News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

The GidDy uP Kid

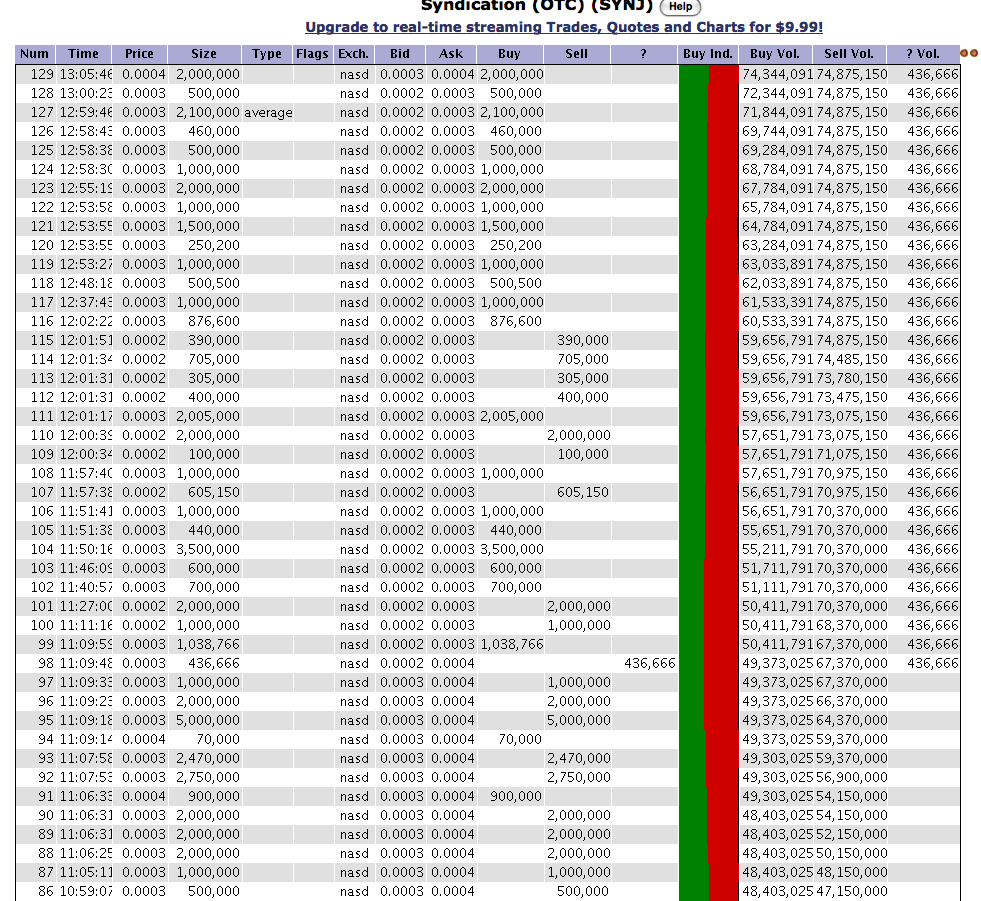

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

yes he does!

yep mine was just mirrored I believe.

what does that level 2 look like?

Thomas Boone Pickens, Jr. (T. Boone) is an American businessman and investor who is the head of private equity firm BP Capital Management. During the 1980's, Pickens helped Mesa Petroleum became one of the first independent oil companies to use mergers and acquisitions to promote growth rather than just exploration. Pickens' most notable takeover bid was for Gulf Oil during the 80's, landing him on the cover of Time magazine.

T. Boone successfully predicted that crude oil would cross $100 per barrel in 2008. His oil predections are market moving.

Syndication Inc. CEO, Sorrentino is Nominated as Co-Leader of Maryland's Congressional 6th District for T. Boone Pickens New Energy Program

"My relationship with the program allows me to strategically place Syndication at the crossroads of a massive new technological revolution. A revolution born from necessity and obligation and laden with opportunity," said Syndication CEO Sorrentino. Pickens reports that in the month of January 2009, US oil imports amounted to 67.4% or 408.7 million barrels representing a $17 billion dollar transfer of America's wealth to foreign Countries. The solution to this problem lies within green energy technology. The relationship with the Pickens Energy Program has yielded a multitude of opportunities both with companies and individuals that currently have extensive experience, background and involvement it the green energy sector. "A few of the many proposals currently being evaluated by the BOD are more than just exciting," said Sorrentino, the CEO of Syndication Inc. The Company hinted that it will release information on the developments of its new energy division in due time.

You are correct, VERY BIG!

I agree.

I was thinking the same thing.

Lets break it! LOL

HOLY #$#%# that was some MAJOR EOD buying!

did I just see over a 10 mil block buy?

yep the accumulation/dis. keeps climbing.

yep notice as soon as soon as the buys caught up with the flipper sells it upticked.

welcome to the million block buy club! lol

If anyone missed this post/news release its worth a reading. It is a good one IMO.

http://investorshub.advfn.com/boards/read_msg.aspx?message_id=35898036

nope I was buying 4s earlier too.... LOL

ask at 4s now... hope everyone took advantage and got the 3sss

LOL prolly me!

SYNJ looking good here!

a lot of accumulation has been occurring.

CINT is ready for a breakout!

yes, I agree. CINT accum. has been occuring

moving now!

Shortable Stocks

Reg-SHO Restricted Stocks

The following stocks are listed on the Reg-SHO watch list. Reg-SHO is a US regulation governing stock shortability. In general, Reg-SHO restricted stocks are not permitted for shorting. However, IB may allow Reg-SHO stocks to be shorted when inventory conditions permit. The main shortable list defines the actual availability.

Please see following web page from the NYSE for additional information: http://www.nyse.com/threshold/ regarding Reg SHO and restricted stocks.

Key Search:

Last updated:Tue, 24.Feb.09 07:02EST

Symbol Currency Long Name

CINT USD Crystal International Travel Group Inc Check Availability

Symbol: CINT

Availability: 0

Exchanges: NITE, PINK

http://individuals.interactivebrokers.com/en/trading/ViewShortableStocks.php?key=cint&cntry=regSHO&tag=Reg+SHO&ib_entity=llc&ln=

agree on PFEH

I agree.

Thanks, I think CINT has a good solid foundation.

CINT is definitely making some good updates. New website http://www.purchaseifares.com/ for itellifares fully working on all levels now (had some glitches before for some users)

Plus CFO magazine feature on Intellifares http://www.cfo.com/whitepapers/index.cfm/download/11525920

CINT is a Monster in the working!

The table didnt copy well, but one can see the full article from the business intelligence center here http://www.cfo.com/whitepapers/index.cfm/download/11525920

(I had to fill out a form to get access to the white paper; one may have to also)

By Peter Gallic, Director, Intellifares, LTD.

A case for cost control techniques for the Airline Industry: Airline ticket purchasing can be greatly enhanced by hedging purchases over a five year period thereby converting future airlines ticket purchases to cash today allowing carriers to better manage cash flow, investment activities and forward planning processes.

The airline industry is being buffeted today by the stress of rising fuel prices and falling dollar. While bifurcating cost centers on the actual ticket, such that fuel surcharges are separated from the base fare, has ameliorated the strain to a degree, it has become overwhelmingly evident that the discussion of forecasting methodologies and price prediction in combination with a fresh look at yield management disciplines is warranted.

Clearly, economies run in multiyear cycles that drive up or down variation in fare cost components, such that the industry faces a recurring problem; pricing in the short term is perennially at odds against future costs, both positively and negatively. Imbalances in pricing and cost timing result in short term pricing decisions that, when implemented, are not reflective of current environment. The industry’s dilemma is one of selling something without having control over the ultimate cost of goods sold.

In reality the airlines will not be able to control or predict with any accuracy neither the price of oil, the exchange rate for the dollar or a host of other variables that make up the cost factors in pricing out an airline seat. And even with proper hedging mechanisms in place, ranging from fuel cost hedging paired with fuel surcharges received to structural upgrades with more efficient fleet components, current news suggests that more work needs to be done. It is too early to tell whether the most recent moves to contract capacity will have any effect, especially when demand changes.

Additionally, the yield management practice of offering dozens of fares for a particular flight or flights, while seeming to address supply and demand and the desire to fill a particular flight, in susceptible to the vagaries of this short term price/long term cost scenario. This writer posits that the only solution is to drop the current adopted paradigm and adopt a new set of rules for revenue management that take in to account more of the present day factors affecting costs, and the commoditization of airline fares which has accelerated the obsolescence of the yield management state of the art. The science and art of yield management is extremely complex, as it amalgamates multiple business strategies, including revenue management, marketing, sales, capacity utilization both

from an income statement and investor relations perspective, et. al. As such this article will address revenue management from a pure price, cash flow and cost perspective here, and leave the whole art part of the yield conversation (marketing, capacity utilization, supply and demand perceptions vs. reality, customer loyalty generation, etc.) to another article.

The first step is to identify the problems at hand, analyze them, then to decide what are the best optimization mechanisms, either from a cost, revenue or cash flow perspective. Currently the biggest problems are rising fuel costs, exchange rate volatility and revenue and cost synchronization over time.

By far the greatest problem is the issue of matching cash revenue and cost. If just this one problem was addressed the benefits to the industry would be enormous. Estimates for the savings are in the hundreds of millions. What the industry would benefit from is a longer term revenue model.

It is my contention that airlines can lock in customers for multiyear fare contracts to the bulk of customers who travel in predictable patterns (both frequency and route), and provide a viable market that allows for the transference of those contracts. Benefit would come in the form of a floor on revenue with the ability to profit from market fluctuation by either buying back capacity or selling capacity. Basically risk would shift in a small portion of the market to consumers. A the same time by locking in revenue on a longer term basis the airlines would be able to convert those future revenues to cash and use different cash management techniques to effectively protect themselves from market cycles.

IntellifaresTM was designed as a possible solution. We carefully analyzed the overall travel market and identified groups of predictable pattern travelers, travelers that travel on regular basis over multi year periods from either a route or seasonality basis, or both. Some obvious examples are timeshare owners. Others include family members who live away from parents who travel on holidays or significant dates (i.e. birthdays), or families making regular excursions to a second home. In another example we looked at cruises. Here the paradigm is a little different, we isolated an event that has a schedule and looked at the passengers traveling into that activity. We then identified the seller for the tickets on behalf of that entity as a periodic traveler. We did a survey on these groups to identify key motivators and gauge perception to program savings. One survey result was that consumers preferred five year programs over longer programs. Also consumers did not trust that airlines would keep multi year pricing but trusted the airlines more if money center banks were involved in the process.

Once we isolated the multiyear travel grouping we analyzed the cost associated with airline operations and built a model to forecast ticket prices over a multi year period. We assumed for this exercise a 2.7% increase on a yearly basis for cost based on the ten year trend reported by the DOT. This was consistent with trends over the last ten years. We also discounted prices to allow for savings in customer acquisition, marketing and servicing costs, and the elimination of some of the negative revenue inputs of the current

yield management practice. We used these elements to form a price today for the following five years of travel.

This also has other benefits for the airline market. By removing inventory from online retailers you reduce supply in the market and provide positive pressure on prices. The law of averages lets you dollar cost average the near term fluctuation in the market over extended periods of time giving you the benefit when oil costs drop and providing investment cushion to offset fuel increases (also acknowledging the availability of the continuation of fuel surcharges separate from fare bases during acute spikes.)

Net result is that by establishing essentially a five year flat rate market, airlines are able to more effectively deal with expenses. By selling, what are essentially, five year ticket vouchers consumers and businesses are able to develop a new airline business that protects the ability of an airline to fly at the same time give flyers price advantages.

In the process of modeling the price increases over a five-year period and adding in the following years programs we were able to increase the actual revenue received by the airlines at a premium to consumer realized price increases.

The chart assume an original dataset of (DS) based on a $100 fare flight. ( This was a $100 base flight increased by 2.7% a year for five years.) Again this is for illustration. Our model calculates yearly fare increase of 2.7%. The IFARE price column shows where we would price five years of airfare based on the 2.7% increase. The Perceived Value Column is what the pricing would equate to a consumer for each of five tickets. In year 2009 the Ifare would be $532.84 or $106.57 a year for five years. The 2010 program would raise this to $548.83 or $109.77 a year for five years.

The Cost allocation table represents the money allocated to purchase tickets in each period. The average is the average of all tickets in that year as each Intellifares overlaps period with others. For purposes of illustration we have given each period equal weight

Intellifares

Perceived Consumer Value

Program Year

Route

IFARE Price

Cost Allocation Table

2008

2009

2010

2011

2012

$ 106.57

2009

EWR-FLL

$532.84

$ 113.49

$ 120.87

$ 128.73

$ 137.10

$ 146.01

$ 109.77

2010

EWR-FLL

$548.83

$ 116.90

$ 124.50

$ 132.59

$ 141.21

$ 113.06

2011

EWR-FLL

$565.29

$ 120.41

$ 128.23

$ 136.57

$ 116.45

2012

EWR-FLL

$582.25

$ 124.02

$ 132.08

USD

113.49

118.88

124.54

130.48

138.96

(the number of tickets sold in each period equals 1). So while the consumer locked in a price in 2009 for $106.57, this would yield $118.88 for the purchase of the ticket that year.

The conclusion is that while the perceived increase to consumer for fares is 3% a year, this increase results in close to a 5% annual increase in funds available to purchase tickets after a 7% first year premium.

As CFO’s taking a new approach to the travel budget by making a longer term plan enables us to control costs. Using other financial tools and borrowing techniques from other industries allows us to gain control of an increasingly uncontrollable aspect of our budgets. In analyzing the problem we need to address areas over which we can exert control and maximize those efficiencies thereby offsetting cost fluctuations. By extending the time period we can assume a clearer strategy.

We need to reformulate our strategy on travel cost control to take into account the ever changing world. Airlines must do the same. Only by revisiting our base assumptions and utilizing techniques associated with other industries will we be able to overcome the problems we face today.

Comments can be sent to Pdgallic@gmail.com

we'll have to see what transpires; see what actually happens....

This was before the recent filings. One can see the insider shares were acquired in "penny land" As some have pointed out before, the %10 in change of ownership "probably" changed because the OS increased. IMO they are reporting this because they are coming out with some updates in the near term, and this is a good first step. NO I dont think they were selling recently because of the price where they were acquired and the current PPS exchange rate would not be worth it IMO. If one looks back at the PPS around that time in July of 07, one can see that Dugan bought at the last highest PPS of the stock. It appears that the PPS has been naked shorted to the current levels (the recent adding to the REG SHO list helps confirm this; not the first time it has been on the list)and has been affected by the overall market conditions (like other stocks). Updates/company news will greatly turnaround the PPS and these current low PPS levels will be gone as well as the naked shorting IMO.

Dugan Peter A Director10% Owner 7,234,999

STEFANSKY DAVID Director 1,139,981

ROSENBLUM RICHARD Director 1,119,962

BALBIRNIE BRIAN R Chief Financial Officer 3,500,000

LLOYD MARK President 376,637

Cohn Hank Director

Busso-Campana Fabrizzio PierVincenzo C.E.O/President 1,155,000

Gallic Peter D Director10% Owner 1,155,000

SALERNO FRANK Director 350,000

Dugan Peter A Common Stock 07/25/2007 100,000 Acquired $0.04 $3,850.00

Dugan Peter A Common Stock 07/19/2007 200,000 Acquired $0.03 $6,720.00

Dugan Peter A Common Stock 07/23/2007 200,000 Acquired $0.03 $6,600.00

Dugan Peter A Common Stock 04/11/2007 50,000 Acquired $0.05 $2,475.00

Dugan Peter A Common Stock 04/04/2007 130,000 Acquired $0.04 $4,706.00

Dugan Peter A Common Stock 04/04/2007 125,000 Acquired $0.04 $5,000.00

Dugan Peter A Common Stock 04/11/2007 50,000 Acquired $0.04 $2,210.00

Dugan Peter A Common Stock 04/11/2007 50,000 Acquired $0.05 $2,450.00

Dugan Peter A Common Stock 11/29/2006 250,000 Acquired $0.08 $19,550.00

Dugan Peter A Common Stock 12/01/2006 100,000 Acquired $0.12 $12,080.00

LLOYD MARK Common Stock 08/23/2005 346,155 Acquired $0.00 $0.00

STEFANSKY DAVID Common Stock 06/06/2005 100,000 Acquired $0.00 $0.00

ROSENBLUM RICHARD Common Stock 06/06/2005 1,000,000 Acquired $0.00 $0.00

BUYINS.NET: CINT Has Been Added To Naked Short List Today

Feb 18, 2009 (M2 PRESSWIRE via COMTEX) -- BUYINS.NET, www.buyins.net, announced today that these select companies have been added to the NASDAQ, AMEX and NYSE naked short threshold list: Crystal International Travel Group, Inc. (OTC: CINT). For a complete list of companies on the naked short list please visit our web site. To find the SqueezeTrigger Price before a short squeeze starts in any stock, go to www.buyins.net.

Crystal International Travel Group, Inc. (OTC: CINT) operates as a multi-asset travel company. The company offers products and services to address price stability in the travel industry with a focus on higher income, frequent, leisure travelers. Crystal offers IntelliFares, a service that provides five years of air travel at a fixed price. The IntelliFares flat pricing model enables consumers to engage in multi-year marketing programs with travel product retailers. The company intends to distribute its product through traditional travel supplier networks, including airlines, online and off line travel agencies, cruise lines, time share developers, and sellers. Additionally, Crystal owns and operates a travel agency business. The company is based in Morristown, New Jersey. With 41.58 million shares outstanding and an undisclosed short position, there is a failure to deliver in shares of CINT. According to quarterly data provided by the SEC, there were still 4,088,966 shares of CINT that were failing-to-deliver as of November 21, 2007.

PFEH

---------UPLISTING AND MERGER PLAY----------

-- 415M O/S SEEKING ACQUISITION TARGETS

-- NEWS ANTICIPATED THIS MONTH ON NEW VENTURES PER NOV'08 PR

PFEH is a good one.