News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

BioHunter

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

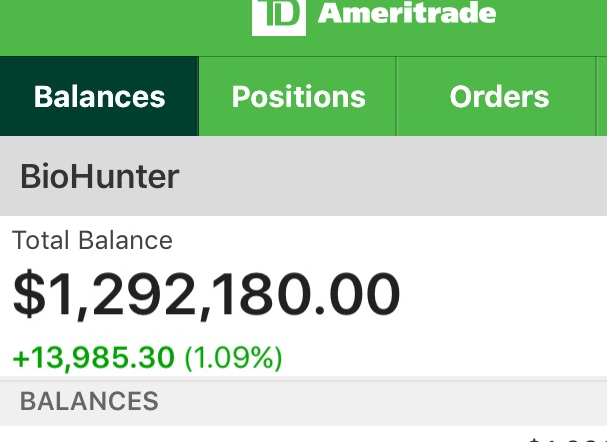

Year End final numbers:

I thought I would post my final numbers for BioHunter 2017. I realize Sheff and I are not on the Ihub platform much, but thought I should close out the year with everyone on the board.

It was my best trading year particularly given the starting number, it gets harder to put up big percentage years when the total account assets gets larger.

So here is the final screen cap 2017, up over 200% 2017

12/29/31 last day of trading 2017:

I don't know how to make the screen caps smaller so sorry they are jumping off the page, not my intent.

Start 2017 January 1

3/31/2017 Q1

6/30/2017 Q2

9/30/2017 Q3

12/29/2017 Q4

*all screen caps posted earlier through out the year on SheffStation Board.

* added $300K in June 2017

-Biohunter

@TheBio_Hunter

$PIOE Posting here I have exited my full position of $PIOE. It took a while to exit, average sale price near current levels.

My central concern is lack of disclosure by management. That is a significant red flag and prevents proper modeling of value. Stock could be worth more although the risk/reward has changed.

I will not be posting further unless something materially changes my valuations views.

Good luck to all

-BioHunter

Float Estimate...

The float should be the same (in number of shares) as it has been since the 210 Capital investment post bankruptcy in April/May.

210 Capital was diluted by the issuance of shares in connection with the acquisition of RCP Advisors 2, LLC and now owns roughly 24% of the company.

If 210 Capital & RCP are taken out of the calculation, that leaves plus or minus 23.5m shares that are potentially out there.

Assuming that Kinderhook, Asen, and Ascolese (options) are still holding (which past volume and filings would indicate that they are), that takes it down to 16.5m.

Although the 16.5m number is an educated guess, it does not include others who one or more potential large owners with under 5% which would not have been required to report who could hold

north of 2m shares each (a significant portion of the float)

Keep in mind that 210 Capital can now acquire substantially more shares in the open market (or privately from Kinderhook or Asen) without risking the NOLs and they as the board can approve any purchase although it is restricted by the charter amendment.

On the flip side, Kinderhook and Asen are now below the restriction point in the charter amendment and can purchase more shares. The same holds true for a large investor that was just below the 5% threshold.

All of that said, I would estimate the float to be between 10m - 15m or 11% - 16% of total shares

-BioHunter

PIOE M&A RCP

The part of RCP which we are interested in here is only their Advisory Business which as of the year ended 2016 managed roughly $4.0 Billion on a discretionary basis and $467 Million on a non-discretionary basis, primarily providing services to the various RCP Private Equity Funds and a small amount of SMA (Separately Managed Account) business.

The Advisory Business is conducted under a combination of three Delaware LLCs:

RCP Advisors, LLC

RCP Advisors 2, LLC

RCP Advisors 3, LLC

In December of 2016, RCP Advisors 2, LLC went thru some ownership changes and prior to its sale to PIOE was owned by its Managing Partners - Thomas Danis, Jr., Jeff Gehl, Charles Huebner, Jon Madorsky and William Fritz Souder.

During 2016, RCP Advisors 3, LLC was formed and the employees of RCP Advisors 2, LLC were transferred to the new entity, which is owned by the same managing partners as RCP Advisors 2, LLC with the addition of David McCoy (who joined RCP in November 2010) and several other unnamed partners of RCP.

RCP was founded in 2001 and since its inception, the Advisory Business to its Private Equity Funds is allocated among the three LLCs as follows:

RCP Advisors, LLC - (Funds formed prior to 2011)

RCP Advisors 2, LLC - (Funds formed between 2011 - 2015)

RCP Advisors 3, LLC - (Funds formed after 2015)

Although each of the respective entities is the Advisor for the funds formed during the aforementioned time period, RCP Advisors 3, LLC is considered the sub-advisor for each since it is the entity which all of the employees work for and covers the combined overhead expenses for all three entities, it appears to be the only operating entity of the three.

For the services that RCP Advisors 3, LLC provides to the other two entities, it is paid a portion of the management fees the collect from the respective underlying funds.

As a general rule, all of the RCP Funds pay an annual Management Fee of 1.0% percent to one of the three entities (depending on when the fund was formed) based on the total committed capital for the fund (even if it is not fully raised from the investors)

The focus today is on RCP Advisors 2, LLC, which is most likely collecting 1.0% of the committed capital of the various RCP Funds formed between 2011 - 2015 and paying an unknown amount to RCP Advisors 3, LLC for the employees and overhead it provides.

All of that said, based on the details available it is hard to place a valuation on the acquisition until more information is given, most importantly how much PIOE paid for this deal. My assumption is stock is not yet fairly valued.

-BioHunter

@TheBio_Hunter

For those who were patient ENJOY the day! Hopefully my DD and others helped you click your heels today!

Exit targets are difficult given what has been disclosed, so I will not comment on when or where to harvest.

-BioHunter

@TheBio_Hunter

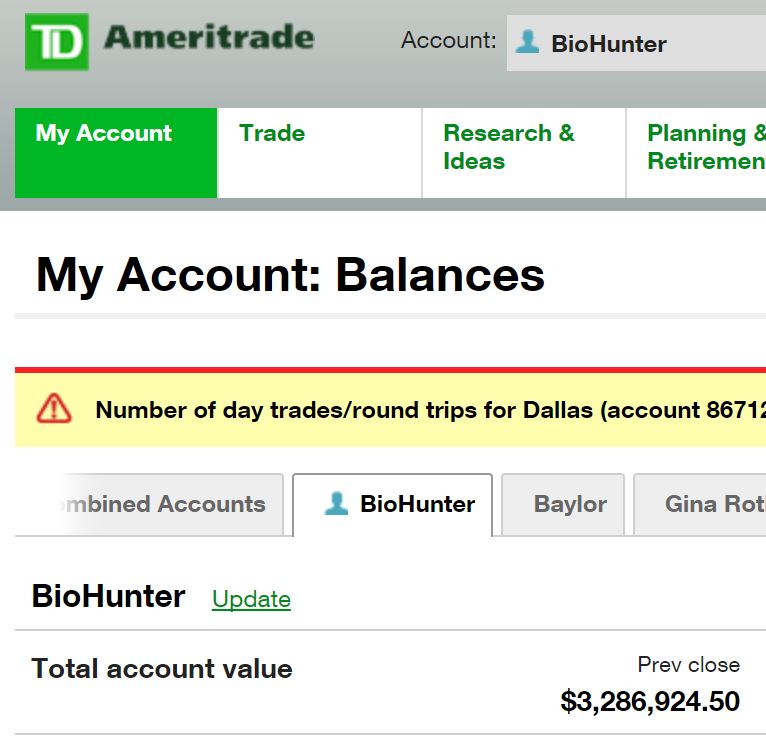

Q3 results+ YTD+ some thoughts on makret

Hi, I have not posted much on the board as it seems like Sheff and I are more focused on twitter. But I thought I would circle back to the board at the close of Q3. See results below

Highlights:

Q3 34% return

YTD 139%

Portfolio Value $3,286,924

Recap:

July through mid August was more or less flat to somewhat positive, but 2H of Q3 everything seemed to work. My patience on $VYGR, $STML, $EIGR really paid off. Traded $NEOS, $ACRX, $MRNS multiple times with big gains. Other trades that were big winners $FENC, $KURA,$RXDX,$FGEN,$FCSC, $DVAX. There were other smaller trades as well. On the negative side $VSAR was a blow up, but reasonable risk management, went into data with 2% PV position, but sold at the money calls against to lower risk. $ZGNX was also a recent loser as I played the straddle, making a profit between $2 and $28. I panicked a little bit in pre-market and covered mid 30's. I had others that did not work $EYEG, $CPRX, $AMRN...

Market is rewarding data and PDUFA runs. Seems like anything with a hard catalyst is really ripping. For example $RDHL, $CAPR, $EARS they offer a specific catalyst date they are going up 20%+ What works and what is not working always changes in the market, currently SheffStation style catalysts trades are working. Especially with tute support and hard catalyst dates.

Q4 Plays:

$STML - my largest position at 10% - I expect they will announce cohort 3 Nov 1 around the time late breaker abstracts do for ASH. I think we see mid teens and expect very good data

$BLRX - been holding this one a bit long but data Q4, I like their 8040 compound

$EARS with specific catalyst date I expect this to run to $1+ before p3 read late November.

$RXDX October data at IALSC conference 10/15-18 with great tute buying/support expect it to doe well Q4

$AGRX - PDUFA 12/26 I expect early approval, I have been trying to build a position.

$ATRS PDUFA 10/17, joining Sheff on this one

$COLL upcoming PDUFA 11/4 with high short interest, this could really run

$CRMD - expecting DSMB decision Q4 if they stop early which I think is possible, but maybe not my base case this one will rip.

$EIGR - 7% potion two big catalyst data reads, late October and JPM healthcare HDV data.

$FENC 8% position full data in two weeks at SIOP 10/14. They will have top line data on their P3 SIOPEL 6 trial, I fully expect great data and stock to revalue higher.

Q3-17

Q2-17

Q1-17

Start 2017:

*Note took posted this after week 1, so 12/31/16 value $1,250,000

-BioHunter

@TheBio_Hunter

In case you missed it

http://secfilings.nasdaq.com/filingFrameset.asp?FilingID=12225533&RcvdDate=8/10/2017&CoName=GLOBALSCAPE%20INC&FormType=4&View=html

210 Capital took advantage of the price drop. Essentially gabbed 50% of the volume over 2 days.

-BioHunter

Ps: I am not saying P10 and $GDB get together. Certainly tied together via 210 cap

Yes,

I follow and had a 2 hour meeting with CEO back in the spring. I don't see how one can invest today. They have a major cash problem, combined with low market cap and no catalysts until 2018. The problem is any cash raise will be massively dilutive given their market cap. I like management and think they have a reasonable chance as success. But I don't see why one would own it today.

An unexpected day, some nice wins

I thought I would post to support others on the board trying to make dollars in bio. It can be really really hard at times. 2016 was brutal, volatility was massive, just ending the year positive was an achievement much less Sheff up 40%. I am posting my results to encourage others and say it can be done!

A few takeaways from today - PATIENCE and CONVICTION are important parts of trading bios. For ex

$STML - big breakout today. Most know I have been somewhat pounding the table on this one since trial deaths announced in February causing the move from $10 to $5. It's still cheap IMO as I fully expect it to hit $14/15 by xmas, post cohort 3 data. But it's a trade that has taken time to play out aka PATIENCE

$NEOS - I know this name well, spent tons of DD time on it and had booked nice profits along the way. But during the move from 8 to 7 I was buying, then the move to 6.50 yesterday I also was a strong buyer aka CONVICTION

$PIRS - most know I have been pounding the table on this from early 2016 and it took a long time to play out, but $1.41 to $6 is worth it. CONVICTION and PATIENCE.

SHEFFSTATION: The board is less active I should post more DD,sorry :) but the important takeaway is Sheff's style works. Don't get greedy target 12% to 25% and move on. Don't "look back!" It is part of our success, sure we leave profits on the table, but when you "look back" it leads to a bigger mistake aka GREED which too often leads to BUST!

1) DD - you can't just follow a trade you have to understand the name.

2) CATALYST - this market is missing generalist. Pharma trading at historically low PE levels, so unless you get a over riding bid from market generalist, you really need catalyst to drive shares price. Plus these Bios burn so much cash and management is often overly optimistic since they are always begging for cash, catalyst are key.

3)Take Profits, take profits, take profits... you got it?

4) Don't hold through catalyst - or do at your own peril, think of how rare it is that Sheff or I hold through a catalyst. Generally if we do it's a small percentage or where we have seen a good bit of data, such a "cohort 3 data" On the other hand $IPCI and $DVAX I would never hold through an ADCOM, way too much risk around FDA. Plus lack on management disclosures around FDA feedback prior to ADCOM creates tons of risk.

Today's gains :) good example of all the above trading points

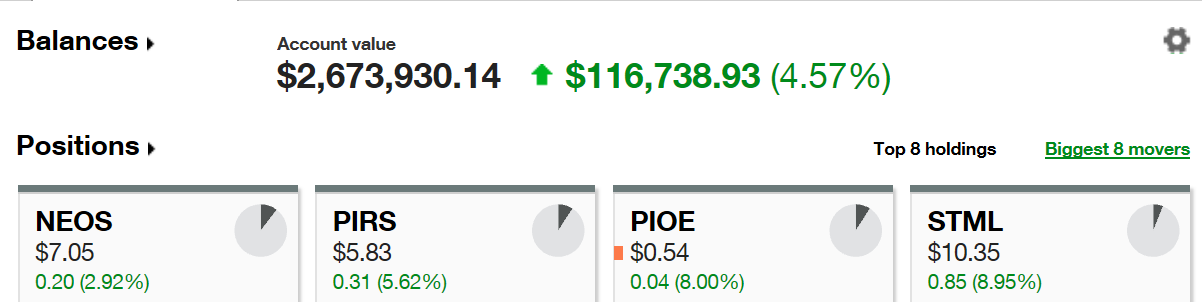

Current plays besides the ones in the jpeg.

$ABIO, $AXSM, $ACRX, $EARS,$AXON, $FGEN, $PRTK, $RPRX, $VYGR, $CLRB, $KMDA, $AXON. $AFMD, $AMRN... that's a lot of ticker's with "A"'s kind of funny actually.

Took profits today as well

$DVAX, $CERC (2/3), $EIGR (sm. pos.), $STML (1/4), $PRTK (1/3)

Good luck and trade well!

-BioHunter

@TheBio_Hunter

$EIGR

Revisiting this here, on my watch for a 2H play.

-Loaded with catalyst next 12 months, 5 P2 readouts all orphin indications.

-Cash 45M est, call is Q3-18

-Market Cap 64M

-low floater 8m shares

-institutions owns 70%

-Defined catalyst date for PAH, 4 billion market today. Company will have last patient visit in Ocotber for their P2 trial with "topline results at JPM Conference in 2nd week of January." $EIGR on my watch for Fall purchase as we get closer to several catalysts.

Jefferies Conf presentation:

Jefferies Presentation June 7

-BioHunter

@TheBio_Hunter

Not a reccomendation to buy or sell, DD only

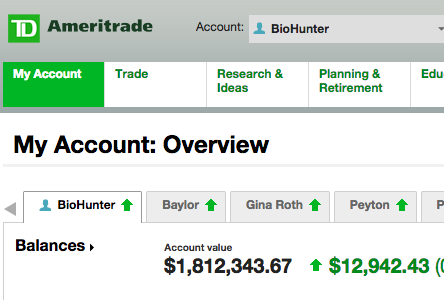

1H-2017 /Q2 SheffStation Portfolio results :)

Q2-17 YTD up 72.8% from starting value 1,250,000. Ending value $2,160,930 (actual $2,460,930 see screen cap below. Added $300k cash in May)

Another solid trading quarter, although the first two months seemed like two steps forward and 1 or 2 steps back. Hopefully my results are proof postitive that Sheff's bio trading style works!!!! I am probably a little more patient then Sheff with my trades and maybe I trade a few larger SMID's, othewise we are pretty similar. Alternatively my version of a Total Economy portfolio (mainly bio's but larger SMIDS and companies like $CELG) is also doing well, easily outperforming IBB. But it's not having a 2017 like my SheffStation BioHunter account. I am finding it's more difficult to trade my BioHunter portfolio as the account value is now almost 2.5M. (actually today's close is 2.506M!) Some of the nano cap names Sheff and I like to catalyst trade can be a bit thin on daily volume. Going into 2H, I am going to be cautious around not giving too much back, so I may be less active and move position sizes down a bit.

Q2 Winners: traded $ADMP, $STML, $SELB, $SRPT, $NEOS, $DRRX, $ITEK, $AVEO, $ZSAN, $MRNS, $RXDX, $NBIX, $BLUE, $PIRS + several others, but these stand out from memory. Some like $NEOS, $STML and $ITEK, I traded 2 or 3 different times as they offered great channel trading.

$PIOE was a massive win as well. For those that followed that trade my SheffStation account had half my total pos. I made a few post on $PIOE IHub board.

Most who follow me know I have been pounding the table on $PIRS since 2016. It's been ripping in 2017 and I will continue to hold vs trade. I have trimmed some to keep position size to 12%

$MTNB - I gave back some of my Q1 booked gains on this one, but happy with how I traded and risk management. June 3 data gave traders an opp for early look at platform tech and efficacy. Traders then had opportunity to exit for only 10% loss. So risk reward for holding until June 3 was absolutely in my tolerance window. As most know after the NIH data I assumed they would fail VVC trial.

$PSDV was frustrating, traded and booked gain from 1.70 to 2.20-2.30. Then repurchased for data and gave a bunch back.

$VYGR, $CRVS, $ECYT, $CLRB, $SKLN, $MRUS, $EIGR were my main losing trades. I am still suffering with $VYGR and $CLRB. See below on active positions.

Trading lessons - $CRVS mainly re learning known lessons. Book profits, pigs get happy hogs get slaughtered. Purchased at $13-$14 but did not take enough profits at $20's and got smashed AAN poster data. Ultimately exited $10-11. $EIGR I was not aggressive enough on exit. Stock probably too thin for my account size, got smashed on it. $VYGR and $CLRB slow bleed down action, I tend to get caught in these slow bleeders, as mental stop losses didn't trigger. I don't use actual stop losses in bios due to bear raids near data and SMID bio daily vol. So I can struggle with loss management on the slooowwww bleeders. I do like $VYGR going into 2H with key catalyst July. The news last week should dampen the main bear argument around commercial viability.

Primary Current positions 3% or more:

$EARS - starter .66 ave

$STML - solid $7.90 ave (took 35% off table after data)

$VYGR - solid $10.8x ave

$PRTK solid pos $21.75 ave

$NEOS - 11% repurchased after PDUFA $7.45 ave

$AXSM solid 5.32 ave grabbe a bunch today

$ADMS starter $16.92

$EYEG starter $1.32

$DVAX solid $9.65

$VYGR solid $10.81

$CLRB starter $2.10

$PIRS - longterm hold 12% pos

$PIOE - full pos, holding for next leg as company needs to use M&A to unlock NOL (net operating tax loss ) which is their main asset post bankruptcy. ONLY NON BIO I OWN.

I own are am watching some of these others. Current pos size too small to list. $ARNA, $RPRX, $ABIO, $ACRX,$IPCI, $CERC. Overall I am 90%+ investest here. I think we move higher after the major breakouts of $XBI and $IBB. We might retest support, even so I would still be bullish here unless IBB breaks support with volume.

-TheBioHunter

@TheBio_Hunter

Post is information only. It is not meant to be a recommendation to buy or to sell securities nor an offer to buy or sell securities. My opinions only!

Response to this post

There are two primary reasons why many of the Biotechs sitting with large amounts of NOLs do not go down the path of P10.

1. Previous Ownership Change of the Company under Section 382 (see my previous posts for more details on what constitutes an Ownership Change)

Most simplistically, in order for the Company NOLs to be used effectively (and not subject to limitations), the Company must not have undergone an Ownership Change in the past or in the process of raising capital to fund the acquisition of a profitable target.

In most cases biotech companies with undergo one or more Ownership Changes after a drug fails and larger shareholders bail out. Once this happens, it is almost impossible to remedy the NOL usage limitation.

Further, the possibility of raising the substantial capital necessary to fund an acquisition and provide that investor with enough of an equity stake to make them interested in the opportunity, will in most cases create another Ownership Change.

Why did these things work with P10? - They had no Ownership Change prior to the Bankruptcy (rare) and investment from 210 Capital fell under a Section 382 exemption which allows one Ownership Change during the process of Chapter 11 if certain conditions are met (which they were)

2. Residual Liabilities

Absent a full sale of assets and operating business with an indemnity or going thru the bankruptcy process the Company will not be clear of potential legacy liabilities and that overhang is not something large investors are typically comfortable with.

Why did these things work with P10? Thru the sale to Langley, all liabilities were assumed by Langley and P10 was fully indemnified - Further P10 went thru the bankruptcy process which further cleaned up the past.

All of that said, P10 was a unique target because it did not have a past Ownership Change, Langley assumed all past liabilities and provided an indemnification (and their indemnification has value), and it had a business reason to go thru the bankruptcy process (the Braker Facility Lease) which allowed the 210 Capital investment and also cleaned up any other potential residual liabilities. Maybe several Biotechs could fit this fact pattern, but it would not be that likely.

Raiser typo should be "easier"

$NEOS approved! That was one of the raiser PDUFA plays. They don't come around to often sub 300m market cap bios

-BioHunter

$LPCN portfolio update. Sold all shares 4.01 to 4.07. I don't today's PR. Trial and data straight forward not sure why they are having a cc post 4pm data unless it's got problems. Taking my 11% profits here

$PIOE, I made a long post on the PIOE IHub board as Sheff keeps this as Bio only except rare occasions.

$PSDV, I like it and was an aggressive buyer 1.66-1.75 range. Will trade accordingly based on price action. My guess is we see $2 next week if XBI holds

As mentioned in my last post on 5/21/17, this board is not my primary focus and I do not always have time to make full comments, but I do want to respond to some earlier questions and comments on the board.

TRADING

It appears that P10 is now ready to commence trading on Monday 6/19/17, it has been a long time coming. Before discussing any predictions, I would like go back to a section from my post of 4/25/17..

I discussed valuation in several previous posts and irrespective of what value is placed on P10 based on your own judgement, I think it is important to recognize that getting to that number is not as simple as wrapping up Chapter 11.

In a rough order of magnitude, I would say that the following catalysts need to take place to extract the appropriate value of P10 and get from “here” to “there”

1. Final Confirmation of Chapter 11

2. Issuance of New Shares to current stockholders, 210 Capital, and the corresponding investment by 210 Capital

3. P10 begins trading again without the “Q” attached to the ticker

4. Announcement by P10 that they have a company under contract to acquire (NEW CO)

5. Closing on the NEW CO and the subsequent infusion of $10m by 210 Capital under the preferred line of credit.

6. Any news on Patent licensing or the potential sale of a Patent or Patents (this could happen simultaneously with prior steps or at a later time)

Until Steps 1-4 happen, we will not see the maximum value of the NOLs reflected in the stock price because under conventional valuation methods, it is not possible to apply an appropriate DCF model to the NOLs without first having a profitable company (and associated profit forecast) on the books of P10. Once a profitable company is acquired, it will be possible to forecast the time necessary to extract the value of the NOLs which will then allow the market to apply the appropriate DCF and discount the value accordingly to arrive at a NPV for the NOLs.

Upon commencement of trading, we have only completed steps 1-3 and as previously stated, until step 4 is completed, P10 should not trade at a proper valuation. Where P10 trades until we have some further clarity around step 4 is not something that I want to speculate, but do not forget that on a per share basis, P10 has seen 48% dilution since it last traded outside of the grey market and in reality no new catalysts to increase market cap have occurred that were not contemplated at the time.

I do anticipate a few dynamics to occur once trading commences.

1. We may see some sellers who do not fully understand the story exiting simply because they are tired of waiting and have a lack of confidence in P10 due to the extended period of grey market trading.

2. We may see some larger buyers who were bumping up on the 4.99% ownership limit prior to investment from 210 Capital.

3. We may see new buyers that were following the story and were reluctant to invest until the Chapter 11 case was resolved (this would be the first real opportunity out of the grey market)

4. My initial view was that we would not see a substantive announcement on an acquisition or patent monetization transaction within the first 5 days of trading due to the exercise price determination on the Ascolese stock options. I still stand by this view, but if P10 has an acquisition lined up (which I believe they do) it may be necessary to announce sooner.

All of that said, I do not have a prediction on where the stock will trade or how much volume will change hands until an acquisition is announced, but I am ready to participate if the opportunity presents itself.

PATENT MONETIZATION

For the purposes of this discussion I will not discuss the monetization strategy for the patent portfolio. I do believe that significant value could reside here, and I would not be surprised to see one or more favorable monetization transactions come out of the patents, but quantifying that value and predicting the path toward extracting that value is too uncertain at this point. The only assumption that I am operating under regarding the patents, is that P10 has conveyed, although they would sell if the right opportunity presented itself, they are looking to create partnerships or license the patents.

CHARACTERISTICS OF TARGET ACQUISITION

I will begin by saying that I still believe that P10 has at least one company lined up to acquire.

Before identifying any specific target acquisitions for P10, it is important to circle back to the core investment thesis, which can help define what characteristics are most valuable to P10 in a target acquisition.

The core investment thesis has always been to monetize the significant federal tax attributes held by P10 to shield future income (including patent monetization) from federal taxation. Although P10 has discussed the state tax attributes, in my view the core thesis has always been centered around federal taxation and any value derived from the state tax attributes would simply be a bonus at this point.

The federal tax attributes are primarily what brings an investor like 210 to the table with a significant amount of cash, experience and resources.

P10 has stated on their website and in various press releases that they are looking to acquire well run operating companies in the commercial and industrial sectors that generate positive cash flow and most importantly to P10 generate profit. P10 is incentivized to look for a particular type of acquisition with certain characteristics.

The focus on utilizing the tax attributes should cause P10 to target a company with some or all of the following characteristics

• Generates consistent and predictable taxable income (more important than future growth trajectory or cash flow)

• Long term (10+ year) view of consistent profitability

• Requires low ongoing CAPEX or investment in growth

• Not a cyclical business

• Not heavily dependent on outside variables

• Operational predictability and ease of operational execution

In my analysis, thru a combination of one or more acquisitions (and patent monetization), P10 needs to reach an average taxable income of roughly $18m per year over the next 10 years to fully utilize the federal tax attributes.

In the bankruptcy filings, P10 released their 2015 tax return which shows the following for amounts of NOLs per year.

12/31/1998 $5,274,632.00

12/31/1999 $2,745,996.00

12/31/2000 $20,091,876.00

12/31/2001 $36,732,972.00

12/31/2002 $24,453,087.00

12/31/2003 $22,088,027.00

12/31/2004 $24,276,095.00

12/31/2005 $23,778,622.00

12/31/2006 $18,370,794.00

12/31/2007 $13,509,729.00

Although P10 has NOLs in later years (which I have not listed above) roughly 70% of the total NOLs will expire within the next 10 years and they start to expire in 2018.

On the positive side, the 1998 and 1999 NOLs are smaller relative the later years so P10 will have some time to ramp up profitability without the risk of a substantial amount of the NOLs expiring.

Keep in mind that the later dated NOLs can always be used ahead of time.

INDUSTRY OF ACQUISITION

Using the requirements of cash flow positive and profitable, P10 should be looking for a business that can capitalize on the internal knowledge base and leverage the core competencies of P10. Being that P10 only has two employees (Ascolese & Powers) and a board of directors, that decision should be based on the collective skills and experience of all leadership, including the board. A quick survey of the leadership team would show significant experience in the following industries

• Energy/Power/Electrical Infrastructure

• Infrastructure Management Solutions

• Process Control & Building Control Software

• Telecom Infrastructure Integration

In addition some general themes that are mostly consistently thru the leadership team

• Manufacturing

• Intellectual Property Development & Management

• High Growth Companies

• Finance/Private Equity Contacts

The most common themes are Energy/Power/Infrastructure and this is also within the general realm of where the patent opportunities exist. That said, to leverage the leadership team, opportunities within this arena would be the most logical going forward, but I DO NOT believe that the success of P10 would require an acquisition within this realm.

GLOBALSCAPE- SPECULATION

I have been watching Globalscape (GSB) since January when 210 Capital announced that they had acquired a large block of stock in private transactions @ $3.88.

This was not the first holding in GSB for C. Clark Webb & Robert Alpert (owners of 210 Capital). Between May and August of 2016, Webb began building his position in GSB and acquired more than 230k shares in the open market. In addition, Alpert via Atlas Capital (his fund), owned 50k shares prior to the January 2017 purchase.

The dates around the initial positions and the fact that the subsequent purchase in January 2017 was done before the P10 story had unfolded (as well as some other details) lead me to believe that the two investments (GSB & P10) are not related, but I will not rule it out.

It is possible that Webb & Alpert had lined up the deal with the anticipation that P10 could resolve the lease issues and they could invest in P10 without bankruptcy and due to the delays in the P10 story unfolding, they were forced to buy some of the shares outside of P10 back in January.

GSB had a great first quarter and the stock is up 20% - 25% + since January on relatively higher volume, which would clearly make an acquisition more expensive.

All of that said, my gut tells be that the two transactions are not related but I will not rule out the possibility at this point because GSB (as a company) checks several of the boxes in characteristics of what P10 would be looking for.

FINANCING OF ACQUISITION

To maximize the use of the tax attributes, P10 will need to acquire one or more companies that will require them to have more capital than the $4.5m cash and $10m credit line currently in place.

That said, P10 will need to raise capital and this will most likely be done via a combination of a common stock rights offering, debt and preferred stock. The use of debt and preferred stock do not provide the best use of the tax attributes, because the associated interest expense lowers taxable profit.

Monetizing tax attributes is a game of efficient capital allocation and creating the best return possible on the invested cash, which is mostly achieved with common equity.

The use of a common stock rights offering is very common when tax attributes are involved because it will allow 210 Capital to maintain the same equity percentage and not trigger an ownership change. Further, it typically allows all other stockholders the ability to participate on a pro-rata basis at which is usually at a beneficial valuation based on a discount to volume weighted average price of the stock for a finite period prior to the offering.

The downside is of course that if a stockholder does not participate in the rights offering, they will be diluted.

In conclusion, we are on to another chapter for P10 now that we are back to trading and it will be exciting to watch.

The boat is headed in the right direction with a great captain and crew, now we just need to unfurl the sails (with each additional monetization step) and allow them to catch some wind to drive forward with momentum and most importantly, shareholder value.

$NEOS sold half 8.70. Still holding 6%

Closed $ADMP 5.70 on remaining shares from 3.60 entry. Not sure where this trades near term but thinking of selling naked July calls

$MTNB sold all remaining shares $2.67. I am not confident they have dose high enough to work VVC. Data as soon as next week. Flat trade unfortunately.

$MTNB

I was offline remote part of S America last week. Looks like I missed a lot of fun in bio. I just went through MTNB call this morning and as usual the Q&A was interesting.

It's disappointing NIH had only two patients with data. After seeing what those two individuals had to do with flight from across the country several times to participate it's somewhat understandable. Basically they had to fly to Baltimore multiple times to participate. One patient from Minnesota the other I think was Arizona.

The data was important proof of concept. Basically will the immune system transport the cochleate drug wrapper to site of infection. That appears to be confirmed. P2 trials normally answer some question but often create new question and that appears to be the case here.

The VVC data in a few weeks becomes an important catalyst. This is a company sponsored trial and will have over 70 patients. If positive MTNB will be off to the races. But it's hard to handicap here.

I sold 1/2 of my position today with part stopped out last week at current levels. Small loss on these shares but still a big gain on the year from the trade 1.60 to 3.80.

-BioHunter

RE Trade thoughts Top 10 June Catalyst

I am headed to S. America for 10 days so will be off the biogrid during an important end to Q2. Here's a quick look at my active positions.

1st $MTNB June 3rd data will be key, think of their tech as a Trojan horse , they have essentially proved they can get drug past the GI, kidney and blood protected, can they now unravel/open the door in the city walls. Why is this important... Huge opportunity to take IV drugs into oral, extend patents, and importantly take approved drugs with high tox and avoid the tox and get to target. Also think of drugs shelved in P1/2 because of tox issues could become viable. NIH will publish results on small 16 patient trial. SOC with this population is 5% effective rate, NIH trial seeks 20% for positive read out or 4 patients. Importantly they will have a large vulvovaginal candidiasis (VVC)P2 trial read out "end" of June. So you have back to back platform validation events that ultimately would be a practice changing medical breakthrough.

ClinicalTrials.gov

https://clinicaltrials.gov/ct2/show/NCT02629419?term=mat2203&rank=2[/tag]

2nd $NEOS This is a commercial stage bio with two PDUFA's next 4 months. I am willing to hold through the June 15th PDUFA and think we see +$10. $NEOS has been through the FDA rodeo before and learned from their past CRL. Management seems confident they will be approved and I agree. Remember it's CNS side of the FDA. That group typically approved last minute last day. I will hold through this event.

3rd $PSDV 2nd P3 on deck here late June, first trial had excellent resutls and stat sig P value .00001. This trial is essentially the same except 100% run in India. Drug is already and approved for Illuvien. $PSDV licensed to $AILM. I think we see $3+ on data. $PSDV should be a good trader in June.

4th $PIRS what can I say, pounded the table at $1.60, nice move today with volume to $4.45. They will have 080 data early June at European Renal Association & European Dialysis and Transplant Association (ERA-EDTA) Congress in Madrid, Spain. PIRS-080 is first platform validation of the Anticalin tech. Most of the economics are partnered, but trail should provide validation and help $PIRS continue it’s march to double digits. One of my few long view trades

5th $STML will have more mature cohort 1-2 data EHA17 and cohort 3 data later in Q3. It’s a name a really like and I look for it to get over $10 soon

6th $SLEB we had nice result in their gout trial cohort 1 and cohort 2. We will get update and cohort 3 data at EULAR 2017 June 14-17. Under the radar bio and catalyst.

7th $LPCN looking for data results June. P3 to address 2016 CRL. Pretty sure it's a low bar hurdle, I think it runs here into data.

8th $ECYT – ASCO data play, low EV value and abstracts were simply place holders. One to watch for ASCO market over reacted to abstracts that had no color. Management has been talking up ASCO data presentation.

9th $CRVS like $ECYT it’s a sleeper ASCO play that I think is miss priced by the market. The drug show monotherapy activity. How many oncology assets are out there that have monotherapy efficacy similar to anti-pd1? Not many and buying one for a $300M

10th $ADMP PDUFA is 3rd time a charm? no idea but trade opportunties before PDUFA June 19th

-BioHunter

Well you don't really have much choice but to sit and wait. That said it's typically a 3 week process on average and we are are not yet at 3 weeks. My base assumption is 3 weeks maybe 4.

I don't always have time to make full comments on this board as it's not my primary focus. But to add some color I will contribute the following to the conversation:

I want to begin by saying that P10 began the long and complicated process of enhancing shareholder value in early 2016 and their transparent actions thus far have been in the best interest of shareholders. Let's review:

In June 2016, a NOL Rights Plan was adopted to protect the value of all tax attributes held by P10.

In July 2016, the board of directors engaged Vinson & Elkins LLP to explore strategic and financial alternatives including the sale of the company, new investors, and a transition to a profitable business.

In November 2016, P10 sold the operating business to Langley and retained some cash, patents, and several liabilities.

In November 2016, following the sale to Langley, P10 put forward their new business plan with a goal of maximizing long-term shareholder value thru the monetization of non-core intellectual property assets and raising additional capital to acquire a well managed, profitable business.

In March 2017, P10 announced that they had a commitment to raise additional capital from 210 Capital and would be going thru the bankruptcy process to clear all remaining liabilities from the Langley sale and to further preserve the value of all tax attributes held by P10.

In April 2017, P10 announced the confirmation of their bankruptcy plan.

In May 2017, P10 announced the bankruptcy plan effective date, the closing of all items pursuant to their bankruptcy plan, the investment from 210 Capital was completed and that all common shareholders would be issued new shares on a 1:1 basis.

On May 9, 2017, P10 announced that a new trading symbol for P10 (PIOE) had been established and that to their knowledge at least one market maker was engaged in the process of filing the necessary forms with FINRA for a broker dealer to provide a quotation (bid/ask) for the new ticker PIOE. It was further noted by P10 that they have no control over processing time of the FINRA form 211 filing or when trading will commence for PIOE.

Just to recap, P10 has been working towards the complicated process of enhancing long-term shareholder value for well over one year and in my view with a few delays has delivered effectively and transparently on this plan while continually demonstrating a commitment to long-term shareholder value.

DELAYS IN ORDINARY TRADING

The timing of when PIOE ceases to trade in the Grey Market and commences normal trading with a quotation (bid/ask) is inconsequential relative to long-term shareholder value. Every step that P10 has completed up until this point has NOT been focused on creating a short term trade and anyone who invested based on that pretense should probably not be in the stock in the first place.

Sure, do I expect to see a marginally higher trading PIOE once it commences normal trading? Yes, but as I have articulated in several previous board posts, this story requires several steps to be completed for substantial value creation.

Now that P10 has a clean balance sheet with cash, solid protection of their tax attributes and a new investor with further financial commitment, the next step is the announcement of an acquisition to properly utilize their tax attributes and/or some further certainty around the value/opportunities related to the patents.

That said, when PIOE commences normal trading is currently irrelevant and to have diminished confidence in P10 management as a result of the trading delay is simply short sighted. The Form 211 was not something within their control to file and the FINRA processing time is only within the control of FINRA.

Lastly, to insinuate that the extended Grey Market trading was orchestrated to provide Ascolese with a lower options exercise price is a stretch. If Ascolese and the Board were truly concerned about this, his options agreement could easily be amended or supplemented to make him whole as opposed to risking something that would potentially be harmful to shareholders and hence deemed illegal.

NOTE: If I were to speculate on one cause of the delay in processing the Form 211, I think it could be related to the Charter Amendment and issuance of new shares (see more detailed commentary below in “Tax Attributes”

TAX ATTRIBUTES

The P10 tax attributes are clearly the most valuable company asset at this point, so I feel it is important to highlight the actions P10 has taken to protect them for the long-term.

Most if not all of the risks associated with the tax attributes have been eliminated and P10 has managed this asset very well to date, starting with the adoption of the NOL Rights Plan in June 2016.

The IRS rules on the subject of NOLs are VERY COMPLEX and the use of NOLs is limited if there is a deemed “Ownership Change” which would severely impair the value of the NOLs. Simply put, the most common way to trigger an “Ownership Change” is to create more 5% shareholders or for existing 5% shareholders to acquire more stock.

Many notable companies like Ford Motor, Pulte Homes, Krispy Kreme (to name a few) have adopted a Poison Pill or NOL Rights Plan for the sole purpose of to protecting the value of their NOLs. The Poison Pill or NOL Rights Plan distributes one or more preferred share purchase rights to each outstanding share of common share. These preferred share purchase rights are redeemable by the company until someone acquires 4.99% or more of the common stock in the company, at which point they become exercisable by the common shareholder. These rights, when exercised, are substantially dilutive to all outstanding common shares. Any rights held by someone who acquires 4.99% or more of the outstanding common shares become void and are not exercisable. The company hopes that this acts as a deterrent to acquire more than 4.99% or more of their outstanding common shares and in turn mitigates the chances of an “Ownership Change”.

Despite case law supporting the Poison Pill or NOL Rights Plan in Delaware, shareholder approval is always required to adopt and enforceability against shareholders who did not vote for the action is uncertain. Further, the time and difficulty necessary for the company to go thru the mechanics of triggering the plan and diluting out the shareholder can make the actions of the company less legally defensible and in the view of the IRS who would determine that an “Ownership Change” DID OCCUR during the process of executing the plan.

The better way to protect the value of their NOLs is in the form of a Charter Amendment and subsequent issuance of new shares because is mechanically much cleaner. In a Charter Amendment, the company sets a flat ownership limit at 4.99 percent that is tied to the shares and if a shareholder goes over the 4.99 percent ownership limit the company can simply unwind the portion of the transaction over 4.99 percent without incurring the time and difficulty of trigger the plan and subsequently diluting the shareholder out.

Once a Charter Amendment is in place, it means that an activist shareholder attempting to acquire more than 4.99% can not intervene with the actions of the company to unwind any further purchase or amend the company charter, that can only be done with board approval.

Further, in the past the IRS has specifically recognized Charter Amendments of this type and has stated that if an “Ownership Change” were to occur which would limit the status of the NOLs held by the company, any actions taken by the company to invoke the provisions of the Charter and unwind the transaction are respected ARE RESPECTED by the IRS and valid for the purposes of saving the character of the NOLs.

One value that P10 derived from the process of going thru Chapter 11 (which I believe was strategic) was the ability to take the 48% investment from 210 Capital without triggering an Ownership Change.

Sections 382 & 383 of the IRS code provide an exemption which allows one Ownership Change to occur during the process of Bankruptcy, hence 210 Capital was allowed to gain such a large percentage of ownership without limiting the future use of the NOLs.

However, for the Bankruptcy exemption to be effective, P10 MUST NOT undergo another Ownership Change within the next two years or the NOLs will be limited.

Hence the importance and strong value of the Charter Amendment and new shares.

All of that said, P10 has done all within their power to protect the value of the NOLs with a Charter Amendment and the issuance of new shares. Both actions which truly protect the most valuable asset of P10.

I Have some ideas on aquistion targets, and will try to post soon. Where P10 trades in the short term, I have no idea as we have seen 48% dilution since stock was freely traded, but this 'should' have been priced in. On the flip side, the dilution allows past investors who were bumping up to the 4.99% owership limits to now able to add shares. It will be interesting to watch the action, as I will be ready to participate.

-BioHunter

@TheBio_Hunter

Your calc on tradable float seems about right, around 5m

Probably less.

Not sure why anyone cares when this starts trading again, it's all about who they buy, not when this trades off grey mkt. This board is unreadable relative to this topic.

-BioHunter

Nice trade $NEOS. CEO on call today said they are talking to FDA, normal type questions, nothing unexpected in FDA dialog. Sales growing ahead of expectation at 20% month over month.

My view is we see mid 8's before PDUFA $10 on approval.

Profits are profits nice job Sheff.

Portfolio update.

Adding to $NEOS 6.90 before quarterly results tomorrow. Now 11% position

Added $PSDV 2.95 now 10%

-BioHunter

For some reason I feel compelled to add some color before this board turns into a mess.

- Why would share price go up post bankruptcy ? Any level of DD one could predict clean bankruptcy was going to happen, that was priced in the stock.

-Big Holders? How can you look at the trading volume, dollar volume and dollar weighted average trade price and draw ANY conclusion that large holders are selling. It's totally stupid to 'read' trading tea leaves when dollar weighted volume is so small. Plus any large stakeholder can't sell into the bid. There is no bid to sell into, spanking 20k shares into a bid when you hold 500k or 1m shares is chump change.

- There is no float. Most shares locked up or held by 5% stake holders. Those individuals correctly understand that value won't be created until they acquire a business. NOL's can then be modeled in a DCF and instant value created.

So will the shares bleed here? probably. Could we see .30 or a bit less sure. Will we see .40+ unlikely. Will dropping the Q matter, I don't think, so shares could dip from the dilution. But once new shares are issued current holders can add, that is where you may finally see a real bid.

Once they acquire a business investors will get paid. Traders, who knows, depends on how good you are at trading. Most strong hands are not playing the short term price swings on $50k in daily dollar volume.

-BioHunter

$PIOI DD- Important to understand CEO's option structure

I don't expect company to do more then the minimum required PR's for 5 days post bankruptcy. The CEO is pretty motivated to keep share price down for 5 days. Here is why:

(i) Mark Ascolese has agreed that (x) he will accept 1,600,000 in new stock options with respect to the Debtor’s common stock to be conferred on him on the Plan Effective Date in full satisfaction, settlement, and release of any and all claims he holds, or will hold, against the Debtor for unpaid compensation or restricted stock units through the Plan Effective Date, and (y) the 1,600,000 in new stock options will have an exercise price of the higher of either (i) $0.215 cents or (ii) the average share price of the Debtor’s common stock over the first five (5) stock trading days after the Plan Effective Date, provided however that Mark Ascolese must provide the Debtor’s board with notice of his intent to exercise any of the new stock options and the Debtor shall have the option, in its sole and absolute discretion, to settle the new stock options for cash in lieu of issuing stock;

As per my post yesterday - clean balances sheet coming out of bankruptcy this week looks very likely based on docs filed to-date with court. Next is to drop the "Q". I am sure those events will get reported by company. But the bigger valuation inflection point will come around the company acquisition target and any color on patent value/monetization. I am making a pretty educated guess the former is already lined up, but I could see the press release around that delayed for a few weeks, in part due to the option language above.

-BioHunter

$PIOI DD- Important to understand CEO's option structure

I don't expect company to do more then the minimum required PR's for 5 days post bankruptcy. The CEO is pretty motivated to keep share price down for 5 days. Here is why:

(i) Mark Ascolese has agreed that (x) he will accept 1,600,000 in new stock options with respect to the Debtor’s common stock to be conferred on him on the Plan Effective Date in full satisfaction, settlement, and release of any and all claims he holds, or will hold, against the Debtor for unpaid compensation or restricted stock units through the Plan Effective Date, and (y) the 1,600,000 in new stock options will have an exercise price of the higher of either (i) $0.215 cents or (ii) the average share price of the Debtor’s common stock over the first five (5) stock trading days after the Plan Effective Date, provided however that Mark Ascolese must provide the Debtor’s board with notice of his intent to exercise any of the new stock options and the Debtor shall have the option, in its sole and absolute discretion, to settle the new stock options for cash in lieu of issuing stock;

As per my post yesterday - clean balances sheet coming out of bankruptcy this week looks very likely based on docs filed to-date with court. Next is to drop the "Q". I am sure those events will get reported by company. But the bigger valuation inflection point will come around the company acquisition target and any color on patent value/monetization. I am making a pretty educated guess the former is already lined up, but I could see the press release around that delayed for a few weeks, in part due to the option language above.

-BioHunter

$PIOI some thoughts here going forward...

On Wednesday 4/26 10:30am (Central Time) P10 will be going before the judge in a combined hearing seeking final confirmation of the prepackaged plan and disclosure statements.

The final claims date (last day for a creditor to file a claim against P10) was 4/21 and no additional claims were filed.

The final day for objections to the prepackaged plan and disclosure statement was also 4/21 and no objections were filed.

One claim that does exist is to the IRS for several older Payroll Tax related returns that were supposedly not filed, a 2017 Payroll Tax Return which was not filed before the Chapter 11 case commenced and the 2016 Federal Income Tax Return (which is not currently due)

My feeling is that the older Payroll Taxes were paid (P10 has used ADP payroll for years) and that this is simply a clerical error which should not cause any problems with confirming the Chapter 11 Plan.

I believe at this point is that the plan will be approved as presented on Wednesday 4/26 or will be approved contingent on one or more minor administrative items which need to be completed by P10 in a very short time frame.

In discussed valuation in several previous posts and irrespective of what value is placed on P10 based on your own judgement, I think it is important to recognize that getting to that number is not as simple as wrapping up Chapter 11.

In a rough order of magnitude, I would say that the following catalysts need to take place to extract the appropriate value of P10 and get from “here” to “there”

1. Final Confirmation of Chapter 11

2. Issuance of New Shares to current stockholders, 210 Capital, and the corresponding investment by 210 Capital

3. P10 begins trading again without the “Q” attached to the ticker

4. Announcement by P10 that they have a company under contract to acquire (NEW CO)

5. Closing on the NEW CO and the subsequent infusion of $10m by 210 Capital under the preferred line of credit.

6. Any news on Patent licensing or the potential sale of a Patent or Patents (this could happen simultaneously with prior steps or at a later time)

Until Steps 1-4 happen, we will not see the maximum value of the NOLs reflected in the stock price because under conventional valuation methods, it is not possible to apply an appropriate DCF model to the NOLs without first having a profitable company (and associated profit forecast) on the books of P10. Once a profitable company is acquired, it will be possible to forecast the time necessary to extract the value of the NOLs which will then allow the market to apply the appropriate DCF and discount the value accordingly to arrive at a NPV for the NOLs.

Based on the proposed capital structure of P10 upon exiting Chapter 11, I think that the company can afford to acquire a company with a value of $75m - $100m through a combination of cash, the preferred line of credit, rights offering of common shares, and external debt.

Alternatively, P10 could also bring a private company public via a quasi-reverse merger and do so mainly thru the issue of common shares.

On risk going forward is that through some of the proposed actions above, although the market cap of P10 could increase dramatically, if an excessive number of common shares were issued to accomplish this, the dilution will not help the overall stock price in the short term.

-BioHunter

$PIOI my thoughts on upcoming catalyst and bankruptcy hearings.

On Wednesday 4/26 10:30am (Central Time) P10 will be going before the judge in a combined hearing seeking final confirmation of the prepackaged plan and disclosure statements.

The final claims date (last day for a creditor to file a claim against P10) was 4/21 and no additional claims were filed.

The final day for objections to the prepackaged plan and disclosure statement was also 4/21 and no objections were filed.

One claim that does exist is to the IRS for several older Payroll Tax related returns that were supposedly not filed, a 2017 Payroll Tax Return which was not filed before the Chapter 11 case commenced and the 2016 Federal Income Tax Return (which is not currently due)

My feeling is that the older Payroll Taxes were paid (P10 has used ADP payroll for years) and that this is simply a clerical error which should not cause any problems with confirming the Chapter 11 Plan.

I believe at this point is that the plan will be approved as presented on Wednesday 4/26 or will be approved contingent on one or more minor administrative items which need to be completed by P10 in a very short time frame.

In discussed valuation in several previous posts and irrespective of what value is placed on P10 based on your own judgement, I think it is important to recognize that getting to that number is not as simple as wrapping up Chapter 11.

In a rough order of magnitude, I would say that the following catalysts need to take place to extract the appropriate value of P10 and get from “here” to “there”

1. Final Confirmation of Chapter 11

2. Issuance of New Shares to current stockholders, 210 Capital, and the corresponding investment by 210 Capital

3. P10 begins trading again without the “Q” attached to the ticker

4. Announcement by P10 that they have a company under contract to acquire (NEW CO)

5. Closing on the NEW CO and the subsequent infusion of $10m by 210 Capital under the preferred line of credit.

6. Any news on Patent licensing or the potential sale of a Patent or Patents (this could happen simultaneously with prior steps or at a later time)

Until Steps 1-4 happen, we will not see the maximum value of the NOLs reflected in the stock price because under conventional valuation methods, it is not possible to apply an appropriate DCF model to the NOLs without first having a profitable company (and associated profit forecast) on the books of P10. Once a profitable company is acquired, it will be possible to forecast the time necessary to extract the value of the NOLs which will then allow the market to apply the appropriate DCF and discount the value accordingly to arrive at a NPV for the NOLs.

Based on the proposed capital structure of P10 upon exiting Chapter 11, I think that the company can afford to acquire a company with a value of $75m - $100m through a combination of cash, the preferred line of credit, rights offering of common shares, and external debt.

Alternatively, P10 could also bring a private company public via a quasi-reverse merger and do so mainly thru the issue of common shares.

On risk going forward is that through some of the proposed actions above, although the market cap of P10 could increase dramatically, if an excessive number of common shares were issued to accomplish this, the dilution will not help the overall stock price in the short term.

I am NOT going to post my exits on PIOI, at this point everyone on this board should have solid profits, when to exit is up to you based on your trading plan and greed.

-BioHunter

Everything I am seeing out of court docs is looking good here. A few positives that I don't have time to write about but so far so good.

-BioHunter

$TXMD out here 5.21 of second half. 40 cent loss on pos. :(

$TXMD stopped out at half $5.27 damm... I still like my trade thesis of FDA delay vs CRL but hard to fight the tape. watching closely here with second half that I did not have a stop loss.

-BioHunter

More DD relative to the lease for those that care-

The Assumption & Assignment proposal for the Braker Lease is integral to the 210 RSA & Langley RSA which are both covered in the Omnibus motion granted by the Judge on 4/6 for the assumption of both RSA agreements. Like I my previous post, the power of the judge is somewhat constrained by the interplay between Texas law and Federal Bankruptcy law and an assumption & assignment of the Braker lease without landlord consent is not 100% clean due to the conflict of law. Several cases have challenged this interplay in Bankruptcy and the outcome in each was very fact dependent and not something that would create a strong precedent. Absent being subject to Texas law the assignment subsequent assumption would be no issue and the judge would do it based on the mechanics Federal Bankruptcy law and would have many cases to support the action. However, the means to navigate around the Texas roadblock is drafted into the original Braker lease:

D. Notwithstanding anything herein to the contrary, Tenant may assign its?entire interest under this Lease or sublet the Premises to a wholly-owned?corporate or controlled subsidiary or parent of Tenant or to any successor to?Tenant by purchase, merger, consolidation or reorganization (hereinafter?collectively referred to "Corporate Transfer") without the consent of Landlord?provided: (i) Tenant is not in default under this Lease beyond any applicable?cure period; (ii) if such proposed transferee is a successor to Tenant by?purchase, said proposed transferee shall acquire all or substantially all of the?stock or assets of Tenant's business or, if such proposed transferee shall?acquire all or substantially all of the stock or assets of Tenant's business or,?if such proposed transferee is a successor to Tenant by merger, consolidation or?reorganization, the continuing or surviving corporation shall own all or?substantially all of the assets of Tenant; (iii) in no event shall any transfer,?release or relief of Tenant from any of its obligations under this Lease, unless?Tenant ceases to exist as a result of the Corporate Transfer; and (iv) such?transferee assumes in writing Tenant's obligations under this Lease or such?transferee assumes Tenant's obligations under this Lease by operation of law.?Tenant shall give Landlord written notice at least twenty (20) days prior to the?effective date of such Corporate Transfer. As used herein, the terms "control"?or "subsidiary" shall mean a corporate entity wholly-owned by Tenant or at least?51 percent of its voting stock is owned by Tenant. A transfer pursuant to the?provisions of this Paragraph 15D shall sometimes be referred to herein as a?"Permitted Transfer".

The Texas law would be overridden but the intent or mechanism expressed in the original lease to allow a “Permitted Transfer”. The risks here are that P10 is deemed in default beyond a cure period and/or that the landlord could argue that P10 did not sell “all or substantially all” of their assets to Langley. At the very lease if those points are argued, it would no longer be about lease assignment but rather and argument of interpretation. That said, assuming the “Permitted Transfer” failed as a result of those issues (although remote), at least the judge would be able to establish that the lease WAS assignable under Texas law and could rule to grant the assignment.

LIABILITY RELEASE

Yes, the landlord (Braker) must consent to release P10 from the lease but P10 is being indemnified by Langley, that is the most realistic outcome here.

On Stonehollow, see the below section from the original Stonehollow lease. Even though the landlord consented, P10 was still not released.

Why did Langley not just release P10 at the time of the assignment? It appears that the assignment was executed simultaneously with the Langley closing and the Langley APA did not contemplate either the Braker Lease or Stonehollow lease as liabilities that Langley would release for P10. My feeling is that in both cases P10 felt that the they would be able to get released by the landlord but it did not happen and Langley did not want to assume the lease liabilities or release/indemnify P10 just the Stonehollow lease until the Braker lease was put to bed and other pending issues under the APA, this make sense.

Now, we are in Chapter 11 and the Langley RSA (in exchange for some cash) will provide basically a release and indemnification for Braker, Stonehollow, and all other liabilities under the Langley APA. In short, the Langley APA had excluded items that Langley was not willing to release at closing and now they will release them in exchange for some cash and having some finality on the lease issues. ??

Lastly, yes, the best outcome for all parties (including the landlord) is to following the RSA plans presented to the court and allow P10 to survive. The landlord is in a much better position as a result.

I am done discussing this topic!!!! good luck to all

-BioHunter

$TXMD Recent presentation

For those who have not done much DD, a good overview is the recent Oppenheimer presentation from late March. A few things to note is the quality of BOD and team. Both drugs billion dollar opportunities. 80% tute ownership

http://ir.therapeuticsmd.com/phoenix.zhtml?c=60779&p=irol-EventDetails&EventId=5251425

-BioHunter

$TXMD added here $5.52 now 10% Full position. Ave 5.63

STATE NOL'S

Why did I not place a value on the State NOLs?

Primary reason is that based on the historical P10 filings (all that we have to work with) it is impossible to ascertain enough details.

In general, a corporate taxpayer in the US will be taxed in any state which it has Nexus, defined as a connection between the taxpayer and a taxing jurisdiction sufficient enough for the jurisdiction to impose tax on the taxpayer.

If a taxpayer is determined to have sufficient Nexus in one or more states(including the taxpayer's home state), income is apportioned one or more states. Most states apportion based on (“UDITPA”) the Uniform Division of Income for Tax Purposes Act of 1957. UDITPA uses the average of three ratios: property in the state divided by property everywhere, payroll in the state divided by payroll everywhere, and sales in the state divided by sales everywhere.

That said it is possible that although P10 incurred Federal losses for many years, during some of those years, they could have actually paid tax on a state level and the NOLs would not match.

Further, in many cases the calculations for state and federal income diverge on several fronts (Depreciation, Credits, Deductions, etc.) which can cause a significant difference in the amount of taxable income in any given year between state and federal.

To ascribe a value to the state NOLs would require knowing which state, what year the loss was incurred, what the federal taxation in that year was, and a whole host of other details.

Could the State NOLs have value to P10 in the future? Yes, even if the home state did not have a corporate tax (like DE, TX, ETC.) but not enough detail exists to count on it in a near term valuation.

-BioHunter