News

News  Market Data

Market Data  Discover

Discover

Support: 888-992-3836

Copyright © 2023 InvestorsHub Inc.

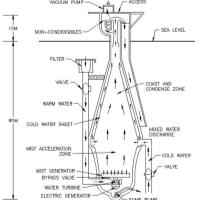

Ocean Power

![]()

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

Register for free to join our community of investors and share your ideas. You will also get access to streaming quotes, interactive charts, trades, portfolio, live options flow and more tools.

That be me.

Here is a link: https://contracts.justia.com/companies/ocean-thermal-energy-corp-7307/contract/252377/

THIS STOCK PURCHASE agreement (“Agreement”) is made and entered into as of the 25th day of August, 2022 (“Effective Date”), by and among: Ocean Thermal Energy Corporation, a Nevada corporation (“Shareholder”), Epaphus Global Energy, LLC, a Delaware limited liability company (the “Buyer”) and OCEES International, Inc., a Hawaii (“Company”) (each a “Party” and collectively the “Parties”) ...

Thank you for posting this exiting news!

Defiance ETFs is launching the Next Gen H2 Fund (HDRO), the first hydrogen ETF in the U.S. Listed on the NYSE, HDRO will give investors exposure to companies involved in the development of hydrogen-based energy sources and fuel technologies. The fund comes with an expense ratio of 0.30%.

According to the prospectus, HDRO’s underlying index, the BlueStar Hydrogen & NextGen Fuel Cell Index, can include up to a 15% weight in non-pure play companies, though it does not include vehicle manufacturers. To be eligible, companies must meet size and liquidity requirements that can be drawn from developed and developing markets.

The fund’s top holdings include such companies as FuelCell Energy, Plug Power, and Ballard Power Systems. The United States, the United Kingdom, and South Korea represent the fund’s largest country exposures.

“We’re already starting to see hydrogen take on a larger role as a viable energy source,” Defiance ETFs President Paul Dellaquila said. “We believe that as governments and corporations continue to demand renewable energy sources and adopt more environment-friendly policies, Hydrogen will be a pivotal resource to help fuel a cleaner economy.”

https://www.etftrends.com/defiance-etfs-launches-first-u-s-hydrogen-etf-hdro/

New Energy for Europe - green hydrogen?

NEW HYDROGEN ETF - The First in The US - Should You Buy Or Not? Video popped up on YouTube

Blockchain guy to invest 30 million and has big plans to alleviate droughts, besides produce abundant energy, in of all places, the Virgin Islands where the first of many new planned communities are being built.

... When Brett “Mac” McClafferty reorganized his private equity fund in the U.S. Virgin Islands, he did so with a promise to “do well by doing good.” McClafferty has apparently committed to that pledge after announcing a plan to invest $30 million in ocean thermal energy conversion (OTEC) projects impacting the U.S. The Virgin Islands over the next decade; an unusual move for a fund that’s made its name in blockchain technologies. ... https://communalnews.com/fund-manager-brett-mcclafferty-pledges-millions-for-thermal-energy-projects-in-the-us-virgin-islands/

New OTEC study published for Panama.

https://ieeexplore.ieee.org/document/8943656

Triple play since Thursday as things get underway with new projects announced by others in Kiribati, Bonaire and the Maldives. Floating OTEC for resorts.

Loop Cayman (OTI) Floating OTEC along the north coast of Grand Cayman Island.

... The advantage of OTEC is that it has the potential to provide renewable baseload power generation.

In the Integrated Resource Plan Report, July, 2017, there was an evaluation of the OTEC technology by Pace Global which assessed the benefits of introducing natural gas for fuel (rather than diesel), the value of energy storage and various baseload renewable baseload power generation technology.

While the technology holds promise, it has not yet got the green-light in the Cayman Islands due to concerns over the commercial viability. A US-based company, OTEC International LLC (OTI) has proposed a floating offshore OTEC platform offshore along the north coast of Grand Cayman. ...

http://www.loopcayman.com/content/integration-consumer-generated-renewable-energy-cayman-pt-3

YES - round-about played unexpectedly as I began watching this video. Can't hear the CEO so better now, but YES will do!

Music app on mac mini went weirdly whacko ...

Investors willing to immediately put more than $600 million into the island. CEO Feakins tweeted: https://twitter.com/i/topics/tweet/1088457761602433026

Caribbean Business

... snip ... Maldonado said Puerto Ricans who took their investments abroad now

have a financial incentive to bring that money back to the island and invest it in the Puerto Rican economy. Locally, the benefit would be for about 15 years.

The chairpeople of the island’s House and Senate Treasury committees, Antonio “Tony” Soto and Migdalia Padilla, respectively, support the measure.

“I don’t think it’s something that we would take too long to pass like the tax reform,” Padilla said, adding that because Thursday is the last day to pass bills, she expected the bill to be voted on by the Senate. Soto said the legislation is an important economic development tool that could bring millions of dollars in investments to Puerto Rico.

Maldonado urged the legislature to evaluate the bill as soon as possible to allow Puerto Rico to gain a competitive edge over the states.

“This cannot be seen as a tax bill but as one of economic development. This is a bill to move the economy, to strengthen it,” Maldonado said. “We are competing with other states and our offer should be as broad and attractive as in other states.”

He stressed that there are a number of investors already willing to immediately put more than $600 million into the island.

01/10/19 ... Equity Purchase Agreement and Registration Rights Agreement with L2 Capital, LLC

Subject to the terms and conditions of the Equity Purchase Agreement, we have the right to “put,” or sell, up to $15,000,000 worth of shares of our common stock to L2 Capital. Unless terminated earlier, L2 Capital’s purchase commitment will automatically terminate on the earlier of the date on which L2 Capital has purchased shares for an aggregate purchase price of $15,000,000 or December 11, 2020. We have no obligation to sell any shares under the Equity Purchase Agreement. This arrangement is also sometimes referred to herein as the “Equity Line.”

As provided in the Equity Purchase Agreement, we may require L2 Capital to purchase shares of common stock from time to time by delivering a put notice to L2 Capital specifying the total number of shares to be purchased (such number of shares multiplied by the purchase price described below, the “Investment Amount”); provided there must be a minimum of 10 trading days between delivery of each put notice. We may determine the Investment Amount, provided that such amount may not be more than 300% of the average daily trading volume in dollar amount for our common stock during the five trading days preceding the date on which we deliver the applicable put notice. Additionally, the amount may not be lower than $10,000 or higher than $1,000,000. L2 Capital will have no obligation to purchase shares under the Equity Line to the extent that such purchase would cause L2 Capital to own more than 4.99% of our common stock.

For each share of the our common stock purchased under the Equity Line, L2 Capital will pay a purchase price equal to 85% of the “Market Price,” which is defined as the lowest closing traded price on the OTCQB Marketplace, as reported by Bloomberg Finance L.P., during the five consecutive trading days including and immediately prior to the settlement date of the sale, which in most circumstances will be the trading day immediately following the Put Date or the date that a put notice is delivered to L2 Capital. On the settlement date, L2 Capital will purchase the applicable number of shares subject to customary closing conditions, including a requirement that a registration statement remain effective registering the resale by L2 Capital of the shares to be issued under the Equity Line as contemplated by the Registration Rights Agreement described below. The Equity Purchase Agreement is not transferable and any benefits attached thereto may not be assigned.

The Equity Purchase Agreement contains covenants, representations, and warranties of us and L2 Capital that are typical for transactions of this type. In addition, we and L2 Capital have granted each other customary indemnification rights in connection with the Equity Purchase Agreement. The Equity Purchase Agreement may be terminated by us at any time.

In connection with the Equity Purchase Agreement, we also entered into Registration Rights Agreement with L2 Capital requiring us to prepare and file a registration statement registering the resale by L2 Capital of shares to be issued under the Equity Line, to use commercially reasonable efforts to cause a registration statement to become effective, and to keep such registration statement effective until: (i) three months after the last closing of a sale of shares under the Equity Line; (ii) the date when L2 Capital may sell all the shares under Rule 144 without volume limitations; or (iii) the date L2 Capital no longer owns any of the shares. In accordance with the Registration Rights Agreement, we filed the registration statement, of which this prospectus is a part, registering the resale by L2 Capital of up to 52,631,578 shares that may be issued and sold to L2 Capital under the Equity Line. The registration statement was declared effective on January 29, 2018.

The 52,631,578 shares being offered pursuant to this prospectus by L2 Capital will represent approximately 47% of our shares of common stock issued and outstanding held by nonaffiliates as of the date of this prospectus assuming the offering is fully subscribed.

The foregoing description of the terms of the Equity Purchase Agreement and Registration Rights Agreement does not purport to be complete and is subject to and qualified in its entirety by reference to the agreements and instruments themselves, copies of which are filed as Exhibits 10.1 and 10.2 to our Current Report on Form 8-K dated December 21, 2017, and incorporated into this prospectus by reference. The benefits and representations and warranties set forth in these agreements and instruments are not intended to, and do not, constitute continuing representations and warranties by us or any other party to persons not a party thereto.

We intend periodically to sell our common stock to L2 Capital under the Equity Purchase Agreement and L2 Capital may, in turn, sell such shares to investors in the market at the market price or at negotiated prices. This may cause our stock price to decline, which will require us to issue increasing numbers of common shares to L2 Capital to raise the intended amount of funds as our stock price declines.

Likelihood of Accessing the Full Amount of the Equity Line

Notwithstanding that the Equity Line is $15,000,000, we anticipate that the actual likelihood that we will be able access the full amount of the Equity Line is low due to several factors ... https://ih.advfn.com/stock-market/USOTC/ocean-thermal-energy-corp-CPWR/stock-news/79031737/post-effective-amendment-to-registration-statement

11/19/18 ... Our Operational Strategy and Economic Models

We have developed economic models of costs and potential revenue structures that we will seek to implement as we develop OTEC and SWAC projects.

OTEC Projects

The estimated construction costs for a 20-MW plant are approximately $445 million. The hard costs of approximately $301 million consist of the power system and platform construction and piping, which make up 68% of the total. The remaining 32% consists of other construction costs and the deployment of the cold water pipe. The soft costs of approximately $58 million consist of design, permits and licensing, environmental impact assessment, bathymetry, contractor fees, and insurance.

Once operational, the capacity factor, which is the projected percent of time that a power system will be fully operational, considering maintenance, inspections, and estimated unforeseen events, is expected to be 95% annually. This factor is used in our financial calculations, which means the plant will not be generating revenue for 5% of the year. Most fossil-fuel plants have capacity factors around 90%, as a result of the major maintenance for high-temperature boilers, fossil-fuel feed in systems, safety inspections, cleaning, etc. The normal maintenance cycle for the pumps, turbine, and generators used in the OTEC plant is typically every five years. This includes the cleaning of the heat exchangers and installation of new seals.

We anticipate that project returns will be comprised of two components: First, as the project developer, we will seek a lump-sum payment as a development fee at the time of closing the project financing for each project. These payments will be allocated toward reimbursement of development costs and perhaps a financial return at the early stage of each project. The development fee will vary, but initially we will seek a fee of approximately 3% of the project cost, payable upon closing project financing. Second, we will retain a percentage of equity in the project, with a goal to retain a minimum of 51% of the equity in any OTEC project in order to participate in operating revenues.

We will seek to generate revenue from OTEC plants from contract pricing charged on an energy-only price per kWh or on the basis of a generating capacity payment priced per kW per month and an energy usage price per kWh. In addition to revenue from power generation, in many of the countries of the world where we intend to build OTEC and SWAC plants, water is in short supply. In some locations, water is considered the more important commodity. Depending on the part of the world in which the plant is built, supplying water for drinking, fish farming, and agriculture would significantly increase plant revenue.

We cannot assure that we can maintain the revenue points noted above, that any fees received will offset development costs incurred to date, or that any operating plant will generate revenue.

SWAC Projects

The estimated construction costs are approximately $150 million. The hard costs of approximately $91 million consist of piping and installation, which make up 60% of the total. The remaining 40% consists of the pump house, central utility plant (CUP), mechanical and engineering equipment, design, and other contingency costs. The soft costs of approximately $30 million consist of the CUP license, permits, environmental impact assessment, bathymetry, and insurance.

Under our economic model, it will seek to generate revenue at two stages of the project. First, as the project developer, we will seek a lump-sum payment of a development fee equal to approximately 3% of the project cost at the time of closing the project financing for each project. Such payments would provide the Company with income at the early stage of each project. If we are able to negotiate a development fee, we estimate that it will vary but typically will be in the $2,500,000-$3,500,000 range. The second component of project returns is based upon the percentage of equity we will retain in the project.

SWAC contract revenue will be based typically on three charges:

* Fixed Price–this is based upon the capital costs of the project paid over the term of the debt and with the intention of covering the costs of debt.

* Operation and Maintenance–this payment covers the cost of the labor and fixed overhead needed to run the SWAC system, as well as any traditional chiller plant operating to fulfill back-up or peak-load requirements.

* Chilled Water Payment–this is a variable charge based on the actual chilled water use and chilled water generated both by the SWAC and conventional system at the agreed upon conversion factors of kW/ton and current electricity costs in U.S. dollars per kWh.

We will seek to structure project financing with the goal of retaining 100% of the equity in any SWAC project. We cannot assure that we will recover project development costs or realize a financial return over the life of the project. ... https://ih.advfn.com/stock-market/USOTC/ocean-thermal-energy-corp-CPWR/stock-news/78720117/post-effective-amendment-to-registration-statement

@CNBCnow BREAKING: Apple shares halted for pending news

BREAKING: Apple shares halted for pending news. https://t.co/jn8limUSe7

— CNBC Now (@CNBCnow) January 2, 2019

Affiliate DCO may cover them in the absence of the AC company acquisition. The team looks ready to go, but like you say, funds may be running low. They filed a Quarterly report in November so aren't due again until February.

CEO Feakins tweeted Fundraising for public companies just became a lot easier with the new Regulation A+ rules adopted by the SEC - https://go.shr.lc/2CL2DQP

... Recent changes in capital markets have made it more difficult for small public companies to raise capital. I believe that by opening up the simplified offering circular and SEC review procedures available through Regulation A, these companies will have a resource that allows them to access capital markets more efficiently. Furthermore, by being able to offer investors freely tradable securities, small public companies will have less pressure to enter into highly dilutive financing arrangements.

In addition to the obvious benefit to small and emerging company capital formation of allowing small reporting companies to utilize Regulation A, there is also an added potential benefit to the capital markets as a whole. The flow of freely tradable securities into the marketplace for existing public companies could have a positive uptick on the liquidity and overall growth and vitality of small-cap market trading. Institutional investors generally do not invest in thinly traded securities and accordingly, increased liquidity in the secondary marketplace could attract more institutional investments in small public companies. Likewise, increased activity could prompt additional analyst coverage for these companies. ...

CPWR doesn't do much dilution, which should entice Institutional Investors, and Analysts to increase funding.

PureCircle PRs at TDAmeritrade is London company who also claim many patents. Is this thing a dead horse?

Their PR said Air Conditioning company. Kwajalein and other military projects may be in the works pending the defense budget. Hopefully news is forthcoming soon.

More on Kwajalein:

https://link.springer.com/article/10.1007/s40095-018-0278-4

No worries about tropical storms near the equator.

Picked up 5000 additional shares on the dip. Rather it rose, but helped prop it up and happy to increase my position. Worldwide the opportunity is immense and it’s good to see developments, even from other than CPWR as theses small floating plants will validate things like algae blooms, fouling of water intakes, etc. 100 small OTEC plants planned in next two years. Here are links to a video and article.

Up 25% and OTEC News released today.

UK company Global OTEC Resources has released images of its first design concepts for the company’s 1MW floating ocean thermal energy conversion (OTEC) device.

https://mobile.marineenergy.biz/2018/12/18/global-otec-resources-unveils-floating-otec-concept/

Different company from OTE(CPWR), but will help establish proof of concept.

Me too, picked up another cheap chunk of VPLM!

Well in the green on this one.

Dip was a great buying op!

OP, over and out.

Patent plays work differently.

Me got error using brave browser, but saw Mr. Meatloaf moderates site suggestions, of which I have one. My suggestion is to support an/or signify Impact Investors. Call it virtue signaling, if you must, but some invest for reasons that go beyond ROI in monetary dollars.

Did Abraham Lincoln walk 6 miles to return a penny?

yes he was a clerk and a lady forgot her change, so he walked 6 miles to her house to give it to her, the change was only 1 cent ... https://www.answers.com/Q/Did_Abraham_Lincoln_walk_6_miles_to_return_a_penny

I keep hearing reference to President Lincoln today, and my memory was that he walked 1 mile to return 6 cents. 6 cents in those days was a good sum, but 6 miles is seriously a long way to walk. The original basis for this stock saw the PPS over 10$, meaning 100/1 returns may become a delayed reality.

Great technology, and curious why PPS has dropped?

PPS up 18.81% at 0.060 and volume is way up too!

Resilience RELi is a thing, as Bluerise retweeted

Nov 29

Such energy! Great group of #SIDS energy professionals from across the #Caribbean at the “Resliience of Islands through RE” conf by @IRENA and @COE4SIDS, ...

OTEC offers up ultimate resilience with its potential to neutralize hurricanes, typhoons or whatever your preferred word is to describe tropical cyclones. Besides electricity, extra energy can propel the hydrogen economy, it too can greatly aid many communities with food and fresh water production.

WIRED 2005: The Mad Genius from the Bottom of the Sea

SIMPLE SOLUTIONS FOR PLANET EARTH AND HUMANITY: CAN OTEC NEUTRALIZE HURRICANES?

The retweet from the 29th appeared in my email, about an hour ago. Interesting sequence of events indeed.

Roger that, just saw it a one of your stocks.

Weird that an EQ drove the point home, as my home escaped unscathed, except a chandelier fell, which is what happened to Jon Pina aka Mad Genius under the sea.

Resilient Design

USGBC is further refining the program to synthesize LEED Resilient Design credits with RELi Hazard Mitigation and Adaptation credits.

Last fall, USGBC and GBCI announced the adoption of the RELi rating system (RELi). RELi takes a holistic approach to resilient design. With more than 50 requirements and credits spread throughout eight categories, including panoramic design, hazard mitigation, materials used in construction and community vitality, RELi encompasses a wide variety of strategies and techniques. RELi also overlaps with other rating systems, particularly LEED.

First developed by the Institute for Market Transformation to Sustainability (MTS) and its Capital Markets Partnership coalition in 2012, RELi includes a robust integrative process, acute hazard preparation and adaptation, along with chronic risk mitigation at the building and neighborhood scale.

USGBC is now leading the further refinement of RELi to synthesize the LEED Resilient Design pilot credits with RELi’s Hazard Mitigation and Adaptation credits.

The increasing frequency of dramatic weather events has brought an even greater urgency to create buildings and communities that are better adapted to a changing climate and better able to bounce back from disturbances and interruptions.

Unlike other resilience rating systems now available, RELi combines hazard-specific design criteria, such as tornado preparedness, with general resilience strategies, like energy efficiency. Instead of functioning merely as a benchmarking system, RELi’s system of requirements and credits, in addition to the third-party certification provided by GBCI, improves the resilience and accountability of a project at every level, including facility planning, design, operations and maintenance. ... http://www.gbci.org/reli-rating-system-improves-project-resiliency-every-level

Think that’s it, and today I can attest to its validity, having just ridden out a 7.0 EQ North of Anchorage. OTEC ECO Village on St. Croix employs top designers and urban planners, such that it may also be an excellent place to live, as a way to reap the rewards of what I hope remains a worthy investment.

According to the OTE project page, the Philippines too, are one of several projects planning to get underway!

PTABs: The USPTO has revised its standard operating procedure (SOP) governing the assignment of judges to panels in Patent Trial and Appeal Board (PTAB) cases. The SOP, available here, provides guidance to Board administrative personnel for assigning panels of at least three administrative patent judges to ex parte appeals, reexamination appeals, reissue appeals, interferences, and AIA proceedings. Among other things, the SOP details processes and considerations for initial panel assignments and provides reasons for why a panel may be changed or expanded. Key provisions of the SOP are summarized below.

Guidelines for Panel Assignments. The SOP includes provisions for avoiding conflicts of interest in panel assignments. ... https://www.lexology.com/library/detail.aspx?g=e86923dd-bc52-46c2-b706-dd4842b19bdc

Equitize Patent Prosecutors, meaning offer up shares to the legal team. The case would of been tossed out years ago, if they were not without merit, don’t you think?

Equitize patent prosecutors?

Picked me up a starter today!

Good to know 57 days to remain a slacker. :)

DRUSFully Dreadful Dilution Doth Drop Do Do into my little bucket of stock wisdom.

Really it’s tuff to say if/when/how Drus will fly, but I’ll retain what I have and apply lessons learned elsewhere. Education and Experience both teach valuable lessons, but Experience hurts, making us less likely to forget; so said my survival instructor as we prepped for a crash landing.Thanks to all that have posted here, where I have leaned much.

OP, over and out.

Algae, OTEC or Nuclear are the three bigs, when it comes to replacing fossil fuels. Nuclear doesn’t directly produce food or fresh water, but OCLN can definitely help there too. This looks great! Heres hoping the strong patent portfolio trumps shorts and dilution.

Dilution and Dr. Gundry’s interview of affiliate Catalina Sea Ranch, are my main concern and motivation with Origin Clear. I’m more than half-way to my intended million share acquisition and may consider going more, but the dilution here looks DRUSfully dreadful.

THE MAD GENIUS FROM THE BOTTOM OF THE SEA

June 1, 2005

... CHC's success depends on two projects that expand on Craven's ideas: a vineyard in Kona to grow table grapes for local restaurants, and a more complex, much larger-scale version of his oasis, on Saipan. A stable US territory, the island is a booming destination for Japanese tourists. Tokyo is just two and a half hours away by air. And the Marianas offer generous tax deals to Japanese who retire there. But Saipan has a limited supply of freshwater and must import, at great expense, all of its food and oil. On the northern end of the island, CHC plans to sink a 24-inch-diameter pipe and build a hundred-acre development featuring 100 townhouses, a golf course, soccer fields, and even an athletic complex where Japanese sports teams can train. ... Wired