuate based on the market price of our common stock during the term of the Purchase Agreement, we are not able to determine at this time the exact number of shares of our common stock that we will issue under the Purchase Agreement and, therefore, the exact number of shares we will ultimately register for resale under the Securities Act.

Specifically, because the per share purchase price for the Shares subject to a Draw Down Notice will be equal to a 7% discount to certain trading prices of our common stock as set forth in the Purchase Agreement, Magna Equities II, LLC will pay less than the then-prevailing market price for our common stock, and the actual purchase price for the Shares that we may sell to Magna Equities II, LLC will fluctuate based on the VWAPs and closing prices of our common stock during the term of the Purchase Agreement. As a result of this discount, Magna Equities II, LLC may have a financial incentive to sell our common stock immediately to realize the profit equal to the difference between the purchase price and the market price. If Magna Equities II, LLC sells the common stock, the market price of our common stock could decrease. If the market price of our common stock decreases, Magna Equities II, LLC may have a further incentive to sell the common stock that it holds. These sales may have a further impact on the market price of our common stock.

Moreover, there is an inverse relationship between the market price of our common stock and the number of shares of our common stock that may be sold pursuant to the Purchase Agreement. That is, the lower the market price, the more shares of our common stock that may be sold under the Purchase Agreement. Accordingly, if the market price of our common stock decreases (whether such decrease is due to sales by Magna Equities II, LLC in the market or otherwise) and, in turn, the purchase price of our common stock sold to Magna Equities II, LLC under the Purchase Agreement decreases, this could allow Magna Equities II, LLC to receive greater numbers of shares of our common stock pursuant to draw downs under the Purchase Agreement. Although the number of shares of our common stock that our existing stockholders own will not decrease, the common stock owned by our existing stockholders will represent a smaller percentage of our total outstanding shares after any such sales to Magna Equities II, LLC. Depending on market liquidity at the time, the sale of a substantial number of shares of our common stock to Magna Equities II, LLC at a discount to the then-prevailing market price for our common stock under the Purchase Agreement, and the resale of such shares by Magna Equities II, LLC into the public market, or the perception that such sales may occur, could cause the trading price of our common stock to decline, result in substantial dilution to existing stockholders and make it more difficult for us to sell equity or equity-related securities in the future at a time and at a price that we might otherwise wish to effect sales."

Pretty clear to me IMO. It's dilutive and they, the company itself BHRT, just wrote a small "text-book" explanation of "toxic" or "death spiral" financing risks and scenarios playing out IMO, if and when they make use of Magna's "credit line".

WHAT "reduction" is there of BHRT using dilutive, and what's called by the SEC and Bloomberg and other financial sources "toxic" or "death spiral" or "ratchet" financing (THEIR WORDS and NAMES, NOT MINE as previously stated by another poster- that I created a "derogatory label" when those are INDUSTRY RECOGNIZED TERMS)

Where is there any proof that BHRT is "reducing" their use of this type of financing- when qty-3 new deals were just inked in early 2015 and one of those 3 last month in Feb of 2015?? Not seeing it myself- no indication to me of any "reduction in use" of this type of financing? Where and when and how?

Here is a link to thee SEC itself- and they use the term "toxic" and "death spiral" to describe the very kinds of financing deals being discussed, aka "convertible debt" deals- based on "conversion formulas" and typically a "note" and a share discount to the lender of some sort.

http://www.sec.gov/answers/convertibles.htm

Quoting THEE SEC:

"Because a market price based conversion formula can lead to dramatic stock price reductions and corresponding negative effects on both the company and its shareholders, convertible security financings with market price based conversion ratios have colloquially been called "floorless", "toxic," "death spiral," and "ratchet" convertibles."

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

Bloomberg similarly uses the exact same terms- even has a graph on the left side of the written article - showing a "spiraling down share price" aka the "death spiral" scenario playing out and explained using a graphic.

LOL, quote, "I am really liking this review of the 10K looking great!

"

Well, all except that pretty much everything stated in that 10-K so called "review" is just TOTALLY INCORRECT.

I wouldn't even know where to begin - it's so full of just plain wrong information.

Personally, I just READ THE 10-K ITSELF and not some micro blogger's "review" of it. The 10-K speaks totally for itself and doesn't need any "review" IMO.

Especially when the info in the "review" is just plain wrong.

I'll pick just one line from the start of that so called "review"- and that line is 100% TOTALLY FALSE and TOTALLY INCORRECT.

Quote, "The doubling of the o/s in 2014 over 2013 is due settlement of debt and also shares being issued to the insiders. "

That statement is just 100% FALSE. The doubling of the O/S shares in 2014 was due to DILUTION primarily due to endless use of toxic debt financing, the issuing of 10's of millions of shares to pay common bills, and some issuing shares to insiders and "some" debt-to-equity swaps. But convertible debt deals made up a great portion of that massive dilution. NOT due to "settlement of debt" as claimed.

The main BHRT "debt that was settled" in 2014 was done using NO SHARES. William Beaumont hospital "discharged" (took a bad debt write down) and simply forgave BHRT the debt they owed- NO shares were involved at all. And that made up the bulk of the debt reduction in 2014 by BHRT.

Just filed 10-K, PAGE 13:

"In June 2000, the Company had entered into an agreement with William Beaumont Hospital, or WBH, pursuant to which WBH granted the Company a worldwide, exclusive, non-sublicenseable license to two U.S. method patents covering the inducement of human adult myocardial cell proliferation in vitro, or the WBH IP. The term of the agreement was for the life of the patents, which expire in 2015. The Company did not use this license in any of their technologies or made any payments to WBH other than the initial payment to acquire the license. On April 2, 2014, the Company received confirmation from WBH that it has no obligation under the patent license agreement and WBH agreed to terminate the patent license agreement pursuant to a termination letter dated March 3, 2014.

Accordingly, the Company recognized approximately $2,122,130 in settlement of debt which represents the accumulative accrual and related interest from past years under the 2000 patent license agreement."

That $2 million plus made up the bulk of all "debt reduction" by BHRT in 2014- and it didn't involve ONE SHARE of common stock changing hands.

Just ONE example of the gross inaccuracies and just plain wrong info in that so called 10-K "review".

Here is the 10-K itself in full. Just read it and forget the blogger "reviews"- especially the ones that are just plain full of wrong and incorrect information.

http://www.sec.gov/Archives/edgar/data/1388319/000114544315000378/0001145443-15-000378-index.htm

10-K amateur "blogger" 10-K "reviews"- no value to me. Most of that "review" is so poorly written- I can't even understand most of what it's even trying to say, let alone the totally wrong "claims" it's attempting to make?

Just incorrect info IMO. The 10-K speaks for itself.

Regarding use of what's known as "toxic debt" to finance high risk, cash poor penny stocks such as Bioheart (aka Magna, Asher, etc)-

Unfortunately, the Sr Mgt of these companies such as Bioheart willingly and knowingly do the "convertible debt" (floorless, toxic debt) deals knowing full well there is a high probability that it will have an extremely negative effect on the common share price and thus common shareholders. They want the cash the toxic lender has to offer and thus willingly sign on the dotted line of each deal. That's the bottom line IMO.

This Bloomberg piece on Magna, who Bioheart just used for "toxic" type financing (along with Asher, Daniel James, KBM Worldide, Fourth Man and now a latest firm called Vis Vires group, among the many they, BHRT use for on-going financing)- gives very specific examples of how the CEO's or BOD etc knew full well that these deals were "toxic" , as the SEC calls them, but they willingly take and sign for the money anyways.

If these lenders of last resort were banned- a company such as BHRT would have gone BK a long, long, long time ago IMO. As no regular lender of any type is going to loan to a asset poor, cash poor, no positive cash flow, debt laden, 3 person, extremely high risk, going concern warning company. By the time a BHRT penny firm gets to the end of the line cash sources such as the Ashers and Magnas of the world- they've already exhausted all attempts typically at "regular" or "conventional" financing, etc

The ONLY reason a toxic lender is even willing to lend to a BHRT type penny stock (or sub penny) - is that the "convertible debt" type loan is "floorless" and thus provides near perfect down-side protection to the lender. In fact- the lower the share price goes and the more desperate the company gets- most of these lenders make even more money. That's the real incredible part of the "toxic" or "death spiral" type of cash-for-shares convertible loan type product.

The Bloomberg journalistic write up and video profiling Magna explains this in great detail- how it "works" when "toxic" convertible debt is used. They, Bloomberg called these hedge fund type lending firms- the desperation loan firms or lenders of last resort to penny stocks and said they're like the "pawn shops" to the penny stock world- the last ditch effort at cash at pretty much any cost for penny firms, including wiping out the common shares in many, many cases. They even interviewed a CEO of a firm that used Magna and saw his firms stock eventually hit the 1000ths' of a penny level. He said firms like Asher and similar were still calling him willing to lend more to his penny stock firm. They didn't even care what business he was in, if they had a product or not, etc As long as the shares still traded with some decent liquidity- the "toxic" lenders would give him the cash, no questions asked pretty much.

http://www.bloomberg.com/news/articles/2015-03-12/josh-sason-made-millions-from-penny-stock-financing

It's all explained in that excellent piece of financial journalism by Bloomberg IMO. If BHRT didn't go to Magna and Asher and Daniel James and similar- just look at the last 10-K, they'd be BK already IMO. They lost a tremendous amount of money in 2014 and that's despite numerous, numerous use of these "convertible debt" lenders and loan "notes" that carry the right to be converted to common shares. W/O that cash coming in, they'd of more than likely gone BK- and the "going concern" warning from their auditor and Sr Mgt pretty much spells that out. They state that w/o "substantial, continual, additional financing" they'd end up ceasing operations, cutting head count, cancelling all business plans and/or filing BK most likely and rendering the common stock shares worthless (That's Sr Mgt's words (paraphrasing) see PAGE 27 just filed 10-K, it's all spelled out there in detail)

Thus "banning them", these "toxic" type lenders- I don't know. The company's that typically rely on this money of last resort would all go BK in short order IMO. Not that their common stock isn't eventually, often, going to decline to near worthless anyways eventually, based on the staggering dilution that takes place- reaching a BILLION or more shares typically as a stock's price goes to less than ONE CENT. And w/o the floorless "toxic" conversion features built in- then the lenders would never do the deals in the first place- as company's like BHRT are just way past too high risk to lend money to. They have no real assets, no real estate, no plant and equipment, etc which is the typical "collateral" for a more conventional loan. The common stock of firms like BHRT is so near worthless at SUB ONE CENT or the ONE CENT range and their market caps so low (BHRT about $6 million or less right now) that they can't sell stock in typical stock offerings- as no one's going to buy it in bulk unless given the tremendous share discounts such as these toxic lenders are getting (45% or more to market price).

So the only reason these lenders still touch these penny, or SUB PENNY stocks- is the down-side protection provided by the "toxic" floorless conversion formula built into these types of loan deals and the initial, up front mega steep share discounts and fairly high interest on the "note" itself- all insuring they, the toxic lender almost can't lose and in fact can make enormous amounts of profit in very short periods of time via selling and dumping the stock on the open market as fast as they get it typically.

My .009 or so cents worth.

http://www.sec.gov/answers/convertibles.htm

LOL, quote "3. A 42% decrease in year over year cash used in operating activities to $1.1 million in 2014 from $1.9 million in 2013."

Well, yeah. When a company HACKS OUT R&D spending to near ZERO, by say, oh about $500K plus- it's pretty easy to play "smoke and mirrors" and make it look like they reduced cash use.

Any "clinical trials" being funded or any R&D actually taking place? For a company that on its own web site calls itself some "medical leader in stem cell research" (paraphrasing) but- some nonsense statement like that (same on twitter, total nonsense IMO about supposed world leader in stem blah, blah whatever) but nonsense IMO since they haven't paid for, or conducted a single, large scale, FDA level trial since the 2009/2010 time frame. FIVE years or more now.

ADD BACK THE R&D MONEY THEY SPENT and then tell what their imaginary "cash decrease" was. Also, they cut head count from 4 full time and 1 part time to now only THREE full time people left. Again, DUH- they cut "cash use" supposedly.

Hey, when you do no actual business, cash use can really, really be cut- like magic.

From the just filed 10-K, PAGE 55:

"Research and Development

Research and development expenses were $66,420 in 2014, a decrease of $560,563 from research and development expenses of $626,983 in 2013. The decrease was primarily attributable to a decrease in the amount of available funds.

The timing and amount of our planned research and development expenditures is dependent on our ability to obtain additional financing."

Wham-bam, like magic. Look at that. R&D CUT by $560,563. And the ole "cash use" managed to decrease- SHAZAM.

If they were to even "try" and make a micro down payment on a real, FDA level Phase 3 trial- their cash use is going to explode through the roof, not be "reduced".

Take that "PR" claim of the ole "cash use reduced" and add back in R&D spending and see how much that ole cash would have been "reduced" supposedly.

Quote from the PR:

"3. A 42% decrease in year over year cash used in operating activities to $1.1 million in 2014 from $1.9 million in 2013."

OK, add back the $560,563 they hacked from their R&D spending- a key supposedly to their future and the business's ability to survive and thrive per their own 10-K statements.

Actual cash use would have been $1.1 million + $560K = $1.6 million on the low side, back to nearly the 2013 level of $1.9 million. And 2013 is higher as they spent even more on R&D for the entire yr.

It's just accounting gimmicks IMO. Of course I can show I "cut cash" use- if I hack and cut-out a key part of my budget. A part (R&D) that according to my own SEC filings and web site and all the rest- is a supposed back-bone and key part of my business. Except in the case of ole Bioheart now, it's really not as THEY'RE SIMPLY NOT FUNDING ANY R&D anymore for all intents and purposes.

My .009 cents worth. Easy and clear as a bell to me.

LOL quote, "I don't get what you're trying to say... But EVERYTHING LOOKS GOOD TO ME. REVENUES UP, DEBT DOWN, BUSINESS GROWING."

Too funny.

Real situation from reading the 10-K versus the one liners of a carefully "crafted" and selectively worded (IMO) "PR"- for example claiming cash use was greatly reduced but FAILING to say they hacked the R&D spending by over $500K. DUH, they used less cash, no kidding- but what actual "business" did they do or even conduct? They sure ain't running any clinical trials which is the "supposed" business they claim to be in.

Reality:

LOSS FROM OPERATIONS biggest since as far back as 2010. "revenues up"?? So what? What difference did that make? None. Top line "revenues" make no difference when one's EXPENSES grow even faster- as in doubling in a one yr period, despite R&D being hacked to near nothing and employee head count being cut, etc. "revenues" don't make a business successful or not- not when it loses money on those revenues.

ONE TIME debt reduction via a debt being forgiven (discharged) by an old creditor- not because you generated any cash as a business to be able to actually pay down debts. Just since the last qtr the current liabilities is already back on the rise again- gaining $775K in just the last 3 months. They won't get that one-time debt reduction gain again. It's a one freebie- won't be repeated again.

MASSIVE share dilution- as in staggering amounts, as in more than doubling your outstanding shares and the resulting share price crushing effect playing out in real time right now as the stock goes well into SUB ONE CENT territory and is at a 52 week low despite all the imaginary "good news" spin doctoring. Stock touched within a micro cent of the all, all, all time low very recently

A continual, un-ending use of toxic, convertible debt financing (3 more toxic, convertible debt deals just in Jan/Feb 2015 alone for survival cash)- right up until just one month ago in February and also now tapping the dilutive Magna "credit line"- pouring out more shares like water into the magic price crushing dilution machine. There's gonna be so many 10's of millions, if not 100 million or more shares hitting the sell-side of the free trading market in the next 6 months or so, I don't see how this will ever come up for a breather. The buying demand would now have to be astronomical to off-set the dilution houses who IMO, for all intents and purposes now have 100% control over the common stock share price

Ending the fiscal year CASH BROKE like always- with a whopping $36K total cash left on-hand for a company now reduced to THREE total "employees" per their own 10-K filing, a head count reduction of 1 full time and 1 part time compared to just the last 10-Q filing, but supposedly going to "conduct" all this supposed business and sales and blah, blah, blah same old variations on the 5 plus yr old "story" IMO.

Facing a $2 million plus lawsuit for alleged failure to pay back a creditor- who's original debt principal of $1.5 MILLION is sitting right on the duly filed 10-K, right where the lawsuit alleges it to be. "subordinated debt, related party" of $1.5 million. Legal costs stated in 10-K as being part of the reason their "general/admin" expenses exploded up so high- in addition to "salaries" of course.

Yeah, heck- what could possibly be wrong here? $36K total cash left to their name and THREE total people left, LOL !! The market's just all over it? Look at all the buyers just rushing to get in on it at SUB ONE CENT? CLOSED RED today- despite the old "PR" and the 10-K and all the rest? SUB ONE CENT, wow? Looking fantastic. Right on. 52 week low and just lingering off the all, all time lows. Just rocking n rolling- sure. Looking great.

"net loss" is NOT LOSS FROM OPERATIONS.

That PR line about "reduced net loss" blah, blah is only due primarily to a ONE-TIME debt being "forgiven" (aka written off) by a past creditor. When that ONE-TIME debt gets forgiven it gets moved from the "liabilities" side of the ledger to being a "gain" and thus is booked as a gain now, a one-time gain. That won't be there next time around- and in fact, if one looks from just the last 10-Q (Q-3) to this 10-K filing, a 3 month period, their "current liabilities" actually INCREASED back up by about $750K in just that 3 month period. A rapid increase getting added back to their obligations owed. (Back up to $11 mil or so, going the wrong direction again)

Back-out that ONE-TIME GAIN, and their "net loss" would have been larger than in 2013. It's as simple as that. It's just accounting gimmicks- it didn't affect their desperate cash situation in the slightest as they did not actually pay back the "forgiven" debt using any cash of their own. Thus their "true loss" situation reflecting that their expenses are far exceeding any ability to self-generate cash is much better indicated via looking at the LOSS FROM OPERATIONS (which would not include a one time gain on something like settlement of debt, or interest, etc) - it's much more reflective of their true operational losses, and THAT number was the largest in 5 yrs, going back through every 10-K filing since 2010.

There it is, right on their STATEMENT OF OPERATIONS.

NET LOSS FROM OPERATIONS:

2010 (3,266,030)

2011 (2,665,884)

2012 (2,534,843)

2013 (2,841,750)

2014 (3,529,452)

Most recent 10-K, just filed- their largest operational LOSS checking all 10-K filings back to 2010 when Tomas took over as CEO.

LOL, the ole PR - what a surprise. CLOSED SOLID RED.

Bid .0088/ Ask .009 (dropped the Ask, looks like PR isn't going over too well IMO) Trying to "Paint the tape" with few shares at .0099 at end of day, still SUB ONE CENT, big a whoop, it still couldn't hold even .0099

0.0088 / 0.009 (129498 x 278000)

The rose colored ole "PR" IMO kinda-sorta LEFT OUT THE "little" tid bits about the LARGEST LOSS FORM OPERATIONS since before 2010, biggest operational loss since even 2010.

Their LARGEST LOSS FROM OPERATIONS in FIVE YEARS:

From their 10-K filings going back 5 yrs to 2010

NET LOSS FROM OPERATIONS (parenthesis is a LOSS, this yr was the LARGEST LOSS IN THE PAST 5 YEARS OF OPERATIONS, despite enormous amounts of toxic convertible debt deals, Magna financing and the "revenues"- they out-spent it all to take their largest LOSS FROM OPERATIONS going all the way back to 2010)

NET LOSS FROM OPERATIONS:

2010 (3,266,030)

2011 (2,665,884)

2012 (2,534,843)

2013 (2,841,750)

2014 (3,529,452)

Most recent 10-K, just filed- their largest operational LOSS checking all 10-K filings back to 2010 when Tomas took over as CEO.

That $3.5 MILLION NET LOSS FROM OPERATIONS is bigger than any loss from operations going back through every 10-K to year 2010.

The "PR" "net loss" claim is ONLY because of a ONE TIME settlement on a debt they had forgiven, but did not pay back. It fails to show their increased LOSS FROM OPERATIONS, which is more indicative IMO of actual lack of internal cash being generated, aka a REAL LOSS, not a paper reduction from a one-time "debt forgiveness". Big, big difference.

Their expenses have exploded- outpacing any cash coming in from continual dilutive toxic financing deals or bottom line "revenues" after cost of sales. They finished the year, 2014 with only $36K total cash left on-hand, one of their worst years since 2010. They are in horrible financial condition IMO and their auditor's own "GOING CONCERN WARNING" states just that IMO.

BHRT's "general and admin" expense line more than DOUBLED in the past 1 yr. (to $4,669,432 for 2014, PAGE F-4 of 10-K, for a company now of just THREE PEOPLE per their own 10-K verbiage) And that's despite spending almost nothing on R&D, conducting no major clinical trials such as an FDA Phase 3 or similar, and reducing their headcount to just THREE employees left according to the 10-K filing itself.

Definition of NET LOSS FROM OPERATIONS or "operational losses" from Investopedia:

"DEFINITION OF 'OPERATING LOSS - OL'

The net loss recorded as a result of a company's unprofitable operation, considering only the company's operating income versus its operating expenditures. An operating loss does not consider the effects of interest income, interest expense or taxes, but in some cases includes depreciation expense. A company which consistently generates operating losses will require outside financing in order to avoid bankruptcy."

Most recent 10-K filing PAGE 56:

"At December 31, 2014, we had cash and cash equivalents totaling $36,674; our working capital deficit as of such date was $10,957,443. Our independent registered public accounting firm has issued its report dated March 16th, 2015 in connection with the audit of our financial statements as of December 31, 2014 that included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern."

Most recent 10-K filing PAGE 27:

"Our independent registered public accounting firm has expressed substantial doubt about our ability to continue as a going concern.

Our independent registered public accounting firm issued its report dated March 16th, 2015 in connection with the audit of our financial statements as of December 31, 2014, which included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern. In addition, our note to our financial statements for the year ended December 31, 2014 included an explanatory paragraph describing the existence of conditions that raise substantial doubt about our ability to continue as a going concern. If we are not able to continue as a going concern, it is likely that holders of our common stock will lose all of their investment. Our financial statements do not include any adjustments that might result from the outcome of this uncertainty."

Funny how that ole PR just manages to leave out those choice little morsels of FACTS, eh? The ole "selective" PR IMO. No surprise though to me. None.

Any "PR" about ending a fiscal yr with $36 TOTAL CASH ON-HAND left in their bank account- less than in 2013? LOL. Or how bout any PR about using qty-3, THREE MORE toxic debt, convertible financing deals as recent as one month or so ago- for pittances of survival cash like $38K or $25K, etc. PAGE F-34 of the just filed 10-K: (oops, MISSED THAT IN THE OLE "PR, eh?)

"Subsequent financing

On January 7, 2015, the Company entered into a Securities Purchase Agreement with KBM Worldwide, Inc. (“KBM”), for the sale of an 8% convertible note in the principal amount of $38,000 (the “Note”).