News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Looking at that TMC vrs GDP chart (reportedly Buffett's favorite metric for determining overall market valuations), the next recession should bring it back down from 140 toward the mean of 80. A recession is overdue and could come next year, even with the Fed now in dovish mode and trying engineer a soft landing. But that chart speaks volumes, and the fact that Buffett uses it also speaks volumes.

John Bogle said that his personal 'most bearish' asset allocation was 50/50 stocks to bonds (he would normally be 70% or 80% in stocks). Adjusting the asset allocation is about as close as Bogle would ever come to market timing, and because stocks have a much higher return over the long haul, avoiding stocks completely is a very bad idea. As we know, Bogle was strongly against market timing and trying to pick individual stocks.

>>> One of Warren Buffet's favorite metrics is flashing red — a sign that corporate profits are due for a hit

Fortune

by Shawn Tully

7-17-19

https://www.msn.com/en-us/money/savingandinvesting/one-of-warren-buffets-favorite-metrics-is-flashing-red-%e2%80%94-a-sign-that-corporate-profits-are-due-for-a-hit/ar-AAEtoGA?li=BBnb7Kz&ocid=mailsignout#page=2

Here's a crucial question for investors that the Wall Street crowd seldom addresses: Can corporate profits keep booming by growing faster than the economy? Is this the new normal, or will the GDP-gobbling trend reverse, as it always has in the past, turning today's record-shattering rally into a rout?

Shareholders beware. It's the unhinging of profits from the overall economy that has been propelling stock prices, and that dynamic is now in danger. Either the normal ebb and flow of markets will pull equity values back to their traditional share of GDP, or Congress is likely to do the job by attacking Big Tech and mandating that workers get a lot more of the bounty now flowing to shareholders. Either way, America's companies and its economy are one in the same. Over the long-term, they need to move in tandem. And if they stray too far apart, getting back to balance can pummel share prices.

The S&P 500's fantastic performance since late 2016 is all about earnings. Since the fourth quarter of that year, profits, based on the trailing twelves months of GAAP earnings, have jumped 41% to a blowout record of $134.39 per share. In that period, share prices have followed earnings like a postage stamp on a letter, rising precisely the same number to just over 3000. That's because investors are awarding shares a consistent P/E multiple in the 22 to 24 range.

But it's critical to assess whether or not a profit bubble has driven shares to unsustainably high prices.

To gauge if that's happened, let's examine one of the best measures of where stocks stand on the continuum from excessively cheap to dangerously expensive. It's the ratio of Total Market Cap (TMC), the value of all U.S. publicly traded companies, versus GDP, the value of all goods and services produced annually within our borders. Put simply, it shows the dollar size of the equity market as a share of the economy.

If the value of equities represents a far bigger than average share of national income, it probably means that epic earnings are devouring a much bigger share of national income than usual, leaving less for wages. That's certainly the case today. In the past, the gravitational force of competition for both goods and labor has always restored balance by curbing excessive profits, and in most cases, driving down stock prices.

The TMC to GDP ratio is a favorite yardstick of Warren Buffett, who's stated, that "it's probably the best measure of where valuations stand at any given moment." (We'll refer to the measure as the "cap ratio.")

Today, the value of all stocks to national income stands at 146.4. That's the second highest reading in the past half-century, exceeded only by the 148.5 posted at the peak of the dot.com bubble on March 30, 2000. The cap ratio has averaged around 80 over the past decade, so it now exceeds that benchmark by 80%.

The cap ratio has varied widely over the past five decades, but typically returns to that reading of 80 after spiking well above, and plunging far below, that mean. By definition, over each period the ratio starts and ends at 80, earnings simply grow with GDP. (We'll express GDP in 'nominal,' not inflation-adjusted terms.) Still, it's informative to study the careening course in between.

We'll start at the 80 mark reached at the start of 1971. The cap ratio fell as low as 35 in the deep 1982 recession, and generally stayed below 50 from 1976 to 1986. It didn't get back to 80 until the end of 1995, an interlude of 25 years. Over that period, the S&P 500 rose on average 7.3% a year, reflecting economic growth inflated by high inflation from the oil shock of the 1970s and early 1980s.

From that 80 reading at the end of 1995, through March 30 of 2000, the cap ratio went wild, jumping 86% to that record level of almost 150 at the height of the internet craze. Then, gravity took over, and by April of 2003, the "cap" had crashed back to 80. Over that 7-plus year period, the S&P 500 rose by a more or less normal 5.6%, half as fast as in the past half-decade, once again, tracking GDP.

From the 80 reading in early 2003, the ratio plunged to the low 50s during the 2009 financial crisis, and didn't hit 80 again until October of 2011. Over those seven-and-a-half years, the S&P gained just 3.1% annually, as cratering home prices hobbled the economy.

Since returning to a "normal" level in late 2011, the cap ratio soared hockey-stick style, hitting the current 146.2 while suffering only minor blips along the way. Over those 7 years and 9 months, GDP rose 35%, from $15.6 trillion to $21.1 trillion. Total market cap leaped from $12.6 trillion to $3.014 trillion, or 148%. The S&P 500 delivered annual gains of 11%, while national income rose less than half as fast, by 4%.

Put simply, companies cut back on workers, held down wages, feasted from low interest rates on their debt, and otherwise benefited from a perfect calm for profits. And those trends totally trumped mediocre economic growth.

Two additional measures are flashing red. I often interviewed Milton Friedman, the legendary economist, before his death in 2006. Friedman told me that "in the long term, earnings cannot remain above their historical average as a share of national income." The Nobel laureate also declared that although profit performance determines companies' values over lengthy periods, "markets in the short term are far from 'efficient,'" meaning that equity prices can vary significantly from the enterprises' underlying value.

Today, according to the St. Louis Federal Reserve, corporate profits account for 9.2% of GDP. That's one-third higher than the half-century average of 7%. Since profits normally "revert to the mean" a la Friedman, that gap is destined to shrink. Operating margins also look unsustainably high. According to S&P, the figure for the S&P 500 averaged 11.25% over the past four quarters, 25% above the average of 9% posted in the previous 30 quarters.

It's conceivable that our economy really has changed, as the break-up-tech crowd in Congress argues, and that internet is enabling tech giants to operate as monopolies. That's the position adopted by a number of influential economists, including former Treasury Secretary Larry Summers. Another possibility: Because they're so profitable, these players are prime targets by hungry startups that will eventually erode their profitability.

The best bet is that equity valuations return to a more normal share of national income. The past few years look like the kind of crazy uncoupling that happens every couple of decades, not a structural downshift from the world's most competitive market to a network of cartels.

The market hasn't failed to rein in runaway profits yet, and it won't fail this time.

<<<

Gold's role in asset allocation -

Trying to figure out where gold 'should' be trading is tough since central banks have routinely suppressed the price to make their own unbacked fiat currencies look better/less bad. And China has possibly been suppressing the gold price in order to continue accumulating on the cheap.

As Jim Rickards points out, gold itself isn't really good for very much except as money, or as a backing for money. Countries like China and Russia have been aggressively building up their gold reserves over the past decade for a reason. When the coming financial reset comes (SDR), having large gold reserves will give a country a strong place at the global 'dinner table'.

There's a good chance the SDR will need to be partially backed by gold, at least in the beginning. Rickards does the math, and to provide a 40% backing would put the gold price at approx $10,000/ounce. During the transition to the SDR, US paper assets like stocks/bonds will be hit big time. Rickards says the US standard of living could drop 60% overnight as the dollar loses its role as the world's reserve currency to the SDR. The dollar will become just another 'local' currency for use within the US.

Rickards recommends investors have 10% in physical gold as disaster insurance. You hope the gold doesn't do well since that means your paper investments are still doing OK. In a $1 mil portfolio with $100 K in gold (70 ounces), $200 K in cash, $350 K in stocks, $350 K in bonds, if the stocks and bonds dropped 50% and gold went to $10,000/oz, your portfolio would be worth $1.25 mil instead of the $600 K it would be worth without the gold.

So think of gold as portfolio insurance, a diversification tool. You don't want a huge position in gold, but 10% could save the day when the dollar system unravels, as it eventually will. The global finance 'oligarchy' have been preparing the way for the SDR for a long time. They know the US dollar won't be suitable as the world's reserve forever, and the SDR has many advantages.

>>> Sector investing using the business cycle

It may be possible to enhance returns over an intermediate time horizon.

FIDELITY VIEWPOINTS

5/31/2019

https://www.fidelity.com/viewpoints/investing-ideas/sector-investing-business-cycle?ccsource=email_weekly

Key takeaways

The business cycle can be a determinant of sector performance over the intermediate term.

The phases of the economy provide a framework for sector allocation.

For example, the consumer discretionary and industrials sectors tend to outperform in the early cycle.

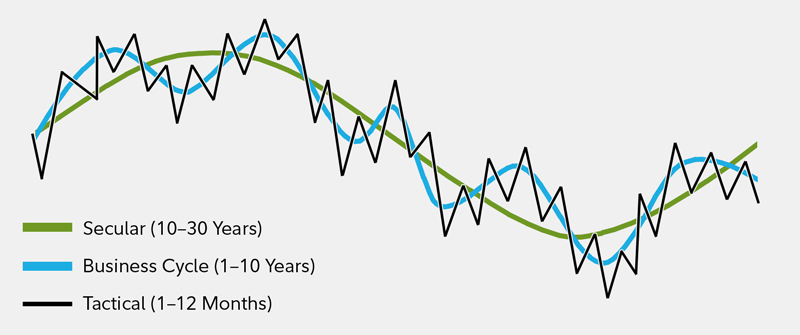

Over the intermediate term, asset performance is often driven largely by cyclical factors tied to the state of the economy, such as corporate earnings, interest rates, and inflation. The business cycle, which encompasses the cyclical fluctuations in an economy over many months or a few years, can therefore be a critical determinant of equity market returns and the performance of equity sectors. This article demonstrates Fidelity’s business cycle approach to sector investing, and how it potentially can enhance returns over an intermediate time horizon.

Asset allocation framework

Fidelity’s Asset Allocation Research Team (AART) conducts economic, fundamental, and quantitative research to produce asset allocation recommendations for Fidelity’s portfolio managers and investment teams. Our framework begins with the premise that long-term historical averages provide a reasonable baseline for portfolio allocations. However, over shorter time horizons—30 years or less—asset price fluctuations are driven by a confluence of various short-, intermediate-, and long-term factors that may cause performance to deviate significantly from historical averages. For this reason, incorporating a framework that analyzes underlying factors and trends among the following 3 temporal segments can be an effective asset allocation approach: tactical (1–12 months), business cycle (1–10 years), and secular (10–30 years).

Asset performance is driven by a confluence of various short-, intermediate-, and long-term factors

This chart shows that asset performance is driven by a confluence of various short-, intermediate-, and long-term factors.

For illustrative purposes only. Source: Fidelity Investments, Asset Allocation Research Team (AART).

Understanding business cycle phases

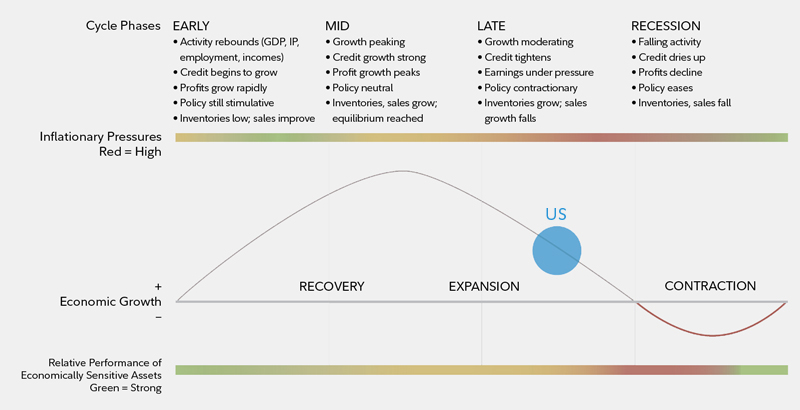

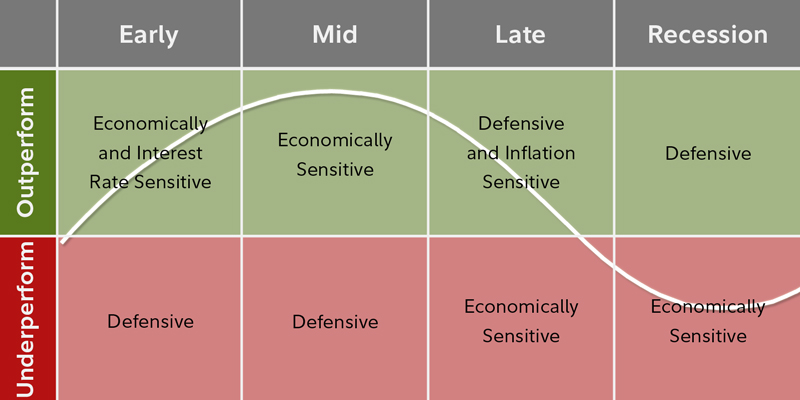

Every business cycle is different in its own way, but certain patterns have tended to repeat themselves over time. Fluctuations in the business cycle are essentially distinct changes in the rate of growth in economic activity, particularly changes in 3 key cycles—the corporate profit cycle, the credit cycle, and the inventory cycle—as well as changes in the employment backdrop and monetary policy. While unforeseen macroeconomic events or shocks can sometimes disrupt a trend, changes in these key indicators historically have provided a relatively reliable guide to recognizing the different phases of an economic cycle. Our quantitatively backed, probabilistic approach helps in identifying, with a reasonable degree of confidence, the state of the business cycle at different points in time. Specifically, there are 4 distinct phases of a typical business cycle (see chart).

Early-cycle phase: Generally, a sharp recovery from recession, marked by an inflection from negative to positive growth in economic activity (e.g., gross domestic product, industrial production), then an accelerating growth rate. Credit conditions stop tightening amid easy monetary policy, creating a healthy environment for rapid margin expansion and profit growth. Business inventories are low, while sales growth improves significantly.

Mid-cycle phase: Typically the longest phase of the business cycle. The mid-cycle is characterized by a positive but more moderate rate of growth than that experienced during the early-cycle phase. Economic activity gathers momentum, credit growth becomes strong, and profitability is healthy against an accommodative—though increasingly neutral—monetary policy backdrop. Inventories and sales grow, reaching equilibrium relative to each other.

Late-cycle phase: Often coincides with peak economic activity, implying that the rate of growth remains positive but slows. A typical late-cycle phase may be characteristic as an overheating stage for the economy when capacity becomes constrained, which leads to rising inflationary pressures. While rates of inflation are not always high, rising inflationary pressures and a tight labor market tend to crimp profit margins and lead to tighter monetary policy.

Recession phase: Features a contraction in economic activity. Corporate profits decline and credit is scarce for all economic actors. Monetary policy becomes more accommodative and inventories gradually fall despite low sales levels, setting up for the next recovery.

The performance of economically sensitive assets such as stocks tends to be the strongest during the early phase of the business cycle, when growth is rising at an accelerating rate, then moderates through the other phases until returns generally decline during the recession. In contrast, more defensive assets such as Treasury bonds typically experience the opposite pattern, enjoying their highest returns relative to stocks during a recession, and their worst performance during the early cycle.

The business cycle has 4 distinct phases. The US is firmly in the late cycle as of 2019.

This graphic shows that the US is firmly in the late cycle as of 2019.

Note: The diagram above is a hypothetical illustration of the business cycle. There is not always a chronological, linear progression among the phases of the business cycle, and there have been cycles when the economy has skipped a phase or retraced an earlier one. Economically sensitive assets include stocks and high-yield corporate bonds, while less economically sensitive assets include Treasury bonds and cash. We use the classic definition of recession, involving an outright contraction in economic activity, for developed economies. Source: Fidelity Investments (AART), as of March 31, 2019.

Equity sector performance patterns

Historical analysis of the cycles since 1962 shows that the relative performance of equity market sectors has tended to rotate as the overall economy shifts from one stage of the business cycle to the next, with different sectors assuming performance leadership in different economic phases.1 Due to structural shifts in the economy, technological innovation, varying regulatory backdrops, and other factors, no one sector has behaved uniformly for every business cycle. While it is important to note outperformance, it is also helpful to recognize sectors with consistent underperformance. Knowing which sectors of the market to reduce exposure to can be just as useful as knowing which tend to have the most robust outperformance.

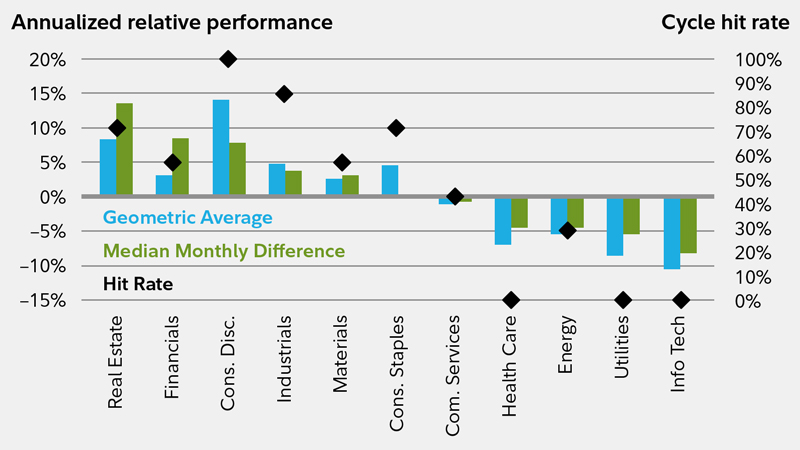

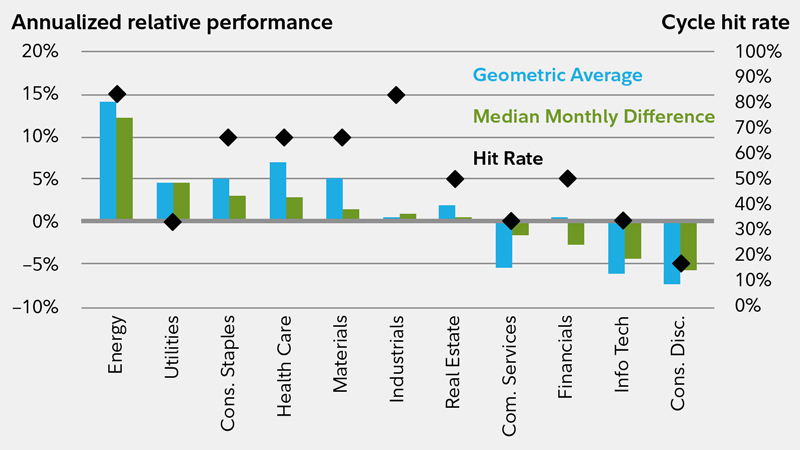

Early-cycle phase

Historically, the early-cycle phase has featured the highest absolute performance. Since 1962, the broader stock market has produced an average total return of more than 20% per year during this phase, and its average length has been roughly one year. On a relative basis, sectors that typically benefit most from a backdrop of low interest rates and the first signs of economic improvement have tended to lead the broader market’s advance. Specifically, interest-rate-sensitive sectors—such as consumer discretionary, financials, and real estate—historically have outperformed the broader market (see chart). These sectors have performed well, due in part to industries within the sectors that typically benefit from increased borrowing, including diversified financials and consumer-linked industries such as autos and household durables in consumer discretionary.

Elsewhere, economically sensitive sectors—such as industrials and information technology—have been boosted by shifts from recession to recovery. For example, the industrials sector has some industries—such as transportation and capital goods—in which stock prices often have rallied in anticipation of economic recovery. Information technology and materials stocks typically have been aided by renewed expectations for consumer and corporate spending strength.

Laggards of the early-cycle phase include communication services and utilities, which generally are more defensive in nature due to fairly persistent demand across all stages of the cycle. Energy sector stocks also have lagged during the early phase, as inflationary pressures—and thus energy prices—tend to be lower during a recovery from recession. From a performance consistency perspective, consumer discretionary stocks have beaten the broader market in every early-cycle phase since 1962, while industrials also have exhibited impressive cycle hit rates. The financials and information technology sectors both have had healthy average and median relative performance, though their low hit rates are due in part to the diversity of their underlying industries. The communication services sector has historically underperformed in the early-cycle phase, but its evolving mix of industries provides less confidence in the persistence of this pattern moving forward.

Sectors that have performed well in the early cycle are interest-rate sensitive and economically sensitive sectors

This chart shows sectors that have performed well in the early cycle.

Includes equity market returns from 1962 through 2016. Returns are represented by the top 3000 US stocks ranked by market capitalization. Sectors as defined by GICS. Source: Fidelity Investments (AART), as of March 31, 2019. Past performance is no guarantee of future results.

Mid-cycle phase

As the economy moves beyond its initial stage of recovery and as growth rates moderate, the leadership of interest-rate-sensitive sectors typically has tapered. At this point in the cycle, economically sensitive sectors still have performed well, but a shift has often taken place toward some industries that see a peak in demand for their products or services only after the expansion has become more firmly entrenched. Average annual stock market performance has tended to be fairly strong (roughly 15%), though not to the same degree as in the early-cycle phase. In addition, the average mid-cycle phase of the business cycle tends to be significantly longer than any other stage (roughly 3.5 years), and this phase is also when most stock market corrections have taken place. For this reason, sector leadership has rotated frequently, resulting in the smallest sector-performance differentiation of any business cycle phase. No sector has outperformed or underperformed the broader market more than 75% of the time, and the magnitude of the relative performance has been modest compared with the other 3 phases.

Information technology has been the best performer of all the sectors during this phase, having certain industries—such as semiconductors and hardware—that typically pick up momentum once companies gain more confidence in the stability of an economic recovery and are more willing to make capital expenditures (see chart). We also expect the new communication services sector to outperform during the mid-cycle phase, largely due to the strength of the media industry at this point in the cycle.

From an underperformance perspective, the materials and utilities sectors have lagged by the greatest magnitude. Due to the lack of clear sector leadership, the mid-cycle phase is a market environment in which investors may want to consider keeping their sector bets to a minimum while employing other approaches to generate additional active opportunities.

Sector leadership has rotated frequently in the mid-cycle phase, resulting in the smallest sector performance differentiation of any business cycle phase

This chart shows how sector leadership has rotated frequently in the mid-cycle phase.

Sectors as defined by GICS. Source: Fidelity Investments (AART), as of March 31, 2019. Past performance is no guarantee of future results.

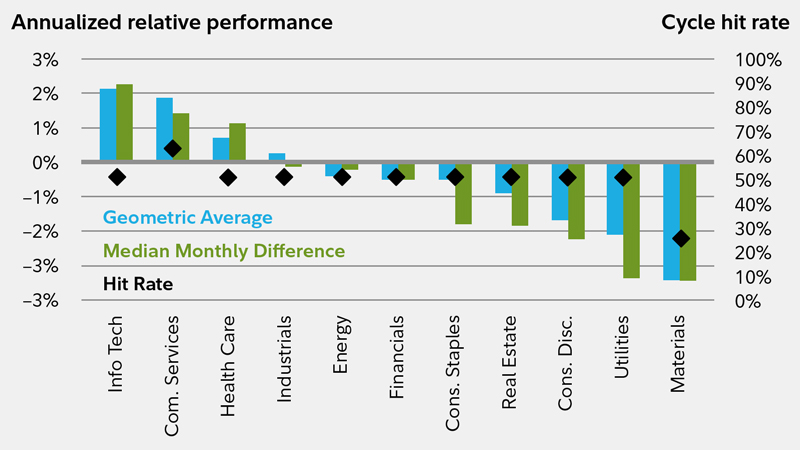

Late-cycle phase

The late-cycle phase has had an average duration of roughly a year and a half, and overall stock market performance has averaged 6% on an annualized basis. As the economic recovery matures, the energy and materials sectors, whose fate is closely tied to the prices of raw materials, previously have done well as inflationary pressures build and the late-cycle economic expansion helps maintain solid demand (see next chart below).

Elsewhere, as investors begin to glimpse signs of an economic slowdown, defensive-oriented sectors—those in which revenues are tied more to basic needs and are less economically sensitive, particularly health care, but also consumer staples and utilities—generally have performed well. Looking across all 3 analytical measures, the energy sector has seen the most convincing patterns of outperformance in the late cycle, with high average and median relative performance along with a high cycle hit rate.

Information technology and consumer discretionary stocks have lagged most often, tending to suffer the most during this phase, as inflationary pressures crimp profit margins and investors move away from the most economically sensitive areas.

As the economic recovery matures, the materials and energy sectors have typically performed well, as have defensive-oriented sectors

This chart shows which sectors have performed well as the economic recovery matures.

Sectors as defined by GICS. Source: Fidelity Investments (AART), as of March 31, 2019. Past performance is no guarantee of future results.

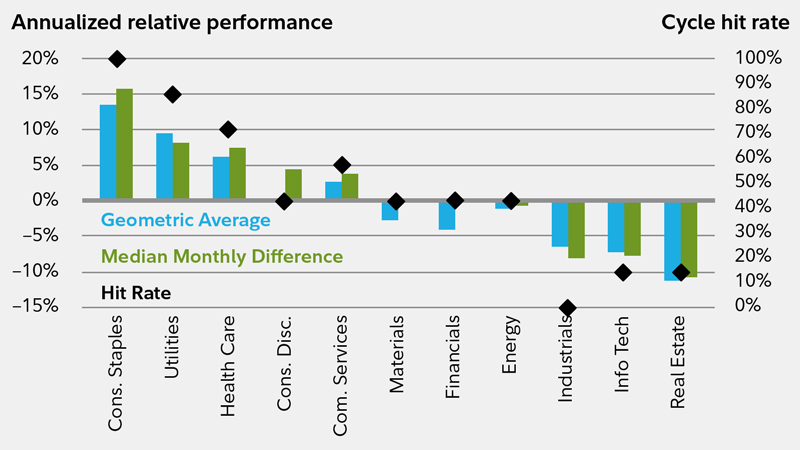

Recession phase

The recession phase has historically been the shortest, lasting slightly less than a year on average—and the broader market has performed poorly during this phase (-15% average annual return). As economic growth stalls and contracts, sectors that are more economically sensitive fall out of favor, and those that are defensively oriented move to the front of the performance line. These less economically sensitive sectors, including consumer staples, utilities, and health care, are dominated by industries that produce items such as toothpaste, electricity, and prescription drugs, which consumers are less likely to cut back on during a recession (see next chart below). These sectors’ profits are likely to be more stable than those in other sectors in a contracting economy. The consumer staples sector has a perfect track record of outperforming the broader market throughout the entire recession phase, while utilities and health care are frequent outperformers. High-dividend yields provided by utility and telecom companies also have helped these sectors hold up relatively well during recessions. On the downside, economically and interest-rate-sensitive sectors— such as industrials, information technology, and real estate—typically have underperformed the broader market during this phase.

This chart shows that defensive-oriented sectors tend to outperform during the recession phase.

Sectors as defined by GICS. Source: Fidelity Investments (AART), as of March 31, 2019. Past performance is no guarantee of future results.

The merits of the business cycle approach

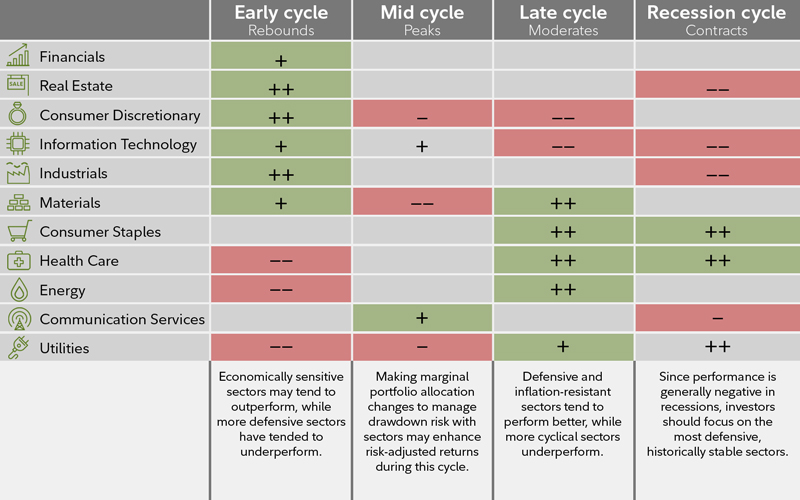

For those interested in a more active approach to managing their equity exposure, the business cycle approach offers considerable potential for taking advantage of relative sector-performance opportunities. As the probability of a shift in phase increases—for instance, from mid-cycle to late-cycle—such a strategy allows investors to adjust their exposure to sectors that have prominent performance patterns in the next phase of the cycle (see next chart below). Our views on these phase shifts are presented in recurring monthly updates on the business cycle.2 By its very nature, the business cycle focuses on an intermediate time horizon (i.e., cycle phases that rotate on average every few months to every few years). This may make it more practical for some investors to execute than shorter-term approaches.

Looking at sectors throughout the business cycle

Note: The typical business cycle shown above is a hypothetical illustration. There is not always a chronological progression in this order, and in past cycles the economy has skipped a phase or retraced an earlier one.

Source for sector performance during business cycle: Fidelity Investments (AART). Unshaded (white) portions above suggest no clear pattern of over- or underperformance vs. broader market. Double +/– signs indicate that the sector is showing a consistent signal across all three metrics: full-phase average performance, median monthly difference, and cycle hit rate. A single +/– indicates a mixed or less consistent signal. Returns data from 1962 to 2016. Annualized returns are represented by the performance of the largest 3,000 US stocks measured by market capitalization, and sectors are defined by the Global Industry Classification Standard (GICS®). Past performance is no guarantee of future results. See below for important information.

Additional considerations for capturing alpha in sectors

Incorporating analysis and execution at the industry level may provide investors with greater opportunities to generate relative outperformance (“alpha”) in a business cycle approach. Industries within each sector can have significantly different fundamental performance drivers that may be masked by sector-level results, leading to significantly different industry-level price performance (see next chart below).

In addition, there are other strategies that can be incorporated to complement the business cycle approach and potentially capture additional alpha in equity sectors. Consider the following:

Macro-fundamental analysis: Macro-fundamental industry research can identify—independently of typical business cycle patterns—variables specific to the dynamics of each industry that may affect performance. For example, a significant change in the cost of key raw material inputs—such as oil prices for airlines—can drive a deviation in an industry's performance.

Bottom-up analysis: Company-specific analysis— through individual security selection—can identify unique traits in individual companies that may outweigh the impact of the typical business cycle pattern on that company’s future performance.

Global business cycle analysis: The US stock market has global exposure, which may warrant allocating toward or away from domestically focused sectors, depending on the phase of the US business cycle relative to the rest of the world. When the US business cycle is more favorable than the global cycle, sectors with more global exposure are likely to face greater headwinds to revenue growth, while more domestically linked sectors could fare relatively well.

Inflation overlay: The inflation backdrop can heavily influence some sectors’ profitability. Short-term inflation trends tend to ebb and flow with the movement of the business cycle, but longer-term inflation trends sometimes move independently of the business cycle.

Secular overlay: Long-term secular trends that are expected to unfold over multiple business cycles can warrant a permanently higher or lower allocation to a given sector than a pure business cycle approach would suggest.

This graphic shows that each industry within a sector has specific drivers that may affect performance.

Investment implications

Every business cycle is different, and so are the relative performance patterns among equity sectors. However, using a disciplined business cycle approach, it is possible to identify key phases in the economy and to use those signals in an effort to achieve active returns from sector allocation.

Analyzing relative sector performance

Certain metrics help evaluate the historical performance of each sector relative to the broader equity market (all data are annualized for comparison purposes):

Full-phase average performance: Calculates the (geometric) average performance of a sector in a particular phase of the business cycle, and subtracts the performance of the broader equity market. This method better captures the impact of compounding and performance that is experienced across full market cycles (i.e., longer holding periods). However, performance outliers carry greater weight and can skew results.

Median monthly difference: Calculates the difference in the monthly performance of a sector compared with the broader equity market, and then takes the midpoint of those observations. This measure is indifferent to when a return period begins during a phase, which makes it a good measure for investors who may miss significant portions of each business cycle phase. This method mutes the extreme performance differences of outliers, and also underemphasizes the impact of compounding returns.

Cycle hit rate: Calculates the frequency of a sector’s outperforming the broader equity market over each business cycle phase since 1962. This measure represents the consistency of sector performance relative to the broader market over different cycles, removing the possibility that outsized gains during one period in history influence overall averages. This method suffers somewhat from small sample sizes, with only 7 full cycles during the period, but persistent outperformance or underperformance still can be observed.

We updated our Business Cycle Sector Framework as a result of the September 2018 changes to the Global Industry Classification Standard (GICS) structure. This framework was last refreshed in 2016, following the elevation of real estate as the 11th GICS sector.

As of September 2018, the newly formed communication services sector combined the legacy telecommunication services sector with entertainment software, traditional media, and internet media companies. As a result, this new sector is more cyclical than its more-defensive predecessor, telecom, and we expect it to perform well in the mid cycle and underperform during recessions. Our assessment of communication services is more qualitative than that of the other sectors, given its evolving mix of industries.

Other sectors were also impacted by the shift in the GICS structure. Consumer discretionary lost some large internet media companies and gained online marketplaces. The departure of internet companies made the outlook for consumer discretionary less favorable in the mid cycle. Information technology was also affected by losing some internet and entertainment software companies, but the overall business cycle playbook for information technology companies did not change as a result.

<<<

The gold breakout has resolved some of the questions that have surrounded gold. The question now isn't whether to have gold in your asset allocation, but -

1) How much?

2) Buy now, or wait for a pullback?

3) Physical gold, or ETFs?

4) Gold mining sector?

Rickards has been recommending up to 10% in physical gold, and has mentioned having some exposure to the miners.

Buy now or wait? It might be best to average in over the next period of months. The breakout has been strong, but there could be a pullback to re-test the breakout level (1350-65).

>>> Wealthy Families Are Adding Forests to Their Portfolios

It’s a long-term bet on growth.

Bloomberg

By Lananh Nguyen

June 16, 2019

https://www.bloomberg.com/news/articles/2019-06-17/wealthy-families-are-adding-forests-to-their-portfolios?srnd=premium

Tom Crowder spent much of his two-year career in the NFL running away from men who weighed upwards of 300 pounds. These days? He worries about bears and snakes. As a senior vice president at Bank of America Corp., Crowder spends most days in the woods, from the evergreen forests of New England to the wetlands of the Carolinas, scouting U.S. timberland assets for people with a net worth of at least $100 million and a minimum of $10 million to invest.

“Trees don’t move as fast as Pro Bowl linebackers,” Crowder says on a recent field trip to a client’s timber farm in South Carolina overlooking the alligator-populated Waccamaw River. As turtles sun themselves and wild turkeys roam, he recounts over a picnic lunch the “neat experience” of his stint as a wide receiver and safety for the Dallas Cowboys. After a busted jaw and emergency surgery, he was happy to go back to his roots, as a third-generation forester.

Crowder is among more than 200 experts employed by Bank of America’s Specialty Asset Management group, or SAM, which manages more than 94,000 assets with a value of $13.6 billion for individuals and institutions. The target client is looking for timberland, farms, ranches, energy interests, or real estate, so-called alternative investments that can diversify portfolios mostly made up of stocks and bonds and can provide a hedge against inflation.

Returns for timberland totaled 3.2% in 2018, compared with 2.4% so far this year, according to an index from the National Council of Real Estate Investment Fiduciaries.

John Kelley, a SAM national executive, says “long-term themes” sell. The decline in arable land and rising global food demand, for example, are reasons to invest in farmland. “People have to eat, and what we believe about the intrinsic nature of these assets is that they have real value and they will persist over time,” he says.

For clients willing to make these long-term bets, SAM brings in what it calls boots-on-the-ground specialists from 38 offices across the U.S. They have an average of more than 15 years of experience, Kelley says, and some have been in their field for more than 30 years. Many, like Crowder, come from families who’ve been in those businesses for generations.

An exception is Nancy Fahmy, the head of alternative investments who was tapped to also lead SAM last year after spending most of her 23-year career dealing in esoteric financial assets in New York. “This is a different world for me,” she says, recalling the novelty of climbing onto a tractor for the first time and being intrigued by meeting a colleague wearing an impeccably tailored suit and alligator-skin cowboy boots, the product of a family hunt.

For Crowder, who grew up in Arkansas on his family’s timber farm, it’s familiar territory. While on the trip to the client’s timber tracts, a half-hour drive from Myrtle Beach in South Carolina, he used GPS maps on an extra-large iPad to show off an aerial view of pine trees annotated by the date they were planted. Then he offered instructions on how to use a T-shaped forestry tool, called an increment borer, to extract a section of wood about the size of a drinking straw from a tree to count its rings and gauge its pace of growth.

“People have to eat, and what we believe about the intrinsic nature of these assets is that they have real value and they will persist over time”

Crowder covered a lot of ground over the course of a day, giving a crash course in timber management. He detailed the widespread problem of wild hogs damaging timber properties. He talked about the benefits of recreational hunting clubs, which can offer a revenue stream for owners. He laughed about a catchphrase among colleagues—“release the deer”—a reference to the Chevy Chase movie Funny Farm. That’s what SAM staff say when an impressive animal is spotted on a site visit, as if they’d arranged it specifically to impress prospective buyers.

The bank’s roster of clients includes people from both the U.S. and overseas. Investors new to the arena are strongly encouraged to visit what they might be buying into, and it’s during these trips that the idea of passing on a legacy to future generations hits home, Kelley says. Wealthy families are also becoming more interested in environmental and sustainable investments, he says.

“It has a transformative effect in a lot of ways when they actually get to see it, feel it, touch it, and—sometimes in the case of farmland—smell it,” Kelley says. “It goes beyond the numbers.”

And the numbers for real-asset deals, such as predicted profits and hurdle rates, don’t correspond to typical Wall Street metrics. In some cases, the bank has to explain to sophisticated investors that the investments might not work for them.

The assets do produce revenue—in the form of logs, crops, livestock, or oil and gas—but buyers have to get comfortable with multiyear time horizons for returns. A timber farm could generate immediate sales or take years to harvest, depending on tree maturity and market conditions, or decades if starting from seed.

“This is not like stocks and bonds,” Kelley says. “This is not something that you buy on Monday and sell on Wednesday. That’s not the deal. If you’re not coming in with at least a minimum of a 10-year investment horizon, you really don’t belong in this investment class.”

There are other reasons to be careful. Universities including Yale and Harvard ran into trouble with their forestry investments in recent years after endowment funds bought into huge tracts of land as a way to hedge against inflation. The bets paid off handsomely until 2017, when returns slumped and the universities came under criticism from local residents and environmentalists. The various complaints included concerns about overlogging, destruction of scenery, and the disruption of animal habitats.

The California Public Employees’ Retirement System, the largest U.S. public pension system, is restructuring its forestland portfolio after its investments lost an average of 1.1% annually over the last 10 years, according to a presentation at a September meeting. The forestlands program has been under review the past few years and will likely be part of a broader examination by Ben Meng, who started in January as chief investment officer, CalPERS spokesman Joe DeAnda says.

That’s why Bank of America emphasizes the importance of its experts, who handpick properties for direct purchases. Farmland specialist Katie VanMeter comes from a family who owns thousands of acres of wheat and chickpeas in Montana. Shelda Owens, who runs operations for the timber business, has a master of science in forest economics. It might be argued that Crowder’s forestry experience goes as far back as his childhood. He cultivated his own sandbox-size plot of trees when he was a kid and had to make “hard decisions” about which ones to thin so the others could grow.

That depth of knowledge is important when the SAM experts are sitting across a table from savvy investors and being grilled by them—and, of course, when they’re showing off the land.

Crowder goes to great lengths out there. He once waded through a waist-deep river, holding the iPad overhead, to assess a property that housed a cave of endangered bats. It wasn’t a good fit, and the bank decided not to manage the property. He prepares for site visits in great detail, readying contingency plans for weather-related disruptions. And he’s learning Mandarin to speak to Chinese clients, but it’s hard going: The Rosetta Stone program doesn’t always understand his Arkansas accent.

Among his clients are New Yorkers who consider Central Park a forest. He points out differences—on timber farms, there are no sidewalks, no lights, and sometimes no cellphone coverage. That off-the-grid experience and the opportunity to learn about nature are refreshing for visitors who might be titans of industry. Crowder enjoys being their guide.

“It’s incredible to make a career out of something that you’re so passionate about,” Crowder says. He spends much of his free time hiking in the forest next to his home in Little Rock, accompanied by his 100-pound giant schnauzer, Ranger. “That’s his passion, too.”

<<<

>>> How to Invest and Profit in the Next Recession

A slump is likely in the next year or so. There are ways to prepare for it.

By Barry Ritholtz

June 17, 2019

https://www.bloomberg.com/opinion/articles/2019-06-17/how-to-invest-and-profit-in-the-next-recession?srnd=premium

Ever since the Great Recession ended in June 2009, investors have been treated to a stream of forecasts warning that another slump is right around the corner. As we have seen, none of these predictions have come to pass. Smart investors paid little heed to predictions that were subjective and of little value.

Enter Campbell R. Harvey. He's a finance professor at Duke University’s Fuqua School of Business. He also is a research associate at the National Bureau of Economic Research, which among other things provides the official start and end dates of expansions and contractions. Most important of all, he maintains one of the more rigorous models for analyzing the potential for a future economic contraction.

Harvey is not an alarmist; to the contrary, he is a sober-minded researcher. In a recent YouTube discussion of the warning signs of an impending recession, he cited four signals. One is the Duke-CFO Global Business Outlook survey, which this month found that more than two-thirds of corporate chief financial officers expect that a recession will be underway by the end of 2020. His second factor is “the realization of anti-growth protectionism,” aka tariffs and rising trade-war tensions; the third is market volatility, which he notes frequently gives false signals, but has generally been on the rise the past few months.

The last, and most important component, is the yield curve, or the schedule of bond yields based on maturity dates. His focus is on the five-year Treasury bond yield, which now is lower than the yield on three-month Treasury bill. According to Harvey’s research, when this inversion -- short-term rates being higher than long-term rates -- lasts for a full quarter, or 90 days, then a recession will occur in 12 to 18 months.

Inversion occurred on March 7 and earlier this month we crossed the 90-day threshold. Thus, all four of the conditions for a future recession in Harvey’s model now have been met. 1

I am not in the business of predicting recessions. However, since the previous one was a decade ago, I am quite comfortable with the idea we are closer to the next one than we are to the last one.

Since we can all agree that another recession is inevitable, I am going to go out on a limb and suggest that now is the time to plan for it. Maybe these will help you get through relatively unscathed:

No. 1. Clean out your portfolio: We all accumulate holdings for reasons that are too silly to go into and look terrible in hindsight: your brother-in-law’s stock recommendation, the initial public offering that didn’t work out, the hot tip from a broker.

Sell ‘em all! With markets near record highs, this is your best opportunity to minimize your losses, since this might be as good as it gets. Remember, weaker companies will do much worse than average ones in recessions. If you own any junk bonds sell them, too.

No. 2. Pay down debt: Today, markets are near all-time highs, unemployment is near 50-year lows and wages are rising. It might not be this easy to lower your outstanding obligations for a while. Give yourself a little maneuvering room and maybe sock away some cash in your emergency fund.

No. 3. Be ready to buy when stock prices plunge: Markets typically tank in recessions. Use the cash you raised from selling your garbage holdings and develop a plan of action while you are still calm and objective. Have the confidence to act when the time comes.

It can be simple, too. For example, plan on deploying your cash in tranches: Buy a U.S. index fund when markets are down 20 to 25%; add a developed global index fund when markets fall by 30%. And if we are lucky enough to enjoy a 35 to 40% decline (that's assuming you prepared for this moment), buy emerging-market stocks.

The trick to create this plan NOW, set some alerts and be prepared to put the cash to work when the predetermined levels are hit. You might look (and feel) foolish for a few months, but seem like a genius a few years later.

No. 4. Check and clean up your credit score: I found an erroneous blemish on my credit rating some time ago that took two years of arduous work to remove. Improving your credit score allows you to borrow at more advantageous prices. This helps if you want to refinance when mortgage rates drop, which usually happens during recessions, or take advantage of falling prices to buy a home. Improve your credit score when you don’t have to.

I hope I am wrong, and we don’t see a recession for a long time to come, although that seems unlikely. But even if we are fortunate enough to never have another recession, all of the steps described above will serve to help you get your financial house in order and make you a better investor.

Harvey says the model has delivered no false signals in the modern era, and a variety of out-of-sample evidence has also validated the model.

<<<

>>> Barry Ritholtz is a Bloomberg Opinion columnist. He founded Ritholtz Wealth Management and was chief executive and director of equity research at FusionIQ, a quantitative research firm. He is the author of “Bailout Nation" <<<

>>> Powell’s Concern Over Zero Rates Expected to Lower Bar for Fed Cut

Bloomberg

By Craig Torres

June 16, 2019

https://www.bloomberg.com/news/articles/2019-06-16/powell-s-concern-over-zero-rates-seen-lowering-bar-for-fed-cut?srnd=premium

Fed chairman says extending expansion an ‘overarching’ goal

No interest rate move expected when officials meet this week

Chairman Jerome Powell’s frequent assurance that sustaining the U.S. economic expansion is the Federal Reserve’s “overarching’’ goal is opening the door to potentially aggressive interest-rate cuts.

The timing, size and whether such moves are indeed in his plans may become clearer when Powell and his colleagues meet on Tuesday and Wednesday in Washington.

While investors are agitating for the Fed to shift, economists don’t see a move this week and are divided on whether officials will cut at all in 2019. The median estimate of Bloomberg’s most recent survey shows a quarter point reduction in December, though it was a close call.

Policy rate has been closer to zero compared with any expansion since 1950s

The suspicion of a number of Fed watchers, though, is that the hint of a slowdown would be enough for the Fed to move, and that policy makers will acknowledge that readiness this week. One reason is that the chairman has signaled he’s concerned about how just low rates still are, meaning it may be better to act sooner and avoid a recession than wait and find the economy slumping with the Fed having limited room to act.

Prospects for a shift have mounted in recent weeks as President Donald Trump’s trade war with China has escalated and the U.S. economy had displayed some signs of weakness.

“They will be very reactive if the data even confirms a small amount of slowing,’’ said Priya Misra, global head of interest rate strategy at TD Securities. “They are going to be more pre-emptive and more aggressive. They will open the door for a rate cut’’ at the meeting this week.

That perspective of Fed policy has a lot to do with Powell’s perception of risk at a time of high uncertainty and Trump’s dispute with China.

The Fed’s benchmark policy rate has never been this low during a prolonged economic expansion in records going back to the 1950s. That means when the next recession occurs rates will be closer to the zero limit: in effect, U.S. central bankers have less room to cut.

The Fed chairman described the zero boundary as “the preeminent monetary policy challenge of our time, tainting all manner of issues’’ in a speech in Chicago this month.

Fed watchers read those words as a new trigger point for the central bank. It won’t take an overwhelming confirmation of weakness in data for the Fed to ease, in their view, and a sense that risks are particularly heightened might be enough to prompt a move.

“The bar for precautionary cuts is lower if you are worried about the zero lower bound,’’ said Michael Gapen, chief U.S. economist at Barclays Plc, which predicts 0.75 percentage points of easing this year, one of the most aggressive calls on Wall Street.

That said, economists are still parsing how much weight the Fed will put on the economic data in hand versus risks and uncertainties, and there isn’t much consensus. Twelve firms expect at least one cut this year, the Bloomberg survey showed, while 12 expect two cuts. Sixteen firms expected no cut at all, and two projected a hike.

“I am hard pressed to figure out what all the fuss is about,’’ said Ward McCarthy, chief financial economist at Jefferies LLC, who expects rates to remain unchanged this year. “I think the slowdown’’ in the data now “is the slowdown we are going to get.’’

Monthly job growth in 2019 has slowed to an average of 164,000, down from 230,000 in the first five months of 2018. Job openings remain near record highs and consumption is holding up, but concerns over tariffs have hit household confidence. It all paints a picture of an economy that’s down-shifted a bit with inflation below the Fed’s 2% target.

“We see weak inflation impulses,’’ said Julia Coronado, founder of MacroPolicy Perspectives LLC, who forecasts two rate cuts this year. “It is not like the consumer has rolled over, but you are now seeing a slowing in the pace of growth that makes the economy look more vulnerable to the uncertainties ahead.’’

Perhaps the biggest source of uncertainty is Trump. World leaders meet in Osaka for the G-20 summit later this month, and investors hope for fresh trade talks between the U.S. and China.

Anything short of a clearly positive reset between Trump and Chinese President Xi Jinping would weigh on business confidence and investment as it could upset supply chains and roil markets. That risks a steeper slowdown in U.S. growth that Fed officials won’t tolerate, warned Barclays economists, who predict a 0.50 percentage point cut as soon as July.

Fed independence will also be on Powell’s mind. Trump has relentlessly attacked the central bank for months for having tightened too far, including a fresh broadside on Friday.

If rates were lowered back to zero, the Fed would have to return to emergency-era policies such as buying bonds, an unpopular measure with lawmakers of both parties.

“In the long wake of the crisis, they just don’t have that much political capital to fall back on. Add to that unprecedented presidential pressure and party polarization and it gets ugly,” said Mark Spindel, co-author of a recent book about the Fed’s relations with Congress. “They are the only game in town -- and they are without deep pockets or ammo” to address the next recession.

<<<

>>> Opinion: This is the only protection your stock-market investments will ever need

MarketWatch

By Howard Gold

May 30, 2019

https://www.marketwatch.com/story/this-is-the-only-protection-your-stock-market-investments-will-ever-need-2019-05-30?siteid=yhoof2&yptr=yahoo

Bonds are the simplest and cheapest way to hedge your investment portfolio

As the Dow Jones Industrial Average DJIA and S&P 500 index have fallen more than 5% from their recent highs, investors have rushed toward safety. Funds that aim to lower risk and limit stock market losses raised almost $10 billion in the first four months of 2019, The Wall Street Journal reported.

But there’s a much simpler, cheaper way to hedge your stock-market investments — bonds. And they’ve been the most effective way to do that for more than a decade. Recently, haven buyers have scooped up 10-year Treasury notes, driving yields down a full percentage point since last October, to as low as just above 2.20% at one point Wednesday.

New research by Christine Benz, Morningstar’s director of personal finance, confirmed the superiority of bonds — especially Treasurys — as hedges over the long run.

Benz looked at asset classes traditionally considered stock-market hedges over different periods, from one year to 15 years. She used Morningstar Direct’s database and stuck mostly to funds and ETFs available to institutional and individual investors.

Benz looked at the correlation coefficient between different pairs of asset classes over time. That’s a number between -1 and 1 that measures how closely two variables move together. A correlation of 1 means the two are perfectly in sync, 0 means no correlation, and -1 means the two are going in the opposite direction. In short, it tells us how much other assets have zagged when stocks zigged, and vice versa. Ideally, to hedge your equity risk, you’d want something that has as negative a correlation with the S&P 500 as possible.

“The goal is when stocks tumble, that you have something in your portfolio with the ability to at least hold its ground, or maybe even earn a little bit,” said Benz. That’s important for maximizing your holdings’ long-term growth.

This table tells the story.

Bonds: The best hedge

Correlation - 5-year, 10-year, 15-year

Asset class

Real estate 0.57 0.69 0.74

SPDR Gold Shares (GLD) -0.18 0.06 NA

Managed futures 0.12 0.22 NA

Cash 0.04 -0.01 -0.11

U.S. Aggregate Bond -0.05 -0.13 0

U.S. Treasury 20+ Year -0.18 -0.46 -0.3

U.S. Treasury 5-10 Year -0.28 -0.37 -0.28

Real estate, often recommended as a portfolio diversifier, actually is highly correlated with stocks — 0.74 over 15 years. Managed futures, which have been touted by some investment advisers, are mediocre hedges at best, showing positive correlations with stock prices. Developed and emerging markets international stocks had similarly high correlations with U.S. equities over the past 10 to 15 years, as did high-yield bonds. Long-only commodities also were highly correlated with stocks — 0.4 to 0.5.

Gold GLD was an excellent hedge over the past five years and cash did its job over the last 15; both were solidly in negative territory over those periods.

Then there were two categories — long-short equity and market-neutral — that supposedly mimic the strategies of hedge funds. Their high correlation with stocks (up to 0.97 for long-short and 0.47 for market-neutral) point to why the only thing hedge funds have successfully hedged against over the past decade has been good returns.

But the big winner across the board was bonds. The Bloomberg Barclays U.S. Aggregate Bond index AGG, which covers a broad swath of Treasury, agency, and investment-grade corporate bonds, had zero correlation with stocks for 15 years, but negative correlations over five and 10 years.

Treasurys did even better protecting against equity risk, and here’s the big surprise: Treasurys with maturities longer than 20 years weren’t much better at protecting your portfolio than intermediate-term Treasurys; over the past five years, they did worse.

That’s great news for investors, because intermediate-term Treasurys — those with maturities of five to 10 years — are less interest-rate-sensitive and less volatile than long bonds.

In that category, I like the Vanguard Intermediate-Term Treasury ETF VGIT, the SPDR Bloomberg Barclays Intermediate Term Treasury ETF ITE, or the Schwab Intermediate-Term U.S. Treasury ETF SCHR. All have full exposure to intermediate Treasurys and rock-bottom expense ratios.

Bonds haven’t always been good hedges; in the four decades before the 1990s, stocks and bonds had positive correlations, a study by Graham Capital Management found. But I doubt the complex alternative investing products the ETF industry has concocted over the past few years would have done better — if anybody can figure out how they actually work.

“So, the takeaway is that for most investors, at least based on…history, simpler and cheaper has been better than investing in alternatives,” said Benz.

Nobel Prize-winning economist Harry Markowitz reportedly called diversification “the only free lunch in finance.” If that’s true, then bonds, especially Treasurys, are the only free dinner.

<<<

>>> The Fed May Have No Choice But to Bail Out Trump

The stage is set for an interest-rate cut, but probably not until September.

Bloomberg

By Tim Duy

June 6, 2019

https://www.bloomberg.com/opinion/articles/2019-06-06/the-fed-may-have-no-choice-but-to-bail-out-trump

The U.S.-China trade war may force the Federal Reserve to cut rates.

Federal Reserve Chair Jerome Powell addressed nervous market participants this week by assuring them that the central bank “will act as appropriate” to keep the U.S. expansion on track. This wasn’t a signal that a rate cut is imminent. It was, however, a clear signal that the bar to lowering rates is fairly low. Considering the growing risks to the outlook, the Fed only needs a push to justify a cut. The push will likely come in the form of softer economic data, but could also be a severe bout of financial turmoil.

Fed officials have resisted sending signals about the direction rates, assigning equal possibilities of either an increase or a cut. The shifting balance of risks, however, make that an increasingly difficult story to sell. The escalation of trade wars from China to Mexico create substantial uncertainty for the outlook, and none of it good.

Some complain that the Fed would only be bailing out President Donald Trump in his ill-advised use of tariffs by cutting rates. Such charges will fall on deaf ears at the Fed. Policy makers may not like responding to Trump’s escapades with easier policy, but they ultimately have little choice but to do so. The Fed responds to shocks in a systematic fashion, even those created by the government. The Fed will respond to this shock with easier policy as they seek to sustain the expansion and meet their employment and inflation objectives.

Won’t the inflationary impact of tariffs stay the Fed’s hands when it comes to rate cuts? Most likely not. First, the Fed views tariffs as a temporary price shock expected to fade over time. They will look through any acceleration in inflation.

Second, Fed officials adhering to a symmetric price target will tolerate inflation overshoots to the same degree they tolerate undershoots. In practice, this means that just like they have not pursued an excessively easy policy to push the rate inflation back up to their 2% target, they will not pursue an excessively tight policy to push it back down. Going forward we may see a distribution of inflation outcomes centered above 2%. This would have the benefit of proving the Fed’s inflation target is in fact symmetric.

Third, the Fed will err on the side of caution. The Fed is well aware of the dangers of the zero bound in rates. I suspect that those dangers will lead them to conclude that the policy risks are very asymmetric. Their tools will prove more effective at pulling down an inflation overshoot in the future relative to stimulating the economy at the zero bound. There is much to be said for an insurance rate cut, especially at this challenging point in the business cycle where growth is slowing and companies worry that they should be retrenching in anticipation of the next recession.

The Fed, however, still needs to see greater evidence that growth is in fact slowing as forecast. Policy makers do not see large macro impacts from tariffs, which makes it difficult to justify substantial changes to the outlook on tariffs alone. Moreover, while we have seen some softness in the data, it is not excessive. The Institute for Supply Management’s manufacturing report for May showed that the sector was still expanding. The ISM’s services report, covering the much larger sector, revealed that activity, including hiring, accelerated in May.

In contrast, the ADP Research Institute’s employment report indicated that job growth slowed in May. A sustained slowdown in job growth would go a long way toward justifying a rate cut. The ADP number, however, is not always a reliable signal. The Fed will pay much more attention to the Labor Department’s employment report for May that comes Friday. But even there one weak number will be seen as an outlier, not a trend. The Fed typically needs a wider range of data to shift gears.

Although the stage is set for the Fed to cut rates, policy makers won’t have sufficient data to act until the end of the summer. A move at the September meeting is a reasonable baseline at this point. If the data deteriorate more quickly, or if markets seize up, pull that cut forward into July. If trade tensions ease and growth stays strong, push it back.

<<<

Performance comparison of HDGE, short S+P ETFs, and long Treasury ETFs during the big December swoon -

S+P 500 (SPX) - down 16%

________________________

HDGE - up 19%

1X Short S+P (SH) - up 19%

2X Short S+P (SDS) - up 40%

3X Short S+P (SPXS) - up 69%

________________________

1X Long 20+ year Treasuries (TLT) - up 8%

3X Long 20+ year Treasuries (TMF) - up 22%

________________________

So while the Treasury approach won't give you the best 'bang for the buck' for short term trading, as an asset allocation tool to reduce risk and overall volatility, Treasuries work well.

>>> Asset Allocation for Beginners

An Introduction to Diversifying Between Asset Classes

BY JOSHUA KENNON

December 30, 2018

https://www.thebalance.com/asset-allocation-basics-357311

In its simplest terms, asset allocation is the practice of dividing resources among different categories such as stocks, bonds, mutual funds, investment partnerships, real estate, cash equivalents, and private equity. The theory is that the investor can lessen risk because each asset class has a different correlation to the others; when stocks rise, for example, bonds often fall. At a time when the stock market begins to fall, real estate may begin generating above-average returns.

The amount of an investor’s total portfolio placed in each class is determined by an asset allocation model. These models are designed to reflect the personal goals and risk tolerance of the investor. Furthermore, individual asset classes can be sub-divided into sectors (for example, if the asset allocation model calls for 40% of the total portfolio to be invested in stocks, the portfolio manager may recommend different allocations within the field of stocks, such as recommending a certain percentage in large-cap, mid-cap, banking, manufacturing, etc.)

Model Determined by Need

Although decades of history have conclusively proved it is more profitable to be an owner of corporate America (viz., stocks), rather than a lender to it (viz., bonds), there are times when equities are unattractive compared to other asset classes (think late-1999 when stock prices had risen so high the earnings yields were almost non-existent) or they do not fit with the particular goals or needs of the portfolio owner. A widow, for example, with one million dollars to invest and no other source of income is going to want to place a significant portion of her wealth in fixed income obligations that will generate a steady source of retirement income for the remainder of her life.

Her need is not necessarily to increase her net worth but to preserve what she has while living on the proceeds. A young corporate employee just out of college, however, is going to be most interested in building wealth. He can afford to ignore market fluctuations because he doesn’t depend upon his investments to meet day to day living expenses. A portfolio heavily concentrated in stocks, under reasonable market conditions, is the best option for this type of investor.

Model Types

Most asset allocation models fall somewhere between four objectives: preservation of capital, income, balanced, or growth.

Preservation of Capital.

Asset allocation models designed for the preservation of capital are largely for those who expect to use their cash within the next twelve months and do not wish to risk losing even a small percentage of principal value for the possibility of capital gains. Investors that plan on paying for college, purchasing a house or acquiring a business are examples of those that would seek this type of allocation model. Cash and cash equivalents such as money markets, treasuries, and commercial paper often compose upwards of eighty percent of these portfolios. The biggest danger is that the return earned may not keep pace with inflation, eroding purchasing power in real terms.

Income.

Portfolios that are designed to generate income for their owners often consist of investment-grade, fixed income obligations of large, profitable corporations, real estate (most often in the form of Real Estate Investment Trusts, or REITs), treasury notes, and, to a lesser extent, shares of blue-chip companies with long histories of continuous dividend payments. The typical income-oriented investor is one that is nearing retirement. Another example would be a young widow with small children receiving a lump-sum settlement from her husband’s life insurance policy and cannot risk losing the principal; although growth would be nice, the need for cash in hand for living expenses is of primary importance.

Balanced.

Halfway between the income and growth asset allocation models is a compromise known as the balanced portfolio. For most people, the balanced portfolio is the best option not for financial reasons, but for emotional. Portfolios based on this model attempt to strike a compromise between long-term growth and current income. The ideal result is a mix of assets that generate cash as well as appreciates over time with smaller fluctuations in quoted principal value than the all-growth portfolio. Balanced portfolios tend to divide assets between medium-term investment-grade fixed income obligations and shares of common stocks in leading corporations, many of which may pay cash dividends. Real estate holdings via REITs are often a component as well. For the most part, a balanced portfolio is always vested (meaning very little is held in cash or cash equivalents unless the portfolio manager is absolutely convinced there are no attractive opportunities demonstrating an acceptable level of risk.)

Growth.

The growth asset allocation model is designed for those that are just beginning their careers and are interested in building long-term wealth. The assets are not required to generate current income because the owner is actively employed, living off his or her salary for required expenses. Unlike an income portfolio, the investor is likely to increase his or her position each year by depositing additional funds. In bull markets, growth portfolios tend to outperform their counterparts significantly; in bear markets, they are the hardest hit. For the most part, up to one hundred percent of a growth modeled portfolio can be invested in common stocks, a substantial portion of which may not pay dividends and are relatively young. Portfolio managers often like to include an international equity component to expose the investor to economies other than the United States.

Changing with the Times

An investor that is actively engaged in an asset allocation strategy will find that his or her needs change as they move through the various stages of life. For that reason, some professional money managers recommend switching over a portion of your assets to a different model several years prior to major life changes. An investor that is ten years away from retirement, for example, would find himself moving 10% of his holding into an income-oriented allocation model each year. By the time he retires, the entire portfolio will reflect his new objectives.

The Rebalancing Controversy

One of the most popular practices on Wall Street is “rebalancing” a portfolio. Many times, this results because one particular asset class or investment has advanced substantially, coming to represent a significant portion of the investor’s wealth. To bring the portfolio back into balance with the original prescribed model, the portfolio manager will sell off a portion of the appreciated asset and reinvest the proceeds. Famed mutual fund manager Peter Lynch calls this practice, “cutting the flowers and watering the weeds.”

What is the average investor to do? On the one hand, we have the advice given by one of the managing directors of Tweedy Browne to a client that held $30 million in Berkshire Hathaway stock many years ago. When asked if she should sell, his response was (paraphrased), “has there been a change in fundamentals that makes you believe the investment is less attractive?” She said no and kept the stock. Today, her position is worth several hundred millions of dollars. On the other hand, we have cases such as ?Worldcom and Enron where investors lost everything.

Perhaps the best advice is only to hold the position if you are capable of evaluating the business operationally, are convinced that the fundamentals are still attractive, believe the company has a significant competitive advantage, and you are comfortable with the increased dependence upon the performance of a single investment. If you are unable or unwilling to commit to the criteria, you may be better served by rebalancing.

Strategy

Many investors believe that by merely diversifying one’s assets to the prescribed allocation model is going to alleviate the need to exercise discretion in choosing individual issues. It is a dangerous fallacy. Investors that are not capable of evaluating a business quantitatively or qualitatively must make it absolutely clear to their portfolio manager that they are interested only in defensively selected investments, regardless of age or wealth level.

<<<

S&P 500 PE Ratio - 90 Year Historical Chart

https://www.macrotrends.net/2577/sp-500-pe-ratio-price-to-earnings-chart

S&P 500 Index - 90 Year Historical Chart

(this chart shows why investors need at least some allocation to stocks)

https://www.macrotrends.net/2324/sp-500-historical-chart-data

>>> Vanguard Patented a Way to Avoid Taxes on Mutual Funds

By Zachary R. Mider, Annie Massa and Christopher Cannon

May 1, 2019

https://www.bloomberg.com/graphics/2019-vanguard-mutual-fund-tax-dodge/?srnd=premium

Like flipping a light switch, Vanguard Group Inc. has figured out a way to shut off taxes in its mutual funds.

The first to benefit was the Vanguard Total Stock Market Index Fund. Investors’ end-of-year tax forms abruptly stopped showing capital gains in 2001, even as the fund went on to generate billions of dollars of them. By 2011, Vanguard had flipped the switch in 14 stock funds. In all, these funds have booked $191 billion in gains while reporting zero to the Internal Revenue Service.

This astounding success gives Vanguard funds an edge over competitors. Yet the world’s second-largest asset manager has avoided drawing attention to it. Top executives at the Malvern, Pennsylvania-based firm don’t want U.S. policymakers looking too closely at how they’re doing it, according to a former insider.

But a review of financial statements and trading data shows that Vanguard relies substantially on so-called heartbeat trades, which wash away taxes by rapidly pumping stocks in and out of a fund. These controversial transactions are common in exchange-traded funds—a record $98 billion of them took place last year, according to data compiled by Bloomberg News—but only Vanguard has used them routinely to also benefit mutual funds.

Here’s how it works: Vanguard attaches a more tax-efficient ETF to an existing mutual fund. Then the ETF siphons appreciated stocks out of the mutual fund without incurring taxes, often using heartbeat trades. Robert Gordon, who has written about the concept and is president of Twenty-First Securities Corp. in New York, calls it a tax “dialysis machine.”

How to Spot a Heartbeat

Rapidly pumping money into and out of the exchange-traded portion of the Vanguard Small-Cap Index Fund removes taxable gains for the benefit of the mutual fund’s shareholders.

Vanguard even got a patent on the design, valid until 2023, so competitors can’t copy it.

Rich Powers, Vanguard’s head of ETF product management, acknowledged the design’s tax advantages. But he said in an interview that they’re not the driver of the company’s strategy and that all of its trading complies with the law.

“We agree the Vanguard funds have been extremely tax efficient, enabling us to provide higher after-tax returns to our shareholders and better their chances of achieving long-term investment success,” Freddy Martino, a spokesman for the company, said in an email.

Although the dialysis treatment shut off taxable gains in the 14 stock funds, it didn’t completely neutralize them in a separate real estate index fund, which invests in trusts that aren’t taxed like stocks.

Taxable Gains Begone

Unlike competitors that follow similar indexes, Vanguard mutual funds stopped saddling investors with ? taxable gains once ETF share classes were added.

The main benefit of avoiding taxable gains in a mutual fund is tax deferral. Funds distribute their taxable gains to investors, who pay income taxes on them in the same year. By avoiding tax events within the fund, investors get to delay taxes until they sell the fund, which could be years or decades later. It’s akin to a zero-interest loan from the IRS.

The stakes for the U.S. Treasury are significant. While heartbeats already help eliminate taxable-gain distributions in the $3 trillion U.S. equity ETF industry, the mutual fund market is more than three times as big. When Vanguard’s patent expires four years from now, other mutual fund managers may have the chance to build their own dialysis machines.

To understand how the process works, consider an investor who owns a portfolio of stocks. If one is sold for more than what it cost, capital-gains tax is due on the difference.

Theoretically, owning stocks through a mutual fund or ETF works the same way. If the fund sells a stock for a profit, the taxable gain shows up on each investor’s end-of-year Form 1099.

But thanks to an obscure loophole in the tax code, ETFs almost always avoid incurring taxable gains.

The rule says that a fund can avoid recognizing taxable gains on an appreciated stock if the shares are used to pay off a withdrawing investor. The rule applies to both ETFs and mutual funds, but mutual funds rarely take advantage of it because their investors almost always want cash.

ETFs use it all the time, because they don’t transact directly with regular investors. Instead, they deal with Wall Street middlemen such as banks and market makers. It’s those firms, not retail investors, that expand the ETF by depositing assets or shrink it by withdrawing. These transactions are usually done with stocks rather than cash. The middlemen, in turn, trade with regular investors who want to buy and sell ETF shares.

Trading with middlemen presents ETFs a tax-cutting opportunity. Whenever one of these firms makes a withdrawal request, an ETF can deliver its oldest, most appreciated stocks, the ones most likely to generate a tax bill someday.

If the ETF wants to cut its taxes further, it can generate extra withdrawals just to harvest the tax break. A heartbeat is when an ETF asks a friendly bank or market maker to deposit some stock in the fund for a day or two, then take different stock out. Some critics call these trades an abuse of the tax code. But with the help of heartbeats, most stock ETFs, even ones that change holdings frequently, are able to cut their capital-gains taxes to zero.

Customer-owned Vanguard, founded in 1975 by John Bogle, built a reputation for low fees and tax efficiency by offering simple buy-and-hold funds that follow broad indexes such as the S&P 500. It now has about $5 trillion of assets under management.

In 2000, after Bogle had stepped down as chief executive officer, the firm unveiled a novel strategy to enter the ETF business, a market dominated by State Street Corp. and iShares, now part of BlackRock Inc. Rather than establish new, freestanding ETFs, Vanguard proposed to add an ETF share class to existing mutual funds. ETF and mutual fund investors would jointly own the same underlying pool of stocks.