News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

Zilidium

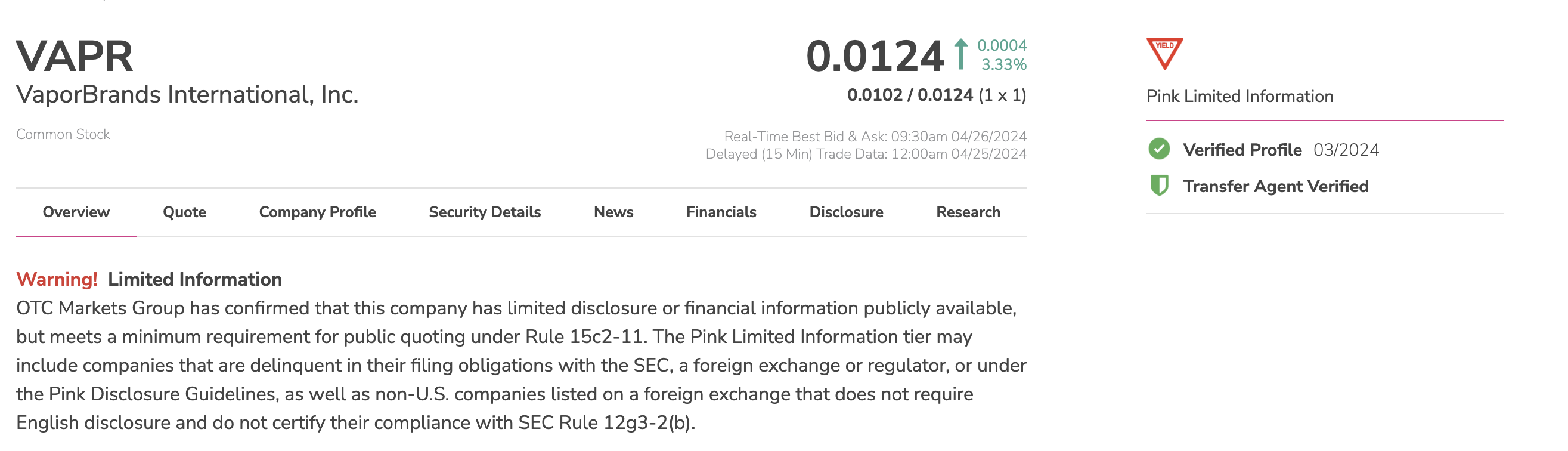

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Interesting. For an idea of what is considered "good quality", According to the World Gold Council, larger and better-quality underground mines contain around 8 to 10 g/t gold, while marginal underground mines average around 4 to 6 g/t gold. Open-pit mines usually range from 1 to 4 g/t gold, but can still be valuable.

Any idea if this is a lode deposit and placer deposit?

As NAK, no it will not happen as per the SC ruling. However, if a new corporation is created it will have legal precedent to challenge the EPA. So if/when NAK creates a new company, keep a close eye on things.

Time will tell.

You sound like an Englishman from the 1800's...we are onto you time traveler.

relax, I'm just posting news, nothing more nothing less.

or...This flies to .4-.6 range once people start buying here.

Two sides to every investment...bet.

We are all investors here, your opinion is your strategy, and that's generally true for everyone. If we all had the same strategy the market would be flat.

My opinion: the NVD floor is about to drop out...

I believe it was eight countries. Regardless, very impressive.

You can see the animated video of the journey here:

he is either chatgpt or grok, I can't tell.

As disclosed in Luminar’s earnings report, in the first quarter of 2024, Tesla contributed over 10% of Luminar’s revenue, totaling more than $2 million. I guess Elon needs a crutch. ;)

Maybe, just maybe, one should get off the pink sheets before posting a link on their new shiny website that takes you to a big fat Warning! about buying the stock.

Coinbase is FDIC insured. The fiat value of your Coinbase wallet will be insured up to $250,000 in the same way that a traditional bank insures your deposits.

maybe you are on to something, they can call it Knight Industries Two Thousand (KITT).

Coinbase is notorious for high fees, where do they make their money, thanks for the milk out the nose laugh this morning.

https://thestrategystory.com/2022/05/28/how-does-coinbase-make-money-business-model/

Agreed, he would f'up a one car junk yard.

30 days later and Ninja's premonition was about as wrong as one can be, maybe not a pumper, but a terrible forecaster nonetheless... https://investorshub.advfn.com/boards/read_msg.aspx?message_id=174022286

with 36 employees, about $110k/yr.

Did someone mention fundamentals? Trump Media lost $58.2 million in 2023 and sales totaled just $4.13 million 🤮

As an owner of an EV, getting a type II charger at home is money well spent, pull into the garage , plug 'er in, every morning your topped off for the day ahead...easy peasy. Way easier than filling up with gas. I will say from experience, EV's do not like cold weather, Range goes down considerably, so a charger at home is a must if you live up North.

I believe those were turn around times during covid, the article was dated September 2020.

Is this more to your liking, I can spin it both ways? Tethering a nation's currency solely to gold is oftentimes dismissed by those who fail to see the enduring value of traditional, tangible assets amidst the whirlwind of modern economic theories. Those "libs" cite the complexities of our global economy, the supposed necessity of an elastic monetary policy, and the purported challenges of sustaining sufficient gold reserves to underpin the currency in circulation. However, this perspective overlooks the stabilizing force that a gold standard could reintroduce, amidst the reckless monetary expansion and the inflationary policies that have become all too common. While it's true that approximately 6.3 billion ounces of gold have been extracted throughout history, valued at about $2200 per ounce in today's market, summing up to a total value slightly over 14 trillion dollars, the argument that a gold standard would inevitably constrict economic growth and usher in deflation is one rooted in a shortsighted understanding of economic resilience and prosperity.

Furthermore, as we witness the burgeoning interest in digital currencies and assets, it's crucial to approach these modern financial instruments with a healthy dose of skepticism. The volatility and uncertainty surrounding these digital ventures render them, at this stage, as less reliable foundations for an economy than the proven stability of gold. Should there ever come a time when a digital currency is considered for backing a tangible currency, it must embody the core principles of sound money:

1. Stability: It must exhibit a high degree of steadiness, resistant to whimsical market fluctuations.

2. Scarcity: Its value must be derived from its rarity, yet it must remain sufficiently accessible to serve its purpose in the economy.

3. Acceptance: The asset should be universally recognized and valued as a store of wealth.

4. Durability: Its worth and physical state must not degrade over time.

5. Divisibility: It must be capable of subdivision to accommodate transactions of varying scales.

Only when a digital asset meets these stringent criteria, might it be considered as a potential candidate for backing a currency, mirroring the steadfast qualities of gold that have underpinned prosperous economies through the ages.

In the modern era, backing a currency with a single commodity (gold) is seen as less practical due to the complexities of global economies, the need for monetary policy, flexibility, and the challenges of maintaining adequate reserves to support the currency in circulation. Many economists, would argue that returning to a gold backed system would limit economic growth and lead to deflation. 6.3 billion ounces (one estimate) of gold have been removed from the earth (in all history), at today's prices ~$2200 that would put all the gold in the entire world worth slightly more than 14 trillion ($14,067,312,644,231.22). So it seems that if the gold standard were to return, we would experience a bit of economic deflation,

Moreover, with the rise of digital currencies and assets, there's a growing interest in exploring new forms of value backing. However, these ideas are still in the exploratory phase and come with their own set of challenges and uncertainties.

Could crypto be considered suitable for backing a currency, it should ideally have the following characteristics:

Stability: The commodity should be relatively stable and not be prone to extreme fluctuations.

Scarcity: It should be rare enough to be valuable but not so rare that it's not accessible for the purposes of backing a currency.

Acceptance: The commodity should be widely accepted and recognized for its value.

Durability: It needs to be long-lasting and not prone to deterioration over time.

Divisibility: The commodity should be easily divisible to facilitate transactions of various sizes.

one day, maybe.

It's outrageous, egregious, preposterous!...definitely preposterous.

30 days..hmm, this will be interesting. I hope your tea leaves are correct. All other indicators are not pointing in a favorable direction and nobody can argue the fact that LAZR's negative debt to equity ratio = financial distress. I think this is a decent HODL, but doubling in 30 days, thats for crypto.

Running in where others fear to tread can be a good strategy, however, in this case I would not be so sure. Pebble is facing some pretty epic hurdles and does not have a lot of support on the home field (Alaska residents by and large oppose the mine). This is the crushing blow from the EPA, and past vetoes by the EPA , made only three times in the last 30 years, suggest that Pebble has little hope of winning in court. Those high value share prices you mentioned never happend after the EPA's decision.

🍀

or even 29

Baby steps is why I am in this. The massive Arizona facility is truly impressive. $50k model on the horizon. Plenty of growth potential. ya, ya, ya they are hemorrhaging money, but it's being invested, and for me, that's smart spending.

Don't lose sight that this is a luxury car, it's not intended for the masses.

HODL'ing

early morning happened in the afternoon.

First of this is not advice, just an answer to your question, do with it as you will:

When analyzing a stock that trades with low volume it's important to approach with caution due to the inherent risks associated with low liquidity.

Insider Transactions: Insiders being paid in stock options isn't inherently negative, as it can align their interests with shareholders. Keep an eye on buy sell patterns. Buying = good, Selling = bad.

Price Volatility: Low volume can lead to higher volatility. Small trades can significantly impact the stock price, which can be RISKY. Consider that many who follow this company probably own more shares than are traded in a typical day.

Financial Health of the Company: Roll up your sleeves and do some digging (Assess the company's balance sheet, income statement, and cash flow statement.) LBSR will not bode well in this department, read no revenue.

News and Developments: Watch closely for news or developments (buy the rumor sell the news some might suggest)

Volume: watch for spikes. Sell positions that are positive as the volume may support a better ROI.

Technical Analysis: In my opinion tend to be less reliable in low-volume stocks due to erratic price movements, take this with a healthy dose of salt.

What I like, insiders who are actively acquiring shares and options, what I dont like, this stock has been like a Chinese water torture, drip drip drip with no substantial activity that could drive up the price. Mining exploration is inherently risky. I've been here since LBSR was digging in Alaska and I got bored with the inactivity. I don't pay to close attention to whats going on and dable more in crypto than penny stocks. At the end of the day, dont invest more than you can afford to lose.

Form 4:

The form is used primarily by company insiders, such as officers, directors, and shareholders owning more than 10% of a class of the company's equity securities. It documents their transactions in the company's shares. Insiders must file Form 4 to report transactions in the company's stocks within two business days of the transaction date.

The Directors were compensated for services , this happens every year:

Pete O’Heeron

Hemmerly Nicholas

Elmasri Saleem

Does anyone remember when TSLA was under $3.00?

I'm getting the vibe you like to put salt in wounds, head over to LCID you may have some fun there.

Can you provide a source? I'm not seeing your doom and gloom.

insidersales

Mindless, ergo no reason. COVID put the smack down on this company. Don’t buy the stock, buy the company.

People mindlessly panic selling. HODL!