News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

santafe2

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

I'm afraid the 1:15 split and the requirement to raise additional millions did not inspire confidence. I bought this as a speculative stock @ $10 and sold at a loss of a few dollars a share. Now it's down to ~15 cents a share pre-split. I don't see anything investible at this point. Too bad they didn't know how to make rockets they could deploy in space. It was a good idea three years ago.

Retail sales were up .6%. Most of that was in higher gasoline prices but none-the-less, consumers are still spending. I still think this will begin to change when Q4 numbers are coming out.

I think Romney's idea for a 3rd party run may ensure a Trump win as he will only siphon off reasonable republicans and conservative democrats.

Here's more background on the planning for the January 6 insurrection. If one has any doubt this was a well planned effort to take over the government of the US, read the following:

Romney knew Jan6 what was coming and asked McConnell to ensure proper defensive measures were in place.

Angus King had warned Romney on January 2nd that the Pentagon had informed him Trump supporters planed to take over the Capitol building.

Chris Miller, the acting Secretary of Defense, wrote a memo to the DC National Guard on January 4th ordering:

* You may not issue weapons, ammunition, bayonets, batons, ballistic protection equipment or body armor.

* You may not physically interact with Trump’s protestors.

* You may not deploy any riot control agents.

* You may not share equipment with law enforcement agencies.

* You are not authorized to use intelligence, surveillance or reconnaissance assets to assist the capitol police.

* You are not allowed to deploy helicopters.

* You are not to employ searches, seizures or other law enforcement activities.

* You are not to seek support from any non-DC national guard units.

It's like the Taliban was working from inside the government.

I'm sure the WSJ editorial board got some input on this goofy article but sweet capitalistic Jesus, these people lived during the easiest period in history that a white person of average intelligence and meandering thrift could accumulate a retirement fund. Apology to Nick, This story is reported from Naples.

Why More Baby Boomers Are Sliding Into Homelessness

The aging of America means more old people on fixed incomes are overwhelmed by the high cost of housing and other financial shocks; ‘not seen since the Great Depression’

NAPLES, Fla.—Judy Schroeder was living a stable retirement in this affluent Florida enclave. Then her apartment building was sold to a new owner during the pandemic and she lost her part-time job working at a family-owned liquor store.

What followed was a swift descent into homelessness.

Faced with a rent increase of more than $500 a month, Schroeder, who had little savings and was living month-to-month on Social Security, moved out and started couch surfing with friends and acquaintances. She called hundreds of other landlords in Naples and southwest Florida but failed to find anything more affordable. She applied for a low-income housing voucher. She began eyeing her 2004 Pontiac Grand Am as a last resort shelter.

“I never thought, at 71 years old, that I would be in this position,” she said.

Baby boomers, who transformed society in so many ways, are now having a dramatic effect on homelessness. Higher numbers of elderly living on the street or in shelters add complications and expenses for hospitals and other crisis services. The humanitarian problem is becoming a public-policy crisis, paid for by taxpayers.

Aged people across the U.S. are homeless in growing numbers in part because the supersize baby boomer generation, which since the 1980s has contributed large numbers to the homeless population, is now old. But other factors have made elderly people increasingly vulnerable to homelessness, and the vast numbers of boomers are feeding the surge.

Here's my less than sympathetic response: You have no family that cares about you? You expected the government to support you because you wasted your life doing what? I've zero sympathy for anyone who's Anglo and grew up in our generation and did not build a retirement nest egg. Of course, all of these whinners are white. The WSJ may be pushing their editorial Idiocracy into the news department to help Trump get reelected. We should watch for more of this nonsense over the next year.

The new Investorhub interface is live tonight. It seems improved but I'll just have to give it some time before I comment further.

The iPhone 15 is out and the big news according to the WSJ is that they've finally supplied the phone with a standard USB-C port. I think I can live with the proprietary port in my 14 for a few years. I suspect many will hit the snooze alarm on this one. Not a knock on AAPL, if this one doesn't sell well enough they'll just bump a few features up into the 16. Wired chimed is as well;

The biggest change is the charging port.

Not that I'm an authority but I've been planning for a mild recession in Q1 or Q2 next year for quite some time now. I don't see a near term detonator. What is the immediate existential threat? We'll see.

Let me see if I've got Trump's big idea regarding Mexico about right: I was thinking of parking my truck across my neighbor's driveway entry because they don't keep their lawn cut to my satisfaction. I'm sure that will go well..:).

All four of us are on our Verizon plan so we buy an iPhone every year. We have an 11-14. The 11 is a bit old but not that much different than the 14. I was the last to come into the AAPL fold as I always liked my Samsung Galaxy 8S Plus. It was the first larger format phone I'd bought and did everything I wanted but it was time to upgrade and Samsung has done almost everything wrong with their newer phones. The 14 is excellent. I suspect we're iPhone users for the rest of this decade. Maybe longer.

I'm Out! Quiet Quitting This Market

Kim Jong Un’s Bulletproof Train Spotted as He Travels to Russia

Some thoughts on the US housing market. As the summer market fades both lenders and builders are discounting interest rates, usually for an abbreviated time frame to keep business moving. There's more inventory than a year ago but not that much. However loan interest rates continue to move up. It's now 7.6% according to bankrate.com. I think that's a bit high for a well qualified buyer but it's certainly over 7%. Housing prices are moderating in the hottest markets but flat in most others as inventory remains low. I think it will be a tough winter for housing. Not 2008 housing crash tough but less than excellent. We keep looking here in Annapolis but we're not buying as it feels too early and who can complain about making more than 5% to wait. As some will know, 5% bond interest is the tipping point. Stock market investing is less interesting, home mortgages 2% higher are less interesting and, in general, saving instead of spending is more interesting.

It's all Tesla and Twinkies this morning..:)

As you noted, I don't think Trump sees himself as a fascist, but he is a fascist leader. From Wiki:

Fascism is a far-right, authoritarian, ultranationalist political ideology and movement characterized by a dictatorial leader, centralized autocracy, militarism, forcible suppression of opposition, belief in a natural social hierarchy, subordination of individual interests for the perceived good of the nation and race, and strong regimentation of society and the economy.

This will prove to be a very expensive fad for most investors.

I would refer to the Chinese government as a Leninist-Maoist economy. Karl Marx envisioned a socialist economy owned directly by the workers who produced the products in the economy. Marx was a true socialist while Lenin and Mao were communist-fascists. As I view Trump, at his core, he's either a modern communist-fascist like Xi or more likely, just a criminal-fascist like Putin.

And a 20-year chart of US oil production, reported in thousands of barrels. While this is not the only reason the US dollar has been strong for the last 15 years, it's certainly a strong contributing factor. Data is from EIA and part of their more than 100 year history of US oil production, first reported in January of 1920 at just over 1MM barrels.

A chart for those who think the US dollar is becoming weak. 20 year chart below.

A simple solution is to FDIC insure non-interest bearing accounts. Every business has them. Even a small business can easily have several million dollars of money in the bank they will owe vendors at the end of the month. This would solve much of the problem.

Between DeSantis and Charter, nothing is going well for the mouse. At least they're not DISH which is down 55% this year.

I have my suspicions...

Tried to buy some stocks this afternoon but Schwab says someone else is buying all of it, then selling it, then buying it back again...:).

Maybe tomorrow.

Let's try to analyze this chart to see if we think we're seeing a repeat of the same pattern. I'm not convinced as I see the following issues:

A: In instance 1&2 the fall in openings is reactionary and occurs during and after a recession.

B: In instance 3 the fall is proactive. It's before COVID or the recession. The 2nd half is COVID, the economy closing.

C: In instance 4 the fall is proactive. So far only taking us back to a normal rate of job openings.

I'm not saying I think we will not see a recession, just that I don't think this chart makes the case that a sharp decline in openings will lead to a major? recession. One gets the sense that the author is correlating the two phenomena.

Mr. Rosenthal may be confusing job creation with job recovery. The specialty of the modern Republican party is causing or deepening recessions while giving the very wealthy tax breaks. When Democrats come back into power these jobs are recovered as often as created. This idea of job "recovery" comes from the Republican led House Budget Committee so it must be right..:). Of course they forget to tell us why the jobs had to be "recovered".

Banning new installations of natural gas started with Berkeley, (of course it did), and is spreading across the country in states without a majority GOP legislature. In Maryland, Montgomery County, just outside DC has banned gas stoves in new buildings beginning in 2027. DC's ban begins in 2026. I'm not sure how burning natural gas and coal to create electricity to heat your stove makes sense but I'm sure the lobbyists have nice slides that show how it's the only way to go. This from the WSJ:

The sale comes as lawmakers and regulators across the U.S. debate the future of natural gas and more towns and cities look to reduce its use in homes and businesses. In response, utilities are working to determine how to modify, repurpose or sell their natural-gas delivery networks, which may risk becoming stranded assets, or facilities that retire before they pay for themselves.

Below is a 30 day chart of the SPX. It was positive yesterday when the close was above the Aug. 15 close but obviously that didn't hold and we're in a new channel. I'm watching 4,415 as the next support.

The number of days predicted until the next recession are not as interesting as the fact that inverted yield curves do often lead to recession. They say another 275 days, I'll take the under. From Market Watch:

Where is this long-anticipated recession? Analysts at Bespoke think the next economic pullback still could be about 275 days away, or starting roughly in early June 2024, according to data as of Wednesday.

That’s because past recessions took an average 589 days to materialize after the 10-year and 3-month yield curve first inverted, based on data since the early 1960s.

Hey, let's pass some laws that will only bankrupt Freddie and Fannie during a black swan event. From Wiki:

(in 1992)...For the first time, the GSEs were required to meet "affordable housing goals" set annually by the Department of Housing and Urban Development (HUD) and approved by Congress. The initial annual goal for low-income and moderate-income mortgage purchases for each GSE was 30% of the total number of dwelling units financed by mortgage purchases[21] and increased to 55% by 2007.

In 1999, Fannie Mae came under pressure from the Clinton administration to expand mortgage loans to low and moderate income borrowers by increasing the ratios of their loan portfolios in distressed inner city areas designated in the Community Reinvestment Act (CRA) of 1977.[22]

In 1999, The New York Times reported that with the corporation's move towards the subprime market "Fannie Mae is taking on significantly more risk, which may not pose any difficulties during flush economic times. But the government-subsidized corporation may run into trouble in an economic downturn, prompting a government rescue similar to that of the savings and loan industry in the 1980s

Over the next couple of years we may begin using this acronym regularly: CMBS. Commercial mortgage backed securities. 2008 redo, fun stuff.

As Jerry Seinfeld asked: Is this anything? I would suggest that one should not ignore this evidence without taking the time to build a contrary case and investment strategy. I'm somewhat agnostic as I'm mostly invested in fixed income but none of this looks excellent. From the WSJ which can be classically useless. It reminds me of the famous Meryl Streep line from Death Becomes Her: Now a warning?

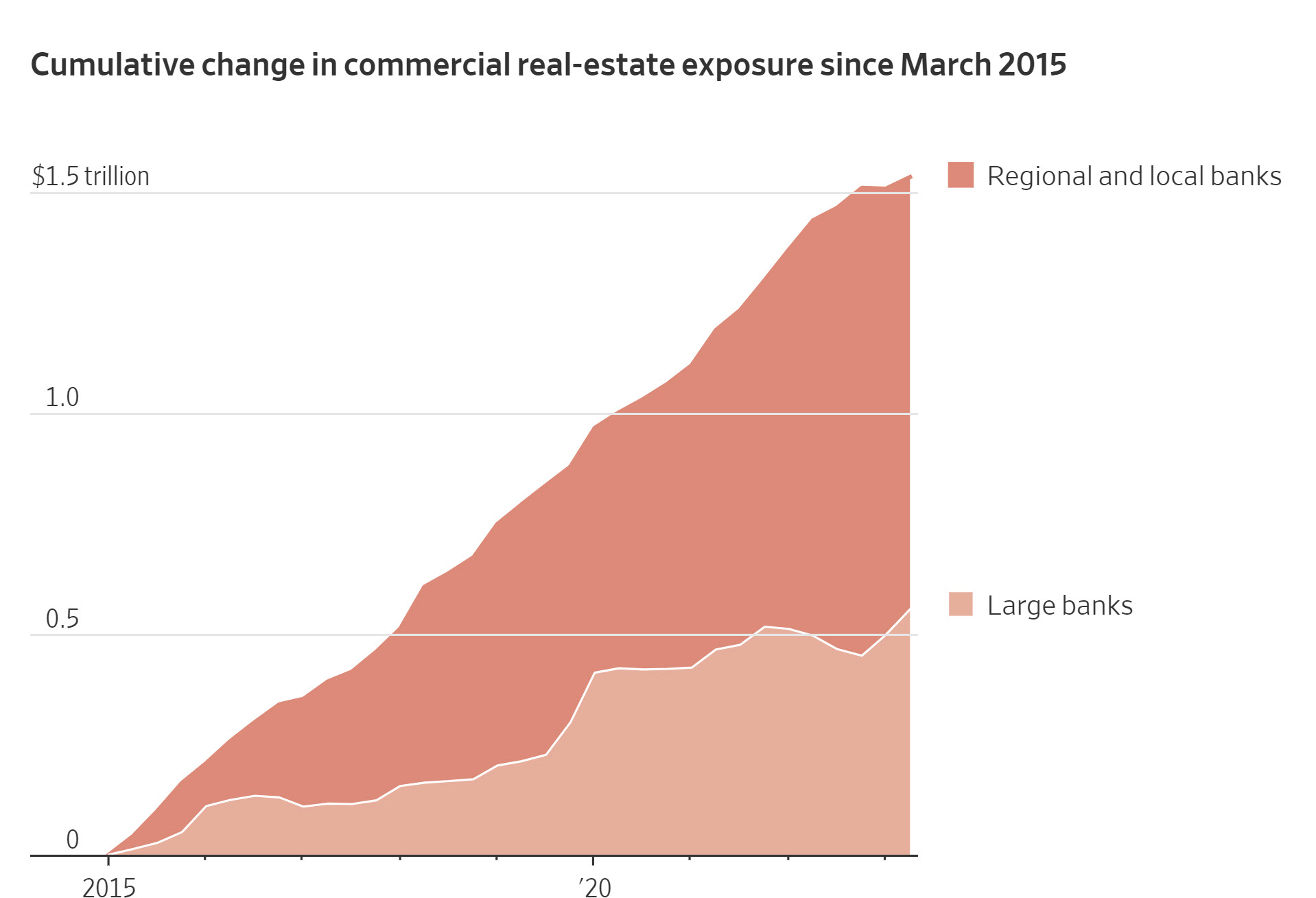

Real-Estate Doom Loop Threatens America’s Banks

Regional banks loaded up on commercial real-estate loans and investments that are now a looming danger—and their exposure is more substantial than it appears.

Bank OZK had two branches in rural Arkansas when chief executive officer George Gleason bought it in 1979. The Little Rock lender today has billions of dollars in commercial real-estate loans, including for properties in Miami and Manhattan, where it is helping fund the construction of a 1,000-foot-tall office and luxury residential tower on Fifth Avenue.

Regional banks across the country followed a similar playbook, gorging on commercial real-estate loans and related investments in big cities over the past decade.

With the commercial real-estate market now in meltdown, those trillions of dollars in loans and investments are a looming threat for the banking industry—and potentially the broader economy. Banks’ exposure is even bigger than commonly reported. The banks are in danger of setting off a doom-loop scenario where losses on the loans trigger banks to cut lending, which leads to further drops in property prices and yet more losses.

Bank OZK hasn’t pulled back from lending, but it has started to see some signs of market trouble. In January, a developer defaulted on a roughly $60 million loan from Bank OZK after construction costs escalated, the bank said. The loan was considered relatively safe because it was far below the building site’s value of $139 million in 2021. In December, a new appraisal put the property’s value at $100 million.

The bank is effectively stuck with the property. “Buying land in the current unstable environment is not something that a lot of people will do,” Gleason, the CEO, said during an April earnings call. Bank OZK declined to comment.

Today’s troubled market, fueled by rising interest rates and high vacancies, follows years of boom times. Banks roughly doubled their lending to landlords from 2015 to 2022, to $2.2 trillion. Small and medium-size banks originated many of those loans, and all that lending helped push up property prices.

Bank OZK’s success over the years allowed Gleason to build himself a 27,000-square-foot French chateau-style mansion in Little Rock, which he filled with a vast collection of European art. “I’ve never said that what we do is risk-less,” Gleason told the Journal in 2019. Still, he added, he considers OZK “probably the most conservative” commercial real-estate lender.

Over the past decade, banks also increased their exposure to commercial real estate in ways that aren’t usually counted in their tallies. They lent to financial companies that make loans to some of those same landlords, and they bought bonds backed by the same types of properties.

That indirect lending—along with foreclosed properties, trading portfolios and other assets linked to commercial properties—brings banks’ total exposure to commercial real estate to $3.6 trillion, according to a Wall Street Journal analysis. That’s equivalent to about 20% of their deposits.

The volume of commercial property sales in July was down 74% from a year earlier, and sales of downtown office buildings hit the lowest level in at least two decades, according to data provider MSCI Real Assets. When deals begin again, they will be at far lower prices, which will shock banks, said Michael Comparato, head of commercial real estate at Benefit Street Partners, a debt-focused asset manager. “It’s going to be really nasty,” he said.

Lending is the lifeblood of all real estate, and regional and community banks have long dominated commercial real-estate lending. Their importance grew after the 2008 financial crisis, when the country’s biggest banks reduced their exposure to the sector under scrutiny from regulators. Low interest rates made higher-yielding real-estate loans lucrative to hold.

That strategy now appears risky after the Federal Reserve raised interest rates. Banks are under pressure to pay depositors more to keep customers from fleeing to higher-yielding investment alternatives. Without cheap deposits, banks have less money to lend and to absorb losses from loans that go bad. Depositors withdrew funds from many small and regional lenders earlier this year after the collapse of three midsize banks stoked fears of a systemwide crisis.

The doom-loop scenario is starting to play out in big cities where office vacancies have soared. Real-estate investors that are unable to refinance their debt, or can only do it at high rates, are defaulting. The lenders, no longer getting the debt payments, often have to write down the value of those mortgages. Sometimes the bank ends up owning the property.

“The plumbing is clogged right now,” said Scott Rechler, chief executive of real-estate investor RXR. “And that is going to create a backup that will eventually overflow on the commercial real-estate markets and on the banking system.”

When Rechler asks banks to refinance his office loans now, few respond. In some cases, he said, it’s not even worth trying. Rechler had a $240 million mortgage coming due on a 33-story office building in lower Manhattan. Vacancies were high, renovating or converting the building would be expensive and the cost of a new mortgage was way up. He ran the numbers and decided to default on the loan. RXR said that it’s been working with the lender to market the building for sale to repay the loan at a discount, and that they have discussed possible loan modifications if the building isn’t sold.

Besides banks, lenders such as private debt funds, mortgage REITs and bond investors can also provide funding—but many of them are financed by banks and can’t get loans. “We are seeing a serious credit crunch developing,” said Ran Eliasaf, managing partner of Northwind Group, a private real-estate lender.

Earlier this year, Buffalo, N.Y., regional lender M&T Bank reported nearly 20% of loans to office landlords were at higher risk of default. The bank has reduced commercial estate lending by 5%.

At the end of June, the bank wrote off $127 million worth of loans for three offices and a healthcare facility in New York City and Washington, D.C., according to the company. It also has unrealized losses on $2.5 billion worth of securities that are tied to loans for offices, apartments and other commercial properties, according to the Journal’s analysis. M&T declined to comment.

Darren King, who oversees retail and business banking at M&T, said at a June investor conference that the bank’s commercial-real estate losses would be a slow grind. “It won’t be Armageddon all in one quarter,” he said.

For its analysis, the Journal tallied hundreds of billions of dollars worth of indirect lending, which often isn’t clearly disclosed, by analyzing banks’ reports filed with the Federal Deposit Insurance Corp. and tapping former bank examiners for their knowledge of bank lending practices.

Between 2015 and 2022, banks more than doubled their indirect real-estate exposure. That included loans to nonbank mortgage companies and to real-estate investment trusts that own and operate buildings and lend to landlords. It also included investments in bonds known as commercial mortgage-backed securities, or CMBS. Banks boosted lending to small businesses that used property as collateral as well.

Holdings of CMBS and loans to mortgage REITs and other nonbank lenders accounted for about 18% of the nearly $3.6 trillion in commercial real-estate exposure in 2022, or nearly $623 billion, according to the Journal’s analysis.

The first quarter of 2023 marked the first decline in banks’ commercial real-estate holdings since 2013, according to the Journal’s analysis. At that point, banks’ overall securities holdings had lost nearly $400 billion in value, largely due to higher interest rates. Banks don’t have to mark down the value of loans in most cases, so the real losses are likely greater.

Banks with less than $250 billion in assets held about three-quarters of all commercial real-estate loans as of the second quarter of 2023, the Journal’s analysis shows. They accounted for nearly $758 billion of commercial real-estate lending since 2015, or about 74% of the total increase during that period.

That increase in lending helped boost commercial real-estate prices by 43% from 2015 to 2022, according to real-estate firm Green Street.

Banks and real-estate developers could be relieved from a downward spiral by lower interest rates or by investors stepping up to buy distressed properties. Wall Street firms are raising funds to scoop up properties, but many properties will likely be sold at well below their recent prices, potentially triggering losses for owners and lenders. Roughly $900 billion worth of real-estate loans and securities, most with rates far lower than today’s, need to be paid off or refinanced by the end of 2024.

Real-estate developer Riaz Taplin’s financier of 20 years, First Republic Bank, failed in May. That put him on a scavenger hunt for cash.

The San Francisco Bay-area developer was turned down by a subsidiary of regional lender PacWest Bancorp. The bank was a big real-estate lender but many of its depositors fled in the spring, worried about potential losses. “They’re like: Riaz, we’re just trying to get through the storm,” he said. “Call back when it’s not a torrential downpour.”

PacWest was bought by Banc of California in July for about $1 billion. By then the bank had already sold a real-estate lending unit and a $2.6 billion property portfolio. PacWest and Banc of California declined to comment.

Taplin said he is still able to get loans from other banks, but they are smaller, more cumbersome and take longer to close. And banks will only lend to him if he deposits money there, he said. He now has deposits with four banks and has to constantly move money among them.

Regulators have been warning banks about commercial real-estate lending for years. In 2015, the country’s banking regulators joined together to warn that high concentrations of commercial mortgages and poor risk management put banks “at greater risk of loss or failure.”

Many banks responded by making individual loans less risky, but collectively increased lending and loosened their underwriting standards in other ways.

Centennial Bank, based in Conway, Ark., became a big funder of developers building luxury skyscrapers in New York and Miami. Construction loans are among the riskiest types of real-estate lending.

John Allison, chairman of the bank’s holding company, Home BancShares, told the Journal in late 2019 that representatives from the Federal Reserve urged him to slow down the bank’s lending. “They’re telling us the construction lending space is going to blow up…and the world is coming to an end,” Allison recalled. “And I said, ‘You know what? I don’t see it.’” Centennial continued increasing its construction loans, although they grew more slowly than deposits during the pandemic.

Home BancShares said it didn’t lose money on construction loans and that a surge in deposits stashed away in supersafe investments reduced the bank’s risk. “If the big, bad wolf shows up it will hurt a lot of banks, but it won’t hurt Home BancShares,” Allison said in a recent interview.

In June, after the failure of three regional banks, Federal Reserve Chairman Jerome Powell called for “regulatory strengthening” for regional and local banks because of risky levels of commercial real-estate exposure.

Regulators’ playbook for banks now is similar to its strategy after the 2008 financial crisis: allow banks to work with struggling borrowers and allow them to keep mortgages on their books at face value in many cases.

That approach will be ineffective because interest rates have risen so much, said Tyler Wiggers, a lecturer at Miami University in Ohio and former adviser to the Federal Reserve Board on commercial real estate. “All of a sudden banks have borrowers who are saying, holy crap, I was paying at 3.5% and now I’m paying 7.5%,” he said. “If borrowers aren’t able to service their debt then banks have to recognize this as a bad loan.”

Banks are selling commercial mortgage-backed securities. While mortgage-backed securities helped cause the 2008-09 financial crisis, more recently issued securities are considered safer than their precrisis counterparts because lending standards are now more conservative. Banks own about half of the bonds outstanding, according to Bank of America Global Research, the result of a pandemic-era buying binge.

Banks added $131 billion to their CMBS holdings in 2020 and 2021. Real-estate companies happily met that demand by doubling their annual issuance to $110 billion in 2021, according to commercial real-estate data company Trepp. CMBS issuance fell to $16.4 billion in the first half of this year.

When banks were snapping up CMBS, property owners were able to load up on debt tied to their buildings. In early 2021, an affiliate of Brookfield Asset Management borrowed $465 million in CMBS and other debt against the Gas Company Tower, a 52-story office building in downtown Los Angeles.

At the time, appraisers valued the property at $632 million, according to Trepp, up from a valuation of $517 million when Brookfield bought the building in 2013. When the loans came due this February, the owner defaulted. An appraiser earlier this year cut the building’s estimated value to $270 million.

These should always be complimentary products. Whether one is using a GLP-1 drug to lose weight or manage diabetes the natural inclination for a person participating in active disease management is to measure one's success. Imagine dieting without ever stepping on a scale. CGM products are the scale.

GLP-1 drugs can have serious side effects as, (among other functions), they mimic pancreatic function as it relates to the digestion of food. Not everyone's system or fully functioning pancreas manages this intrusion well. That said, GLP-1 drugs have proven to be quite safe and therapeutic.

As for the business end of this discussion, the primary cause of diabetes and weight gain is the consumption of highly processed foods. As that distinctly American habit spreads across the world, I suspect managing these twin diseases will never revert to eating whole foods any more than solving the climate problem will be solved by humans deciding to cut back on energy use.

Strike two - or 202 depending on where you want to start counting. We'll find out how much he'll never pay in January.

Judge Rules Donald Trump Liable for Defaming Writer E. Jean Carroll

I knew it was bad in Silicon Valley but according to Kastle Systems office occupancy in San Jose, California is currently 38.8%.

He should have paid the billion and walked away.

Musk bought Twitter, now known as X, last year for $44 billion. After initiating the acquisition in April, Musk spent months involved in legal disputes in which he tried to drop his bid–a move which would have cost a $1 billion break-up fee if the deal fell through.

September is a month that can often be deceptive. Over the last 70+ years the first half of September has averaged just below the annualized SPX return of 9% but the 2nd half has averaged over 20% negative return, (again on an annual basis). I don't think October is much better.

Yup, state's rights. Insurance companies love it as they pay off the politicos to Balkanize the US.

As I've mentioned before, Barron's can be annoyingly dumb. Yes, I pay for it because there are good ideas inadvertently left in the weeds of annoyance. I'm not sure if this writer is actually paid to write this drivel while one can make well over 5% in treasuries instead of a 2% dividend with a likely upcoming recession, but here it is:

Walmart, Lowe’s, and 11 Other Dividend Stocks That Are Solid Bets for a Recession

In uncertain economic times, certainty has a welcome spot in investor portfolios.

But even within value names, some are more recession-proof than others. One strategy is to look at companies that have recently been able to grow their dividends. Increasing payouts at a time when other companies fear that cash is scarce is surely a sign of confidence. Even better would be to stick with so-called “dividend aristocrats,” or companies that have been able to raise their dividends for 25 consecutive years.

While the economy—and market—have proved to be resilient this year in the face of recession worries, many on Wall Street still fear that danger lurks around the corner. Interest rates are likely to stay higher for longer, many on The Street concluded following Federal Reserve Chair Jerome Powell’s speech at Jackson Hole last week. That’s eventually going to put pressure on growth-oriented stocks, presumably making value-oriented names more attractive.

“This cohort of stocks has outperformed heading into and out of recessions historically,” Chris Senyek, chief investment strategist at Wolfe Research, wrote Thursday. As a group, dividend aristocrats yield 2.5.%—not a super-exciting yield when short-term Treasury bills yield more than 5% but still a secure spot. The dividend aristocrats’ price-to-earnings ratio relative to the S&P 500 is roughly 0.95x, slightly below 10-year average of 1.03x, implying that the stocks look cheap.

Within the S&P 500SPX –0.42% there are 67 dividend aristocrats with nearly half of the names coming from the industrial and consumer staples sectors. Investors who hope to narrow down that list may want to look at companies that are dividend aristocrats that have also bought back shares in each of the last 10 consecutive years—basically doubling down on returning capital to shareholders.

Senyek identified 13 companies that meet the mark on this metric: Lowe’s (ticker: LOW), Genuine Parts GPC –1.77% (GPC), Walmart WMT –0.80% (WMT), Colgate-Palmolive CL –0.67% (CL), Aflac (AFL), Cardinal Health (CAH), Expeditors International of Washington (EXPD), C.H. Robinson Worldwide, (CHRW), Emerson Electric (EMR), A.O. Smith (AOS), Illinois Tool Works (ITW), W.W. Grainger , (GWW), and Automatic Data Processing (ADP).

On average these companies have a dividend yield of 2% and a buyback yield over the last 12 months 5%. While the pace of buybacks could change, historical data would imply a total yield of 7%.

That’s something for investors to get excited about.

Nice work if you can get it Henry, and 22 years guaranteed. Your parents would be so proud...boys.

Interesting interpretation of US culture. I liked El Norte as it's quite familiar with common terms in Santa Fe. There's a local credit union, Del Norte which is more familiar to people from Santa Fe as everyone above Santa Fe is "from the North". Also known as Norteños, A common colloquialism is a joke; "I'll take you up North". I derives from the very real past tense reality, "They took him up North".

Here are a few colloquialisms all Norteños understand:

I was born here all my life.

You're gonna land up in trouble

..or what? - goes on the end of any question.

Eh, or Eeee. Added to the end of any sentence.

ABT has done a good job over the last year getting hospitals to approve distribution during care and, insurance, including Medicare to cover cost. This is normally covered at 50% cost or roughly $80 a month. The Libre 3 is a much improved product. This is still a middle class and up product because of the monthly cost and the requirement of a modern smart phone. It's also excellent if a patient has a doctor willing to download and review data. Patients who use a Freestyle and pay attention to smart phone alerts can easily remain in range 95% of the time or more. As docs will tell you, staying in range is, (for most patients), the biggest challenge.

I'm not affiliated with ABT or this product, I've just seen how well it helps patients willing to change lifestyle and monitor progress. Diabetes is generally not a killer but inattention to the disease will eventually take a toll.

So far, short term support at SPX ~4,494 is holding.